MARKET INTELLIGENCE

a

Source: 1/1/2021 – 7/31/2021 provided by FMLS

2022 Q4 ATLANTA, GEORGIA

ENGEL & VÖLKERS ATLANTA

Contents Market Trends 13 Interest Rates 14 Inventory 17 Home Prices 19 Transaction Volumes 23 Growth & Migration 26 Peer Markets 27 Market Snapshot 29 Single-Family Homes 36 Single-Family Homes - Inside the Perimeter 38 Single-Family Homes - Outside the Perimeter 43 Townhomes 48 Townhomes - Inside the Perimeter 51 Townhomes - Outside the Perimeter 56 Condominiums 61 Condominiums - Inside the Perimeter 64 Condominiums - Outside the Perimeter 69 Submarket Profiles 75

ENGEL & VÖLKERS

ENGEL & VÖLKERS

A Word From Us

The past three years in the real estate industry have brought us a series of ups and downs. We finally believe we have reached a sense of normalcy again and are back to a more balanced market across Georgia.

The first half of 2022 saw an extension of the hot market of 2021, with a cooling off that settled in for the second half of the year. This was fueled by rising interest rates, inflation, the lack of affordability and market uncertainty. Without question, 2020 and 2021 were outlier years in real estate where we saw less travel, very low interest rates, and an increased focus on home life. Because these years were such outliers, real estate trends in 2019 are also referenced throughout this report as a a comparison to a more typical year.

The recent decline in sales began in June of 2022 when rates moved over 5.25%. These rising interest rates increased the cost of home ownership for buyers, pricing many would-be buyers out of the market and forcing others to consider homes at a lower price point than they may have been exploring earlier in the year.

Market inventory is rising but still low with 2.1 months of inventory in Metro Atlanta overall at year end. Demand is down, but so is supply, which is helping to limit significant price declines. While prices are down slightly compared to the summer peak, this reflects an accelerated version of normal seasonal price fluctuations. Notably, the average sales price in Metro Atlanta in the second half of 2022 was still up 9.9% year over year. New listings have been down every month since June, which is, again, an accelerated version of a normal seasonal trend. Inventory reached its lowest level in a decade in December of 2022.

Although national forecasts call for home prices to stabilize or decline in some markets next year, Atlanta is rated the #1 top real estate market for 2023 by the National Association of REALTORS, with home prices expected to increase at least 5% in 2023.

Consumers demand is shifting and home quality matters again. Houses that are well designed, located in desirable areas, and priced well continue to sell. Those with less desirable characteristics are staying on the market longer and in some cases selling below asking price.

There is still latent demand as many people have been in “wait mode,” hoping that interest rates fall and more inventory comes to market. Market uncertainty is still compelling buyers to wait to buy until things look more favorable, which they perceive to be right around the corner. Buyers and sellers are just beginning to realize we are not going to snap back to the same market as a year ago, are adjusting to new interest rates, and are finally making buying and selling decisions again.

Christa Huffstickler Founder & CEO Engel & Volkers Atlanta

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 5 ENGEL & VÖLKERS www.evatlanta.com

A Guide to the Report

Interested in getting to know the Atlanta real estate market? See how this guide is structured and learn about key indicators to help you make sense of what is happening in the market.

2022 End-of-Year Market Intelligence Report

A Guide to the Report

This report is designed as a guide to the Metro Atlanta real estate market, helping savvy homebuyers and sellers make informed, strategic decisions in the year to come. Whether you’re an Atlanta native or new to the area, this guide will give you the intel you need to understand what is happening in the market overall and hone in on the best options for you and your family.

Where to Start

This report has three sections, beginning with an overview of the market before getting into specifics about home types and submarkets within Metro Atlanta:

1 Market Trends

Take a deep dive into broader market and economic trends driving the real estate market, including interest rates, inventory levels, price trends, and the Atlanta economy, framed through our seller and buyer clients’ top FAQs this season.

Beginning on page 14.

Data Sources

2 Market Snapshot

Are you selling or looking for a single-family home, townhome, or condominium? Check out what’s happening market-wide for each home type and how prices and products in different neighborhoods compare.

Beginning on page 30.

3 Submarket Profiles

Metro Atlanta has many neighborhoods, homes, and lifestyles to offer. See what’s happening across each submarket and what new development is on its way to the neighborhoods on your mind.

Beginning on page 75.

What is FMLS?

Data referenced throughout this report comes primarily from the First Multiple Listing Service (FMLS), TrendGraphix, and MarketNsight. Sources are noted with tables and charts, or as endnotes compiled at the end of this report. This report is focused on the second half of 2022 and most data refers to Q3 and Q4 overall (July 1, 2022 to December 31, 2022), or select months where specified.

First Multiple Listing Service is a regional real estate database for the Atlanta area, with data on most of the active, pending, and closed sales in the area. Additional off-market transactions may have occurred, but are not included in FMLS data.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 9 ENGEL & VÖLKERS www.evatlanta.com

Defining Metro Atlanta

This report discusses the market from the metro level down to specific neighborhoods. Here’s how we define the geographies referenced throughout the report:

Metro Atlanta

This 11-county area includes Cherokee, Clayton, Cobb, DeKalb, Douglas, Fayette, Forsyth, Fulton, Gwinnett, Henry, and Rockdale Counties. Some of our data sources use the term “Greater Atlanta Area” to refer to this same geography.

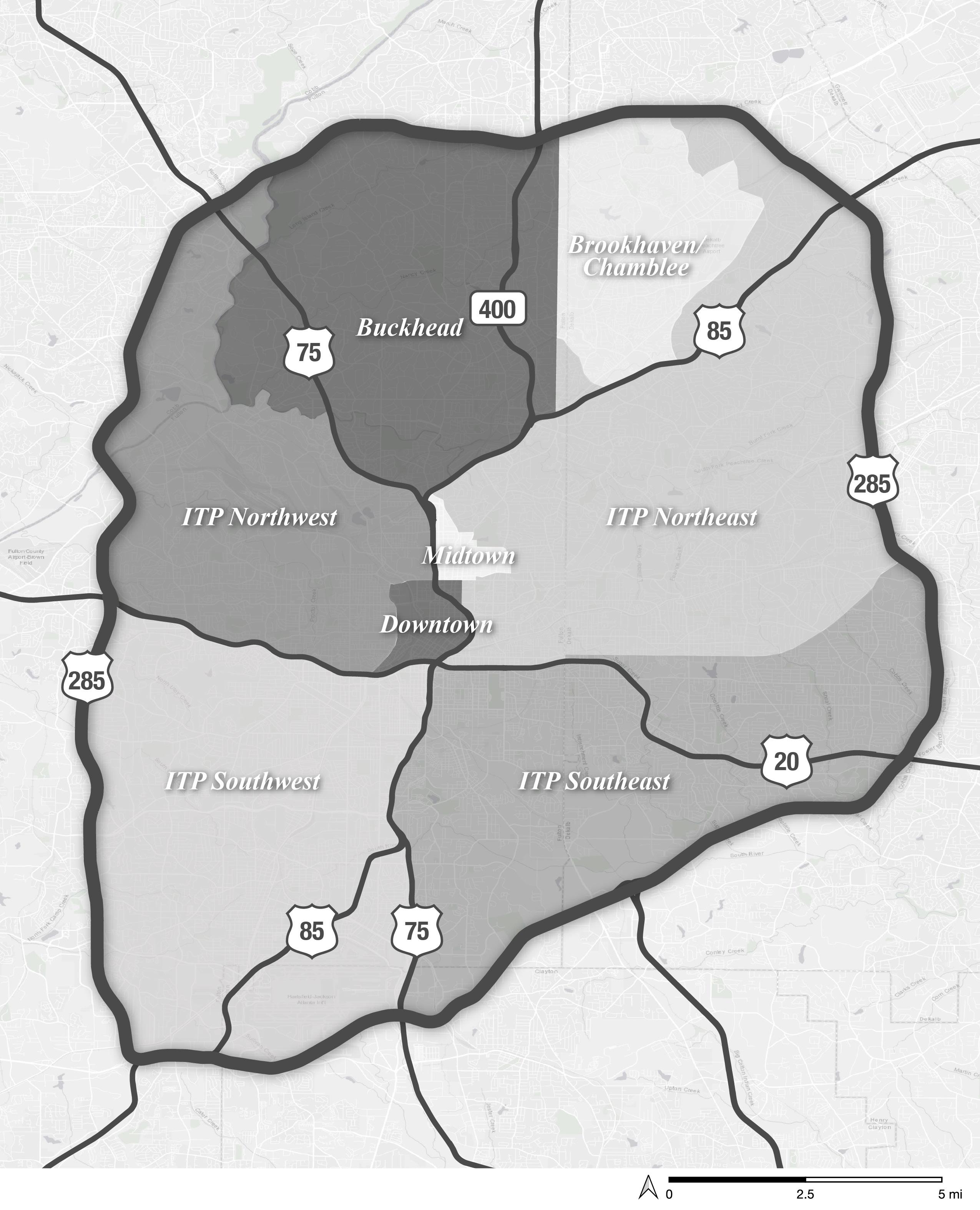

Inside the Perimeter (ITP)

Interstate 285 (I-285) forms a ring around Atlanta known as The Perimeter. Neighborhoods inside the perimeter are called “ITP.” This includes most of the City of Atlanta and nearby places like Brookhaven, part of Sandy Springs, Chamblee, Vinings, East Point, College Park, Hapeville, and Decatur.

Outside the Perimeter (OTP)

Neighborhoods and cities outside the I-285 perimeter are “OTP.” This area covers most of suburban Atlanta.

NW, SW, NE, & SE Quadrants

The four quadrants of Atlanta are a way to organize the city by subareas. They are delineated by major streets in the center of the city. Peachtree Street runs north-south and generally aligns with where Interstates 75 and 85 (I75/85) run outside of the center of the city. This line distinguishes “west” from “east” neighborhoods. Interstate 20 (I-20) runs east-west through the metro just south of Downtown. It delineates the “north” part of the metro from the “south” part.

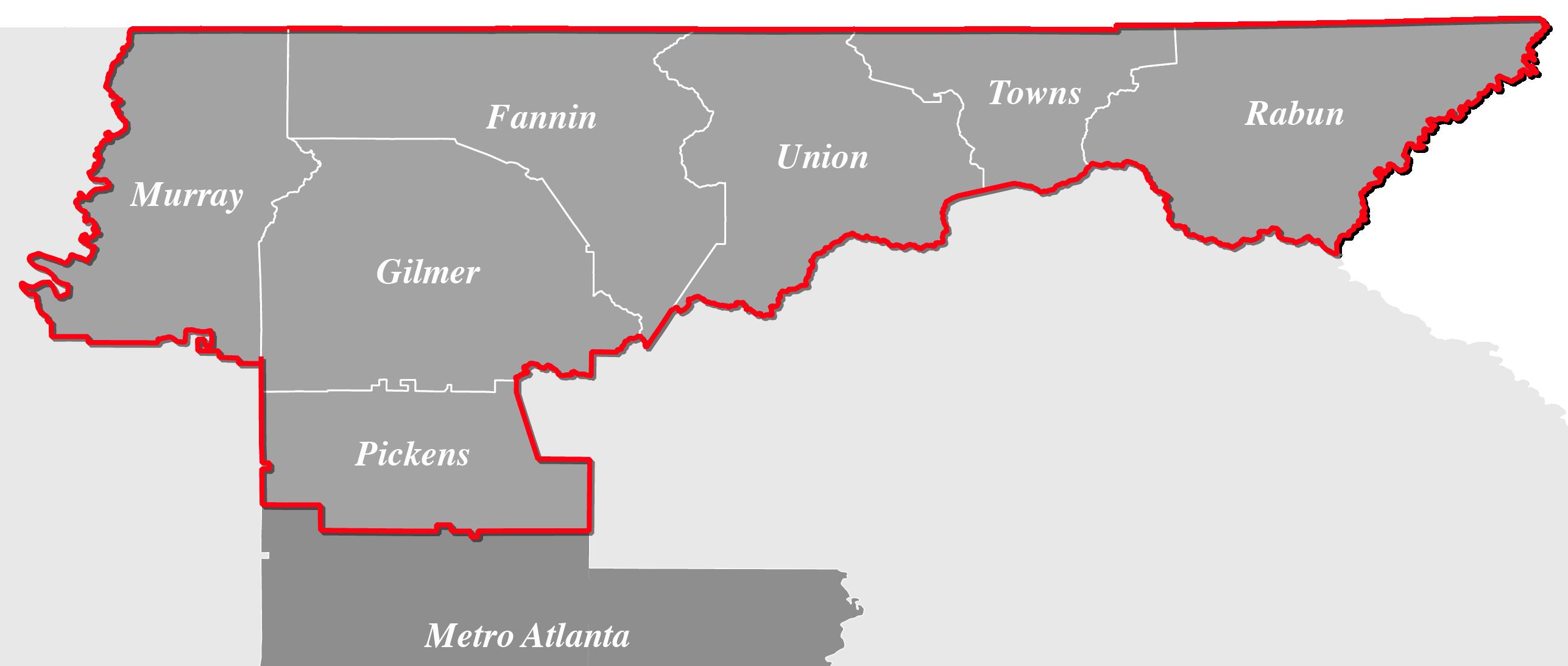

North Georgia

The North Georgia market has close ties to Metro Atlanta as a nearby escape to nature, surrounded by the hills and mountains. It includes places like Blue Ridge, Ellijay, and Helen in Clay, Fannin, Gilmer, Murray, Pickens, Rabun, Towns, and Union Counties.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 10 ENGEL & VÖLKERS www.evatlanta.com

Key Indicators

The following key indicators are used throughout this report to describe market trends:

Active Listings

Properties that are currently listed for sale on FMLS. Additional properties may be for sale at any given time— such as for-sale by owner homes or off-market listings— but are not included in the count of “active listings” in this report if they are not in the FMLS database.

New Listings

New listings are those that have been added to FMLS in a given month. They do not include active listings that were entered in previous months.

Closed Sales

Closed sales represent homes that have sold and transactions have been finalized. This indicator tends to lag market trends slightly because properties typically close one to two months after an offer has been accepted and buyers have locked their interest rates.

Pending Sales

Pending sales are properties that have accepted an offer from a buyer and is in the due diligence period. The sales transaction has not happened yet. This is a leading indicator because it give us insight

Sale Price

The sale price is the final amount paid for a home. It is measured as either an average or a median, with the average price tending to be skewed higher by the highest priced homes. It does not reflect seller concessions, such as closing costs that may have been paid.

Sale Price to List Price Ratio

The sale price to list price ratio (SP/LP) indicates if a home sold at (100%), above (>100%), or below (<100%) the listed asking price. The sale price to original list price ratio (SP/OLP) compares the sale price to the original asking price, as the current asking price may have reflected price changes.

