DNA FINANCIAL E-GUIDE

Section 1: The Financial ‘Myth(s)”

Financial Topics that you have been trained and conditioned to believe!

• Amortization Why we are misled on Mortgage borrowing?

• Refinancing Why do banks push refinancing when loan interest drops only .50%, below your current rate.

• Reverse Mortgages advantage with a Home Equity Line. No payments anymore, or income for Life? Which is best for you?

• Payment Due Date Fallacy – Why pay on the 1st of month?

• Student Loans out of control – Refinancing over & over

•

• “Zero Percent Interest” Credit Card Offers Zero to 18%

• Retirement Plans: IRA, 401k, 403b Right or Wrong X?

Which is best? TAX on the SEED, or TAX on the CROP?

• Credit Scores and How to keep 700+ score every month.

• Savings: Risk vs. Equity – The unknown or No Mortgage at all?

• Investment Risk vs Tax-free Choices Pay ZERO Tax

• Wills & Trusts – Why, How or Do-it-yourself in the cloud.

Section 2: The “Truth” (s) How to?

The DNA Course 90-days to Wealth and Debt Free

• The truth about financial strategies that contradict what you’ve been taught and conditioned to believe.

• The truth about debt, about getting to zero debt as quickly as possible, and paying less interest to the banks

• The truth about mortgages, refinancing, and amortization

• The truth about loan “due dates” and using them to your advantage (leverage)

• The truth about “interest only” loans, good or bad?

• The truth about savings vs. equity (leverage like Banks)

• The truth about investment risks vs safety? and Results

• The truth about credit scores and using it to your advantage (leverage like the bank’s game).

Pg. 1

Section 3 - The “Rescue” - The DNA 90-Day Course Solution

Commit to the DNA 90 day course and surrender (in a good way) to financial facts. Test and eliminate the myths that you have been taught and conditioned to believe.

Start today by learning how to convert debt and savings to wealth it is possible! We are doing it and you can too. Learn how to live a “Rich” life, be able to make any adjustments and changes with your cash flow each week or month, plus be able to see the future results instantly. The Dashboard of our software is just like the dashboard in your car. Find out how our Course can keep your Financial tank full every week.

THE COURSE – THE SOLUTION: This valuable Course uses a Software tool that tells you how you can take action to ensure paying the Bank less interest regardless of your mortgage rate. Plus, it shows you exactly how you can save thousands of bank interest in your own pocket. Whether the rates go up, or down or stay the same, you will end up with an equivalent rate of less than 2% 3% without refinancing. In addition, it will help you evaluate whether to refinance to a lower rate, including all the upfront fees.

The bonus you will get with the course is you can also alter different scenarios using hypothetical numbers to take advantage of your IRA, 401k, or 403b plan. In many cases, your investment portfolio can be added and see instant results of your decisions, mathematically, for instant scenarios.

This financial course will arm you with more knowledge that applies to you, your exact numbers, not what a generic brochure or pitch illustrates. When you take this course, it goes beyond just saving interest on your mortgage, it arms you with information that encourages positive financial results every week, every month for you and family.

This course will improve your lifestyle, your credit scores and increase your savings at an amazing pace. So, before you apply for a mortgage or are deciding to refinance your home or are renting and looking to buy………

CALL US FIRST! We can provide you with an advanced technology analysis that will help you mathematically make the best decision. No need for any social security number, no account numbers, just the numbers on any current statement of all your debt and interest. Complete the DNA Worksheet

Pg.

2

FINANCIAL MYTHS The Problem

A – AMORTIZATION MYTH: by definition - Amortization is an accounting technique used to periodically lower the principal of a loan or intangible asset over a set period of time. The term "amortization" is often related to a Mortgage that is paying off the original debt through monthly payments. Combined part principal reduction and interest costs over a set number of years. Example over 10, 15, 20 or 30 years

• Mortgage rates have seen major highs and lows since Freddie Mac started tracking them in 1971. Rates have gotten as high as 18.63% and as low as 3.31% for a 30-year fixed rate loan.

