SIDEWAYS

Bitcoin Caught in a Range

Slowing Growth, Sticky In ation And Rising Legal Uncertainty In The US Economy

Bitcoin Caught in a Range

Slowing Growth, Sticky In ation And Rising Legal Uncertainty In The US Economy

Bitcoin remains confined within the $66,000$70,000 range, consolidating after the February 5 drawdown, currently the deepest of this cycle. Volatility has compressed and momentum has faded, signalling a transition from a liquidation-drivendeclineintoamorebalancedenvironment.On-chaindatashows thatmuchoftherecentdownsidehasbeenabsorbedwithinthe$60,000$69,000 demand band. This cohort of holders, who are now near breakeven, has largely refrainedfromacceleratingdistribution,helpingstabilisepriceandcontributetoa moresidewaysmovingmarket.

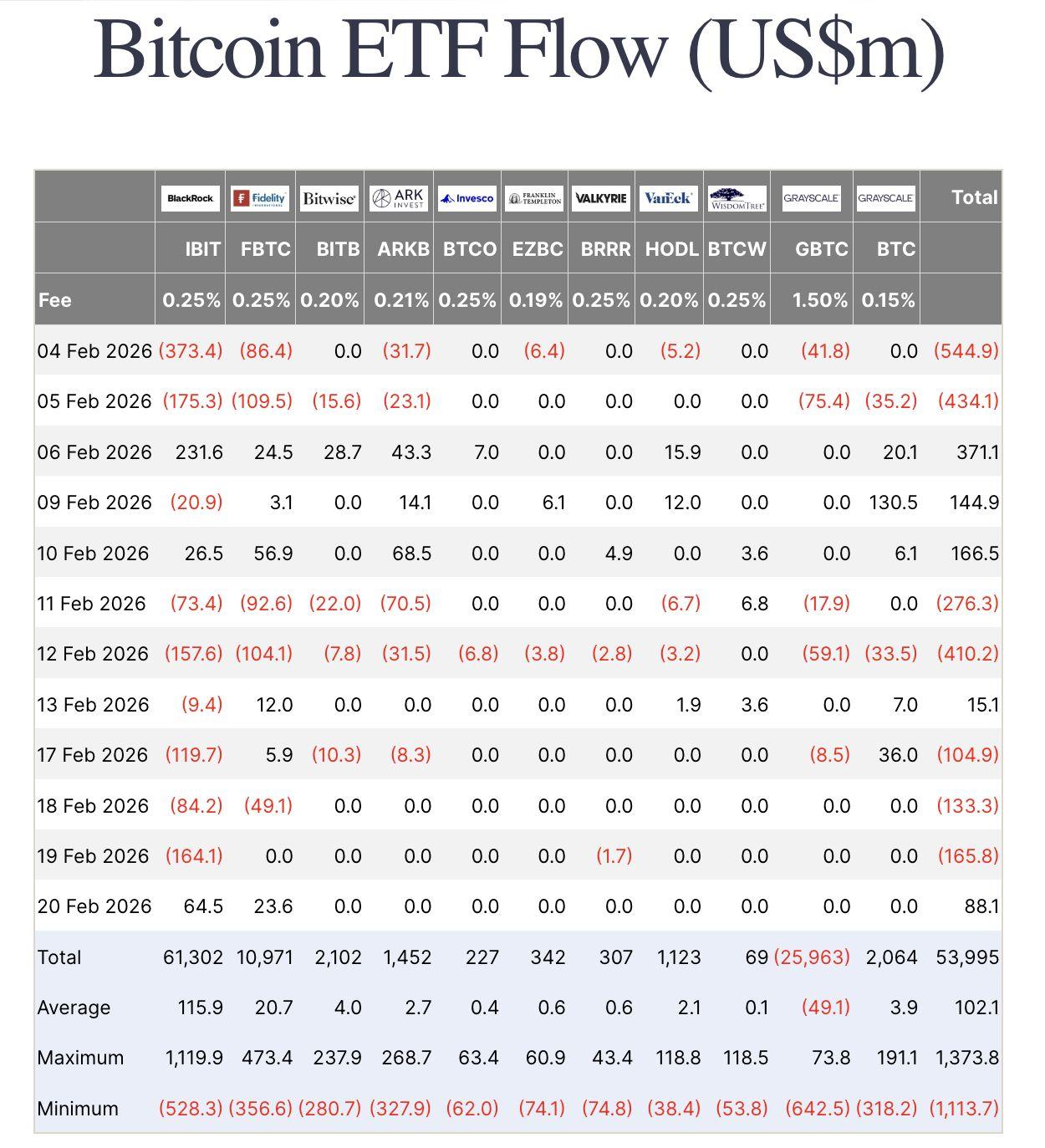

Institutional flows, however, remain cautious.BitcoinETFsrecordednetweekly outflows of roughly $166 million, with Ethereum products also seeing persistent redemptions, underscoring that sustained accumulation has yet to return. While late-week inflows offered a tentative stabilisation signal, the broader liquidity backdrop remains subdued. The Realised Profit/Loss Ratio continues to compress toward historically defensive territory, indicating limited capital expansion across the network. Meanwhile, derivatives positioning has normalised, with funding rates neutral to slightly negative, reducing liquidation risk but also limiting upside acceleration.

Foradurablebreakouttomaterialise,themarketwillrequireaclearresurgencein spot demand and stronger institutional participation; until then, Bitcoin is likely to remainrange-boundwithinitsestablishedabsorptionzone.

TheUSeconomyclosed2025withslowerheadlinegrowthbutwithstillpersistent inflation,reinforcingarestrictivepolicybackdrop.Fourth-quarterGrossDomestic Productexpandedatanannualised1.4percent,weigheddownsignificantlybythe federal government shutdown and reduced public spending. However, private-sector momentum remained resilient. Business investment, particularly in artificial intelligence infrastructure, strengthened, while industrial production improved,andhousingstartsrose.

Inflation remains the key constraint. Core Personal Consumption Expenditures reached 3 percent year-on-year, limiting the Federal Reserveʼs scope for near-termratecuts.Atthesametime,theSupremeCourtʼsdecisiontostrikedown emergency tariffs introduces potential fiscal stimulus through refunds that could reachupto$175billion,thoughthiswouldwidenthedeficitandaddcomplexityto inflationexpectations.

Meanwhile,WashingtonhassetaMarch1deadlinetoresolvedisagreementsover the Digital Asset Market Clarity Act CLARITY Act), which would divide oversight betweentheSECandtheCFTC,establishalegalframeworkfordigitalcommodity spot markets, and potentially end regulation-by-lawsuit. The central dispute is whetherstablecoinholdersshouldbeallowedtoearnyield,withbankspushingfor a comprehensive ban on rewards while crypto firms argue this would distort competitionandundermineexistingbusinessmodels.

