As the vibrant energy of spring unfolds across the continent, so too does the dynamic evolution of digital banking. In this edition, we turn our focus to “The Empowered Consumer: Shaping the Future of Digital Banking in Africa.”

The landscape of financial services is being fundamentally reshaped by increasingly digitally savvy and demanding consumers. Their evolving needs and expectations are no longer just influencing change –they are actively driving it. This edition delves deep into understanding this empowered African consumer, exploring how their preferences are dictating the future trajectory of digital financial services.

We examine the profound and continuing impact of mobile banking, a cornerstone of financial inclusion that continues to adapt and innovate. We also explore the crucial role of financial literacy in this digital age, empowering individuals to navigate the complexities and opportunities of modern finance with confidence.

Recognising that with empowerment comes responsibility, we address the critical concerns surrounding data privacy and security in this

increasingly digital realm. Building and maintaining trust in digital finance is paramount, and our expert contributors offer insights into fostering secure and reliable financial ecosystems.

Beyond the empowered consumer, this edition will also continue our vital exploration into the impact of mobile money. We analyse its ongoing evolution and its crucial role in furthering financial inclusion across the African continent, reaching even the most underserved communities.

Inside, you’ll find a collection of thought-provoking articles from leading voices across the industry, offering their expert analysis and perspectives on these pivotal themes. We trust that their insights will provide you with a comprehensive understanding of the forces shaping the future of digital banking in Africa and equip you to navigate this exciting era with clarity and strategic foresight.

We hope you find this edition both insightful and engaging.

The Digital Banker Africa Team.

The Digital Era, Your Bank is a Thumb Away Enabled by Access How Mobile Money and AI are Reshaping Financial Inclusion in Africa

The Impact of Mobile Money & Digital Finance Literacy The Influential Consumer Redefining the Future of Digital Banking in Africa

Unlocking Africa’s Digital Future

Beyond the Like Button Social Media and Africa’s Financial Future

The Ethical Equation Educating Customers & Building Trust in African Digital Banking.

The Digital Leapfrog How Africa’s Innovation in Finance is Rendering the ATM Era Obsolete The Transformative Power of RealTime Payments and why banks should embrace them

Customer service is further enhanced through the use of chatbots and self-service tools, enabling users to resolve issues, inquire about transactions, and access banking services without human intervention. Digital banks like TymeBank – a fully digital South African bank has embraced AI-powered solutions to provide round-the-clock assistance, low-cost transactional accounts and high-yield savings accounts mainly for low-income rural customers.

Finally, partnerships between fintech companies; who have typically shown themselves to be more agile in churning out customer-centric innovation solutions, and traditional banks; who have typically been more meticulous and deliberate, has often yielded the right balance of optimal user experience anchored on a strong compliance regime. This careful balance ensures that customers are both delighted and protected, and the right balance between financial inclusion and financial stability is calibrated.

As digital banking continues to expand, the balance between convenience and security remains a concern. While consumers enjoy seamless access to financial services, they also face growing risks related to cybersecurity, fraud, and data privacy. To address these challenges, central banks across Africa are implementing policies that promote open and digital banking while ensuring robust consumer protection measures. Ghana, for example,

Dr Maxwell Opoku-Afari Former First Deputy Governor Bank of Ghana

has emerged as a global leader in mobile money regulation, recently claiming the top spot in the GSMA Mobile Money Regulatory Index for its strong policies that foster innovation while safeguarding consumers. The country’s supervision framework includes a guideline on consumer recourse mechanism, a directive to mobile money providers on unclaimed balances and dormant accounts, a data protection law among others. In 2023, the Central Bank of Nigeria issued operational guidelines on Open Banking while Bank of Ghana also published a Draft Open Banking Directive in 2024 for Regulated Institutions to facilitate the sharing of customerconsented financial data amongst Regulated Financial Institutions (RFIs) .

In addition to regulation, financial literacy initiatives play a crucial role in consumer protection, equipping users with the knowledge to make informed decisions, recognise fraud, and fully understand their rights.

Remarkably, these principles hold true even for future digital banking instruments as Central Bank Digital Currencies (CBDCs). Studies such as Bank of Ghana’s eCedi pilot continue to reveal that one of the most important features of a CBDC for consumers, besides transaction fees and safety standards, was that it was backed by the central bank , reinforcing trust in its stability, reliability, and legitimacy as a secure digital currency.

Empowering consumers in Africa’s digital banking landscape requires more than just technological advancement. There must be a prioritisation of interoperability, collaboration and continuous innovation.

One critical factor is crossfunctional cooperation and interoperability across markets. Consumers should have full control over their financial choices, supported by clear and standardised disclosures, proper consent mechanisms, and seamless access to financial services across different platforms and regions. There must be a concerted effort to standardise digital banking regulations and frameworks across Africa, enabling a more integrated financial ecosystem where consumers can transact effortlessly, regardless of borders.

Emerging innovations, such as CBDCs, AI-driven financial services, and cross-border banking solutions, hold immense potential in shaping the future of consumer empowerment. CBDCs could provide greater financial stability, reduce cross-border transaction costs, and improve monetary policy transmission, while AI-powered banking solutions continue to enhance personalisation, automate customer support and expand credit access.

Continuous education is another critical factor. Regulators, financial institutions, and FinTechs must work together to ensure that consumers fully understand their rights, financial options, and available protections. Trust remains a cornerstone of financial engagement, and efforts must be made to safeguard data privacy, prevent fraud, and uphold ethical banking practices.

Finally, a dynamic and vibrant fintech ecosystem must be encouraged through policy enablers such as regulatory sandboxes, innovation funds and risk-based licensing regimes, as well as private sector investment to achieve scale.

Ultimately, the success of digital banking in Africa hinges on how well the empowered consumer is understood and served.

The modern African banking customer is informed, connected, and expects financial services that are accessible, transparent, and tailored to their needs. By embracing collaboration, education, innovation, and trustbuilding, the digital banking ecosystem can evolve in a way that truly puts the consumer in control, driving financial inclusion and economic growth across the continent.

• World Economic Forum (https://www. weforum.org/stories/2023/11/africadigital-mobile-banking-financialinclusion/)

Demirgüç-Kunt, A. et al. (2022) The Global Findex Database, Financial Inclusion, Digital Payments, and Resilience in the Age of COVD-19. World Bank Publications.

• GSMA (2024) ‘The State of the Industry Report on Mobile Money,’ GSMA, p. 12. https://www.gsma.com/sotir/wp-content/ uploads/2024/03/GSMA-SOTIR-2024_ Report.pdf.

• OPay: https://www.opayweb.com/about-us

• Jeník, I. (2024) TymeBank Case Study: The Customer Impact of Inclusive Digital Banking. https://www.cgap.org/research/ publication/tymebank-case-studycustomer-impact-of-inclusive-digitalbanking.

(2025) ‘Best in the world: Ghana claims top spot in new GSMA mobile money regulatory ranking - Ghana Chamber of Telecommunications,’ Ghana Chamber of Telecommunications -, 20 January. https://www.telecomschamber.org/ industry-news/best-in-the-world-ghanaclaims-top-spot-in-new-gsma-mobilemoney-regulatory-ranking/.

• Bank of Ghana (2024a) DRAFT OPEN BANKING DIRECTIVE FOR REGULATED FINANCIAL INSTITUTIONS. https://www. bog.gov.gh/wp-content/uploads/2024/12/ Draft-Open-Banking-Directive-forRegulated-Financial-Institutions-201224. pdf.

Bank of Ghana (2024) The eCedi Report. https://www.bog.gov.gh/wpcontent/uploads/2024/10/The-eCediReport-221024.pdf

EXPLORING THE POWER OF DIGITAL

FINANCIAL LITERACY FOR NATIONAL GROWTH

Dr Charity Chikumbi

Technical Consultant

Examining digital financial inclusion in Zambia from the streets of Lusaka can be “a walk in the Park”! In the heart of the capital, there are many financial institutions in the form of banks, micro-finance companies and several mobile money agents. The digital financial services (DFS) have brought vivid inclusivity to most social levels of society.

