Born + raised in Golden, CO, Emily Breaker has spent her entire life in this beautiful state of Colorado - why would she ever want to leave?? Throughout her career, Emily has maintained a high attention to detail, handling a high volume of multi-million dollar transactions. She has indepth knowledge of short-term rental investment and management, and helps her partner in his fixand-flip business, giving her expertise in offmarket/wholesale and the renovation processes In just 3 short years Emily has surpassed many of her peers in terms of volume and expertise and can’t wait to continue to fine-tune her craft and provide top-notch service and experience for her buyers and sellers alike.. Her experience, combined with Emily's communication, listening, time management, and dedication, makes Emily the perfect person to help you make your real estate dreams come true.

Stats

Emily Breaker BROKER ASSOCIATE

Meet the Team

Emily Breaker Camille Sheppard Taylor Whitton Kassidy Benson

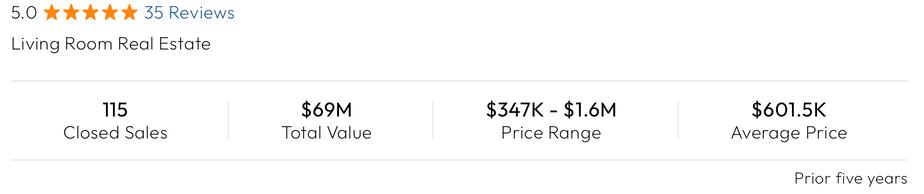

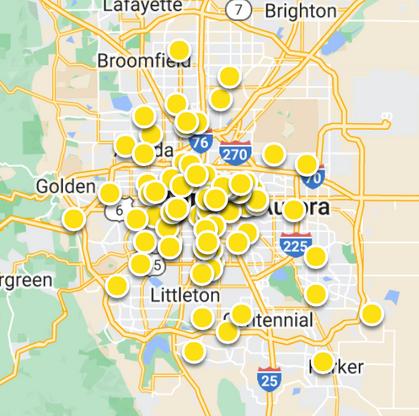

Our mission is to pair people with the right place for a prosperous life. Living Room Real Estate is a boutique Denver brokerage founded in 2019 We are 100% dedicated to helping our clients find their happy place while also building wealth We believe all real estate is an investment and every buyer has the opportunity to make a great one. As a millennial owned and operated company, we provide the keys to the largest generation of home buyers and help sellers properly reach this audience. We are socially conscious, digital natives, information-centric, and socially networked. We've also created a niche in Accessory Dwelling Units (ADU)specializing in helping clients understand and purchase homes zoned for a secondary unit on the property for income opportunities

Every Closing Matters

The Park People work to preserve, enhance, and advocate for Denver's parks, recreation resources, open space and urban forest. We partner with them to plant trees throughout Denver each year. For each house we sell we donate a tree.

TESTIMONIALS

Words from some of my happy clients.

"Working with Emily was great, her professionalism, integrity, and genuine care for her clients in every interaction. I would recommend Emily to anyone in need of a topnotch real estate agent She deserves every bit of my five-star review and more!Vladimer

From the initial consultation to the closing of the deal, we had an extremely positive experience working with Emily. She went above and beyond to advocate for our best interests and leveraged her local expertise to find us our dream home in Golden We were in a very competitive bidding situation and Emily's knowledge of the Golden market put us in a position to be the winning offer and get into the exact home we wanted Emily's professionalism, attention to detail, and passion for real estate (especially the golden market) make her an excellent realtor. Highly recommend!

-Nick & Zoe

Emily was hands down the best realtor I've ever worked with Not only did she listen and find me the perfect house, but she was diligent in protecting me during the negotiations and she supported all my requests. She answered my questions immediately and was just a great person. She made this easy!

-Anne

EI had such a great experience working with Emily The sale of my house was unconventional and required a lot of attention and focus I don’t think I would have been able to do it without her! She went above and beyond for me, from staging to checking in even during times where we didn’t have urgent updates I will, without a doubt work with her when I purchase my next home!

-Megan

TESTIMONIALS Words from some of my happy clients.

No nonsense and professional.

Definitely would hire Emily again!

