DIGITAL EDITOR Kaitlin Secord ksecord@ensembleiq.com

ADVERTISING SALES & BUSINESS

NATIONAL ACCOUNT MANAGER Karishma Rajani (437) 225-1385 - krajani@ensembleiq.com

NATIONAL ACCOUNT MANAGER Julia Sokolova (647) 407-8236 - jsokolova@ensembleiq.com

NATIONAL ACCOUNT MANAGER Roberta Thomson (416) 843-5534 - rthomson@ensembleiq.com

NATIONAL ACCOUNT MANAGER Angela Jones ajones@ensembleiq.com

DESIGN/PRODUCTION/MARKETING

CREATIVE DIRECTOR Nancy Peterman npeterman@ensembleiq.com

ART DIRECTOR Jackie Shipley jshipley@ensembleiq.com

SENIOR PRODUCTION DIRECTOR Michael Kimpton mkimpton@ensembleiq.com

MARKETING MANAGER Jakob Wodnicki jwodnicki@ensembleiq.com

EDITORIAL ADVISORY BOARD

RAY HEPWORTH , METRO BRENDA KIRK , PATTISON FOOD GROUP CHRISTY MCMULLEN , SUMMERHILL MARKET GIANCARLO TRIMARCHI VINCE’S MARKET

SUBSCRIPTION SERVICES

Subscriptions: $102.00 per year, 2 year $163.20, Outside Canada $163.20 per year, 2 year $259.20 Single Copy $14.40, Groups $73.20, Outside Canada Single Copy $19.20.

Digital Subscriptions: $60.00 per year, 2 year $95.00

Category Captain: Single Copy $20.00, Outside Canada Single Copy $30.00

Fresh Report: Single Copy $20.00, Outside Canada Single Copy $30.00

Phone: 1-877-687-7321 between 9 a.m. to 5 p.m. EST weekdays Fax: 1-888-520-3608 Online: canadiangrocer.com/subscription-centre

CORPORATE OFFICERS

CHIEF EXECUTIVE OFFICER Jennifer Litterick

CHIEF FINANCIAL OFFICER Jane Volland

CHIEF OPERATING OFFICER Derek Estey

CHIEF PEOPLE OFFICER Ann Jadown

MAIL PREFERENCES: From time to time other organizations may ask Canadian Grocer if they may send information about a product or service to some Canadian Grocer subscribers, by mail or email. If you do not wish to receive these messages, contact us in any of the ways listed above.

PM 42940023 Canadian Grocer is Published by Stagnito Partners Canada Inc., 2300 Yonge Street, Suite 2900, Toronto, ON M4P 1E4. Printed in Canada

MARKING A MILESTONE

Canadian Gro C er is turning the ripe old age of 140 this year (our cover may have given you a hint!). It’s a remarkable anniversary and one that few companies, let alone magazines, can claim.

Since our first issue rolled off the press in 1886, we’ve had the privilege of documenting the evolution of this dynamic industry. We’ve reported on the mundane—the price of baking powder in 1889 (10 cents a tin)—and the momentous—the rise of supermarket chains and the acceleration of artificial intelligence. We’ve covered periods of rapid growth alongside periods of profound challenge and disruption.

For this issue, we’ve dug deep in our extensive archive to bring you “Grocery at a glance,” (page 16) a visual snapshot of some of the pivotal moments that have shaped the industry we know today.

We’re also shining a light on some standout companies that have made an impact on the Canadian grocery industry over the years. In this issue, we feature Chapman’s Ice Cream, a homegrown success story that for more than half a century has been churning out innovation and making a positive impact while doing so. (Read the story on page 19.)

There’s more to come. In upcoming issues we’ll take a closer look at influential grocery leaders of the past, trailblazing women, the evolution of technology, store design and more. We also want to hear from you. We’ve launched a photo contest and are inviting you to dig into your archives and share photos that help tell your company’s grocery story (details on page 9). We’ll feature the most

compelling submissions in an upcoming issue and on canadiangrocer.com.

We’re proud of our history and excited to continue to bring you stories from the next era of grocery. An era that will surely be shaped by rapid, sweeping technological change, an ever-changing consumer and a new generation of leaders who will move the industry forward.

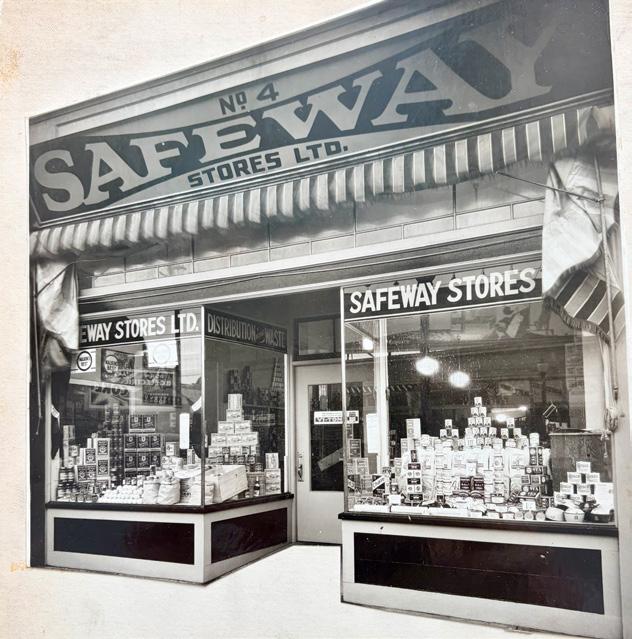

Canadian Grocer’s archive is full of photos, like the one above of Dominion Stores, which provide a fascinating glimpse into the evolution of the grocery shopping experience

The Buzz

Foodland opens in Niagara-on-the-Lake, Ont. with a locally focused, full-service grocery offering

Following a year of construction, FOODLAND, an Empire-owned banner, opened its doors at The Village Centre in Niagaraon-the-Lake, Ont., bringing a full-service grocery experience to the area. Rooted in local, the new store features local murals on its walls, a robust offering of local products as well as local ownership.

WALMART CANADA is expanding its Supercentre footprint with two new approximately 140,000-sq.-ft. stores planned for Ontario and Alberta. The London, Ont. Supercentre is set to open in 2028, serving as an anchor tenant for an expanding commercial development at the intersection of Wonderland Road South and Wharncliffe Road South. A second location is slated for a 2027 opening in Edmonton’s Desrochers Villages on Heritage Valley Trail SW. Both Supercentres will feature full grocery, bakery and deli departments, and general merchandise.

Loblaw’s discount banner MAXI celebrated a milestone with the opening of its 200th store in Huntingdon, Que. The more than 22,000-sq.-ft. location was backed by a

The

Walmart Canada has two new approximately 140,000-sq.-ft. Supercentre stores in the works for Ontario and Alberta

multimillion-dollar investment and has created 60 new local jobs. Meanwhile, in Edmundston, N.B., this summer, Loblaw is converting an Atlantic Superstore to the Maxi banner.

Vancouver’s Kitsilano neighbourhood is home to a new FRESH ST. MARKET—the grocer’s ninth location in the province. The store features locally sourced foods such as beef, poultry, charcuterie meats and cheeses, in addition to a variety of readyto-eat options including the grocer’s largest hot bar, sushi bar and burrito bar.

HEALTHY PLANET opened a 14,000-sq.-ft. store in Etobicoke, Ont., featuring a curated selection of organic produce, organic and natural groceries, vitamins, supplements, sports nutrition products and natural beauty essentials.

Costco opens a 137,000-sq.-ft.

Business Centre in Markham, Ont., targeting grocery, offices, restaurants and convenience

ough of Montreal has a new look. After an extensive renovation, the store now offers a significant assortment of local and international products, and a range of high-quality, ready-to-eat meals.

COSTCO WHOLESALE CANADA converted its Newmarket, Ont. warehouse—which has since relocated down the street—into a 137,000-sq.-ft. Business Centre, marking the opening of its 10th Business Centre in Canada. It offers more than 3,000 high-quality items targeted at restaurants, convenience/grocery stores and offices, including bulk food items, commercial kitchen wares, cleaning supplies, office furniture, coffee needs and more.

Loblaw’s PROVIGO store on Rachel Street in the Rosemont-La Petite-Patrie bor -

Fresh St. Market opens in Vancouver’s

Healthy Planet’s new Etobicoke, Ont. store is 14,000 square feet and carries organic and natural groceries, vitamins and more

BOLD FLAVOUR MEETS MAYO

Functional beverage brand Cove Soda has put a senior leadership team in place that it says will guide its expansion across North America. Bryan Crowley has been tapped as chief executive officer, Craig Olkiewicz as chief commercial officer and Joe Lee as chief operating officer.

Advantage Group International (AGI) has appointed Matt Nitzberg as chief client officer to lead global client services, sales, marketing and commercial activities. He will continue to serve as head of North America. Nitzberg’s background includes senior leadership roles at leading analytics and insight firms such as Dunnhumby and Circana.

Mars Petcare has a new global president. Marc Carena—who joined Mars in 2022 as regional president Mars snacking Europe, central Eurasia and international travel retail—has been tapped to lead the business, which includes such brands as Pedigree, Royal Canin and Whiskas. Prior to joining Mars, Carena was a managing director for McDonald’s in Russia.

Keurig Dr Pepper Canada has appointed Audrey Nault-Cloutier to senior director, human resources. Nault-Cloutier joined the company in 2015 and has since progressed through a series of senior leadership roles. Before joining Keurig Dr Pepper Canada, she held senior human resources roles at Bombardier, Cirque du Soleil and Publicis.

