FREQUENTLY ASKED QUESTIONS MEET THE TEAM YEAR-END CHECKLIST TAX HARVESTING TIME 18 AGGRESSIVE INVESTING

C O N T E N T S 04 07 LETTER FROM THE CEO & COO 09 10 12 13 17 CLIENT WORKSHOPS

www.compasscapitalmgt.com

918-423-3222

215 E Choctaw Suite 101 McAlester, OK 74501

Welcome to the bi-annual issue of COMPASS Magazine, an official publication of Compass Capital Management, LLC.

Fall is in the air and thus comes a time of rest and reflection as we Fall Into Focus on our financial journey. Through this Fall issue of COMPASS Magazine, we hope you’ll feel inspired by the accumulation of articles to help educate you on your financial journey.

In this issue, you will find a range of articles designed to inform and inspire: Retirement Planning Making your Portfolio Tax Efficient End of the Year Financial Checklist Schedule of client events, workshops and more!

We hope you continue to find valuable resources and inspiration through these pages. Our team is ready to help you find financial growth and security as we reach the end of this year and help you Fall Into Focus for the year ahead.

We want to take a moment to express our heartfelt appreciation for the trust and confidence you continue to place in our firm. It is truly a privilege to walk alongside you in your financial journey. Every decision we make is guided by our commitment to helping you live with greater financial clarity and peace of mind

Over the past several months, we've seen continued changes in the retirement landscape rising healthcare costs, market shifts, and legislative updates all of which make strategic planning more important than ever With that in mind, we'd like to share a couple of key focus areas we believe are essential as we head into the remainder of the year

If you're approaching retirement or already collecting benefits, it's a great time to revisit your Social Security strategy. Recent cost-of-living adjustments and filing age considerations may open new opportunities to optimize lifetime benefits. We're here to help you assess your options and align them with your long-term income needs.

Additionally, as you transition from saving to spending, ensuring your retirement income is sustainable and tax-efficient becomes critical We encourage you to review your withdrawal strategy with us especially in light of recent changes in required minimum distributions (RMDs) and market performance The goal is always to protect your lifestyle while reducing unnecessary tax burdens