Ken and Tammy

Whether you’re buying or selling a home it’s stressful, but not with Emily! My husband and I recently needed to sell my grandparents homestead in eastern Colorado. Very unique property, outdated home but with 5 acres so it was difficult to compare with similar properties. She was extremely knowledgeable about the Colorado Market and even brought market specific analytics to review! Emily provided great information for pricing, and when it was time to post the property we had 18 showings in 3-4 days. An absolute breeze with Emily at the helm! This also included her being in Germany for a wedding and still keeping up with constant communication and managing situations with the buyers realtors! Sold in less than a week with 5 offers! You need a good local realtor, please look up Emily!! e-Angel

My husband and I just purchased our first home together after getting married last year with Emily as our realtor, and we're so happy we did.

As first time home buyers, navigating the real estate/ home buying world & market is HARD. Emily did a fantastic job at making it as easy as possible for us - being a very clear communicator, excellent at keeping us informed with deadlines, etc. She is professional and a joy to work with. Her knowledge of this market and her experience is clear to see. She is prompt, timely, and attentive to our needs and wishes. She was able to pinpoint exactly what we would need in order to save as much money as possible and get the most value for what we were paying for. She has great connections as a professional too - everyone from an arborist to a roofer to a plumber and everything in between. Don't hesitate to utilize Emily for your real estate service needs - you won't be sorry you did!

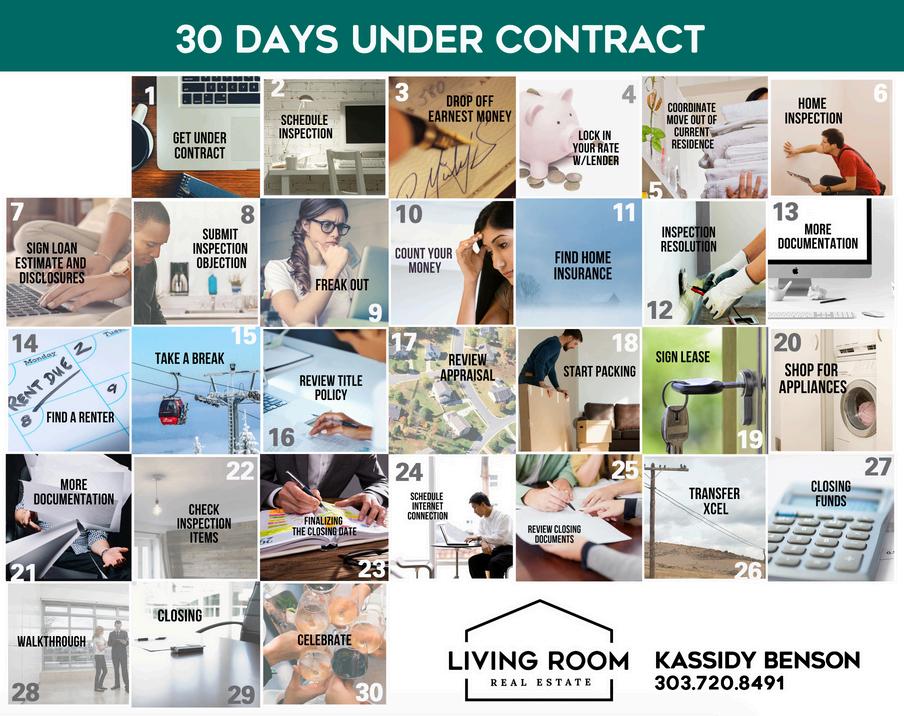

The home buying process is different for everyone Once we submit an offer and it is accepted, here is a realistic look at the timeline of most home sales Typically a buyer has a 30 day due diligence period we call “being under contract”. This allows you time to learn as much as possible about the home and obtain financing before you make the big commitment of purchasing your new home.

PART 2: FINANCES

Working with a Great Lender

Before you begin your home search, I recommend talking to a few lender to have a solid grasp of your budget and get fully underwritten. A lender will be able to answer all of your questions regarding down payment options, closing costs and give you a clear understanding of what you can afford and an estimate of the expenses to expect.

QUESTIONS

TO ASK WHEN INTERVIEWING POTENTIAL LENDERS...

