• The Hidden Supply Line: Inside America’s Shadow Inventory and Off-Market REOs

• Creative Capital: Financing REO Deals in a High-Rate Market

• The Psychology of the Deal: How Buyer Perception Shapes REO Demand in 2025

• Clearing the Clouds: Legal Tactics for REO Title Risk and Lien Resolution

• The Risk Premium: How Climate and Insurance Costs Are Repricing REOs

• The Clock and the Conversion: How Lenders Decide When a Foreclosure Becomes an REO

• Hidden Markets: Finding Off-Market and Under-Market REO Opportunities

• The Exit Equation: Mastering Deeds, Short Sales & Strategic Foreclosures

• The Delinquency Curve: Reading the Early Warnings of 2026

• The Winter Turn: How Seasonal Cycles Reset the REO Market

Editor’s Note

Welcome to the November edition of The Real Estate Magazine, published by REOBroker.com. As 2025 draws to a close, the real estate market finds itself at an inflection point where data, discipline, and strategic vision matter more than ever. The decisions professionals make now will echo well into 2026, defining who is positioned to seize opportunity in a rapidly evolving housing and REO landscape

Signals Beneath the Surface

While the broader market debates rate cuts and affordability, those of us in the REO and investment sectors know that the real story is always beneath the surface. Behind the headlines, lenders are tightening loss-mitigation pipelines, servicers are recalibrating valuations, and investors are beginning to sort markets by long-term potential rather than short-term volatility.

This month’s issue unpacks these underlying trends through a series of in-depth features designed to help you read the market before it moves From regional REO surges to subtle lender behavior shifts, our contributors focus on what data and experience tell us about the next phase of the cycle.

Inside This Issue

We begin with a national snapshot: The REO Momentum Index, a data-driven feature tracking year-over-year changes in foreclosure filings, bank repossessions, and asset dispositions. This piece identifies the metro areas showing early signs of inventory acceleration often months before those trends reach mainstream analysis.

Next, our article on “The Return of the Institutional Buyer” examines how hedge funds, private equity firms, and large-scale aggregators are quietly re-entering select markets Their activity provides not just competition but also valuable signals about pricing floors and asset-class preferences.

Our coverage of servicer workflow dynamics reveals how end-of-year accounting pressures are influencing REO release patterns, with some lenders pushing properties to market before Q1, while others delay listings until after fiscal close. Understanding these internal pressures helps agents, brokers, and asset managers time their acquisitions and marketing strategies effectively

On the valuation front, we investigate how appraisers and BPO providers are adapting to today’s hybrid pricing environment, where automated valuation models (AVMs) intersect with human expertise. The article breaks down how to challenge or validate valuation discrepancies that can make or break an REO deal

Beyond the Numbers

This issue also steps beyond metrics to explore the human and operational side of distressed real estate Our profile on several REO agents highlights the growing use of AI-driven CRMs, virtual walkthroughs, and automation in listing management tools that are transforming how professionals handle high-volume pipelines with precision and transparency

In “The New Frontier of REO Renovation,” we feature investors who are turning distressed assets into modern, sustainable homes through strategic design and adaptive reuse. These projects prove that profitability and community impact are not mutually exclusive they are increasingly intertwined.

We also confront the insurance and climate risk realities reshaping how distressed assets are underwritten and sold. As insurers retreat from high-risk zones and premiums climb, investors must adapt financing and exit models accordingly. This article offers frameworks for risk-adjusted acquisition planning in 2026.

The Year-End Mindset

November is the month to take inventory—not just of properties, but of priorities. The most successful professionals in this business don’t wait for January to plan; they use Q4 to sharpen focus, strengthen relationships, and prepare for the next market turn.

Our closing feature, “2026 Outlook: The Year of Strategic Repositioning,” offers forecasts on rate policy, credit markets, and distressed supply pipelines, drawing from economic data and interviews with leading analysts. The conclusion is clear: adaptability, liquidity, and knowledge will define the winners of the next phase

A Word from REOBroker.com

At REOBroker.com, we are committed to equipping our readers with the foresight and factual clarity needed to navigate the real estate market’s most complex corridors. Whether you are an agent, investor, lender, or asset manager, this publication exists to connect you with the data, ideas, and community that keep you ahead of the curve

Thank you for being part of our readership and for making this growing community a place where expertise is shared and opportunity is created May this November issue sharpen your insight and strengthen your strategy as you prepare to close the year with purpose and step into 2026 ready to lead.

Warm regards, The Editorial Team REOBroker.com Clarity. Insight. Opportunity

Asset Managers rely on REObroker.com to consistently find the nation's top REO specialists. We pre-screen our members for years of experience, training & certification, and asset manager references, holding each application to the highest standards.

The Benefits of Membership

In addition to the clear benefits of our referral network, REObroker.com members receive training, networking & advertising opportunities, and a wealth of pay-it-forward knowledge from our daily Member Discussion Forum.

REObroker.com is an esteemed designation and valuable association. Many of our members have stayed with us consistently through several REO cycles, realizing the long-term benefits.

Member Benefits

Minimum of 2 (BD) Broker Development Seminars a year

REOBroker.com Member Benefits

Minimum of 2 (BD) Broker Development Seminars a year

Access to a Minimum of 2 Zoom mastermind/training calls a month

Access to asset management company Roster

Access to Private Lender Roster

The internal chat line provides access to a wealth of knowledge and support through our diverse membership.

REOBroker.com does sponsorships with NADP, 5 Star, and other related Events.

National Exposure to asset managers and companies

Included on the REOBroker.com website with contact information and areas served

Included in REOBroker.com online HUD and Real Estate Magazines and National Campaigns

Opportunities to submit market updates and real estate articles in the magazines.

Membership benefit pricing for additional advertising in the following:

REOBroker.com HUD Magazines | REO Broker Real Estate Magazine | REOBroker TV | and Podcast.

Every real estate cycle contains a ghost market a volume of properties that exist but aren’t visible. In 2025, that market has reemerged as shadow inventory: foreclosed homes held by banks, GSEs, and private-equity firms that have not yet been listed or auctioned.

To the public, supply looks constrained To insiders, it’s clear that the distressed backlog remains substantial, just strategically withheld. This shadow supply represents both risk and opportunity: risk, because delayed releases distort pricing; opportunity, because professionals who find or forecast it can buy ahead of the crowd.

In essence, shadow inventory is a form of supply management, not secrecy It reflects the financial logic of institutions operating within regulatory and reputational constraints. TheHiddenSupplyLine:InsideAmerica’s

Understanding where these properties sit and why they’re hidden is the first step toward profiting from them.

Why Banks Hold Inventory Off-Market

There’s no conspiracy in shadow inventory, only strategy. Banks and servicers manage distressed portfolios like investment funds: they release properties when demand is strong and hold them when absorption weakens

Three main motives drive this behavior:

1. Price Stabilization.

Flooding the market with foreclosures drives values down, reducing recovery across the entire portfolio. Controlled release preserves balance-sheet optics and neighborhood stability.