UNFI Canada has promoted Sylvain Chopra from senior sales manager for the organization’s national independent business to regional sales director. He succeeds Deborah Viti, who has transitioned to lead UNFI’s mass and national retailers. In his new role, Chopra will oversee Whole Foods Market and lead UNFI’s independent customer strategy across Eastern Canada.

AWARDS/RECOGNITION

In recognition of their contributions to the food industry, the Canadian Federation of Independent Grocers (CFIG) is recognizing Jamie Nelson (Pattison Food Group), Doug Lovsin (Freson Bros.) and Linda and Brooke Kynoch (Scotch Creek Market and Safety Mart Foods, B.C.) with 2026 Life Member designations during the Grocery & Specialty Food West exhibition and conference on April 21 in Vancouver.

Moments in time

This year, Canadian Grocer marks 140 years of covering the people, brands and moments that have shaped the country’s grocery industry—and we want to celebrate that history with our readers.

We’re inviting grocers and CPGs to dig into their archives and share historic photos: early stores, team photos, milestone moments and/or iconic products. Selected images will be featured as part of our 140th anniversary celebrations.

Let’s bring Canada’s grocery history to life! Send your submissions (maximum of three photos) as an email attachment to Canadian Grocer’s managing editor Kristin Laird (klaird@ensembleiq.com).

Include the photographer’s name and your company, the names and titles of any individuals featured in the image, and two to three sentences providing details about your submission.

*Only enter photos you own or have the express permission of the photographer to use.

Choices Market chief operating officer, Jon Janower, is retiring this spring after nearly 49 years in the grocery business. Janower began his career at age 10, working alongside his father at a grocery store in Prince George, B.C. By 18, he was managing his own store. He joined Choices Market in the late 1990s and helped with its expansion from two to 11 locations, and its integration into Pattison Food Group. He became chief operating officer in 2012.

Audrey NaultCloutier

Sylvain Chopra

Matt Nitzberg

Marc Carena

Bryan Crowley

Doug Lovsin Jamie Nelson Linda and Brooke Kynoch

People

FROM SOCCA TO SUCCESS

How two friends turned a French street food into Peacasa—a fast-growing snack brand

By Andrea Yu • Photography by Jaime Hogge

(L to R) Aaron Johnstone and Victor Delage

AARON JOHNSTONE AND VICTOR

Delage first met in 2015, when the two were studying business at the University of Ottawa. It wasn’t until the end of 2018, however, that a Mediterranean street food called socca would inspire the duo to start a food company.

While hiking through France—where Delage was working as a professional sailor—he introduced Johnstone to socca, a light flatbread Delage had grown up eating. “They make it from chickpea flour and olive oil,” Johnstone explains. “They make it in these big copper pans and cook them in wood-fired ovens on the streets. It’s super simple ingredients and it’s amazingly delicious.”

The two thought the high-protein snack would be a great product to sell in Canada. By the summer of 2019, Delage left his sailing career and moved back to Toronto and into the basement of the Johnstone family home in Markham, Ont. to give their business idea a shot. Johnstone followed, quitting his job as a retail analyst to go all-in on launching a chickpea chip business called Peacasa.

Their first step was to develop a recipe using Canadian-grown chickpeas. “It was trial and error,” Johnstone explains. “Every month, we’d get a bit better at the recipe and figure out what was working and what wasn’t.” They sold their chips at local farmers markets in Toronto, regularly selling out. However, Delage and Johnstone then faced the challenge of scaling up their homemade snack. “We were making around 40 bags in Aaron’s parents’ kitchen per eight-hour shift,” Delage says. “We had a lot of people at the markets asking us what stores they could buy them in, but we couldn’t make enough by hand to sell in grocery stores.”

The dilemma forced the duo to reassess their manufacturing process with an eye for commercialization, discovering a “secret” technique that would allow them to make their chips with machines. “We started getting into the food science behind it,” Johnstone explains. “We were learning what makes a chip crispy and the science of frying and moisture. We discovered this new process that no one was using, which allowed us to make chips with just chickpea flour and no filler.”

By early 2020, they began speaking with co-packers to manufacture their product. “Most of them just shut the door in our faces,” Delage recalls. “They weren’t willing to take on this new process or take a risk on a new product.” The entrepreneurs realized they’d have to

manufacture their chickpea chips themselves. Delage began sourcing equipment from Europe while Johnstone took the lead on financing and figuring out how to start their own factory. In 2021, they set up shop at The Grove—an agri-business manufacturing facility in London, Ont. COVID delayed a few key equipment shipments, so the pair came up with a workaround. “We bought this small tabletop unit, which we ‘MacGyvered’ to work on our line, but we still had to cut every chip by hand individually for the first four or five months of production,” explains Delage.

Meanwhile, they signed on with a major national distributor, Jonluca Neal, which led to launches in about 50 independent stores by the end of 2022. Then, after participating in the CHFA East trade show in fall 2022, they got their first big break into a major grocer, debuting in 200 Loblaws stores the following spring.

“I felt like we had an actual business when we got that listing,” says Johnstone. Shortly after their Loblaws launch, the equipment they needed finally arrived.

What followed was a big year for Peacasa. In 2024, they completed a rebranding and packaging refresh and got their second major listing in seven Whole Foods Market stores in British Columbia early in the year, which expanded to 12 stores nationally a few months later. They also launched with the Sobeys local program into 50 Ontario stores, along with 40 Longo’s locations, 50 Healthy Planets and more independents, bringing their total store count to 500 in 2024.

New product innovations came that year, too. While the duo launched with Sea Salt and Honey Dijon flavours, they added Salt & Vinegar. In 2025, Peacasa expanded into about 200 Safeways across Canada, 30 Co-op stores in Alberta and 25 IGAs in British Columbia.

Johnstone and Delage have plenty to look forward to in 2026. They just launched mini, 30-gram bags and variety packs and they’ll also begin selling their products in Walmart and Amazon.

Running a successful business is one thing, but doing it with a friend makes it better. “Victor is such a good guy to be in business with,” says Johnstone. “I don’t know anyone who works harder than him, and he also happens to be really smart.” Delage echoes Johnstone’s sentiments: “Our friendship has evolved over the years as we’ve built this out. We’ve always had the same vision of building this into something bigger.” CG

30 seconds with …

VICTOR AND AARON PEACASA

What do you like best about your job?

AARON: I like that it’s challenging and that every day there’s something I need to learn or work on. I’m constantly learning, which is a good thing.

What has been your worst day in business so far?

AARON: One bad day from recent memory was when we were working on our packaging redesign and did a concept test with some market research and it performed horribly, worse than our current packaging. That really shook me, but I quickly rebounded, took the learnings from that and we ended up making something that was so much better.

What’s the best career advice you’ve received?

VICTOR: If you’re gonna cut down a tree, spend 90% of your time sharpening the axe and the other 10% cutting down the tree.

What’s your favourite product from the lineup?

VICTOR: I like Sea Salt. I have a long commute, so I like to eat them when I’m driving.

AARON: Mine is the Salt & Vinegar. I’ll have a bag of chips with dip for dinner sometimes if I’m feeling lazy. I like them better than potato chips because you actually feel satisfied and full after.

What do you like to do when you’re not working?

VICTOR: I like hiking, camping and sports like hockey and tennis. I like playing them and watching them, too.

AARON: I play video games and board games. I like running, rock climbing, hiking, trail running and cycling, too. Victor and I are hoping to go on another long hiking adventure soon.

Ideas

HEALTH REGULATIONS

BEYOND THE LABEL

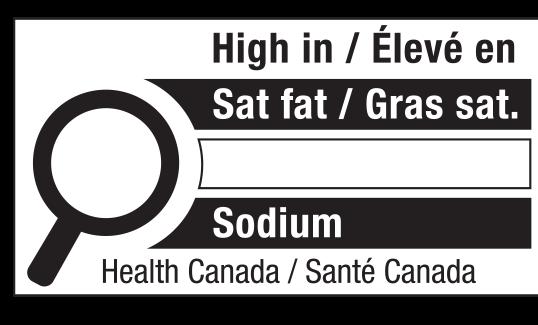

HealtH Canada’s front-of-paCkage (fop) nutrition labels, identifying packaged food and beverage products that are high in sugar, sodium and saturated fats, are now in effect.

As of Jan. 1, regulations require products to display the blackand-white symbol if one or more of those nutrients meets or exceeds specified thresholds.

Retailers tell Canadian Grocer they worked hand in hand with vendors to ensure products are meeting the new requirements, and any items currently on shelves without the label were manufactured before the deadline.

“We have worked closely with our vendor partners to ensure compliance for products in our assortment, including our private-label offerings,” says Stephanie Bonk, communications manager at Metro.

She adds Health Canada’s new FOP labelling requirement serves as “an additional touchpoint for Canadians to engage with nutrition information as part of their overall shopping experience,” alongside Metro’s own initiatives.

One example is Metro’s My Health My Choices program. Launched in 2021, it categorizes thousands of products under more than 40 attributes—such as “aluminium salts free,” “fat free,” “no

palm oil,” “vegan” and “no artificial nitrates”—helping “customers navigate options and make choices that align with their values and lifestyle,” Bonk explains.

The symbols are less ubiquitous at health-focused chains such as Healthy Planet, which prioritizes better-for-you brands.

“Because of our strict ingredient standards, our assortment naturally excludes many products that require the new high saturated fat, sodium or sugar warning labels,” says the Ontario retailer’s general manager Muhammad Mohamedy.

That said, Health Planet carries some popular brands that now require the symbol, and Mohamedy says it’s already influencing purchasing decisions. “We’re seeing customers pause when they encounter a warning on items they may have previously perceived as healthy,” he says.

Rather than creating confusion, those moments are prompting conversation. “We have expert nutritionists on the sales floor specifically to help customers navigate these choices and guide them toward the many alternatives we stock that better support their health and well-being,” says Mohamedy.