Days on Market

Days on market (DOM) measures how long it takes from the time a home is listed until the owner signs a contract for the sale of a property. This tends to vary based on the desirability of a given property, market conditions, and season.

Months of Inventory

Months of inventory indicates how long it would likely take to sell currently listed homes, if no new inventory were added. It is measured as a ratio of active listings to homes sold. 5 to 6 months of inventory is considered a balanced market. Less than 6 months supply tends to favor sellers, and more tends to favor buyers.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 11 ENGEL & VÖLKERS www.evatlanta.com

Market Trends

Learn about the factors that shaped the Metro Atlanta housing market in the second half of 2022 and what it means for real estate in 2023.

2022 End-of-Year Market Intelligence Report

Market Trends Overview

Over the past year, macro trends like rising interest rates and tight housing inventories have shaped the way buyers and sellers have approached the real estate market. Check out what has been happening with these key trends with our clients’ top FAQs and see how they’re shaping the market ahead in 2023.

Client FAQs

Interest Rates

• What’s next for interest rates?

(page 16)

• Market Trend: Rate Buydowns

(page 17)

Inventory

• Is supply beginning to exceed demand? (page 18)

• Why are there more listings but it still doesn’t feel like there are any good homes to choose from?

(page 19)

• Will there be an influx of foreclosed homes like in the Great Recession? (page 19)

• Are there more new construction homes on the way? (page 19)

Home Prices

• What is normal for price appreciation?

(page 20)

• Has normal seasonality returned?(page 21)

• How do sale prices align with appraised values? (page 22)

• Will home prices drop dramatically this year? (page 23)

Transaction Volumes

• Which price points had the most sales?

(page 25)

• Can Atlantans afford current homes?

(page 26)

Growth & Migration

• How is Atlanta’s economy doing? (page 27)

• Where are people who move to Atlanta coming from? (page 27)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 14 ENGEL & VÖLKERS www.evatlanta.com

?

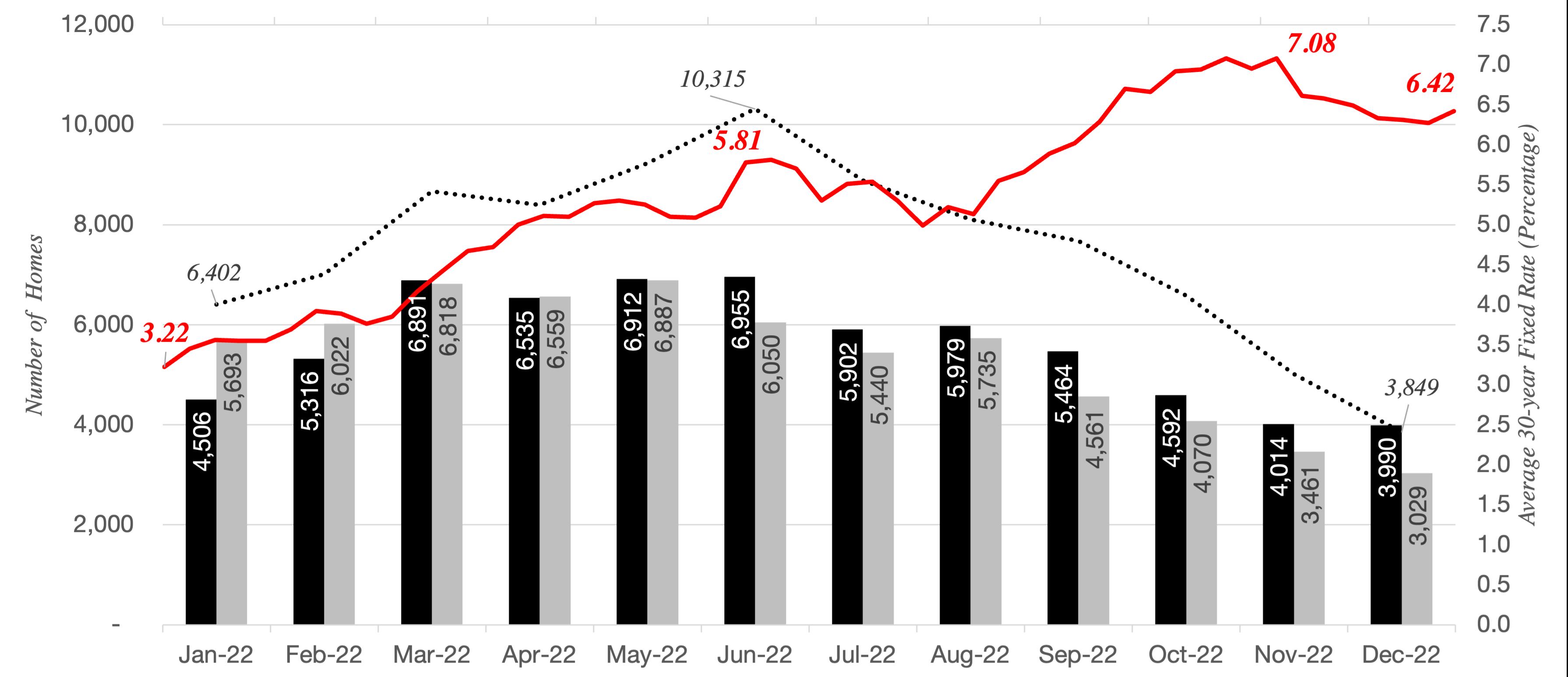

Interest Rates

Mortgage interest rates have been a driving force in the housing market in 2022. The year started with near record low rates for a 30-year fixed rate mortgage, which averaged 3.22% nationally at the start of the year.1 At the same time, inflation was on the rise globally and home prices were rising rapidly as low borrowing costs enticed buyers and contributed to stiff competition for a limited inventory of homes. To reign in inflation, the Federal Reserve began raising its benchmark interest rates in the spring, a factor leading to an increase in mortgage rates. The Fed’s goal in raising interest rates was to cool demand and slow price

increases, an effect that has been felt in the housing market more than in most sectors of the economy.

Mortgage interest rates more than doubled over the course of 2022, the largest single-year increase since the early 1980s. By June, the average rate for a 30-year fixed-rate mortgage exceeded 5.25%, which proved to be a sensitivity threshold above which buyer demand dampened, leading to declines in home sales beginning in late summer. The average interest rate for a 30-year fixed-rate mortgage reached a 20-year high of 7.08% in November, which most economists

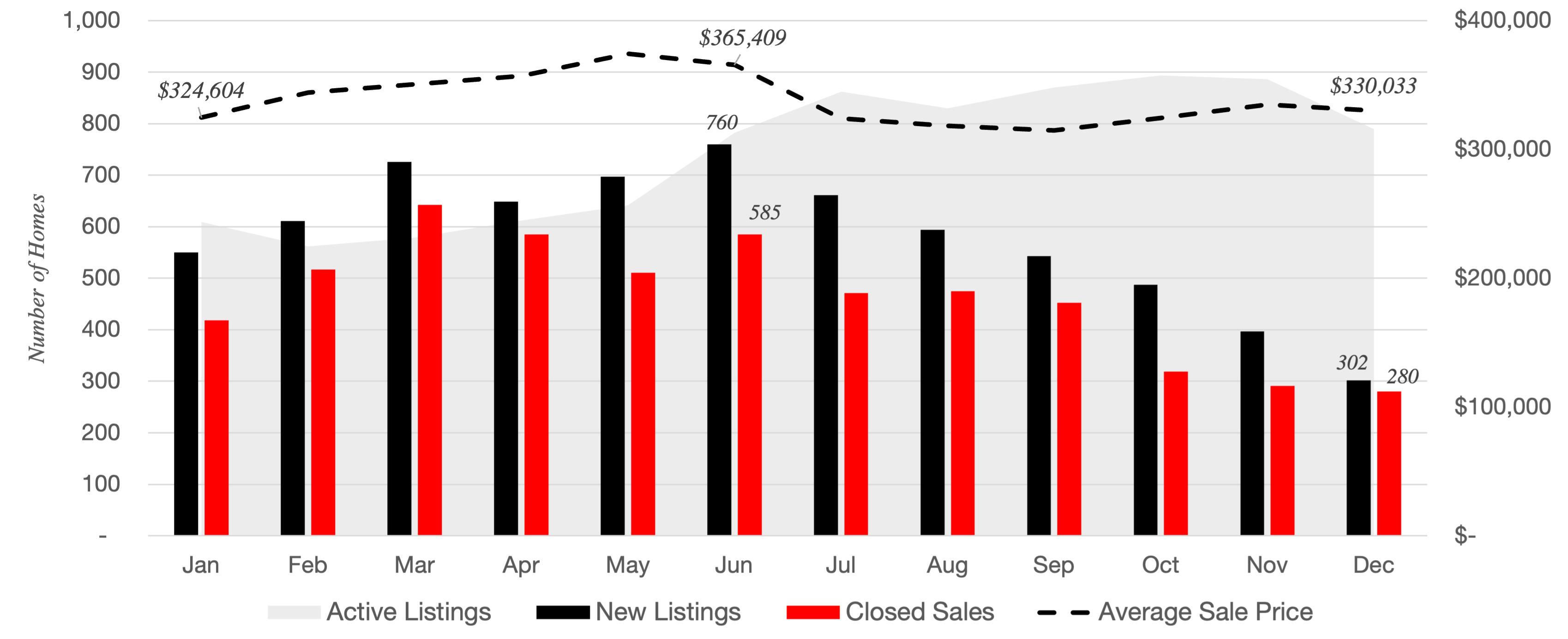

Metro Atlanta 2022 Monthly Pending and Closed Sales vs. Interest Rates

Most economists believe mortgage interest rates for this cycle peaked in November 2022 and will stabilize in 2023, ranging from about 6.5% to 5.5%.

believe to be the peak rate for this cycle. It declined to 6.42% by the end of the year,2 returning to a level typical in the early 2000s, but still above levels that are likely needed to bring significantly more buyers into the market.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 15 ENGEL & VÖLKERS www.evatlanta.com

Source: FMLS InfoSparks (Greater Atlanta Area), Freddie Mac Primary Mortgage Market Survey (National)

Interest rates over 5.25%

Brief drop in interest rates Interest rates peaked in November

(Seasonal#SalesandNewListingsDecline Trend+InterestRates)

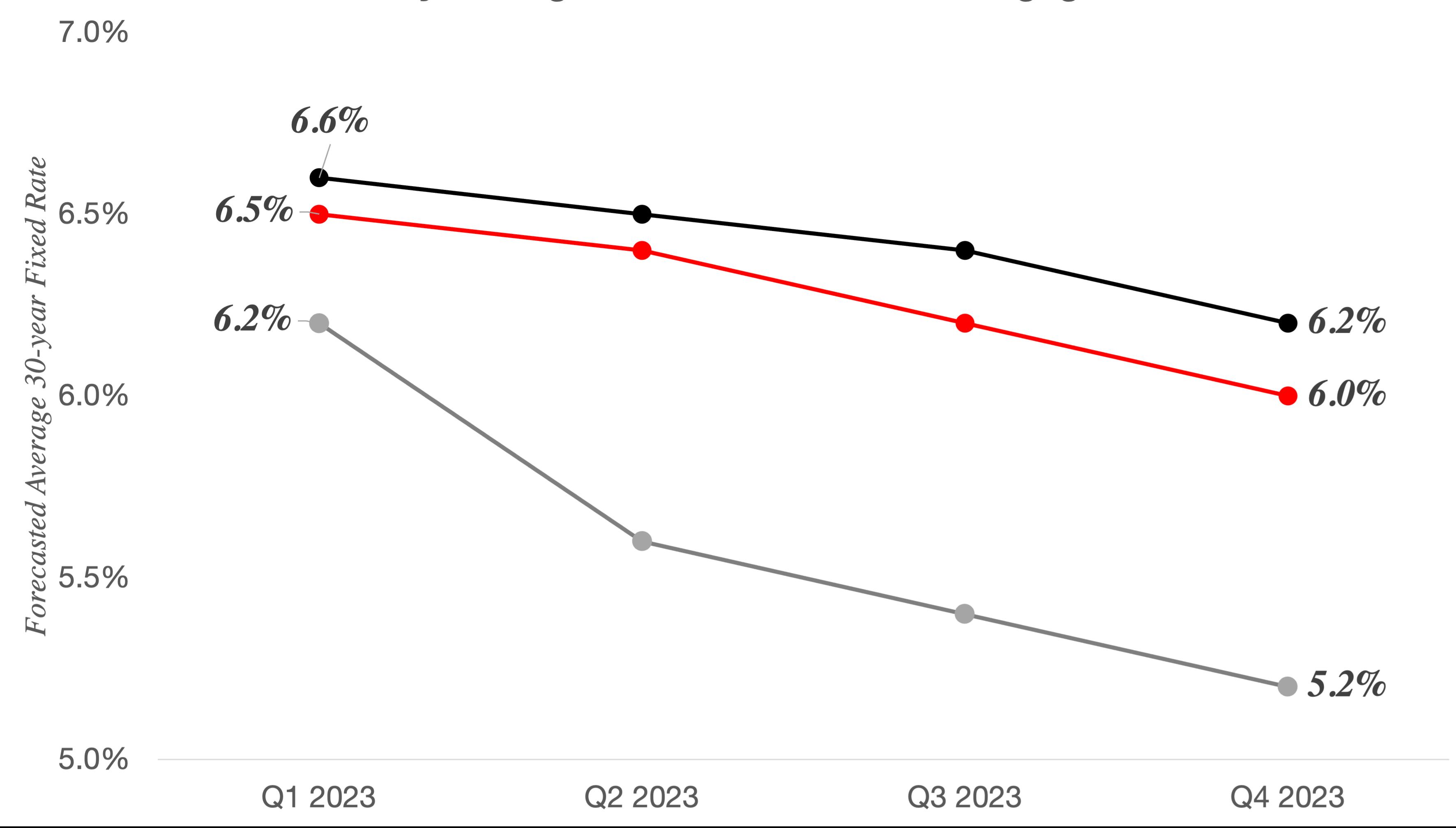

What’s Next for Interest Rates?

The Federal Reserve has stated its intent to continue restricting monetary policy until it believes inflation is under control. This means that although mortgage interest rates are expected to decline slightly

in 2023, they are not likely to return to the 3% range in the next couple of years. The Federal Reserve has not yet made a clear statement about their policy for rates in 2023. Most economists are forecasting that inflation and mortgage interest rates already peaked for this cycle in late 2022.

Forecasts for mortgage interest rates next year vary,3, 4, 5 typically stabilizing near current levels (6% to 6.5%) in the first half of 2023, with a slight decline in the latter half of the year. Buyers interested in making a purchase over the next year will need to adjust to mortgage rates staying within the 5.5% to 6.5% range.

