13

13

To state the obvious, the COVID-19 health crisis was the dominant factor impacting the global economy and financial markets in 2020. A financial crisis looked possible in March when much was still unknown about the virus, but was averted by extremely strong action at the U.S. Federal Reserve (Fed). Fed policymakers reacted early in the pandemic by pushing short-term interest rates to zero, and began programs to purchase large amounts of U.S. Treasuries, agency mortgage-backed securities, corporate bonds, and other fixed income instruments. At the same time the Fed began a wide variety of additional lending facilities, many of which were unprecedented for the institution. Fiscal stimulus was also a significant aid for the economy and market sentiment in 2020, as was

optimism that successful vaccines would eventually be found, but the Federal Reserve did the most to instill confidence that the shock to the real economy brought about by COVID19 would not turn into a financial crisis. Once the Fed’s intentions became clear in late March the stock market began recovering, and spreads on corporate bonds fell considerably.

Remarkably, in spite of all the economic damage wrought by COVID-19, broad stock market indices ended 2020 with healthy gains: the S&P 500 Index rose 18.4%, the Russell 3000 Index (a broader measure of U.S. equities) was up 20.9%, and the MSCI All Country World Index returned 16.8%.

A few more words on 2020. There was some consternation in the

Equity Returns Last 12 months (normalized)

financial markets before the November election in the U.S., as many investors predicted that Democrats would sweep power in Washington, resulting in higher corporate tax rates. Ultimately, Republicans did well enough in Senate races to likely block significant changes to the tax code, and stocks rose once this became clear in early November.

Additionally, there was a subtle change in market sentiment in November once the first two potential vaccines proved to be effective at preventing serious complications from COVID-19. After these results were announced, technology and other “growth” sectors began to underperform the broader equity market, with more

Source: Bloomberg

cyclical and other “value” sectors outperforming. International and small cap stocks also outperformed broad equity indices in November and December. These moves reversed trends that had been ongoing for several years.

Investors face a series of questions as 2021 begins. The first and most fundamental is how long it will take for the health crisis to abate. The vaccine administration will be hugely complex, and the best estimate is that we won’t begin to see serious progress toward widespread inoculation until the summer, or possibly the fall. Given the large numbers of people who are likely to resist a vaccine, combined with the fact that it will take far longer to roll out vaccines throughout the rest of the world, it’s virtually certain that COVID-19 will remain a major factor in the financial markets throughout 2021 and, in all likelihood, for some years to come. Still, getting a large proportion of the populations of the U.S., Europe, and the rest of the developed world inoculated will do a lot to

slow the health crisis and should be a positive development for the world economy this year.

Another issue facing investors in 2021 is the pace of the economic recovery. This, of course, is inextricably linked to the health crisis and inoculation drive, as sustainable economic recovery will not be possible until infection rates fall. The best estimate today is for this to begin in the second half of 2021, with badly-hit sectors such as hospitality and travel beginning to see real recovery at that time.

An additional question for equity investors in 2021 is whether the current high valuations in the stock market will hold up (the S&P 500 is trading at 22.9X expected 2021 earnings). This type of short-term forecasting is very difficult, but it’s not unreasonable to believe that valuations will remain elevated as an abatement of the health crisis appears to be in sight, while the Federal Reserve continues to pursue broad and forceful stimulus measures.

