BELL WEALTH

— BY GREG SWEENEY CFA, SVP/Chief Investment Officer

— BY GREG SWEENEY CFA, SVP/Chief Investment Officer

from Here?

After an eventful 2024 that saw three rate cuts and a presidential election among its numerous economic developments, what will the next 12 months bring? From interest rates to inflation to the equity market, Greg Sweeney looks ahead to 2025 – while also looking back to the 1920s.

The decade of the 1920s was characterized by economic prosperity, rousing optimism and cultural shifts. During that time, the U.S. economy accelerated on the heels of the second industrial revolution in part due to an increasing use of factories to improve efficiencies. By the late 1920s, 65% of households were serviced by electricity, up from about 20% 10 years earlier. With households’ access to electricity, refrigerators, washing machines, vacuums and radios followed.

A booming stock market also characterized the 1920s. Many investors figured it was a never-ending story. Stock prices reached elevated heights as the Dow Jones Industrial Average delivered 14% annualized returns from the start of the decade to the peak in August 1929. From the Dow’s low in the middle of 1921, the annualized return through August 1929 was 24%.

At its peak during the 1920s, the Dow reached $380 in August 1929. By July 1932 it had fallen to $42, which amounted to an annualized loss of 54%. Imagine investing $380 and watching the market value fall to $42 in less than three years! Since January 1, 1900 until today, the annualized return on the Dow is 7%. If we exclude the last 15 years of elevated returns and go back to March 2009 during the Great Financial Crisis, the long-term return on the Dow drops to just 6%. (We are using the Dow because we can get information all the way back to the start of the 1900s.) The returns highlighted in previous paragraphs show some of the successes and agonies that occurred over the long term.

Why am I using this example? Consider this: In more recent years, the Dow saw its low in March 2020 sink to 18,590,

and in late November 2024 was up over 44,000. That is a 21.6% annualized return, but the decade of the 2020s isn’t even half over yet. We do not know where interest rates will be a year from now. We also do not know whether the stock market will be up or down a year from now. What we do know is, just like what occurred in the 1920s, the market does not sustain 20% returns, and there will be a lull or correction at some point.

We don’t know what the economic and market indicators will look like a year from now, but as I always say, we can use the (imperfect) data available to us to make forecasts about a range of potential outcomes. With that in mind, here is a list of my top 10 predictions for what could happen in 2025.

1

The yield curve will return to “normally sloped,” where short-term interest rates are lower than longerterm interest rates.

2

The era of ultra-low – and in some cases negative – interest rates is gone. The ultra-low interest rate environment that lasted from the Great Financial Crisis until 2021 was an aberration, and it will not return short of some huge disaster. Don’t hold your breath waiting for those 3% mortgage rates to return anytime soon.

3

Speaking of mortgage rates: they will remain mostly between 6% and 7%, and the cost of housing will remain a heavy burden for first-time homebuyers because of interest costs and the underlying price of a home. Perhaps there may be some sort of expansion of homebuying assistance programs, but such programs would come with even more upward pressure on

We don’t know what the economic and market indicators will look like a year from now, but as I always say, we can use the (imperfect) data available to us to make forecasts about a range of potential outcomes.

— Greg Sweeney

home prices if building did not increase proportionately. Tony Weick, president of Bell Bank Mortgage, shares his annual mortgage outlook later in this newsletter.

4

Inflation will have a hard time returning to the Federal Reserve’s 2% target level. There are various measures for inflation and some could show it near 2%, but consumers will likely continue to have a “price” experience that exceeds the reported inflation rate.

5

As I hinted at earlier, the equity market returns seen in 2024 will not be repeated in 2025. Consistent with the outline for longterm return averages, the stock market will need to take a breather. Valuations are better in developed foreign markets, but we still give the nod to the U.S. for the best expected return performance in 2025.

6

It will take companies longer than expected to profit from artificial intelligence (AI). Until then, we will have to continue relying on a different form of AI – actual intelligence – to navigate the markets, the economy and asset allocation.