2023 Quarterly Average 30-Year Fixed Rate Mortgage Forecasts

30-year Fixed Rate Mortgage Interest Rate Forecasts

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 16 ENGEL & VÖLKERS www.evatlanta.com Historic Forecasted 2022 2023 2024 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Freddie Mac (Oct. 2022) 3.8% 5.3% 5.6% 6.8% 6.6% 6.5% 6.4% 6.2% - - -Fannie Mae (Dec. 2022) 3.8% 5.2% 5.6% 6.7% 6.5% 6.4% 6.2% 6.0% 6.5% 6.4% 6.2% 6.0% Mortgage Bankers Association (Jan. 2023) 3.9% 5.3% 5.7% 6.6% 6.2% 5.6% 5.4% 5.2% 5.0% 4.7% 4.4% 4.4%

“It is likely that restoring price stability will require holding policy at a restrictive level for some time. We will stay the course until the job is done.”

-Federal Reserve Chairman

Jerome Powell

Freddie Mac Forecast Fannie Mae Forecast Mortgage Bankers Association Forecast

Market Trend: Rate Buydowns

In the new construction market, some homebuilders have begun to work around the prevailing interest rates by offering incentives like rate buydowns to attract buyers who are sitting on the sidelines waiting for rates to drop. In certain cases, individual homeowners have offered similar rate buydown incentives as well.

Rate buydowns allow a seller to pay an upfront fee to reduce the buyer’s interest rate by a set amount for a set period of time, before returning to a fixed rate. The most common types are 2/1 buydowns—which reduce the interest rate by 2% in the

first year and by 1% in the second year—and 3/1 buydowns, which reduce the interest rate by 3% in the first year, 2% in the second year, and 1% in the third year. With these temporary buydowns, buyers typically hope that interest rates will decline in the next few years, at which point they can refinance their loans at a lower rate, generally for a fee. For a permanent reduction, the seller may pay discount points to reduce the interest rate over the life of the loan, at a higher cost.

For more information about these trending tools, check with your mortgage provider for available programs and terms.

Types of Rate Buydowns

2/1 Buydown

The mortgage interest rate is reduced by 2% in the first year and by 1% in the second year

3/1 Buydown

The mortgage interest rate is reduced by 3% in the first year, 2% in the second year, and 1% in the third year

Discount Points

Fee paid to permanently reduce a fixed interest rate

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 17 ENGEL & VÖLKERS www.evatlanta.com

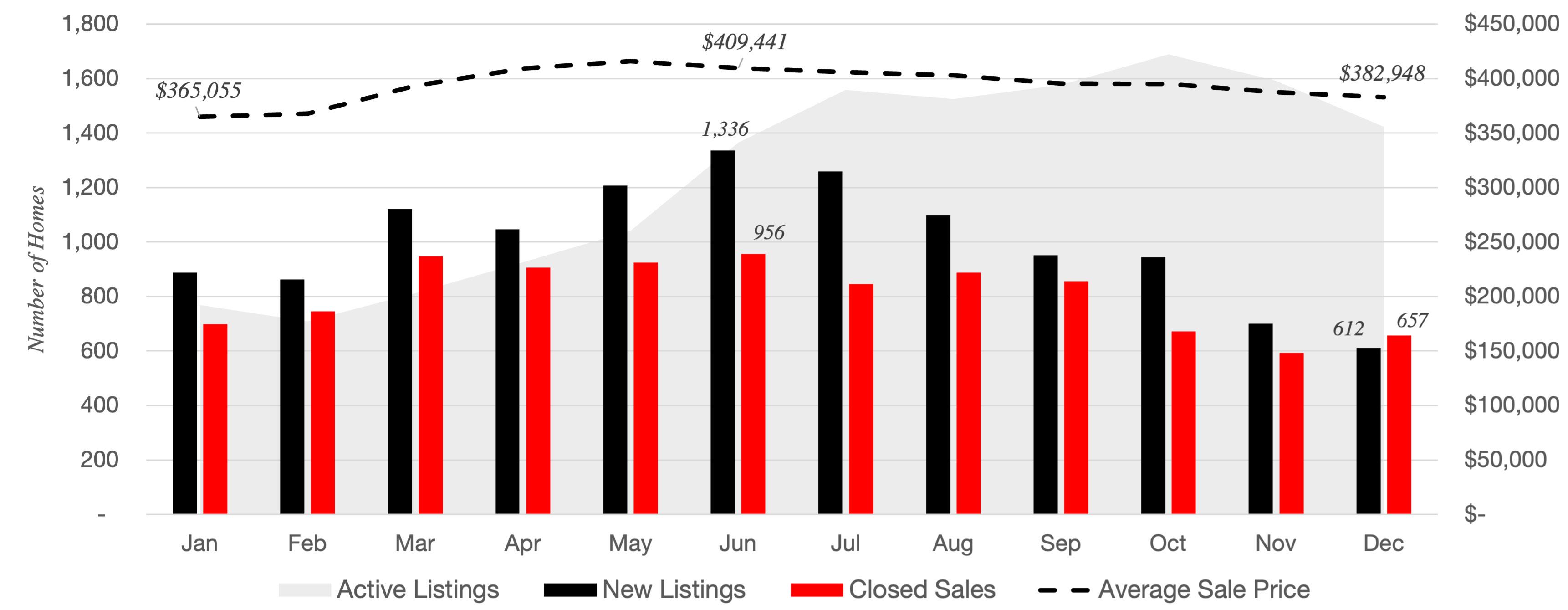

Inventory

Is supply beginning to exceed demand?

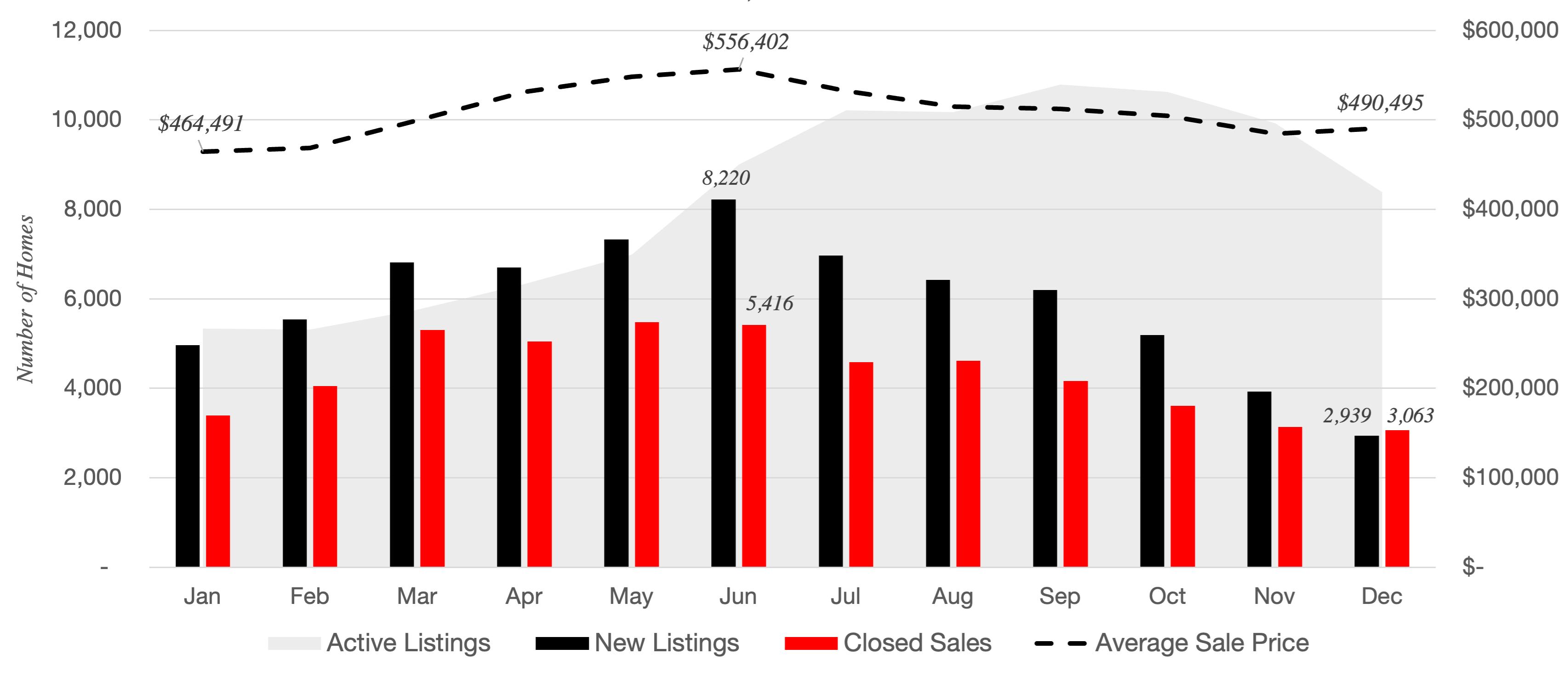

Demand continues to outpace supply in Atlanta. In January 2022, home inventory was at a record low of 1 month of supply. Although it has risen significantly since then, there was still only a 2.1-month supply of homes for sale by year end.6

At the start of 2022, the very limited number of available homes in Atlanta could not match pandemic era buyer demand in a time with low mortgage rates and an increased focus on life at home. This inventory shortage contributed to competitive conditions that heavily favored sellers and led to bidding wars, rapidly rising home prices, and ultrafast timelines, with most homes selling in less than a week.

Home inventory is measured as “months of inventory,” a term that describes how long it would likely take for all the actively listed homes to sell, if no new homes were listed, based on the recent pace of home sales. A 6-month supply is considered a balanced market, with fewer months of inventory favoring sellers and more favoring buyers.

summer, buyer demand declined, but so did new listings, with current homeowners hesitant to give up their low interest rates. Atlanta reached a peak of 2.3 months of supply in October and dropped back to just 2 months in December, following a typical seasonal slowdown in the winter.

Supply ticked up heading into the spring market as more homes were listed, a normal seasonal trend. As mortgage interest rates rose over the Metro Atlanta 2022 Monthly Home Inventory

Despite lower demand, the Atlanta market remains at less than half of the supply that would be considered a balanced market (6 months of inventory), with select submarkets approaching a balanced market. Assuming interest rates peaked in November and demand bottomed out at that time, months of supply in spring and summer 2023 are not expected to go above 3 months.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 18 ENGEL & VÖLKERS www.evatlanta.com

Source: FMLS InfoSparks (Greater Atlanta Area)

Much of the increase in home inventory in late 2022 can be attributed to homes taking longer to sell than they did early in the year, rather than a major increase in the number of homes buyers can choose from. After lightning fast sales in early 2022, the time it takes to sell the average home also increased in the second half of the year, a return to normal seasonality after an unusually hot market in 2020 and 2021. By December, the median days on market rose to 23 days in the Greater Atlanta Area, still a week faster than in December 2019, a typical year when the median days on market was 30 days.7

Buyers feel like they have more to choose from when new listings that fit their criteria are added. New listings in Metro Atlanta declined every month from June to December, slightly outpacing the normal seasonal trend of fewer new listings in the second half of the year. The number of new listings in December 2022 was the lowest of any month in a decade. Just 3,849 new listings were added, about a third of the new listings added in June 2022 and 29% lower than the average of Decembers in 2017 to 2021.8 Fewer homeowners are choosing to sell, discouraged by higher interest rates and limited inventory. As of November 2022, 99% of U.S. homeowners with mortgages had rates below 6%,9 which disincentivizes them from selling their current home to buy another at a higher rate, leading to

stagnation in home inventory and limited choices for buyers.

In January 2023, the number of new listings went up for the first time since June 2022, with 45% more new listings than December. Although new listings were still below average for January, this uptick is a sign that sellers who have been waiting are beginning to get off the fence.

Will there be an influx of foreclosed homes like in the Great Recession?

Current homeowners often have a significant amount of equity in their homes due to recent price appreciation. Combined with a strong labor market and less risky loan underwriting in recent years, this means they are not likely to be forced into a sale for financial reasons, as was the case for some homeowners during the Great Recession. Several indicators show current homeowners in a strong financial position with a low likelihood of a wave of foreclosures:

• The foreclosure rate today is at a historical low of 0.6% nationally.10

• Significant price appreciation in past two years has given homeowners stronger equity positions in their investments. In the third quarter of 2022, the average U.S. loan-tovalue (LTV) ratio was 43.6%, significantly lower than the average 71.3% LTV heading into the great recession in Q1 2010.11

• Nationally, distressed property sales made up just 2% of all sales in November 2022, well below the 30% mark seen during the Great Recession.12

• Mortgage delinquency is also low at 3.6%, compared to 10.1% during the Great Recession.13

• The national unemployment rate is at 3.4%, the lowest in 53 years14

Are there more new construction homes on the way?

New homes are under construction, but not enough to meet demand. As of January 2023, the Atlanta market had an annual housing deficit of 62,000 units,15 with just 13,000 new homes expected to be constructed over the next 12 months.16 As builders begin to pull back on new starts due to economic conditions, we may see even fewer of these homes actually completed this year, furthering the deficit. This low level of inventory is one of the factors that has shielded Atlanta from the kind of significant price reductions that some buyers may have expected to coincide with a significant increase in mortgage interest rates.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 19 ENGEL & VÖLKERS www.evatlanta.com

Why are there more listings but it still doesn’t feel like there are many good homes to choose from?

Home Prices

Homes in the Metro Atlanta appreciated in value at record pace in 2020, 2021, and the first half of 2022 before returning to a more typical pace of appreciation in the second half of 2022.

In the last three years—between December 2019 and December 2022—the average sale price in Metro Atlanta rose by 40% from $335,948 to $461,667, an increase of $125,719. That rapid growth was more than double the pace of the previous 3-year period from December 2016 to 2019, when prices rose 17%, or an average of $50,804.17 As a result, many homeowners have significant amounts of equity in their homes from price appreciation, but the cost of buying a new home is higher than ever.

The average sale price varies by home type. In Q3 and Q4 2022 the average sale prices in Metro Atlanta for each type were:

• Single-Family Home: $499,874

• Townhome: $391,205

• Condominium: $323,137

What is normal for price appreciation?

For the past 47 years, the Atlanta market has averaged 4.6% annual home price appreciation.18

After a few of years with historically high levels of price appreciation, we are returning to these more moderate levels of price growth. As of December 2022, the average Metro

“Metro Atlanta home price appreciation in December 2022 was 4.2% year-over-year, near the 47-year average of 4.6% annual price growth.”

Atlanta home price of $461,598 was up 4.2% year-over-year, near that historic norm. For Q3 and Q4 overall, average prices were up 9.9% yearover-year, with an average sale price of $477,682.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 20 ENGEL & VÖLKERS www.evatlanta.com

Metro Atlanta Average Sale Price Growth by Home Type (Rolling 12 months, December 2016 to 2022)

40% increase in average sale price for all homes in 3 years

Source: FMLS InfoSparks, Greater Atlanta Area, Average Sale Price, Rolling 12 months, December 2016 to 2022

Has normal seasonality returned?