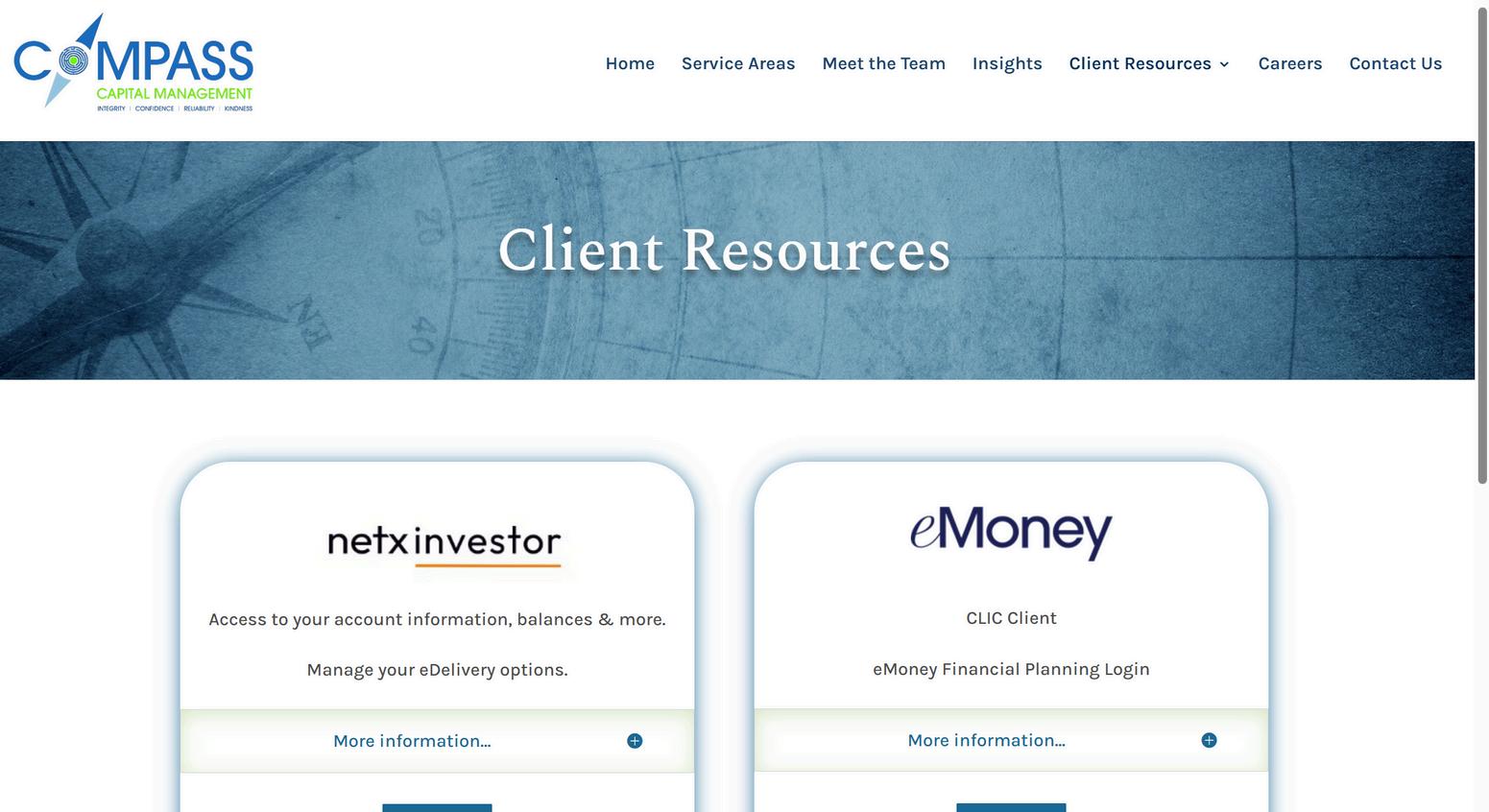

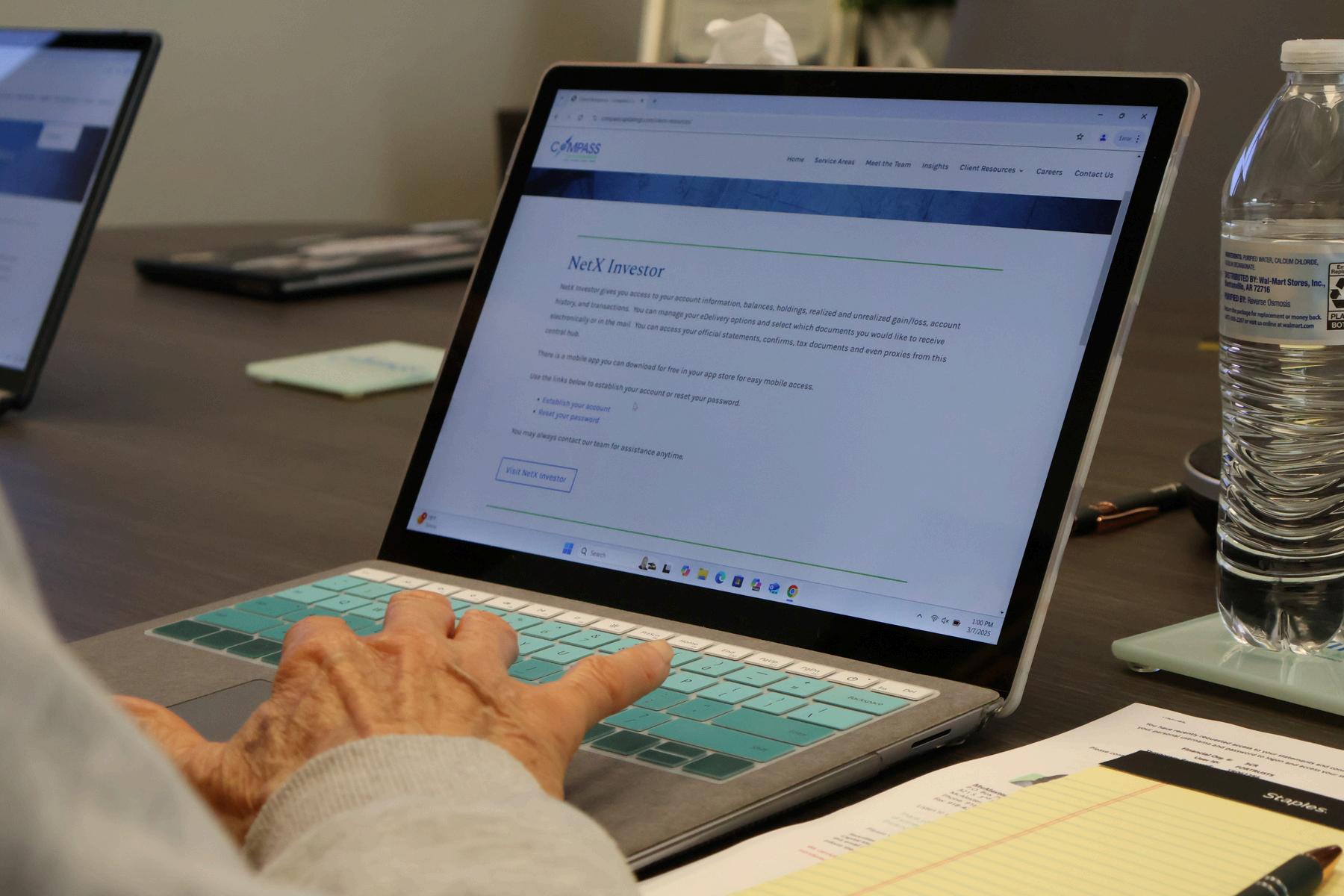

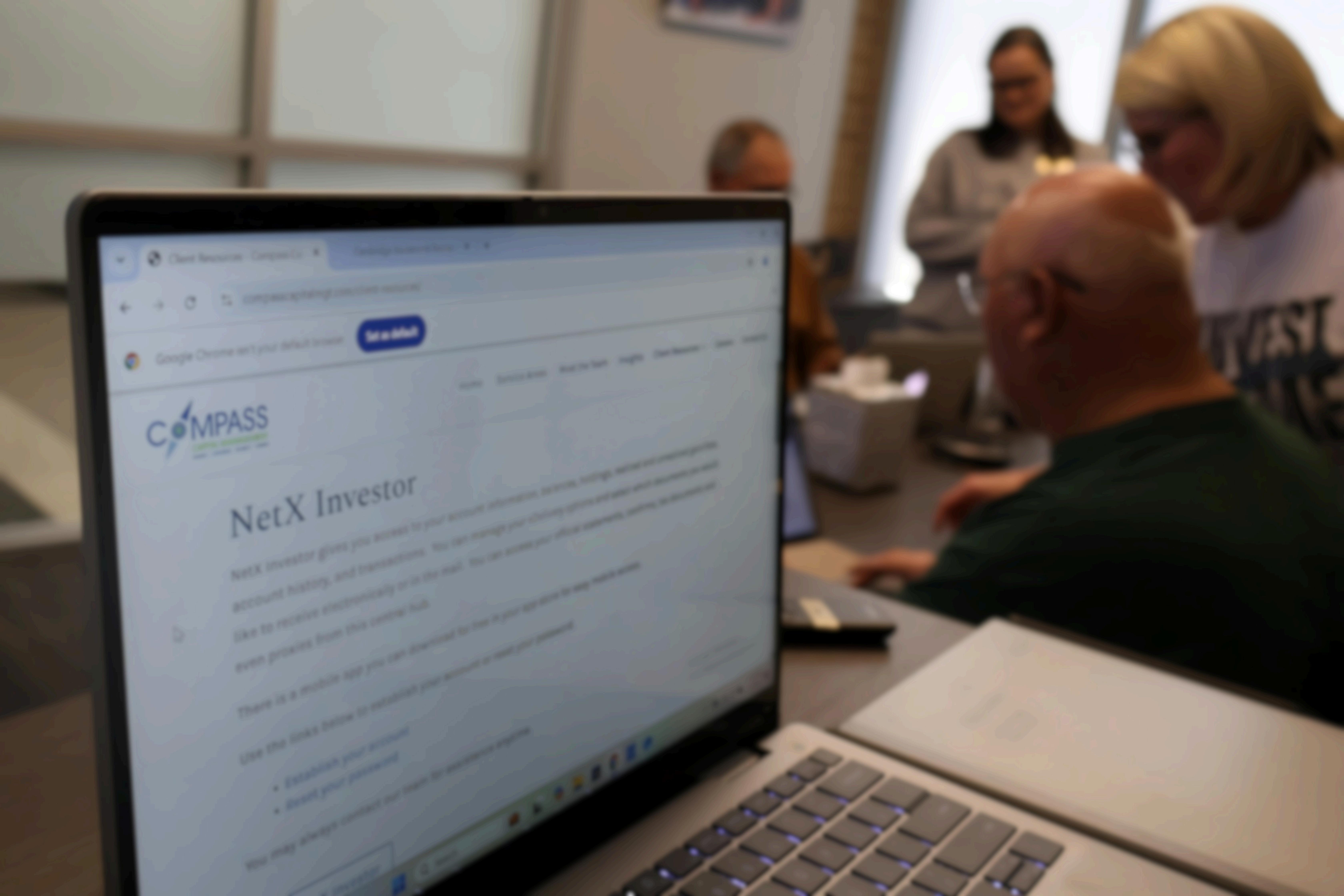

Finally, we hope you have had time to check out the resources available to you via our website, our client education events, and the software we have available to help you stay on track with your financial goals We will continue to offer workshops each quarter to teach you about navigating and understanding how to utilize NetXinvestor and CLIC Client access We remain committed to providing personalized guidance that’s proactive, not reactive We are continuing to schedule reviews throughout the remainder of this year, and we look forward to collaborating with you to ensure your plan stays on track

On behalf of the entire team at Compass Capital Management, LLC thank you again for the opportunity to serve you Your financial future is our shared mission, and we’re honored to be part of it.

Jimmy J. Williams CEO