However, just some fifty minutes drive eastwards brings you to a small town called Chongwe. There, in the heart of a small town, you find only one or two banks, but still many mobile money agents scattered all around the town and its suburbs. In the dusty lanes of Chongwe, a young woman named Chanza, runs a chain of mobile money agent booths, dotted around the town. Through these agents, many women and youths are able to access, use, and explore digital financial services with only a basic phone as the needed device. To Chanza, this business is her lifeline, but to the financial sector, the business is part of a digital revolution progressively unfolding across Zambia. Such businesses thrive on mobile phones and financial apps that form not just tools of convenience but vehicles for empowerment and economic transformation. As Zambia pursues its ambitious development goals, one of the keys to inclusive progress may lie in an often overlooked skill: digital financial literacy.

A nation on the move, powered by mobile phones

Financial technology in the era of digital disruption has transformed traditional mechanisms of financial services into more efficient endeavours. Digital financial literacy has become an important digital competency that enhances financial inclusiveness with technology (Formosa Journal of Multidisciplinary Research,2023).

Further, the National Digital Transformation Strategy records that Zambia’s private sector, particularly the financial sector, has made significant strides in driving digital access to services such as payments, credit, insurance and investment (National Digital Transformation Strategy, 2023).

According to the Bank of Zambia website, mobile transactions continued to grow in 2023. The value and volume of transactions processed increased by 41.8 % and 52.8% to K452.0 billion (2022: K295.8 billion) and 2,242,443,898 transactions (2022: 1,581,355,224 transactions) respectively.

On the other hand, the growth in the number of mobile phones also keeps soaring. The total number of registered mobile phone subscribers in 2023 reported by the three mobile money operators increased by 2.3% to 19,477,324 (2022: 19,048,234) while the total number of mobile money subscribers increased by 8.6% to 17,290,646 (2022: 15,917,092).

The number of active mobile money subscribers increased by 14.9% to 12,924,894 (2022:

11,246,686). Active wallets which are wallets that had customerinitiated transactions in the last 90 days constituted 74.8% (2022: 70.7%) of the total number of registered mobile money wallets, representing an upward trend.

With such high statistics, it is imperative to ensure that careful investment is made into digital financial literacy to build consumer trust. While access is growing, usage remains uneven (Youngjoo Choung a, Swarn Chatterjee b, Tae-Young Pak c ScienceDirect, 2022).

Recognising that most excluded people are found in rural areas (Finscope,2020), it is understood that they still lack the knowledge to distinguish secure platforms from scams or to leverage digital tools for savings, budgeting, or small business growth. Along with the rural population are MSMEs that may be too busy to take the necessary precautions, financial literacy and digital savvy. Without digital financial literacy, access can result in exposure to fraud, mismanagement, and missed opportunities, (The Payers.com)

Bridging this skills gap is essential.

Digital financial literacy is the ability to use digital tools and platforms—like mobile money, online banking, budgeting apps, and fintech services—confidently and safely for personal and business finance, (Golden & Cordie, 2022). It’s an extension of traditional financial literacy, adapted to today’s digital-first economy. In Zambia, where mobile phone penetration is above 90%,

with a voice-based system for learning (FSD Zambia, 2021).

A user can call a short code (USSD number) to listen to financial lessons or tips. These could range from understanding mobile money to budgeting basics.

Example: “Dial *443# to listen to daily financial tips.”

Users can also interact with the system, answering basic questions (e.g., “What percentage of your income should you save?”) to test their knowledge.

Unstructured Supplementary Service

Data (USSD): This is another method that works well on feature phones. USSD allows users to access services without needing internet access. Banks, mobile money providers, or other institutions can set up USSD-based education modules that feature short lessons or quizzes on personal finance, such as Mr Isaac Malemelo on LinkedIn.

Interactive Quizzes: Users can take a simple quiz via USSD after completing a lesson. Correct answers could be rewarded with small incentives like airtime or discounts on financial services.

Radio Broadcasts: Radio is one of the most popular media platforms in Zambia, especially in rural areas. Financial literacy content has been broadcasted in local languages, focusing on simple, relatable financial advice. Programs covered topics like how to budget, how to use mobile money, and how to access micro-(Bank Yako Yako Radio Drama Launch | FSD Zambia | Diamond TV Bizweek - YouTube.

Leveraging Mobile Money Networks: Since mobile money platforms like MTN Mobile Money, Airtel Money, and Zamtel are widely used in Zambia, they can play a significant role in delivering financial literacy. Financial institutions or fintech organisations can partner with mobile money providers to send educational SMS directly to users about how to save, send money securely, or use the platform to pay for services and goods.

Micro-Learning via Mobile Money: Short tips, reminders, or “how-to” guides can be integrated into mobile money services. For example, when a person makes a payment or sends money, they could receive an SMS with a brief educational message, such as “Remember to save a small portion of your earnings for the future!”

With the rise of online financial transactions, cybersecurity has become a cornerstone of financial literacy. Cybercriminals are becoming increasingly sophisticated, targeting individuals through scams, phishing attacks, and data breaches. Understanding how to protect sensitive financial information is no longer optional—it is a necessity.

Financially literate individuals must be aware of best practices, such as using strong, unique passwords for financial accounts, enabling two-factor authentication, and being cautious about sharing personal information online.

• Adel, N. (2024). The Impact of Digital Literacy and Technology Adoption on Financial Inclusion in Africa, Asia, and Latin America. Heliyon, 10(24), e40951–e40951. https://doi.org/10.1016/j. heliyon.2024.e40951

Desy, N., None Khresna Bayu Sangka, & Salman, N. (2024). Digital Financial Literacy and Digital Financial Inclusion in the Era of Digital Disruption: Systematic Literature Review. Formosa Journal of Multidisciplinary Research, 3(5), 1563–1576. https://doi.org/10.55927/fjmr. v3i5.9213

• FSD Zambia. (2021, November 29). Real People Real Stories: Interactive Voice Response campaign changes livelihoods Richard Mesa. YouTube. https://www. youtube.com/watch?v=C4rnCVthY18

• Financial Sector Deepening (FSD Zambia). (2020). Women and Financial Inclusion in Zambia FinScope 2020 Focus Note May 2022 – fsdz. Https://Www.fsdzambia.org/. https://www.fsdzambia.org/2024/09/01/ women-and-financial-inclusion-inzambia-finscope-2020-focus-notemay-2022/

• FSD Zambia. (2022, March 23). Bank Yako Yako Radio Drama Launch | FSD Zambia | Diamond TV Bizweek. YouTube. https:// www.youtube.com/watch?v=4cPp53i5Z9o Golden, W., & Cordie, L. (2022). Digital Financial Literacy. Adult Literacy Education: The International Journal of Literacy, Language, and Numeracy, 4(3), 20–26. https://doi.org/10.35847/wgolden. lcordie.4.3.20

• Government of the Republic of Zambia. (2024). MINISTRY OF FINANCE AND NATIONAL PLANNING- NATIONAL FINANCIAL INCLUSION STRATEGY II. https://www.boz.zm/NFIS_II_2024__2028.pdf

• Koskelainen, T., Kalmi, P., Scornavacca, E., & Vartiainen, T. (2023). Financial literacy in the digital age—A research agenda. Journal of Consumer Affairs, 57(1), 507–528. https://doi.org/10.1111/joca.12510 Mumbi, L. (2023, March 24). FINANCIAL LITERACY AND TECHNOLOGY | BongoHive. BongoHive. https://bongohive.co.zm/ financial-literacy-and-technology/

• The Payment Association of Zambia (PAYZ). (2023). Fintech Driving Financial Inclusion in Zambia | Payments Association of Zambia | PAYZ. Payz.co.zm. https://payz.co.zm/fintech-drivingfinancial-inclusion-in-zambia/ United Nations Capital Development Fund. (2021). Digital financial literacy. Rural Finance and Investment Learning Centre. (2021). Digital Financial Services Report. https://www.rfilc.org/wp-content/ uploads/2021/05/Digital-FinancialLiteracy.pdf

• Youngjoo Choung a, Swarn Chatterjee b, Tae-Young Pak ( 2023, dec).Digital financial literacy and financial well-being. Digital financial literacy and financial well-being - ScienceDirect

The global climate crisis is one of the most pressing issues of our time. Rising temperatures, more frequent and severe natural disasters, and dwindling natural resources are all symptoms of this crisis, primarily driven by human activities such as burning fossil fuels, deforestation, and industrial processes. As the average global temperature rapidly approaches 1.5°C above pre-industrial levels, the urgency for ambitious mitigation efforts has never been greater. Current estimates suggest that without significant action, the world is on course for a temperature rise of between 2.6°C and 3.1°C during this century. In response to the climate crisis, several jurisdictions, businesses and individuals globally have started implementing innovative strategies to mitigate environmental risks and foster a more equitable and resilient future. And it is against this background and in the midst of this crisis, that green financial technology (green fintech) has moved to the foreground. Green fintech has emerged at the intersection of technology and environmental responsibility, leveraging financial technology to redirect capital towards renewable energy projects, conservation initiatives, sustainable businesses and clean tech. With this in mind, let us delve into the world of green fintech and its promising prospects.