2. Regulatory Reporting.

Certain assets are kept off-market until documentation or compliance issues are resolved often title defects, eviction holds, or municipal liens

3. Accounting and Tax Strategy. REO sales affect realized losses By timing disposition after fiscal year-end, institutions can defer recognition and present stronger quarterly statements.

Tracking the Invisible: Data and Field Clues

The trick for professionals is identifying where these properties sit in the cycle. Because shadow inventory isn’t listed, tracking relies on data triangulation reading between public filings, servicer reports, and field conditions

Start with foreclosure completion data. If trustee sales are increasing but public REO listings aren’t, the delta represents unlisted stock.

Next, analyze Fannie Mae and HUD REO performance dashboards they often show national totals far higher than active MLS counts.

Finally, look locally: boarded windows with recent lawn maintenance, winterized utilities, or posted inspection notices often signal “held” REOs. Field brokers, preservation vendors, and code enforcement staff are invaluable sources of intelligence when databases fall short.

The Role of Institutional Investors

Another layer of hidden supply sits within private-equity portfolios. Large funds that acquired bulk REO pools from HUD or Fannie Mae between 2010 and 2015 continue to hold residual assets Many are re-entering the market through secondary sales or joint-venture partnerships.

These institutional sellers operate discreetly, preferring off-market package sales to public listing exposure Their goal is liquidity without optics moving inventory to smaller investors in bulk transactions.

For brokers and syndicators, these relationships can be transformative Access to one portfolio partner can unlock hundreds of units over time, establishing a repeat pipeline insulated from retail competition.

Government and Servicer Disclosure Gaps

While transparency has improved since the Great Recession, federal reporting still lags behind real-time reality. HUD’s public data often trails actual repossessions by 90–120 days, and GSE reports exclude non-performing loans in interim management

This delay creates opportunity for those who monitor county recording offices or REO assignment filings directly Every recorded transfer from lender to trustee or asset management company is an early signal of coming listings. Professionals who aggregate these signals especially regionally can project the next wave of supply months ahead of competitors.

Turning Knowledge Into Leverage

Once shadow inventory is identified, timing and tact determine profitability Investors and agents can approach servicers offering pre-marketing purchase proposals, or position themselves as local listing partners when institutional releases begin.

The negotiation advantage lies in market readiness: if you can demonstrate proven capacity to move multiple assets quickly verified contractors, clean title partners, ready capital you become part of the solution, not the speculation

Lenders don’t want to hide forever; they want partners who can liquidate efficiently when release time comes.

Strategic Takeaways

1. Monitor Foreclosure-to-Listing Ratios. When auctions rise faster than MLS REOs, shadow stock is building

2. Follow County Recording Patterns. Title transfers to servicers or government agencies precede releases by 30–60 days.

3. Network with Preservation Vendors. Field contractors often see assets months before they’re assigned

4. Track Institutional Liquidations. Hedge funds quietly offload non-performing pools through brokers they trust.

5. Offer Solutions, Not Speculation. Banks respond to readiness fast closings, clean paperwork, and compliance capacity.

Conclusion: Seeing the Market

Before It’s Measured

Shadow inventory is not a mystery; it’s a market in waiting. Those who measure it through data, relationships, and diligence will dominate the first quarter of 2026 The next wave of REO opportunity will not appear suddenly It’s already here, invisible to the untrained eye.

The professionals who know how to look behind the numbers will once again prove that real estate rewards foresight more than fortune.

By the Editorial Team

The Real Estate Magazine | REOBroker com Seeing tomorrow’s listings today.

The defining challenge of 2025 has been the cost of money. After two years of rate volatility, lenders have tightened underwriting, investors are more selective, and many traditional buyers have been priced out. Yet the distressed-asset market continues to expand.

For REO professionals, the question isn’t whether deals can still be financed it’s how The winners in 2026 will not be those waiting for lower rates but those mastering alternative capital pathways that keep acquisitions and rehabs moving despite the credit squeeze

Private & Portfolio Lending: Speed Over Spread

Private lenders and portfolio banks have quietly become the backbone of the modern REO market Unlike conforming lenders, they lend against asset value, not borrower profile, allowing quick closes on properties that need work or lack retail comparables

Portfolio banks community and regional institutions that keep loans on their own books offer flexibility in underwriting repairs, title issues, or unconventional structures. Rates may run higher, but speed and certainty outweigh cost when a property’s window of opportunity is measured in days, not weeks.

For agents representing investors, cultivating direct relationships with these lenders is strategic infrastructure, not optional networking.

Bridge Loans & Interim Financing

Bridge financing has evolved from a niche product to a mainstream tool. Investors now use short-term, interest-only loans to acquire, stabilize, and refinance REOs once improvements lift value

A 6- to 12-month bridge loan often fills the gap between distressed acquisition and conventional take-out financing. Lenders favor these instruments because collateral is tangible and turnaround measurable Investors favor them because they preserve liquidity while unlocking control

The new discipline lies in exit precision underwriting every bridge with a clear refinancing or disposition plan before closing, not after.

Seller Financing & Structured Participation

With institutions eager to move assets off their balance sheets, seller financing is resurfacing as a tactical solution Banks, hedge funds, and government-contract servicers occasionally offer carryback notes especially for seasoned investors with a track record of performing rehabs

These arrangements reduce REO holding costs while producing predictable income for the lender. Some are even structured as shared-appreciation models, where the seller retains a percentage of resale profit in exchange for lower entry pricing.

For buyers, the advantage is obvious: immediate control with manageable capital outlay For lenders, it’s risk mitigation with upside potential a rare equilibrium in distressed finance.

Equity Syndication & Crowdfunding Evolution

Another innovation reshaping the capital landscape is fractional investment. Real-estate crowdfunding platforms and private syndicates allow multiple investors to participate in REO acquisitions through limited partnerships or digital tokens

While regulatory compliance remains complex, the democratization of access means liquidity now flows from broader sources. Seasoned operators use these models to fund multi-property portfolios quickly, leveraging their expertise while sharing risk and reward across partners.

For agents and brokers, this ecosystem opens new client categories investors seeking deal flow rather than physical ownership The opportunity is no longer just to sell property but to curate participation.

Renovation & Construction Loans Reimagined

FHA 203(k), Fannie Mae Homestyle, and private rehab loans remain underused tools for REO buyers. These programs finance both acquisition and renovation, consolidating costs into a single loan.

However, with rising rates, borrowers must be more strategic. Selecting contractors with proven draw-schedule discipline, locking materials early, and maintaining contingency reserves are now essential. Lenders increasingly require scope-of-work validation by licensed consultants a step that, though procedural, actually protects investors from cost overruns.

When structured properly, renovation financing transforms distressed assets into stabilized equity within one loan cycle

Partnerships Between Agents, Lenders & Investors

In today’s environment, deals are rarely closed by a single entity. Brokerages that build integrated capital networks pairing investors with private lenders, credit unions, and rehab specialists control the pipeline.