LeAnn Lewis COO

*Find the answer key on page 21!*

sodacan

breifcase

Sam is our Client Relationship Manager. He provides financial planning and relationship management to the firm’s small to mid-size clients. Sam obtained his Bachelors in Psychology at Southwestern College in Winfield, athlete in tennis. He is currently obtaining his MBA with a concentration in Management Information Systems at Fort Hays State University. When Sam is not working, he enjoys spending time with his wife, Erin, and their son, Theodore. His family is growing as they’re expecting another baby due in October!

My first few months at Compass Capital Management have been incredibly insightful. I've gained valuable experience in meeting clients where they are and helping them work toward their financial goals. Each day, I grow more confident in my role as I take on new responsibilities, apply what I’ve learned, and witness the positive impact of our work with clients One of the most rewarding aspects so far has been building relationships with our clients, especially during our social events. I’m excited for what’s ahead!

training as a student the children's department at Dream Kansas while

In his spare time, Sam enjoys Pickleball,

drumming, the outdoors and serving in

City Church of McAlester.

Gettoknow Sam DeNike

RetirementIntentionalityRequires

No one successfully retires by simply waking up one day and saying, “I am going to retire today. ”My statement is not correct. There are a select few of the people on the planet who have the means to

simply walk away from their career and live life on their own terms without planning to do so. However, my argument would be that these few people planned for retirement in the way they led their career paths to a certain pinnacle that would avail to them the opportunity to make these types of spontaneous choices.