Green fintech refers to the integration of fintech solutions and environmental sustainability goals. This emerging field leverages financial technologies to manage environmental challenges and promote sustainable practices in the financial sector. These practices include the development of digital tools and platforms aimed at facilitating green investments or reducing carbon foot; encouraging transparency in environmental reporting; and supporting environmentally friendly financial products and services.

Enabled by factors such as technological advancements, data availability, consumer demand and policy and regulatory support, green fintech has the potential to play a transformative role in combating climate change.

Green fintech is experiencing significant growth globally. Financial institutions are increasingly offering green loans and bonds aimed at supporting eco-friendly projects. They provide favourable terms to encourage businesses and individuals to invest in renewable energy, energyefficient technologies and similar sustainable practices.

The global green fintech market is projected to grow at a compound annual growth rate (CAGR) of 22.4% between 2024 and 2029, reflecting the rising demand for sustainable financial solutions. There is a surge in platforms facilitating investments in green projects.

Additionally, the rise of digital payment methods, such as contactless payments and mobile banking, contributes to sustainability by reducing the reliance on cash and paper-based transactions. This trend not only enhances convenience, but also supports environmental goals by minimising resource consumption associated with traditional payment methods.

Many jurisdictions and regulatory bodies across the globe are considering and implementing policies that promote sustainable finance. Initiatives such as the Paris Climate Agreement, latest

Keith Sabilika Senior Fintech Specialist Financial Sector Conduct Authority

publication on sustainable finance by South Africa’s Financial Sector Conduct Authority (FSCA) titled FSCA Sustainable Finance Update Report 2025 and the introduction of laws and regulation that prioritise sustainability – such as the European Union Sustainable Finance Disclosure Regulation (SFDR), the Task Force on Climate-related Financial Disclosures (TCFD) and the Principles for Responsible Banking and the Net-Zero Banking Alliance – are encouraging the development of green fintech solutions, and provide a supportive framework for innovation in this space.

Green fintech is enabled by several key technologies which include:

Artificial Intelligence (AI) and Machine Learning (ML) which automate carbon footprint calculations, track environmental impacts, and provide personalised green investment insights.

Blockchain and Distributed Ledger Technology (DLT) ensure transparency in carbon credit trading and green investments, with smart contracts automating green finance processes such as green loans or claims based on environmental data.

Big Data and Analytics enable the evaluation of sustainability performance, environmental, social and governance (ESG) metrics, and climate risks, enhancing investment decisions.

Cloud Computing supports scalable and energy-efficient data processing for green fintech applications, optimising energy use and lowering the carbon footprint compared to traditional information technology (IT) systems.

Internet of Things (IoT) devices collect real-time data on emissions and resource use, enabling dynamic underwriting, usage-based insurance, and efficient asset management.

Geospatial Technology offers detailed environmental insights, supporting risk assessment, sustainable asset management, and location-based environmental impact analysis.

Together, these technologies enable innovative solutions that drive environmental sustainability while allowing green fintech to flourish.

classification

The Green Fintech Classification report, issued by the Green Digital Finance Alliance and the Swiss Green Fintech Network, provides a standardised categorisation of green fintech solutions. The report identifies eight categories: Green digital payment and account solutions: Payment platforms integrating green features (e.g., carbon footprint tracking, automated offsetting).

Green digital investment solutions: Robo-advisory and algorithm-driven platforms offering automated green investment services.

Digital ESG data and analytics solutions: AI-powered ESG rating, automated carbon accounting, and impact reporting tools.

Green digital crowdfunding and syndication platforms: Platforms that raise funds for green projects via crowdfunding or syndication.

Green digital risk analysis & insurtech: AI and IoT-driven climate risk modelling, green insurance, and parametric coverage.

Green digital deposit and lending solutions: Digital lending and mortgage solutions tied to green performance.

Green digital asset solutions: Blockchainbased green asset tokenisation and climate-positive cryptocurrencies.

Green regtech solutions: Technology for regulatory compliance, green disclosures, and taxonomy alignment.

This classification aims to facilitate better industry alignment, improve regulatory oversight and accelerate green fintech adoption globally.

With our scale, expertise and deep desire to satisfy your needs, we will deliver exceptional experiences for the moments that matter the most to you.

The African banking landscape is undergoing a digital revolution, with traditional banks and fintech companies reshaping the financial future. Digital Banker Africa speaks with Ciko Thomas, Group Managing Executive for Retail and Business Banking at Nedbank Group, to understand how Nedbank is adapting and leading in this dynamic environment. We delve into Nedbank’s digital transformation strategy, its collaborative approach with fintechs, and its focus on financial inclusion. Ciko shares insights on leveraging AI, ensuring security, and the bank’s longterm vision for sustainable growth across the continent.

DBA: How do you see the evolving relationship between traditional banks and fintech companies in Africa? Is it primarily competitive, collaborative, or a mix of both, and how is Nedbank navigating this dynamic?

CT: Nedbank that the rise of digital-only banks and fintech players is reshaping the financial sector. Rather than viewing them solely as competitors, Nedbank has adopted a collaborative approach, integrating fintech capabilities into our ecosystem while continuing to build on our digital banking leadership. Nedbank has a long history of collaboration with when it comes to payments, for example. Our award-winning Avo by Nedbank super app, which extends beyond traditional banking into lifestyle services, is a prime example of this strategy. Additionally, Nedbank’s fosters open banking innovation, third-party developers to with our financial services. These initiatives demonstrate Nedbank’s ability to compete with digital-first players while delivering enhanced experiences to our customers. The supporting the Avo super app, includes APIs for accounts, personal loans, wallets, and rewards, enabling value exchange among customer segments and integrating Nedbank’s ecosystem with thirdparty providers for data exchange, purchases, payments, and loans as well as access to markets Nedbank historically couldn’t participate in. By December 2024, 73 third parties were active on the platform.

Group

Ciko Thomas

We also partner with Fintechs to gain access to innovative products, faster product development and access to new markets. On collaborating with Fintechs, traditional banks like Nedbank bring a strong understanding of regulatory requirements, giving collaboration an edge in ensuring compliance when integrating fintech solutions. Fintechs may also leverage the expertise that traditional banks have in cybersecurity and risk management, enhancing overall customer trust. On the other hand, Fintechs can provide traditional banks with nimble capabilities and access to new the underserved segments and rural areas where digital solutions can increase financial access. Additionally Fintechs embrace innovation that traditional banks aren’t as agile to explore in areas such as instant payments, digital lending, and blockchain solutions, ensuring competitive offerings for customers. Nedbank also has a Corporate Venture Capital unit invests in FinTech companies across Africa, under Corporate and Investment Banking.

DBA: What are the most significant challenges and opportunities you foresee for banks operating in the African digital finance space over the next 3-5 years?

CT: Africa is primed for rapid growth in digital finance for a myriad of reasons which present transformative opportunities like expanding payments and remittances also a key opportunity and a critical need for the continent. Another big challenge for the continent is bridging the gap on customer readiness — both individuals and small juristics — between cash and digital payments options. The market has evolved significantly the different types of digital payments solutions moving at a slower rate than anticipated. Building trust is key to scaling digital solutions.

Navigating regulatory evolution while driving innovation at scale is a key challenge. Africa’s fragmented regulatory landscape requires

banks to ensure compliance across multiple jurisdictions, minimise the costs of doing so while rapidly advancing digital transformation to obtain scale. Balancing disruptive innovations with cybersecurity risks, customer trust, and data protection in an increasingly digital ecosystem is critical. However, the opportunities are immense—from deepening financial inclusion to leveraging digital payments and AI-driven insights.

