Head of Sales & Marketing 07881 502 705 graeme.foster@diyinvestor.co.uk

INVESTING IN A TIME OF UNKNOWN UNKNOWNS

Anecdotally, the period between Christmas and New Year is the busiest for brokers and platforms as, with time on their hands, people finally get around to opening an account and starting their journey to financial independence.

In the same way, accounts were opened in record numbers during lockdown because people sought certainty and control in unnervingly unfamiliar times‘Coronavirus lockdown fuels spike in DIY Investing’.

But as we eye an increasingly uncertain future, financial first footing could see geopolitical upheaval vying with social, economic and environmental crises as the key influences in the year ahead.

DIY Investor was founded in the belief that people would inevitably have to take more personal financial control as self-reliance replaced state provision.

In the last ten years that conviction has only grown stronger, but there is a very real threat that the financial certainties we have relied upon are no longer a given; possibly tipping the debate from carrot to stick, those that do not make additional financial provision, could face a seriously diminished quality of life in retirement.

And the warning signs are there for all to see. Women born in the 1950s may have thought they had everything under control as they entered a glide path to their autumn years that included access to the state pension aged 60.

However, the 1995 Pension Act hiked that to aged 66 today, throwing plans for potentially millions of women into disarray. Chancellor Rachel Reeves recently confirmed that no compensation would be paid; I’d be a bit ‘Waspi’ too. There are almost too many metaphorical elephants to consider.

Adult social care is just another political hot-potato with the potential to scupper the best laid financial plans; fully 25 years after Labour’s plans were dubbed a ‘death tax’ and 18 years since the Tory version was derided as a ‘dementia tax’, Health and Social Care Secretary Wes Streeting, has just announced yet another enquiry, due to report in 2028.

It is an intractable problem that sucks in questions over other key issues such as low pay and immigration; there appear few grounds for optimism, and the sky-high cost of residential care could blow away even the most diligently constructed financial plan.

Whether it is better to have striven and had your nest egg taken away, or to never have lifted a finger, is philosophy 101.

Exaggerating only for effect, what about when Doge tsar Elon Musk, high on the Reform victory he funded, is rewarded with a brief to improve efficiency in the NHS.

On day one he identifies treatments and procedures that will no longer be automatically funded and hands you a menu of pricing options for you to fund your own care.

Too fanciful? Didn’t you once have an NHS dentist.

Those not wishing to be subject to the vagaries of a government struggling to fill the ‘black hole’ or Trump tearing up the Net Zero playbook, simply must weigh in.

And that is why DIY Investor will redouble its efforts to make understanding and analysing risk, an integral part of the investing process.

In 2002 US Secretary of Defense Donald Rumsfeld told us there are ‘unknown unknowns’ and introduced the ‘Awareness-understanding matrix’

It’s not as complex as it may seem at first glance, but if universally adopted, and delivered alongside an assessment of probability, could provide a standardised way of conducting apples-and-apples comparisons of all kinds of investments.

Knowing and accepting that there are unknown unknowns is part of acknowledging and accepting risk and a basis to move forward as an investor.

Now, more than ever - ‘Do it Yourself, Do it With me, Do it For me; just don’t do nothing!’ Happy New Year.

MAKE SURE YOU DON’T MISS AN ISSUE; CLICK HERE TO RECEIVE DIY INVESTOR MAGAZINE TO YOUR INBOX

To invest with confidence, seek out experience.

abrdn Investment Trusts

Now more than ever, investors want to know exactly what they’re investing in.

abrdn investment trusts give you a range of carefully crafted investment portfolios – each built on getting to know our investment universe through intensive first-hand research and engagement.

Across public companies, private equity, real estate and more, we deploy over 800 professionals globally to seek out opportunities that we think are truly world-class – from their financial potential to their environmental credentials.

Allowing us to build strategies we believe in. So you can build a portfolio with real potential. Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested.

MURRAY INTERNATIONAL TRUST MANAGERS DISCUSS THE IMPORTANCE OF GEOGRAPHICAL AND SECTORAL DIVERSIFICATION IN GLOBAL INVESTMENT PORTFOLIOS, PARTICULARLY AS US MARKET DOMINANCE REACHES AN ALL-TIME HIGH

Martin Connaghan, Co-Manager, Murray International Trust

KEY HIGHLIGHTS

• US dominance of global stock markets is at an all-time high.

• Donald Trump will return to power in January.

• Murray International strives for a more geographically and sector-diverse portfolio.

The US remains the largest and most liquid stock market in the world. It has been the birthplace for a number of the world’s most innovative companies and remains one of the faster growing developed economies. However, it is now a huge weight in many major global indices, and this may be a risk for investors – whatever thoughts they may have on the emphatic results of the recent presidential election.

After what had been a bad-tempered contest, Donald Trump declared victory in the early hours of November 6th with what he termed “an unprecedented and powerful mandate”.

‘IT IS NOW A HUGE WEIGHT IN MANY MAJOR GLOBAL INDICES, AND THIS MAY BE A RISK FOR INVESTORS’

The President Elect has a fully formed plan of action for when he returns to the White House in January, with material policy changes lined up. The recent period of US political uncertainty is now at least over and global leaders have rushed to congratulate Trump on his emphatic victory. However, no one yet knows what the impact of the forthcoming US policy changes will be on relationships between the US and its overseas partners.

Samantha Fitzpatrick, Co-Manager,

Murray International Trust

BURGEONING DEBT BACKDROP

While politics may not always have a direct bearing on the fortunes of individual companies, the recent political fragility in the US needs to be set against the backdrop of burgeoning debt in the US. The US debt is currently $35.7 trillion, 10x that of the (also highly indebted) UK. It is taking up an increasingly vast share of government revenues. Trump will likely cut taxes, implying that he has no plans to address this deficit.

This appears a precarious backdrop, and one that could dent sentiment towards the US market. Yet US dominance of global stock markets is at an all-time high. The MSCI AC World is now 64% weighted to US stocks. Within that US exposure, there is also high concentration in technology companies, and the Artificial Intelligence (AI) theme in particular – Apple, Microsoft, Nvidia, Amazon, Meta and Alphabet comprise around 18% of the MSCI AC World index.

This also creates risks. The US technology sector has been a superb place to be invested over the past decade for capital growth, but the circumstances are different today. Interest rates are structurally higher, which typically creates a less favourable environment for high growth companies. Valuations are also higher. Apple, for example, has seen its price to earnings ratio double over the past five years. Nvidia’s price to earnings ratio is also double its level since October 2022. These companies are growing fast, but if that is already in the valuation, they may not make good investments.

‘THE US TECHNOLOGY SECTOR HAS BEEN A SUPERB PLACE TO BE INVESTED OVER THE PAST DECADE FOR CAPITAL GROWTH’

A CONCENTRATION ISSUE

This concentration is an issue for passive funds, but also for any global fund where the starting point is the index. These funds are likely to contain similar biases and will focus on the same handful of US technology companies. This argues for introducing greater diversity into a portfolio. Given the distinct investment objective of Murray International, we believe in a ‘blank slate’ approach, paying far closer attention to a company’s ability to grow its capital and dividends over time, than its weighting in an index which would not actually deliver the investment mandate.

This creates a more geographically and sector-diverse portfolio. We do find opportunities in North America, but it is 29% of the portfolio and there are no holdings in the mega-cap technology companies which pay little or income. We hold similar weighting in Europe (24%), Asia ex Japan (24%), and the rest of the world, with significant holdings in areas such as Latin America, which barely feature in the MSCI AC World index. The sector mix is also broader, with around 16% in technology, but also 17% in financial services, another 16% in consumer-facing companies, and around 13% in healthcare.

The AI theme is still represented in our portfolio: we recognise its long-term growth potential – but we are investing in it through companies where we believe valuations are more compelling and income is also available, including Taiwan Semiconductor Manufacturing (TSMC). TSMC makes the majority of Nvidia chips, and yet trades on a far lower valuation.

‘WE BELIEVE IN A ‘BLANK SLATE’ APPROACH, PAYING FAR CLOSER ATTENTION TO A COMPANY’S ABILITY TO GROW ITS CAPITAL AND DIVIDENDS OVER TIME’

AI is also a new technology, which brings risks, which is why our portfolio is balanced across a range of ideas, many of which are only lightly represented in a typical global equities portfolio. Our aim is to have a range of different moving parts, with different factors contributing to performance. The trust has always looked distinct from the index and continues to do so. We would worry if all the portfolio started to move in unison.