For the rest of us, it is critical that we are intentional in the process of planning for the future. We do not know how much time we will get in the retirement phase of life. Recently, a dear friend of mine that is at the door to retirement received some very disturbing news about his health. Mortality is being evasive but could be as long as a year or two. This type of medical news changes the landscape for retirement. Intentionality has become more necessary and important for his family since this terrible news arrived.

Planning for the distinct phases of life requires deliberate action. This is the time to begin the process of thinking about your children’s education, your career path, your retirement desire outcomes and, ultimately, the disposition of your wealth to those people and charities you wish to leave it. It sounds odd to say someone in their 20’s should be thinking about retirement. However, the earlier one starts on saving for the future, the greater probability of success in reaching the goal. For example, if you are 25 years of age and starting your first career position, it would be wise to consider the amount of funds you may defer from your pay to a retirement plan for the future. If you were to save the amount of funds necessary to meet your employer’s maximum matching percentage, your funds would grow despite the market conditions. Compound the amount of your contributions and employer matching contributions to your retirement account for a period of forty years and you will be prepared for a good retirement outcome.

The challenge in being intentional is behavioral stimuli. That is a fancy word to simply say, “life happens.” Most people do not plan on a catastrophic event (i.e., loss of job, home lost to fire, death in the family, etc.) and these activities can derail the most disciplined of planners. By collaborating with a CERTIFIED FINANCIAL PLANNER™ practitioner, your future can be designed in a manner that accommodates these challenges of life.

Working with a planner does not ensure your future outcomes will be met but it does give you the insight and foresight to plan for contingencies that you may not realize. What if you were intentional in saving a sum of funds to meet your lifestyle needs for a year and you never needed the funds? Now, you have an option of taking that year of vacation prior to retiring and doing so with you controlling your destiny.

You are intentional in selecting your spouse for a lifetime of enjoyment. It is true that you should use such an approach to your finances. Treat your contributions to your employer provided retirement plan as if it were a mortgage on your future. You should have the confidence and comfort to enjoy life on your own terms. No one knows how much time we may be given so it is vital that you maximize your enjoyment each day. Seek out a complimentary consultation with a CERTIFIED FINANCIAL PLANNER™ professional. A plan for your future may just be what you need to build your confidence for a wonderful retirement.

Another of my favorite philosophies of life was authored by Friedrich Nietzsche, “The future influences the present just as much as the past.”

It’s harvest season again … not crops from the field, rather tax harvest time for investors. Before the end of the year, investors with non-qualified accounts should be totaling their realized gains for the year to date with an eye toward offsetting those gains by selling assets in which they have losses.

Tax efficiency should be an integral part of any investor’s strategy. By making tax-wise moves and reducing potential capital gains and ordinary income taxes the investor can often add a few percentage points to the overall returns performance of the portfolio In a time when markets are giving single digit returns, a point here or a point there can add up to real money.

There are a variety of techniques that can be used to make a portfolio tax efficient. Perhaps the most effective is tax-loss harvesting. Essentially, this means selling securities to realize a capital loss, using the loss to offset realized gains.

Unrealized gains that exist on paper only are not taxable until realized, or sold. Realized gains and losses result from selling activity for individual securities, but they also come from realized gain distributions from mutual funds The latter can catch the unwary by surprise.

Mutual funds are required to distribute 90% of their realized gains during the year.

Even if this distribution is reinvested into the mutual fund in the form of additional share purchases, it counts as a realized gain and is taxable. That’s the bad news, the good news is that this adds to the cost basis so when the fund is eventually redeemed, the increased cost basis minimized the final gain on the sale

In cases where the investor does not have a realized capital gain but does have losses in a portfolio, the tax code allows a $3,000 deduction in capital losses to be deducted from ordinary income each year. That’s worth a possible $1,050 (35%) federal and/or state tax savings. Losses in excess of the $3,000 may be carried forward indefinitely an important planning tool for future portfolio strategy moves

Some investors are reluctant to sell a losing position for any number of reasons. They are free

to buy it back … providing they wait 31 days

from the date of sale to do so. Otherwise they run afoul of the wash sale rule, which states if the asset sold is replaced by the identical position, either within 31 days before or after the date of sale, the tax loss is voided

Since we are only in September it is still possible to double up a losing position by buying before the sale to count for this year as a loss Therefore if we were to reacquire the position after the sale we would have to wait until January. But if this leaves the portfolio uncovered in a particular sector or industry, the investor could consider replacing it in the portfolio with a like company, Procter & Gamble® for Gillette® for example.