For property managers, these alliances provide recurring assignments; for lenders, they create reliable exit strategies. The REO professional’s value now extends beyond transaction management to capital orchestration the ability to match opportunity with funding instantly.

Strategic Takeaways

1. Prioritize Certainty Over Rate. A fast, reliable close at 9 percent is often cheaper than a failed one at 7 percent.

2. Maintain Multiple Lender Relationships. Diversify sources private, portfolio, bridge to adapt to deal type and timeline

3. Underwrite the Exit, Not the Entry. Every financing strategy must begin with a clear repayment or resale path.

4. Use Renovation Financing Intelligently. Integrate construction budgets early; lenders reward organization.

5. Think Like a Capital Manager. The modern REO agent is as much financier as facilitator.

Conclusion: Creativity as Currency

High rates don’t kill opportunity they clarify it. They expose inefficiency, reward preparedness, and elevate creativity to a financial skill. Those who master hybrid capital combining speed, structure, and strategy will continue to close while others wait for the cycle to shift.

In 2026, liquidity will belong not to the largest portfolios but to the most inventive minds.

Every real-estate transaction carries emotion, but nowhere is it more pronounced than in the sale of a distressed property. REOs once conjured images of blight and bureaucracy boarded windows, delayed closings, and endless paperwork Today, that stigma is fading A generation of digital-native buyers raised on renovation shows and house-flipping culture now view “distressed” as synonymous with potential

Yet perception remains uneven In markets like Atlanta, Phoenix, and Tampa, REOs are mainstream investment vehicles; in higher-income metros such as San Francisco or Boston, the term still triggers caution Understanding these psychological divides and communicating accordingly is the next frontier for REO professionals.

From Stigma to Strategy

The post-pandemic era reshaped consumer psychology. Limited supply and soaring prices pushed many would-be homeowners to explore alternative inventory sources. When faced with tight competition for retail listings, REOs began to look less risky and more opportunistic. What once symbolized failure now signals access.

Agents who adapt their messaging accordingly are outperforming peers. Instead of presenting REOs as “discount opportunities,” they frame them as “equity-building projects” or “value-add investments.” Language matters: “distressed” suggests decline, while “redevelopment opportunity” evokes creativity and control.

Behavioral economists call this framing bias the phenomenon in which the same data elicits opposite reactions depending on presentation. In REO marketing, framing determines whether buyers see obstacles or outcomes.

Risk, Reward, and the

Millennial Mindset

Millennial and Gen Z investors now dominant in small-to-mid-tier acquisitions interpret risk differently than their predecessors. They prize transparency over perfection and flexibility over guarantees. For them, a property needing work is not a deterrent but a path to customization. Technology reinforces this comfort: online 3-D tours, virtual inspections, and data-driven valuation tools mitigate uncertainty that once discouraged participation

Psychologically, these buyers are motivated by agency the belief that their personal effort can unlock value. An REO that requires vision aligns perfectly with this mindset. They aren’t chasing turnkey convenience; they’re chasing transformation.

Price Anchoring and Negotiation Behavior

Behavioral finance also explains why REOs continue to attract competitive bidding even in high-rate environments Buyers anchor expectations to list price, perceiving any discount as “winning.” Savvy investors exploit this by offering near-ask on undervalued properties while negotiating credits or post-closing repairs instead of headline reductions.

Lenders, meanwhile, anchor to broker price opinions (BPOs) and historical recovery ratios. Understanding both anchors allows brokers to mediate more effectively. When agents contextualize pricing using market psychology “this discount represents a $400/month equity advantage” they translate data into decision-ready emotion.

Trust and Transparency: The New Currency

In 2025’s information-saturated market, credibility drives conversion Buyers who feel informed are statistically more likely to close, even when risk remains. Full disclosure of repair estimates, title conditions, and neighborhood data turns skepticism into confidence. Paradoxically, exposing flaws strengthens trust; withholding them destroys it.

The emotional logic is simple: fear grows in the absence of facts. REO professionals who narrate risk honestly supported by visuals, third-party data, and repair timelines reduce cognitive friction and accelerate commitment

Designing the Buyer Experience

The most forward-thinking REO brokers are redesigning their digital presence around experience psychology. Listings now integrate storytelling: before-and-after imagery, renovation budgets, projected rents, and neighborhood revitalization narratives. This transforms a transactional listing into an aspirational journey

On-site showings mirror this shift Simple cues clean signage, professional photography, daylight scheduling reshape first impressions. Research in environmental psychology shows that buyer confidence increases by 20 percent when distressed properties are presented with contextual optimism rather than austerity.

Strategic Takeaways

1. Frame the Narrative. Replace negative terminology (“foreclosure,” “bankowned”) with constructive language (“equity opportunity,” “stabilized asset”).

2. Educate to Empower. Provide transparent repair data and financing options up front; informed buyers act decisively.

3. Leverage Behavioral Anchors. Understand how both list price and perceived discount drive emotional satisfaction.

4. Build Digital Trust. High-quality imagery and verified data increase perceived legitimacy critical for younger buyers.

5. Tell the Redevelopment Story. Connect each property to community improvement and personal creativity, not just profit

Conclusion: Selling Confidence, Not Inventory

In the emerging REO economy, perception is value

The assets themselves haven’t changed but the audience has Modern buyers respond to narrative, transparency, and empowerment more than to discounts or urgency Those who master the psychology of the deal turn skepticism into momentum and inventory into movement

When buyers stop fearing the word “foreclosure” and start imagining possibility, the REO professional’s job is done. That transformation mental, not mechanical is the real transaction

By

the Editorial Team

The Real Estate Magazine | REOBroker.com

Because markets move at the speed of perception

CLEARING THE CLOUDS: LEGAL TACTICS FOR REO TITLE RISK

AND LIEN RESOLUTION

The Hidden Cost of a Clouded Title

Every REO professional knows that a property’s biggest obstacle isn’t always its condition it’s its title. Behind many distressed assets lie years of unresolved encumbrances: unpaid taxes, code violations, unreleased loans, or heirs disputing ownership.

In a rising-interest-rate market where carrying costs grow by the day, these title defects can destroy profit margins and delay closings. The difference between a 30-day escrow and a 90day legal tangle often determines whether an investor stays liquid or locks capital indefinitely.

Title risk management, then, is not a closing detail it’s a core discipline. In distressed real estate, those who clear clouds fastest win first

Common Title Defects in REO Transactions

1. Unreleased Liens and Judgments.

Prior mortgages or HELOCs often remain open in county records even after payoff. Without proper reconveyance, the title remains encumbered.

2 Municipal Violations and Utility Liens.

Code enforcement fines and unpaid utilities can attach directly to property, surviving foreclosure if not addressed during transfer

3. Probate and Heirship Issues.

Inherited properties frequently enter foreclosure without clear succession, triggering claims from heirs or estate administrators.

4. Tax and HOA Super-Liens.

Certain states allow tax districts and homeowners’ associations to claim senior lien status, superseding even first-position mortgage rights.

