MONEY MOVES FOR MODERN GIRLS

INTRODUCTION

This booklet is your guide to starting your own investment journey. Inside, you'll find an introduction to investments, an overview of different types of investments, my personal investment journey, reasons why you should invest, tools to help you get started, and additional cited information for further research.

DISCLAIMER

I am not a professional investor and have limited knowledge in this field. In fact, I am a beginner myself! However, I believe everyone should have a basic understanding of investing and stocks and shares ISAs, even if it’s just a little. Let’s get comfortable being uncomfortable when it comes to investing.

WHY YOU SHOULD INVEST

A quick Google search will reveal numerous

Additionally, I wanted to spend without

WHY I HAVE CREATED THIS BOOKLET

I created this specifically for the women in my life. While men are not excluded and are encouraged to benefit from this information as well, the current economic climate highlights the urgent need to address the gender financial gap. Women

Empowering women with equal financial power as men can statistically boost the global economy and contribute to a more sustainable future for ourselves, our children, and future generations. For example, improving gender equality could increase the EU’s GDP per capita by 6.1 to 9.6% by 2050, amounting to €1.95 to €3.15 trillion, according to the European Institute for Gender Equality.

Feel free to scroll to the bottom of this booklet for all my sources and additional information. It’s important to educate yourself whenever you feel inspired to do so!

WE ARE LITERALLY GOING THROUGH A COST OF LIVING CRISIS?

This might seem like an unusual time to start investing, given the global economic decline and the cost-of-living crisis we’re facing. However, despite these challenges, the market typically grows by 7-10% each year.

While saving is important for creating a financial cushion, investing offers the potential for greater financial growth and long-term security.

Investing is key to building long-term wealth and achieving financial independence. We deserve to at least have the opportunity to understand this and that’s why I want to create this opportunity and hopefully learn, myself, from you along the way.

WHERE AND WHEN TO INVEST

It’s never too late to start investing, and your approach will depend on your personal circumstances. I’m not suggesting you invest all your paycheck or savings right away; you can begin with as little as £100.

First, assess your situation.

• Do you have any debts?

• Are you currently managing your expenses comfortably?

• Can you cut back on non-essential spending to save for your future?

Once you’ve addressed these factors, evaluate how much risk you’re willing to take with your investments. Consider your time horizon, age, and financial goals.

(Remember, it’s important to enjoy life and not deny yourself small pleasures!)

If you’re financially involved with a partner, discuss your plans with them if you feel comfortable. It’s important to communicate and make these opportunities available to yourself if that’s what you want.

A TIME HORIZON

In investing, a time horizon refers to the length of time you expect to hold an investment before needing to access the funds. It’s a crucial factor in determining the appropriate investment strategy for your needs.

HERE IS HOW IT WORKS

• Short-Term Horizon: If you plan to access your money within the next few years (e.g., 1-3 years), you might opt for lower-risk investments, such as savings accounts or short-term bonds, to preserve your capital.

• Medium-Term Horizon: For a time frame of 3-10 years, you might consider a mix of stocks and bonds. This period allows for a balance between growth and risk, as you have time to recover from potential market fluctuations.

• Long-Term Horizon: If you’re investing for goals 10 years or more in the future, you can typically afford to take on more risk, such as investing in stocks or real estate, with the potential for higher returns. Over a long period, the market has time to recover from volatility, which can benefit long-term investors. Your time horizon helps determine how aggressive or conservative your investment strategy should be.

EXAMPLES

An example of your potential financial goals can vary widely based on individual circumstances and aspirations.

Any goal requires a different approach and timeline, which will influence your investment strategy and financial planning.

It’s also how it makes you feel, each of your investments should make you excited for your future or your community, we are human, and it is ridiculous to look at this without adding emotion because that doesn’t work. (Especially for a women like me, I need to work with my emotions and certainly not against them!)

Emergency Fund: Save enough to cover 3-6 months of living expenses to protect against unexpected events, such as job loss or medical emergencies.

Debt Repayment: Pay off high-interest debt, such as credit card balances or student loans, to reduce financial stress and improve credit health.

Home Purchase: Save for a down payment on a house. This might involve building a substantial savings fund over several years.

Retirement: Accumulate a certain amount of savings or investments to ensure a comfortable retirement. Goals might include reaching a specific retirement savings target or achieving a desired monthly income in retirement. (Including private pensions and current investments you make today in a stocks and share isas!)

Major Purchase: Plan and save for a significant purchase, such as a new car, or long-term travelling.

Investment Growth: Build a portfolio with a target growth rate or value, aiming to achieve specific financial milestones or wealth accumulation over time.

Charitable Giving: Set aside funds to donate to causes or organizations that are important to you.