Againstthismacrobackdropofmoderatinggrowthandfirmprices,cryptomarkets continue to institutionalise. Harvard Universityʼs endowment diversified its digital assetexposurebyreallocatingfromaBitcoinETFintoanEthereumETF,signalling portfolio refinement rather than reduced conviction. CME Groupʼs move toward 24/7 crypto derivatives trading further aligns regulated markets with cryptoʼs continuous structure, reflecting sustained institutional demand. Meanwhile, new SEC guidance reducing stablecoin capital haircuts to 2 percent lowers balance sheetfrictionandsupportsdeeperintegrationofblockchain-basedsettlementinto traditionalfinance.

1.MarketSignals

● BitcoinCaughtinaRange

2.GeneralMacroUpdate

● USGrowthSlowsasInflationStaysFirm, LimitingScopeforRateCuts

● SupremeCourtStrikesDownEmergency Tariffs,LeavingPolicyandFiscal QuestionsOpen

● MidweekStrengthinInvestmentand HousingOffsetbyShutdown-DrivenGDP Drag

● TheCLARITYAct'sMarch1Moment

3.NewsFromtheCryptosphere

● HarvardUniversityAdjustsBitcoinand EthereumETFExposure

● CMEGroupAnnounces24/7Trading Launch ●

Bitcoin remains confined in the same $66,000$70,000 range that was establishedtwoweeksago.Priceactioncontinuestoreflectconsolidationfrom theFebruary5pullback,currentlythelargestofthiscycle.

It is telling that the mechanical 20.3 percent rebound which immediately followedthesharpdroponFebruary5,reflectedshortcoveringandpositioning resetsratherthansustainedstructuraldemand.

Figure1.BTC/USD4HChart.Source:Bitfinex)

With volatility compressing and directional momentum fading, we believe the market is now transitioning from a liquidation-driven environment into a more balanced one. In such environments, ETF flows and on-chain dynamics become theprimaryleadingindicatorsforanticipatingthenextimpulsemove.

A closer examination of price action following the breakdown below the True MarketMean(currentlynear$79,000)suggeststhatmuchoftherecentdownside pressure has been absorbed within a dense demand band between $60,000 and $69,000. This supply cluster was largely formed during the first six months of 2024, when investors accumulated within a prolonged consolidation phase, and havesincemaintainedthosepositions.

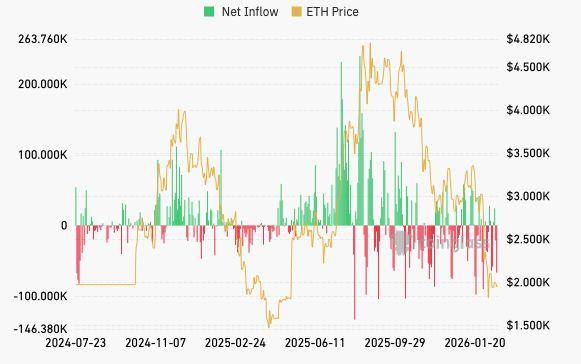

ThisweekʼsETFflowprofilewascharacterisedbysustaineddistributionfollowed byatentativelate-weekstabilisationbid.BitcoinspotETFsclosedtheweekwith approximately$165.8millioninnetoutflows,despiteameaningfulreboundinthe final trading session. Ethereum products also finished the week weaker, with roughly $130.1 million in net outflows, confirming that the de-risking impulse extendedbeyondBTCandwasnotasset-specific.

The bulk of the pressure emerged midweek, where flows remained consistently negative across multiple sessions, and which saw the heaviest redemptions, limiting the priceʼs ability to generate sustained momentum within the $65,000$70,000consolidationrange.

Last Friday offered the first constructive counter-signal. BTC ETFs recorded approximately $88.1 million in inflows, while ETH flows were broadly flat to marginallynegativeataround$0.7millioninoutflows.Solanaproductsregistered modest inflows of roughly $3.7 million. However, this should be interpreted as selectivestabilisationratherthanadefinitivereversal.Itdemonstratesthatbuyers arepreparedtore-engageatcurrentlevels,buttheaggregateweeklyprofilestill suggests that institutional demand has not yet shifted into a sustained accumulationregime.

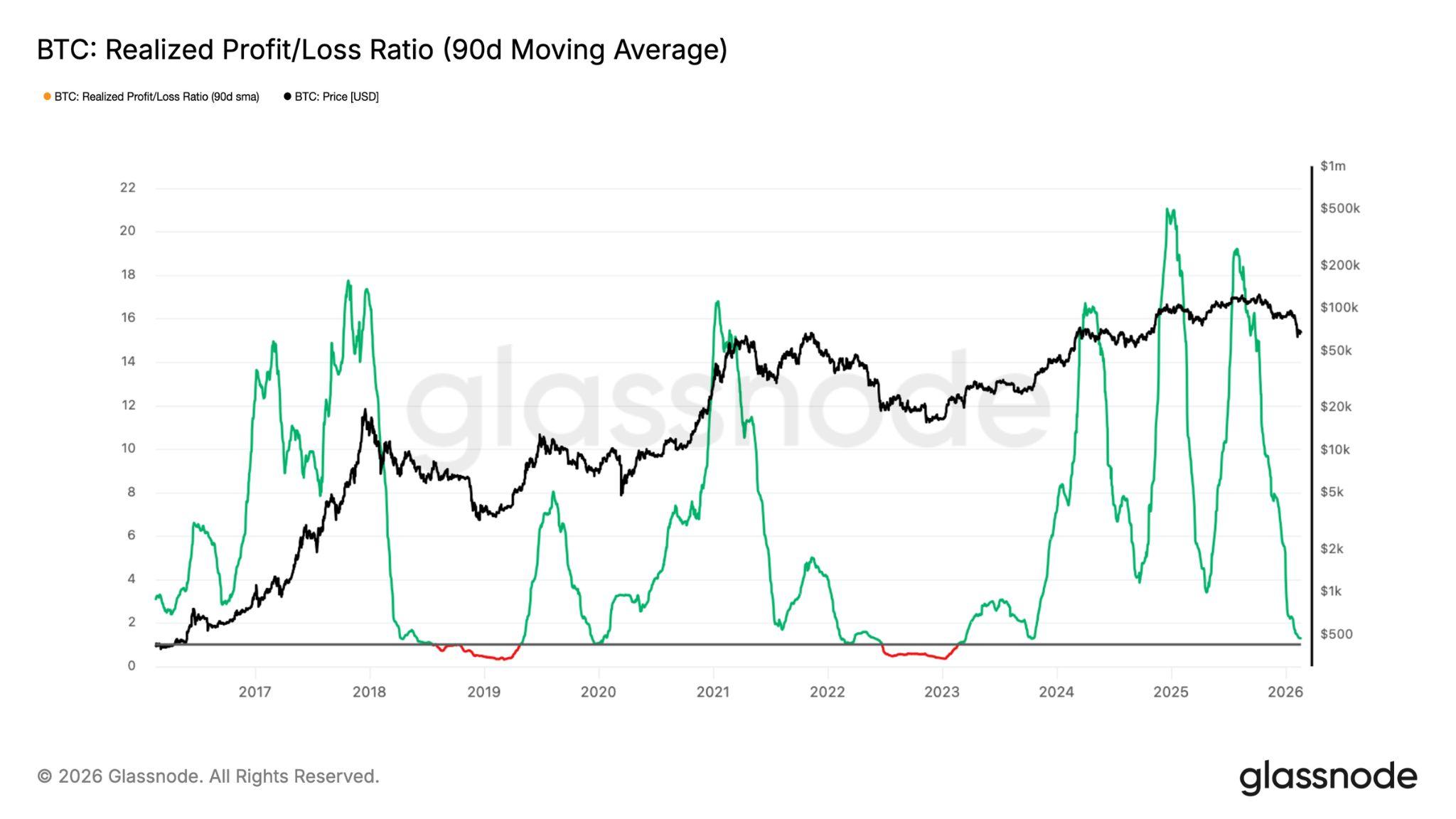

Beyond the lack of sustained accumulation, broader liquidity conditions continue to signal structural fragility. One useful proxy for internal capital rotation is the RealisedProfit/LossRatioSeeFigure5below),whichmeasurestheaverageUSD valueofrealisedprofitforeverydollarrealisedinloss.