Problem: The method of interest being charged from a lender to the borrower appears to be a fixed number or interest rate. Such as 5% for 360 payments. When you look at the Amortization Table a bank prepares for each loan, the confusing aspect of the Loan is the Interest costs and how they are calculated using a skewed acceleration method. Result is favoring the bank. They receive more interest in the first 10 years of the loan and then more principal in the last 10 years of the loan.

Let us look at the Math - when you take the monthly payment of $534.00, the Principal payment is only 22% of that payment and Bank Interest is 78%. In the 10th year the Principal is then 37% and Interest is 63% of that 120th payment. To borrow $100,000 at 5% your paying back the bank a total of $193,246.

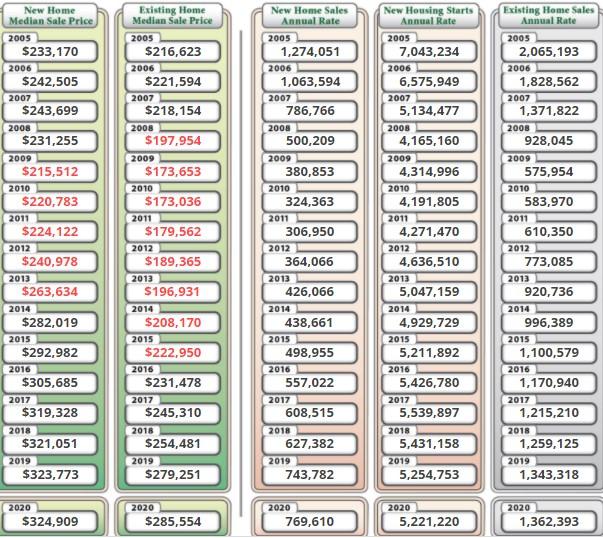

The average Mortgage amount borrowed in 2019 was $354,500. That loan would pay back to the bank over 30 years, $683,092. So, a house that sold for $404,500 with $50,000 down payment, is costing $783,092 over 30 years. Result, the home needs to appreciate +2.75% per year for 30 years, just to break even.

The Charts on page of the appendix illustrate the above data.

Pg. 3

AMORTIZATION MYTH: Now we have discussed the Problem and reviewed the MATH, let’s look at the SOLUTION. In an effort, to make better decisions, based on the math only, not bias or pitches; should you refinance a mortgage at a lower rate; $100,000 borrowed at a fixed rate of 5% for 360 months, has a monthly payment of, $

THE BANK PITCH: If you’re looking to refinance your mortgage, it’s important to know what interest rates, monthly payments and loan terms may be available to you. Just a half a point difference in your rate could mean you save thousands of dollars over the life of your loan. If you shorten your loan term, it may mean you could pay off your loan sooner and enjoy your home debt free.

PROBLEM The Banks intend to illustrate that if your rate is lower, then your monthly payment will be lower, thereby saving money to invest or buy more stuff. You now know what Amortization math means, the interest you have been paying for the past 3 to 5 to 10 years has been accelerated during that period. As a result, if you refinance you then start the same accelerated interest costs all over again in the next 10 years. So how do you get the real facts and math, to make a refinance decision? Let us help.

SOLUTION: When you obtain a free math report through our DNA Analysis, you will be able to compare the math. We take your current numbers, then our proprietary software combines all the different interest rates you have with Credit Cards, Loans, Student Loans, Car loans and more. Our free Analysis enables you to see the future results, how much money you could save in interest and what it would be in 30 years, versus your current plan. To refinance or not? By using a more cost effective method, with our 90 day Financial Course, you get the truth. During the course you will be able to not only see the results mathematically today, you will be seeing exactly how to bring a current mortgage down to the equivalent of less than 2%, without refinancing. The Analysis is free, the result is amazing.