Homes sales—and sale prices—tend to ebb and flow with the seasons of life, with the greatest demand in the spring and summer and a natural slowdown in the winter months. In Atlanta, home prices typically rise throughout the spring market, peak in June, decline in the second half of the year, see a slight end-of-year bump in December. With frenzied demand in 2020 and 2021, that

normal historical pattern did not occur, and prices continue to rise through much of the fall and winter.

2022 largely brought a return to seasonality, with prices peaking in June and declining heading into the fall. However, the declines in home prices between June and December 2022 were greater than a typical historical decline for this period. From 2009 to 2019, the average sale price for all homes in the Greater Atlanta Area typically declined between June and December, ranging from -1.9% to -14.5%, averaging

-4.8%. In 2022, the average sale price declined -9.7% from June to December, outpacing normal seasonality for most years, but still less than the maximum decline during this period, which occurred in 2011. The most significant price declines in 2022 occurred between June and August—when normal seasonality coincided with mortgage interest rates first exceeding 5.25%—and leveled off toward the end of the year.19

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 21 ENGEL & VÖLKERS www.evatlanta.com

Metro Atlanta Home Price Seasonality (Monthly Average Sale Price 2012 to 2022)

Atlanta home prices typically rise in the Spring, peak in June, and decline in the Fall Normal seasonality did not occur in 2020 and 2021

Source: FMLS InfoSparks, Greater Atlanta Area, Average Sale Price, All Home Types

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Average Sale Price

How do sale prices align with appraised values?

Earlier this year, home prices were rising rapidly due to intense buyer competition and homes were often appraising below the contract price, requiring buyers to pay the appraisal gap in cash. In April 2022,

a record high 20% of homes had an appraisal gap. As mortgage interest rates rose and demand cooled over the summer, offers began to more closely align with appraised home values. By October 22, just 6.3% of homes were appraised below the contract sales price,20 reflecting a market more in line with actual home values.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 22 ENGEL & VÖLKERS www.evatlanta.com

Will home prices drop dramatically this year?

The question on everyone’s minds as of late has been how far—if at all—homes prices can be expected to drop in 2023. Home price growth in 2023 will vary significantly by region. In Atlanta, there are several fundamental conditions that have prevented dramatic price declines even as interest rates doubled over the course of a year, including:

• Low inventory levels;

• Low construction activity;

• A strong economy; and

• A growing population.

These fundamentals are so strong that the National Association of Realtors (NAR) named Atlanta the #1 housing market in the U.S. with the most potential for growth in 2023. It was also ranked #9 on Zillow’s list of the hottest housing markets for 2023.

Home price forecasts vary widely and are adjusted often, and actual prices will depend on factors like inflation, prevailing mortgage interest rates, unemployment levels, submarket, and individual home quality. Despite forecasts of home prices plateauing or declining slightly on a national level in 2023,21, 22, 23 , 24, 25, 26 the Atlanta market is forecasted to see home prices grow by at least 5% this year.27

Mortgage interest rates are also expected to level off in the first half of 2023 and gradually decline in the second half of the year, with many economists anticipating rates stabilizing below 6% later in the year. This rate reduction and stabilization would lower the cost of home ownership and increase the sense of certainty in the market, increasing demand by widening the pool of eligible buyers and enabling buyers of all kinds to get more for their money.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 23 ENGEL & VÖLKERS www.evatlanta.com

“The Atlanta market is rated the #1 real estate market to watch in the U.S. in 2023, with home prices forecasted to grow by at least 5% this year.”

according to the National Association of Realtors forecast

Zillow Regional Home Values Forecast (November 2022 to November 2023)

Map and Data Source: Lance Lambert, Zillow, 20 January 2023

Transaction Volumes

Fewer people have been buying and selling homes since higher interest rates set in during summer 2022. Pending sales are a leading indicator of sales activity— typically about a month ahead of closings— and had a strong relationship to ongoing interest rate changes in 2022.

Pending sales began to decline in April, as interest rates first began to rise and more significantly in June, when they rose above 5.25%. Pending sales continued to decrease throughout most of the second half of the year, in keeping with seasonal trends accelerated by rising interest rates.

August was the only month that did not post month-over-month declines in pending sales. When interest rates dipped to 4.99% in early August, there was an uptick in transactions, with 5.4% more pending sales than July. Pending sales reached what is believed to be the low point for this cycle in November, when interest rates peaked at 7.08%.

In December, interest rates came down for six consecutive weeks and pending sales bounced slightly.28

In early January 2023, they continued to pick up. Although they were still down year-over-year (YOY), they were down 16% YOY (and just -5% compared to 2019) the third week of January, an improvement over the low point in November when pending sales were down 45% YOY,29 showing signs of buyers returning as rates stabilize. That same week, mortgage applications nationally were up 7% over the previous week, another sign of buyers getting ready to enter the spring market.30

As of the week of February 2nd, the average 30-year fixed rate mortgage rate was at 6.09%.31 With interest rates expected to land in the 5.5% to 6.5% range for most of 2023, the total number of homes sold in 2023 is expected to be lower than in 2022. Nationally, the NAR is forecasting a 7% decline in home sales for 2023 compared to 2022.32

67,095 homes were sold in all of 2022 (13% fewer than the annual average for 2017-2021)

17,345 homes were sold in Q3 (19% fewer than the average for the same period 2017-2021)

12,596 homes were sold in Q4 (32% fewer than the average for the same period 2017-2021)

7% fewer homes expected to be sold in 2023 than in 2022 according to the National Asssociation of Realtors

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 24 ENGEL & VÖLKERS www.evatlanta.com

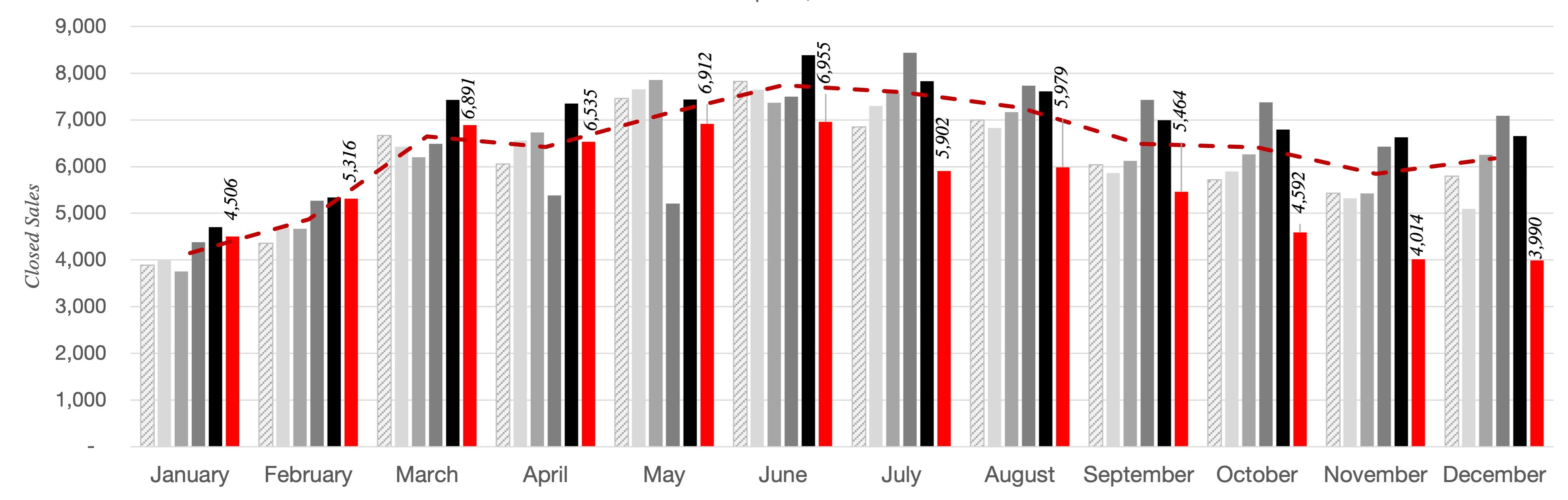

Metro Atlanta Closed Sales by Month (2017 to 2022)

Interest rates rose above 5.25% in June and sales began to slow Q1 Q2 Q3 Q4

Source: FMLS InfoSparks, Greater Atlanta Area, Closed Sales, All Home Types

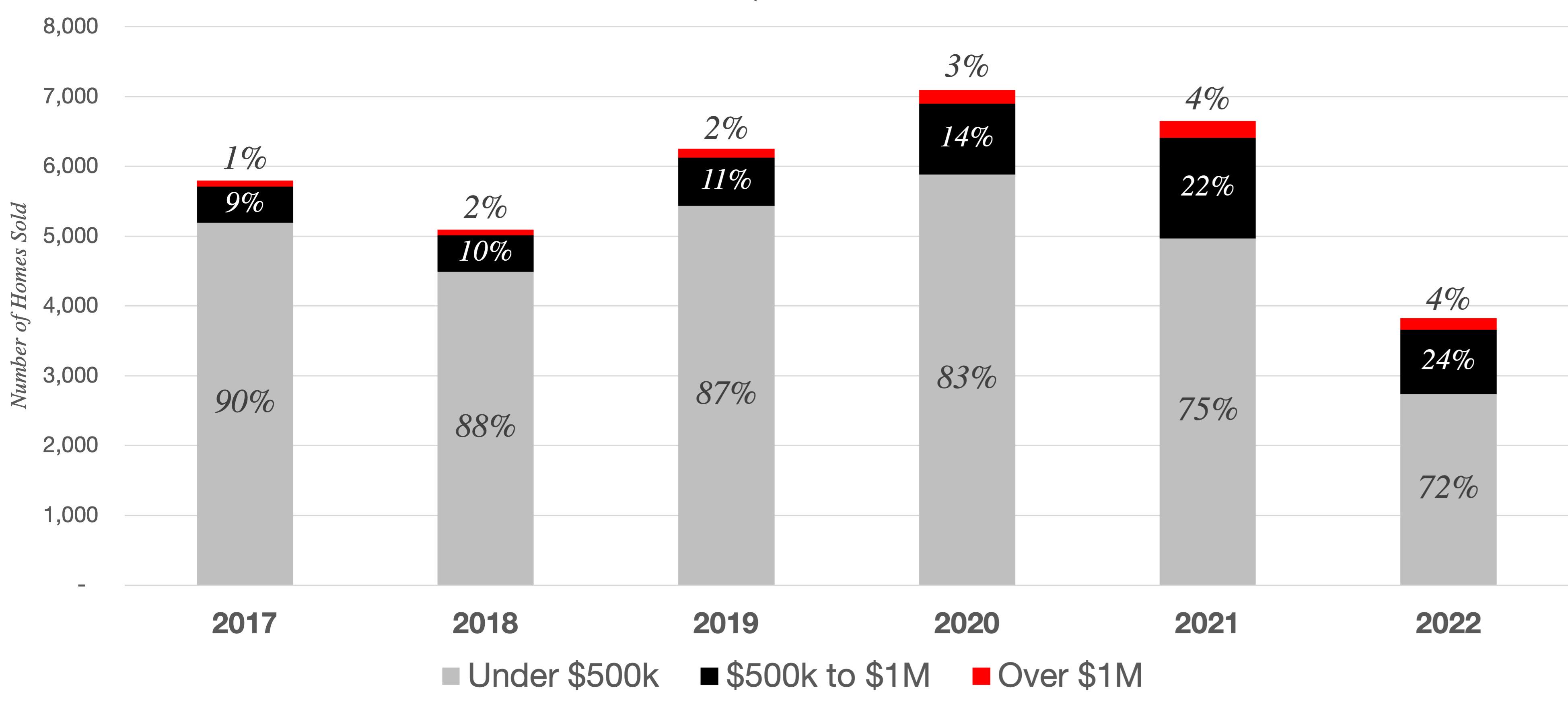

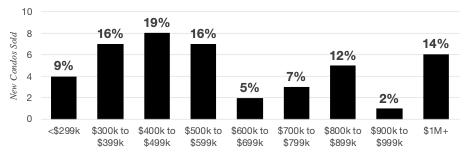

Which price points had the most sales?

Entry level homes continue to make up the bulk of sales, but have taken the biggest hit in transaction volume declines since higher interest rates set in during summer 2022:

Entry Level (< $500,000)

Most homes sold in the Greater Atlanta Area have been under $500,000, both historically and in 2022. However, the share of homes priced under $500,000 has declined in the last several years as prices overall have risen and more homes now fall into higher price brackets. In December 2022, only 72% of homes in the Greater Atlanta Area sold for less than $500,000 compared to 90% of homes in 2017.33

In December, there were 2,739 homes sold for less than $500,000 in the Greater Atlanta area, 47% fewer sales than the average for the previous five Decembers, and down 45% compared to December 2021. This was a greater decline in transaction volume than higher price points, reflecting fewer homes for sale in this price range and potentially that entry level buyers may be more price sensitive and experiencing greater constraints from the higher mortgage rate environment.

Move-Up ($500,000 to $1 million)

Move-up buyers—those purchasing homes priced between $500,000 and $1 million, often upgrading from an entry level home—have also been affected by increased interest rates. Closed sales in this price range were down 36% yearover-year in December 2022, a less dramatic decline in sales than entry level homes. This may be in part due to rising prices, which pushed more homes into this price range.

Luxury (Over $1 million)

Luxury buyers were the least responsive to the higher interest rate environment of the past year. There was a 30% decline in closed sales for homes over $1 million in December 2022 compared to December 2021, the smallest decline of any price bracket. Even with this slower pace of sales, about twice as many homes sold for over $1 million in December 2022 as in December 2017, largely due to the overall escalation of home prices in Atlanta over the past five years.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 25 ENGEL & VÖLKERS www.evatlanta.com

Source: FMLS InfoSparks, Greater Atlanta Area, Closed Sales, All Home Types, December 2017 to 2022

Metro Atlanta Closed Sales by Price Point - December 2017 to 2022

Declining share of home sales under $500,000

Rising share of home sales over $500,000 (2.8x since 2017)

Can Atlantans afford current home prices?

Although Atlanta remains more affordable than many major cities, continued home price growth and rising mortgage rates have led to an increased cost of homeownership that has outpaced income growth in the past few years, making it more difficult for some Atlantans to afford to buy a home and leading some buyers to consider a wider range of potential homes that fit their budgets.

Decreased affordability leads to a smaller pool of potential buyers and therefore fewer total transactions. The average sale price for a home in Metro Atlanta increased by 44% between December 2019

and December 2022.34 The typical monthly payment for the average home increased even more* due to higher interest rates. Meanwhile, the monthly take home pay for the median household increased by 11% from 2019 to 2021 (2022 data is not yet available).35

In December 2017, the monthly payment for the average priced home in the Atlanta area cost about 39% of the net monthly income for a family earning the median household income. By December 2022, a typical monthly mortgage payment for the average priced home reached 59% of the median household’s monthly budget. This increased cost has pushed some would-be buyers to wait to buy a home.