Each of these defects carries its own legal path to resolution some administrative, others judicial. Knowing which is which saves time, money, and credibility.

Legal Tools for Title Clearance

1. Quiet Title Actions.

The most definitive remedy, a quiet title suit requests judicial confirmation of ownership and extinguishment of competing claims. Though effective, it requires time (30–120 days) and legal expense

2. Indemnity and Curative Instruments.

When the defect’s financial impact is minor or historical, servicers often opt for indemnity agreements, title endorsements, or gap insurance to proceed with closing while disputes resolve in parallel.

3. Escrow Holdbacks.

For unresolved liens with quantifiable amounts, escrow reserves can enable transaction completion without waiting for full clearance This tactic maintains liquidity while keeping liability controlled.

4. Re-Recording and Administrative Releases.

Many defects stem from clerical errors missed satisfactions or misindexed deeds. A proactive title officer can often secure releases through direct communication with lenders or clerks, avoiding litigation altogether

Each solution carries tradeoffs in time, certainty, and cost. The professional’s role is to select the tool that aligns with both transaction velocity and risk tolerance

Preventive Due Diligence: The Smart Investor’s Edge

The most successful REO buyers conduct title reconnaissance before the auction or offer stage. Reviewing county filings, verifying mortgage reconveyances, and checking for municipal or HOA violations ensures no unpleasant surprises at closing.

Technology now aids this process. Advanced title-reporting software integrates with county record databases, flagging liens, tax delinquencies, or code enforcement actions in real time Investors using these systems can model “true acquisition cost” purchase price plus remediation exposure long before title commitments arrive.

This preparation not only p negotiating leverage When probable cure, they can servicers rather than arbitrar

Servicer Coordination and L

Lenders and government en their own legal teams and these institutional protocols

HUD requires marketable before conveyance. Fannie Mae often ma vendor lists. Private lenders may re resolutions.

Professionals who can spe providing concise, com approvals and repeat busin just a marketer but a liaison

Strategic Takeaways

1 Start with the County Rec Public records reveal 80% review

2. Document Every Step. Maintain a digital file of corr for compliance audits.

3. Leverage Specialized Tit REO-savvy title companies generalists.

4 Negotiate with Precision Convert known defects into cost, then discount accordin

5. Time Is Value. Every extra day in escrow re to-delay ratio

Conclusion: The Real Estate of Record

In REO, every profit margin passes through the courthouse door You can underwrite perfectly, rehab efficiently, and market beautifully but if title isn’t clean, value isn’t real.

The next wave of distressed inventory will not be won by those who move fastest, but by those who close cleanest. Behind every recorded deed lies the true test of professionalism: precision, patience, and an unyielding respect for the chain of title

The Risk Premium: How Climate and Insurance Costs Are Repricing REOs

When risk maps shift faster than markets, investors must learn to price exposure as carefully as opportunity.

The New Variable in Valuation

For decades, the REO equation was straightforward: acquisition price, repair cost, market comp, resale value But in 2025, a new variable has permanently entered the model climate exposure. From wildfire-prone California corridors to floodthreatened Gulf states and hurricane-vulnerable coastal regions, insurance volatility has become one of the most disruptive forces in real estate pricing.

In several major markets, the cost or unavailability of property insurance has turned once-stable assets into unpredictable liabilities. For distressedproperty investors, these shifts can mean the difference between a profitable turnaround and an unrecoverable loss

The question for 2026 isn’t just What’s it worth? but What will it cost to keep it insured?

Insurance Withdrawal and Market Distortion

Over the past two years, more than a dozen national insurers have either reduced coverage or exited entire states. California, Florida, and Louisiana top the list, but ripple effects are spreading inland as reinsurance costs surge globally.

This retrenchment is forcing lenders to adjust lossreserve models When a property cannot be insured or can only be insured at punitive rates its resale potential and loan recoverability plummet For REO portfolios, this creates uneven valuation layers: two identical houses on the same block may carry vastly different risk premiums based on elevation, firescore, or FEMA flood-zone data

How Risk Is Quantified in Modern REO Valuation

Servicers and BPO analysts increasingly include climate-risk overlays in asset scoring models. These overlays combine data from FEMA flood maps, NOAA fire-risk analytics, and private actuarial firms such as CoreLogic and Verisk. Each property is assigned a Hazard Impact Score (HIS) that directly influences lender disposition timelines and reserve requirements

A property with a high HIS may face:

Longer marketing and escrow periods

Reduced loan-to-value (LTV) ceilings for buyers

Higher insurance deductibles or limited perils coverage

Elevated cap-rate expectations from investors

Understanding these scoring models allows REO professionals to anticipate lender flexibility. A property with an HIS above the servicer’s acceptable threshold is often discounted aggressively simply to exit the balance sheet.

Investor Strategy: Turning Risk into Leverage

Climate risk doesn’t eliminate opportunity it reframes it. Savvy investors now specialize in risk-adjusted acquisitions: purchasing high-exposure assets at steep discounts, implementing mitigation upgrades, and re-marketing with documented resilience improvements.

For instance, properties in fire-zone areas can regain value through defensible-space certification, fire-resistant roofing, and updated electrical panels. Flood-risk homes can be elevated, fitted with sump systems, or converted to rental inventory with higher yield expectations.

These enhancements do more than protect physical structures they restore insurability. Investors who can present verifiable risk-reduction documentation often secure lower premiums and faster resale cycles. In effect, they arbitrage between fear and fact.

Lender and Servicer Adaptation

Lenders are also adapting, building climate-resilient lending frameworks into REO management. Some institutions are partnering with parametric-insurance providers firms that pay out automatically based on environmental triggers like rainfall or windspeed to limit portfolio exposure. Others are developing geo-diversification mandates, ensuring that no more than a fixed percentage of their REO inventory sits within designated highrisk zones.

For agents and brokers, this evolution means tighter listing scrutiny Expect servicers to request detailed environmental disclosures and insurance verification prior to marketing approval. Those equipped to deliver accurate data rather than anecdotal reassurance will rise to the top of the preferred vendor lists.

The Future of Pricing Risk

1. Include Insurance Cost in Every ProForma. Replace flat expense estimates with verified premium quotes or regional averages.

2. Access Public and Private Risk Maps. Combine FEMA, NOAA, and state-specific fire-hazard data for full exposure analysis

3 Partner with Specialty Insurers. Surplus-lines carriers and mutual associations often fill gaps mainstream insurers abandon.

4 Document Mitigation Measures. Photographic and permit evidence of upgrades can materially influence valuation.

5 Advise Clients Honestly. Transparency about risk builds long-term trust even when deals don’t close

Climate pressure and insurance volatility are not temporary distortions they are structural. The REO sector now operates at the intersection of finance, environmental science, and public policy.

The professionals who thrive will be those who treat risk not as a deterrent but as a dimension of valuation to be quantified, managed, and monetized. Every flood zone, every fire corridor, every wind map tells a story and inside those stories lie tomorrow’s opportunities for informed, disciplined buyers.

