$8,371,415,427 In Sold Volume Since 2019

13,340 In Sold Transactions Since 2019

340+ Local Real Estate Experts

12 Offices

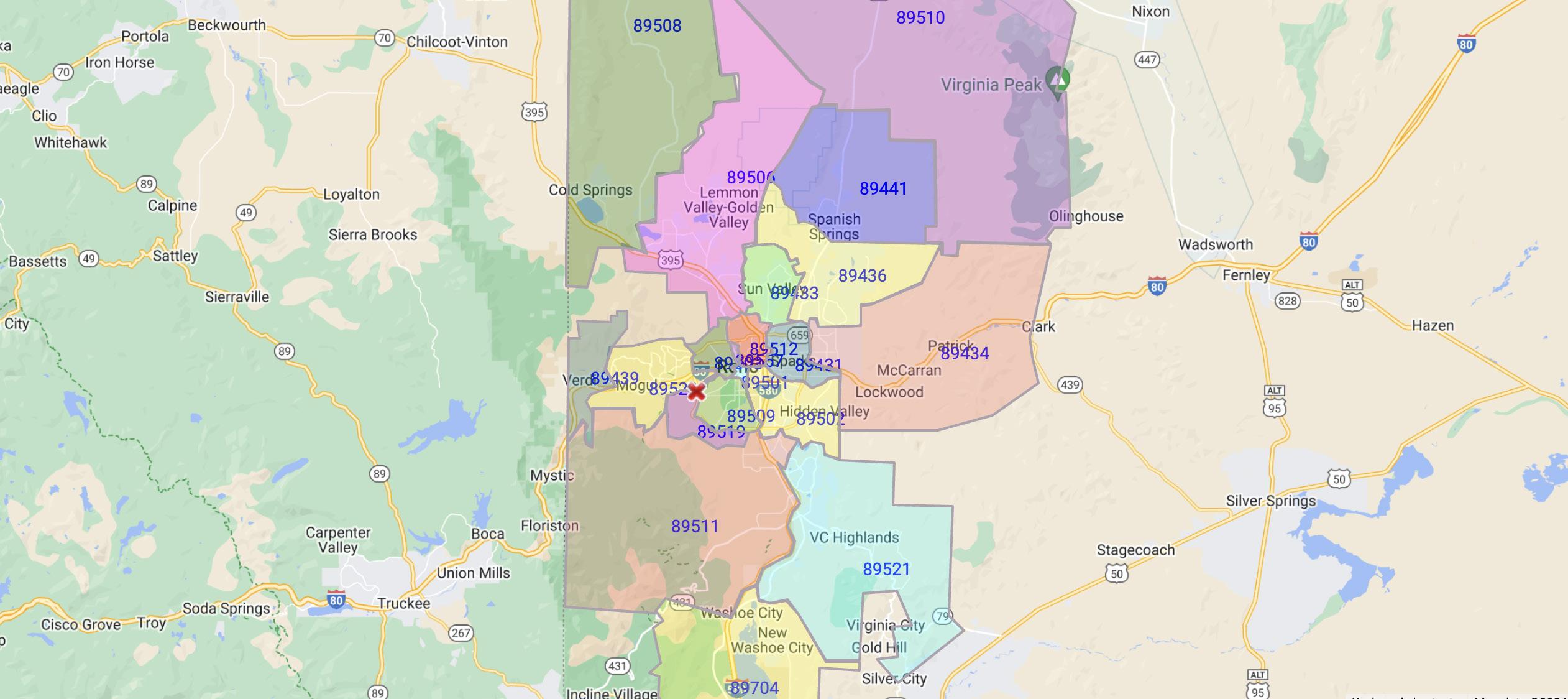