There would need to be a change in dynamics for a greater share of

Atlantans to comfortably afford home ownership— and for the number of home sales to rise signficantly— such as a reduction in mortgage interest rates, more affordable home prices, or an increase in income.

For those who are able to purchase a home, some may choose to lower their target price range to account for a higher interest rate. To meet their financial goals, some buyers today are expanding their searches to different types of homes—such as a smaller home, a townhome, or a condominium— or considering a wider range of neighborhoods, allowing them to find homes that meet their lifestyle goals while fitting their budget. Others are taking advantage of mortgage rate buydown programs to lower their initial payments, with plans to refinance at a lower rate.

* Assumptions: Annual median household income from U.S. Census American Community Survey estimates as net monthly household income (based on the ADP Gross to Net Calculator for a Georgia resident); FMLS InfoSparks average sale price (all home types) for the Greater Atlanta Area in December of each year; Average 30-year fixed rate mortgage interest rate from Freddie Mac Primary Mortgage Market Survey for the given month.

Metro Atlanta Key Housing Affordability Statistics

a) U.S. Census American Community Survey, Atlanta-Sandy Springs-Roswell MSA, 2017 to 2021

b) 2022 Median Household Income had not yet been published at t he time of this report; 2021 data shown for reference

c) Net monthly income estimated using the ADP Gross to Net Calculator for a Georgia resident

d) FMLS InfoSparks average sale price (all home types) for the Greater Atlanta Area in December of each year

e) Freddie Mac Primary Mortgage Market Survey, average of weekly average rates for December of each year

f) Assumes a 20 percent down payment and no PMI; includes estimated property taxes and insurance, but not HOA dues

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 26 ENGEL & VÖLKERS www.evatlanta.com

2022 2021 2020 2019 2018 2017 Median Household Income (Gross Annual) a $77,589 b $77,589 $71,193 $71,742 $69,464 $65,381 Estimated Median Household Income (Net Monthly) c $4,798 b $4,798 $4,447 $4,313 $4,170 $3,773 Average Sale Price – December d $469,890 $442,993 $375,045 $335,948 $313,268 $297,631 Average 30-year Fixed Rate – December e 6.36% 3.10% 2.68% 3.72% 4.64% 3.95% Estimated Monthly Payment (Assuming 20% Down) f $2,849 $1,995 $1,632 $1,622 $1,651 $1,476 Monthly Mortgage Payment for Average Sale Price Home with Average Interest Rate as Percentage of Net Monthly Income for Median Household 59% b 42% 37% 38% 40% 39%

Growth & Migration

Atlanta continues to hold its position as the economic powerhouse of the Southeast, attracting new companies and residents with its culture, climate, and relative affordability. Metro Atlanta grew by 64,940 people in the past year, bringing the 11-county area to 5.1 million residents (+1.3%). About 10% of metro area residents live in the City of Atlanta (507,015 people).36

Each of the 11 counties grew this year, with the greatest number of new residents in Gwinnett (13,460), Fulton (11,200), Cobb (6,900), and Cherokee (6,890) Counties. As a percent of its total population, the northern edge counties saw the greatest rates of population growth, with Forsyth County growing by 2.6% and Cherokee County growing by 2.5% year-over-year.37

Atlanta’s strong job market and growing population are key reasons it is expected to be the #1 top U.S. real estate market to watch in 2023.38 In addition to growth in staple industries like life sciences and manufacturing, Georgia’s growing film industry and a number of major West Coast companies—including Apple, Microsoft, and Visa—opening

large offices in Atlanta have also brought new residents to the metro. The number of jobs in Metro Atlanta was up 6.7% year-over-year, making it #2 of all large metros for job growth in 2022. The unemployment rate was just 2.7% in November 2022, below the national average of 3.4%.39 Atlanta workers are more likely to be working from home, with 24% telecommuting, three times as many teleworkers as there were prepandemic.40

This job growth has resulted in population growth to fuel demand for housing. Metro Atlanta was the #5 moving destination in the country in 2021.41 People are choosing to move to our region from all over the country and the world. In the U.S., the metro areas around New York City, Miami/Fort Lauderdale, Chicago, Washington, D.C., Los Angeles, and Orlando were among the top feeder markets for people relocating to Atlanta in recent years. Fellow Georgians are also migrating to Atlanta from places like Athens, Gainesville, and Savannah.42

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 27 ENGEL & VÖLKERS www.evatlanta.com

Metro Atlanta Population (2022)

City of Atlanta Population (2022) 507,015 New Metro Atlanta Residents (2022) 64,940 Metro Atlanta Job Growth (2022) +6.7% 2nd Highest Among Large U.S. Metros Metro Atlanta Median Household Income (2021) $77,589 Metro Atlanta Median Home Price $400,000 (Q3 & Q4 2022) Metro Atlanta Average Home Price $477,701 (Q3 & Q4 2022) Zillow Observed Rent Index $2,002 (+53.3% in 5 years)

5,091,644

2022 End-of-Year Market Intelligence Report Market Snapshot Take an inside look at market trends by home type and price point across Metro Atlanta, including single-family homes, townhomes, and condominiums.

Market Snapshot

Across Metro Atlanta, home sales slowed in the second half of 2022, reflecting normal seasonal trends at an accelerated pace due to higher interest rates and uncertain economic conditions. The number of homes sold was down about 30% marketwide compared to Q3 and Q4 2021, and down 22.7% compared to the same period in 2019, a more normal year.

Although new listings declined consistently, the total number of listings went up as homes stayed on the market longer than they did in the hot early 2022 market. went up as homes stayed on the market longer than they did in the hot early 2022 market. Homes averaged

25 days on market in Q3 and Q4 2022. More affordable homes were typically scooped up faster than the more expensive inventory, and townhomes and condominiums sold faster than single-family homes. Inventory remained low at just 2.1 months of supply. This limited

Metro Atlanta Market Summary - All Home Types (Q3 & Q4 2022)

inventory helped to stabilize home prices despite a decline in demand. The average sale price was up 9.9 % year-over-year, and up 44.8% from the same period in 2019, with an average increase of $147,969 since 2019 (including $18,593 last year).

Source: FMLS InfoSparks, Greater Atlanta Area/City of Atlanta/ITP, All home types, All price points, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 30 ENGEL & VÖLKERS www.evatlanta.com

Metro Atlanta

Atlanta ITP closed Sales 29,963 q -29.5% 5,036 q -35.4% 5,773 q -34.9% Pending Sales 26,299 q -32.8% 4,460 q -37.2% 5,052 q -37.3% active Listings 12,429 p +43.7% 2,508 p +4.3% 2,854 p +4.6% New Listings 40,193 q -12.6% 7,708 q -16.3% 8,801 q -15.3% Median Sale Price $400,000 p +9.6% $410,000 p +8.8% $438,250 p +9.6% average Sale Price $477,701 p +9.9% $546,332 p +8.0% $570,771 p +8.6% average Price Per Square Foot $205 p +10.8% $274 p +8.3% $282 p +8.9% average Sale Price to Original List Price Ratio 97.5% q -3.3% 97.1% q -1.5% 97.2% q -1.2% Months of Inventory 2.1 p +75.0% 2.4 p +33.3% 2.3 p +27.8% average Days on Market 25 p +31.6% 26 q -3.7% 26 q -3.7%

City of

q Down YOY p Up YOY

$400,000 median sale price

$477,701 average sale price

2.1 months of inventory

Single-Family Homes: 2.2 months

Townhomes: 1.9 months

Condominiums: 1.7 months

(Q3

Average Price Per Square Foot

& Q4 2022, All Home Types)

(Q3 & Q4 2022, Metro Atlanta, All Home Types)

(Q3

& Q4 2022, Metro Atlanta, All Home Types)

+9.6% year-over-year +9.9% year-over-year

Supply Dynamics by Home Type

Metro Atlanta 2022 Supply Dynamics - All Home Types

Source: FMLS InfoSparks, Greater Atlanta Area, All Home Types, January to December 2022

Metro Atlanta 2022 Supply Dynamics - Single-Family Homes

Source: FMLS InfoSparks, Greater Atlanta Area, Single-Family Homes, January to December 2022

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 32 ENGEL & VÖLKERS www.evatlanta.com

Average Sale Price Average Sale Price

Metro Atlanta 2022 Supply Dynamics - Townhomes

Source: FMLS InfoSparks, Greater Atlanta Area, Townhomes, January to December 2022

Metro Atlanta 2022 Supply Dynamics - Condominiums

Source: FMLS InfoSparks, Greater Atlanta Area, Condominiums, January to December 2022

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 33 ENGEL & VÖLKERS www.evatlanta.com

Average Sale Price Average Sale Price

Metro Atlanta Market Summary by Price Point - All Home Types (Q3 & Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, All home types, Rolling 6-months as of December 2022 (year-over-year change com

pared to rolling 6-months as of December 2021)

Metro Atlanta Market Summary by Price Point - Single-Family Homes (Q3 & Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, Detached Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 34 ENGEL & VÖLKERS www.evatlanta.com

# Closed Sales % of All Closed Sales # Active Listings % of All Active Listings Months of Inventory Average Days on Market < $300k 6,938 q -47.2% 23% 2,025 q -3.9% 16% s 1.4 s 24 $300k - $499k 13,653 q -27.9% 46% 5,226 p +70.3% 42% s 2.0 s 24 $500k - $699k 5,416 q -13.9% 18% 2,355 p +74.4% 19% r 2.4 w 25 $799k - $999k 2,520 q -3.6% 8% 1,270 p +61.4% 10% r 2.7 w 25 $1M+ 1,401 q-8.8% 5% 1,173 p +38.8% 9% r 4.5 r 32 Total 29,928 q -29.6% 100% 12,412 p +43.5% 100% w 2.1 w 25

-

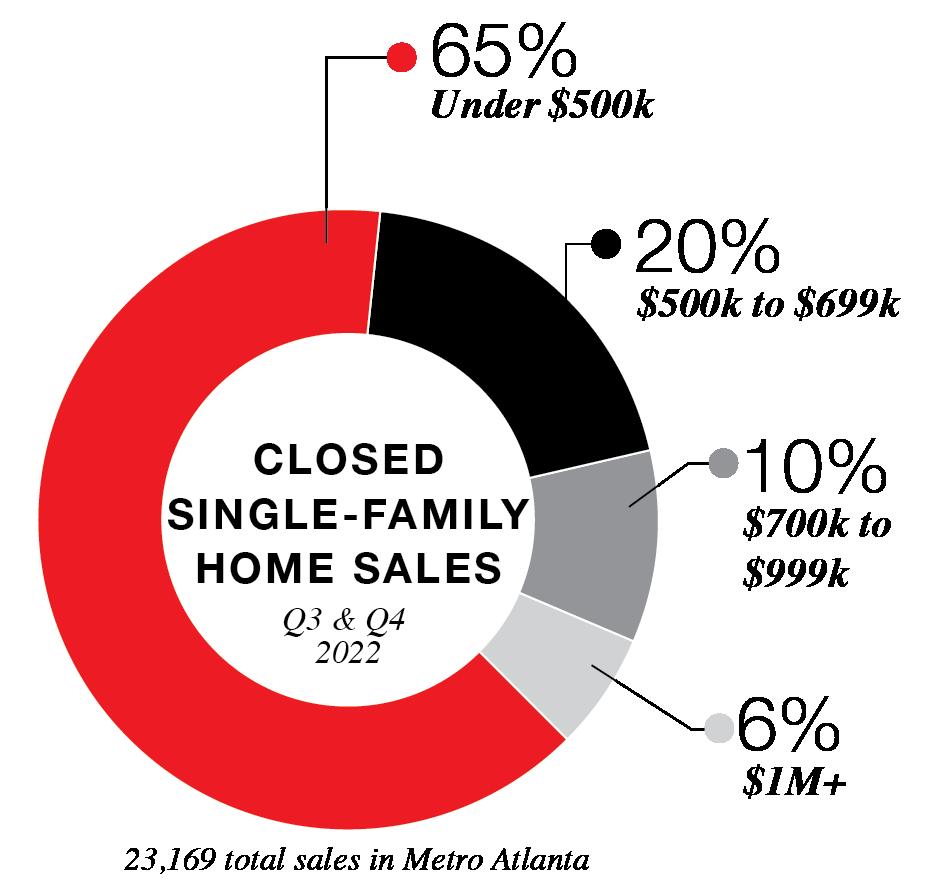

# Closed Sales % of All Closed SFH Sales # Active Listings % of All Active SFH Listings Months of Inventory Average Days on Market < $300k 4,079 q -50.5% 18% 1,329 p +6.0% 13% s 1.6 r 28 $300k - $499k 10,916 q -29.6% 47% 4,318 p +77.3% 43% s 2.0 w 25 $500k - $699k 4,593 q -14.4% 20% 1,939 p +84.0% 19% r 2.3 s 24 $799k - $999k 2,239 q -4.7% 10% 1,070 p +70.9% 11% r 2.6 s 24 $1M+ 1,312 q -8.6% 6% 1,051 p +43.0% 11% r 4.4 r 31 Total 23,169 q -29.6% 100% 9,998 p +52.9% 100% r 2.2 r 26

q Down YOY p Up YOY s Below Market Average r Above Market Average w Equal to Market Average

Metro Atlanta Market Summary by Price Point - Townhomes (Q3 & Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, Townhomes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

Metro Atlanta Market Summary by Price Point - Condominiums (Q3 & Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, Condominiums, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 35 ENGEL & VÖLKERS www.evatlanta.com # Closed Sales % of All Closed TH Sales # Active Listings % of All Active TH Listings Months of Inventory Average Days on Market < $300k 1,548 q -39.2% 34% 365 q -7.8% 23% s 1.2 s 18 $300k - $499k 1,981 q -21.8% 44% 638 p +73.4% 41% s 1.8 s 22 $500k - $699k 689 q -7.6% 15% 323 p +68.2% 21% r 2.7 w 25 $799k - $999k 230 p +14.4% 5% 141 p +50.0% 9% r 3.5 r 33 $1M+ 57 p +14.0% 1% 49 p +32.4% 3% r 5.0 r 44 Total 4,505 q -25.9% 100% 1,559 p +38.6% 100% s 1.9 s 22