Nedbank’s expansion of digital lending solutions and focus on embedded finance in sectors like energy, mobility and retailers position us well to on these opportunities while addressing challenges head-on. Our initiatives, such as the PayShap real-time payment solution and the, exemplify our commitment to innovation and financial inclusion. In 2024, the PayShap API enabled approximately R570 million worth of payouts. We aim to scale digital capabilities across Africa, aligning with the Nedbank Africa Region regulatory frameworks and enhance cross-border financial transactions. These efforts pave the way for a more integrated and inclusive financial ecosystem across Africa.

Sustainable and green finance is another important opportunity. As Africa faces challenges in climate change, access to energy and water supply at affordable costs, and sustainable development financing, Nedbank capital for green projects, promotes financial inclusion, and integrates environmental, social, and governance principles. The Avo platform offers solar and water solutions, and soon, green financing for mobility and

infrastructure will accelerate. With urbanisation, financing for electric vehicles, sustainable public transport, and smart city projects will increase. Carbon trading and offsetting mechanisms will enable clients to purchase carbon credits to support carbon offsetting initiatives.

DBA: Beyond the hype, what emerging technologies do you believe will have the most transformative impact on banking in Africa, and how is Nedbank preparing for their integration?

CT: Artificial (AI) and machine learning are central to Nedbank’s digital evolution, supporting our. We’ve invested in AIdriven risk assessment and fraud detection tools to enhance security, while leveraging AI for personalised client experiences through predictive analytics and engagement across the customer journey, including onboarding, usage, and retention. Cloud computing and blockchain are also key focus areas, with Nedbank integrating distributed ledger technology (DLT) to improve transactional transparency, to gain efficiency and scale. Blockchain and can also enable more seamless and solutions. Our supports these technologies by enabling seamless integration and innovation. The use of (API) drives growth in SME markets. Our CashOut API facilitated approximately R2.4 billion in cashout payments by December 2024. We continue to explore blockchain-powered financial solutions in cross-border payments and smart contracts.

Nedbank is expanding into African markets, focusing on digital banking to meet growing demand. Enhancements to digital platforms

like the Nedbank Money app and provide secure and convenient services. The bank’s presence in multiple African countries through allows for tailored services. Our platform offers a seamless experience for personal and business needs, enabling local and international payments, statement downloads, and financial management.

Generation Z, poised to dominate the consumer landscape by 2030, presents challenges and opportunities for traditional banking. Through the significant investment in sharpening digital transformation proposition, Nedbank is poised to meet Gen Z’s demands through enhanced digital experiences like gamification, machine learning, and AI, aligning with their values of sustainability, equality, and transparency.

DBA: How can banks effectively balance the need for innovation with the imperative of maintaining robust security and regulatory compliance in the rapidly evolving digital landscape?

CT: At Nedbank, we believe security and innovation are not mutually exclusive. Our approach is built on “secure by design” principles, where cybersecurity is integrated into every stage of product development rather than being an afterthought. We have dedicated risk and compliance framework ensuring alignment with global best practices, such as (ISO) 27001 and Systems and Organisation Controls (SOC) 2 compliance. Furthermore, Nedbank’s investments in AIdriven anomaly detection allow us to pre-empt cyber threats while maintaining a frictionless user experience. Our leverages

industry-standard frameworks like Open Authentication 2.0 for authentication and authorisation, ensuring secure and compliant integrations. We include advanced security features such as biometrics and QR code scanners, as well as protection factors for clients when they use self-service options, such as-factor authentication, digital card blocking, and realtime management of personal profiles and security. Nedbank also continues to educate customers and employees on cybersecurity to recognise phishing attacks, scams and social engineering threats.

DBA: Nedbank has made significant strides in digital banking. Can you elaborate on the strategic vision driving Nedbank’s digital transformation and how it aligns with your broader business goals?

CT: Nedbank’s digital transformation is around Managed Evolution (ME) 2024, we completed our billion investment to core banking systems and enhance digital capabilities. Our strategy is focused on key pillars: Client-Centric Innovation, Scalability, and Sustainable Growth to inform our mobile first, integrated strategy that gives our clients the option of ‘Digital when you want it, human when you need it’ option.

Nedbank has made significant strides in digital innovation, offering a range of advanced solutions to enhance the banking experience for individuals and businesses. The Nedbank Money provides a comprehensive banking experience with instant payments, transactions, and

personal financial wellness capabilities. Additionally, the app supports small business owners with features lik ability to acquire machine digitally, context switching, and small merchant acquiring, making it a versatile tool for both personal and business banking needs. For can apply for a transactional account in less than 15 minutes, clients receive personalised offers in-app, clients can access more than 80 digitised services in the assisted by our Enbi, clients can access beyond — banking services like licences and direct payment of traffic fines, to name a few example.

SimplyBiz supports SMEs with digital banking services, business tools, and dedicated support, helping them streamline operations and manage finances more effectively. The Nedbank Business Hub (NBH) offers a secure environment for managing business banking needs, supporting approximately 535,000 active business clients with enhanced security, user management, and advanced transactional features. Nedbank’s (VAS) platform offers over 500 unique products and services, including instant payments, enhancing customer experience and providing additional benefits. The Avo allows clients to purchase essential products and services online with secure home delivery, featuring a comprehensive marketplace and various specialied services, with 2.7 million registrations. Lastly, the integrates Nedbank’s ecosystem with third-party providers, enabling value exchange among customer segments, with 73 active third parties by December 2024. These digital innovations highlight Nedbank’s commitment to

enhancing customer experiences, supporting business growth, and driving financial inclusion through advanced technology solutions.

These metrics highlight Nedbank’s significant impact on the South African economy, demonstrating our commitment to customer growth, digital innovation, sustainable development, and economic resilience. Our strategic focus on sustainable financing, coupled with our digital transformation efforts, positions us well to meet the evolving needs of our customers while maintaining a strong balance sheet. These efforts not only enhance the bank’s competitive position but also contribute positively to the broader financial sector and the economy. We are encouraged to have maintained #1 NPS ranking for the past 3 years, an achievement that bears testament to our strateg augmented by our entrenched and continuous service excellence programme, integrating behavioural economics in our solution solutions and engagement with customers and the leading digital capabilities we have built.

DBA: What specific initiatives has Nedbank undertaken to enhance financial inclusion, and what metrics are you using to measure the impact of these efforts? What are some of the key learnings you have had along the way?

CT: Nedbank is a organisation ‘financial experts who do good’. we leverage our financial expertise with the principle of ‘design for inclusivity’ embedded into our CVP design across the board. We are dedicated to making banking accessible to everyone in South Africa through innovative digital solutions, comprehensive

support program, and sustainable development initiatives. Here are the key proof points of our efforts:

Nedbank Money App: Our app allows for safe and secure banking 24/7 offers enhanced security with biometric login, instant money transfer, personalised offers — free credit score, bill payment, car licence renewal ability to purchase value-add services [airtime, data & electricity], shop deals on Avo, manage cards & profile and find an ATM or branch. We also offer a comprehensive range of insurance products on the Money from quotation to fulfilment with ~3 million digitally active clients.

MiGoals Accounts: The Nedbank MiGoals transactional account offers digital capabilities like virtual cards, MoneyTracker for budgeting, Balance Peek, 24/7 digital banking via the Money app, Online Banking, and Cellphone Banking. It supports contactless payments, Greenbacks rewards, MyPocket savings, and servicing capabilities through our, Enbi, the virtual assistant, enhancing convenience and security for users.

Greenbacks Rewards Programme: The Greenbacks leverages digital capabilities like the Nedbank Money for managing rewards, including to 2% unlimited on transactions. Online Banking for redeeming Greenbacks, and the Avo SuperShop for exclusive discounts. Users can also utilise the Greenbacks SHOP Card for cash withdrawals and purchases, and benefit from a tiered rewards system that

increases earn rates.

Value-Added Services (VAS) platform is a big driver of financial inclusion which offers over 500 unique products and services, including instant payments like PayShap at low costs and money transfer product, enabling clients to send money to any South African cellphone numbe continues to show significant growth. Our offerings were enhanced to include vehicle quick-quote insurance, licence renewals, traffic fine payments as well as expanded assurance and funeral product functionality.