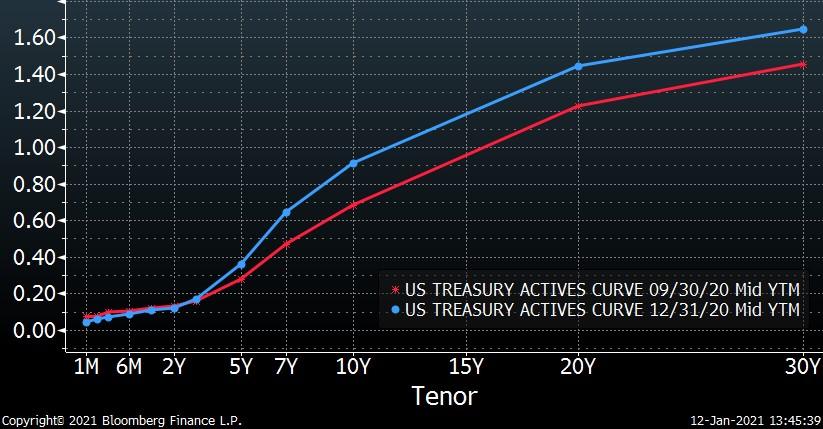

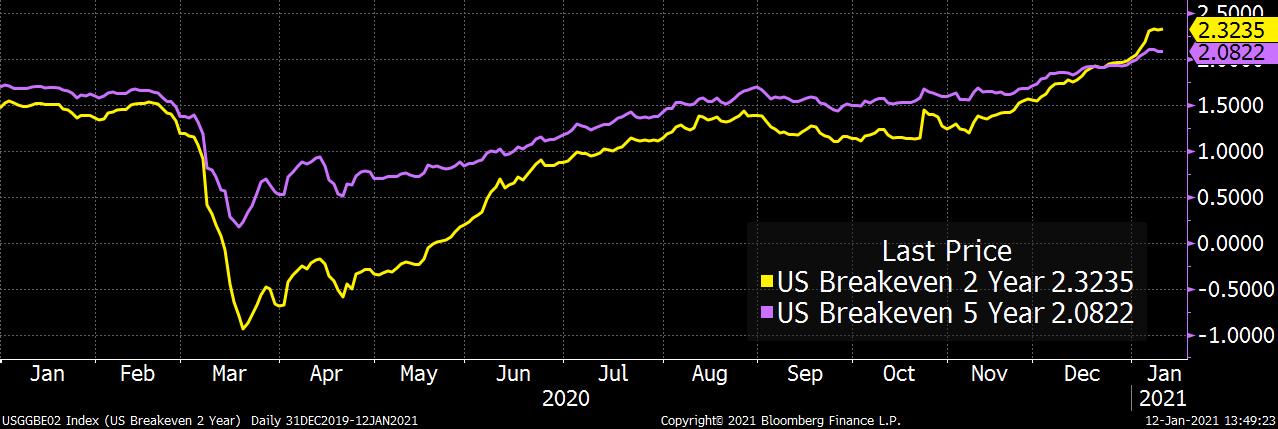

The U.S. Treasury yield curve steepened in the fourth quarter of 2020, with the yield of a 10-year Treasury bond up 26 basis points to 0.91% at year-end. The short end of the curve remained tethered close to zero, as Fed policymakers kept the fed funds rate at 0.0%. The two COVID-19 vaccines approved for emergency use in November buoyed investor confidence that a

stronger economic recovery will begin in earnest by the second half of 2021, and this helped push inflation breakeven rates significantly higher. The 2-year inflation breakeven rate was 2.01% at the end of December, as high as it’s been in almost three years and up dramatically from the negative figures seen last March.

As the vaccine rollout continues in the first half of 2021 and infection rates eventually begin to decline, there is likely to be pressure for long-term Treasury yields to move higher. If so, Federal Reserve policymakers will have a difficult decision to make, as most of the key Fed board members – including chair Jerome Powell – appear quite nervous regarding the long-term

impact of the health crisis on the real economy, and want interest rates to remain low. There was some discussion last year about implementing “yield curve control” – the explicit targeting of Treasury yields for specific maturities – though nothing official has been announced. Nonetheless, it’s clear that Fed policymakers are nervous about higher interest rates slowing the economy while the pandemic is still ongoing. Given this, we don’t believe the Fed will allow longterm Treasury yields to increase markedly from current levels for some time.

There was more activity than usual in the mortgagebacked security market in 2020, as significantly lower interest rates led to heightened prepayment speeds. Higher quality MBS – defined as those with underlying loans less likely to pay off – outperformed MBS with more generic collateral during the year. Interest

Source: Bloomberg

rates were a driving force of this dynamic, with the 30 -year mortgage rate reaching a record low of 2.66% in late December. We’re forecasting prepayment speeds to remain elevated during the first quarter as a fairly large percentage of home borrowers still have an incentive to prepay in today’s low interest rate environment. Significantly higher Treasury yields on the longer end of the curve would change the dynamic.

We remain cautious regarding credit in our fixed income portfolios, emphasizing high credit ratings and shorter maturities. Our MBS positioning in intermediate duration strategies is quite close to that of the Bloomberg Barclays U.S. MBS Index, though we are slightly up in coupon and underweight Ginnie Mae securities. Our short duration fixed income strategies hold mainly seasoned MBS, which have been per-

Source: Bloomberg

Source: Bloomberg

forming well in this period of heightened prepayment speeds.

Mortgage-backed securities are attractive today versus fixed income alternatives, as their yield-to-maturity compares favorably with Treasuries and high-rated corporate bonds, while their interest rate sensitivity today is quite low. And, of course, agency MBS do not have credit risk as corporate bonds do. We’ll be watching the duration of our MBS positioning closely in the first quarter of 2021, as any significant move higher of Treasury bond yields is likely to result in duration extension with MBS. Still, as the figures above indicate, much higher interest rates will be required for the U.S. MBS Index to approach the interest rate sensitivity of similar-yielding Treasury or corporate alternatives.

THIS PUBLICATION IS FOR INFORMATIONAL PURPOSES ONLY. THIS PUBLICATION IS IN NO WAY A SOLICITATION OR OFFER TO SELL SECURITIES OR INVESTMENT ADVISORY SERVICES, EXCEPT WHERE APPLICABLE, IN STATES WHERE DB FITZPATRICK IS REGISTERED OR WHERE AN EXEMPTION OR EXCLUSION FROM SUCH REGISTRATION EXISTS.

INFORMATION THROUGHOUT THIS PUBLICATION, WHETHER STOCK QUOTES, CHARTS, ARTICLES, OR ANY OTHER STATEMENT OR STATEMENTS REGARDING MARKET OR OTHER FINANCIAL INFORMATION, IS OBTAINED FROM SOURCES WHICH WE AND OUR SUPPLIERS BELIEVE RELIABLE, BUT WE DO NOT WARRANT OR GUARANTEE THE TIMELINESS OR ACCURACY OF THIS INFORMATION.

BLOOMBERG FINANCE L.P. IS THE SOURCE UTILIZED FOR GRAPHS THROUGHOUT THIS PUBLICATION. THE GRAPHS ARE USED WITH PERMISSION OF BLOOMBERG FINANCE L.P. NEITHER WE NOR OUR INFORMATION PROVIDERS SHALL BE LIABLE FOR ANY ERRORS OR INACCURACIES, REGARDLESS OF CAUSE, OR THE LACK OF TIMELINESS OF, OR FOR ANY DELAY OR INTERRUPTION IN THE TRANSMISSION THEREOF TO THE USER. THERE ARE NO WARRANTIES, EXPRESSED OR IMPLIED, AS TO ACCURACY, COMPLETENESS, OR RESULTS OBTAINED FROM ANY INFORMATION CONTAINED IN THIS PUBLICATION.

NOTHING IN THIS PUBLICATION SHOULD BE INTERPRETED TO STATE OR IMPLY THAT PAST RESULTS ARE AN INDICATION OF FUTURE PERFORMANCE.