The real question isn’t how much risk costs it’s how much value understanding risk can create.

Every real estate professional sees the finished product the bank-owned property listed for sale but few understand the complex timing decisions that bring it there. Between the first missed payment and a property’s formal REO status lies a labyrinth of servicer discretion, investor oversight, and financial calculus.

The decision to convert a foreclosure into an REO isn’t merely procedural; it’s economic strategy. Lenders weigh dozens of factors asset value, carrying costs, insurance exposure, and market velocity before pulling the trigger. In a market like late 2025, where rates remain high and liquidity uneven, those decisions can swing entire regional inventory cycles.

Why Some Properties Stall—and Others Accelerate

Contrary to public perception, foreclosures don’t move on fixed timelines. Most servicers maintain conversion models that calculate the optimal moment for repossession If market conditions suggest recovery rising comps, lower inventory, or new investor appetite a servicer may delay REO transfer to preserve value.

Conversely, if local prices stagnate or repair costs climb, lenders often fast-track foreclosure completion to lock in recoverable value before further decline. This is particularly true in non-judicial states like California and Arizona, where foreclosure timelines are shorter and liquidation flexibility is higher.

By contrast, judicial states (Florida, Illinois, New York) involve court proceedings that stretch for months or years, forcing banks to carry properties longer often vacant, depreciating, and uninsured.

The Financial Equation: Cost vs. Carry

Every day a foreclosed property remains unresolved, the lender bears costs: taxes, maintenance, insurance, and lost interest income

The moment those carrying costs exceed projected recovery value, conversion becomes inevitable

This inflection point known internally as the loss-minimization threshold is where lenders decide whether to hold, sell, or walk away entirely. For large banks, this threshold is determined by national portfolio analytics; for smaller institutions, it’s often a case-by-case judgment.

Investors who learn to approximate these calculations gain a powerful edge Knowing when a lender’s holding cost becomes unsustainable lets you time bids and acquisitions with precision.

Seasonal and Regulatory Timing

Late-year REO conversions are not coincidence they are compliance events. Federal reporting standards under the FDIC and OCC require banks to reconcile nonperforming assets by fiscal close As a result, foreclosure completions often surge in November and December.

Moreover, loan servicers under GSE or HUD contracts operate on performance scorecards tied to resolution velocity. Delays can reduce servicer compensation, incentivizing faster REO transfers near quarterend.

For brokers and investors, understanding these institutional pressures turns the calendar itself into a forecasting tool When regulators push, inventory moves and those watching closely can catch the first wave.

Reading the Pipeline Before It Hits the Market

Professionals who track trustee sale results, county auction data, and recorded assignments can predict REO conversions weeks before they surface publicly Watch for clusters of canceled auctions often the prelude to bank repossession or sudden increases in lender-filed deeds.

Platforms that aggregate Fannie Mae, Freddie Mac, and HUD pre-REO data can help identify “pending transfers,” allowing agents to prepare BPOs, investors to arrange financing, and managers to plan marketing strategies before assets are formally released

Strategic Takeaways

1. Understand Servicer Behavior. Each lender has unique liquidation policies based on portfolio goals, not market rumor.

2. Anticipate Conversion Seasons. Q4 and Q1 are peak transfer windows; plan capital allocation accordingly.

3. Track Carry Costs. When property taxes or insurance rates spike, expect faster liquidation decisions.

4. Leverage Pre-Foreclosure Data. County filings and trustee records often reveal which properties are nearing REO conversion.

5 Time Negotiations to Pressure Points. End-of-quarter and year-end deadlines create flexibility in lender pricing.

Conclusion: Timing Is the Real Asset

In the REO world, knowledge of timing is more valuable than cash on hand Understanding when a lender must act allows investors and brokers to be present where opportunity emerges. The property may be physical, but the advantage is intellectual gained by reading the hidden clock behind every conversion.

As 2026 approaches, that clock is ticking louder

By the Editorial Team

Most Homeowners Wish They’d Sold Sooner

79% of homeowners

surveyed

say they wish they’d sold sooner.

79% of homeowners surveyed regret waiting to sell.

If you’ve been holding off, take this as your sign.

Don’t let “I wish I sold sooner” become part of your story.

Hidden Markets: Finding Off-Market and UnderMarket REO Opportunities

Why the best distressed-property deals never reach the MLS and how professionals can uncover them before everyone else.

The Invisible Pipeline

Every experienced REO investor knows that by the time a property appears on the MLS, the real money has already moved. Off-market and under-market opportunities those buried in lender portfolios, pending loss-mitigation files, or servicer shadow inventories constitute the true early market of distressed real estate.

These properties exist in limbo: neither fully liquidated nor publicly listed Some are post-foreclosure assets awaiting title clearance; others are loans flagged for default but not yet referred to foreclosure counsel For investors, brokers, and asset managers who know where to look, this liminal space offers unmatched pricing leverage and speed.

The Gatekeepers: Servicers, Asset Managers & Special Advisors

The key to under-market access lies in relationships, not listings. Servicers rely on networks of trusted brokers and investors to quietly evaluate and acquire assets before the expense of public marketing Establishing rapport with REO asset managers, government-contract vendors, and private-equity disposition teams can yield steady deal flow.

HUD contractors, GSE field managers, and bankowned portfolio specialists often issue internal “premarketing” lists to vetted professionals for quick offers. Being on those lists requires credibility accurate BPOs, fast closings, and consistent communication. In an age of automation, human trust remains the rarest currency in real estate.

Data as a Compass

Technology has made it easier to map distress before it becomes visible. County recorder databases, default notices, and assignment filings reveal where delinquent loans cluster months before REOs hit the market.

Third-party tools that aggregate Notice of Default (NOD), Lis Pendens, and trustee sale data enable predictive acquisition models. By cross-referencing these with census and demographic datasets, investors can estimate not only where foreclosures will occur, but which neighborhoods are poised for rebound after liquidation.

This approach transforms off-market hunting from speculation into data-driven prospecting the digital equivalent of surveying gold veins before the rush begins.

Institutional Channels and Bulk Sales

Large-scale opportunities often emerge through bulk-note and REO package sales. Regional banks, credit unions, and hedge funds periodically offload pools of nonperforming loans or partially processed REOs to institutional buyers.

While these deals typically require higher capital thresholds, they can also produce double-digit returns when assets are repositioned or resold individually. Partnering with private lenders, forming acquisition syndicates, or working under a master broker agreement can give mid-tier investors entry into these institutional spaces.

The secret is preparation: have verified funding lines, entity documents, and management infrastructure ready before the call for bids. When the window opens, hesitation costs more than capital.

The Legal and Ethical Balance

Off-market access comes with responsibility. Transparency, compliance, and fairdealing standards still apply even when deals move outside the MLS Confidentiality clauses, non-circumvention agreements, and conflict-of-interest disclosures are standard practice when dealing directly with banks or government contractors.

