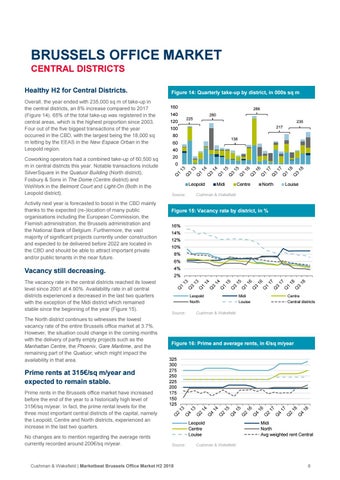

BRUSSELS OFFICE MARKET CENTRAL DISTRICTS Healthy H2 for Central Districts. Overall, the year ended with 235,000 sq m of take-up in the central districts, an 8% increase compared to 2017 (Figure 14). 65% of the total take-up was registered in the central areas, which is the highest proportion since 2003. Four out of the five biggest transactions of the year occurred in the CBD, with the largest being the 18,000 sq m letting by the EEAS in the New Espace Orban in the Leopold region. Coworking operators had a combined take-up of 60,500 sq m in central districts this year. Notable transactions include SilverSquare in the Quatuor Building (North district), Fosbury & Sons in The Dome (Centre district) and WeWork in the Belmont Court and Light-On (Both in the Leopold district). Activity next year is forecasted to boost in the CBD mainly thanks to the expected (re-)location of many public organisations including the European Commission, the Flemish administration, the Brussels administration and the National Bank of Belgium. Furthermore, the vast majority of significant projects currently under construction and expected to be delivered before 2022 are located in the CBD and should be able to attract important private and/or public tenants in the near future.

Figure 14: Quarterly take-up by district, in 000s sq m 160 120

The North district continues to witnesses the lowest vacancy rate of the entire Brussels office market at 3.7%. However, the situation could change in the coming months with the delivery of partly empty projects such as the Manhattan Centre, the Phoenix, Gare Maritime, and the remaining part of the Quatuor, which might impact the availability in that area.

Prime rents at 315€/sq m/year and expected to remain stable. Prime rents in the Brussels office market have increased before the end of the year to a historically high level of 315€/sq m/year. In fact, the prime rental levels for the three most important central districts of the capital, namely the Leopold, Centre and North districts, experienced an increase in the last two quarters. No changes are to mention regarding the average rents currently recorded around 200€/sq m/year.

280 225

235 217

100 80

138

60 40 20 0

Leopold Source:

Midi

Centre

North

Louise

Cushman & Wakefield

Figure 15: Vacancy rate by district, in % 16% 14% 12% 10% 8% 6% 4%

Vacancy still decreasing. The vacancy rate in the central districts reached its lowest level since 2001 at 4.90%. Availability rate in all central districts experienced a decreased in the last two quarters with the exception of the Midi district which remained stable since the beginning of the year (Figure 15).

286

140

2%

Leopold North Source:

Midi Louise

Centre Central districts

Cushman & Wakefield

Figure 16: Prime and average rents, in €/sq m/year 325 300 275 250 225 200 175 150 125

Leopold Centre Louise Source:

Cushman & Wakefield | Marketbeat Brussels Office Market H2 2018

Midi North Avg weighted rent Central

Cushman & Wakefield

8