Brad Fletcher, president of The Village Grocer in Markham, Ont., says customers are eager for this type of information. “It seems every day more and more customers want to be educated about their food and beverage intake,” he says. “From a consumer perspective, it’s information they can work from.”

Consumer interest in nutrition labels is already high. According to research from Ipsos, more than half (54%) of Canadian adults say they are frequent label readers.

“Canadians are on a self-driven path to monitor their intake of different nutrients,” says Emma Balment, director, food and beverage group, market strategy and understanding, Ipsos. “FOP labels will help those consumers make choices.”—Chris Daniels

TECH TALKS

From AI-powered pricing to checkout solutions and even finding the right technology partner, NRF ’26 Retail’s Big Show in New York City last month offered a front-row seat to leading innovations and strategies. Here are a few of the conference sessions that caught our attention.

MOVE ALONG, ANALOG

CANADIANS ARE LOOKING for consistency and transparency when it comes to grocery prices, said Janet Rickford, vice-president, stores and merchandising solutions at Loblaw Companies Limited.

“They want to see if commodity prices go down, we can react quickly,” she said.

Rickford was part of a panel moderated by Matthew Pavich of Revionics, a software company that provides AI-powered lifecycle price optimization solutions for retailers— and a partner of Loblaw.

To provide consistency and transparency to its customers, Loblaw shifted its pricing practices.

Once centralized—relying on manual

HOWDY PARTNER!

work and teams of specialists— pricing is now part of each division. Of using pricing technology, Rickford said, “Yes, your pricing gets better, but it’s also the practices around it and the way you look at your data, the way you store it, the way you keep it clean and all of the small things you can do along the way.”

Scott Winburn, senior director of pricing strategy at Coborn’s, a grocery retailer headquartered in Minnesota, agreed—it’s out with analog and in with AI.

“We’re at the beginning stages of our AI journey, but we recognize we need to move away from Excel and manual process to pass value to consumers,” he said.

“IN THE WORLD we’re living in, the deployment of successful AI solutions and use cases is not your typical IT project,” said Hayley Tabor, vice-president, global alliances, industries, at Dell Technologies.

Tabor, who moderated a panel of senior execs from Nvidia, Everseen and Accenture, said partner ecosystems are becoming critical to the successful deployment of AI in retail.

“Trying to develop everything in house, in my opinion, is a mistake,” said Azita Martin, vice-president and general manager, retail & CPG at Nvidia, a dominant player in the AI space.

Instead, retailers should seek strategic collaborations with partners who have proven expertise in their areas. That approach, the panellists said, allows retailers to unlock AI’s transformative potential and scale solutions to complex challenges across supply chain, e-commerce, merchandising and more.

SHELVES TALK, SHOPPERS LISTEN

IF YOUR SHELVES could talk, what would they say? They should share stories of products needing restocking, real-time promotions and detailed product information.

Increasingly, grocers are turning to electronic shelf labels (ESLs) to bridge the gap between physical and digital retail, which is mission critical in the modern age of retail.

In fact, according to research conducted by Pricer, a Swedish ESL provider, eight out of 10 shoppers are “ambient” and expect the same experience across multiple channels.

“They expect the exact same experience in store as on their phone, which they bring to stores,” said Pricer’s global chief product officer Finn Wikander. “So, if prices don’t match [instore and online], or if product isn’t available, trust is gone and

the shopper will be, too.”

Not only this, but ESLs can contribute to the bottom line. Seven in 10 customers walk out of a store if the item they want is out-of-stock, according to Pricer. Adopting ESLs can keep stock levels as accurate as possible.

“We think an empty shelf breaks trust,” said Rob Smith, technology officer at East of England Co-op—a regional, member-owned cooperative serving local communities through its food stores, gas stations and more. “If you haven’t got [the product], the customer isn’t going to come back. With a digitized solution, the shelves tell the truth in real time.”

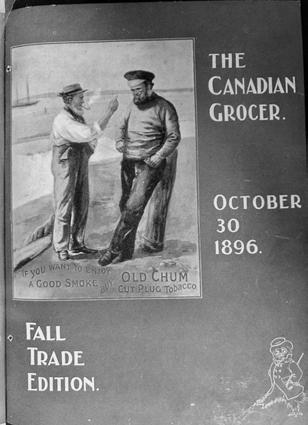

Canadian Grocer debuts in 1886 to provide retailers and wholesalers with practical information for their business. At the time, independents anchor towns and cities. Most products are sold in bulk and counterservice (or clerk-assisted shopping) is the norm.

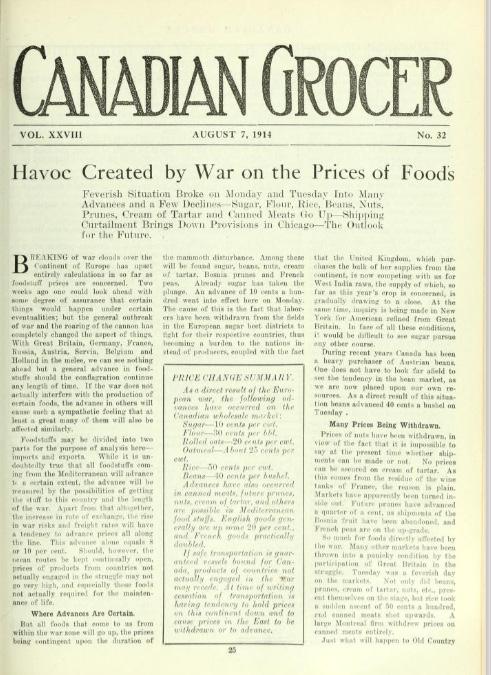

Grocers grapple with rising prices and shortages following the start of the First World War. The federal government introduces a war tax to fund the conflict, targeting staples such as sugar and coffee.

GROCERY AT A GLANCE

For a remarkable 140 years, Canadian Grocer has reported on the business of selling groceries in Canada. It all began in 1886, when John Bayne Maclean— who had been a financial editor at The Toronto Daily Mail—recognized a need in the market and launched Canada’s first trade journal dedicated to the grocery industry. Regular publication began the following year under the name The Canadian Grocer and General Storekeeper

It has often been said, “if there’s one constant in grocery, it’s change.” And over the decades, Canadian Grocer has been there documenting all the big changes—from emerging retail models to evolving customer preferences and game-changing technologies. Here, we’ve dug deep into our archive to bring you a snapshot (this is just a taste!) of some key moments that helped shape the dynamic grocery industry we know today.

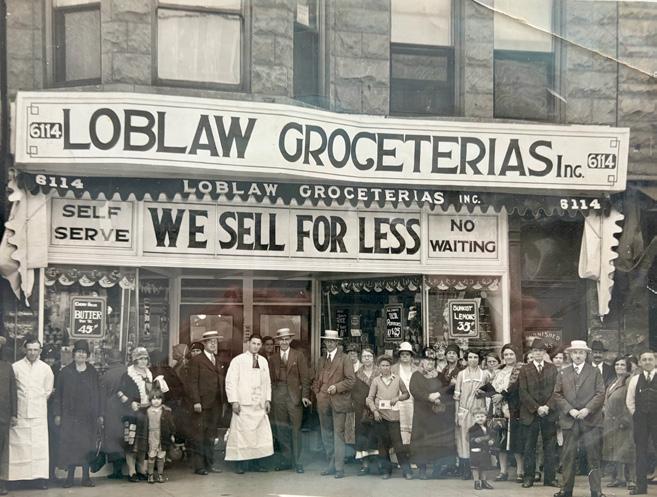

Loblaw Groceterias debuts in Toronto, marking a pivotal shift to self-service—a model that would come to define modern grocery shopping.

Though they first appeared in the 1930s, frozen foods become a mainstream grocery category helped by better technology, packaging and postwar consumer demand. Suburbanization fuels expansion of grocery chains around the country.

Supermarkets begin to emerge in urban centres. The model is characterized by self-service aisles and wider assortments. Chain operators gain ground during the decade at a time when the Great Depression heightens price sensitivity. Austerity means shopping baskets are mainly filled with staples such as canned goods, potatoes, tea, sugar and flour.

The Universal Product Code (UPC) is introduced to address rising labour costs and slow checkouts. The first barcode (on a package of Wrigley’s Juicy Fruit gum) is scanned at a supermarket in Ohio in 1974; Canadian retailers soon adopt the technology, transforming pricing accuracy, inventory control and data collection.

Warehouse clubs with membership pricing arrive in Canada in the form of Costco, which made its Canadian debut in Burnaby, B.C. Rival Sam’s Club (owned by Walmart) has a short-lived run in Canada opening in 2003 and exiting the market in 2009.

Walmart arrives, having acquired 122 Woolco stores from Woolworth Canada. The U.S. giant rapidly expands, eventually adding a full grocery offering to its locations, intensifying price competition across the sector.

After establishing a foothold in Europe, click and collect arrives in Canada. Loblaw launches the service at a single store in Richmond Hill, Ont. Eventually, home delivery would prove to be the preferred model among online grocery shoppers.

By the 2010s, selfcheckouts are a prevalent feature in larger grocery chains, reshaping front-end operations and the customer experience.

The COVID-19 pandemic shocks the grocery system. Supply chains and operations are tested and hoarding (toilet paper is the hottest item), empty shelves, social distancing and Plexiglas become the new normal. Online grocery adoption accelerates during the crisis.

As persistent inflation and a rising cost of living squeeze Canadians, discount grocery stores gain momentum. The period sees conventional retailers doubling down on their discount banners, such as No Frills, FreshCo and Food Basics, with a spate of new openings and store conversions.