Maintaining documentation integrity is not just a legal safeguard it’s a reputation strategy. In a field built on repeat relationships, credibility sustains opportunity far longer than luck

Tactical Approaches for 2026

1. Leverage Public Data Proactively. Build a quarterly default-map dashboard to monitor NOD filings, eviction notices, and probate transfers.

2. Join the Pre-Marketing Circles. Apply for inclusion on HUD M&M contractor lists, GSE vendor panels, and major servicer rosters

3. Cultivate Private-Equity Contacts. Many hedge funds quietly sell residual assets to trusted small investors after bulk disposition rounds.

4 Invest in Local Reputation. Bank officers and title reps often tip reliable professionals about forthcoming liquidations.

5. Automate Follow-Ups. Use CRM triggers to re-engage leads every 30 days distressed deals often reappear when financing collapses

Seeing Before Selling

Under-market REO strategy is about anticipation, not reaction The professionals who dominate 2026 will not wait for listings; they will forecast them. By combining relational capital, public-record intelligence, and disciplined timing, investors can position themselves one step ahead of both the market and their competitors

In a field where margins are thin and timing is everything, the next wave of success will belong to those who see the property before it’s for sale.

By the Editorial Team

The Real Estate Magazine | REOBroker.com Finding opportunity where others see opacity.

The Exit Equation: Mastering Deeds, Short

Sales & Strategic Foreclosures

How lenders, servicers, and investors are redefining title conveyance strategies in the new REO era.

The Anatomy of an Exit

In distressed real estate, the real story isn’t just acquisition it’s exit discipline Whether a property transitions through a deed in lieu, a short sale, or a strategic foreclosure, the path to REO status defines profitability, legal exposure, and market timing.

As 2025 draws to a close, lenders are reevaluating how to manage these exits amid higher interest rates, slower buyer demand, and growing title complexity. Each option deed in lieu, short sale, or foreclosure represents a unique balance between speed, cost, and control. The professionals who understand those levers will own the next phase of opportunity.

Deed in Lieu: The Quiet Handshake

A deed in lieu of foreclosure remains the most discreet and cost-efficient solution for both parties. Borrowers voluntarily transfer title to the lender, avoiding a full judicial foreclosure and limiting credit damage. Lenders benefit by eliminating court costs, property deterioration, and reputational risk.

However, these agreements are not without pitfalls Unreleased junior liens can complicate title insurance, and lenders must ensure clear consent from all vested owners. Proper documentation including satisfaction letters and release forms is essential to prevent downstream disputes

For investors, deed-in-lieu opportunities often enter REO inventory in cleaner condition and with shorter holding periods making them the “quiet gold” of distressed pipelines.

Short Sales: The Managed Release

Short sales are the art of compromise The lender agrees to accept less than the total owed, recognizing that a discounted payoff beats prolonged default. The borrower avoids formal foreclosure; the lender reduces losses and clears the asset faster.

In today’s climate of high interest rates and stalled equity growth, short sales are resurging particularly in FHA and VA portfolios where homeowners bought at 2021–2022 peak values.

The key for brokers and investors lies in timeline management. Servicer approvals, valuation reviews, and investor sign-offs can drag transactions for months Success depends on precision: clean BPOs, transparent offers, and proactive communication. Professionals who master these processes can convert short sales into swift pipeline inventory before competitors even notice the trend.

Strategic Foreclosure: The Calculated Reset

Not every property warrants rescue For lenders, strategic foreclosure is a costbenefit decision one rooted in mathematics rather than emotion. When carrying costs exceed recovery potential, liquidation becomes the logical path.

High insurance premiums, vandalism risk, or regulatory delays can all shift the equation. In these cases, lenders calculate “strike prices” (the walkaway thresholds where losses stop worsening) and move decisively to REO

For agents and investors, understanding this logic transforms negotiation. The question isn’t “Will the bank take less?” it’s “Where does the loss curve flatten?” Those who can identify a servicer’s break-even point speak the bank’s language and win the deal.

Legal and Operational Considerations

Each conveyance path carries distinct legal and tax implications. Deeds in lieu require due diligence on subordinate liens. Short sales may involve debt forgiveness reporting under IRS Form 1099-C. Strategic foreclosures demand compliance with both state-specific timelines and federal servicing regulations

Operationally, the best outcomes come from early intervention engaging with borrowers and servicers before litigation or abandonment. Proactive communication reduces costs, preserves asset value, and accelerates transition to REO resale.

The Strategic Takeaway

1.Know Every Exit Option. Each pathway deed, short sale, foreclosure offers a different balance of risk and reward.

2. Time Equals Margin. Early identification of distressed assets lets you guide the exit instead of reacting to it

3. Data Is Negotiation Power. Servicers respect professionals who frame offers around financial logic, not emotion.

4. Clean Title Is Non-Negotiable. Every deal’s true value begins and ends with insurable ownership

Conclusion: The New Efficiency Game

In the tightening REO environment of late 2025, exit strategy is everything.

The most profitable investors and brokers aren’t waiting for properties to hit auction they’re embedded in the process, helping servicers structure exits that make financial sense. The market will reward not just those who buy, but those who understand how properties become REO. In that understanding lies the true edge.