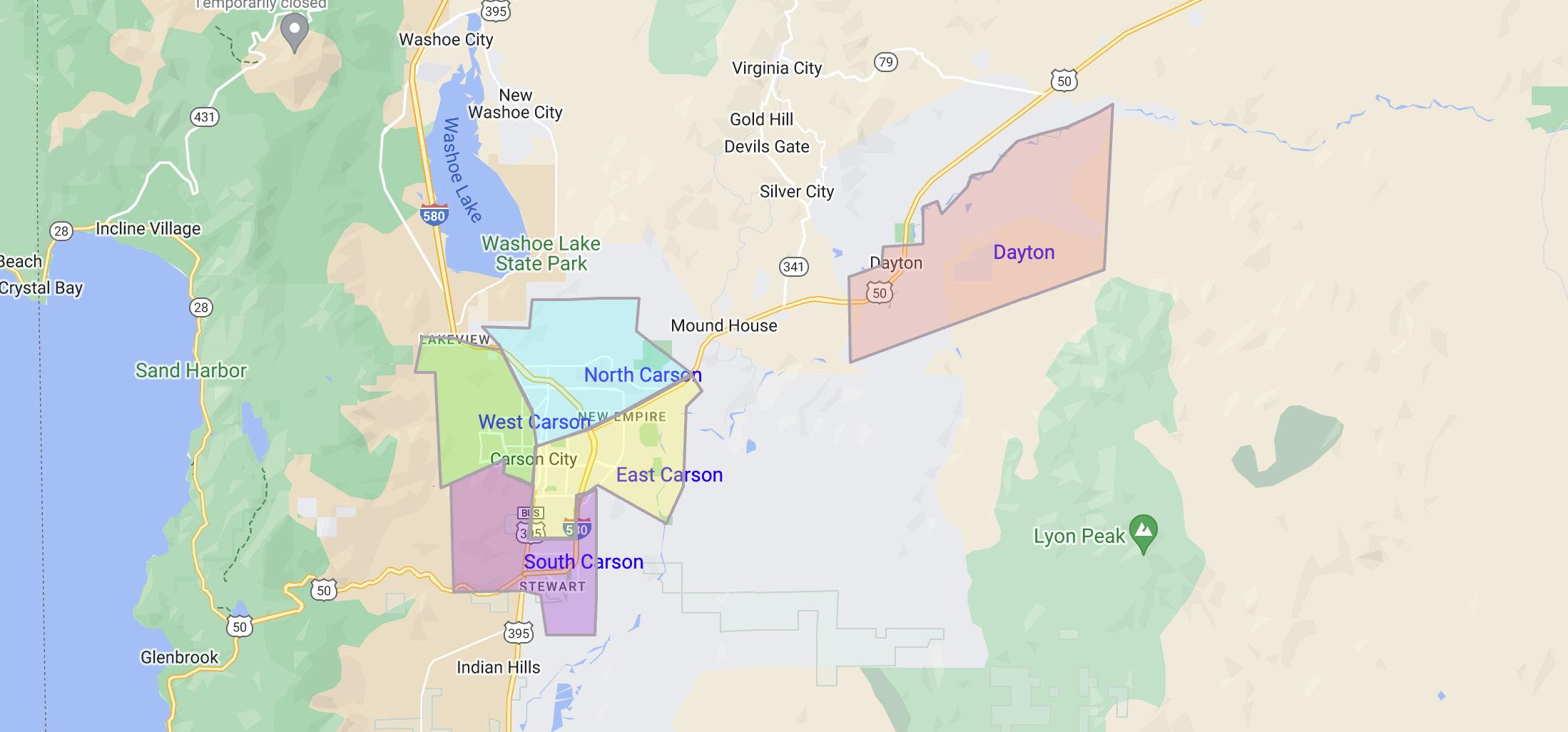

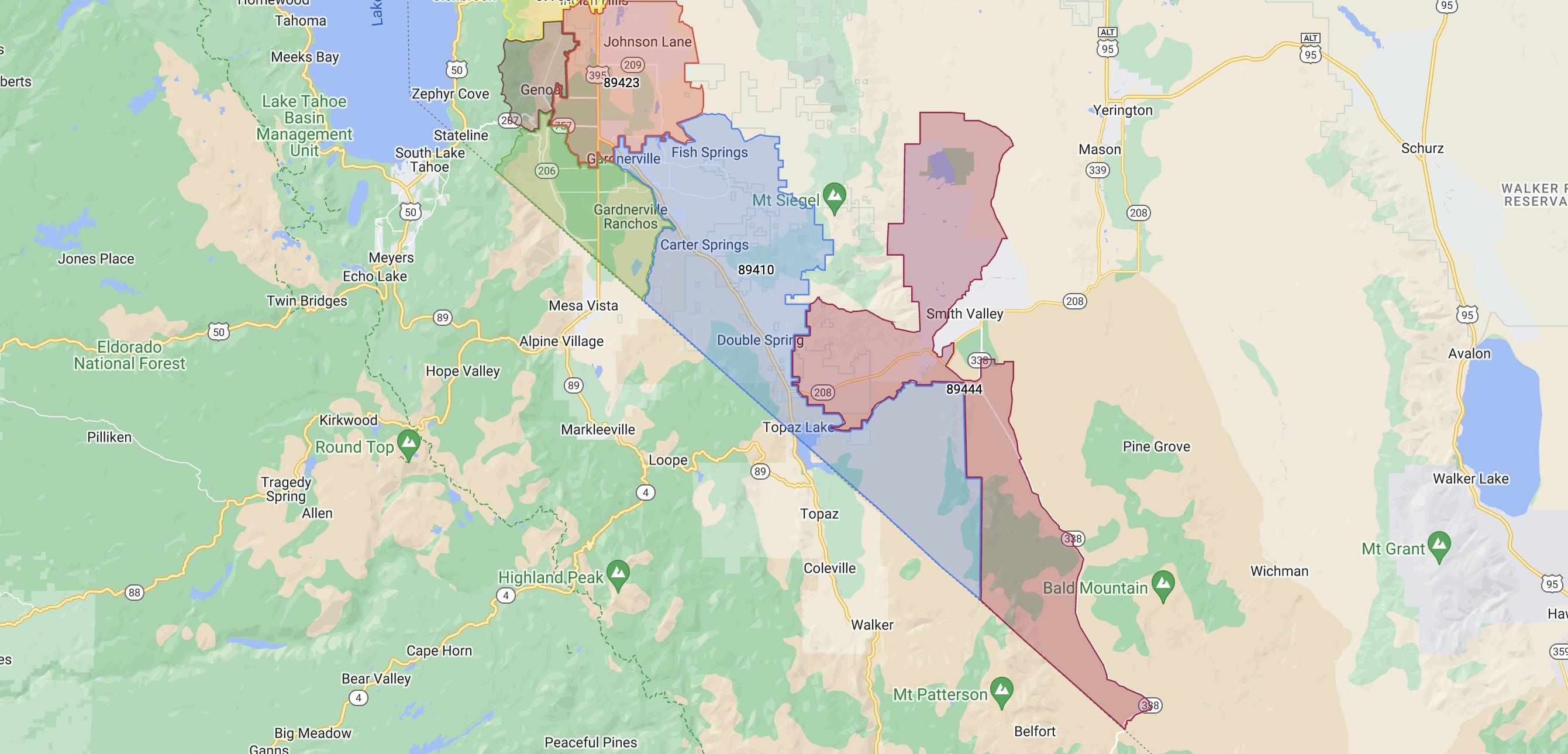

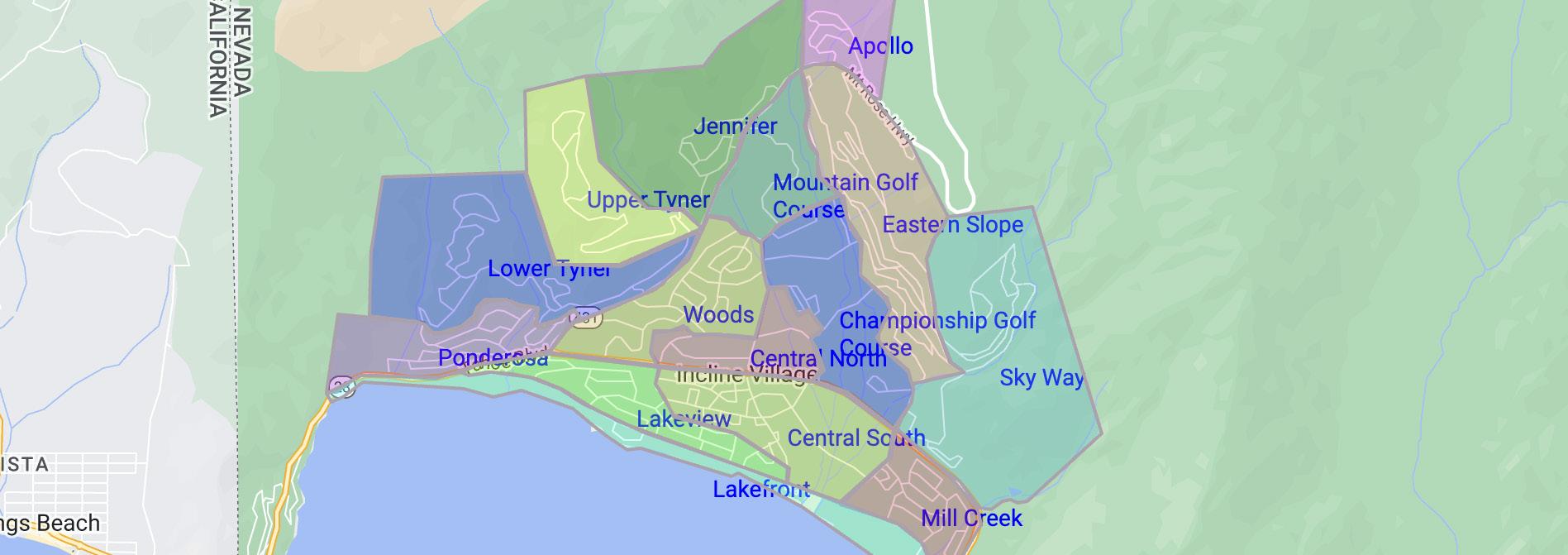

1,686 1,196 70 2ND

237 148 111 2ND QUARTER Apr 1st - Jun 30th

$543,975

2ND QUARTER Apr 1st - Jun 30th

2ND QUARTER Apr 1st - Jun 30th $1,208,000

‘I

Think you’re not ready to unlock homeownership yet?