7

Federal debt levels will continue to push higher along with the interest costs of supporting it. The increasing federal debt will make

frequent headlines, but the political resolve to address it will be nowhere to be found. As Winston Churchill supposedly once said, “You can count on Americans to do the right thing after they have exhausted all other possibilities.”

8

The demand for electricity from AI, crypto blockchain and the electrification of automobiles will be so great that it will take all existing generating resources to provide it and then some. This will make global carbon initiatives difficult to meet over the next three to five years.

9

Bonds will be in a better position to deliver returns in the range of 3.5% to 5.5% following the last five years of dismal performance (Bell’s 5yr 401K bond model had annualized returns of 0.76%, compared to the popular Bloomberg Aggregate Bond Index, which had an annualized loss of -0.24%).

10

The Minnesota Vikings will win the Super Bowl! This last forecast is to remind you, as I like to say, that “those that forecast don’t know, those that know don’t forecast.”

Putting this all together, we expect the economy to continue growing in 2025. Consumers will become a bit guarded as interest rates take more of their earnings and the job market cools. AI will continue

to be a buzzword, but its effects on the equity market will be more muted than in 2024, with stock returns expected to be closer to long-term averages. Bond interest income will be half to three-fifths of the return in the equity market. Expect inflation to remain part of the landscape, settling in around the 3% area. The Fed will look to continue reducing short-term interest rates, but perhaps less than the market currently expects. Our estimate is in the range of 3.5% to 3.75%.

When I started my investment management career in 1985, I had no idea I would be preparing an annual economic outlook 40 years later. The biggest compliment given to an investment management firm is to recognize them as still in business, which means they have competed among the best of them. Thank you for the opportunity to remain in business with you as our clients! Best wishes for a great 2025!

Tony Weick | President, Bell Bank Mortgage

As we look ahead to 2025 for the mortgage industry, it’s important to look back at what has occurred over the past 12 months to understand where we are today and where we may be going. Entering 2024, the industry was anticipating change in a variety of ways, but unfortunately, anyone who thought change would start early in the year was certainly disappointed.

When 2024 began, the Federal Reserve’s tightening efforts of the previous 12 months had led to a slowdown of an overheated U.S. economy. However, markets remained resilient and inflation remained stubborn, and as a result, mortgage rates stayed higher for most of the year. We also experienced significant volatility with several fits and starts – there were multiple times when we believed markets were “turning the corner,” but whenever that happened, things quickly reversed course.

Eventually, economic data began to show sufficient cooling for the Fed to start

cutting rates in September. Unfortunately for the mortgage sector, the markets had already priced in rate cuts going into fall. Following the Fed’s first rate cut, mortgage rates actually increased. Through the fourth quarter, which included two more rate cuts in November and December, as well as the results of the U.S. presidential election, we are still seeing market volatility – and expect this to continue for some time.

So, now that we’ve covered 2024, what can we expect in 2025? Is there any clarity in what the markets may do next? On one hand, we definitely had some questions answered last year, particularly with respect to when the Fed would start cutting rates and who would win the election. However, the answers to those questions may have just led to additional uncertainties for the months ahead.

Starting with the Fed funds rate, the markets continue to evaluate a variety of factors that will impact the speed and

number of future rate cuts. As recently as this fall, many economists were still predicting up to six additional rate cuts in 2025. In recent weeks, however, those predictions have pulled back, with some now only calling for a couple more cuts. Time will tell.

As we know, the Fed funds rate isn’t directly tied to mortgage rates, but they do tend to move in similar directions. If you recall last year’s article, we had expected mortgage rates to drop into the low-6% range by the end of 2024, but that didn’t happen. Instead, due to the factors mentioned earlier, rates stayed higher, bouncing between the mid-6% and high-7% range at different points in the year. Moving into 2025, we’ll likely see a continuation of this trend. We believe rates will moderately decrease throughout the year, starting in the high-6%/low-7% range and progressing down to around mid-6% in the second half the year.