Another solution is to use ETFs, or exchange traded funds, to fill the void. Selling a losing emerging-market stock or fund could be replaced by the emerging market’s ETF, EEM. Also, losing ETF positions can be treated as any other security for purposes of loss recognition.

If a losing position has been acquired at different times and at different costs, partial positions may be sold to take advantage of the differing costs If the portfolio needs more losses … sell the tax lot with the greatest loss, or the highest gain, if the reverse is true.

Finally, if the investor does annual gifting to charitable organizations, more tax benefits come from gifting highly appreciated stock, verses selling the stock, being taxed on the gain and gifting cash

If the stock is a losing position and earmarked for a gift, sell it first, take the loss and give the cash.

Executive Assistant / Client Service Associate ANNA AMOS

MADDIE COOPER CEO / President JIMMY WILLIAMS Co-Owner

M EE T OU R T E A M

CHECKLIST YEAR-END FINANCIAL PLAN

Income Tax Planning

Harvest capital losses to offset any realized gains or rebalance taxable investment accounts.

Consider harvesting any capital gains that can be realized in the 0% tax bracket.

Review charitable contributions to maximize income tax deductions

Consider donation of appreciated assets that have been held for more than one year, rather than cash

Opening and funding a Donor Advised Fund (DAF) as it allows for a tax-deductible gift in the current year and also the client’s ability to dole out those funds to charities over multiple years.

Qualified Charitable Distributions (QCDs) are another option for those over 70 5 and especially for those who don’t typically itemize on their tax returns When reviewing charitable contribution decisions, consider bunching the contributions to exceed the standard deduction.

Maximize contributions to a retirement plan, SEP IRA (self-employed) and Health Savings Accounts

If a beneficiary of an applicable inherited IRA, take any required distributions before end of 2025.

If income is expected to increase in the future, consider making Roth 401(k) contributions.

Evaluate income as related to tax brackets and net income tax (NIIT) and consider options to lower bracket and NIIT before year end

Weigh the benefits of converting Traditional IRA to a Roth IRA to lock in lower tax rates on some pre-tax retirement accounts.

Remember that Roth Conversions can no longer be recharacterized so there’s no reversing once executed.

Keep in mind that Roth conversions will be more beneficial when the tax can be paid by funds outside of the IRA.

Remember that all IRA balances are included in the tax calculation of the conversion limiting the ability to only convert after-tax amounts.

Review income tax withholding on retirement account distributions or wages and recommend any needed changes for the new year

Review the timing of income and deductions such as payments for tuition.

Consider any changes that may be needed in tax planning due to the 2025 One Big Beautiful Bill Act

Review any changes in income that may result in a client paying IRMAA (incomerelated monthly adjustment amount) increasing their Medicare premiums. Consider ways to reduce income over the IRMAA.

CHECKLIST YEAR-END FINANCIAL PLAN

Estate & Gift Planning

Make use of annual exclusion gifts ($19,000 per donee, $38,000 per married couple )

Capitalize on the unlimited gift exemption for direct payment of tuition and medical expenses.

Consider gifting to a 529 plan by year-end if saving for a child's or grandchild's education.

Many states offer tax deductions for residents contributing to their state programs.

Consider gifting up to 5 years of the annual exclusion amount to an individual’s 529 plan and filing a gift tax return, electing to treat it as if it were made evenly over a 5-year period

Review your assets to determine if each asset should be held in your name or your revocable trust.

Confirm wills, trusts, and power of attorneys are up-to-date and consistent with current plans

Review lifetime gift and GST gifting opportunities to use additional applicable exclusion and exemption amounts.