This is also important in fulfilling our income objective. Growing the income on the trust year in, year out, means having a diversity of income sources. We cannot be reliant on a single sector, country or type of company for income. We draw income as widely as possible.

EVERY POSITION COUNTS

Unlike an index-focused portfolio, we try to ensure that every position counts, holding a minimum of 1% and maximum of 5% in each position. While the MSCI AC World index has some exposure to Latin America, it is less than 1%. This means it is often neglected by investors. Not only is this an oversight – Latin America has been the best-performing region in 11 out of the previous 26 years in Sterling terms – it creates mispricing that can be exploited. We hold around 9% of the trust there, spread across six holdings.

Our ‘go anywhere’ approach gives us real flexibility to exploit mispricing when markets are temporarily derailed by factors that are unlikely to matter in the long term. For example, in Mexico, market confidence has been knocked by the uncertainty surrounding the new President, and her reform agenda. We don’t believe her accession will significantly impact holdings such as Mexican airport operator Grupo ASUR. The company has just paid a large special dividend, which has helped cushion short-term volatility in its share price.

We are long-term in our time horizon, which helps us navigate volatility.

‘OUR

‘GO ANYWHERE’ APPROACH GIVES US REAL FLEXIBILITY TO EXPLOIT MISPRICING WHEN MARKETS ARE TEMPORARILY DERAILED’

For example, our new holding in Mercedes has been volatile since initiation: the company has undergone some restructuring, and the car industry is difficult. However, we can wait for its value to be recognised by the market, and in the meantime, the company is paying an attractive and growing dividend, which appears to be well-supported by cash flows.

The US is important, but it has become a very large part of global stock markets and there are potential growing risks. We believe it is important to have more balance in a global portfolio, looking beyond the US for growth and income opportunities at the individual stock level.

Companies selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or indication of future performance.

There is no guarantee that the market price of the Company’s shares will fully reflect their underlying Net Asset Value.

As with all stock exchange investments the value of the Company’s shares purchased will immediately fall by the difference between the buying and selling prices, the bid-offer spread. If trading volumes fall, the bid-offer spread can widen.

With funds investing in bonds there is a risk that interest rate fluctuations could affect the capital value of investments. Where long term interest rates rise, the capital value of shares is likely to fall, and vice versa. In addition to the interest rate risk, bond investments are also exposed to credit risk reflecting the ability of the borrower (i.e. bond issuer) to meet its obligations (i.e. pay the interest on a bond and return the capital on the redemption date). The risk of this happening is usually higher with bonds classified as ‘sub-investment grade’. These may produce a higher

MURRAY INTERNATIONAL TRUST: ELEVATOR PITCH

level of income but at a higher risk than investments in ‘investment grade’ bonds. In turn, this may have an adverse impact on funds that invest in such bonds.

Yields are estimated figures and may fluctuate, there are no guarantees that future dividends will match or exceed historic dividends and certain investors may be subject to further tax on dividends.

The Company invests in emerging markets which tend to be more volatile than mature markets and the value of your investment could move sharply up or down.

Other important information:

Issued by abrdn Fund Managers Limited, registered in England and Wales (740118) at 280 Bishopsgate, London EC2M 4AG, authorised and regulated by the Financial Conduct Authority in the UK.Find out more at www.abrdn.com/MYI or by registering for updates. You can also follow us on X and LinkedIn.

IMPORTANT INFORMATION

Risk factors you should consider prior to investing:

• The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested.

• Past performance is not a guide to future results.

• Investment in the Company may not be appropriate for investors who plan to withdraw their money within 5 years.

• The Company may borrow to finance further investment (gearing). The use of gearing is likely to lead to volatility in the Net Asset Value (NAV) meaning that any movement

in the value of the company’s assets will result in a magnified movement in the NAV.

• The Company may accumulate investment positions which represent more than normal trading volumes which may make it difficult to realise investments and may lead to volatility in the market price of the Company’s shares.

• The Company may charge expenses to capital which may erode the capital value of the investment.

• Movements in exchange rates will impact on both the level of income received and the capital value of your investment.

WATCH VIDEO HERE

To be ahead in Asia, be on the ground.

abrdn Asian Investment Trusts

In Asia, life and business move fast. To invest here successfully, you need local knowledge.

abrdn has had investment teams in Asia for almost 40 years. So we get to know markets, companies, trends and innovations first hand. And you get to select from investment trusts featuring the most compelling Asia opportunities we can find.

To harness the full potential of Asia, explore our Asian investment trusts on our website.

Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested. Asian funds invest in emerging markets which may carry more risk than developed markets.

EARNINGS AT MANY OF AIE’S HOLDINGS REMAIN STRONG… BY

DAVID KIMBERLEY

The seemingly endless turmoil the world has seen over the past few years has made it very hard not to engage in macroeconomic predictions.

Two years ago it was what the impact of Covid lockdowns would be. Today investors are more focused on inflation and how far central banks will go in hiking interest rates.

It is easy to understand why investors like to partake in this sort of behaviour. Take interest rate hikes as an example. Leaving aside how they are used as an input for valuing assets, rate hikes may lead to an economic slowdown, which would in turn lead to many companies performing poorly.

However, attempting to make macroeconomic calls like this is extremely difficult and you can end up a bit like the inhabitants of Laputa from Gulliver’s Travels, engaging in an activity that seems deeply logical but is ultimately closer to pseudoscience.

This is part of the reason that the analysts and managers of Ashoka India Equity (AIE) avoid making such calls. The managers views on doing so are captured succinctly by a letter they wrote to shareholders in 2021, where they noted that “decisions that are bereft of bottom-up fundamental analysis and are instead driven by macro considerations, are fraught with high risk of substantial absolute and relative losses.”

It is worth noting that this does not mean macroeconomics is irrelevant. That something is hard to predict is not the same as saying it has no impact. But to try and make precise predictions to the detriment of actually analysing the companies you’re investing in is not likely to end well. Perhaps more importantly, doing proper due diligence on the companies you’re investing in can often negate the negative impact a future event you’re concerned about may have.

‘DOING PROPER DUE DILIGENCE ON THE COMPANIES YOU’RE INVESTING IN CAN OFTEN NEGATE THE NEGATIVE IMPACT A FUTURE EVENT’

AIE’s portfolio arguably illustrates this. The managers have developed an in-house cash flow analysis system and also spend a significant amount of time undertaking due diligence efforts on prospective investments. They also avoid companies whose success is more driven by cyclical factors, as well as those that are more at risk of being beholden to a small group of stakeholders, like a family owner.

It is still early days and we may indeed see more of an impact if we do head into an economic downturn. However, even after a period of inflation, rate hikes and perpetual uncertainty, we can see that companies in the AIE portfolio continue to perform well.

For example, Titan Co is one of the trust’s largest holdings. The company sells watches, jewellery, eyewear and clothing, via its own brands and third-party companies. Although it has begun expanding abroad, the bulk of the company’s revenue is derived from India.

In its most recent financial results, the company saw a 50% uplift in its year-on-year profit numbers during the last quarter. Significantly, the firm saw growth across the segments it operates in, although more than three-quarters of revenue comes from its jewellery business.

It’s plausible that this was driven by a desire for ‘real’ assets as inflation rises. However, Titan has seen its revenue rise every year, bar one, for the past two decades, with a compound annual growth rate of close to 20%. The most recent quarterly growth may be more pronounced but it fits with the broader trend we’ve seen drive the company’s success, namely a growing demand for discretionary consumer goods in India, where the average annual salary is now close to $5,000.

‘IT

SEEMS WISER TO FOCUS ON FINDING GOOD COMPANIES THAT CAN PERFORM WELL IN A DOWNTURN, RATHER THAN TRYING TO DETERMINE EXACTLY WHEN THAT DOWNTURN MIGHT HIT’

Avalon Technologies, another AIE top 10 holding, represents a similar growth story but with a different customer base.

The company was founded in 1999 and manufactures components for a variety of industries, including the clean energy and communications sectors.