Additionally, like I mentioned earlier, markets and mortgage rates will likely

experience ongoing volatility driven by economic data and national developments, and this may be the norm for the foreseeable future. Don’t be surprised if rates fluctuate by 25%-50% above or below the averages at different points in 2025.

Now, let’s look at homeownership affordability and what we may see in 2025. A key aspect of affordability is, of course, housing values – the cost of a home. A key component to what drives property values is the available inventory – or how many homes are listed for sale at any given time. In recent years, there has been a severe shortage of available inventory, a trend that was amplified during and following the pandemic. This has occurred for a number of reasons, including:

• Low levels of new construction: Over the past decade, new construction activity has lagged where many people believe it needs to produce.

• Institutional ownership: During the same timeframe, many single-family housing units have been acquired by large institutions or even hedge funds and turned into rental properties.

• The “handcuff” factor: The majority of current homeowners with financing have rates in the 3%-4% range, far below current levels. This is keeping many homeowners from selling due to the potential impact on their housing payments.

In the past year, we’ve started to note some positive changes, with many markets across the country seeing 10%-20% year-overyear increases in homes for sale – although it’s important to remember that we were coming off very low levels the year before. (Different markets, as well as different price ranges, will vary within these statistics, as real estate is definitely market specific.) This

increased availability is a welcome change for homebuyers, but we still remain undersupplied in nearly all categories relative to what is considered a healthy balance.

We believe this positive inventory trend will continue in 2025 – albeit slowly. Every month, more and more properties “turn over,” resulting in fewer homeowners being handcuffed to their very low mortgage rates. Whether it’s someone looking to refinance and pull equity out of their home or just the reality of life happening (such as people getting married, having a baby, relocating or downsizing), more homeowners will move, resulting in fewer properties being tied down.

As for affordability, not only do property values and interest rates matter, but now more than ever, real estate taxes and insurance – things that used to be an afterthought – also have major impacts on payment levels. These have always been part of homeowners’ monthly obligations, but recent increases, especially in insurance, have added to rising costs that households need to budget for. As mortgage rates start to moderate and inventory builds its way back, we should see a slowing of home price appreciation. As that happens, things will begin to improve for homeowners and homebuyers after a challenging couple of years.

One final note on affordability: many homebuyers still mistakenly believe it takes a 20% down payment to buy a home. This is not the case, and there are a number of local, state and national programs designed to help with the cost of down payments. Recently, there’s been an increased industry commitment to making sure homebuyers understand some of the available options. From lenders to secondary market investors to city and state governments, many around the industry are working to develop and market programs to help qualified applicants overcome affordability challenges.

After a third straight year littered with negative headlines and limited activity, the mortgage and real estate industries have confidence that we are finally beginning to turn the corner. Here’s why:

• Mortgage rates are expected to gradually decrease, which will not only spur overall activity, but provide opportunities for people to pull equity out of their home or reduce their monthly payments by refinancing.

• The amount of quality housing inventory available for sale will continue to rise throughout 2025, which, combined with a level of pentup demand, will drive an increase in purchase opportunities and activity for buyers.

• As a result of that increase in inventory, price appreciation is forecast to remain in the 4%-5% range, a much more stable and affordable level than in previous years.

• The evolution of mortgage financing options will provide new solutions and opportunities for potential homebuyers, helping them overcome the affordability challenges that can limit homebuying today.

WE CAN HELP! Using good old-fashioned professionalism, competitiveness and customer service, we expect great things for Bell Bank Mortgage and our business partners and clients in 2025. If you’re thinking about building or buying a new home, or considering refinancing alternatives, we’d love the opportunity to help you determine what’s in your best interests. As always, we welcome your business and referrals and would be honored to serve you.

As mortgage rates start to moderate and inventory builds its way back, we should see a slowing of home price appreciation.