WHERE TO INVEST

With the timing established, let’s turn our attention to the “where” of investing. There are various investment options available, including commodities, real estate, luxury items, stocks, bonds, savings accounts, cryptocurrencies, ETFs, index funds, and more.

Since I’m still exploring each of these options, I’ll keep things simple and focus on the investments I’m currently engaged with: savings accounts and ISAs.

SAVING ACCOUNTS

When selecting a savings account, it’s important to consider factors such as interest rates, accessibility, and account requirements. Some accounts may not offer immediate access to your funds, so if you need an emergency fund, prioritize accounts that allow quick access.

Regular Saver Accounts typically offer the highest interest rates but often require consistent monthly deposits.

For example, I have two savings accounts: one with a lower Annual Equivalent Rate (AER) but instant access, and another with a slightly higher rate that requires a one working day notice for withdrawals. If you have a MONZO current account, their savings pot is easily accessible and a great option for beginners.

Take advantage of current account offers and review your accounts frequently to ensure you get the best returns. Some current accounts provide high introductory interest rates or cashback rewards. For instance, the Nationwide FlexDirect Account offers 5.00% AER on balances up to £1,500 for the first 12 months. Since interest rates and account benefits change regularly, it’s wise to review your accounts periodically and switch to better options as they become available. Websites like MoneySuperMarket and MoneyFacts can help you compare the latest offers.

STOCKS AND SHARES ISAS

Remember, compound interest is your best ally when investing in stocks. For beginners (like me!), it’s crucial to keep this in mind, especially when your stock is performing poorly. Investing can be complex, but don’t let that intimidate you. The key to becoming comfortable is viewing investment as a longterm endeavor, where compound interest helps you understand why we invest.

Compound interest in stocks and shares means the value of your investment grows over time as the earnings generate additional earnings. Simply put, the longer you’re in the market, the more likely you’ll earn higher returns.

When considering compound interest, think about dividends and capital gains, which vary depending on your investments.

Example of Compound Interest with Stocks

Imagine you invest £1,000 in a stock that pays an annual dividend of 5%. Instead of taking the dividend as cash, you reinvest it to buy more shares. Here’s a simplified example of how the investment compounds over a few years:

Year 1: You earn £50 in dividends, bringing the total to £1,050.

Year 2: You earn 5% on £1,050, which is £52.50, bringing the total to £1,102.50.

Year 3: You earn 5% on £1,102.50, which is £55.13, bringing the total to £1,157.63.

As you can see, each year the amount of dividend earned increases because it is calculated on an ever-growing base.

Consider your time horizon and market volatility. Remember, it’s about time in the market, not timing the market!

WHERE TO INVEST

When it comes to a Stocks and Shares

ISA, you have a couple of options: you can either have it managed by a professional or manage it yourself.

This choice depends on how much time and effort you want to invest in researching and handling your investments. If you’re interested in starting but aren’t comfortable managing it on your own, many UK banks offer managed options.

For example, MONZO provides a managed stocks and shares option (this is just an example from my personal experience, so I encourage you to explore other banks to find what suits you best). You can visit their website for more information on how they handle investments on your behalf.

In the next section, I’ll discuss my specific self-managed investments, which are still suitable for beginners.

InvestEngine is a user-friendly, commissionfree platform for investing in ETFs (Exchange-Traded Funds), suitable for both individuals and small businesses.

It’s the platform I personally use for my investments. With InvestEngine, you have the option to create a self-managed portfolio and choose specific ETFs to invest in.

I have a referral code for InvestEngine. This isn’t about making money off you, but if you’d like to use it, we could both potentially get up to £50 to invest in our portfolios. No pressure at all—just an option if you’re interested.

HOW DOES AN ETF COMPARE TO A STOCK?

An ETF is an investment fund that holds a collection of assets, such as stocks, bonds, or commodities. When you buy shares in an ETF, you’re purchasing a small portion of the entire portfolio of assets that the ETF holds, allowing you to diversify your investment across multiple assets with a single purchase.

In contrast, a stock represents ownership in a specific company. When you buy a stock, you are acquiring a share of that particular company, making you a partial owner. The value of your investment is directly tied to the performance of that single company.

In summary:

ETF: Provides diversification by holding multiple assets within a single fund.

Stock: Represents ownership in a single company. Both options come with their own benefits and risks, and the right choice depends on your investment goals and risk tolerance.

WHY SHOULD BEGINNERS CONSIDER INVESTING IN ETFS?

ETFs are an excellent way to maintain a diverse portfolio. For example, you can invest in the top 100 companies worldwide and emerging markets simultaneously, spreading your risk across various assets. This diversification reduces the risk compared to investing in a single company.

However, ETFs are still subject to factors that affect individual stocks, such as political events and the global economic environment. It’s important to stay informed and continue learning as you invest.