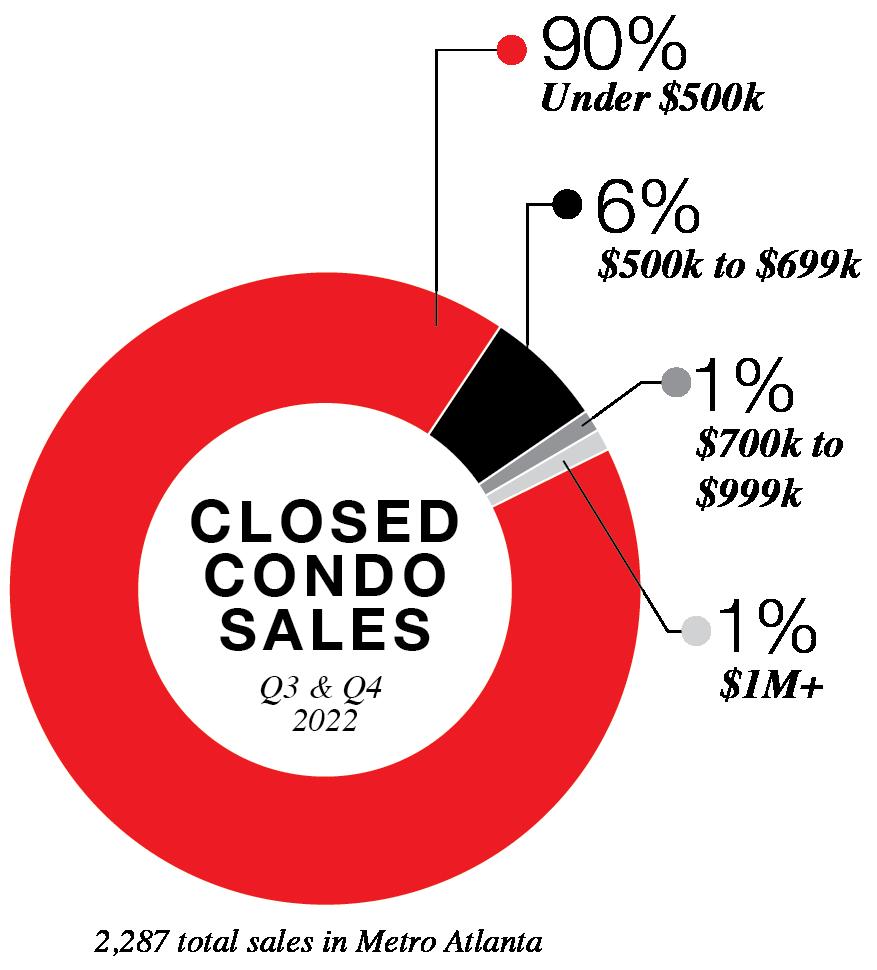

# Closed Sales % of All Closed Condo Sales # Active Listings % of All Active Condo Listings Months of Inventory Average Days on Market < $300k 1,311 q -44.3% 57% 331 q -27.9% 36% s 1.1 s 21 $300k - $499k 756 q -14.7% 33% 271 p +1.9% 32% s 1.8 s 21 $500k - $699k 134 q -27.2% 6% 94 q -8.7% 11% r 3.2 r 37 $799k - $999k 51 q -19.0% 2% 59 q -13.2% 7% r 4.2 r 36 $1M+ 32 q -38.5% 1% 74 p +1.4% 9% r 7.5 r 57 Total 2,284 q -35.5% 100% 854 q -13.6% 100% s 1.7 s 23

q Down YOY p Up YOY s Below Market Average r Above Market Average w Equal to Market Average

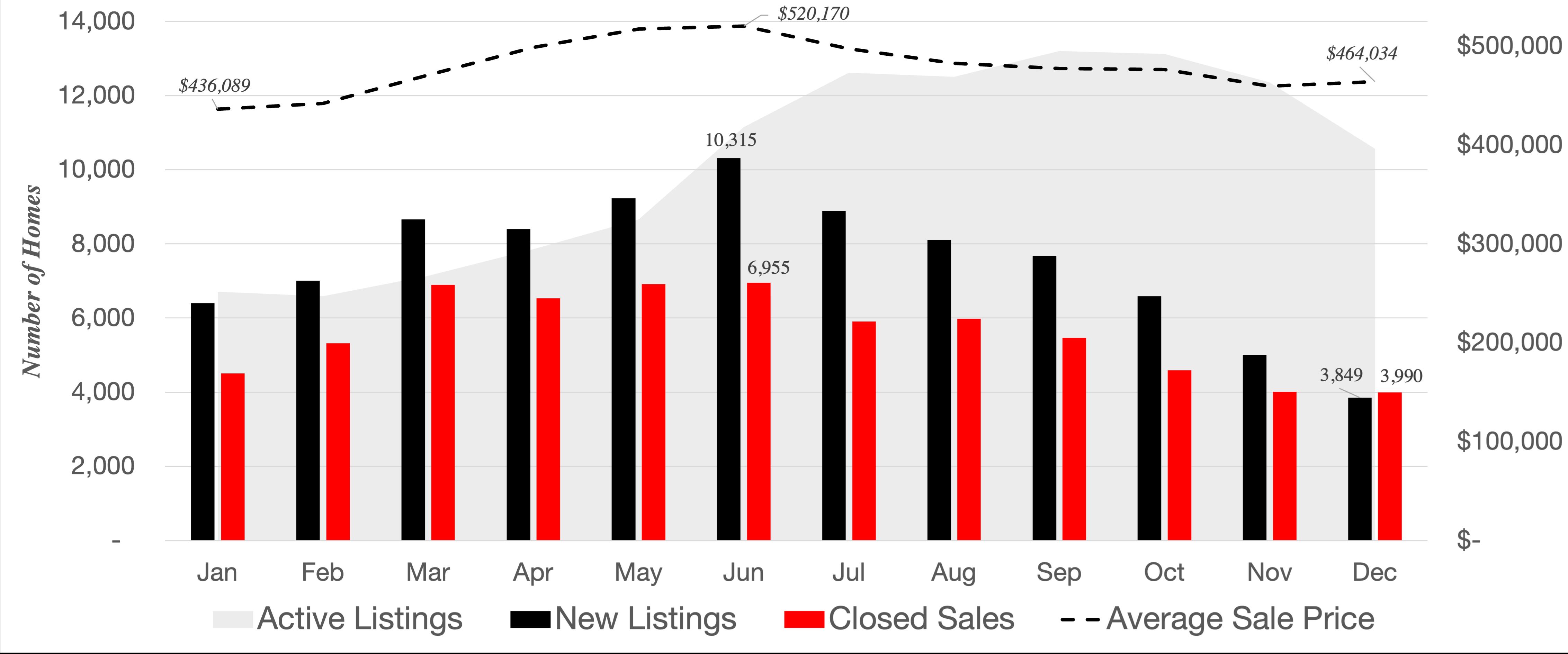

Single-Family Homes

In 2022, most homes sold in Metro Atlanta were detached single-family homes (77%). There were 51,855 single-family homes sold last year, the fewest of any 12-month period since 2015. Like the market overall, there were about 30% fewer singlefamily homes sold in the second half

of 2022 (23,169 homes) compared to the same period in 2021, a trend related to higher mortgage interest rates.

The average single-family home in Metro Atlanta sold for $509,136 in Q3 and Q4 2022, up 10% year-

Metro Atlanta Single-Family Home Summary (Q3 & Q4 2022)

over year. Since the same period in 2019, the average sale price was 49% ($167,570), resulting in significant equity for existing homeowners. While negotiation and some seller concessions became more common than early in the year, sellers continued to get close to

Source: FMLS InfoSparks, Greater Atlanta Area, Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 36 ENGEL & VÖLKERS www.evatlanta.com Metro Atlanta City of Atlanta ITP closed Sales 23,169 q -29.6% 2,716 q -34.0% 3,297 q -32.8% Pending Sales 20,319 q -32.6% 2,447 q -34.2% 2,921 q -34.2% active Listings 10,004 p +53.0% 1,528 p +18.7% 1,838 p +19.1% New Listings 31,1614 q -11.7% 4,615 q -10.8% 5,572 q -8.8% Median Sale Price $421,400 p +9.5% $490,000 p +7.8% $526,250 p +10.8% average Sale Price $509,136 p +10.0% $657,850 p +6.3% $682,681 p +7.3% average Sale Price to Original List Price Ratio 97.2% q -3.7% 96.2% q -2.3% 97.9% q -1.7% Months of Inventory 2.2 p +83.3% 2.7 p +50.0% 2.7 p +50.0% average Days on Market 26 p +44.4% 26 p +13.0% 26 p +8.3%

q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

their asking price in late 2022, with an average sale price to original list price of 97.2%.

The tight inventory of single-family homes for sale (2.2 months of inventory) is a key reason prices have continued to rise even as higher interest rates dampened demand.

Single-family home sales under $500,000 (-36.9%) were down more than higher priced homes in late 2022. This is in part because rising home prices overall pushed more homes into higher price brackets.

Source: FMLS InfoSparks, Greater Atlanta Area, Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

Source: FMLS InfoSparks, Greater Atlanta Area, Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 37 ENGEL & VÖLKERS www.evatlanta.com Less than $499,999 $500,000 to $699,999 $700,000 to $1 million Over $1 million closed Sales 14,978 q -36.9% 4,590 q -14.4% 2,237 q -4.8% 1,311 q -8.6% Pending Sales 13,177 q -40.2% 4,133 q -13.4% 1,919 q -4.3% 1,090 q -16.9% active Listings 5,651 p +53.1% 1,941 p +84.2% 1,072 p +71.2% 1,051 p +43.0% New Listings 19,452 q -21.7% 6,211 p +12.9% 2,973 p +19.7% 2,173 p +20.5% average Sale Price to Original List Price Ratio 96.7% q -4.5% 98.1% q -2.7% 98.4% q -1.5% 97.4% u 0.0% Months of Inventory 1.9 p +111.1% 2.3 p +64.3% 2.6 p +44.4% 4.4 p +41.9% average Days on Market 26 p +62.5% 24 p +33.3% 24 p +9.1% 31 q -8.8% 1-bedroom 2-bedroom 3-bedroom 4-bedroom + Median Sale Price $186,000 q -25.4% $295,000 p +11.3% $339,000 p +11.1% $499,900 p +12.3% average Sale Price $233,761 q -26.3% $321,689 p +8.7% $368,869 p +10.7% $605,113 p +10.8% closed Sales 33 q -31.3% 856 q -21.7% 8,360 q -27.6% 13,920 q -31.1% Pending Sales 36 q -18.2% 765 q -26.0% 7,592 q -29.5% 11,977 q -34.5% active Listings 187 p +83.3% 385 p +18.8% 3,361 p +50.4% 6,077 p +56.7% New Listings 512 p +66.2% 1,202 q -12.7% 11,245 q -13.3% 18,684 q -11.7% average Sale Price to Original List Price Ratio 91.7% q -2.7% 96.1% q -2.5% 96.8% q -4.3% 97.4% q -3.5% Months of Inventory 28.0 p +85.4% 2.4 p +26.3% 2.1 p +75.0% 2.2 p +83.3% average Days on Market 31 q -11.4% 25 p +13.6% 26 p +62.5% 26 p +44.4%

Metro Atlanta Single-Family Home Summary by Price Range (Q3 & Q4 2022)

Metro Atlanta Single-Family Home Summary by Number of Bedrooms (Q3 & Q4 2022)

q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

Single-Family Homes - Inside the Perimeter

Homebuyers looking for a singlefamily home ITP paid an average of $682,681 in the second half of 2022, up 7.3% from the same period in 2021. Intown living commanded a substantial premium compared to more suburban locations, with an average price $173,545 (34%) higher for ITP homes compared to the metro average.

Although prices continued to grow year-over-year, the market was quieter in the second half of 2022, with 32.6% fewer single-family homes sold ITP compared to the same period last year. Homes priced between $700,000 and $1 million kept the closest pace to 2021 (-4.8% fewer sales), likely because these more affluent buyers may be less sensitive to interest rates, more homes were priced in this range, and buyers previously looking at homes priced over $1 million may have shifted their search to this range.

Continued price growth has reduced the number of single-family homes

available at an entry level price point in Metro Atlanta. In the second half of 2022, just 65% of single-family homes sold for less than $500,000. This is down from the same period in 2021, when 72% of homes sold for less than $500,000. In 2019, it was 86%. This trend was even more pronounced ITP. In the second half of 2022, less than half of all singlefamily homes (47%) ITP sold for less than $500,000.

Fewer homes have been listed in Metro Atlanta each month since summer 2022, reflecting seasonal trends and rising interest rates that have made current homeowners hesitant to move. In the ITP singlefamily home market, this trend held up for homes under $500,000. There were 14% fewer new listings in the second half of 2022 compared to the same period in 2021, a decline that outpaced the dwindling share of homes sold for less than $500,000. Homeowners in this price range may be more sensitive to rising interest rates, less willing to move, or may be listing their homes at higher prices. At higher price points, the number of listings rose compared to the same period in 2021, with 20% to 22% more homes for sale in 2022.

Key Stats ITP Single-Family Homes

(Q3 & Q4 2022)

• $682,681 average sale price (+7.3% YOY)

• 14% of all single-family home sales were ITP

• 18% of all single-family home listings were ITP

• ITP homes sold at the same pace as the metro average (26 days on market)

• Homes sold for 97.9% of the original list price on average

Inventory levels remained relatively low at 2.1 months of supply for homes between $500,000 and $999,999 and 3.3 months of supply for homes over $1 million.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 38 ENGEL & VÖLKERS www.evatlanta.com

Q3 + Q4 2022 ITP Single-family Home Superlatives

Most Expensive Area to Buy a Single-Family Home ITP Chastain Park (Average sale price of $2,281,660)

Fastest Growing Average Single-Family Home Prices ITP

Brookwood Hills (+29.9% Q3/Q4 average closed sale price in 2022 vs. 2021)

Highest Price Per Square Foot for Single-Family Homes ITP Cabbagetown (Average $449/SF)

Shortest Average Days on Market ITP Inman Park (Average 10 days on market)

Where Can You Buy the Typical Single-Family Home for...