The company held its IPO in April and saw a 30% uplift to revenue in its most recent results but a near doubling in operating income, as the increase in sales was not offset by a commensurate increase in costs.

Unlike Titan, which is benefitting more from the growing wealth of Indians, Avalon’s success seems more driven by the move away from manufacturing in China. For example, Apple want to shift 25% of global iPhone production to India by 2025. Samsung also announced in February that it will invest over $200m to build a new refrigeration manufacturing

THEMES FOR YOUR ISA WEBINAR –ASHOKA INDIA EQUITY

Disclaimer: Disclosure – Non-Independent Marketing Communication This is a non-independent marketing communication commissioned by Ashoka India Equity. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

facility in India, adding to the mobile phone facilities it already has in the country.

Is it plausible something will derail these trends and harm Avalon’s prospects? Perhaps. But for now the company, along with other AIE holdings, is still producing strong cash flows and earnings growth.

And the trust’s decision to invest in the firm was based on those types of factors, as opposed to what external forces may or may not impact it. Given that AIE delivered annualised share price total returns of over 14%, in GBP terms, since its IPO in July 2018 through to the end of May 2023, it’s probably fair to say that – at least so far – it’s a strategy that’s held up well.

As is probably clear from this article, predicting whether or not that will continue isn’t easy to do. But as the spectre of an economic downturn looms in the distance, it seems wiser to focus on finding good companies that can perform well in a downturn, rather than trying to determine exactly when that downturn might hit.

SEE THE LATEST RESEARCH ON AIE HERE

A SIGNIFICANT CAPITAL ALLOCATION SHIFT IN THE UK

THE INCREASING POPULARITY OF SHARE BUYBACKS IN THE UK MARKET BY SUE NOFFKE, HEAD OF UK EQUITIES

Anyone who follows the UK investment trust industry will be familiar with the concept of the share buyback as a mechanism for managing the discount between a trust’s share price and its net asset value (NAV). They are a commonly used tool, increasingly so in the current environment in which, discounts have notably widened.

Not everyone is a fan of them, but the economic argument in favour of the buyback is simple and strong. From the perspective of demand, a buyback programme introduces an additional buyer of the trust’s shares which can put upward pressure on the share price. As a secondary impact, the presence of the buyback can also signal confidence in the trust’s underlying assets and strategy, which may attract more investor interest over time, further increasing demand.

‘THE PRESENCE OF THE BUYBACK CAN ALSO SIGNAL CONFIDENCE IN THE TRUST’S UNDERLYING ASSETS AND STRATEGY’

Meanwhile, from the perspective of supply, a share buyback reduces the number of shares in circulation for the trust in question, thereby enhancing earnings and dividends on a per share basis. Remaining shareholders are therefore rewarded by owning a larger proportion of the trust as a whole. Furthermore, buybacks only make sense when a trust’s shares are trading at a discount –by definition, this means the investment trust is effectively buying itself back at the price implied by its share price, which is lower than its NAV. This also has a beneficial impact for shareholders, because NAV per share is enhanced. The greater the level of discount, the more value that accrues to shareholders.

On a daily basis, most investment trust buybacks are modest in scale, but if conducted consistently and with discipline, they can have a very material impact for shareholders over time. Taking the maths to an extreme, if an investment trust retires half of its equity over a period, all other things being equal, its earnings and dividends will double on a per share basis. All other things never are equal, of course, but it is difficult to argue against this powerful logic.

A POTENTIAL STRATEGY FOR ANY COMPANY

Investment trusts are listed businesses and undertake share buybacks within the framework of UK company law, specifically the Companies Act 2006. This permits companies to repurchase their shares, provided they have the necessary shareholder approval and can meet solvency requirements. The same legal principles apply to all UK listed businesses, and while companies operating in industries outside of the investment trust sector may not need to worry about managing their discount to NAV, management teams are often highly sensitive to their market rating and can utilise buybacks to return surplus capital, improve financial metrics and signal market confidence.

In an environment where most market commentators acknowledge the significant undervaluation of the UK stock market, both in the context of history and when compared to other regions, we should not be surprised to see share buybacks becoming more popular with UK company management teams.

‘MOST MARKET COMMENTATORS ACKNOWLEDGE THE SIGNIFICANT UNDERVALUATION OF THE UK STOCK MARKET’

Across its recently completed financial year, some 29 (more than 60%) of the portfolio holdings in Schroder Income Growth Fund plc – an investment trust I have had the privilege of managing since 2011 – conducted share buybacks. This compares with 17 (38%) of the fund’s holdings in the prior year. This is a significant increase, which encompasses a broader range of companies across a wide range of sectors and all sizes.

I believe this is a very positive development – for shareholders in trust and for the UK stock market more broadly –for three key reasons. Firstly, we have a strong preference for businesses with healthy cash flows and solid balance sheets – these types of businesses have the resources to deploy towards share buybacks when the time is right [1]. Secondly, this is a clear indication that the management teams responsible for the companies in which we have invested have the inclination to reward their shareholders.

And thirdly, the increasing prevalence of share buybacks in the UK is a sign that businesses recognise that their shares are undervalued and are increasingly looking to do something about it. As is the case for investment trusts, the more undervalued a company’s shares are, the more value can be created by retiring equity.

CLEARING THE HURDLE

Indeed, it could be argued that management teams should view the returns they can achieve on a share buyback as a “hurdle”, which any other potential use of surplus capital must clear in order to proceed. If the projected returns on, for example, an investment in new facilities or a potential acquisition, are not as attractive as the hurdle rate of return delivered by a buyback, then that particular use of capital should perhaps not be pursued. This would demonstrate good capital discipline.

Ultimately, businesses that have shown such capital discipline in the past have been rewarded for it. One that we have held in the past in the Schroder Income Growth Fund portfolio is the retailer Next. Its management team has consistently demonstrated capital discipline in recent years by using surplus cash flow for a combination of share buybacks (when the shares have been lowly valued) or special dividends (when the shares have been more fairly valued). Between 2000 and 2023, overall group sales growth was relatively modest (5.7% per annum).

However, over the same period EPS and DPS grew annually by 12.5% and 10.4% respectively. Good control of costs played a role here too, as did a degree of operating leverage, but a significant part of this per share growth stemmed from the consistent deployment of share buybacks. Share price performance was even more impressive (+15.3% annualised total return), with the valuation of the shares rising as the market increasingly came to appreciate the company’s impressive capital discipline[2]

Next isn’t currently held in the Schroder Income Growth Fund portfolio, but we are confident that the successes of the past can be emulated by the many undervalued UK companies that are currently demonstrating a similar degree of capital discipline.

‘AS WELL AS DELIVERING A DIVIDEND YIELD OF 5.5% TO SHAREHOLDERS ANNUALLY, SHELL IS CURRENTLY IMPLEMENTING A $3.5BN BUYBACK PROGRAMME’

Among them is Shell. As well as delivering a dividend yield of 5.5% to shareholders annually, Shell is currently implementing a $3.5bn buyback programme, having already returned £13.5bn through buybacks over the last 12 months[3]. Shares outstanding have already reduced by 20% since 2019, which is already making a material difference to the company’s per share financial metrics.

Another example is the mid-cap construction business, Balfour Beatty. Among its many attractive characteristics is management’s consistent capital allocation policy which has delivered £755m in shareholder returns over the last four years through dividends and share buybacks.

This represents almost a third of its current market capitalisation. It has retired more than a quarter of its shares in issue during this period and, notably, its share price has more than doubled[4]

Other examples of portfolio companies that are currently buying back shares include Unilever, NatWest, Qinetiq, Hollywood Bowl and Lloyds. Indeed, with well over half of the current portfolio’s constituents having bought back shares in the last 12 months, this represents a profound shift in capital allocation decision-making that spans a wide range of sectors and all parts of the market cap spectrum. All, however, are united by their management team’s belief that buying back shares is a disciplined and value-enhancing use of surplus cash flow.

GAME CHANGER

To conclude, it certainly doesn’t surprise me to see so many buybacks in the UK currently. It is well observed that the UK stock market is currently undervalued. Indeed, it may represent one of the cheapest asset classes available to investors anywhere in the world.