The90-daymovingaverageofthismetrichassteadilycompressedbackintothe 12 range, a zone that historically aligns with transitions from early bear phases into more stressed regimes. In prior cycles, sustained readings below 2 and especiallyamovetoward1,havereflectedweakeningprofitabilityandagradual dominance of realised losses. A break below 1 typically marks environments whereforcedsellingandcapitalerosionoutweighfreshinflows.

The current compression suggests that profit-taking remains muted and capital rotation across the network is limited. In other words, liquidity is not expanding meaningfully,itismerelyrecyclingatsubduedlevels.

For market structure to shift constructively, the Realised Profit/Loss Ratio would needtoreclaimlevelsabove2,signallingareturntohealthyprofitrealisationand stronger liquidity inflows. Until that transition occurs, the broader bias for Bitcoin islikelytoremainstructurallydefensiveratherthanexpansionary.

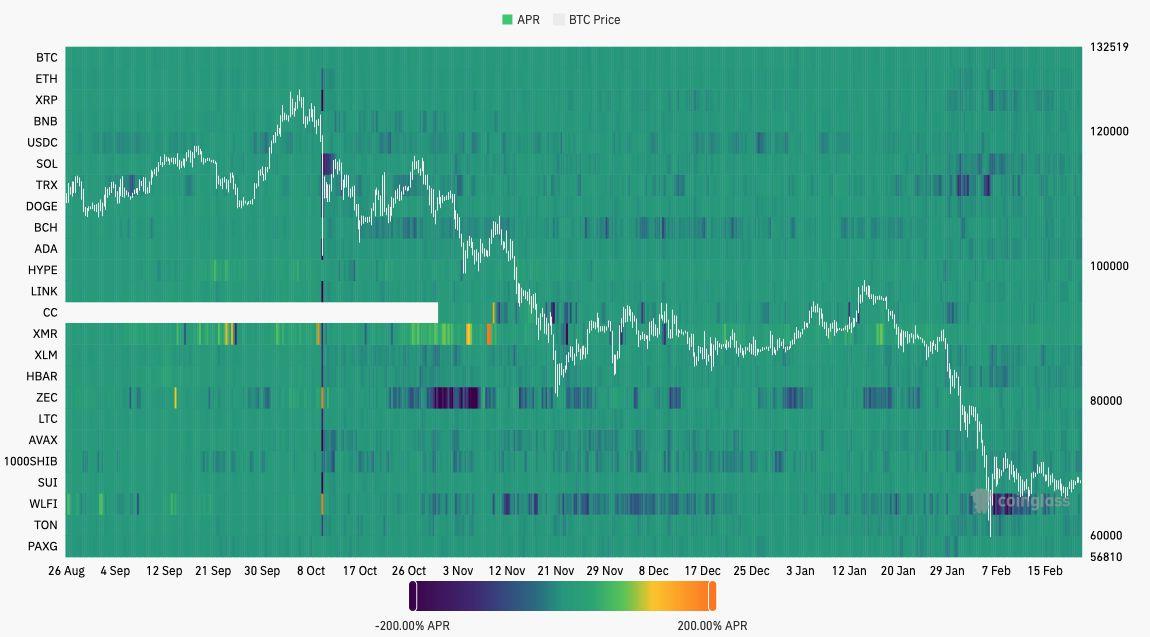

Derivativesmarketsalsoremainrestrained;andthisisbothstabilisingandlimiting. Perpetual funding rates have compressed materially across major venues, with theFundingRateHeatmap(seeFigure7below)illustratingacleartransitionfrom persistentlypositivefundingduringtheadvancetoward$120,000toincreasingly neutral and, at times, negative prints as Bitcoin retraced toward the $70,000 region.Thisshiftreflectsadecisiveunwindoflong-sideleverage.

Source:Coinglass)

Inpreviousexpansionaryphases,sustainedpositivefundingwasthenorm,aclear signal of aggressive long positioning that consistently reinforced the prevailing trend. This time, however, the landscape looks fundamentally different. We are seeing episodic spikes into negative funding, which suggests traders are either hedging spot exposure or opportunistically positioning short during moments of weakness.

What this tells us is that leverage is no longer structurally skewed to the long side. The derivatives complex has settled into a more defensive equilibrium. Without the crowded long positioning weʼve seen in the past, the risk of cascading liquidations on the downside is significantly reduced. But thereʼs a trade-off: upside momentum can no longer rely on the fuel of short-covering alone.

Foradurablerecoverytotakehold,weneedtoseefundingstabilisealongsidea genuine resurgence in spot demand and not just mechanical squeezes playing outinaleverage-lightenvironment.

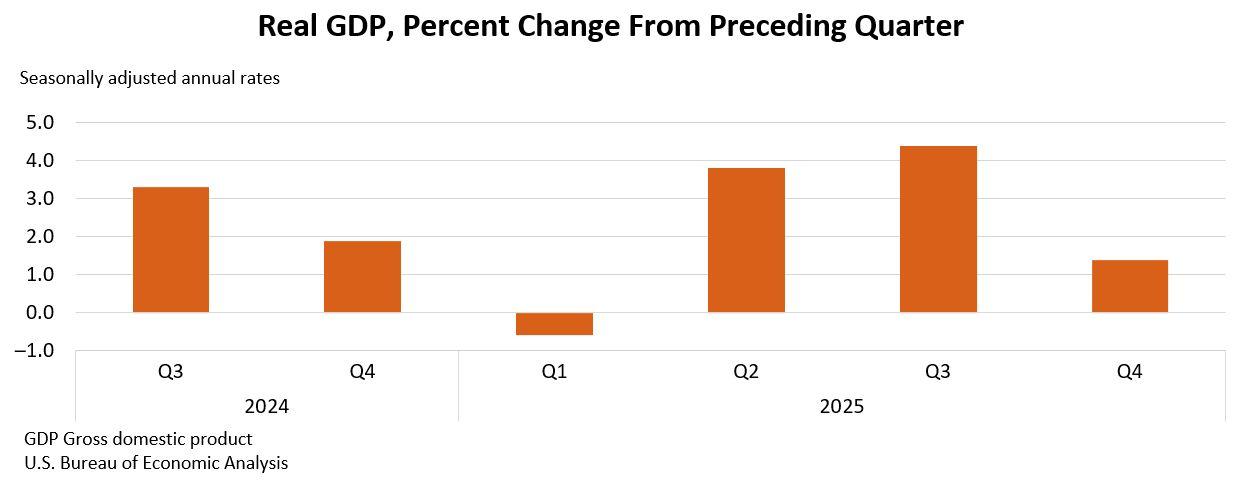

TheUSeconomylostmomentumattheendof2025,whileinflationremained elevated. Such uneven growth continued to shape public sentiment, and althoughunderlyingdemandheldup,persistentpricepressuresandtheimpact of a prolonged government shutdown are likely to keep the Federal Reserve cautiousoninterestrates.