What is the best type of loan for me?

Do I qualify for any special discounts or loan programs?

What interest rate will I get based on my scenario?

Are there options to lower my interest rate?

What fees do you charge as a lender?

How much would you estimate for my closing costs?

FINANCES

Getting your pre-approval

There a many different factors that the lender will use to calculate your pre-approval It's always best to be prepared, so here are a few of the documents you can begin to gather together and can expect to be requested:

In response to the 2024 $418M National Association of Realtors settlement, buyer agent commissions will no longer be advertised nor necessarily seller-funded. To comply, buyer’s agents must secure a buyer’s representation agreement prior to home showings. We commit to transparently negotiating commissions with all parties. Our policy encourages sellers to provide a 2.8% buyer representation fee, but if this is not feasible, buyers will commit to a minimum fee of $10K, which can be included in their loan This fee supports our dedicated service in guiding buyers through one of their most significant financial decisions. We remain focused on delivering exceptional service as we adapt to these industry shifts.

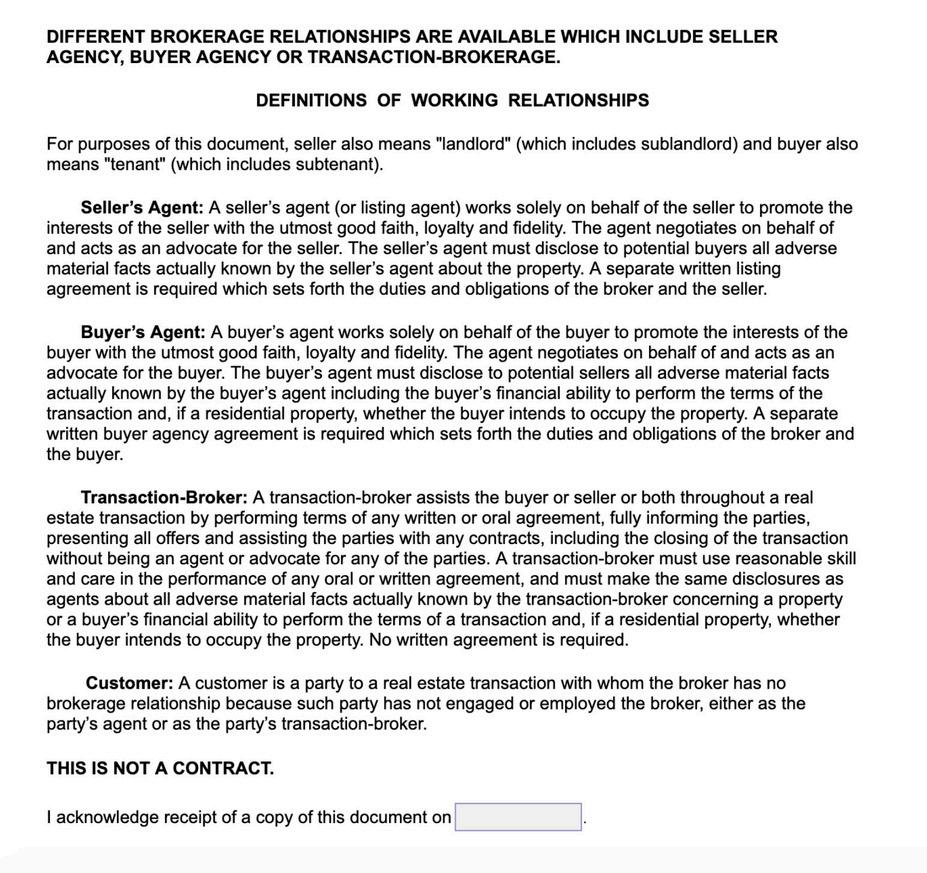

This is a standard form defining the ways you can work with a real estate agent to purchase a home. I'm legally required to disclose this information by state regulatory agencies. I would like to represent you as your "buyers agent".

Due to the recent changes In the Real Estate Industry, all Buyers Agents must have this signed before showing properties in order for me to represent you. I will send you the “Exclusive Right to Buy” prior to touring houses.