This is not new news, however, and readers may be becoming bored of being told it. What is new is that the current trend towards share buybacks[5] is potentially powerful enough to ultimately make a difference to this undervaluation. As we have seen from the case study of Next – and many other businesses around the world that have consistently bought back their shares to the benefit of their remaining shareholders – eventually, the market responds.

‘REASONS TO BE INCREASINGLY POSITIVE ABOUT THE OUTLOOK’

Perhaps it is already happening. It is interesting to note that the share prices of all the portfolio holdings mentioned above as examples of businesses that are buying back shares are, at the time of writing, up by more than 25% year-to-date[6]

Company management teams aren’t the only marginal buyers of UK equities, however. Overseas corporates are also responding to the undervaluation of UK plc by stepping in and bidding for domestic companies at a record rate. Although this is immediately positive for the shareholders of the companies that are being acquired, it does raise broader longer-term issues about the health of the UK stock market and the broader financial ecosystem.

Hence, we are seeing more public discussions around structural reforms which could revitalise prospects for the UK equity market. These have concerned potential changes to listing rules to create a more attractive environment to be a UK plc. There is also focus on whether more UK pension fund capital could be allocated to UK assets. If implemented effectively both of these policy initiatives could also be positive for UK equities.

Some of this improving narrative may be behind the moderation of UK equity outflows and the improved performance of UK equities over the last 12 months. We are hopeful that this will continue and would point to the increasing prevalence of share buybacks, the continued interest of overseas corporates and the prospect of more supportive policies initiatives as reasons to be increasingly positive about the outlook.

[1]It is important to note that, as active and engaged shareholders, we would not be supportive of a share buyback unless the company in question possessed this financial strength. Without it, or in situations where a company is contemplating borrowing money to retire equity, a buyback can introduce more financial risk to the investment case, which generally speaking is not a good idea. Typically, a buyback should only be considered as a use for surplus cash flow (the clue is in the name).

[2]Source: Bloomberg from 1 January 2000 to 31 December 2023. Past performance is not a guide to future performance and may not be repeated.

WHY INVEST IN SCF?

The Schroder Income Growth Fund aims to achieve income growth in excess of inflation and capital growth as a result of that rising income.

SCF has grown its dividend for 29 consecutive years, since it was launched in 1995 – a feat that has earned it a place on the Association of Investment Companies’ list of dividend heroes.

Please remember that the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

This marketing material is for professional clients or advisers only. This site is not suitable for retail clients.

[3]Source: Company records, as at 1 August 2024.

[4]Source: Company records / Bloomberg to 30 September 2024. Past performance is not a guide to future performance and may not be repeated.

[5]A buyback can introduce more financial risk to the investment case, which generally speaking is not a good idea. Typically, a buyback should only be considered as a use for surplus cash flow (the clue is in the name).

[6]Source: Bloomberg to 16 October 2024 in capital return terms. Past performance is not a guide to future performance and may not be repeated.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England.

For illustrative purposes only and does not constitute a recommendation to invest in the above-mentioned security / sector / country.

Schroder Unit Trusts Limited is an authorised corporate director, authorised unit trust manager and an ISA plan manager, and is authorised and regulated by the Financial Conduct Authority.

On 17 September 2018 our remaining dual priced funds converted to single pricing and a list of the funds affected can be found in our Changes to Funds. To view historic dual prices from the launch date to 14 September 2018 click on Historic prices

BELLVUE HEALTHCARE (BBH)’S COMBINATION OF DEFENSIVE AND OFFENSIVE QUALITIES LOOK ATTRACTIVE… BY

DAVID BRENCHLEY

Safety and comfort mean different things to different people. In an investment sense, the traditional safe havens have historically been things like government bonds, gold and the Japanese yen. That’s not been the case in the past few tumultuous years.

Egged on by the seemingly relentless rise in popularity of index trackers, the new safety has been found in the arms of mega-sized, monopolistic American technology stocks. The so-called Magnificent Seven accounted for 29.15% of the S&P 500 on 18/09/2024.

It’s helped, too, that themes du jour also play into the size argument: the artificial intelligence leader is Nvidia, a $3 trillion chipmaker, and the bigwigs in GLP-1, or weight-loss, drugs – Novo Nordisk and Eli Lilly – have a combined market capitalisation of $1.4 trillion.

This isn’t new. Think back to the 1960s and 1970s, when the Nifty Fifty (a collection of 50 buy and hold forever blue-chip US stocks) were all the rage. Still, eventually these trends come to an end – and we may be witnessing the end of the Magnificent Seven’s dominance.

‘WE MAY BE WITNESSING THE END OF THE MAGNIFICENT SEVEN’S DOMINANCE’

To be clear, we’re not suggesting that technology is in a bubble that’s about to burst. There’s no need to sell your exposure to the sector. However, a couple of recent milestones suggest that market leadership is changing.

Nvidia has been in and out of bear market territory since its June peak, leading the technology-heavy Nasdaq Composite to falter after an astonishing bull run. Berkshire Hathaway, Warren Buffett’s value-investing conglomerate recently became the first non-technology company to breach the $1 trillion market cap barrier.

Since 09/07/2024, the S&P 500, an index that weights America’s largest 500 publicly listed companies by size, has returned 1.2% in US dollar terms. By contrast, the S&P 500 Equal Weight Index, which weights the same 500 firms equally, is up 7.6%. The Russell 2000, the US small-cap barometer, has surged 8.1%.

This points to a broadening out of market leadership, which the imminent interest rate cuts from central banks could accelerate.

The US economy seems to be slowing enough to justify rate cuts, but it does continue to grow and data does not suggest that a recession is on the cards. Still, it’s certainly worth considering positioning for two potential scenarios.

A SOFT-LANDING PLAY

Smaller companies are perhaps the best way to play a scenario where the global economy skirts a recession. Recessions are particularly tough environments for small companies, because they are naturally more attuned to local economies, meaning demand for their goods can wane. In addition, banks become less likely to lend to riskier enterprises so their potential sources of capital dry up.

Fears about a potential recession may have contributed to mega-cap stocks pulling further away from their smaller counterparts. If investors start to doubt that the recession will come, that wall of cash that went into the Magnificent Seven may start to take profits that get recycled further down the market cap spectrum.

Rate cuts would also benefit smaller companies. These firms tend to have more debt than larger firms and more of it is variable, meaning the amount of interest they must repay goes up when rates do, crimping profit margins, and vice versa.

STAYING DEFENSIVE

It could pay to own some assets that might do relatively well if a recession does occur, offsetting what you might lose elsewhere but not dragging on returns too much if the landing is soft.

‘HEALTHCARE IS PERHAPS THE MORE INTERESTING AREA HERE’

We suggested earlier that mega-cap stocks seem to have become a new safe haven, but that may not hold. High valuations may scare off some investors, with profit-taking adding to the pain.

In this scenario, cash may be recycled into the more traditionally defensive equity market sectors. These include consumer staples, telecommunications and healthcare. Companies lumped into these categories tend to benefit from consistent and stable demand for their products and services and reward shareholders attractive dividends.

Healthcare is perhaps the more interesting area here. Treatments should go ahead no matter what happens with the economy – if you’re seriously ill, you will go to the doctors or the hospital, or get checked out online, recession or no recession.

MEET ME IN THE MIDDLE

One could argue that the investment company universe’s Venn diagram of small-cap and healthcare investors brings up just one match: Bellevue Healthcare (BBH).

BBH sits in an interesting area. It is predominantly small and mid-cap healthcare, giving it exposure to the higher-risk but higher-reward parts of the market such as biotechnology, which is balanced out by its investments some of the more traditionally defensive areas such as health insurers and software providers.

As mentioned, the MSCI World Health Care Index has been dominated in recent times by Novo and Eli, which have shot to prominence by being first to market in GLP-1 diabetes drugs. The two account for 14.5% of the index. This has weighted on BBH’s relative returns, leading to a long period of underperformance.

Yet, the benefits of BBH’s investment process and expertise has come to the fore in more recent weeks. Since 10/07/2024, BBH’s total share price return has been 10.2%, well ahead of the 4.2% gain for its benchmark.

BBH does have 10% of its portfolio invested in alternative investments that play into the diabetes theme, notably through Dexcom, which provides glucose monitoring systems. The portfolio is ready for phase two of the GLP-1 boom, once it broadens out from its narrow focus on two companies.