By the Editorial Team

Where every transaction begins with strategy

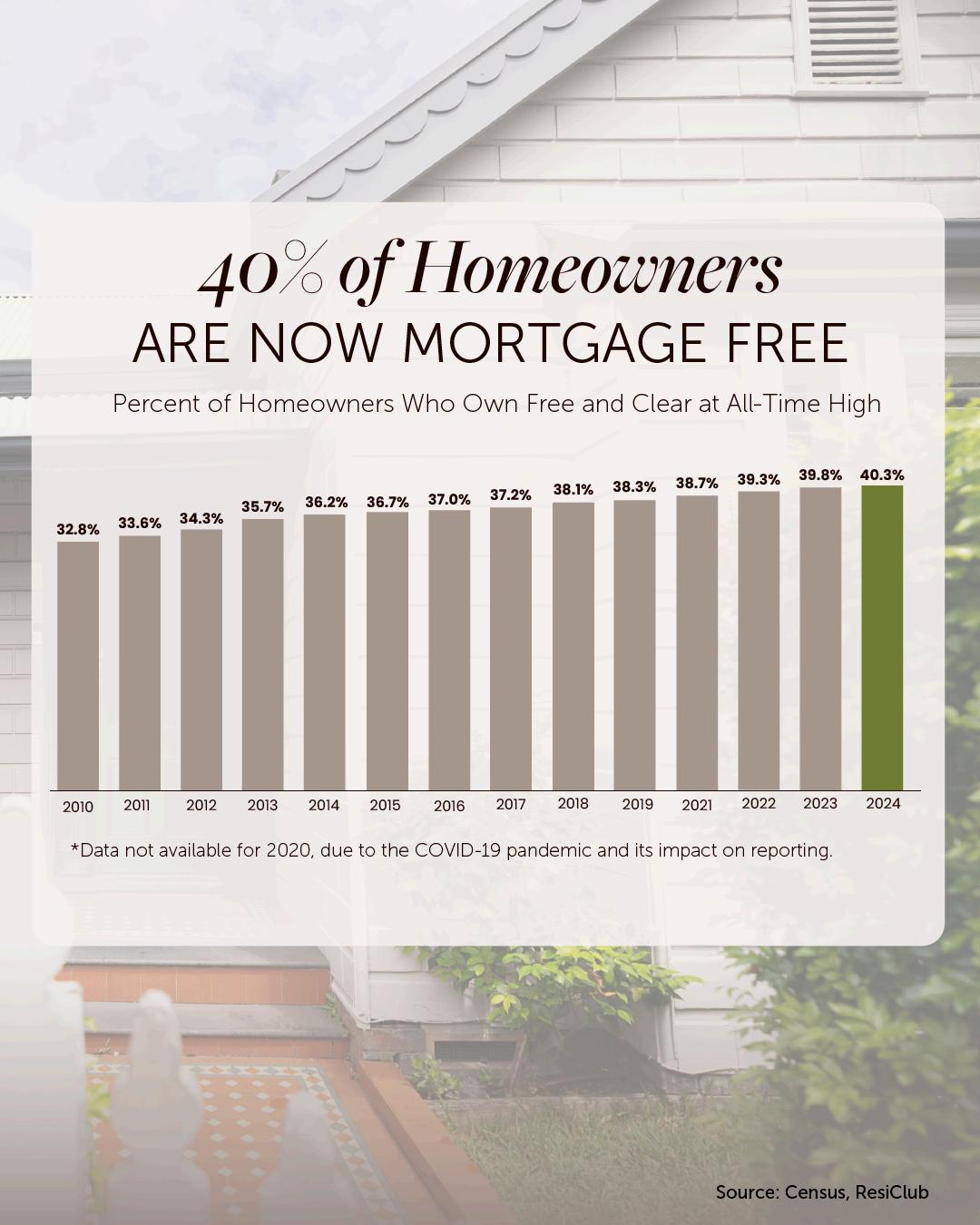

Did you know? A record 40% of U.S. homeowners now own their homes free and clear. That’s the highest share ever recorded.

And that’s an important stat if you’re considering downsizing.

Think about it. If you’ve been in your house for a long time, you may be able to sell and buy your next home in cash

You could get a smaller, less expensive home that better fits your lifestyle today with lower bills, less upkeep, and no new mortgage in retirement.

Want to find out if this could be a possibility for you too? Contact me

The Delinquency Curve: Reading the Early Warnings of 2026

Why rising consumer debt, lagging income growth, and credit tightening could quietly trigger the next REO surge.

The Calm Before the Correction

Markets rarely announce turning points they whisper them through data. Over the past six months, national delinquency indicators have begun to rise, not sharply enough to alarm the public, but consistently enough to alert seasoned observers Credit card and auto delinquencies have reached three-year highs, and mortgage delinquencies especially in FHA and VA portfolios are edging upward after years of record lows.

For investors and REO professionals, this slow build carries profound implications. It suggests that while the surface of the housing market still appears stable, the pressure beneath is building Household debt has grown faster than wage gains for nine consecutive quarters, and refinancing options remain limited by higher interest rates The foundation of borrower resilience is beginning to thin.

In short, the numbers are telling us what the headlines are not: the distressed pipeline for 2026 is forming right now.

Recent data from the Federal Reserve Bank of New York’s Household Debt and Credit Report reveals that U S household debt now exceeds $17.6 trillion, with mortgage balances accounting for nearly three-quarters of that total. While overall delinquency remains below crisis levels, the rate of growth in 30- to 59-day late payments is accelerating especially in the sub-$400,000 loan category.

FHA loans, which serve first-time buyers and lower-income households, have seen delinquencies climb from 3.9% to 5.1% over the past year. VA loans have inched up as well, signaling that even government-backed borrowers are feeling the strain of inflation and wage stagnation.

Historically, these modest upticks serve as early indicators. In prior cycles (2006–2008, 2018–2019), a similar pattern preceded full REO surges by 12–18 months. The first stage of stress always appears at the margins missed payments, partial remittances, small-balance defaults before progressing toward broader asset liquidation

Structural Pressures: Why 2025 Is Different

Unlike prior cycles triggered by speculative lending, today’s pressure stems from affordability compression High rates have locked millions of owners into older mortgages, reducing mobility and supply. Simultaneously, consumer credit utilization has reached record highs as households use cards to offset cost-of-living increases.

This double bind frozen housing equity and rising revolving debt creates a fragile equilibrium. Any macro-shock, from job losses to regional disasters, can push borrowers past the tipping point Meanwhile, servicers are reporting higher lossmitigation inquiries and a rise in “silent defaults,” where borrowers stop communicating before formal delinquency.

The implication for REO professionals is straightforward: inventory expansion is inevitable, though uneven Markets with heavy FHA and VA concentration Texas, Georgia, Florida, and the Midwest corridor will likely see the earliest shifts in 2026

The Coming Wave of Strategic Defaults

As affordability tightens, strategic defaults may return, especially among investors who purchased at peak prices with variable or short-term financing Rising insurance costs in climate-sensitive zones further increase exit pressure.

When property values stagnate while carrying costs rise, investors often cut losses pre-emptively.

Lenders, facing these tactical walkaways, must decide modification, short sale, or REO conversion. Each option distressed ecosystem differently, but together they point towa truth: the next REO cycle will be data-driven, not panic-dr unfold quietly, through thousands of micro-decisions rather th collapse.

Professionals who track these behavioral indicators now de growth, credit tightening, insurer withdrawals will know whe map is heading before it’s drawn.

Positioning for the 2026 Market

1. Follow the Credit, Not the Headlines. Early-stage delinquency data is more predictive than foreclo Monitor 30-day late trends by loan type and region.

2. Map Vulnerability Clusters.

Combine HUD, CFPB, and Fed regional data to identify countie debt-to-income ratios and low liquidity buffers.

3. Reassess Valuation Models. Anticipate softening prices in markets with heavy investor ow elevated insurance exposure.

4. Strengthen Capital Flexibility.

Prepare acquisition financing or private lending relationships a 2026 inventory swell.

5. Engage Servicers Early.

Build relationships with asset managers before assets go publ deals emerge from early-access pipelines.

A Market That Rewards Prepared Minds

The next REO cycle may not mirror 2008’s drama but it will same discipline: data literacy, liquidity, and timing. Rising delinq not a crisis yet; they are a signal of opportunity for those w foresight.

In 2026, the winners will not be those who chase headlines, but learned to read the curve before it turned.

By the Editorial Team

The Real Estate Magazine | REOBroker.com Translating hazard into strategy.

If your home isn’t attracting the kind of offers you want -or any offers at allit may be time to reconsider your asking price.

If your house isn’t selling, it may be your price

The #1 reason homes aren't bringing in offers today is because they’re priced too high for the current market, and that’s turning off buyers.

But here’s the good news: you probably don’t need a big price cut to get results.