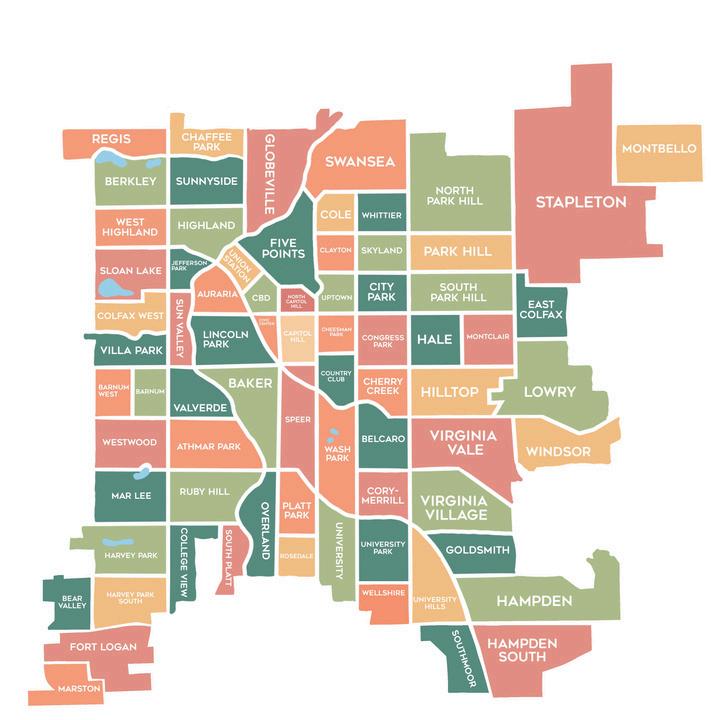

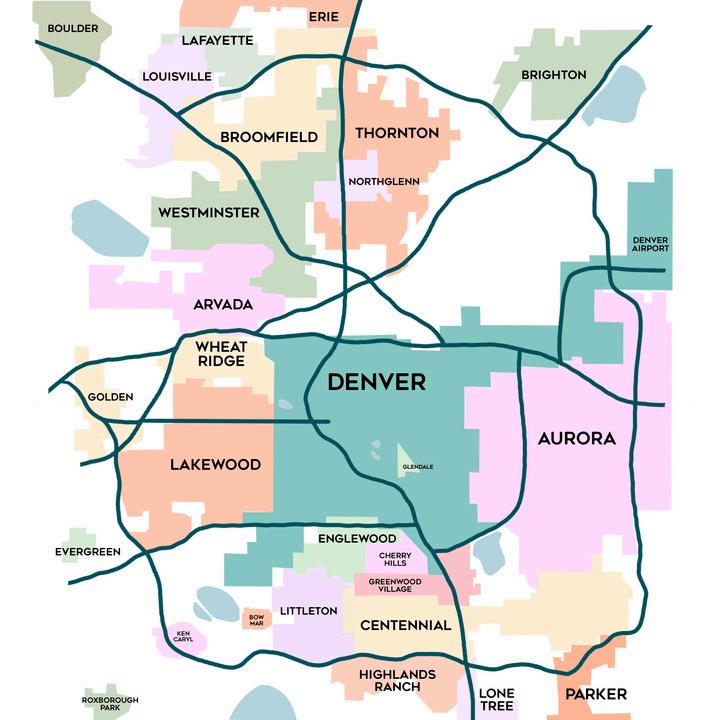

DENVER NEIGHBORHOODS

Denver has many unique neighborhoods that are sought after When starting your home search, it is best to identify the style of house you are looking for as well as the lifestyle you want to live.

Do you want to be able to walk to the store?

Do you need to be close to the bus or train?

Are you needing high performing schools and a kid friendly neighborhood?

Do you want to make an investment in an up and coming neighborhood?

Those are all things we will consider and we will help you navigate when starting your home search with Living Room.

STYLES OF HOMES

When looking at different neighborhoods in Denver some are well establshed with schools and parks. Other places in the city have less stability, yet offer more potential for growth on your investment. When considering your lifestyle and your goals take this into consideration,

Examples of Single Family Homes in Denver/Suburbs

Examples of Attached homes in Denver/Suburbs

Wants & Needs List

Ready to start home shopping? Fill out the form below so I can set you up to start receiving homes that meet your requirements.