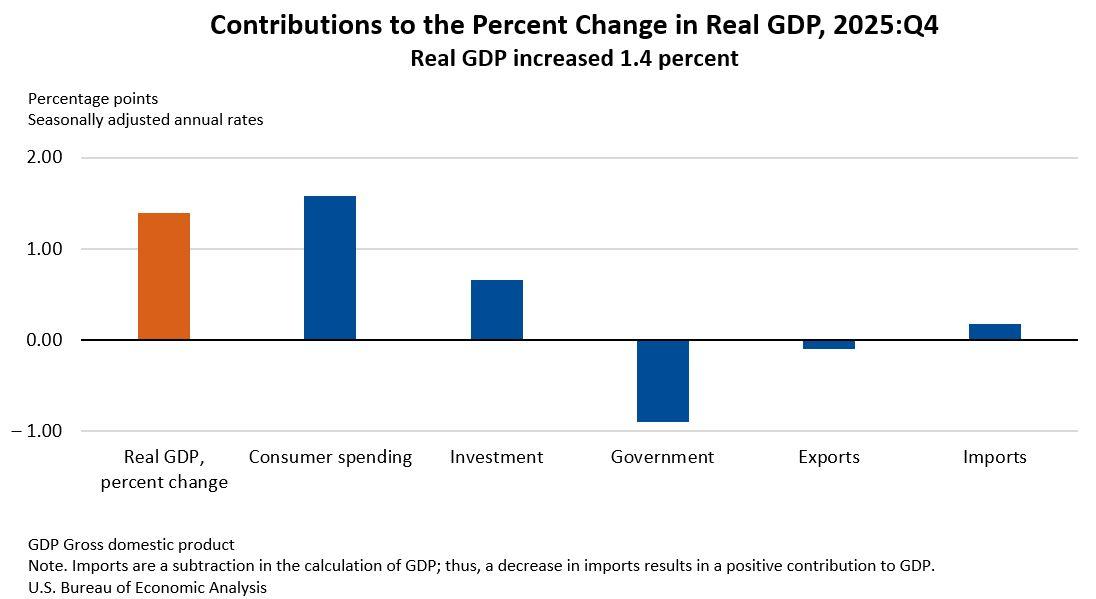

AccordingtotheadvanceestimateofGrossDomesticProductGDPreleasedby the Bureau of Economic Analysis BEA, the US economy expanded at an annualisedrateof1.4percentinthefourthquarter.Thatputsgrowthbelowthe1.8 percent long-term trend, marking a sharp slowdown from the previous quarter. The BEA also reported that the Personal Consumption Expenditures PCE) price index,theFedʼspreferredinflationgauge,stoodat2.9percentinDecember.

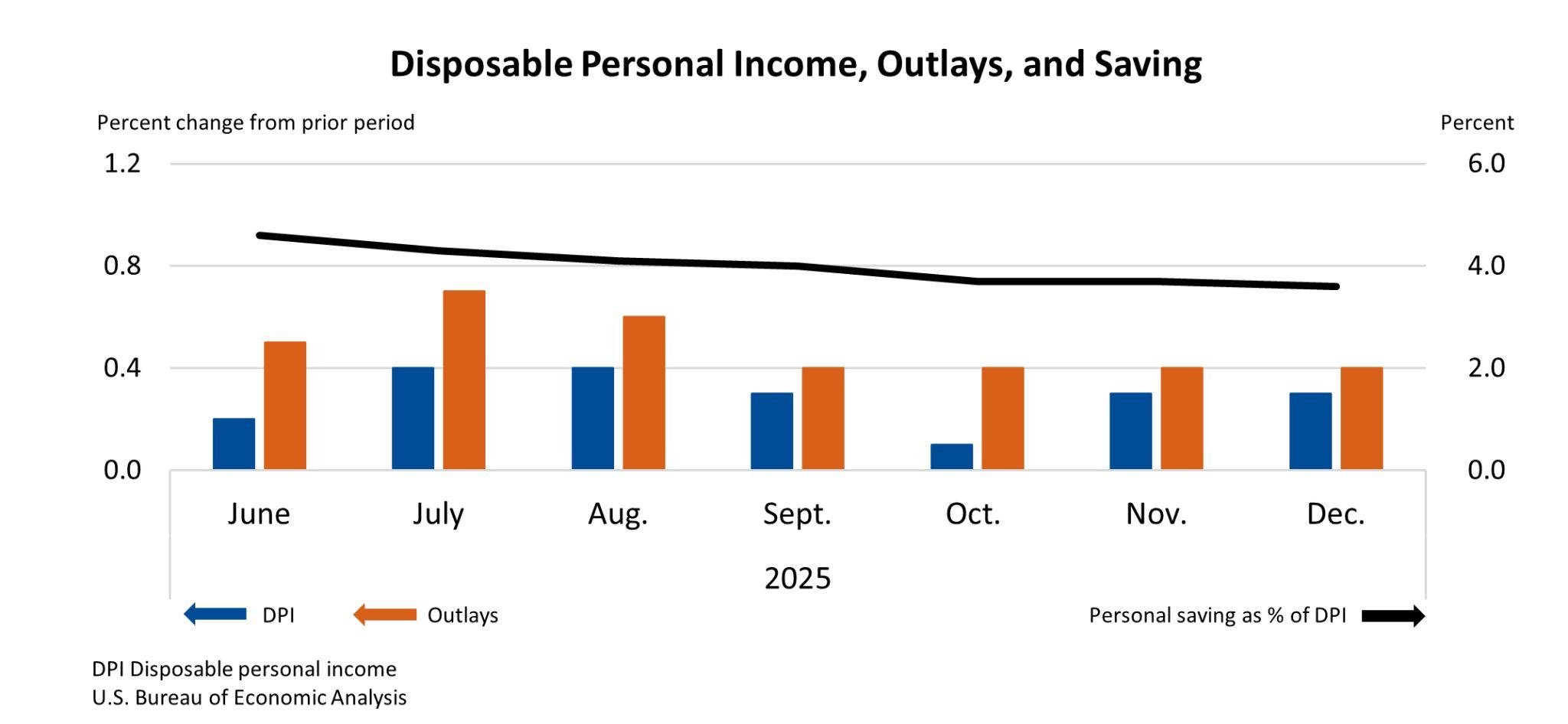

Figure9.DisposablePersonalIncome,OutlaysandSaving Source:USBureauofEconomicAnalysis)

The headline GDP number was heavily influenced by the extended government shutdown in the autumn. Federal services were curtailed for nearly half of the quarter, subtracting roughly one percentage point from growth. Federal government spending excluding defence declined by 24.1 percent, the steepest fall since 2020, and total government consumption dropped by 5.1 percent. Defenceoutlaysfellby10.8percent,whilestateandlocalspendingrosemodestly by 2.4 percent. Overall, reduced federal spending significantly dragged on economicactivity.