Data shows the typical price reduction right now is only about 4%. And that small shift in your pricing strategy can make a real difference

If you’re ready for something to change, you have to be willing to make a change

Ask your agent how much they recommend based on what’s selling in your neighborhood right now.

The Winter Turn: How Seasonal Cycles Reset the REO Market

Understanding why the final quarter of every year quietly defines the next phase of the distressed housing cycle.

The Myth of the Slow Season

In traditional residential real estate, the year-end period is synonymous with slowdown fewer listings, reduced buyer activity, and an overall cooling of the market. But for professionals in the REO and distressed-asset sector, the final quarter tells a very different story.

While many agents are winding down, servicers, lenders, and investors are accelerating. Internal performance metrics, accounting deadlines, and portfolio adjustments drive a flurry of year-end decisions that directly shape inventory levels for the next twelve months.

Historically, HUD and GSE data show an 8–15% spike in REO filings and asset transfers between October and December. This surge is not an accident; it’s a result of fiscal cycles, loan-loss provisioning, and balance sheet optimization. The fourth quarter is when lenders clear aging foreclosures, finalize write-offs, and prepare for regulatory audits.

For investors and brokers who understand this rhythm, the socalled “quiet season” becomes a time of competitive advantage a brief but potent window for strategic acquisitions.

Why Lenders Move Faster at Year-End

Banks and mortgage servicers operate under strict capital adequacy and accounting frameworks By Q4, they must reconcile nonperforming loans (NPLs) to meet reporting requirements. These mandates create financial pressure to liquidate foreclosed inventory or finalize pending asset transfers before the calendar resets

This pressure means REO pipelines move faster and negotiability increases Servicers are more likely to entertain discounted bids, approve “as-is” sales, or accelerate contract timelines. For investors holding liquidity and for agents ready to move, November and December can deliver opportunities that would be unthinkable in spring

Conversely, buyers relying on traditional financing may find themselves disadvantaged during this period. High-rate environments and tightened underwriting standards mean that cash remains king, particularly when banks prioritize speed over margin.

Why Lenders Move Faster at Year-End

Banks and mortgage servicers operate under strict capital adequacy and accounting frameworks. By Q4, they must reconcile nonperforming loans (NPLs) to meet reporting requirements These mandates create financial pressure to liquidate foreclosed inventory or finalize pending asset transfers before the calendar resets.

This pressure means REO pipelines move faster and negotiability increases. Servicers are more likely to entertain discounted bids, approve “as-is” sales, or accelerate contract timelines For investors holding liquidity and for agents ready to move, November and December can deliver opportunities that would be unthinkable in spring.

Conversely, buyers relying on traditional financing may find themselves disadvantaged during this period High-rate environments and tightened underwriting standards mean that cash remains king, particularly when banks prioritize speed over margin.

Investor Psychology and the Seasonal Pivot

Year-end activity isn’t only driven by lenders it’s also influenced by investor psychology.

Sophisticated investors use this period to rebalance portfolios, offload underperforming assets, and position cash reserves for Q1 opportunities Flippers who acquired properties earlier in the year may rush to close or list before December 31 to optimize tax outcomes. Institutional investors often recalibrate holdings, shifting between single-family rentals (SFRs), multifamily acquisitions, or secondary-market note purchases.

This collective activity generates temporary imbalances: motivated sellers, flexible lenders, and limited competition. In essence, the market becomes inefficient and inefficiency is where profit lives

For those in brokerage, this period also marks the ideal time to reconnect with asset managers, revalidate BPO certifications, and review vendor lists before new contracts renew. Q4 is when preparation turns into positioning.

Regional Variations: Where Seasonality Hits Hardest

Not all markets follow the same script. In cold-weather regions, such as the Midwest and Northeast, REO sales tend to dip in volume but increase in discount percentage, as fewer retail buyers brave the winter slowdown. In contrast, Sun Belt states particularly Florida, Arizona, and Texas see robust late-year activity driven by investor migration and year-round construction cycles

Distressed assets in high-climate-risk areas (fire, flood, hurricane) also tend to be released late in the year, when insurers and servicers update risk maps and price adjustments. These listings may carry additional opportunity for buyers willing to navigate higher insurance premiums or mitigation requirements.

By studying seasonal heat maps of REO filings, investors can identify regional momentum shifts that will set the tone for Q1 and Q2 of the following year.

Strategic Takeaways for REO Professionals

1 Watch the Servicers, Not the Seasons - Traditional market rhythms don’t apply to REO. Understand your servicers’ reporting cycles and year-end performance goals.

2 Keep Capital Liquid - Deals in November and December often move quickly, and lenders prefer buyers who can close without extended financing contingencies.

3.Negotiate from the Data. - Use delinquency reports and trustee sale statistics to back your offers with credible metrics. Servicers respect data-backed bids over speculative offers.

4.Rebuild Relationships. - Q4 is when next year’s REO assignments are awarded. Stay visible to asset managers, HUD contractors, and local bank contacts.

5.Prepare for Early 2026 Shifts. - The REO inventory you see today reflects foreclosures that began six to twelve months ago. The real story for 2026 will be determined by what enters default now.

nancy@showcaserealty.net showcaserealty net

With over 30 years of experience, Nancy has built a powerhouse brokerage ranked in the RealTrends Top 1% of America’s Best Real Estate Agents, as featured in The Wall Street Journal.

A trailblazer, award-winning leader, and fierce client advocate, Nancy is celebrated for her unmatched negotiating skills, dedication to community, and her bold service guarantee: “Your home sold in 60 days, or we’ll pay you $2,500.”

She is more than a broker she’s a visionary, a philanthropist, and one of Charlotte’s Most Influential Women, as recognized by the Mecklenburg Times Nancy’s story is one of excellence, resilience, and leadership in REO and beyond

Stephanie D. See is the President and Co-Owner of Results Real Estate, Inc., a boutique brokerage in Largo, Florida With over 20 years of experience and a broker’s license since 2013, she and her husband, John B See, have closed more than 5,000 transactions across the Tampa Bay area Stephanie is known for her integrity, attention to detail, and expertise in residential and REO markets.

A dedicated industry leader, Stephanie has served on the Board of Directors for the National Association of Default Professionals (NADP) for eight years She is committed to raising professional standards through education, mentorship, and collaboration. Under her leadership, Results Real Estate continues to deliver client-focused service in a wide range of market conditions

Fran Altman is an Associate Broker with Coldwell Banker Realty, proudly serving the St Cloud, Minnesota area and surrounding communities A true Minnesotan through and through, Fran was born and raised in central Minnesota and loves helping others find their place here

She graduated from Apollo High School in St. Cloud before earning her Bachelor of Arts in Organizational Management with a minor in Communications from Concordia College in St Paul

Dynamic and results-driven Real Estate Broker with extensive experience as an Area Vice President at Vylla Home, spearheading growth and delivering on the company's mission Adept at empowering agents and transforming the real estate process Specializing in institutional asset sales, risk mitigation, talent acquisition/retention, and marketing, with a strong background in leadership and growth-oriented roles within both for-profit and non-profit corporations.