Any portfolio should, of course, be well balanced and diversified across different sectors, countries and assets and small-cap healthcare is a small part of that, but at the same time, perhaps the sector should no longer be ignored.

VIEW THE LATEST RESEARCH ON BBH HERE

Disclaimer: Disclosure – Non-Independent Marketing Communication. This is a non-independent marketing communication commissioned by Bellevue Healthcare. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

ON 2024

At Allianz Technology Trust, we embrace the transformative power of technology, so our investors can feel more confident in exploring the potential of this dynamic industry.

While tech markets can be volatile, our long-term approach and proven expertise can help you to navigate the risks and stay ahead of trends. With deep connections to global innovation hubs and a strong track record, we aim to position the portfolio for enduring growth in this exciting sector.

There has never been a more compelling time to invest in technology. We’re here to support you through the excitement and challenges of tech inve sting.

REFLECTING ON 2024

Lead Portfolio manager Mike Seidenberg, sat down with host Cherry Reynard to reflect on the past year discussinghis expectations versus how the year unfolded – mentioning some notable winners. He also shared his thoughts on the potential impact of the upcoming US presidential elections and what he’s looking forward to in 2025.

BEYOND THE BEHEMOTHS

In the 27th episode of the Silicon Valley Byte Size Podcast, Mike Seidenberg, Lead Portfolio Manager, joins host Cherry Reynard to discuss the current tech landscape, dominated by a handful of companies.

Mike discusses the importance of looking beyond these giants to uncover new opportunities, sharing his insights on the key secular themes driving long-term growth in the industry. Tune in to find out where Mike and the team are finding opportunities currently.

Disclaimer:

This is a Marketing Communication. Past performance does not predict future returns.The statements contained herein may include statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. We assume no obligation to update any forward-looking statement. LISTEN HERE

Technology powers our daily lives, from smartphones to digital payments. But what about the companies behind these innovations, the ones creating the vital components and software? Drawing lessons from history, this article underscores the importance of strategic investments in midand large-cap tech companies, as demonstrated by Allianz Technology Trust’s tried and tested approach.

KEY TAKEAWAYS

Technology has transformed societies and economies, and the pace of change is continuing with advances in sectors such as artificial intelligence holding huge promise.

That begs the question of how do investors exploit these powerful, disruptive forces? The tried- and-tested investing for growth formula at Allianz Technology Trust plc focuses on investing in medium-sized to large technology companies.

That strategy has served our investors well over the past 20 years, although investors should remember that past performance is no guarantee of future results.

Mobile phones are such an essential part of the modern world that it is easy to take them for granted and to forget how different life was before they arrived. The world’s first widely- purchased smartphone, the Apple iPhone, for example, emerged just seventeen years ago, in 2007. Today, most people could not envisage life without one.

‘THE INCREDIBLE TECHNOLOGY IN THESE HAND-HELD COMPUTERS HAS HAD A HUGE IMPACT ON SOCIETY’

From managing your finances and making digital payments to shopping online, booking a holiday or watching a film on the go, the incredible technology in these hand-held computers has had a huge impact on society. It’s a similar story with the many smart devices that now populate our homes.

The effect has been particularly profound in the fast-growing developing economies, where surging mobile penetration has transformed banking and commerce, agriculture, education, women’s empowerment, and governance. Billions of people who previously could not even open a bank account can now access business start-up loans and other financial services through their smartphones.

In Africa, for example, mobile technologies helped generate 8.1% of GDP across sub-Saharan Africa in 2022, amounting to US$170 billion of economic value added.[1]

INNOVATION IN TECHNOLOGY IS ACCELERATING

Growth in technology is also continuing, with advances in artificial intelligence (AI) and computing power promising further transformations to smartphones and other devices. AI will power phones to instantly translate conversations, make restaurant bookings, alert you to the presence of a friend in town and show the most direct route to where they are staying.

Meanwhile, AI-driven smart-home technologies will simplify daily tasks, adapting to an individual’s routines and preferences, and delivering personalised support, and will be invaluable especially for the elderly or disabled.

REAPING THE BENEFITS OF INVESTING IN TECHNOLOGY

The question for investors is how to tap into the transformative impact of these reliable, rapidly advancing and increasingly ubiquitous technologies. Fortunately, history provides a guide, and a key lesson is that the seemingly obvious route to investments in technology often proves a costly road to nowhere.

The development of the motor car, for example, was one of the most significant advances of the last century, bringing previously unimaginable mobility to billions across the globe and providing a critical block in the foundations of modern economies. Yet as Warren Buffett – arguably the world’s most successful investor – has mused, making money out of automakers has proven incredibly tough.

He explains that while at least 2000 companies entered the US auto business in the early part of the 20th century, “because it clearly had this incredible future”, by 2009 just three of these same

‘A KEY LESSON IS THAT THE SEEMINGLY OBVIOUS ROUTE TO INVESTMENTS IN TECHNOLOGY OFTEN PROVES A COSTLY ROAD TO NOWHERE’

businesses were left – and of those three, two then went bankrupt.[2] So, investing directly in car manufacturers would not have been a successful strategy. However, many companies that were either directly or indirectly involved in the auto industry have profited enormously from its growth and continue to do so. So, investors who targeted those businesses, rather than the carmakers directly, could have done very well.

MID AND LARGE-CAP INVESTING: A SOURCE OF OPPORTUNITIES

It’s a similar story when it comes to investing in technology

For example, Allianz Technology Trust’s (ATT) view is that the sweet spot for long-term investing growth is often found in mid-cap stocks and large-cap companies, even though it’s the mega-caps that generally capture the headlines.

Just as with the auto industry, there are a myriad of companies and sectors benefiting from the growth of smartphones and other technologies. They include businesses that supply the critical software that enables smartphones and smart home devices, as well as those that supply the components required to make them.

‘IDENTIFYING THE COMPANIES THAT WILL PROFIT MOST FROM THIS CHANGE REQUIRES AN ABILITY TO THINK TANGENTIALLY’

Companies in these ancillary activities often have better earnings potential than those that supply the goods to the end user. That could be because they possess a key technological edge, provide a unique service, or are protected from competitors by high barriers to entry. And again, among these suppliers, it might not be the corporate behemoths that will deliver the best returns. Take the semiconductor equipment space, where producers of specialised equipment tend to be found in that mid- to large-cap investments neighbourhood.

Clearly, we are living through an age of unprecedented technological innovation, which will continue to transform societies. But identifying the companies that will profit most from this change requires an ability to think tangentially and the skills and knowledge developed from decades of investing in the sector something that we believe can be found in a technology investment trust.

THE ALLIANZ TECHNOLOGY INVESTMENT TRUST’S ESTABLISHED STRATEGY

The tried-and-tested investing for growth formula at Allianz Technology Trust plc focuses on investing in medium-sized to large technology companies.

Allianz Technology Trust aims to hold companies we expect to benefit from continued growth in particular sub-sectors of technology – especially businesses that provide money-saving solutions or enable companies to improve their relationships with customers and deliver revenue growth.

Allianz Technology Trust holdings also include companies that we anticipate will create shareholder value through the introduction of a new product or new technology. That strategy has served our investors well over the past 20 years. Investors should bear in mind, however, that past performance is no guarantee of future results.

“ALLIANZ TECHNOLOGY TRUST AIMS TO HOLD COMPANIES WE EXPECT TO BENEFIT FROM CONTINUED GROWTH IN PARTICULAR SUB-SECTORS OF TECHNOLOGY – ESPECIALLY BUSINESSES THAT PROVIDE MONEY-SAVING SOLUTIONS OR ENABLE COMPANIES TO IMPROVE THEIR RELATIONSHIPS WITH CUSTOMERS AND DELIVER REVENUE GROWTH”

Past performance does not predict future returns. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. We assume no obligation to update any forward-looking statement.

WHY THE BIOTECH SECTOR IS BOUNCING BACK TO RUDE HEALTH… BY JO GROVES

Billionaire hedge fund manager David Tepper once remarked: “I am the animal at the head of the pack. I either get eaten or I get the good grass.”

The holy grail of investing is arguably finding the most promising pastures ahead of the crowd, with early-bird investors often reaping the greatest rewards.