Pg. 4

PAYMENT DUE DATE MYTH – we have been conditioned to pay bills and mortgages on the 1st of each month. That’s when they ask for us to pay them, thinking we would drop our credit scores, if not on time.

Read the Mortgage Note: When you close a Mortgage and exchange paper for the key to the house, the Bank by law, provides 2 statements. The Note and the Amortization schedule. (see Appendix page ___)

The Note you sign, guarantees personally and conditionally by having a first lien on your home, has a paragraph detailing when the payment is to be made. It is requested and expected on the first of the month.

This is the traditional Clause: Reporting to the Credit Bureaus

After 15 days, your payment is officially "late." However, even a mortgage payment made more than 15 days late won't be reported as delinquent to any credit bureaus. It's only when your mortgage payment is more than 30 days late that it might be reported as such to the credit bureaus. This can drop your credit score by 100 points or more in some cases, and the late payment will remain on your credit report for seven years. If you're heading into creditreporting territory, it's a good idea to speak to the bank and open negotiations for a payment holiday or temporary reduction in payments until you get back on your feet financially. Never forget, though, that mortgage payments are accounted for on a business day basis.

HOUSEHOLD CASH FLOW: Think about it. Banks leverage cash flow, deposits, withdrawals and then can borrow from the Fed against deposits. Banks balance their books every day. When you use a check book cash is deposited to the bank, in and out of your checking account, you do not get Leverage. WHY NOT? Many people state, “I have the money on the 1st, why not pay it” on the 1st?

What if you were getting 8% on your deposits into your check book? would you pay on the 1st or wait for 15 more days interest on your own account? If you deposit your paycheck on the 1st, then leave it there for 15 days, you can earn interest and then pay the mortgage on the 15th. In fact, you could pay it on the 30th, online. Late fees are usually $10 or $15. Do you see that leverage? Remember, no negative reporting to Equifax.

Most people live “paycheck to paycheck” and this is mostly why that phrase has evolved, you get paid on the 1st, then write all your debts and bills and have to wait until 1 week, 2 weeks or monthly to pay it all over again. WHY?

Pg. 5

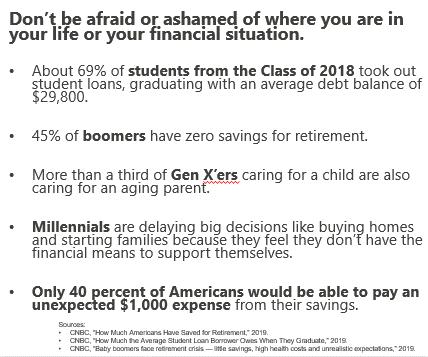

Student Loans out of control – Refinancing over & over

The high costs of College today have created a burden on parents and children. Yet, postponing the interest and payments until a graduate gets a job, is one way to provide temporary relief. But is rarely a solution. In fact, the current system practically encourages refinancing student loan debt, over and over.

However, if a graduate has no credit or only 1 Trade line, then making payments on time, will help increase their credit scores.

Student Loan types are not 30 year mortgages, so the payment is higher than sometimes your take home pay. Take a look at the difference in minimum payments on $39,838 student loan.

CHARTS

30 YEAR PRINCIPAL and INTEREST @4% = $ _________

10 YEAR PRINCIPAL and INTEREST @4.0% = $ _________

Pg.6

ZERO PERCENT CREDIT CARD MYTH:

For how long?

Maintaining a 700 Credit Score is difficult to accomplish.

THE CREDIT SCORE is essential to understand, especially the differences between a Home or Investment property mortgage, an Equity Line on your Home, or an 18-month ZERO rate Credit Card and a car loan.

The FICA score for Mortgages uses the Mid-score number, like in many Olympic sports events, they drop the low score, then drop the high score and the Mid-score is used for approval determination. Since there are 3 credit card reporting agencies, each of them can report a different score, based on their method of interpretation rules.

Pg. 7

Retirement Plans: IRA, 401k, 403b Right or Wrong X?