Years in the making, Canada’s Grocery Code of Conduct comes into effect. The voluntary code aims to bring greater fairness and transparency to retailer-supplier relations.

Chapman’s named Canada’s Most Valued Brand in a study performed by Toronto Metropolitan University which surveyed 2,000+ Canadians on seven traits they value most.

Available in 14 exceptionally creamy flavours. Discover the collection at chapmans.ca

As Canadian Grocer marks 140 years of covering the evolution of grocery in Canada, we’re shining a spotlight on some of the standout companies that have helped build—and continue to shape—the industry. First up, Chapman’s.

CHAPMAN’S SWEET SUCCESS

THEN

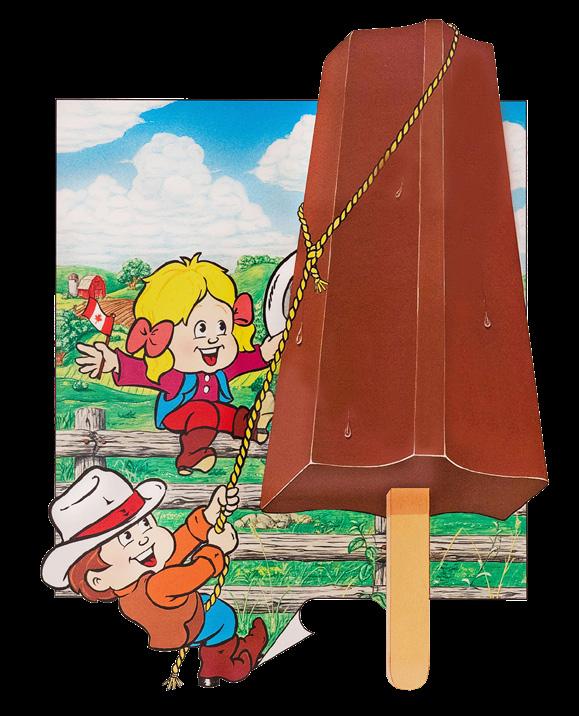

The story of Chapman’s Ice Cream began in 1973 when David and Penny Chapman moved into an apartment above an old creamery in Markdale, Ont. In the early days, the company had just four employees and two used trucks; but what they lacked in resources, they made up for in ambition, producing 15 flavours of ice cream.

“Our early ambitions were to succeed, while shaking up the norm in the value market, offering many flavours and not just four, which was common,” explains Penny Chapman, president of the company. “The biggest challenges at the time were to get both the industry and consumers to accept the black packaging and to get enough space in the stores for the many flavours we were introducing.”

That bold thinking translated into industry firsts: the introduction of its Sorbetto sorbet line in 1985; Canada’s first frozen yogurt line in 1989 (Chapman’s remains Canada’s No. 1 frozen yogurt maker today); and in 1999, Canada’s first certified peanut-free and nut-free ice cream—setting a new standard for food safety and inclusion.

NOW

Today, Chapman’s is Canada’s largest ice cream producer, with products sold in every province and territory. The operation has grown to include a nut-free production site—“The Nut House,” a dedicated facility for nut-containing products—a distribution centre and a wastewater treatment plant, making it one of the most impressive ice cream operations in the country.

The portfolio has also grown to more than 180 products ranging from luxury, premium and economy ice creams alongside sorbets, ice lollys and innovative offerings designed to meet consumers’ dietary needs and preferences.

At its core is a philosophy of “growing with care.” From reducing water consumption and participating in energy conservation initiatives to responsible sourcing and sustainable packaging, Chapman’s is building one of the most efficient— and environmentally responsible—ice cream factories in the world.

For its efforts, in 2025, Chapman’s was named Canada’s Most Valued Brand by Toronto Metropolitan University’s Great Canadian Brand Index.

NEXT

True to its roots, Chapman’s continues to prioritize Canadian suppliers whenever possible, championing Canadian dairy as among the highest quality in the world.

And the company is investing in its future. Construction is underway on a new production facility in Markdale—an expansion that will create 200 high-paying jobs and introduce state-ofthe-art automation. With an investment exceeding $200 million, Chapman’s plans to launch a wave of innovative products, including offerings not currently available in Canada.

“We are committed to Canada, we always have been and Canadians showing their trust in our brand is the greatest feedback we could get,” says Ashley Chapman, the company’s chief operating officer, and David and Penny’s son. “It has been a challenging year for all Canadian businesses. Costs are going up and uncertainty puts a shadow on potential growth, but we are committed to doing our best to continue offering the best possible ice cream products at the best price coast to coast.” CG

Chapman’s vintage branding features Ashley (now COO) and his sister Frances. This poster was used in marketing throughout the late 1970s and 1980s. Illustration by Wilf VanDyk, who

Chapman’s, Canada’s No. 1 frozen yogurt maker, first launched the product in 1989 Humble start: The company began with just two used delivery trucks

All in the family.

The Chapman’s: David, Ashley (COO), his wife Lesya (director of marketing and communications) and Penny (president)

Factory creamery, 1973

CFIG Congratulates Canadian Grocer on 140 Years Supporting the Independents!

Beyond the prescription

How GLP-1 users are re-shaping food and beverage consumption

Traditional meal occasions are somewhat dissolving for GLP-1 users as they embrace continuous grazing patterns, with dinner remaining their focal-point meal

The rise of GLP-1 medications such as Ozempic and Wegovy reveals a new consumer segment that’s rewriting the rules of food and beverage consumption. These consumers aren’t abandoning indulgent foods or avoiding entire aisles—they’re approaching eating and drinking with balance in mind.

Currently representing approximately 6% of Canadian adults, GLP-1 users are predominantly higher-income boomers and generation Xers managing Type 2 diabetes, but the demographic is rapidly shifting. Millennials and gen-Z consumers are flooding into this market seeking weight-management solutions, transforming what began as a medical necessity into a lifestyle choice. It isn’t niche anymore—it’s a movement from medical to mainstream.

THE INDULGENCE PARADOX: PERMISSION OVER PROHIBITION

GLP-1 users consume indulgent snacks at a rate on par with the general adult population—they’re still reaching for chocolate, ice cream and baked goods. The difference? They’re approaching these categories with a “mini-meal” mindset, seeking portion-controlled options that deliver emotional satisfaction without the guilt.

This behaviour demands brands and retailers abandon the traditional diet playbook. Consumers using GLP-1s want products that whisper “yes, you can” rather than shouting “no, you shouldn’t.” Smart brands and retailers are already pivoting, creating premium, portion-controlled offerings that deliver indulgence that supports nutritional guardrails.

THE ALL-DAY GRAZING ECONOMY

Traditional meal occasions are somewhat dissolving for GLP-1 users as they embrace continuous grazing patterns, with dinner remaining their focal-point

meal. Breakfast ranks notably lower among this segment, replaced by five or more small eating occasions throughout the day. This shift represents a fundamental restructuring of how, when and what people consume.

For retailers, this means considering everything from product mix to store layouts. The opportunity lies in creating “mini-meal” solutions—portable, protein-rich options that blur the lines between meals and snacks. Think cheese and fruit combinations, single-serve yogurt parfaits and grab-and-go lean protein boxes. The snacking aisle isn’t shrinking; it’s expanding to encompass the entire store.

CLEAN LABEL COMMAND

GLP-1 users aren’t just changing how much they eat; like many Canadians, they’re scrutinizing what they eat. These label-readers prioritize protein and fibre content while actively seeking “free from” claims. Diet and zero-sugar beverages see significantly higher consumption rates among this segment, as do vitamin-enriched options.

The clean label movement, already strong among mainstream consumers, becomes non-negotiable for GLP-1 users. They’re seeking transparency, nutritional density and functional benefits in almost every bite and sip. Made in Canada claims resonate strongly, particularly among the gen-X and boomer users who currently dominate the segment.

THE FOODSERVICE SURPRISE

Perhaps most counterintuitively, GLP-1 users visit foodservice establishments more than non-users, despite nearly half having made recent dietary changes. This isn’t a contradiction—it’s an opportunity. These high-frequency diners seek protein-forward, grazing-friendly menu options that align with their eating patterns.

For grocery retailers with prepared food sections, this trend signals massive potential. The deli counter, hot bar and grab-and-go sections become critical touchpoints for capturing GLP-1 user dollars. These consumers want convenience without compromise, seeking fresh, customizable options that support specific dietary needs.

The GLP-1 revolution isn’t coming, it’s here. Retailers that recognize these users as lifestyle consumers—not dieters—will capture a growing, high-value market, with halo benefits across the broader health-conscious segment. The question isn’t whether to adapt to GLP-1 users, it’s whether you’ll lead the shift or be left behind by competitors who recognized it early. CG

Jenny Thompson is a vice-president with Ipsos Canada supporting the FIVE service, a daily diary tracking what individuals ate and drank yesterday across all categories, brands, occasions and venues.

Proud to be a partner in your success! Congratulations on your 45th Anniversary!

Independent by design

For 45 years, DCI has delivered scale and leverage while keeping independents in control

Independent grocers have never had more on their plates. Costs are rising, consumer expectations are shifting and competition from national chains continues to intensify. Yet every day, across cities, suburbs and rural communities, independents are negotiating with suppliers, planning promotions and adapting in real time to keep pace with the market—often with far fewer resources than their biggest rivals.

And while they may not have the same scale, they’re increasingly gaining something just as power ful: shared strength.

That’s where Distribution Canada Inc. (DCI) comes in. Even 45 years since its inception, the organization continues to help independent grocers—from single-location operators to multi-store regional businesses—strengthen their competitive position through collective buying power, collaboration and shared access to suppliers and resources.