NEEDS: WANTS:

brainstorming..

HOMETYPES

MUSTHAVES

ARCHITECTURAL

STYLES

FINISHES

ASPIRATION HOMES

LAYOUT

ROOM USAGE

5YEARPLAN SHOWINGAVAILABILTY

M T W T F S S

OFFERS & NEGOTIATIONS

Contingencies - Due Diligence Deadlines

Earnest money

Seller’s Property Disclosure

Due Diligence Docsenergy bills, permits, etc

Lead Based Paint Disclosure

Loan Terms

Title Insurance Objection

HOA Objection

Survey/ ILC / Mineral / Water Rights

Home Inspection

Property Insurance

Appraisal

Conditional Sale

Loan Availability

Multiple Offer Situations

Some homes go into multiple offer situations. This means that your offer is not the only offer on the table for the sellers Here are some strategies to win a multiple offer situation

Submit your Pre-Approval letter with your offer

Have your lender call the listing agent to share your Pre-Approval details

Make a cash offer if possible - higher down payments more favorable

Offer more than the asking price

Be flexible with your closing date - fast close and rent back

More earnest money and/or non-refundable deposit indicates your serious

Remove contingencies and don't ask for any that are not a deal-breaker

Add a personal letter and a photo of you and your family

Earnest Money Deposit

If your offer is accepted, the next step is to turn in your earnest money deposit at the title company. Normally the seller asks for 1-2% of the purchase price but it is negotiable and depends on the amount of money you have on hand. Your earnest money is REFUNDABLE if you terminate within the contigencies.

INSPECTION PERIOD

Thetypicalinspectionperiodisbetween10-7days.

Types of Potential Inspections

Home Inspection

Radon Testing

Asbestos

Structural Inspection

HVAC Inspection

Mold Inspection

Lead Based Paint Inspection

Recommended Home Inspectors

We have a list of our favorite inspectors we trust. Once we are under contract, I will help schedule professionals to come inspect the property. We also have great contacts for reliable contractors who can provide estimates for any repairs we identify. Cost: $500-$1000

Inspection Objection

Before we write the inspection objection, we will need to review all the inspection reports and repair quotes. We will then make a clear and concise list of everything you’d like the seller to repair or credit you before closing.