Which is best? PAY TAX on the SEED, or TAXES on the CROP?

Pg. 8

CREDIT SCORES

How to Keep 700+ mid score every month.

Pg. 9

INVESTMENT RISK? TAX FREE or basic Savings Plans, or Retirement plans.

Which type is best for you? How to evaluate RISK versus REWARD?

Investments in the Market – Stocks, Bonds, ETF? Index Funds, Mutual Funds?

Tax deferred Retirement Plans? IRA, 401k, 403b

Building Equity every month on a tax-free basis up to $500,000 of gains? Which Investment can do this?

Finding the Facts about Modified Endowment Clause in Life Insurance.

Why is a Life Insurance Dividend from a Mutual Life company, different than a stock or bond dividend?

How can the newest TERM Life Insurance design provide CASH for illness or injury, withdrawal without any cash value savings?

What does Conversion of Term to Permanent Life Insurance really work and how can you take advantage of this strategy?

Pg. 10

Which Risk is best for you? Taxable risk versus Tax Free for LIFE. Do not get fooled with terms like Guaranteed Cash.

The “Mortality Merchants” was written in the 60’s, by the Pennsylvania Insurance commissioner. Not much has changed for the benefit of the consumer.

The FACTS tell all and understanding any type of CASH SAVINGS life insurance policy is key to what this Myth is about. There are 3 types of Risks in our DNA Course, that we discuss in depth.

Pg. 11

Out

3.

1. Taking control of RISK –2.

of Control RISK –

No control at all RISK -

What is the Value of having Wills & Trusts: Why bother, after all I am not here to worry about anything, at that point? Why, How, Low-Cost Solution

Pg. 11

SUMMARY – THE ACTION PLAN

pg. 12

For more details and how to take-action, email to: debtnetworkacademy@gmail.com

AUTHOR’S NOTE – HOW IT ALL STARTED AND WHY?

There are 3 key factors in building wealth realistically. I emphasize realistically, due to the false hope of Math results that are promoted, such as assuming an 8% average return for 10 years. When you attempt to build wealth, we work with your numbers, not hypothetical scenarios. We use 3 primary factors.

TIME - MONEY – MATH

The value of time equates to your age. If you are 20 years old versus age 70, that makes a huge difference in reality, right? Time is gauged by understanding Life Expectancy. Back in the early years of my starting out to complete my Life Insurance licensing in 1970, Life Expectancy was to age 65. Today, due to the longevity of Health maintenance and advanced drug inventions, Life Expectancy is now nearing age 78. Also, age of 72 is age to retire.

We humanly lack the full understanding of how precious time is especially as we get older. We fail to realize that you cannot get many things back in life due to the fact we cannot live to age 100. We may live that long, but not in the law of Life Expectancy.

Once time is gone, it’s gone, history. However, when you create the synergy between Time, Money, and Math, you then bring reality into perspective. How long in Time, is the result I want?

If you understand your Time value goals, coupled with Money and Math, you can actually see the reality of how wealthy you can get today and in Retirement. Once you understand this concept, all you need now is the technology to be able to Master this system. You get to realize and see what you do with your money, mapping each week how you can exponentially save and invest more money than you realize you have. Just like having a Genie on your shoulder.

This is how I created the DNA Financial Myths, due to the ability to use Time, Money and Math within a technology platform. Sounds simple right? What is the true value of Time using Money and Math

So, Chuck, when you were evaluating taking the DNA financial course, what specifically was attractive to you, was it only the advanced Technology?

We not only looked at what the technology does and the opportunities that it’ creates for our making better financial decisions, but we also looked at the entire course package".

“What else do we get when we take this course”

"Do we get any Tech support?

"Do we get someone we can talk to that is not out of the country?

More importantly, are the support team and mentor using the software itself?

Those answers helped us make our decision, we are not just buying technology or a product, we have an entire team of people. to help us.

After all, for $495, this was something we felt, why wouldn't we do it?