In a grocery landscape defined by consolidation and constant change, the fact that DCI is still growing underscores that independence and scale don’t have to be mutually exclusive.

“Since 1981 we’ve grown a small network of regional distributors into one of Canada’s most respected buying and marketing organizations representing over 100 independent grocers and suppliers nationwide,” says Barry Lanteigne, DCI President and Director of Operations. “At the same time, our mission has remained steady: to strengthen the competitive position of independent grocers by creating efficiencies, building relationships and fostering collaboration with trusted supplier partners.”

In fact, DCI is coming off its strongest period of growth to date, with membership up more than 50% since 2020, says Lanteigne. At a time when consolidation is reshaping the grocery industry, this growth reflects the continued demand for a collaborative model built specifically around independent operators.

A strategy built for today’s grocery realities

A key fact behind this recent growth is DCI’s five-year strategic plan, which was implemented in 2022 and designed to ensure the organization evolves alongside a rapidly changing

L-R: Barry Lanteigne, DCI Canada, Mike Sharpe, Sharpe’s Food Market

grocery industry. “The focus has been on growth, technology and connectivity,” says Lanteigne. “Ensuring our members have the tools, insights and partnerships they need to compete and thrive.”

The strategy also reflects a clear understanding of the pressures independent grocers face: rising costs, increased competition from national chains, shifting consumer expectations and the accelerating role of technology. Rather than attempting to redefine independence, the plan is about reinforcing it—supporting what independents already do well while helping them compete more effectively at scale.

“Our evolution has always been rooted in collaboration,” Lanteigne adds. “The spirit of cooperation remains the heart of everything we do.”

In preparing for the future, DCI is focused on relevance and value—ensuring membership delivers tangible benefits back to each retailer’s individual businesses. “We’re not a one-size-fits-all organization,” says Lanteigne.

Case in point: DCI represents 106 members across Canada, spanning a wide range of independent grocery formats and regional markets. That breadth is reflected on the board, where retailers from urban centres, small towns and rural regions contribute equally to decision-making. It’s a model that keeps priorities grounded in day-to-day realities, says Lanteigne.

DCI Treasurer Mike Sharpe, owner of Sharpe’s Food Market and a board member for the past six years, echoes this point. “Barry manages the day-to-day operations, but the direction comes from grocers who are actually in the business,” he says.

For members, one of DCI’s core advantages is collective buying power. Rather than negotiating with suppliers individually, independents are able to approach them as part of a national group—strengthening their position at the table.

DCI negotiates programs and partnerships on behalf of its members, helping level the playing field while preserving autonomy at the store level. Just as importantly, the organization avoids exclusivity in favour of choice.

“We want competition,” says Lanteigne. “Our goal is to give members real options and access to partners that make sense for their individual businesses.” That includes welcoming new and emerging suppliers into the network, a priority reflected in DCI’s expanding portfolio of suppliers.

That philosophy extends beyond traditional grocery categories too. DCI works with a broad range of supplier and service partners—including digital companies, benefits providers and insurance organizations—all with the goal of supporting independent grocers as they focus on running their stores.

Some long-term member perspectives

For many long-standing members, DCI’s value extends well beyond programs or rebates. Over time, relationships—both with vendors and with fellow independent grocers—have become one of the organization’s most important differentiators.

Gordon Dean, president of Mike Dean Local Grocer—a family-owned independent grocery business with stores in rural Ontario and Quebec, and a DCI member since

Barry Lanteigne, DCI President and Director of Operations.

“

The focus has been on growth, technology and connectivity”

— Barry Lanteigne, DCI President and Director of Operations

Mike Sharpe, owner of Sharpe’s Food Market

†Made in Canada with domestic and imported material.

®’ Registered trademark of Kimberly-Clark Worldwide Inc., used under licence.

the mid-1980s—points to access as a defining advantage. “Getting into the same room as decision-makers, especially at mid- and large-sized vendors, is massively important for an independent,” he says. “Those conversations don’t happen easily on your own.”

Equally important, Dean says, is the peer network created by DCI’s national footprint. Because members operate in different regions and don’t compete directly, they can share ideas openly and candidly. “You’re talking to people halfway across the country, in completely different markets,” he says. “There’s no competitive tension. You can throw ideas—or even numbers—around and get real feedback.”

That national perspective often exposes independents to alternative approaches shaped by local realities too. “People in Newfoundland or Western Canada may go to market very differently than we do,” notes Dean. “Sometimes those differences are refreshing, and they make you look at your own business differently.”

Dean also underscores the importance of face-to-face connection in an industry defined by complexity. While digital tools play a role, he believes in-person meetings remain essential. “Nothing in grocery is simple,” he says. “Strong, longterm relationships—with vendors and with each other—are what actually make things happen.”

Those same themes—access, trust and shared experience— also resonate with Rick Rabba, President of the family-run chain of convenience/grocery stores, Rabba Fine Foods, a DCI member since 1997.

“The buying power, the ability to negotiate as a national buying group…it really gives independent retailers a much stronger voice than they would otherwise have,” says Rabba who has served on DCI’s board.

Perhaps less tangible but just as crucial, he adds, is the benefit of being part of a national independent network where peers can share their challenges. “You get to learn so many things you might not have otherwise known…and you can bring these back to your own business and share with your team,” he says. “Some of the opportunities and challenges that exist in working with a family business are the same no matter what part of the country you’re from.”

He says it’s not surprising then that this shared experience creates a sense of connection among members—one rooted in serving communities in different ways while navigating many of the same operational pressures.

Embracing technology without jeopardizing connection

Technology has become an increasingly important focus for DCI over the years, particularly as digital tools become more accessible to smaller operators. “Technology used to come with a very high cost of entry,” says Lanteigne. “Now, with software-as-a-service models [which reduce upfront technology costs], it has become much more attainable for independents.”

Sharpe’s Food Market, Campbellford, Ontario

DCI has worked to connect members with e-commerce platforms and digital solutions that help them compete more effectively, while also supporting shifts in marketing strategy. “As print costs have risen, digital and retail media have become more targeted and measurable,” Lanteigne says. “That’s especially important for independents.”

Yet even with these advances, both Lanteigne and Sharpe stress the importance of relationships as fundamental to the success of independent grocers. During periods of disruption—most notably throughout the recent pandemic—members stayed in close contact, sharing information, comparing approaches and adapting as conditions changed.

That collaborative mindset has continued, with members using the organization as a forum to discuss common challenges, explore new opportunities and exchange ideas across regions via technology and in-person.

This emphasis on personal connection is reflected in DCI’s annual Business Summit and charity golf tournament. Held each June in conjunction with the Canadian Independent Grocery Buyers Alliance, the summit brings together members and supplier partners for learning, discussion and structured networking. A key feature is a speed-networking format that allows participants to quickly assess fit and explore opportunities.

Participation has grown steadily in recent years, reflecting DCI’s expanding footprint and relevance. For grocers, the event offers a concentrated opportunity to step away from daily operations, learn about new programs and products, and connect with peers.

That emphasis on connection carries through year-round. Lanteigne also visits member stores across the country regularly to stay in tune to evolving needs and realities in the workplace. “Being present is how we stay relevant,” he says.

Independence with staying power

This kind of mindset resonate with grocers as they navigate their own market realities. For Sharpe, independence is about proximity—to customers, to communities and to dayto-day decision-making. “Independent grocers are deeply connected to the communities they serve,” he says. “That allows them to respond quickly and adapt.”

That agility remains a defining advantage at a time when consumer expectations, technology and competitive pressures are evolving rapidly. It’s also the quality DCI is most intent on preserving—ensuring independents gain scale and support without sacrificing the local focus that sets them apart.

As DCI marks its 45th anniversary, the emphasis remains firmly on the future. Continued membership growth, thoughtful technology adoption and deeper collaboration with supplier partners will shape the organization’s next phase, while its core mission remains unchanged.

“Our journey reflects the resilience, adaptability and entrepreneurial spirit of the people we represent,” says Lanteigne.

After 45 years, DCI’s experience demonstrates that collaboration doesn’t dilute independence—it strengthens it. In a consolidating grocery landscape, DCI offers a clear reminder that independent grocers can remain competitive, relevant and firmly rooted in the communities they serve.

Sharpe’s Food Market, Campbellford, Ontario

NEW WHAT’S

NEW PRODUCTS IN GROCERY

A NEW WAY TO CHIP AND DIP

Canadians are snacking in record numbers, seeking new ways to satisfy old cravings. Enter the all new Quick Crisp Crinkle Chips: a fun twist on a classic snack. Coated in a proprietary batter and made to cook in just five minutes, the warm Crinkle Chips join Cavendish Farms’s game changing Quick Crisp product lineup.

Designed for the air fryer, Quick Crisp Crinkle Chips are helping a new generation of Canadians fall in love with their freezers.

DISCOVER ACTIVIA’S NEWEST ADDITIONS TO THE PLAIN YOGURT FAMILY

The Lactose Free 650 g Plain Tub and the Plain 8×100 g Multipack , offering a creamy texture and delicious taste that can be added to many favourite foods or simply eaten on its own. Made with 100% natural source ingredients , these plain probiotic* yogurts contain no added sugar and no gelatin . Each serving provides a billion active probiotics , it is the perfect addition to everyone’s daily routine.