— Tony Weick

Brian Schumacher has already hit the ground running. Bell’s new market president and wealth management director in Grand Forks, N.D., Brian is leading the bank’s expansion efforts in the northern Red River Valley. A native of Thompson, N.D., and a graduate of Concordia College in Moorhead, Minn., Brian joined Bell from Alerus, where he most recently served as director of consumer banking and wealth management.

Over the next few months, Brian will be building out Bell’s banking team in Grand Forks, which will initially be based in the current Bell Insurance building. Construction will begin later this spring on a new flagship location that will house the Grand Forks retail and commercial banking, insurance, wealth management and mortgage teams, with an anticipated completion date of mid-to-late 2026. We recently caught up with Brian, who shared why he joined Bell, what he’s looking forward to in the next few months, and why every Bell client should be excited about our growth and expansion in the Grand Forks market.

There were a few reasons that made this an exciting opportunity for me. First, as a North Dakota native, Bell’s commitment to this state was a huge factor for me. Second, Bell has a reputation for taking care of both its employees and its customers, and a tremendous culture like that is something I want to be part of. Finally, I’m excited about the opportunity to lead Bell’s expansion in this area. Grand Forks is a $4 billion deposit market, and there will be a huge potential for collaboration among Bell’s different business lines, from wealth management to private banking to insurance, to help serve the needs of our clients. Having Bell Insurance already in Grand Forks is a huge advantage, as the significant commercial and personal relationships they’ve built will provide fuel for our growth and expansion.

When you’re just getting started in a new market like this, you’re playing offense on the field all day, to use a football analogy. So, from both a client and talent perspective, I’m excited to spend each and every day out in our communities here, connecting with and building my network and finding opportunities to help us grow.

Fortunately, as I mentioned, we’re not completely starting from square one – Bell Insurance’s presence here certainly gives us a head start. That team is already out connecting with folks in the community every day. We opened our doors in the Bell Insurance building in early January, and it’s been awesome to hear about our community’s interest in what we’re doing. We’re going to build on that and keep the momentum going.

I hope that clients see this expansion as more than just what’s happening in Grand Forks. What I mean is, this expansion represents Bell’s commitment to growth and to making long-term investments in both the wealth management and banking business.

As we grow and expand, we’ll be able to improve our products and technology offerings, and we’ll be able to hire additional skilled professionals to help us serve our clients. All of this will help enhance the experience for every single client, and I think that’s an exciting thing.

Matt Bushard, CFP® | Senior Wealth Management Advisor

As we enter the new year, there are several meaningful changes to tax and retirement planning limits that are important to be aware of.

The IRS typically updates these figures every year, and by staying informed about the changes, you can adjust your financial and retirement planning strategies accordingly.

Here’s what to know to start your year off right:

The annual contribution limit for qualified retirement plans, such as 401(k) and 403(b) plans, has increased to $23,500 for 2025, while the catch-up contribution limit for people age 50 or over stayed the same at $7,500. One new update to contribution limits this year is an enhanced catch-up contribution amount of $11,250 if you are between the ages of 60 and 63. This change is intended to help people who may be underprepared for retirement by giving them more of an ability to catch up with their savings as they near retirement age.

The annual contribution limit for traditional and Roth IRAs did not change for 2025, and remains at $7,000. The $1,000 catch-up limit for people age 50 or older also remains the same.

For anyone age 70 ½ or older, the limit on making tax-free qualified charitable distributions to charities or nonprofits from an IRA has increased to $108,000.

In 2025, the amount you can contribute to a Health Savings Account has increased to $4,300 for individuals and $8,550 for families.

The annual gift tax exclusion has increased to $19,000 for 2025, and the estate, gift and generation-skipping transfer tax exclusion amount has increased to $13,990,000.

The rates for income tax brackets did not change from 2024, but income levels have increased for each threshold no matter your tax filing status. This is also the case for long-term capital gains tax rates.

The standard deductions for 2025 have increased to $15,000 for single filers and $30,000 for married filing jointly.