Instant Payment Solutions: 27 million PayShap transactions processed.

Small Business Account Offerings: Nedbank offers comprehensive small business solutions, including Startup Bundle (zero maintenance fees for six months), Business Bundle 50 (50 transactions & R50,000 cash deposit benefits), Business Bundle 100 (100 transactions & R100,000 cash deposit benefits).

Merchant/Payment Solutions: Solutions like PocketPOS (a Bluetooth-enabled mobile card reader with chip-andPIN and contactless payment capabilities), Android POS (a standalone payment terminal with receipt printing and sameday settlements), and Scan to Pay, providing affordable, scalable, and technology-driven options to help businesses transact smarter and grow faster.

Small Business Loan on App:

We have prioritised simplifying the lending process for small businesses with our instant Small Business Loan feature on the Money app. Clients no longer need to submit financial documents and can receive automatic payouts upon application approval.

SimplyBiz: Free business development support platform.

Our initiatives reflect our commitment to enhancing financial inclusion and supporting the South African economy. We’ve learn the importance of a customer-centric approach, leveraging technology, fostering partnerships, and continuously improving our services based on feedback and market trends.

DBA: How is Nedbank leveraging data analytics and AI to personalise customer experiences and improve service delivery in the digital realm?

CT: Nedbank’s use of “datadriven intelligence” is central to our customer engagement strategy. We are proud to employ AI-powered credit risk models that enable smarter lending decisions, particularly for SMEs and underbanked individuals. Our innovative AI-driven chatbots and virtual assistants provide 24/7 digital support, significantly reducing friction in customer interactions. Additionally, our cutting-edge analytics allows us to provide recommendations on savings, investments, insurance, and transactional through the Nedbank Money app and prompt to our channels.

Key metrics from our advanced information analytics using machine learning include:

Partners: Partners support our digital and open banking initiatives authentication, account transactions, payments, rewards, wallet services, and value-added services.

BP: Cashback on fuel, Nu Metro Cinemas: Discounts on movie tickets. Avo SuperShop: Earn and redeem Greenbacks, Greenbacks Travel: Discounts on flights and Apple and Samsung: Discounts on products.

When selecting partners, we prioritise those who align with our strategic goals, offer innovative solutions, support our sustainability goals, and enhance our customers’ banking experience.

DBA: What advice would you give to other banks in Africa looking to successfully navigate the challenges and opportunities of the digital banking revolution?

CT: The digital banking revolution presents both challenges and opportunities, and there is no one-size-fits-all approach for banks in Africa. However, there are several key strategies that can help navigate this evolving landscape successfully:

Embrace Open Banking and Collaboration: To create cohesive de-borderised banking, collaboration with Fintechs and regulators is essential to unlocking new business models. De-borderised banking fosters innovation and allows banks to offer more personalised and diverse services to their customers by removing geographical and regulatory barriers.

Prioritise Cybersecurity: As digital adoption grows, so do cyber threats. Implementing a robust AIdriven fraud prevention framework is crucial to protect customer data and maintain trust.

Leverage AI and Automation: AI can significantly enhance personalisation, improve credit scoring, and optimise operations at scale. By leveraging AI, banks can provide better customer experiences and streamline their processes.

Focus on ESG and Impact Banking: Sustainable finance solutions are becoming a key differentiator in the African banking landscape. Banks that combine innovation with purpose-driven growth will thrive. Nedbank’s and digital initiatives exemplify this approach, driving financial inclusion and innovation.

By adopting these strategies, banks in Africa can effectively navigate the digital banking revolution and capitalise on the opportunities it presents.

DBA: What is your long-term vision for Nedbank’s role in shaping the future of financial services in Africa?

CT: The future of financial services that we would want to create is an integrated and connected experience seamlessly into the everyday lives of. Nedbank is committed to driving financial inclusion, digital transformation, and sustainable banking across Africa. Our long-term vision is to be the continent’s most customercentric and digitally innovative financial institution, enabling businesses and individuals to thrive in an increasingly digital world. Through strategic

partnerships, digital-first solutions, and ESG-led banking, we aim to shape the future of finance while making a tangible impact on economic growth and sustainability.

Our purpose is to use our financial expertise to do good for individuals, families, businesses, and society. This purpose underpins all our initiatives and drives us to create meaningful, positive change. By leveraging and data-driven decisionmaking, we ensure that we provide the best solutions for our clients at the right time. Our focus on rewards and shared value further enhances customer engagement and loyalty. Our and initiatives like PayShap and the Avo super app are central to this vision, fostering innovation and enhancing customer experiences. PayShap, launched in 2023, is set to become the new payment medium across the financial services industry, primarily serving as a payment gateway. The Avo super app and, released even earlier, continue to drive our e-commerce and open banking efforts.

In alignment with the NAR drive to create cohesive de-borderised banking, we collaborate with Fintechs and regulators to unlock new business models. This approach fosters innovation and allows us to offer more personalised and diverse services to our customers by removing geographical and regulatory barriers. By focusing on these areas, we strive to build a more inclusive and sustainable financial ecosystem that benefits everyone

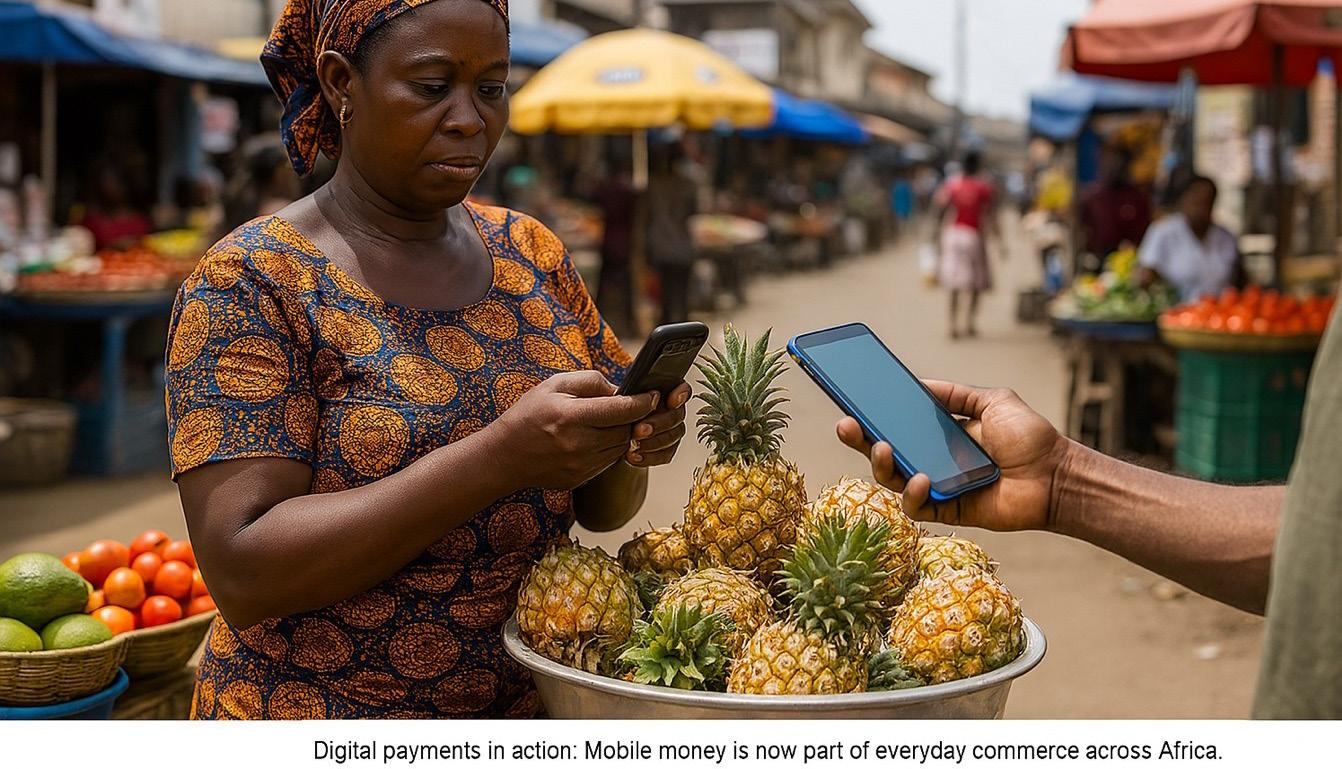

Afruit seller in Accra now accepts digital payments on her feature phone. A motorcycle mechanic in Kigali receives micro-loans based on his mobile transaction history. A teenage girl in Northern Nigeria gets her school fees paid directly into her mobile wallet by a government scholarship program. These aren’t isolated anecdotes. They are reflections of a seismic shift unfolding across Africa:

Mobile money is no longer the disruptive newcomer. It has matured into an essential utility across the continent. According to GSMA, over 160 million active mobile money accounts were recorded in Sub-Saharan Africa in 2023. More than a third of adults in countries like Ghana, Kenya, and Côte d’Ivoire now rely on mobile wallets for daily transactions, bill payments, remittances, and savings.

the digital democratisation of finance, led by mobile money.