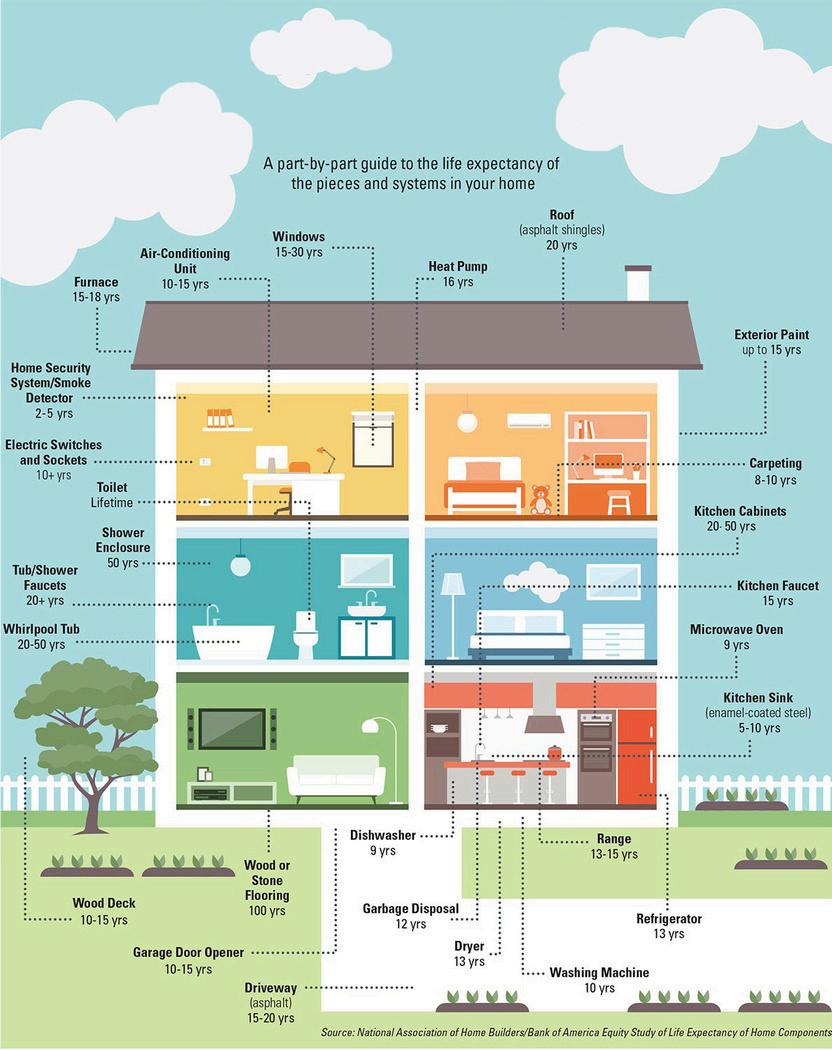

COMMON LIFE EXPECTANCY OF HOUSEHOLD ITEMS

FINDING YOUR HOME APPRASIAL

A home appraisal is needed if you are financing your home. It is required by the bank to estimate the home value.

Just because you and the seller agreed to a price, doesn't mean that the bank will.

After all, the home is their collateral in case you can't make your mortgage payment. The bank can then foreclose on you and resell the home.

If the home is appraised over the contract price, the seller will need to either come down in price, or you will have the choice to make up the difference with cash, or you may back out of the deal.

An appraisal is a good thing for a buyer overall. It will keep you from falling into a bad deal and overpaying.

AN APPRAISAL GAP IS THE DIFFERENCE BETWEEN THE APPRAISED VALUE OF A PROPERTY AND THE PURCHASE PRICE AGREED UPON BY THE BUYER AND SELLER, IN A COMPETITIVE OFFER SITUATION A BUYER MAY WANT TO INCLUDE AN APPRAISAL GAP CLAUSE IN THEIR OFFER TO REASSURE THE SELLER THAT THEY WILL COVER THE DIFFERENCE IF THE APPRAISAL IS LOWER THAN THE AGREED PRICE, THUS PREVENTING THE DEAL FROM FALLING THROUGH

PREPARING FOR CLOSING

Buying Your Home

01.

Loan Application & Appraisal

You will typically have 3-5 days after the contract has been executed to make application for your loan with your lender. The appraisal will be ordered by your lender after we have made our way through the inspection period. If your contract is contingent on the appraisal, this means that if the appraisal comes back lower than the offer you made, we will have an opportunity to negotiate the price once again.

02.

Home Insurance

You will need to obtain a Homeowner's Insurance Policy that will begin on the day of closing on your home. If you don't already have an insurance company you plan to work with, please feel free to reach out to me and I will be more than happy to provide you with a list of recommendations.

03.

Important Reminder

As excited as you may be to begin shopping around for furniture and all of the things that help make a house a home, don't! Be very careful during this period not to make any major purchases, open new lines of credit, or change jobs. If in doubt, be sure to call your Real Estate Agent or Lender.

Clear To Close

These words are music to my ears, and yours too! This means that that mortgage underwriter has approved you loan documents and we can confirm your closing date with the title company or attorney. 04.

"Owning a home is the cornerstone of building wealth, with homeowners having a median net worth 40 times greater than renters. Home values steadily appreciate, providing equity and financial security, while also enhancing stability and well-being. Embrace this journey for a solid foundation in both your financial and personal life."

notes:

HOME BUYING & FINANCING GLOSSARY

Home Buying Glossary

APPRAISAL

An appraisal is a written estimate of the value of something. In real estate, it is a professional opinion on behalf of the bank of the market value of property 99% of the time appraisals come in at the same value as the purchase price

ASSESSMENT

An assessment is a value assigned to real property (your house and land) that is used to determine real property taxes. Assessment can also refer to the process of reaching an assessed value of real property

CLOSING

In real estate, closing is the delivery of a deed, financial adjustments, the signing of a note, and the disbursement of the funds necessary to consummate, or close, the sale or loan transaction “Settlement” is another term for closing