BureauofEconomicAnalysis)

Monthly data also showed that household demand was moderating. Consumer spending rose 0.4 percent in December, but after adjusting for inflation, the gain wasjust0.1percent,indicatingthatmuchofthenominalincreasereflectedhigher pricesratherthanstrongerpurchasingpower.

Inflationdynamicsremainthecentralconcern.CorePCEinflationrose0.4percent in December, exceeding the consensus forecast of 0.3 percent. On a 12-month basis, core PCE advanced 3 percent, up from 2.8 percent in November, with Servicesinflationremainingparticularlysticky.

Real final sales increased 1.2 percent, while gross domestic purchases rose 1.3 percent. These moderate gains suggest that while aggregate output expanded, many households continue to face financial strain. Savings buffers have narrowed, credit usage has risen, and real disposable income growth, which is incomeadjustedforinflation,remainssubdued.Thisdivergencebetweenofficial growthandlivedexperiencecontributestoongoingpublicanxiety.

Private investment provided a notable offset to the government drag. Gross privateinvestmentrose3.8percent,withfixedinvestmentincreasing2.6percent. Non-residentialinvestmentclimbed3.7percent,drivenbya3.2percentincrease in equipment spending and a 7.4 percent rise in intellectual property outlays. Much of this strength reflects sustained investment in artificial intelligence infrastructure, including data centres and information processing equipment. Trade flows contributed modestly to growth as imports declined 1.3 percent and exports fell 0.9 percent. Inventory accumulation added only marginally to output after earlier pre-tariff stockpiling had run its course.

For the full year, the US economy expanded 2.2 percent. However, the combination of softer quarterly growth and renewed inflation momentum complicatesthepolicyoutlook.WithcorePCEinflationat3percentandpossibly risingfurther,theFedisunlikelytoreduceitspolicyrateinthenearterm.Minutes from the Fedʼs January meeting already indicated that some policymakers discussedthepossibilityofadditionaltighteningifinflationremainspersistent.

In practical terms, monetary policy is likely to remain restrictive until clearer evidence emerges that inflation is returning sustainably toward the two percent target. The sequencing of the data is critical: the economy slowed partly due to the shutdown, but inflation did not follow growth lower. For markets, this reinforces a straightforward conclusion: growth has cooled, yet inflation remains toofirmtojustifyimminentratecuts.

Figure10.USSupremeCourtSource:Wikipedia)

TheUSSupremeCourtoverturned acentralpillaroftheTrumpadministrationʼs tariffstrategylastFriday,February20,rulingthatemergencypowerswereused beyondtheirlegalscope.Whilethedecisionrestoreslegalclarity,itleavesopen major questions around refunds, fiscal impact and the future direction of trade policy.

TherulingconcernstariffsthatwereimposedundertheInternationalEmergency Economic Powers Act IEEPA, a 1977 statute. In a 63 decision, the Supreme Courtheldthatthelawdoesnotauthorisethepresidenttoimposebroad-based trade tariffs. Chief Justice John Roberts, writing for the majority, stated that CongresshadnotgrantedauthorityunderIEEPAfortariffsofunlimited“amount, duration and scope.ˮ The decision overturns reciprocal tariffs ranging from 10 percent to 41 percent, as well as a 10 percent baseline duty applied to most tradingpartnersunderthatlegalframework.

The judgment does not remove all tariffs. Measures introduced under other statutes, including Section 232 national security tariffs on steel and aluminium, remaininplace.

In response to the ruling, the US President Donald Trump signalled plans to pursue alternative legal routes, including Section 301 investigations into unfair tradepracticesanda10percentglobaltariffunderSection122.However,Section 122 requires Congressional approval after 150 days, which introduces political uncertainty. He later announced that he will re-impose tariffs to 15 percent. Proclaiming on social media that this was ‘effective immediatelyʼ and ‘legally testedʼ.