That the financial hurdles are too high? You may be short-changing yourself. Many of the things renters believe about homebuying are myths.

Here’s the real deal.

While being in the less-than-20 club saves you up front, your lender may require a monthly fee called private mortgage insurance, or PMI. But you’ll start building equity sooner, and you can ask to stop it after you’ve accrued 20% equity in your home.

Saving 20% of the price of a home in many places isn’t just a challenge; it’s a roadblock. And it’s not a must-do. The typical down payment for first-time buyers is 8%, according to the National Association of REALTORS “Profile of Home Buyers & Sellers.”

How can you become part of the less-than-20 club?

• FHA loans: The Federal Housing Association is an old friend to first-time buyers and others ready to become homeowners with less than a 20% down payment. If you qualify, you may be able to get a loan with as little as 3.5% down if your credit score is at least 580.

• DownpaymentResource.com and NeighborWorks: Some local and state agencies sponsor downpayment assistance programs that help prospective

home buyers differently. Follow the links to find out if any are available near you.

• VA and USDA: Three government-related lenders offer mortgages with as little as zero down. The VA, which is for veterans and their family members, doesn’t require a down payment; however, lenders may require down payments for some borrowers using a VA loan. The USDA — for buyers in qualifying, typically rural, locations — doesn’t typically require a down payment.

• Gift funds: Twenty-three percent of buyers ask friends or relatives to help jump-start their home ownership with a gift. Talk to your lender first, though. They may limit the amount of gifted funds they’ll accept, and they may require your benefactor to sign some paperwork.

So, your credit could use a tune-up. That doesn’t mean you have to forgo your homebuying dreams. Here are some options for those with a less-than-stellar credit score.

• FHA loan: With a credit score of 500, you can apply for a FHA loan, but you’ll need a 10% down payment to offset the risk. Most lenders will require at least a 580 credit score coupled with the 3.5% down payment that is allowable on most FHA loans. This loan provides additional guideline flexibilities that

help people who might not meet conventional loan standards.

• A higher down payment: If you have enough cash to put down more than 20%, the higher down payment can help those with lower credit scores be less risky for lenders.

• A co-signer: Find someone with better credit to cosign the loan. But understand that if you don’t make the payments, the co-signer will be financially responsible. All applicants on a loan must understand their accountability to timely payments.

• Check your credit report: Maybe your credit isn’t that low. Order a copy of your report from all three reporting agencies (Equifax, TransUnion, and Experian). If you find inaccurate or old information, ask the agencies to correct it. (You can order a free report from each bureau once a year at annualcreditreport.com).

“Many lenders have access to credit analyzer tools,” says Nick Serrano, EVP of Omega Mortgage Group. “These can offer some short-term fixes to credit that can help accelerate people down the path to homeownership.”

Here are some facts. The free market sets broker commission costs within markets based on factors like service, consumer preference, and what the market can bear. Compensation between agents and their clients is always negotiable.

Remember that the seller’s agent works for the seller, not you. If you want a pro in your corner, you must contract with a buyer’s agent—money well spent.

There are many positive things to say about working with your local bank, but assuming they’ll give you the best mortgage is a mistake.

Banks are only one type of mortgage lender. Others include credit unions and mortgage companies.

Mortgage rates aren’t the same across the board, so contact several institutions to compare prices.

Or, if you prefer to let the lenders come to you, consider getting a loan through a mortgage broker. Brokers have access to several lenders, and they’ll shop their market, bringing you a more comprehensive selection of loans. But unless you contract with one, brokers aren’t obligated to find the best deal. So, you’ll want to shop around for a broker, just as you would for a lender.

“Independent Mortgage Banks, or IMBs, have garnered a tremendous amount of market share in recent years,” adds Nick Serrano. “This is because they can act as both a direct lender and broker, the best of both worlds. There are also companies wholly focused on home loans, so they have attracted dedicated mortgage professionals.”

Well, no. Don’t order that couch from West Elm or start packing just yet.

You don’t get the loan until:

1. The seller accepts your offer

2. Your lender approves the loan

3. You sign the loan papers

Between 1 and 2, the lender will have the home appraised to check that its value is in line with the purchase price, recheck your credit, and ask you for more documents than you ever knew existed.

So, what does preapproved mean for a loan? It tells sellers you’re eligible for a loan and shows them you’re a serious, qualified buyer. This gives them confidence in your offer... Read More By Scanning The QR Code Below.