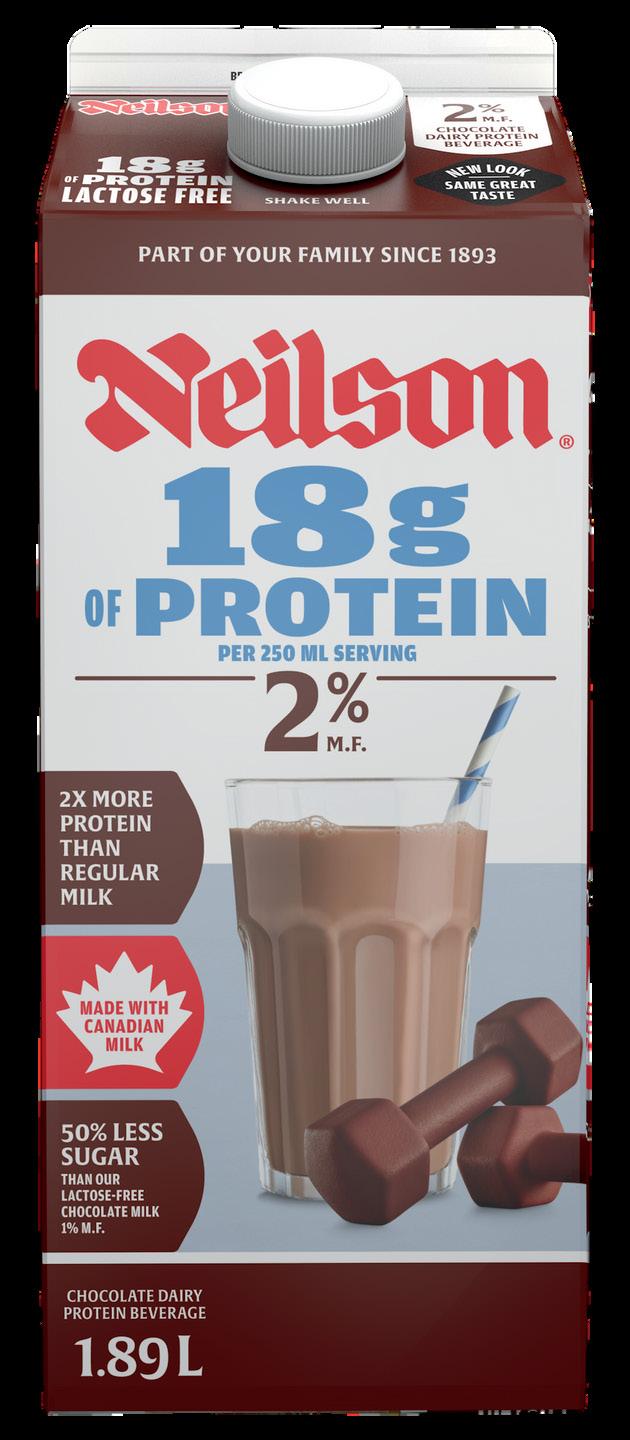

FUEL THE MORNINGS* WITH SILK PROTEIN

— a new plant powered beverage packed with 18g of protein and only 6g of sugar. It offers twice the protein and half the sugar of regular 2% milk, plus 10 essential nutrients including omega‑3. It’s an easy way to power up the day, whether it is added to cereal, blended into smoothies, or enjoyed on its own. Proudly made in Canada. Available in regular and chocolate flavour.

*As part of a complete breakfast and balanced diet.

BRING THE AUTHENTIC TASTE OF MEXICO HOME!

Meet Mi Tierra tortilla chip strips—crispy, bold, and made for dipping, topping, or snacking. Now available across Canada in three crave‑worthy flavours:

Salt – Classic + versatile Hint of Lime – Bright + zesty Pico de Gallo – Inspired by fresh salsa

Crafted with deep corn expertise, Mi Tierra offers high‑quality, culturally rich flavour at an accessible price.

*With more than 109 CFU Bifidobacterium lactis per serving, a probiotic that contributes to healthy gut flora.

MADE FOR THE MIGHTY

Eat clean & feel Mighty. That’s it. Lock in with complete protein, full of everything Canadians need for lasting energy, without the crash. It’s as simple as the ingredients. Fuel the day with clean, protein powered Original Chicken Sticks. Made with chicken raised without antibiotics, these high protein snacks deliver 12g of complete protein with zero sugar and only 110 calories per stick.

THE LEADERS

LESSONS FROM THE TOP NANISS GADEL-RAB, PRESIDENT, MONDELĒZ CANADA

“... LEADING WITH EMPATHY IS PARAMOUNT. EMPATHY IS WHAT TURNS STRATEGY INTO CULTURE; IT IS, AND WILL REMAIN, ONE OF THE MOST POWERFUL LEADERSHIP DIFFERENTIATORS OF ALL TIME” -NANISS GADEL-RAB

What is your leadership story? I started my career on the factory floor as an engineer in Unilever Middle East’s Future Leaders Program. My curiosity and desire to learn pulled me closer to the heart of the business and led me to roles in marketing, sales and strategy. I was fortunate enough to work across nine countries and three continents touching more than 15 global brands. Each transition brought its own challenge with plenty of uncertainty, but it also unlocked new horizons and richer perspectives. And with every leap, a little more magic was created that not only shaped my career, but also who I became as a human and leader.

In early 2025, after more than two decades with Unilever, an unexpected and exciting opportunity to lead Mondelēz Canada came my way. The brands, the culture and the people were simply too sweet to turn down. While change can feel uncomfortable, it’s the birthplace of new possibilities beyond what I thought I was capable of. I’m stepping into this chapter as president with excitement and energy for what’s ahead. If there is one constant in my journey, it’s change. Growth never happens in comfort zones but rather in those uncertain, thrilling moments when everything shifts.

By Shellee Fitzgerald • Photography by Tobi Asmoucha

You’ve worked in several markets around the world. How have these experiences helped shape you as a leader? Working across different markets did not just broaden my scope—it sharpened my perspective, expanded my leadership skills and deepened my strategic thinking. Different cultures elevated my appreciation of diverse thinking and experiences and strengthened my commitment to inclusion. Best of all, having the opportunity to work in different parts of the world in many different roles helped me build a global network that made the world feel

Is there a leadership principle that is nonnegotiable for you? Authenticity and openness are the foundation of trust, and trust is the foundation of everything else. When people feel truly seen, heard and safe to bring their full selves to work every day, something remarkable happens— you don’t just build a strong culture, you build a team that thrives, making the impossible, possible.

How has your leadership style evolved over time? Leading across different teams, markets and challenges shifted my focus from only delivering results to becoming more people-centric, building strong talent and investing behind the capabilities of the teams. Early in my career, I gravitated toward leaders who led this way—those who empowered their teams, invited different perspectives and trusted people closest to the work to make decisions. I realized leadership is not about having all the answers, it’s about asking the questions that unlock creativity, spark curiosity and open doors to uncharted possibilities. That approach had a lasting impact on me because it felt both human and effective, and it created space to learn, grow and contribute meaningfully. In today’s environment of constant change and rising expectations, that same leadership style is even more critical. Over time, when people are empowered to think boldly, the results follow naturally.

How do you evaluate when it is time to pivot from a strategy that isn’t working? This is a powerful leadership question. The first step is to understand what is not working—the strategy itself or the execution behind it. As the saying goes, “execution eats strategy for lunch.” From there, it is important to listen to two important anchors: 1) data—it tells us what is happening in the market, and 2) stakeholders—our consumers and customers help us understand what’s happening. In many cases, only one or two elements of the strategy need recalibration. In others, a new strategy is required. When both the data and stakeholders’ insights consistently tell the same story, it’s a clear signal it’s time to pivot. Every pivot must be grounded in facts and insights, and it must be clearly articulated. Explaining why we are changing the direction is essential

to bring teams and partners confidently along the journey.

How do you stay curious and ahead of industry shifts? The speed of change has never been faster; therefore, curiosity and agility are more critical than ever. To me it’s about intentionally looking beyond the industry, listening closely to employees and customers, and creating space for challenge and debate. This means building learning into my calendar, staying connected to the front lines where early signals emerge, and staying connected to our consumers by actively listening to their voices on social media and engaging with the local culture around us. I also find it important to ask questions, welcome diverse perspectives, and pay attention to cultural and workforce shifts—not just market data but insights and turn them into action before disruption forces it.

As president of a CPG company, what are your main challenges right now? How are you navigating these challenges? The CPG industry, while demanding, is incredibly fulfilling and rewarding. I like to frame challenges as opportunities because this is where transformation begins. For example: Volume growth in CPG is becoming harder, which creates an opportunity to design culturally relevant innovations that resonate with consumers. Margin pressure is intensifying across the board, yet it challenges us to rethink category growth through demand creation, not just cost management. And assortment complexity is increasing, which opens the door to digitization and simplification to improve speed and efficiency. The CPG industry will keep evolving and the winners are those who will act with resilience and agility to reshape the trends of the future.

What’s an important change leaders need to embrace right now? I believe successful leaders need to embrace uncertainty and a flexible mindset to pivot their plans and adapt to the new trends and market realities. Leaders also need to integrate technological proficiency as an enabler to their organizations. Technology empowers a business to work smarter, faster and deliver a better experience for customers and employees. And leading with empathy is paramount. Empathy is what turns strategy into culture. It is, and will remain, one of the most powerful

leadership differentiators of all time. I believe the future belongs to those who can combine compassion, courage and curiosity to build resilient teams.

Is there a piece of advice you return to again and again? A simple yet powerful metaphor I often return to and share with my team is, “be a coffee bean.” When a potato, an egg and a coffee bean are all put into boiling water, each reacts differently. The potato becomes weak and soft, the egg becomes hard inside, but the coffee bean changes the water itself creating something completely new and aromatic. So, in every challenging situation, instead of letting the environment change you, you have the choice to transform the environment to create a positive impact.