Less than $499,999

Cascade East

Cascade West

College Park

East Atlanta

East Point

Hapeville

Summerhill

West End/

Capitol View

$500,000 to $699,999 $700,000 to $1 million Over $1 million

Avondale Estates

Cabbagetown

Chamblee

East Lake

Edgewood

Grant Park/ Glenwood Park

Kirkwood

Ormewood Park

Reynoldstown

West Midtown/ Underwood Hills

Brookhaven

Collier Hills/ Ardmore Park

Decatur

Druid Hills/ Emory

Lake Claire/Little

Five Points

Oakhurst

Old Fourth Ward

Peachtree Hills

Vinings

Ansley Park/ Sherwood Forest

Brookwood Hills

Buckhead

Chastain Park

Garden Hills

Inman Park

Virginia

Highlands/ MorningsideLenox Park

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 39 ENGEL & VÖLKERS www.evatlanta.com

Price brackets based on 6-month rolling average sale price in analyzed area as of December 2022 from FMLS

Source: FMLS InfoSparks, Rolling 6-months as of December 2022

ITP Single-Family Home Summary by Neighborhood - Q3 & Q4 2022

Source: FMLS InfoSparks,Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 40 ENGEL & VÖLKERS www.evatlanta.com

Area Number of SingleFamily Homes Sold in Q3 & Q4 Average Closed Sale Price Median Closed Sale Price Average PPSF Months of Inventory Average Days on Market Ansley Park/ Sherwood Forest 22 $1,446,645 q -25.7% $1,138,350 q -34.6% $426 p +0.7% r 4.3 r 39 Avondale Estates 53 $666,762 p +18.0% $648,000 p +12.6% $263 p +10.5% s 1.1 r 30 Brookhaven 233 $899,054 p +7.6% $770,000 p +6.7% $303 p +9.8% s 1.9 s 23 Brookwood Hills 6 $1,857,417 p +29.9% $1,428,500 q -3.7% $398 p +14.7% s 1.4 r 73 Buckhead 404 $1,483,149 p +6.1% $1,205,000 p +10.6% $354 p +9.9% r 2.7 r 27 Cabbagetown 12 $581,083 p +5.2% $546,500 q -11.4% $449 p +20.4% r 2.3 r 45 Cascade East 107 $359,717 p +16.7% $325,000 p +4.9% $186 p +5.1% r 3.2 r 31 Cascade West 97 $342,230 p +9.5% $287,750 p +8.6% $165 p +12.2% r 2.3 r 27 Chamblee 55 $570,043 p +4.0% $530,000 p +10.6% $280 p +13.4% s 1.9 r 28 Chastain Park 25 $2,281,660 p +23.3% $1,850,000 p +18.3% $398 p +16.0% r 2.7 r 27 College Park 73 $335,665 p +7.1% $275,000 q -6.6% $175 p +18.2% r 3.6 r 27 Collier Hills/ Ardmore Park 18 $931,361 p +13.7% $962,500 p +20.7% $391 p +13.7% s 1.6 s 13 Decatur 98 $782,544 p +8.3% $699,500 p +6.4% $232 p +7.4% s 1.2 s 23 Druid Hills/ Emory 48 $938,275 q -8.2% $834,000 q -1.9% $336 p +5.0% s 2.1 r 38 East Atlanta 55 $491,075 p +2.6% $469,900 p +3.4% $301 q -1.0% s 1.7 s 21 East Lake 35 $674,455 p +23.9% $640,000 p +10.7% $318 p +16.5% s 2.1 s 20 East Point 132 $296,117 p +13.9% $300,000 p +17.3% $196 p +18.1% r 2.6 s 24 q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 41 ENGEL & VÖLKERS www.evatlanta.com Area Number of SingleFamily Homes Sold in Q3 & Q4 Average Closed Sale Price Median Closed Sale Price Average PPSF Months of Inventory Average Days on Market Edgewood 33 $578,905 p +6.8% $525,000 q -5.0% $317 p +3.6% r 2.9 s 18 Garden Hills 17 $1,205,647 p +21.5% $1,200,000 p +20.6% $382 p +11.4% r 2.8 r 35 Grant Park/ Glenwood Park 57 $672,259 p +13.9% $625,000 p +10.8% $362 p +8.7% s 1.0 s 18 Hapeville 23 $307,392 p +6.1% $265,000 p +0.0% $221 p +18.8% s 2.1 s 24 Inman Park 10 $1,134,000 p +16.9% $1,125,000 p +49.0% $441 p +3.5% s 0.9 s 10 Kirkwood 49 $687,373 p +16.3% $645,000 p +8.8% $357 p +10.2% s 1.8 s 18 Lake Claire/ Little Five Points 40 $951,508 p +18.7% $859,750 p +11.7% $363 p +4.9% s 2.0 r 27 Midtown 13 $1,193,869 p +32.7% $1,025,000 p +18.0% $402 p +15.2% r 3.0 r 29 Oakhurst 21 $879,500 p +10.3% $750,000 p +2.0% $403 p +7.5% s 1.1 r 27 Old Fourth Ward 18 $892,312 p +23.3% $726,100 p +5.2% $400 p +7.0% r 3.6 r 30 Ormewood Park 19 $665,18 p +12.4% $530,000 q -3.9% $351 p +6.7% s 1.1 s 22 Peachtree Hills 23 $854,963 p +2.2% $773,000 p +1.0% $413 p +15.7% s 1.5 s 15 Peoplestown/ Chosewood Park/ Lakewood Heights 68 $342,490 p +2.3% $329,000 p +4.8% $226 p +3.7% r 3.7 w 26 Reynoldstown 9 $642,322 p +9.6% $599,900 p +7.8% $353 q -5.4% r 2.6 r 28 Summerhill 9 $474,765 q -5.2% $513,000 p +5.8% $262 q -6.8% s 1.8 r 33 Vinings 38 $861,873 q -5.8% $742,000 q -10.6% $233 q -6.4% w 2.2 r 30 Virginia Highlands/ Morningside 102 $1,182,769 p +0.7% $1,099,000 p +13.2% $412 p +11.1% s 2.1 s 20

q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

ITP Single-Family Home Summary by Neighborhood - Q3 & Q4 2022 (Continued)

ITP Single-Family Home Summary by Neighborhood - Q3 & Q4 2022 (Continued)

New Construction Single-Family Homes ITP

Almost all the single-family homes sold ITP were resale. Of the 3,297 detached single-family homes sold ITP in the second half of 2022, only 160 were new construction, representing just 4.9% of sales. Most were “infill” homes built on a lot in an established neighborhood, rather than as new subdivisions as seen in many OTP areas. They ranged from $279,000 for a 2-bedroom, 742-square-foot home in English Avenue to $5,779,000 for a custom 7-bedroom home with more than 11,000 square feet in Mount Paran.

Most were priced under $600,000 (59%); however, a significant number of homes priced over $1 million (23%) brought the average sale price for a new home ITP to $931,134. New homes priced under $600,000 were typically located on the south and west sides in places like Pittsburgh, Oakland City, Mozley Park, Bankhead, and Hapeville. Homes over $1 million were typically located on the north and east sides of town in places like Oakhurst, Buckhead, and Brookhaven.

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 42 ENGEL & VÖLKERS www.evatlanta.com Area Number of SingleFamily Homes Sold in Q3 & Q4 Average Closed Sale Price Median Closed Sale Price Average PPSF Months of Inventory Average Days on Market West End/ Adair Park/ Pittsburgh/ Capitol View/ Sylvan Hills 227 $377,171 p +14.6% $360,000 +7.5% $227 p +7.1% r 4.0 r 28 West Midtown/ Underwood Hills 173 $545,640 p +9.9% $543,000 p +9.7% $266 p +2.7% r 2.4 s 24

New Construction Single-Family Homes Sold ITP - Q3 & Q4 2022

Source: FMLS, New Construction Single-Family Homes, ITP, Rolling 6-month as of December 2022 (YOY change is compared to rolling 6-month period as of December 2021)

Single-Family Homes - Outside the Perimeter

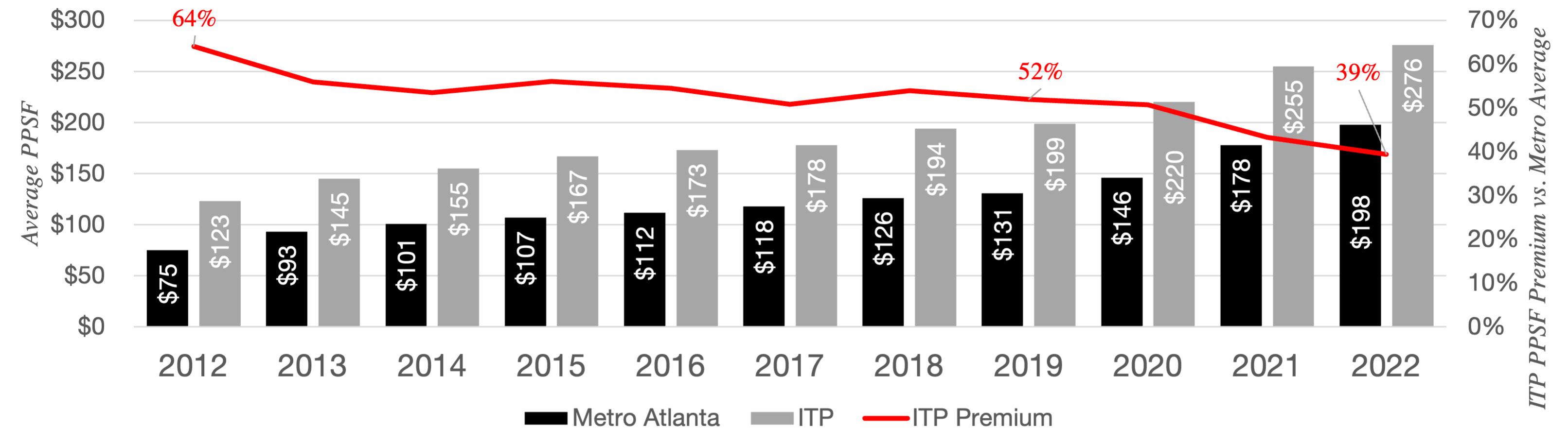

Single-family homes continue to be the primary type of housing outside the perimeter. Homes in suburban areas tend to offer more space at a lower cost per square foot, an appealing option for families and other buyers looking to get more for their money. However, the relative savings of OTP living has been declining in recent years. A decade ago, ITP homes cost 64% more per square foot (PPSF) than the average home in Metro Atlanta ($123/SF ITP compared to $75/SF on average). In late 2022, that premium had declined

to 39% ($276/SF ITP compared to $198/SF on average). This may reflect factors like an increase in the share of homes built OTP since 2012 (which tend to be smaller than those built in previous decades), an increasing share of new homes in the suburbs (which tend to cost more per square foot than resale), rising property values as suburban cities have developed their own town centers and amenities, or shifting preferences toward suburban living since the COVID-19 pandemic, which accelerated the shrinking gap between intown and suburban PPSF.

Still, homes in suburban Atlanta remain relatively affordable, and many places have average home prices below the national average.

Key Stats

OTP

SingleFamily Homes

(Q3 & Q4 2022)

• 86% of all single-family home sales were OTP

• 82% of all single-family home listings were OTP

Metro Atlanta vs. ITP Price Per Square Foot - Single-Family Homes (Q3 & Q4, 2012 to 2022)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 43 ENGEL & VÖLKERS www.evatlanta.com

Source: FMLS, Metro Atlanta, FMLS, Rolling 6-month as of December of each year

Q3 + Q4 2022 OTP Single-family Home Superlatives

Most Expensive Area to Buy a Single-Family Home OTP

Fastest Growing Average Single-Family Home Prices OTP

Highest Price Per Square Foot for Single-Family Homes OTP

Shortest Average Days on Market OTP

Milton (Average Q3/Q4 sale price $1,315,685)

Milton (+24.3% Q3/Q4 average closed sale price in 2022 vs. 2021)

Chattahoochee Hills (Average $397/SF)

Tied between Dunwoody, McDonough, and Tucker (Average 19 days on market)

Where Can You Buy the Typical Single-Family Home for...

Less than $499,999 $500,000 to $699,999 $700,000 to $1 million Over $1 million

Acworth

Clarkston

Douglasville

Fairburn

Fayetteville

Kennesaw

Lawrenceville

Mableton

McDonough

Norcross

Snellville

South Fulton

Sugar Hill

Tucker

Union City

Woodstock

Canton

Cumming

Duluth

Dunwoody

East Cobb

Marietta

Peachtree City

Peachtree

Corners

Smyrna

Suwanee

Alpharetta

Chattahoochee Hills

Johns Creek

Roswell

Milton Sandy Springs

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 44 ENGEL & VÖLKERS www.evatlanta.com

Price brackets based on 6-month rolling average sale price in analyzed area as of December 2022 from FMLS

Source: FMLS InfoSparks, Rolling 6-months as of December 2022

OTP Single-Family Home Summary by Area - Q3 & Q4 2022

Source: FMLS InfoSparks, Single-family homes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 45 ENGEL & VÖLKERS www.evatlanta.com Area Number of SingleFamily Homes Sold in Q3 & Q4 Average Closed Sale Price Median Closed Sale Price Average PPSF Months of Inventory Average Days on Market Acworth 647 $435,543 p +7.6% $395,000 p +7.0% $182 p +11.7% s 2.1 s 24 Alpharetta 666 $771,394 p +14.4% $677,450 p +16.4% $232 p +14.3% s 1.7 s 23 Canton 812 $530,669 p +13.2% $472,000 p +11.7% $194 p +13.5% r 2.4 r 30 Chattahoochee Hills 27 $986,497 p +25.9% $828,815 p +6.0% $397 p +5.9% r 2.3 r 55 Clarkston 18 $317,308 p +4.7% $346,675 p +16.3% $203 p +13.4% r 2.6 r 40 Cumming 1,161 $599,245 p +14.0% $563,911 p +17.5% $204 p +14.0% s 1.9 s 23 Douglasville 735 $339,364 p +9.9% $320,000 p +10.2% $161 p +10.3% r 2.3 r 27 Duluth 290 $536,650 q -4.4% $443,500 p +6.9% $193 p +9.0% s 2.0 s 25 Dunwoody 157 $665,151 p +7.2% $624,000 p +5.8% $224 p +8.2% s 1.5 s 19 East Cobb 1,059 $593,834 p +13.7% $500,000 p +13.6% $205 p +15.2% s 1.6 s 23 Fairburn 260 $370,372 p +13.7% $374,250 p +17.3% $150 p +14.5% r 2.3 s 23 Fayetteville 192 $492,099 p +15.4% $424,875 p +18.0% $168 p +9.1% r 2.8 r 29 Johns Creek 214 $819,597 p +12.5% $750,000 p +19.0% $213 p +13.9% s 1.9 s 23 Kennesaw 504 $459,439 p +10.7% $410,000 p +12.2% $183 p +10.9% s 1.7 s 23 Lawrenceville 1,229 $406,247 p +13.1% $385,000 p +11.6% $172 p +12.4% w 2.2 r 29 Mableton 216 $392,413 p +10.3% $361,750 p +3.3% $182 p +13.8% s 1.8 r 29

q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

OTP Single-Family Home Summary by Area - Q3 & Q4 2022 (Continued)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 46 ENGEL & VÖLKERS www.evatlanta.com Area Number of SingleFamily Homes Sold in Q3 & Q4 Average Closed Sale Price Median Closed Sale Price Average PPSF Months of Inventory Average Days on Market Marietta 1,677 $545,504 p +14.7% $450,000 p +9.8% $203 p +12.8% s 1.7 s 24 McDonough 379 $391,706 p +6.8% $385,000 p +8.8% $155 p +13.1% r 2.9 s 19 Milton 151 $1,315,685 p +24.3% $1,185,000 p +24.6% $266 p +23.1% r 2.9 r 31 Norcross 148 $343,414 p +4.4% $342,500 p +12.3% $189 p +5.0% r 2.4 s 24 Peachtree City 88 $521,049 q -3.7% $522,851 p +8.2% $189 0.0% w 2.2 r 31 Peachtree Corners 126 $620,226 p +13.7% $570,000 p +13.4% $196 p +16.0% s 1.5 s 21 Roswell 512 $715,738 p +14.3% $609,000 p +12.8% $222 p +12.7% s 1.6 s 20 Sandy Springs 198 $1,099,937 p +12.0% $857,500 p +11.4% $250 p +13.1% r 2.3 r 29 Smyrna 373 $528,569 p +6.7% $499,900 p +7.5% $227 p +12.9% s 1.7 w 26 Snellville 550 $382,744 p +9.2% $355,000 p +11.1% $162 p +12.5% w 2.2 r 28 South Fulton 45 $304,235 q -14.1% $275,000 q -8.3% $146 p +10.6% r 4.5 s 23 Sugar Hill 184 $474,377 p +17.1% $437,500 p +13.6% $191 p +15.1% s 1.5 w 26 Suwanee 462 $663,609 p +12.8% $594,000 p +14.6% $193 p +13.5% s 1.7 s 24 Tucker 185 $427,703 p +12.7% $400,000 p +11.1% $200 p +8.1% s 1.7 s 19 Union City 84 $294,830 p +14.1% $302,500 p +18.6% $153 p +15.0% s 2.0 s 22 Woodstock 682 $477,807 p +13.4% $425,000 p +10.4% $202 p +14.8% s 1.8 s 24

q Down YOY p Up YOY s Below SFH Market Average r Above SFH Market Average w Equal to SFH Market Average