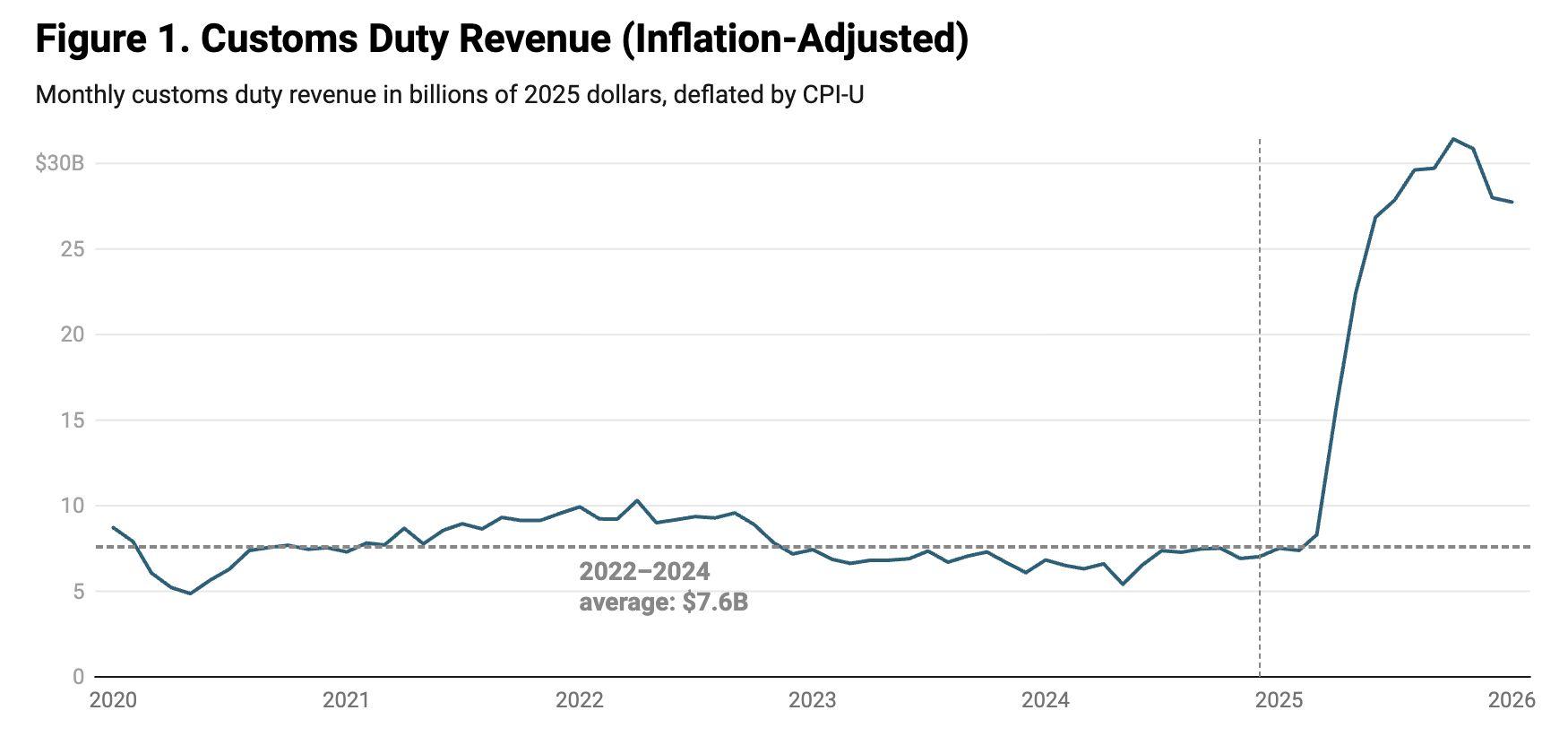

Fromaneconomicperspective,theimplicationsdependonimplementation.Ifthe administration complies with the ruling and the US Treasury establishes a timetable for refunds to companies that were disadvantaged by the tariffs, then paradoxically,therealeconomycouldreceiveasizeableboost.The2025tariffs have raised an estimated $194.8 billion in inflation-adjusted customs revenue above the 20222024 average as of January 2026. The effective tariff rate reached11.7percentinNovember2025.

Estimatessuggestpotentialrefundscouldbeashighas$175billion.Forcontext, current tax reductions are expected to inject between $100 billion and $150 billion into the economy this year. A further $130 billion in tariff refunds would represent a significant fiscal impulse. However, such refunds would widen the budgetdeficitbyroughlyone-halfofonepercent,pushingittowards6.6percent ofgrossdomesticproduct.

Businesses, particularly small and medium-sized firms, stand to benefit most if refunds materialise. These firms absorbed much of the tariff burden through complexsupplychains.Morethan90percentoftheaddedcostswereultimately passed on to consumers through higher prices. If firms choose to lower prices after receiving refunds, this could support consumption and ease inflationary pressures, especially for imported intermediate goods used in domestic production.

The average effective tariff rate currently stands at 16.9 percent. Full implementationoftherulingcouldreducethatrateto9.1percent

Under the Supreme Court ruling, Canadian trading partners, facing an effective rateof5.96percent,couldseethatfigurecutroughlyinhalf.Thiswouldprovide reliefacrossintegratedNorthAmericanmanufacturingandfoodsupplychains.

However, uncertainty remains. Lower courts may need to determine eligibility andtimingforrefunds.Additionallegalchallengesfrombothbusinessesandthe administrationarelikelytodelayanyfiscaltransfers.

The broader significance lies in affirming the rule of law. The Courtʼs decision reinforces that economic powers, including tariff authority, require explicit Congressionalapproval.

Over the medium term however, the combination of legal uncertainty, fiscal implications and new announcements on trade and tariff strategy, could meaningfullyinfluencegrowth,inflationandinterestrateexpectations.

Stronger data on housing starts, business equipment spending and industrial production released last Wednesday, February 25, pointed to firm underlying momentumattheendof2025.However,FridayʼsgrossdomesticproductGDP and inflation figures showed that overall growth slowed, in part due to the federalgovernmentshutdown,whilepricepressuresremainedelevated.

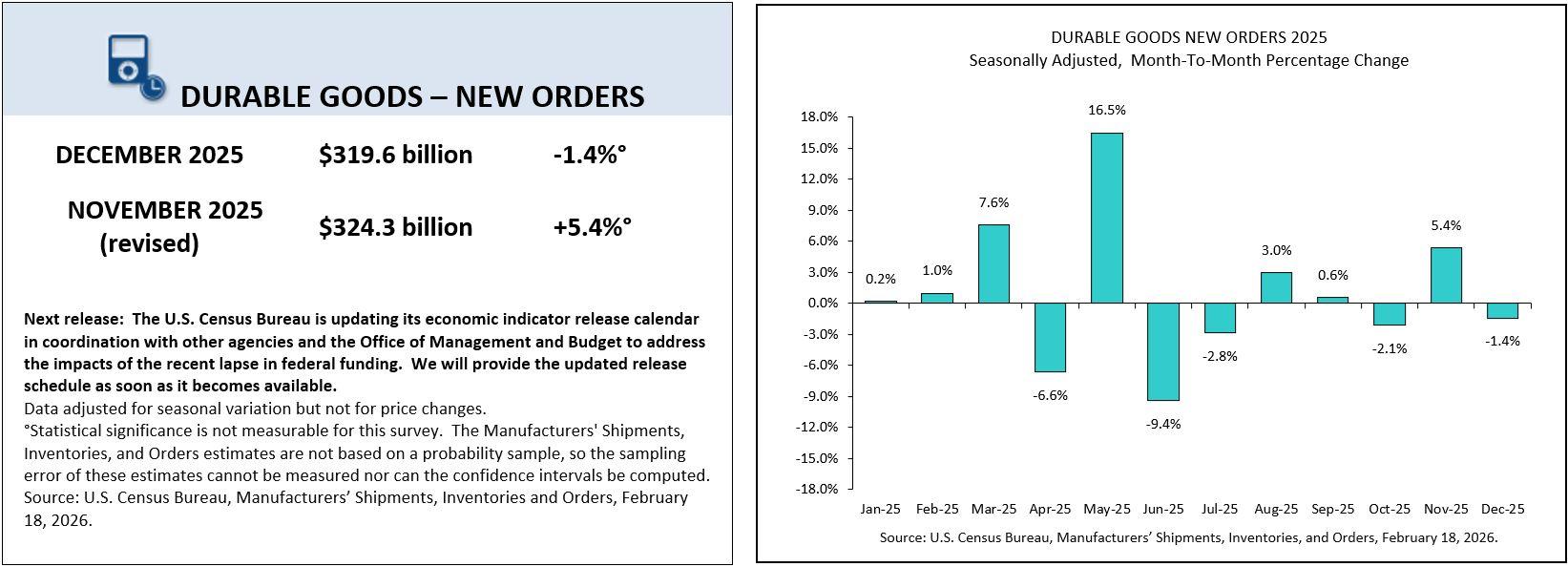

TheCommerceDepartmentʼsCensusBureaureportedthat non-defencecapital goods orders excluding aircraft, commonly referred to as core capital goods, rose0.6percentinDecemberafterarevised0.8percentincreaseinNovember. This measure is widely used as a proxy for business equipment spending becauseitexcludesvolatileaircraftanddefenceitems.Onayear-on-yearbasis, corecapitalgoodsordersincreased3.5percent,signallingsustainedcorporate investment.

Shipmentsofcapitalgoodsalsoadvanced.Thisisimportantbecauseshipments, not orders, feed directly into GDP calculations. In simple terms, shipments represent goods that have been delivered and counted as output. The rise in shipmentsthereforesuggestedthatbusinessinvestmentwouldprovidesupport tofourth-quarterGDP.