What do you want to accomplish in your role? My aim is to leave the organization stronger than when I arrived. This means developing the next generation of leaders and creating a lasting positive impact not just for my team, but also for our customers and consumers. CG

From price to loyalty to prepared foods and more, our exclusive research reveals what’s on the minds of Canada’s grocery shoppers

BRING HOME THE BELL

“Know thy shopper”

remains a retail imperative, but in today’s shifting grocery landscape, it’s no longer enough to understand who shoppers are. Retailers must also have a handle on what they want, when they want it and how they prefer to buy.

In this, our 2026 GroceryIQ Study: Checking Out the Latest Grocery Shopper Insights, we delve into where and how shoppers in Canada are procuring groceries—and what they truly think of everything from the service they receive to the value of their store’s loyalty program and how much appetite they have for supermarket prepared foods.

WHERE CANADIANS ARE BUYING GROCERIES

There’s no question, Canadians are feeling squeezed. According to the latest Bank of Canada survey of consumer expectations, anxiety around higher prices and economic uncertainty remains elevated—and it’s shaping how people shop.

While discounters have a slight edge over traditional chain stores (54% versus 52%) in

BIGGEST PET PEEVES AT THE GROCERY STORE

“Price. This store is the most expensive to shop at, but it’s the closest to me so I have no choice”

“More cashiers available during peak shopping hours when the store is very busy”

PRICE REMAINS PARAMOUNT

Once again, price is the most important factor to shoppers when choosing where to buy groceries

terms of how frequently those surveyed visit, our research points to a broader retrenchment. A growing number of shoppers report never shopping at specialty/natural stores, ethnic shops and online stores, suggesting a back-to-basics shift in priorities.

As Canadians grapple with the cost of living, it’s no surprise that price continues to be the dominant driver for 82% of shoppers when choosing a grocery store. Price is especially important to boomers, with 87% naming it as the most important consideration, followed by women shoppers (85%) and gen-Xers (84%). Other top factors shoppers consider is product quality (72%), sales/promotions (71%, up from 69% last year) and product freshness (70%). Less important to shoppers is store organization (32%, versus 40% a year ago) and healthy/better-for-you products (19%, down from 24% last year).

SIZING UP THE STORE

We also asked shoppers to rate their primary grocery store across a range of factors. The good news is that six in 10 shoppers indicated a high level of satisfaction with store cleanliness and variety of products offered, consistent with last year. And more than half of those surveyed gave their store an “excellent/ very good” rating for organization, helpfulness and friendliness of employees. Grocery shopping, however, continues to be regarded as a chore for most, with just 39% (down from 42% last year) agreeing that their store is fun to shop.

While shoppers generally report positive experiences at their primary grocery store, there’s room for improvement. Shoppers pointed to out-of-stock products (particularly products on promotion), pricing and friction at the checkout as their biggest peeves. Respondents also complained of too few cashiers during peak periods and lax enforcement at the “10 items or less” lanes. The message is clear: keep shelves stocked and checkouts moving to maintain shopper satisfaction.

We also asked shoppers to rate the reputation of their grocery store. Responses mirrored last year’s results, with 57% of shoppers rating their store’s reputation as good and 31% calling it excellent. It’s worth noting that Costco Canada stands out, earning an “excellent” rating from 59% of respondents.

LOVING LOYALTY

Locking in consumer loyalty is a powerful lever for all retailers. Grocers with strong loyalty programs get shoppers through the door more frequently, enjoy bigger baskets and have better data to personalize offers. With the stakes high, grocers have stepped up their efforts to woo shoppers and, for their part, shoppers are keen to participate in programs that serve up benefits and provide some relief at the checkout. In fact, the 2026 GroceryIQ Study revealed a significant uptick in the number of shoppers (73%, up from 69% last year) enrolled in and actively using a grocery store loyalty program. Participation is even stronger in Quebec, where

A LOOK AT LOYALTY

Active loyalty program use has increased significantly versus last year

LOYALTY PROGRAM FEATURES SHOPPERS CARE ABOUT MOST Reward points for redemption on groceries

for

value reward points for redemption from an online catalogue (30%) and the mobile app (41%) more than older generations Active usage is highest among Quebecers (87%), boomers (79%) Exclusive discounts are most important to female shoppers (47%) and Quebecers (54%) Quebecers also place high value on cash back (55%)

Your Experts in Cheese & Deli

Driving Brand and Category Growth

Our passion for exceptional Cheese & Deli is at the heart of everything we do. With a discerning eye for quality and a deep love for the craft, we curate the world’s finest offerings to inspire elevated food experiences. As dedicated category specialists, we don’t just follow trends - we help shape them.

87% of shoppers actively use a loyalty program, and among boomers, with 79% of those shoppers participating.

And shoppers have a favourable view of grocers’ loyalty schemes with an impressive 94% (up from 92% last year) indicating some level of satisfaction. Just 6% of survey respondents reported being dissatisfied with the loyalty program offered at their primary store.

While loyalty programs deliver a spectrum of perks, shoppers have clear favourites. Points redeemable for groceries tops the list as the most-valued loyalty program feature among 69% of shoppers. Exclusive discounts, while still important, have lost favour (43%, down from 49%), though they are more valued by women shoppers (47%) and Quebecers (54%). Cash back and personalized offers resonate with a sizable number

of shoppers, but online catalogue-based rewards lag far behind, valued by just 19% of shoppers surveyed.

For shoppers disinterested in grocery loyalty programs, the biggest barrier is a requirement to sign up for a credit card, cited by 28% of respondents, a five-point jump from a year ago. Other barriers include too many purchases required to earn rewards/points (21%) and the store demands too much information to enrol in the program (20%).

What about flyers? Our survey revealed that more deal-seeking grocery shoppers (54%, up from 50% last year) are taking a look at digital flyers before they head off to the store. Print flyers, however, continue their decline, with just 31% (down eight points) looking at them before shopping. And 19% of shoppers report not using flyers at all.

IN-STORE AND ONLINE SHOPPING

Shopper research

IN-STORE AND ONLINE

In-store shopping continues to dominate. Nearly all shoppers (98%) visit a store at least once a month to procure groceries, and our survey revealed a significant increase in the frequency of in-store shopping trips. In fact, 90% (up from 86% a year ago) of shopping trips were completed in-store. The uptick is driven by males, millennials, generation Xers and Ontario shoppers.

Online grocery is a more challenging story. Unchanged from last year, 19% of shoppers reported using “buy online for in-person delivery” at least once a month, while other e-comm methods

SHOPPER BEHAVIOUR

Millennials more likely than older generations to online shop in past month: Delivery: 34%

In-store pickup: 23%

Curbside pickup: 19%

THE GROCERY SHOP

Shoppers less likely to switch stores for

Buying items on reduced price/clearance

Buying fewer impulse items

Buying fewer groceries in general

Buying more private label/store brand products

Shopping more often at discount grocery stores

Using more coupons

Buying bulk packs

Buying fewer prepared foods

Buying cheaper animal proteins

Buying fewer fresh produce items

Using food saving apps

Buying more plant proteins

Have not changed my grocery store shopping behaviour due to rising prices/inflation

Private label is having a moment

Most likely to have

Fewer shoppers are using expanded services offered at the grocery store

versus

Due to rounding, in some charts, percentages may total

such as curbside pickup and in-store pickup both saw a decline (from 14% to 11%). Further, when asked about future shopping behaviour, a growing number of grocery shoppers anticipate they will not use in-store pickup and curbside pickup services a year from now.

Additionally, satisfaction with online

shopping fell significantly with just 40% of shoppers indicating they are “completely/very satisfied” with the experience, down from 50% a year ago. Fees, out-of-stocks, poor substitutions, dissatisfaction with product quality and order picked incorrectly are persistent peeves for these shoppers. In verbatims captured

by the survey, respondents had the following complaints: “website is designed poorly,” “it takes a long time to place an order … scrolling through all the pages,” and an “obligation to tip driver before order is fulfilled.”

WHAT SHOPPERS ARE BUYING

Few grocery shoppers turn up at grocery stores without a list or an inkling of what they’re going to buy; in fact, just 2% do. Most (82%) arrive with a list in hand, but despite a tightening of household budgets, our survey shows 63% of shoppers are leaving room for spontaneity, permitting themselves to go off-list at the store and add additional items to their carts.

The types of foods shoppers are adding to their carts is consistent with last year, but notably more shoppers (86%, up from 83%) purchased dairy. This puts it in the top spot and overtaking fresh produce, which is purchased by 83% of shoppers, unchanged from last year. Also making gains are salty snacks, coffee, cereal and deli meat. On the other hand, fewer shoppers are purchasing alcoholic beverages, organic foods and frozen desserts. In the non-edible categories, paper products, laundry detergent and personal care items are the most popular among shoppers surveyed, consistent with last year. Flowers and plants, however, showed a significant decline, perhaps indicating a LIKELIHOOD OF

shift away from non-essential items. We also asked shoppers in what ways they’ve changed their shopper behaviours to cope with high grocery prices. About half (47%) reported buying reduced price or clearance items, while 40% are buying fewer impulse items and 32% are buying fewer groceries overall. Perhaps influenced by high prices, a growing number of shoppers (58%, up from 53%) also told us they plan to cook from scratch in the year ahead.

Private-label products are gaining in popularity with shoppers. According to our survey, more shoppers (53%, up from 48%) are reporting “always, or often” adding store-brand items to their baskets, with 38% “sometimes” doing so. Seventy-eight per cent of shoppers (up from 74% last year) say the main reason they’re purchasing private label is to save money. Other reasons given include the quality is similar to a name brand (52%), the store brand is better than the name brand (14%), and that their preferred name brand was out-of-stock so they grabbed a private label as a substitute (11%).