MY PORTFOLIO

WHAT I PERSONALLY INVESTED IN

If you’re still unsure but eager to start investing and want to use the platform I recommend, you can check out my simple portfolio below. I’ve invested in three main ETFs which are over the next 3 pages.

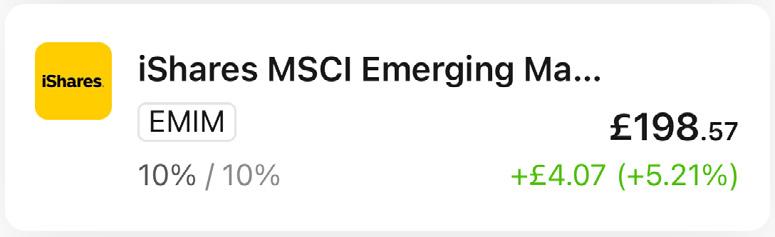

To easily find these ETFs, you can search for them using their specific four-letter codes: VHVG, SPXP, and EMIM.

Vanguard FTSE Developed World (VHVG) - (65%)

Overview: This ETF gives you exposure to a broad range of companies in developed markets across North America, Europe, and Asia-Pacific, excluding emerging markets.

Key Features:

Diversification: Invests in hundreds of companies from various developed countries.

Stability: Focuses on established markets, which are generally more stable.

Sector Variety: Covers different sectors like technology, finance, healthcare, and consumer goods.

Invesco S&P 500 (SPXP) - (25%)

Overview: This ETF tracks the S&P 500 Index, representing 500 of the largest publicly traded companies in the U.S.

Key Features:

U.S. Market Focus: Invests in major U.S. companies across various industries.

Blue-Chip Stocks: Includes well-known, large companies like Apple, Microsoft, and Amazon.

Growth Potential: Historically strong performance reflecting the U.S. economy.

iShares MSCI Emerging Markets (EMIM) - (10%)

Overview: This ETF provides exposure to companies in emerging markets such as China, India, Brazil, and South Africa.

Key Features:

Emerging Markets Focus: Invests in rapidly growing economies.

Higher Risk, Higher Reward: Offers potential for significant growth, but with more volatility.

Diversification: Covers various industries in emerging economies, including technology, finance, and energy.

Now that we’ve covered the essential information, let’s focus on some key principles to keep in mind when investing. I’ve pulled together six important rules from Girls Just Want to Have Funds to guide you:

1. Invest Gradually

Approach: Instead of investing a large sum all at once, consider investing smaller amounts over time. This strategy helps you manage risk and take advantage of market fluctuations.

2. Diversify Your Portfolio

Strategy: Diversification is crucial for reducing risk. A simple way to achieve this is by investing in broad-based funds like the S&P 500, which includes a wide range of companies across different sectors. This approach helps spread your risk and can lead to more stable returns.

3. Do Your Research

Importance: Always take the time to understand what you’re investing in. Research the companies, funds, or assets you’re considering, and stay informed about market trends and economic factors that might affect your investments.

4. Deciding When to Sell

Guidance: There’s no perfect formula for knowing when to sell an investment. If you’re investing for the long term, set a target date or goal for selling. This can help you avoid making emotional decisions driven by fear or greed.

Time Horizon: Determine your investment horizon and make decisions based on your long-term objectives rather than short-term market movements.

5. Use Stop Losses

Protection: If you’re concerned about losing too much, consider setting a stop loss order. This automatically sells your investment if it falls below a certain price, limiting your potential losses.

Trailing Stop Loss: A trailing stop loss adjusts with the price movement of your investment and is triggered when the price drops by a certain percentage. This helps lock in gains while protecting against significant losses.

Last but not least!

6. Understand When to Sell

Considerations: Selling can be challenging, and it’s important to know when it might be appropriate.

Significant Loss: If the value of your investment drops significantly and you believe it won’t recover.

Time Period: If it’s time to review and rebalance your portfolio.

Overexposure: If a particular stock or asset makes up a large portion of your portfolio, you might consider selling some to reduce risk.

Discomfort: If you no longer feel confident about the company or investment.

Take Your Time

Patience: Investing is a learning process. If you’re unsure about a particular investment, take your time to educate yourself. Make informed decisions rather than rushing or gambling with your money.

Acknowledge Losses

Perspective: Losses are a natural part of investing. They can be opportunities to learn and refine your strategy. However, avoid putting all your money into a single investment; diversification helps mitigate risk.

By following these guidelines, you’ll be better equipped to navigate the investment landscape with confidence and make informed decisions.