New Construction SingleFamily Homes OTP

There were 1,891 new construction single-family homes sold in Metro Atlanta in Q3 and Q4 2022. They sold for an average of $638,025, or $216 per square foot. Most single-family home construction in Atlanta is happening in the suburbs, particularly those north of Atlanta. Although some of these new homes were built as infill on lots in existing neighborhoods as is typical ITP, many were constructed as part of new subdivisions in suburban areas.

Gwinnett County had the most new construction single-family homes sold in late 2022 (393 homes), followed by Fulton (327), Cobb (224), Cherokee (219), and Forsyth (218) Counties.

The top cities for new singlefamily construction sales OTP were in the outer ring of the metro: Cumming, Canton, Loganville, and Fairburn. Marietta had the most new construction sales of closer in cities, with an average sale price of nearly $1 million for new single-family homes.

About 10% of new construction single-family homes sold in late 2022 were luxury homes priced at $1 million or higher. Most were in Fulton (45%), Cobb (21%), or DeKalb (16%) Counties. The most popular OTP cities for new homes over $1 million were Marietta (32 homes), Milton (20 homes), Alpharetta (16 homes), Canton (10 homes), and Johns Creek (10 homes).

The most affordable cities for new construction homes were all located south of Atlanta: Jonesboro ($290,000 average sale price), South Fulton ($312,495), Lovejoy ($379,066), East Point ($379,066), and Villa Rica ($382,463).

Top

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 47 ENGEL & VÖLKERS www.evatlanta.com

Rank City # New SFH Sold Q3 & Q4 2023 Average Sale Price Average PPSF 1 Cumming 122 $646,185 $219 2 Canton 121 $637,373 $224 3 Loganville 108 $469,280 $162 4 Fairburn 81 $416,608 $153 5 Marietta 80 $971,059 $254

Source: FMLS InfoSparks,Single-family homes, New construction, 7/1/22 to 12/31/22 Rank County # New SFH Sold Q3 & Q4 2023 % New SFH Sold Q3 & Q4 2023 Average Sale Price Average PPSF 1 Gwinnett 393 21% $549,806 $189 2 Fulton 327 17% $834,746 $250 3 Cobb 224 12% $732,459 $228 4 Cherokee 219 12% $605,668 $227 5 Forsyth 218 12% $664,512 $231 6 DeKalb 142 8% $754,734 $243 7 Henry 136 7% $443,716 $161 8 Rockdale 78 4% $427,955 $165 9 Douglas 73 4% $424,388 $165 10 Fayette 71 4% $569,896 $179 11 Clayton 10 1% $355,291 $140 Total 1,891 100% $638,025 $216 Source: FMLS InfoSparks,Single-family homes, New construction, 7/1/22 to 12/31/22

OTP Cities for New Construction Single-Family Home Sales (Q3 & Q4 2022)

New Construction Single-Family Home Sales by County (Q3 & Q4 2022)

Townhomes

There were 9,689 townhomes sold in Metro Atlanta in 2022, lower than the record sales of the pandemic era due to a slower second half of the year, but still 1% higher than in 2019.

Townhomes have become an increasingly popular choice for Metro Atlanta homebuilders and buyers over the past decade, offering many of the perks of a single-family home with a lower price tag and less exterior maintenance. In late 2012, 10.5% of all homes purchased in the metro were townhomes. In the second half of 2022, about 15% of Metro Atlanta homebuyers opted for townhomes, with 4,500 total sales in Q3 and Q4.

Although the total number of townhomes sold was down in the second half of 2022 (-26% compared to the same period in 2021) sale prices continued to rise. The average price for a townhome in Metro Atlanta

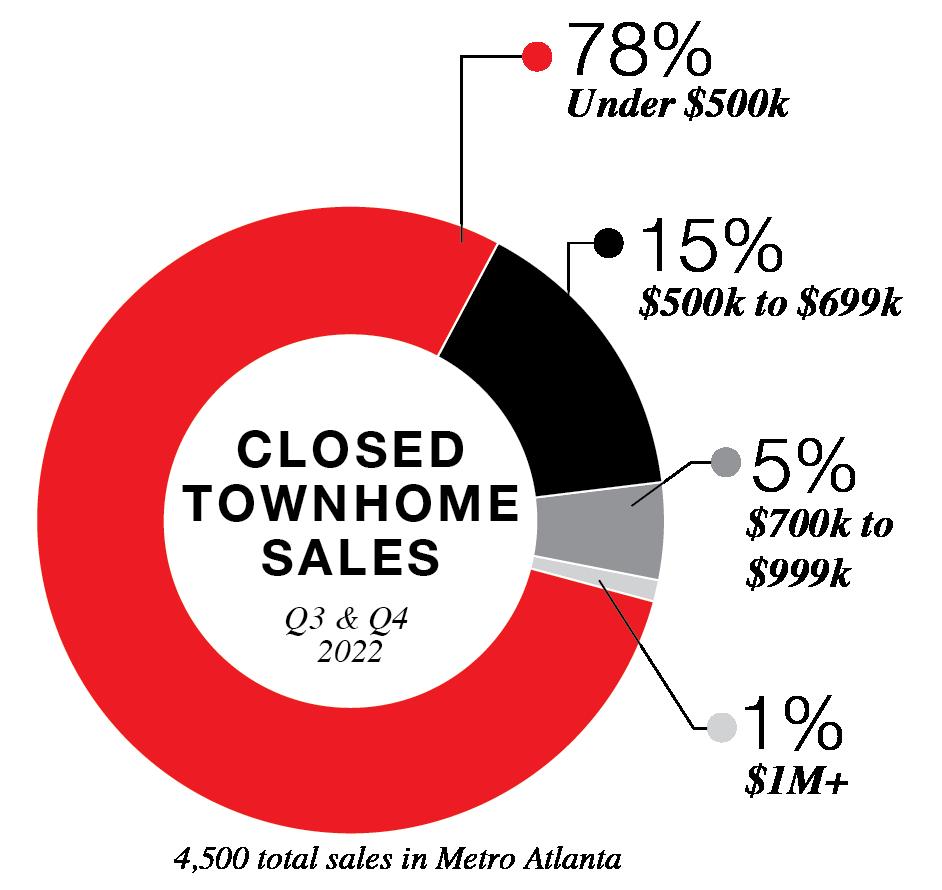

was $395,933 in Q3 and Q4, 10% higher than the same period in 2021, in part because of limited inventory. 78% of townhomes sold for less than $500,000. Even with growing prices, townhomes remain a more affordable option than detached single-family homes, which sold on average for $113,149 more than the average townhome.

This relative cost savings is a key factor in the growing popularity of townhomes. There were just 1.9 months of townhome inventory in late 2022, a slightly tighter supply than the market overall. They went under contract in 22 days on average, faster than single-family homes or condominiums.

Most townhome sales were in suburban areas outside the perimeter, with about a quarter of townhome sales ITP. Threebedroom townhomes were the

Key Stats

Metro Atlanta

Townhomes

(Q3 & Q4 2022)

• $395,933 average sale price (+10.1% YOY)

• 15% of all homes sold were townhomes

• Townhomes sold 3 days faster than average (22 days on market)

• Townhomes sold for 98.7% of the original list price on average, the highest of any home type

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 48 ENGEL & VÖLKERS www.evatlanta.com

most purchased category, making up 62% of all townhome sales and averaging $403,020. Although they made up a smaller share of the market, 2-bedroom townhomes have the highest relative demand, with just 1.5 months of supply in Metro Atlanta.

While luxury townhomes continue to be a small portion of the overall townhome market (less than 2% of sales), there were 14% more townhomes sold for $1 million or more in the second half of 2022

compared to 2021. This shows a growing number of luxury buyers interested in a low-maintenance townhome lifestyle and an expanding portfolio of new luxury townhomes to choose from. With a smaller pool of luxury buyers, these townhomes tended to stay on the market about twice as long as more affordable townhomes, averaging 44 days on the market.

Metro Atlanta Townhome Summary (Q3 & Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, Townhomes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 49 ENGEL & VÖLKERS www.evatlanta.com Metro Atlanta City of Atlanta ITP Median Sale Price $350,000 p +7.7% $440,000 p +6.8% $475,000 p +9.8% average Sale Price $395,933 p +10.1% $490,686 p +11.6% $517,902 p +11.1% closed Sales 4,500 q -26.0% 963 q -31.4% 1,023 q -34.0% Pending Sales 3,871 q -32.6% 804 q -38.6% 835 q -41.6% active Listings 1,559 p +38.6% 383 p +7.6% 402 p +1.8% New Listings 5,561 q -11.7% 1,261 q -16.0% 1,287 q -21.1% average Sale Price to Original List Price Ratio 98.7% q -2.5% 98.7% q -1.1% 98.7% q -0.9% Months of Inventory 1.9 p +72.7% 2.0 p +42.9% 2.0 p +42.9% average Days on Market 22 p +4.8% 26 0.0% 26 q -3.7%

q Down YOY p Up YOY

Source: FMLS InfoSparks, Greater Atlanta Area, Townhomes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

Q4 2022)

Source: FMLS InfoSparks, Greater Atlanta Area, Townhomes, Rolling 6-months as of December 2022 (year-over-year change compared to rolling 6-months as of December 2021)

2022 END OF YEAR ATLANTA MARKET INTELLIGENCE 50 ENGEL & VÖLKERS www.evatlanta.com 1-bedroom 2-bedroom 3-bedroom 4-bedroom Median Sale Price $247,500 p +39.4% $264,000 p +12.2% $367,365 p +11.3% $516,000 p +13.3% average Sale Price $252,273 p +20.7% $283,975 p +8.1% $403,020 p +11.8% $572,671 p +16.9% closed Sales 26 p +4.0% 1,079 q -19.1% 2,807 q -24.4% 593 q -41.2% Pending Sales 22 q -8.3% 1,004 q -21.4% 2,364 q -32.5% 482 q -48.9% active Listings 23 p +76.9% 293 p +18.6% 977 p +46.9% 267 p +33.5% New Listings 92 p +55.9% 1,292 q -8.8% 3,378 q -12.1% 801 q -18.3% average Sale Price to Original List Price Ratio 97.0% q -2.3% 98.3% q -2.5% 99.0% q -2.4% 98.5% q -2.2% Months of Inventory 4.1 p +95.2% 1.5 p +25.0% 1.9 p +72.7% 2.3 p +91.7% average Days on Market 22 q -8.3% 21 p +16.7% 22 p +10.0% 26 q -7.1%

Less than $499,999 $500,000 to $699,999 $700,000 to $1 million Over $1 million closed Sales 3,525 q -30.6% 688 q -7.8% 230 p +14.4% 57 p +14.0% Pending Sales 3,115 q -34.9% 550 q -21.1% 157 q -27.0% 49 q -2.0% active Listings 1,002 p +31.2% 323 p +68.2% 141 p +50.0% 49 p +32.4% New Listings 4,089 q -19.5% 915 p +23.1% 309 p +7.7% 105 p +61.5% average Sale Price to Original List Price Ratio 98.6% q -2.8% 99.2% q -1.0% 98.8% q -0.5% 98.5% p +1.9% Months of Inventory 1.5 p +66.7% 2.7 p +68.8% 3.5 p +20.7% 5.0 p +31.6% average Days on Market 20 p +11.1% 25 q -21.9% 33 q -26.7% 44 p +25.7%

Metro Atlanta Townhome Summary by Number of Bedrooms (Q3 &

Metro Atlanta Townhome Summary by Price Range (Q3 & Q4 2022)

Down YOY p Up YOY

q

Townhomes - Inside the Perimeter

The growing trend toward townhomes has been even stronger ITP than in the metro overall. In the late 2012, 13% of all homes sold ITP were townhomes. By the second half of 2022, 18% were townhomes (1,023 sales). The cost savings compared to a detached single-family home was greater too. In Q3 and Q4 2022, the average ITP townhome cost $517,902, about $164,355 (24%) cheaper than the average detached single-family home. About 55% of ITP townhomes sold for less than $500,000, a higher share than the 47% of ITP single-family homes in the same price range.

Like the market overall, the total number of townhomes sold ITP was down in the second half of 2022 compared to the same period in 2021 (-34%). As with single-family homes, intown sales for townhomes under $500,000 were down more

than those at higher price points (-43.3%), reflecting greater buyer sensitivity to rising interest rates in the entry level price range.

The ITP luxury townhome market is small but growing. Townhomes priced over $1 million were the only price range with more ITP sales in late 2022 compared to 2021 (+2.7%) but remained a fraction of the market with just 38 sales. Though small, that is 475% more luxury townhomes sold than a decade ago. The number of new listings for townhomes over $1 million ITP is up significantly (+41.2% compared to late 2021) while new listings at lower price points is down (-22.6%), reflecting fewer of the less expensive resale townhomes being listed and higher price tags for new construction townhomes being delivered in a period with high construction costs.

Key Stats ITP Townhomes

(Q3 & Q4 2022)

• $517,902 average sale price (+11.1% YOY)

• 18% of all ITP homes sold were townhomes