The biotech sector might just fit the bill on the promising pastures front, with the Nasdaq Biotechnology Index (NBI) bouncing back from its post-pandemic downturn to deliver a total year-to-date return of 13% (in US dollars). A correction of the heady valuations reached in the pandemic may have been somewhat inevitable (and further exacerbated by rising interest rates) but the Darwinian shake-out has created a higher-quality universe for investors.

Ailsa Craig and Marek Poszepczynski, managers of International Biotechnology Trust (IBT), categorise the cyclicality of the investment environment into five stages, from despair and recovery through to euphoria and correction. They believe the biotech sector is entering the mid-cycle ‘equilibrium’ stage where improved investor sentiment drives up valuations, with the potential for attractive returns.

Investor sentiment may be cyclical but the underlying biotech sector itself is not: the sector has driven transformative change over the last few years from game-changing weight-loss drugs to revolutionary gene and cell therapies ‘treating the untreatable’. It also enjoys strong tailwinds from the increasingly complex needs of ageing populations and increasing prosperity in emerging economies, which should underpin growth in the decades ahead.

WHY THE FUTURE’S BRIGHTER…

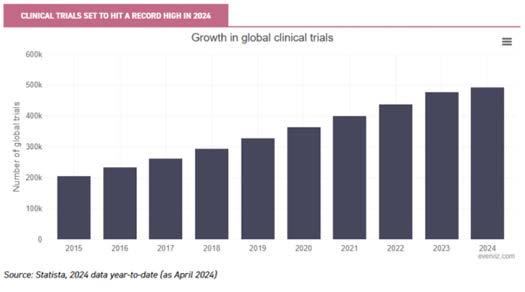

1. Clinical trials hit record high Clinical trials are the lifeblood of the biotech sector, validating the safety and efficacy of new treatments, but their significance extends well beyond regulatory compliance. Positive trial results can drive future revenue potential, enhance investor confidence and shape future innovation by validating new technologies.

The chart below shows the continued growth in global clinical trials, which is forecast to hit a record high this year (with Q1 trials already exceeding the annual total in 2023).

Innovation continues apace, with new methods of treatment (such as cell-based, gene and RNA therapies and gene engineering) helping to address previously unmet medical needs and rapid advances in treatments for diabetes and obesity. This acceleration in innovation should support revenue cycles over the next decade, with a record 70-plus novel medicines approved in the US and Europe in 2023.

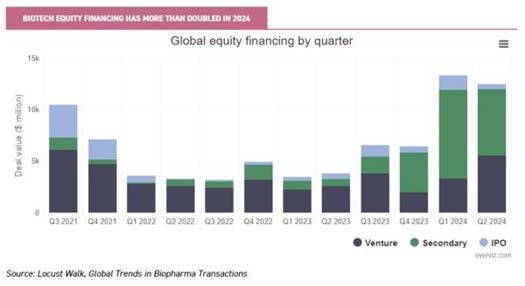

2. Upturn in equity financing The appetite for biotech equity financing is a key indicator of the health of the biotech sector and an important source of funding for earlier-stage companies. There has been a sustained uptick in equity financing in the last six months, as shown in the chart below, and this should continue to benefit from an improving macroeconomic backdrop as interest rates start to fall.

Venture financing in the biotech sector has rebounded from its downturn in 2022 and 2023 to hit its highest level in three years in the last quarter, including renewed interest in earlier-stage companies. It was a similar story for secondary offerings, with the combined deal value in the first two quarters of 2024 comfortably eclipsing the aggregative total for the previous ten quarters combined.

The IPO pipeline also serves as a litmus test of the biotech sector’s health, providing access to public markets and an exit strategy for venture capital investors. Early signs of a modest rebound are emerging, with 15 companies going public in the first eight months of 2024 and more waiting in the wings. As companies remain private for longer, those going public tend to be higher quality and less speculative than during the IPO bubble of the pandemic.

3. Attractive valuations Despite the biotech sector’s recent rally, valuations remain subdued: the S&P 500 biotech sector is currently trading on a forward price-earnings ratio of 19 (according to Yardeni), almost 25% below its pandemic peak, which could provide an attractive entry point for investors.

Ailsa and Marek, managers of IBT, added in a recent note:

“The small-to-mid-sized biotech sector currently trades on an enterprise value/cash ratio of approximately 2, which means that the value of all the companies in this size bracket is around twice the value of the cash they have in the bank.

“In the context of history, this looks attractive. Historically, the sector has traded on an EV/cash ratio of 3.0 to 3.5x for most of the last 20 years. Importantly, cash levels are robust with the average small-to-mid-sized biotech company currently having a healthy cash runway (the time until they would run out of cash at their current rate of spending) of 2.2 years, suggesting the sector is well-financed.”

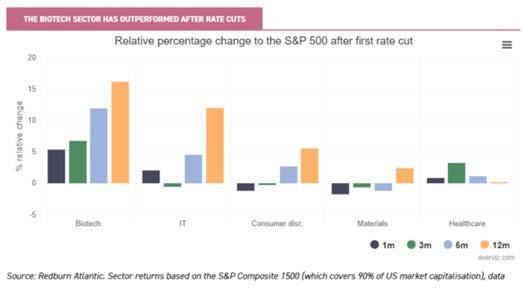

4. Outperformance when rates fall Due to the time taken to develop new drugs, the biotech sector is sensitive to

interest rates (and the associated cost of capital) and, as a result, has typically outperformed other indices when interest rates start to fall.

The chart below shows the relative sector performance against the S&P 500 in the 12 months following the first cut in interest rates. Of the sectors achieving positive returns at the year mark, the biotech sector has delivered by far the highest returns and outperformed the S&P 500 index by an average of 16% in the first year. It has also rewarded early-bird investors with a 5% and 12% outperformance in the first month and six months respectively.

With interest rates having fallen in the UK, and the Fed expected to follow suit in the next couple of months, this shows the potential upside for investors.

PANNING FOR GOLD

However, the biotech sector presents some challenges for retail investors. While it may be difficult for active managers to beat the S&P 500 index due to the dominance of the magnificent seven, a active approach to stockpicking in the biotech sector may make a significant difference to returns. As part of this, specialist scientific knowledge is required to understand highly complex medical technologies and clinical trial data, together with the relevant regulatory frameworks that are fundamental to success.

Ailsa Craig and Marek Poszepczynski, managers of IBT, blend this scientific and industry knowledge with a combined experience of 25 years working on the fund. The managers use various tools to manage risk for investors: they avoid companies that are lower-quality, over-valued or developing ‘me-too’ drugs in favour of well-priced, well-managed and well-financed companies targeting unmet medical needs with drugs that are near to (or have) approval.

Ailsa and Marek adopt a portfolio approach by backing a number of companies targeting the same clinical need rather than trying to pick a likely ‘winner’ and also reduce exposure ahead of binary events such as clinical trial results.

In addition, the level of risk is tailored to the stage in the market cycle, with the managers recently increasing the trust’s small and mid-cap weighting due to the more positive environment. While this potentially increases the volatility of the portfolio, it has the potential to deliver higher returns.

This focus on risk management has underpinned IBT’s returns, with the trust achieving a five-year net asset

Disclaimer: Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by International Biotechnology. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

INTRODUCTORY VIDEO: INTERNATIONAL BIOTECHNOLOGY TRUST PLC (IBT)

value return of almost 50% despite the challenging market conditions. IBT also offers an income for investors and is currently trading on a dividend yield of over 4%.

Looking ahead, falling interest rates and improving investor sentiment should continue to provide a tailwind for the biotech sector. Given the secular growth drivers of an older, richer and sicker population, the biotech sector may well appeal to investors looking for the greenest grass ahead of the pack.

All data as at 18/09/2024 unless stated otherwise.

The Brunner Investment Trust PLC

Established in 1927, The Brunner Investment Trust seeks income as well as capital growth from companies around the world. Because we’re not tied to any one country or sector, we’re free to seek potential opportunities wherever they may be: from European energy to Japanese pharmaceuticals, Swiss healthcare to French luxury goods, U.S. cloud computing to Taiwanese components. As an investment trust, Brunner enjoys other advantages too, such as being able to draw on revenue reserves to support dividend payments in tough times. Although past performance is no guide to the future, we’ve paid a rising dividend to our shareholders for 50 consecutive years, earning the Association of Investment Companies’ coveted Dividend Hero status. So visit us online to learn more or to register for regular updates and insights, and find out how Brunner could help you achieve your investment goals.

www.brunner.co.uk

INVESTING INVOLVES RISK. THE VALUE OF AN INVESTMENT AND THE INCOME FROM IT MAY FALL AS WELL AS RISE AND INVESTORS MAY NOT GET BACK THE FULL AMOUNT INVESTED.