AN EXAMPLE OF LONG TERM GROWTH

Assumptions:

Initial Investment: £10,000

Annual Return Rate: 7% (average annual return, which is typical for a diversified stock market investment over the long term)

Investment Period: 30 years

No Additional Contributions: This example doesn’t include any additional investments or withdrawals during the 30 years.

Key Points:

Compound Growth: The growth of investments benefits from compounding, where you earn returns not only on your initial investment but also on the returns that accumulate over time.

Time Horizon: The longer you invest, the more pronounced the effects of compounding become. A 30-year period demonstrates how even a modest annual return can lead to significant growth over time.

Risk and Return: A 7% return is an average figure and might include a range of investments like stocks, bonds, or ETFs. Actual returns can vary based on market conditions and investment choices.

Illustration:

Year 1: £10,000 grows to £10,700

Year 5: £10,000 grows to approximately £14,025

Year 10: £10,000 grows to approximately £19,672

Year 20: £10,000 grows to approximately £38,697

Year 30: £10,000 grows to approximately £76,123

This example highlights the power of long-term investing and the impact of compounding returns over a 30-year horizon. So even if you think it won’t do much, it will!

OTHER ISAS YOU NEED TO THINK ABOUT

As a quick overview at the end of this booklet, if the Stocks and Shares ISA doesn’t seem right for you, there are other types of ISAs to consider.

Remember, there’s no pressure to invest if you’re not ready. However, it’s worth thinking about your future financial goals, as planning ahead can be very beneficial. Believe in yourself and your potential to make smart financial choices—even if you’re not quite sure yet, I believe in you!

YOUR PENSION!

No matter how you invest, always keep your future self in mind! It’s not just about making it through retirement; it’s about continuing to live well.

Make sure to consolidate your pensions from all employers, stay on top of them, and invest when possible (Look in your contract as most employers will pay more when you have a long service with them!). This could mean contributing extra voluntarily or investing with a long-term perspective in mind!

GLOSSARY

AER (Annual Equivalent Rate):

The annual rate of interest that is paid on savings or investments, representing what the interest would be if it were compounded and paid annually.

Blue-Chip Stocks:

Shares of well-established, financially sound companies with a history of reliable performance and often included in major market indexes like the S&P 500.

Bonds:

Debt securities issued by companies or governments to raise capital, where the issuer agrees to pay back the principal amount on a specified date along with periodic interest payments.

Capital Gains:

The profit realized when an asset is sold for more than its purchase price.

Compound Interest:

Interest calculated on the initial principal, which also includes all of the accumulated interest from previous periods on a deposit or loan.

Debts:

Money that is owed or due to be paid to another party, typically involving interest payments.

Diversification:

A risk management strategy that mixes a wide variety of investments within a portfolio to minimize risk.

Dividends:

Payments made by a corporation to its shareholders, usually as a distribution of profits.

Emergency Fund:

Savings set aside to cover unexpected financial emergencies, typically amounting to 3-6 months of living expenses.

ETF (Exchange-Traded Fund):

A type of investment fund that is traded on stock exchanges, much like stocks, and holds assets such as stocks, commodities, or bonds.

Financial Freedom:

The status of having enough income to pay for one’s living expenses for the rest of their life without having to be employed or dependent on others.

Gender Financial Gap:

The disparity in financial opportunities, wealth accumulation, and investment between genders, often leading to economic disadvantages for women.

Interest Rates:

The percentage of a sum of money charged for its use, typically expressed as an annual percentage of the principal amount.

ISA (Individual Savings Account):

A tax-efficient savings or investment account available to residents in the UK, allowing a certain amount of savings to grow tax-free each year.

Portfolio:

A range of investments held by an individual or institution, including stocks, bonds, ETFs, and other assets.

Managed Portfolio:

A collection of investments that is overseen by a professional investment manager, often on behalf of an individual or institution.

Savings Account:

A bank account that earns interest over time and is used primarily for saving money.

S&P 500 Index:

A stock market index tracking the stock performance of 500 large companies listed on stock exchanges in the United States.

Stocks:

Securities that represent ownership in a corporation and a claim on part of the corporation’s assets and earnings.

Stop Loss:

An order placed with a broker to buy or sell a specific stock once it reaches a certain price, designed to limit an investor’s loss on a security position. (Putting these in place will make sure you don’t lose everything if you’re taking a bigger risk)

Time Horizon:

The expected number of years an investment will be held before it is liquidated, influencing the type of investments an individual should consider.

Volatility:

The degree of variation in the price of a financial instrument over time, often used as a measure of risk.

Thank you so much for taking the time to read through this! I hope it has inspired and educated you. If you’re already on your investment journey, feel free to share this with friends who might find it helpful. And if you’re just starting out, don’t hesitate to reach out with any questions. I’m here to learn alongside you and am happy to share any insights I have.

Let’s get comfortable talking about money, ladies!