January 13

January 13

The equity market proved resilient in 2025, with investor enthusiasm for artificial intelligence (AI) technologies overcoming worries about U.S protectionism and its impact on the global economy. There were hiccups along the way, but by year-end the global stock market had recorded another strong year, with the MSCI All Country World Index returning 22.9% and the S&P 500 (a measure of only U.S.-based stocks) returning 17.9%. Performance was varied but positive across almost all major sectors, with technology and industrials outperforming the broader market, while healthcare and consumer discretionary underperformed.

There are skeptics regarding the longterm economic impact of AI, but for now their doubts have been overshadowed by investor enthusiasm for the technology’s potential. Much of this enthusiasm has focused on chip manufacturers and their suppliers, which are clear early beneficiaries of the huge investments currently taking place in new AIrelated facilities. Investor sentiment suggests a belief

that runs deeper than hardware, however. The market appears to be forecasting that the widespread implementation of AI tools will enhance long-term corporate profitability across the entire economy. This remains a dynamic situation with both risks and opportunities that will play out in the months and perhaps years ahead.

A significant development in 2025 was a resurgence of international stocks after several years of underperformance vis-à-vis the U.S. market. The primary catalyst driving this outperformance was a general decline in the value of the U.S. dollar, which was down 12% compared to the euro during the year. This currency fluctuation greatly aided the dollarbased return of international stocks in

2025. For example, the MSCI EAFE Index (a measure of the developed world stock market excluding the United States and Canada) returned 16% last year valued in euros, a return comparable to the S&P 500 valued in dollars. The MSCI EAFE Index returned 32% when valued in U.S. dollars, which is the relevant figure for U.S.-based investors. It’s not clear whether this trend will continue but given the fairly uneven policy environment in the United States, we believe it makes sense for U.S.-based equity investors to diversify holdings with international stocks and domestic companies with significant operations abroad. We currently have international exposure in our equity portfolios and will continue to evaluate this issue.

Our equity portfolios are in a moderately defensive position, with an overweight to the healthcare sector and high-quality industrial names. We are underweight technology and have only one individual holding of the so -called “Magnificent Seven” technology stocks (Apple, Microsoft, Alphabet, Meta, Nvidia, Amazon and Telsa)

that have grown to comprise a large percentage of the entire S&P 500. AI may well turn out be a gamechanger for various parts of the economy, but we believe that these companies’ valuations are extended today and see better value elsewhere.

2025 was a rewarding year for the bond market. Attractive investmentgrade yields to begin the year combined with falling U.S. Treasury yields throughout the year drove strong performance. Also aiding bond returns last year, credit spreads and mortgage-backed security (MBS) option-adjusted spreads fell or stayed low despite risk caused by the implementation of new tariffs in the U.S. The Bloomberg U.S. Aggregate Index returned 7.3% in 2025, while the Bloomberg U.S. Mortgage-Backed Securities Index returned 8.6%. The Bloomberg U.S. Treasury 1-3 Year Bond Index returned 5.2%.

The short end of the U.S. Treasury yield curve saw the most movement in 2025, as Federal Reserve (Fed) policymakers lowered their key policy rate 75 basis points in the last four months of the year. Intermediateterm Treasury yields also fell, as bond investors reacted to lower shortterm yields and priced in the potential for an economic slowdown in 2026.

Interestingly, the 30-year Treasury bond yield rose a few basis points by year-end, signaling investor concern regarding long-term inflation.