A ranking, a rating or an award provides no indicator of future performance and is not constant over time. You should contact your financial adviser before making any investment decision. This is a marketing communication issued by Allianz Global Investors GmbH, an investment company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, D-60323 Frankfurt/M, registered with the local court Frankfurt/M under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de). The summary of Investor Rights is available at https://regulatory.allianzgi.com/en/investors-rights. Allianz Global Investors GmbH has established a branch in the United Kingdom deemed authorised and regulated by the Financial Conduct Authority. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website (www.fca.org.uk).

WHY WE ARE BETTING ON THE BANKS

SALTYDOG INVESTOR REVEALS A NEW POSITION IN THE FINANCIAL SECTOR, WHICH IS BENEFITTING FROM POLITICS IN THE US

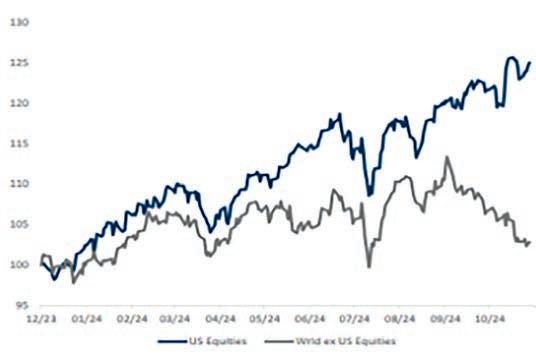

US stock markets have been on a roll since Donald Trump’s presidential election victory.

Last week, S&P 500 and Nasdaq closed at record highs, whilst the Dow was not far off, having peaked earlier in the week. Since the beginning of November, the S&P has risen by 6.7%, Dow Jones Industrial Average is up 6.9%, and the Nasdaq outperformed both with a 9.8% gain.

As a result, our Saltydog demonstration portfolios have invested in sectors we avoided in the run-up to the election. I have written about the North American sectors and Baillie Gifford American Fund, which we bought on 14th November and is already showing a gain of 5.1%.

In the Technology & Technology Innovation sector: we invested in BGF World Technology Fund which has risen by 4.5% since 28th Nov.

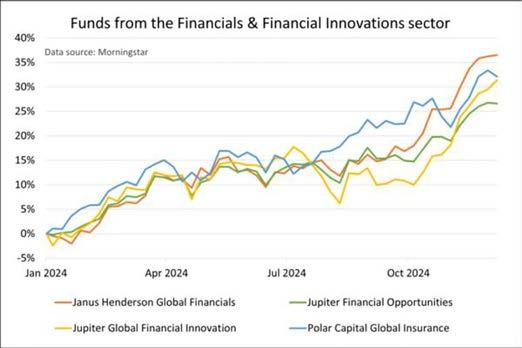

Last week, both Saltydog portfolios invested in Janus Henderson Global Financials Fund. This is a relatively new sector, introduced in 2021; it is also fairly small, so we only track a handful of funds. This chart shows how the top four funds in this sector have performed this year. It updates the graph I produced in October highlighting that Financials & Financial Innovation was the leading sector of 2024 (and still is).

These funds can invest anywhere in the world, but have a strong US focus. E.g. over 60% of the Janus Henderson Global Financials Fund portfolio is invested in US companies - predominantly banks, insurance companies, and businesses providing financial services. Unsurprisingly, Polar Capital Global Insurance fund is almost entirely invested in insurance companies, but the other three funds favour banks, followed by financial services, then insurance.

US bank shares rose sharply at the beginning of November, and I can think of several possible reasons why.

Investors anticipate a Trump administration will benefit the US economy; this is expected to increase commercial lending, which will benefit banks – especially now interest rates have risen from the record lows observed for most of the past 15 years. Whilst rates have declined from the highs of the second half of last year, they remain at levels profitable for bank lending. Next year, the Federal Reserve may gradually lower its benchmark rate from its current range of 4.5% – 4.75%, but no one expects a return to the historically low levels seen after the pandemic anytime soon.

Trump’s pro-business approach involves removing constraints on companies caused by excessive regulation and bureaucracy. This could be particularly beneficial for banks, which have been under scrutiny since the 2008 financial crisis.; for example, he might reduce the amount of capital banks are required to set aside to mitigate risk.

Additionally, the number of mergers and acquisitions is expected to increase, partly due to looser regulatory scrutiny. This would be especially good news for large US investment banks such as The Goldman Sachs Group Inc GS 1.04%, JPMorgan Chase & Co JPM 0.66%, and Morgan Stanley MS 0.40%.

This is all well and good, but it is worth remembering that Donald Trump has not yet been sworn in, and it will take time to see the true effects of his policies. It feels like a case of ‘buy the story,’ but we must also be prepared to ‘sell the news’ if the reality falls short of expectations.

For more information about Saltydog, or to take the 2-month free trial, go to www.saltydoginvestor.com

LEADING THE DIY

Denied access to advice by RDR, or unwilling to pay for something that was previously free, millions of people now take full or partial control of their finances.

Whether seeking to get on the property ladder, planning for tuition fees or taking advantage of new pension freedoms, more than ever are setting their objectives, and building a portfolio of investments that allows them to achieve their goals whilst comfortable with the level of risk their money is exposed to.

Education is the key and technology the enabler - DIY Investor delivers information to existing investors and education to those new to savings and investment; share experience and learn to make informed investment decisions.

NOBODY CARES MORE ABOUT YOUR MONEY THAN YOU

MAJORITY OF BRITISH INVESTORS PREDICT BULL MARKET WILL CONTINUE THROUGHOUT 2025 AMIDST OPTIMISM FOR UK STOCKS

• 53% of UK retail investors expect bull market to run through 2025, with 60% also backing AI stocks to keep rising.

• Majority of British investors now hold domestic stocks, the highest proportion in over a year.

• 3 in 4 British investors rebalancing their portfolios after the US election plan to increase their allocation to crypto.

UK retail investors are optimistic that the current bull market will continue throughout next year, according to the latest quarterly Retail Investor Beat from trading and investing platform eToro.

The study, which surveyed 1,000 retail investors in the UK, found that 53% expect the bull market to persist. Confidence in AI stocks also remains high, with 60% of British investors predicting they will continue to rise in 2025.

UK EQUITIES RETURN TO FAVOUR

Although 2024’s bull market has been mainly driven by the soaring S&P 500, the survey indicates that whilst a new UK government bounce has not meaningfully materialised, UK investors remain hopeful for a home market rally.

While the US was comfortably the most popular choice (41%) when retail investors were asked which market they expected to generate the strongest returns in 2025, the UK (24%) came in second place. This optimism coincides with the fact that the majority (52%) of British retail investors now hold domestic equities, the highest level in over a year, up from 45% 12 months prior.

Despite the perception of UK equities as primarily appealing to older, dividend-seeking investors, ownership is fairly evenly distributed across generations, with Millennials the least likely to hold UK stocks (48%), and Gen X the most (56%). Fixed income has also returned to favour, rising for a third consecutive quarter. UK bonds now feature in 41% of portfolios, up from 35% in Q2, as investors look to lock in higher yields ahead of anticipated rate cuts in 2025.

Analysing the data, Dan Moczulski, UK Managing Director at eToro said: “Despite the FTSE trailing other major indices, British investors continue to keep faith with discounted domestic shares.

One factor may be softening domestic economic sentiment, with the proportion of UK investors citing high inflation or high interest rates as the biggest external risk to their investments at their lowest levels for over a year. Conversely, the leading concerns of global recession and international conflict may be behind a retreat into the relative stability of UK stocks and bonds.

US ELECTION SPARKS REBALANCING AND DEMAND FOR CASH AND CRYPTO

Donald Trump’s promise of radical reform has prompted almost half (47%) of UK retail investors to reposition their portfolios. This is most pronounced amongst younger investors, with 85% of Gen Z and 68% of Millennials rebalancing post-election, highlighting their increasingly active approach to investing.