Thegainswerebroad-based.Ordersforfabricatedmetalproductsincreased0.9 percent.Electricalequipmentandappliancesrose0.6percent.Machinerygained 0.3 percent. Orders for computers and electronic products climbed 3 percent. Much of this strength appears linked to continued investment in artificial intelligenceinfrastructure,particularlydatacentresandrelatedequipment,which hassupporteddemandacrossmultipleindustrialsupplychains.

Industrial production data released the same day by the Federal Reserve reinforcedthemessage.Factoryoutputrose0.6percentinJanuary,markingthe strongest monthly increase in 11 months. Although December production was revisedtoshownogrowth,manufacturingoutputwasstill2.4percenthigherthan a year earlier. Manufacturing accounts for roughly 10.1 percent of the US economy,soevenmoderategainscaninfluencebroadergrowthdynamics.

At the same time, structural pressures remain. Manufacturing employment has declinedby83,000sinceJanuary2025.Outputgainsareincreasinglysupported by automation and productivity improvements rather than hiring, which limits the labourmarketspillover.

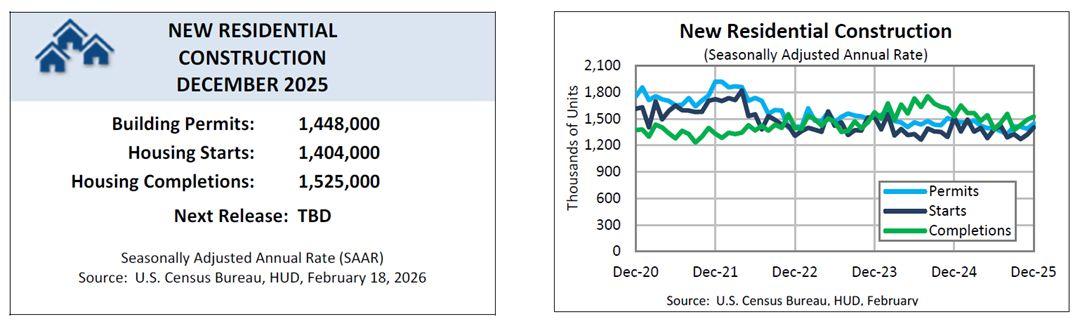

Housing data also surprised to the upside last Wednesday. The Census Bureau reported that overall housing starts increased 6.2 percent in December to an annualrateof1.404millionunits,thehighestsinceJuly.Single-familystartsrose 4.1 percent to 981,000 units, while multi-family projects climbed 10.1 percent to 402,000units.Housingstartsmeasurenewresidentialconstructionandserveas a leading indicator because homebuilding supports employment, materials demandandhouseholdformation.

Building permits presented a mixed picture. Single-family permits declined 1.7 percent to an annual rate of 881,000 units, while multi-family permits rose 18.1 percent to 515,000 units, the highest since August 2023. Overall permits increased 4.3 percent to 1.448 million units, a nine-month high. Permits matter becausetheysignalfutureconstructionactivity.

Despitetheimprovementinstarts,housingcontinuestofaceconstraints.Tariffs on imported materials, labour shortages and still-elevated borrowing costs are weighing on developers. Mortgage rates, which generally track the 10-year US Treasury yield, remain relatively high amid fiscal and inflation concerns. As a result,residentialinvestmentisstillexpectedtocontractforafourthconsecutive quarter.

Wednesdayʼs releases highlighted firm private-sector activity in capital expenditure,manufacturingandhousing.FridayʼsGDPdatathenshowedslower headline growth, but that weakness was amplified by the temporary decline in federal spending during the shutdown rather than a broad collapse in private demand.

Inflation, as measured by PCE, remained firm, reinforcing the view that the Federal Reserve is unlikely to ease policy quickly. In summary, the economy ended the year with resilient pockets of private-sector strength, even as shutdown-related distortions weighed on the top-line GDP figure and price pressuresstayedpersistent.

Washington has set itself a deadline. By March 1st, negotiators from the crypto industry,thebankingsector,andtheWhiteHousearetoresolvedisputesaround the Digital Asset Market Clarity Act, or CLARITY Act, in order to decide how to establishitinlaw.

The Act does three things. It splits regulatory authority over crypto between the SEC and the CFTC, giving each agency a clearly defined lane. It would create a proper legal framework for digital commodity spot markets. And it could end the era of regulation-by-lawsuit that has defined Washington's approach to the industrysinceFTXcollapsedin2022.

But it is stuck not because of ideology or partisan gridlock but because of one simple question: should stablecoin holders be allowed to earn yield on their holdings.

TheSenateBankingCommitteewasscheduledtobegindebatingamendmentson January 15. The session was cancelled shortly before it was due to start, after Coinbase Chief Executive Brian Armstrong posted that the company was withdrawingsupportduetoadraftprovisionthatwouldeffectivelybanstablecoin yield.

Manyplatformscurrentlyofferinterest-likerewardsforholdingstablecoins.Yield on stablecoins forms a meaningful component of portfolio strategy for crypto participantsandrepresentsamaterialrevenuestreamforcentralisedexchanges. Abroadprohibitioncouldthereforealterbusinessmodelsacrossthesector.

The White House had been pushing the bill toward passage ahead of the 2026 midterms. David Sacks, who serves as the White Houseʼs crypto policy lead, statedthatthedelayshouldbeusedto“resolveanyremainingdifferencesˮ.

Subsequent White House-mediated sessions in early February culminated in a thirdmeetingonFebruary20.Seniorlegalrepresentativesfromcryptofirmsmet executives from JPMorgan, Bank of America and Wells Fargo. The banks presented what they described as “Yield and Interest Prohibition Principlesˮ, callingforacomprehensivebannotonlyonstablecoinissuerspayingyieldbuton any financial or non-financial consideration to stablecoin holders. That would includerewards,rebatesorpoints.

Bankexecutiveshavearguedpubliclythatifstablecoinplatformsarepermittedto offer savings-style returns, significant capital could migrate out of traditional bankdeposits.

Crypto stakeholders disagree. They argue that stablecoin rewards, currently in theregionof34percent,arenotequivalenttoinsuredbankdeposits.Theyalso note that the GENIUS Act, the stablecoin law signed last July, excluded exchanges from issuer-level yield restrictions. From this perspective, a platform-level ban would represent regulatory overreach and could tilt competitivedynamicsinfavouroftraditionalfinancialinstitutions.

Some industry participants have expressed willingness to accept a narrower bill rather than risk prolonged legislative paralysis. Others insist that meaningful clarity - pun intended - is preferable to compromise that reshapes the market structureinfavourofincumbents.

TheMarch1deadlineshouldnotbemistakenforafinishline.Evenifnegotiators reach agreement, the bill must pass committee mark-ups, secure a Senate floor voteandbereconciledwiththeHouse.Finalenactmentcouldtakemonths.

The probability of passage, as reflected in market-based assessments, remains elevated but below earlier consensus expectations. Support declined sharply when Coinbase withdrew backing in January, before recovering into late February.