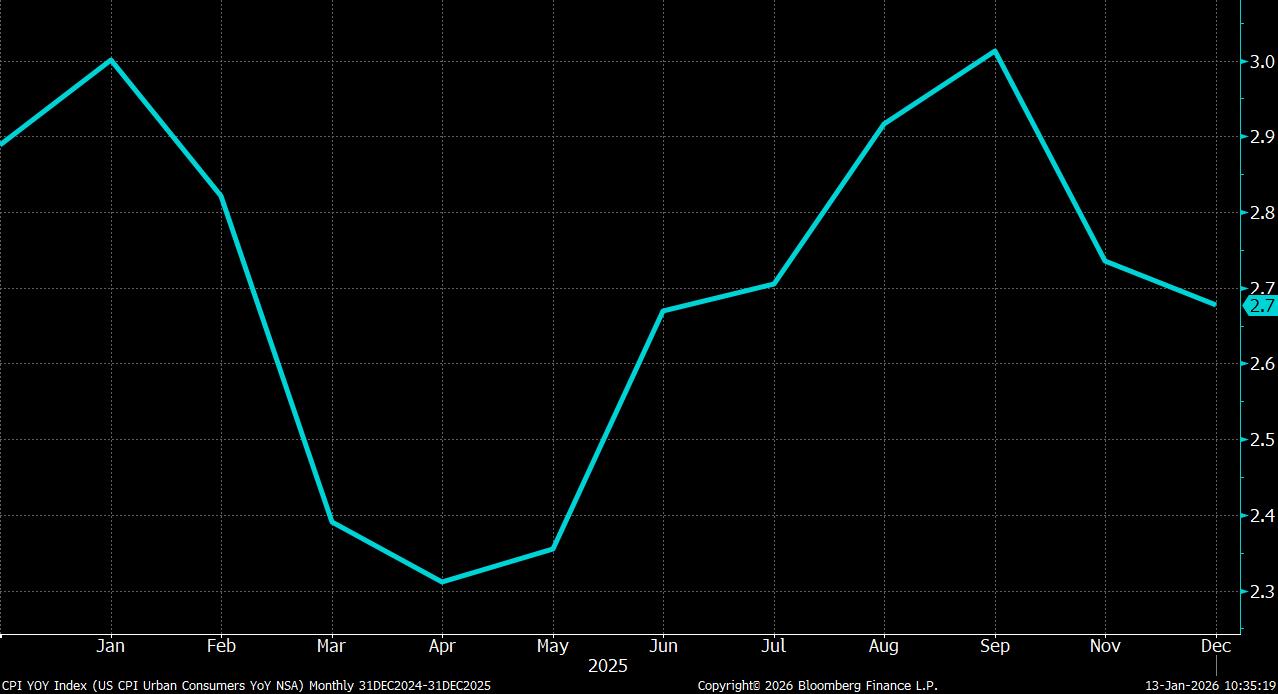

Inflation breakeven rates (what bond investors expect inflation to be going forward) have moderated in recent months towards the Fed’s long-term 2.0% target. Cooling expected nearterm inflation is welcome news for policymakers, but the Consumer Price Index remains elevated – 2.7% at its most recent reading – and the long-term fiscal trajectory of the United States government remains a concern. With this as a backdrop, bond investors will be watching closely in the coming months to see if monetary policymakers gradually relax their long-term inflation target of 2.0%. Such a relaxation would likely begin with a new inflation target “band” of 1.5% - 3.0% (a similar concept has already been floated by U.S. Treasury Secretary Scott Bessent), with movement toward the upper end of the band potentially accepted over

long periods. Such a development would be viewed negatively by the bond market, as many investors would see it as a presage of continued elevated inflation, potentially even beyond 3.0% over the long term. This scenario, of course, would present the most risk for long-term bonds which are especially sensitive to inflation and interest rates.

Credit spreads in the bond market remained low in 2025, buoyed by strong equity market returns during the year and a general “risk-on” sentiment throughout the financial markets. Credit spreads today are historically tight and are likely to be threatened if economic growth slows or if the stock market falters in 2026.

Mortgage-backed security optionadjusted spreads are also fairly low compared to historical averages, as dampened volatility in the bond market has aided the asset class.

As 2026 gets underway we have positioned most of our bond portfolios to

be moderately lower duration than their respective benchmarks. We see little relative value in the corporate bond market and instead favor Treasuries which offer better protection should the market’s current “risk-on” sentiment convert to “risk-off”. There remains good relative value in the MBS market, though investors now have to be more selective when choosing bonds within this asset class. We favor lower coupon MBS, which continue to have attractive spreads above Treasury bonds of similar duration despite their very low prepayment risk. These securities are more attractive than high coupon MBS, whose spreads have contracted considerably in recent months despite the high prepayment risk they would present in a falling interest rate environment.

12/31/2024

12/31/2025

Looking across the broader financial markets, there remains very good relative value in bonds. Stock market valuations are stretched with investors embracing the artificial intelligence theme (the S&P 500 is trading at 22.5x forecasted 2026 earnings), even as risks of general economic slowdown increase. Investment-grade bond yields, on the other hand, are attractive. The Bloomberg U.S. Aggregate

U.S. Treasury Yield Curve

Source: Bloomberg

Source: Bloomberg

Index, for example, has a yield-to-maturity of 4.3% today, while the Bloomberg MBS index is yielding 4.6%.

- Brandon Fitzpatrick, CFA

THIS PUBLICATION IS FOR INFORMATIONAL PURPOSES ONLY. THIS PUBLICATION IS IN NO WAY A SOLICITATION OR OFFER TO SELL SECURITIES OR INVESTMENT ADVISORY SERVICES, EXCEPT WHERE APPLICABLE, IN STATES WHERE DB FITZPATRICK IS REGISTERED OR WHERE AN EXEMPTION OR EXCLUSION FROM SUCH REGISTRATION EXISTS.

INFORMATION THROUGHOUT THIS PUBLICATION, WHETHER STOCK QUOTES, CHARTS, ARTICLES, OR ANY OTHER STATEMENT OR STATEMENTS REGARDING MARKET OR OTHER FINANCIAL INFORMATION, IS OBTAINED FROM SOURCES WHICH WE AND OUR SUPPLIERS BELIEVE RELIABLE, BUT WE DO NOT WARRANT OR GUARANTEE THE TIMELINESS OR ACCURACY OF THIS INFORMATION. BLOOMBERG FINANCE L.P. IS THE SOURCE UTILIZED FOR GRAPHS THROUGHOUT THIS PUBLICATION. THE GRAPHS ARE USED WITH PERMISSION OF BLOOMBERG FINANCE L.P. NEITHER WE NOR OUR INFORMATION PROVIDERS SHALL BE LIABLE FOR ANY ERRORS OR INACCURACIES, REGARDLESS OF CAUSE, OR THE LACK OF TIMELINESS OF, OR FOR ANY DELAY OR INTERRUPTION IN THE TRANSMISSION THEREOF TO THE USER. THERE ARE NO WARRANTIES, EXPRESSED OR IMPLIED, AS TO ACCURACY, COMPLETENESS, OR RESULTS OBTAINED FROM ANY INFORMATION CONTAINED IN THIS PUBLICATION.

NOTHING IN THIS PUBLICATION SHOULD BE INTERPRETED TO STATE OR IMPLY THAT PAST RESULTS ARE AN INDICATION OF FUTURE PERFORMANCE.