But there’s a twist. As mobile money continues its impressive march, artificial intelligence (AI) is quietly entering the stage, reshaping what financial inclusion means for the next generation of African consumers.

Looking forward, mobile money is poised to converge with other digital infrastructure: eIDs, blockchain, cross-border payment rails, and more.

AI will be crucial here too. It can help manage compliance, automate fraud detection, and customise offerings for crossborder users.

But the true frontier is blended finance: public-private collaborations where mobile money becomes a channel not just for commerce, but for social impact. Picture AI-driven health insurance distributed via mobile wallets. Or climate risk alerts bundled with micro-insurance, localised and timely.

The African mobile money story has never been about the technology itself. It’s about what that technology enables: dignity, access, opportunity. As we layer AI onto this foundation, the risk is forgetting the human pulse at the center of it all.

So yes, the future of financial inclusion in Africa is digital. But it must also be deeply human. Because in the end, an empowered consumer isn’t defined by their mobile balance or their algorithmic score. They’re defined by the freedom to choose, to grow, and to belong in an economy that sees them.

Let’s make sure we build that future with them, not just for them.

Faheem Ali

Tech Leader and Expert in AI Insights, with extensive experience in leading AI projects and educating professionals on AI applications.

Faheem has a strong management background in the Inclusive Finance and Banking domain with insightful understanding of financial & technology sector in various markets in Central Asia, Asia Pacific, Africa and USA.

He has extensive experience in digital product development, corporate and product marketing strategies formulation, digital transformations, DevOps, cybersecurity, and FinTech/ FinServ operations.

He also delivers workshops, training, consulting and executive coaching services to support this work including to support a culture (change agent) that encourage people to think differently, take actions, and focus on the customer to drive the business growth. He is an international speaker and trained more than 56,000+ delegates across the globe.

The emancipation of digital banking products has no doubt transformed and contributed to consumer needs across Africa. This has empowered customers and increased the banking customer base alongside the number of users on the continent. Cashless policy is a technological innovation to make banking easier and recognise consumer inclusivity. Over the years before the evolution of mobile banking, we had a low record of 12% banking customers across Africa due to poor roads and insecure access to the physical banks, poor means of communication, locations and regional barriers, among others. Many had a lot of business to conduct with the bank but were disenfranchised of the privilege. However, the evolution of mobile banking has the primary focus and targets of certain entities in the financial markets, which are the Small and Medium Enterprises (SMEs), Fast-Moving Consumer Goods (FMCGs), e-commerce etc., and after these are consolidated, it is then planned to move to the general merchants and corporate banking.

These mobile banking products are a work in progress using an agile methodology, as they require everyday redesign and reinvention of new ideas. We are yet to get there, as it is meant to make Africa transparent in financial literacy,

encourage and grow digital finance, a hub of entrepreneurial giants and a wealthy continent that attracts investors from other continents to run their businesses seamlessly in Africa.

The impact of Mobile Money as a financial infrastructure is to address the weak points of the payment system and aims to make it easier for Africans to build global businesses that can make and accept any payment across Africa and around the world. The Fintech

ecosystem is legally backed up by the apex bank to build services like KYC, account opening, e-cards, payment gateways, account service compliance, crypto-trading and value-added services, all encompassed to serve a single consumer.

Financial inclusion is to penetrate the unbanked downtrodden in society and support them financially to transact their finances for business expansion and create wealth from it, all of this without approaching any physically structured banking institution. In other words, financial inclusion

Esan Head, Fleet and Procurement Management VFD Group Plc, Nigeria

The African consumer is evolving. No longer a passive recipient of financial services, today’s digitally savvy consumer is demanding more—more convenience, more security, more accessibility, and more empowerment. As mobile penetration soars and fintech innovations accelerate, digital banking is undergoing a radical transformation, driven by the needs and expectations of an increasingly informed and proactive consumer base. Financial institutions must adapt or risk irrelevance in a landscape where the influential consumer is not just shaping the future of digital banking but defining it.

Africa is home to some of the world’s most engaged mobile users. The GSMA reports that by 2025, smartphone adoption in sub-Saharan Africa will reach 87%, up from 50% in 2020. With mobile connectivity comes digital fluency, and African consumers are using technology in ways that are redefining the financial services sector. The new consumer expects seamless mobile experiences, instant transactions, and tailored financial solutions that align with their daily realities.

This demand for digital banking is also fuelled by Africa’s youthful population— over 60% of sub-Saharan Africans are under 25. This generation, born into a mobile-first world, expects financial services to match the intuitive and frictionless experiences they enjoy on social media platforms and e-commerce sites. For them, banking is not a place but an action—instant, personalised, and always at their fingertips.

Mobile banking has been at the heart of Africa’s financial revolution, but mobile money has been the true game-changer. From M-Pesa in Kenya to MoMo in Ghana, mobile money platforms have driven unprecedented financial inclusion. According to the World Bank, over 33% of adults in sub-Saharan Africa now have a mobile money account, compared to the global average of 4.5%.

These platforms have moved beyond simple peer-to-peer transactions, integrating with businesses, government services, and international remittances. In doing so, they have influential consumers to take greater control of their financial lives. With digital wallets, micro-savings, and credit facilities embedded within mobile money ecosystems, consumers can now access financial products that were previously out of reach.

However, the growth of mobile money also brings challenges, particularly

in interoperability. Consumers expect seamless cross-border and inter-platform transactions, yet many services remain siloed. The push for interoperability will define the next phase of mobile money evolution, ensuring that consumers can transact effortlessly, regardless of their chosen provider.

As digital financial services expand, so too must financial literacy. The influential consumer is not just one who has access to financial tools but one who understands how to use them effectively. Across Africa, fintech start-ups, banks, and mobile money operators are investing in digital education initiatives to bridge knowledge gaps.

From AI-driven chatbots that provide financial advice to interactive apps that teach budgeting skills, digital literacy is being embedded into the consumer experience. Governments and private sector players alike must continue prioritising education, ensuring that digital financial empowerment does not lead to over-indebtedness or financial mismanagement.

Real-time payment (RTP) systems are rapidly reshaping the global financial ecosystem, offering unprecedented opportunities for banks, businesses, and consumers. More than 70 countries have implemented real-time payment (RTP) services, collectively processing billions of transactions annually, spanning e-commerce, bill payments and peer-topeer payments. These services represent more than technological innovation – they are fundamental infrastructure for modern financial services, particularly in regions with emerging banking landscapes, such as Africa. Changing consumer expectations and technological capabilities are driving the digital transformation of payments. Traditional payment methods – cash, debit cards, and credit cards – are now complemented by cheaper, more flexible, and instant solutions. The rise of e-commerce and mobile technologies has accelerated this shift, creating demand for payment systems that are faster, more convenient, and more inclusive. RTP fills this gap with instant, secure, seamless transactions 24/7, including weekends and public holidays. Settlement is immediate, with both parties getting payment confirmation in seconds.

In developed economies, RTP undoubtedly has utility. The option reduces payment friction and gives consumers more choice about how to pay. RTP gives retailers additional ways to offer value and improve customer experiences, as well as reduce the cost of handling cash and accepting traditional credit card payments.

But it is in emerging markets that its transformative value truly comes to the fore. RTP can drive financial inclusion for unbanked and under-banked people, entrepreneurs and businesses. This, in turn, boosts overall economic potential and broadens the total addressable market for banks.