Some experts have warned that failure to pass the bill could shift crypto into a moregradualappreciationphase,drivenlessbyregulatorytailwindsandmoreby demonstrable real-world adoption. Others argue that failure would not alter the long-term trajectory of the sector but would delay institutional expansion and redirect capital toward assets perceived as more structurally resilient, such as Bitcoinandestablishedinfrastructureproviders.

US Treasury Secretary Scott Bessent has stated that he wants the bill signed before the midterms and has described passage as urgent. Senate Banking CommitteeChairmanTimScotthaspledgedtodeliverlegislationin2026.Senate Majority Leader John Thune has reportedly committed to allocating floor time once committee work concludes. Institutional optimism is visible, but procedural riskremains.

Fortraders,March1islessabinarycatalystandmoreadirectionalsignal.Broad marketstructurelegislationin2026islargelypricedin.Whatisnotfullypricedis theoutcomeonstablecoinyield.Ifbankssecureacomprehensiveprohibitionon stablecoin rewards at the platform level, revenue models for major centralised exchanges would face pressure. That scenario would likely weigh on exchange-linked tokens and stablecoin-adjacent infrastructure, while narrowing thecompetitivemoatthatcrypto-nativeplatformshavebuilt.

If negotiators reach a compromise, for example, permitting transaction-based rewards while restricting passive idle-balance yield, the outcome would be workableformuchoftheindustryandcouldserveasamodestpositivecatalyst.

If March 1 passes without agreement and the Senate Banking Committee once again delays mark-up, attention should shift to subsequent statements from Treasury officials and White House representatives. Political capital has already been invested in the bill, and campaign infrastructure aligned with the crypto industryremainswellfundedheadingintothe2026cycle.

The key variable is not whether legislation eventually emerges. It is how that legislation reshapes incentives within the stablecoin and exchange ecosystem. That distinction matters more for asset allocation than the headline deadline itself.

Recent regulatory filings indicate that Harvard Universityʼs endowment manager hasrebalanceditscryptocurrency-relatedinvestments,signalingthatitwastaking a more diversified approach to the digital asset sector. Through its investment arm, Harvard Management Company, the university reduced its exposure to a majorBitcoinexchange-tradedfundwhilesimultaneouslyinitiatedanewposition inanEthereumETF.Theshiftreflectshowlargeinstitutionalinvestorsarerefining their crypto strategies as the asset class matures and as new regulated investmentvehiclesbecomeavailable.

During the fourth quarter of 2025, the endowment trimmed its holdings in the iShares Bitcoin Trust, reducing the stake by roughly 21 percent. Despite the reduction, the position remains one of its largest crypto-related allocations, with millions of shares still held at a value exceeding $250 million at the end of the year. This suggests that Harvard has not abandoned its long-term conviction in Bitcoin,butinsteadadjustedthepositionaspartofnormalportfoliomanagement, potentiallytomanageriskorrebalanceexposureaftermarketfluctuations.

Atthesametime,HarvardestablishedanewinvestmentintheiSharesEthereum Trust, acquiring several million shares worth roughly $8687 million. This move markstheendowmentʼsfirstsignificantpubliclydisclosedpositioninanEthereum ETF. The addition signals its growing interest in Ethereumʼs broader ecosystem, which includes smart contracts, decentralised finance, and blockchain infrastructure,areasthatmanyotherinvestorsalsoseeascentraltothelong-term developmentofthedigital-asseteconomy.

Combined, Harvardʼs holdings in Bitcoin and Ethereum ETFs totalled more than $350 million at the end of the reporting period. Rather than indicating a retreat fromcryptoexposure,thechangesappeartorepresentastrategicdiversification across leading digital assets. The portfolio adjustment also reflects a wider trend among large investors who are increasingly incorporating cryptocurrency into traditional investment frameworks while balancing risk, liquidity, and long-term technologicalpotentialwithintheirallocations.

CME Group has announced a major expansion of its cryptocurrency derivatives market, revealing plans to introduce 24-hour, seven-day-a-week trading for its crypto futures and options contracts beginning May 29, 2026, pending regulatory approval. The initiative represents a significant shift for regulated financialmarkets,aligningthemmorecloselywiththecontinuoustradingnature ofcryptocurrencyspotmarkets.Byenablinground-the-clockaccess,CMEaims to provide traders and institutions with the ability to manage digital-asset exposureatanytime,regardlessoftraditionalmarkethours.

24-hourtradingonCMEissetto startat400p.m.CentralTimeonMay29and continue continuously on the companyʼs electronic platform, CME Globex, with only a short weekly maintenance window of at least two hours over the weekend.Weekendandholidaytradesexecutedduringthisextendedperiodwill still be processed with the next business dayʼs trade date, and clearing and settlement will follow standard regulatory procedures. This structure allows continuousmarketaccesswhilemaintainingtheoperationalframeworkrequired forregulatedderivativestrading.

The decision comes amid rapidly growing demand for regulated crypto derivatives. CME reported that cryptocurrency futures and options generated about $3 trillion in notional trading volume in 2025, demonstrating a surge in institutional interest in digital-asset risk-management tools. In addition, trading activity has continued to rise in 2026, with average daily volume reaching more than 407,000 contracts, representing strong year-over-year growth. These trends suggest that market participants increasingly rely on CMEʼs regulated marketplace to hedge exposure and gain structured access to cryptocurrency markets.

Beyondtheshifttocontinuoustrading,CMEhasalsobeenexpandingitscrypto derivatives offerings to include a broader range of digital assets. Alongside BitcoinandEthercontracts,theexchangehasintroducedfuturesproductstiedto other cryptocurrencies such as Cardano, Chainlink, and Stellar. This expansion reflectsthegrowingmaturityofthecryptoderivativesecosystemandthedesire among institutional traders to access diversified digital-asset exposure within regulatedfinancialinfrastructure.

The US Securities and Exchange Commission SEC Thursday, February 26, allowing broker-dealers to apply a 2 percent haircut to proprietary positions in certain stablecoins, a significant reduction from the 100 percenthaircutsomefirmshadpreviouslyimposed.

Under customer protection rules, broker-dealers must apply haircuts to reflect asset risk. By signalling that a 2 percent deduction for stablecoin holdings is sufficient,theSECiseffectivelyaligningstablecoinriskmorecloselywithmoney market funds, which hold similar underlying assets such as US Treasuries and cash.

SEC Commissioner Hester Peirce said stablecoins are essential for transactions on blockchain infrastructure and suggested the change could enable broader broker-dealerparticipationintokenisedsecuritiesanddigitalassets.

Market participants argue the move removes a key capital friction point. Lower haircutsimprovebalancesheetefficiency,enhanceliquidity,andsupportdeeper integrationofblockchain-basedsettlementintotraditionalfinance.

Theguidanceformspartofawiderregulatoryrecalibration.Alongsideinitiatives suchastheSECʼscryptotaskforceandProjectCrypto,federalagenciesarealso implementing the GENIUS Act, which establishes a national framework for stablecoins.

While incremental, the shift materially reduces capital constraints, bringing stablecoinsclosertothecoreofinstitutionalfinancialinfrastructure.