Amongst those rebalancing, three quarters (75%) of Brits plan to upweight their exposure to cryptoassets – above the global average of 68%. 57% also plan to increase the amount of assets held in cash, above the global average of 45%, mirroring defensive moves made by Warren Buffet amidst concerns of high market concentration and unsustainable valuations.

Despite cryptoasset ownership currently skewing heavily towards young investors, those who report plans to invest in cryptoassets following the election are relatively evenly spread across age groups, with a relatively small difference between the least interested generation, Gen X (65%) and the most interested generation, Millennials (78%).

Consistently high levels of interest in crypto across generations is notable considering current levels of crypto ownership currently differ greatly between demographics. Despite featuring in the majority of Gen Z (60%) and Millennials’ (52%) portfolios, this proportion falls to 23% for Gen X, and just 5% for Baby Boomers.

Moczulski added: “The sharp rise in those looking to increase their crypto allocations reflects growing confidence in the asset class, bolstered by President Trump’s pro-crypto stance. The fact that demand for crypto is balanced across older and younger investors indicates a cultural shift in how these assets are perceived, on the back of a year that saw the approval of bitcoin ETFs, positive regulatory steps, and all time highs across major cryptoassets.”

TECH REMAINS TOP TARGET FOR RETAIL INVESTORS

When asked which sector they were most likely to increase their allocation to in 2025, tech stocks were by far the most popular answer at 17%, ahead of second-placed financial services (10%).

Despite concerns over high valuations, this optimism was reflected by almost half (47%) of investors expecting the Magnificent 7 to continue outperforming the broader stock market, versus just 6% who think they will suffer a correction and underperform.

Of the seven, British investors are divided over who the main beneficiaries could be in 2025. When asked which of the Magnificent 7 they were most likely to increase their investment in, Amazon came out on top at 13%, narrowly ahead of Tesla (11%), and Apple (10%).

ABOUT THIS REPORT

The latest Retail Investor Beat was based on a survey of 10,000 retail investors across 12 countries and 3 continents. The following countries had 1,000 respondents: UK, US, Germany, France, Australia, Italy and Spain. The following countries had 600 respondents: Netherlands, Denmark, Poland, Romania, and the Czech Republic.

The survey was conducted from 18 November –28 November 2024 and carried out by research company Opinium. Retail investors were defined as self-directed or advised and had to hold at least one investment product including shares, bonds, funds, investment ISAs or equivalent. They did not need to be eToro users.

SAVER > INVESTOR: EMPOWERING INVESTORS WITH SELF-SERVICE TOOLS – GUEST POST BY MIA MILLER

INVESTING CAN FEEL LIKE A MAZE. YOU’RE CONSTANTLY MAKING DECISIONS, MONITORING MARKETS, AND TRYING TO STAY AHEAD OF TRENDS. SELF-SERVICE TOOLS GIVE YOU MORE CONTROL AND FLEXIBILITY BY SIMPLIFYING PROCESSES AND MAKING INVESTING MORE ACCESSIBLE. LET’S EXPLORE HOW THESE TOOLS EMPOWER YOU AS AN INVESTOR AND WHY THEY ARE ESSENTIAL IN FINANCIAL INDUSTRIES TODAY

WHAT ARE SELF-SERVICE TOOLS FOR INVESTORS?

Self-service tools are digital platforms or apps that give you direct access to your investment accounts. They let you make trades, research options, and analyze market trends—all without a middleman.

For example, tools like portfolio trackers or trading platforms help you stay updated on your investments. You can use them to:

• Check your stock performance

• Compare funds

• Even set alerts for price changes

These tools also offer features like equity trackers that can help you monitor market movements and assess your financial goals more effectively.

HOW SELF-SERVICE TOOLS ENHANCE YOUR INVESTMENT EXPERIENCE

Let’s look at some specific ways self-service tools make your investing journey easier and more rewarding:

1. SIMPLIFIED PORTFOLIO MANAGEMENT

Managing investments doesn’t have to be a chore. Self-service platforms let you see all your assets in one place.

You can review your portfolio’s performance, make adjustments, and even explore new opportunities.

Tools like equity trackers can help you monitor individual markets, assets, funds, and more, ensuring your portfolio aligns with your financial goals.

2. PERSONALIZED INSIGHTS

Gone are the days of one-size-fits-all advice. With self-service tools, you get insights tailored to your preferences. Are you a conservative investor? Or would you like to be more aggressive?

These tools gather your data and customize their approach based on your style. Some even offer simulations, so you can test strategies before committing your money.

3. COST SAVINGS

Traditional investment methods often come with high fees for advisors or brokers. Self-service tools save you money by cutting out the middleman. Most platforms charge lower fees or none at all. So, you get to retain more of your earnings!

4. EDUCATION AT YOUR FINGERTIPS

Knowledge is power, especially in investing. Many self-service platforms offer tutorials, articles, and videos to help you learn about financial markets. Whether you’re new to investing or looking to sharpen your skills, these resources can boost your confidence.

5. RISK MANAGEMENT FEATURES

Investment always comes with risks. Self-service tools help you manage them better. Many platforms allow you to set stop-loss orders or alerts, minimizing potential losses. Additionally, fraud protection features help minimize investment fraud, giving you an extra layer of security.

HOW TO GET STARTED WITH SELF-SERVICE TOOLS FOR INVESTING

Taking the plunge into self-service investing might seem overwhelming, but it doesn’t have to be. Here’s an easy blueprint to help you start:

DEFINE YOUR GOALS

Ask yourself what you want to achieve. Are you preparing for your golden years, a property, or simply trying to improve your financial position? Clear goals will help you make judgments.

CHOOSE THE RIGHT PLATFORM

The right platform can make all the difference in investing. There’s a wide range of self-service tools available, each tailored to different needs and levels of expertise.

If you’re a beginner, platforms with user-friendly interfaces and educational resources are a great place to start. These often include guided tutorials, risk assessment tools, and basic portfolio management features.

Alternatively, if your focus is on specific types of investments—like stocks, bonds, or cryptocurrencies— specialized platforms cater to these markets. Some platforms even prioritize ethical investing, allowing you to select portfolios that align with your values, such as sustainability or social responsibility.

START SMALL

You don’t have to dive in headfirst. Starting with a modest investment and getting accustomed to your tools is much more important. You can expand your portfolio as you gain more confidence.

STAY INFORMED

Continue to learn about market developments, dangers, and possibilities. The more knowledgeable you are, the better your financial choices will be.

TIPS FOR LEVERAGING SELF-SERVICE TOOLS FOR INVESTORS

While self-service tools offer plenty of advantages, they’re not without challenges.

Here’s how to address some frequent issues:

INFORMATION OVERLOAD

It’s easy to feel overwhelmed with so much data available. Concentrate on key variables like stock performance, risk level, and diversification. You’ll eventually learn to filter out unneeded noise.

TECHNICAL GLITCHES

Like any tech, self-service tools can experience bugs or downtime. Always have a backup plan, such as keeping important contact numbers or alternative platforms handy.

LACK OF PERSONAL GUIDANCE

Without a financial advisor, you might feel unsure about big decisions. Take advantage of the educational resources many platforms provide. And remember, starting small reduces the risk of costly mistakes.

EMPOWER YOURSELF WITH THE RIGHT TOOLS

Self-service tools are here to empower you, giving you control, convenience, and confidence in your decisions. If you’re ready to take charge of your financial future, now is the time to explore. Look for features that streamline your processes and minimize your risks. With the right tools and mindset, you’re well on your way to achieving your financial goals.

MILLENNIAL DIY INVESTORS’ ARE LOOKING TO TAKE ON MORE INVESTMENT RISK FOLLOWING THE CHANCELLOR’S BUDGET IN OCTOBER ACCORDING TO NEW RESEARCH FROM CHARLES STANLEY DIRECT

• 47% of millennial DIY investors are looking to take a high level of investment risk in the next 3 months.

• This is an increase on the 39% who said the same just five months ago.

• Gen Z investors remain the most adventurous generation in their investment approach.

• 33% of DIY investors have increased their exposure to the Alternative Investment Market, up from 28% who said the same in July 2024.