Two standout examples of RTP in emerging markets illustrate this transformative potential.

In India, the Unified Payments Interface (UPI) has revolutionised digital transactions since 2016. Developed by the National Payments Corporation of India, UPI integrates over 200 banks and processes more than 10 billion transactions monthly. By enabling mobile-based peer-to-peer and

person-to-merchant transactions, UPI has dramatically expanded financial access for Indians.

The platform’s success is remarkable – by November 2022, UPI had over 300 million monthly active users in India. In January 2024, the platform processed 12.2 billion transactions worth $222.17 billion – up 41.72% from transaction values a year ago. The key is that UPI didn’t just introduce a new payment method to existing banking customers. Instead, it fundamentally restructured India’s financial ecosystem by bringing millions of

previously unbanked individuals into the formal financial system.

Banks concerned with RTP cannibalising existing, more expensive, payment channels should pay attention to the Indian model. Once UPI customers reach a certain threshold of transactions they are obliged to open a business bank account – demonstrating how RTP can increase the overall customer base – ultimately a net win for banks.

Brazil’s Pix – created by Banco Central do Brasil – demonstrates another innovative approach to RTP. Processing over 100 million daily transactions with zero consumer fees, Pix operates with minimal intermediaries, reducing transaction costs and increasing market efficiency. Its design allows instant transfers across different account types and provides payment options for non-nationals, showcasing the flexibility of modern payment systems.

Central to the success of both services is appropriate choice about how to pay and be paid. A simple QR code is enough for a retailer to get started, with users paying through dedicated apps or their banking app. Retailers can also integrate RTP into their point of sale (POS) devices, but this is not a requisite to accept payments.

RTP payment providers should also consider local circumstances and user preferences when implementing a system. For instance, USSD is a critical channel for RTP in parts of Africa. Using USSD broadens access to customers who only have basic phones, have limited access to data or are in rural areas with limited internet coverage.

UPI gives merchants the option to accept payments via a payment sound box. Popular with street vendors and small shops, this is a portable speaker that includes a QR code display. Once the payment has cleared, the speaker announces the confirmation of the transaction. This alerts merchants in real time and allows them to continue cooking or assisting multiple customers at once without the need to check their phones for payment confirmation. This also reduces the risk of fraudulent payment confirmations from the customer.

In Africa, RTP services are emerging as critical solutions to longstanding financial challenges. Countries such as Egypt, Kenya, Nigeria, and South Africa are pioneering RTP services: InstaPay, PesaLink, NIBSS Instant Payment, and PayShap respectively. A local nuance is that these services are strategic tools for integrating mobile money platforms with traditional banking, promoting financial inclusion and accelerating economic activity.

While RTP adoption rates are accelerating, with billions of transactions processed annually across the continent, challenges to roll out do exist. Chief among these are infrastructure gaps and regulatory complexities.

Nevertheless, African markets present a unique opportunity for RTP implementation. Low banking penetration, high mobile money usage, and diverse technological infrastructures require adaptive, sophisticated payment solutions.

Trends supporting RTP in Africa include:

Cross-border payments: Partnerships like Namibia’s integration with India’s UPI system showcase efforts to streamline regional and international transactions.

Mobile money evolution: Interoperability between mobile wallets and bank accounts is on the rise.

E-commerce growth: RTP is becoming integral to online retail platforms, reducing the need for cash-on-delivery.

Regulatory support: Central banks across Africa are prioritising digital payment ecosystems to drive economic growth.

Real-time payment systems have the power to transform Africa’s financial landscape. By integrating technology with local needs, RTP drives financial inclusion, economic efficiency, and consumer convenience. As adoption grows, Africa can become a global leader in real-time payment innovation.

The advantages of real-time payments extend far beyond convenience and choice. For consumers, they offer safety, instant access to funds and purchases, and eliminate traditional transfer waiting times. Businesses benefit from enhanced cash flow management and faster transaction processing. Banks can open new revenue streams and improve customer retention by offering cutting-edge financial solutions.

A significant contribution that RTP makes to the overall economy is the reduction of cash in the ecosystem. According to a Boston Consulting report, in developed economies, the cost of cash acceptance is typically higher than most electronic payments. RTP services provide a more efficient alternative, reducing indirect and back-office costs for merchants. RTP drives the digitisation of payments, decreases money laundering and fraud risks, and

creates more transparent financial ecosystems.

Crucially, real-time payments can be transformative for financial inclusion. They allow previously unbanked or underbanked businesses and individuals to build transaction histories. This data enables banks to confidently offer new customers additional financial services like credit and insurance, creating a virtuous cycle of economic empowerment.

While e-commerce has accelerated the need for more convenient ways to pay, these new payment options in turn drive e-commerce. Faster checkouts, reduced cart abandonment, increased basket size, and the ability to offer subscription services and microtransactions are some of the ways RTP boosts e-commerce. Underlying this all is the improved cash flow and working capital, allowing e-commerce providers to grow their businesses.

According to Africanenda’s State of Inclusive Instant Payment System in Africa 2023 report, person-toperson and person-to-business payments make up the bulk of RTP use cases in Africa. But B2B payments, along with digital wages and government-to-person payments are critical for driving financial account and payment adoption. This is an important opportunity for banks bringing RTP to their markets, as B2B and G2P payments are typically high volume, high value, more frequent and repeat regularly.

Implementing RTP services is not without challenges. Infrastructure requirements can be costly, cybersecurity risks are inevitable, and integration and interoperability across different banking platforms and regions remain complex. Concerns about technological capabilities, fraud prevention, and lagging user awareness can slow adoption.

Top of mind for many is how RTP will handle issues such as repudiation and dispute processing, compared to the well-established processes and protections of traditional payment channels, such as credit cards. Both Pix and UPI, as the leaders in emerging market RTP, have welldocumented processes for refunds, fraudulent payments, and dispute redressal.

These challenges and concerns are where strategic partnerships become crucial. By collaborating with experienced payment technology providers, banks can navigate these challenges effectively. The right partner can help financial institutions implement the sophisticated digital infrastructure required to process transactions in real time in a robust, secure way.

It is to banks’ own advantage to actively support the growth of digital payments, and especially RTP. Banks are essential players here, as they control part of the user experience. The benefits to banks include a decrease of cash in the ecosystem and associated costs such as ATM and physical bank

Country System Name Launch Year Operator Pricing Key Feature

Egypt IPN Instapay 2022 Central Bank of Egypt Free Tiered free transactions

Ghana GIP GHIPSS Instant Pay 2016 GhIPSS Free Mobile money integration

Kenya PesaLink M-Pesa 2017 IPSL KES 50–200 Complement to M-Pesa

South Africa PayShap PayShap 2023 BankservAfrica R1–R7.50 Small-value QR transactions

Nigeria NIP NIBSS Instant Payment 2011 NIBSS NGN 50 High transaction volume

Ethiopia EIPS EthSwitch 2020 EthSwitch Minimal fees Mobile wallet integration

Zambia ZECHL Zambia Electronic clearing house limited 2015 Bank of Zambia $0.36 to $0.72 Retail and corporate transfers

Mauritius MACSS Mauritius Automated Clearing and Settlement System 2019 Bank of Mauritius Low routing fees High-value and retail payments

Mozambique SIMO The Real-Time Wholesale Transfer Settlement Subsystem (MTR) 2012 SIMO Institutiondependent Broad interbank coverage

Rwanda eKash RSwitch 2022 RSwitch Minimal fees Mobile money interoperability

Zimbabwe ZIPIT ZIPIT 2013 ZimSwitch 1% of amount Daily high transaction volumes

Uganda UNIS Uganda National Interbank Settlement (UNIS) 2005 Bank of Uganda Set by bank real-time gross settlement

Africa’s digital banking landscape is undergoing a transformative shift, largely driven by governments prioritising consumer empowerment and protection. Today’s African consumer differs significantly from two decades ago—now digitally savvy, connected, and demanding innovation, inclusivity, and security. This article explores how consumer needs are shaping the evolution of digital financial services, from mobile banking to financial literacy, and the critical role of trust in fostering this transformation.