Despite employing tactics to save money, about half of shoppers surveyed (55%) say they are spending more on groceries versus last year, with 23% indicating they’re spending “a lot more.” Among women shoppers, that figure jumps to 27%. Thirty-two per cent of shoppers report to be spending “the same amount” of money on groceries, compared to the year prior, but in Quebec that figure jumps to 44%. Just 9% of shoppers report spending “a bit less.”

Amid a tariff tiff with our southern neighbour, the buy local movement has received a boost in the past year. According to our survey, among those shoppers who purchase local products, 33% say they are doing so more frequently (up from 25% a year ago). This figure jumps to 36% for women shoppers. For 65% of shoppers, the main reason for buying local is a desire to support local businesses, while 53% say they feel local products are of better quality.

WANING INTEREST IN PREPARED FOODS

In recent years, grocers invested heavily in prepared foods and consumers were eating them up. But shoppers’ appetite for these convenient foods is waning. According to our survey, fewer shoppers (62%, compared to 66% a year ago)

PREPARED FOODS

Shopper research

Purchases of prepared foods dipped versus last year, with shoppers citing costs and a preference for home cooking as main reasons

Prepared food shoppers are shifting away from sides, though entrees remain strong 43% of boomers and 47% of Quebec shoppers don’t buy prepared food

FOODS

Prepared entrees Baked

Boomers have the highest scores for food quality (66%) and freshness (67%)

Boomers (72%) and gen X (67%) have the highest scores

FLYING INSECT*

ATTRACTS & TRAPS FLYING INSECTS*

*fruit flies, drain flies, fungus gnats, mosquitoes and small moths

Winner of Insect Devices / Traps Category. Survey of 4,000 people by Kantar.

reported purchasing prepared foods at a grocery store at least once over the course of a month, and those shoppers are buying slightly less frequently (1.7 purchase occasions versus two a year ago).

Price is the main reason shoppers are turning away from prepared foods, with 48% reporting they’re too expensive. Other barriers to purchase include a preference to cook at home and dissatisfaction with the selection of prepared foods on offer.

Entrees are the most popular choice among shoppers who purchase prepared foods, with 62% adding them to their baskets. However, both hot and cold sides have taken a hit with significantly fewer shoppers (just 19% for cold sides, down 7 points and 15% purchasing hot sides, down 5 points) reaching for these items. Grab-and-go refrigerated foods are the most popular prepared foods format, purchased by 51% of prepared food shoppers, followed by made-to-order (28%) and a combination of both (21%).

As with other categories at the store, in these strained times, price and value are the most important considerations for shoppers—this is even more pronounced among boomers and gen-Xers—followed by quality, freshness and taste.

THE HEALTHY SHOPPER

Three-quarters (74%) of grocery shoppers in Canada identify as “health conscious”—among Quebecers and boomers this figure jumps to 87% and 79%, respectively.

Clearly, good health and well-being are important to Canadian shoppers, which is good news for grocers who have stepped up efforts in recent years to position themselves as a partner ready to help with health. However, the number of shoppers reporting being “very satisfied” with their grocer’s selection of better-for-you foods has declined significantly (34%, compared to 39% a year ago). The bulk of shoppers (59%) fall into the “somewhat satisfied” camp, suggesting there’s room for grocers to win over these important shoppers.

No surprise, health-minded shoppers

HEALTH AND WELLNESS

Shopper research

While most shoppers report being health-conscious, those indicating they are ‘very satisfied’ with the healthy options at the store have declined

74

OF SHOPPERS AGREE WITH THE STATEMENT: “I AM HEALTHCONSCIOUS”

Highest

are focused on product freshness, sugar, sodium, non-processed foods, fat and protein. Breaking it down by demographics, women shoppers (48%) reported being more concerned about freshness than males (39%), while boomers also reported higher than average concerns about sodium and ingredients they can understand and pronounce.

When asked what health-focused offerings/services were most important to them, an in-store pharmacy was named by 26% of shoppers, while 17% named healthy recipe cards at shelf. Other expanded offerings such as a healthcare app or healthy cooking classes declined in importance suggesting these offerings are no longer valued by shoppers. CG

Overview & Methodology

•Survey sample: 1,000 grocery shoppers

•Respondents were required to be age 18+, reside in Canada, shop at grocery stores at least once a month and are the primary or shared decision-maker for household grocery shopping

•Quotas were established to accurately represent the population distribution of Canada

Shoppers who purchase local indicate they are doing so more often

Boomers (49%) score highest for “always/often”

WINNER! VOTED BY CANADIANS PRODUCT OF THE YEAR*

PEOPLE’S CHOICE

Canadian consumers have spoken!

A national survey of 4,000 shoppers conducted by Kantar has revealed the 40 products earning the 2026 Product of the Year Canada red seal.

The program, which operates in more than 45 countries, recognizes and rewards manufacturers for quality and innovation.

“Against a backdrop of rapid retail transformation, including more immersive experiences and a heightened focus on sustainability and ethical choices, the Product of the Year Seal serves as a meaningful mark of credibility,” says Mike Nolan, global CEO of Product of the Year Management. “The 2026 winners represent what Canadians value most today: reliable performance, solutions that make everyday life easier, and products that offer genuine value while helping shape the future of retail.”

From quick-and-easy meal solutions to protein-packed snacks, functional beverages and a celebrity brand collaboration, here’s a look at this year’s winners:

BETTER-FORYOU DRINKS

Loop Pro + Prebiotic Fresh Fruit Sodas

LOOP MISSION

These functional beverages are made using rescued fresh fruits and deliver active probiotics and five grams of prebiotic fibre to support gut health.

CANDY

APPS & SNACKS

Western Family Feta & Caramelized Onion Bites

PATTISON FOOD GROUP

An elevated app: Flaky, golden puff pastry with a buttery base, topped with caramelized onions and tangy feta—made with no artificial colours or flavours.

BETTER-FOR-YOU

YOGURT

Activia Expert

DANONE CANADA

Prepared in Canada and designed for gut health, each 115-gram serving delivers billions of active probiotics plus prebiotics and seven grams of protein. Made without the use of gelatin.

Starburst All Pink Gummies

MARS WRIGLEY CANADA

The popular chewy Starburst strawberry candy is now available in a gummy format and made with real fruit juice.

Product of the Year

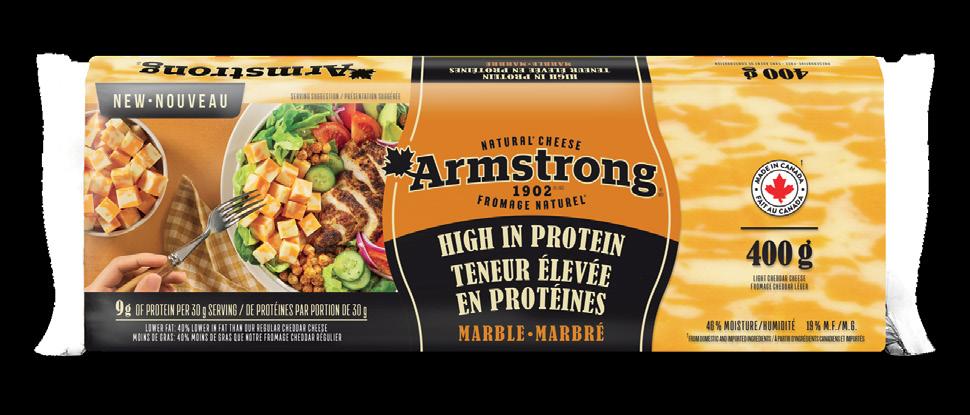

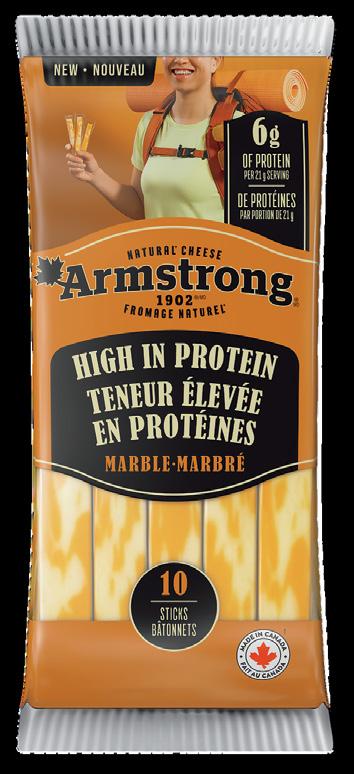

CHEESE Armstrong High in Protein Marble Cheddar Cheese

SAPUTO DAIRY

PRODUCTS CANADA

High-protein, low-fat and made in Canada, this natural cheese comes in sticks, shredded and block formats to help consumers boost protein intake.

CHOCOLATE BARS

KitKat Chunky Rolo NESTLÉ CANADA

Crispy wafers layered with creamy Rolo caramel and covered in a thick chocolate coating. Made with 100% sustainably sourced cocoa.

CHOCOLATEY COOKIES

Cadbury Fingers

MONDELĒZ CANADA

Ideal for dipping in a cup of coffee or tea, Cadbury Fingers are bitesized crunchy biscuits with a rich chocolatey coating.

CONDIMENTS

Heinz Mayonnaise-style Sauce

KRAFT HEINZ

Not just a spread, Heinz is creating new usage occasions with mayonnaise-style dips in Mango Habanero and Pickle, delivering a rich, creamy texture made for dipping.

ENERGY SNACKS

Go Pure Energy Ball in a Bar

BISCUITS LECLERC

Made with dark chocolate, 100% Canadian oats, dates and quinoa, each bar contains six grams of whole grains and no artificial flavours or colours.

FROZEN DESSERTS

7-Select Cookies & Cream Ice Cream

7-ELEVEN CANADA

A creamy, smooth and rich base mixed with crunchy cookie bits provides a satisfying dessert experience.

INDULGENT TREATS