Our team is closely watching what happens with the current federal tax code, portions of which were passed in 2018 as part of the Tax Cuts and Jobs Act. If new legislation is not enacted, several provisions of the tax code will sunset at the end of 2025 and revert back to pre-2017 rules and limits.

The Bell Bank Wealth Management team will be paying close attention as the new administration enters office and begins to work through its agenda. We will share updates with you if or when they become available.

If you have any questions about what these changes mean for you and your financial and retirement planning, please do not hesitate to contact us!

s 2025 Economic Outlook

s Is the Mortgage Industry Turning the Corner?

s Q&A with New Grand Forks President/Wealth Management Director

s Tax and Retirement Planning Updates for 2025

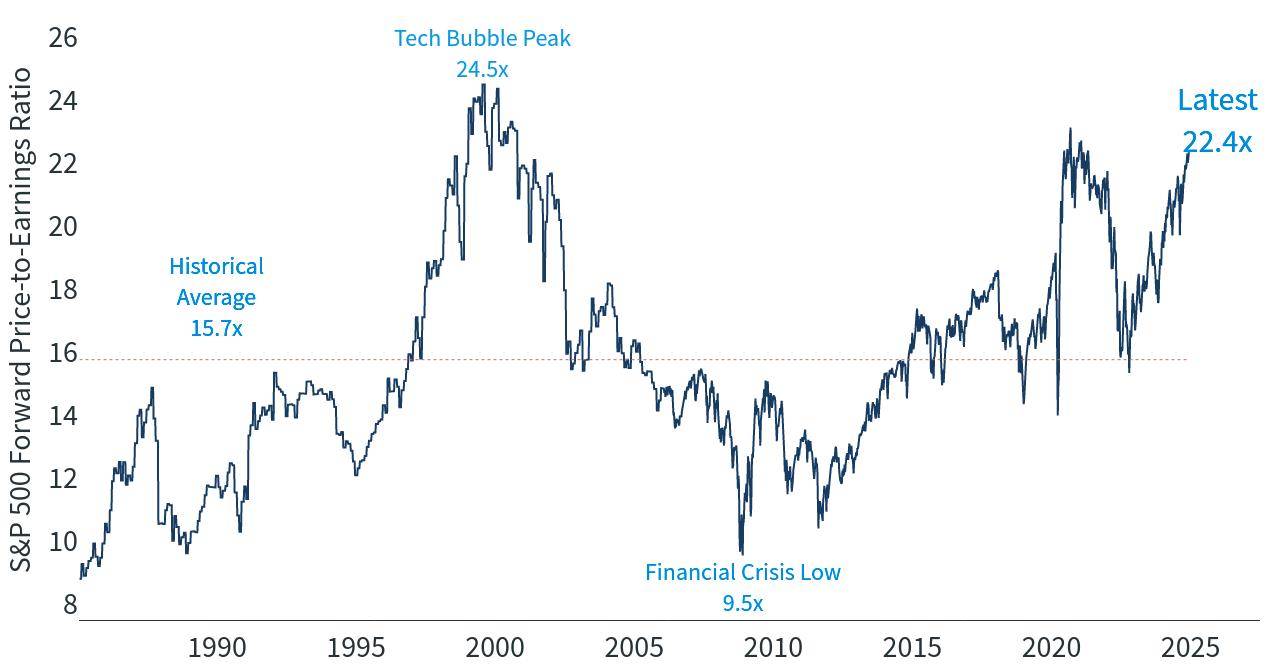

After two very strong years for the stock market, valuations are now well above historical averages, with price-to-earnings ratios exceeding 22x. Elevated valuations reflect the market rally, steady economic growth, and enthusiasm surrounding technology and AI. However, stretched valuations also underscore a crucial principle of investing: the importance of diversification. Maintaining a well-diversified portfolio across sectors, asset classes, and risk levels is critical for managing market volatility as you work to achieve your financial goals.