Over the past two decades, Africa’s financial institutions have increasingly prioritised accessibility and inclusion rather than traditional brick-and-mortar banking infrastructure. Regulatory frameworks have evolved to create additional categories of financial service providers, now classified as payment service providers. When Strive Masiyiwa was advocating for a Mobile Network Operator licence in Zimbabwe, few anticipated the profound impact mobile technology would have on financial services. Today, mobile phones have become our primary banking interface.

Digital finance focuses predominantly on delivering banking solutions directly to consumers, including those in remote or underserved areas, while also addressing the needs of persons with disabilities— one of the world’s largest minority groups.

Banks, on the other hand, often represent physical infrastructure, while “banking” encompasses the broader ecosystem of financial services, including digital platforms, mobile payments, microsavings, microinsurance, and microloans. By emphasising banking functionality over traditional institutions, Africa is accelerating financial inclusion, empowering small businesses, addressing the needs of unbanked populations, and supporting informal sector participants who remain vulnerable to economic shocks due to limited access to appropriate insurance products.

As the sun sets over a small village in Mutasa district in Manicaland province, Zimbabwe, Mwaraseni, a local entrepreneur, reaches for her phone—not to check social media, but to manage her

business and personal finances. With a few taps, she pays suppliers from funds received throughout the day, remits payments to MoneyMart Finance (a local microfinance institution offering daily repayment options to women entrepreneurs), and allocates savings for her children’s education and future needs such as funeral insurance. This scenario, commonplace today, would have been revolutionary just 14 years ago.

Zimbabwe’s relationship with digital finance presents a particularly compelling case study. When many countries were still deliberating the viability of mobile money systems, economic necessity had already transformed Zimbabweans into financial innovators. Few catalysts accelerate financial innovation as effectively as hyperinflation that devalues physical currency below the cost of the paper it’s printed on.

Zimbabwe’s EcoCash evolved beyond merely replicating Kenya’s M-Pesa model—it became an essential financial lifeline during periods of economic challenge, functioning as a pseudocurrency. When conventional currency experiences extreme volatility, digital finance transitions from convenience to survival strategy.

Across Africa, narratives similar to Mwaraseni’s have become routine as mobile money and digital banking

transform financial landscapes. What originated as solutions to infrastructure limitations have evolved into sophisticated ecosystems now influencing global fintech developments.

“Zimbabwe didn’t simply adopt digital finance—it reinvented it,” explains Dr. Ethel Mupambwa, board member at the Digital Finance Practitioners Association of Zimbabwe. “While Zimbabwe’s case has unique elements, this reinvention occurred throughout Africa, pioneered by Kenya. When developed markets focused on advanced technologies and smartphone banking applications, Africa created SMS and USSD-based solutions compatible with basic devices, effectively democratising financial access.”

The debate over customer ownership that once preoccupied banking executives has been rendered obsolete. Traditional power dynamics in banking have fundamentally shifted. The customer owns themselves. Two decades ago, African consumers were largely passive recipients of whatever services financial institutions offered; today, they actively shape the market, demanding solutions that address their specific needs and circumstances. Regulatory frameworks increasingly support and protect consumer interests.

This transformation is particularly evident

The evolution of mobile money across Africa demonstrates how consumer requirements drive innovation. Services that began as simple money transfer mechanisms have developed into comprehensive financial ecosystems.

Gerald Munyaradzi Nyakwawa Head of Digital Channels - Fintech MoneyMart Finance (Private) Limited

in how digital financial services continue to evolve. Mobile money platforms that originated as peer-to-peer transfer services have expanded significantly. Today, consumer demand has compelled providers to integrate savings, loans, insurance, and investment products—all accessible with minimal effort just by thumb tapping.

The power relationship has inverted: rather than banks determining consumer needs, consumers effectively direct banks’ development priorities. Institutions that respond thrive; those that don’t risk obsolescence. Research from the COMESA Business Council identified demand for instant, interoperable cross-border retail payment systems, prompting forwardthinking financial institutions to prepare for this transition.

Financial institutions cannot afford to disregard these trends, particularly given Africa’s predominantly young population of digital natives. Continental initiatives to bypass legacy financial systems include the establishment of the Pan African Payments and Settlement System (PAPSS), designed to enhance affordability of digital finance and promote trade.

Consider Kenya’s M-Pesa, launched in 2007 primarily for remittances. Today, the platform supports savings accounts (M-Shwari), loans (Fuliza), international transfers, merchant payments, and healthcare financing options. Similarly, Zimbabwean consumers can initiate online payments directly from mobile money wallets. Global payment networks like VISA and Mastercard have established partnerships with numerous payment service providers across Africa to enable these capabilities. The COMESA Business Council is exploring escrow account mechanisms to facilitate trade and mobile money payments.

Through interactions with personal and professional networks, I’ve observed that consumer inquiries have evolved beyond basic functionality questions like “Can I transfer money?” to more sophisticated considerations of whether they can manage their entire financial lives via mobile devices. The answer is increasingly affirmative. This expansion reflects growing consumer sophistication. As users become comfortable with basic digital financial services, they seek more complex products previously available only through traditional banking channels. The following financial services are now readily accessible:

Micro-investment platforms such as Piggyvest in Nigeria and Chipper Cash across multiple countries are democratising investment access

Alternative credit scoring systems utilising non-traditional data enable lenders to extend credit to individuals without conventional banking histories

Insurance products

Savings products

“Buy now, pay later” platforms

While I confidently affirm the possibility of managing one’s entire financial life through mobile technology, I consistently emphasise the importance of trust within digital financial ecosystems.

Despite impressive growth, the industry faces significant challenges—primary among them building and maintaining consumer trust. Data breaches, fraud, and system outages can rapidly erode confidence in digital platforms.

“The most sophisticated application or fintech ecosystem provides little value to consumers if they don’t trust it with their financial assets,” explains Foster Ngorima, Data Protection Officer at MoneyMart Finance. “African consumers have become increasingly knowledgeable about security considerations and are demanding enhanced protections. This has prompted numerous regulatory authorities to implement consumer protection legislation, though enforcement remains inconsistent.”

Financial service providers that fail to prioritise transparency, robust security measures, and clear communication during incidents risk developing weak customer relationships, diminishing trust, and ultimately threatening their viability as ongoing concerns.

Financial Literacy 2.0

Traditional financial literacy initiatives focusing on fundamental concepts like saving and budgeting must now be enhanced with content relevant to increasingly sophisticated consumers. Today’s digital financial landscape requires additional knowledge regarding data privacy, digital security, and the evaluation of increasingly complex financial products.

Africa has already implemented innovative approaches to financial literacy. These include interactive voice

response (IVR) systems delivering financial education in local languages to users with limited literacy in Ghana. Rwanda has established a government apprenticeship programme specifically designed to increase digital literacy among its citizens.

As consumers continue driving Africa’s digital financial revolution, several trends are emerging that will likely shape the next development phase.

We have witnessed the integration of informal financial practices into mainstream formal systems. Digital platforms now support traditional savings groups. In Zimbabwe, MoneyMart Finance has introduced a hybrid group savings and lending product. Super apps and embedded finance solutions are following established Asian models. Environmentally conscious consumers are creating demand for sustainability-linked financial products.

The mandate is clear: develop inclusive, accessible, secure, and valuable services that address authentic needs in Africa and for Africa—or risk obsolescence. The principle of “nothing about us without us” has never been more relevant.

For financial institutions, regulatory authorities, and technology providers, this consumer decree represents both a challenge and an opportunity. Organisations that align their offerings with consumer expectations will contribute significantly to the next chapter of Africa’s remarkable digital finance narrative.

In villages, towns, and cities across the continent, millions of individuals like Mwaraseni aren’t merely utilising digital financial services—they’re actively shaping them with each transaction. Through this process, they’re creating financial systems specifically designed for African realities.

Gerald Munyaradzi Nyakwawa is a fintech specialist focusing on emerging markets and consumer trends in digital banking. He has researched digital financial services across multiple African markets and advised financial institutions on consumer-centred innovation strategies.

Africa’s digital finance sector is booming. From mobile money to blockchain-based solutions and digital banking platforms, fintech innovation is reshaping how Africans transact, save, invest, and access credit. For example, according to the GSMA, about two thirds of the globally processed $1.4 trillion value of mobile money transactions occurred in Africa. As the continent leapfrogs into a digital-first economy, two elements will determine the sustainability and scale of this growth: innovation and trust.