DEED

This document shows that an owner of a piece of real property has title to that property Once a deed is filed and recorded by your local government, the deed becomes a public record

EARNEST MONEY

Earnest money is a deposit you pay to the seller of real property to show your good faith and intentions of getting a mortgage to buy the property It is refundable until loan termination if you decide not to complete the purchase

ESCROW

Escrow is money placed with a third party (title company) for “safekeeping” During a real estate purchase, the buyer is typically required to place a portion of their down payment aka Earnest Money in an escrow account where it is held until the closing. After the home is purchased, a portion of each mortgage payment is typically held in an “escrow” account to pay for the property’s taxes and insurance

HOME INSURANCE

Insurancecoveragethatprovidescompensationto theinsuredincaseofpropertylossordamage Your homeinsurancewillbepaidwithyourmonthly mortgagepayment

A contract by which the insurer agrees to pay the insured a specific amount for any loss caused by defects of title to real estate wherein the insured has an interest Homebuyers usually must purchase lender’s title insurance to protect the lender’s interest and sellers traditionally purchase buyer’s title insurance and choose the title company.

Financing Glossary

ADJUSTABLE-RATE MORTGAGE (ARM)

An ARM will have interest rates and payments that change from time-to-time over the life of the loan Depending on the type of ARM you have, your interest rate may increase gradually every few years until it reaches a preset ceiling

AMORTIZATION

Amortization is the process of paying off a loan through a series of periodic payments to a lender The payments include two items: interest, which is what it costs you to borrow the money, and principal, which is the amount of money you borrowed.

ANNUAL PERCENTAGE RATE (APR)

The APR, shown on your mortgage papers, is a standardized way of showing you the total cost of borrowing money The APR is a combination of the interest rate charged by the creditor along with any fees they might charge.

CONVENTIONAL LOAN

A loan that is not guaranteed or insured by a government agency

CREDIT LIMIT

Your credit limit is the maximum amount of money that can be loaned to you or the maximum amount of credit you can use in an open-ended credit account.

DISCOUNT POINT

A discount point is an amount of money a borrower pays to a lender, or seller pays to a lender, to increase the lender’s effective yield. One point is equal to one percent of the loan

EQUITY

Equity is net ownership In other words, it’s the difference between how much your property is worth and how much you still owe on your mortgage (Market value – Mortgage balance = Equity) Equity is also sometimes called owner ’ s interest

FHA-INSURED LOANS

Home mortgage loans insured by the Federal Housing Administration are referred to as “FHA or FHA-Insured Loans.”

FIRST MORTGAGE

A first mortgage gives the lender a security right over all other mortgages on the mortgaged property

FIXED INTEREST RATE

A fixed interest rate is one that never changes over the life of a loan. For example, if you have a fixed rate, 30-year mortgage, you will pay the same interest rate for the entire 30-year repayment schedule

INTEREST RATE

An interest rate is the percentage of the outstanding balance of a loan that you are charged for borrowing money, usually expressed as an annual percentage rate

LOAN ORIGINATION FEE.

This is a fee charged by lenders to prepare documents, make credit checks, inspect, and sometimes appraise property. It is usually stated as a percentage of the face value of the loan.

LOAN ORIGINATION FEE.

This is a fee charged by lenders to prepare documents, make credit checks, inspect, and sometimes appraise property It is usually stated as a percentage of the face value of the loan

PITI

PITI is an acronym for principal, interest, taxes, and insurance. Most monthly residential mortgage payments include these items:

POINT

A point is one percent of the dollar amount of the mortgage loan. For example, if your loan amount is $150,000, a point is $1,500. By paying points, you can generally lower the loan’s interest rate.

PRINCIPAL

1) Principal is the original amount of a loan, excluding interest. Interest is charged based on the unpaid principal of a loan or credit account. 2) The remaining balance of a loan, excluding interest

PRIVATE MORTGAGE INSURANCE

(PMI)

Insurance written by a private company protecting the mortgage lender against financial loss occasioned by a borrower defaulting on the mortgage Typically only applicable with a down payment less less 20%