Consider any changes that may be needed for the estate and gift planning if the 2017 Tax Cuts and Jobs Act provisions expire at the end of 2025.

Retirement, Investments & Other Planning

Are there any major life changes such as marriages or divorces, births or deaths in the family, job or employment changes, changes in residency, and significant planned expenditures (real estate purchases, college tuition payments, etc.)?

Are pre-tax and Roth contribution amounts to retirement accounts for 2026 updated and accurate?

Review various insurance policies and confirm whether the amount of coverage and deductibles are still adequate.

Review beneficiary designations and update, as necessary.

Confirm that Flexible Spending Account balances have been spent or there is a plan to spend the entire balance and set 2026 contribution amounts.

Review the investment portfolio and target asset allocation Confirm whether the allocation is within the targeted ranges for each asset class as recent market performance could have caused allocations to drift dramatically.

Review any scheduled 4th quarter estimated tax payment needs and assess any liquidity for payments.

Consider an additional tax payment or increase in tax withholdings to eliminate a penalty or changes in a tax situation for 2025.

Evaluate progress towards financial goals and review goals for 2026 and any changes in long term goals

Review your credit report to identify any concerns.

Make the Most of Your Resources

Learn How To Navigate & Implement Net X Investor & CLIC Client Resources

As you know, most people invest in the stock market as a way to save for retirement, secure additional income, or create financial security for

themselves and their families. They want to “put their money to work” as the saying goes. This is a healthy mindset, and for most people, it’s the whole point of investing

But “most people” isn’t everybody Anyone who works in the financial industry knows there exists a special type of investor This type wants more than simple financial security They want to do more with their money than save for retirement.

“aggressive investor.” “aggressive investor.”

We’ll call this type an Aggressive investors are more akin to the prospectors of yore the kind of prospector who says, “There’s gold in them hills” and aims to find it To put it simply, aggressive investors want to take a shot at higher returns, even if it means taking on a bit more risk to do it.

To be clear, aggressive investing does not equate to gambling It doesn’t mean abandoning basic investment principles, like supply and demand or relative strength. Aggressive investing is for people who enjoy watching and participating in the stock market It’s for people who want to apply those principles for a chance at a home run hit instead of a lifetime full of singles.

In short, aggressive investing isn’t about risking your entire portfolio It’s about risking a part of it because you can afford to.

That’s the key phrase. All investing comes with some risk, of course, but as a financial advisor, part of the job is to make sure clients never take on more risk than they can afford or feel comfortable with.

Some clients take on very little risk, and yet still make what they need to reach their financial goals

Other clients take on a lot more risk, because they can afford to, it doesn’t bother them, and because their particular goals demand it.

If you feel you’re an aggressive investor or if you want to be one then it’s time to discuss adopting a more aggressive strategy

What does an aggressive investment strategy look like?

The answer: a lot like our current strategy We just take it one step further. Here’s how it works. As you know, our current strategy involves asking the following questions:

Should we be investing in the markets at all? We only invest if conditions warrant it. Otherwise, we stay in cash to protect against losses.

If yes, which markets should we be in? The media likes to refer to “the markets” as a single homogenous entity, but there are many different markets, all specializing in different things or weighted in certain ways When it’s time to invest, we only want to participate in the strongest possible market(s)

Instead of focusing solely on sectors via ETF aggressive investing looks at individual stocks

Instead of focusing solely on sectors via ETF aggressive investing looks at individual stocks

Again, we apply relative strength to the quest Which stocks are strongest relative to other st sector? For example, if we decide sector, and determine Apple looks like a stock than Googl Apple is what we’ll buy

Again, we apply relative strength to the quest Which stocks are strongest relative to other st within their sector? For example, if we decide invest in the technology sector, and determine Apple looks like a stronger stock than Googl Apple is what we’ll buy.

This strategy does involve more risk, because concentrating more money into fewer stocks rather than using ETFs to spread it across dif sectors. But it also gives us a better chance at returns if the stocks we select continue to rise value.

This strategy does involve more risk, because concentrating more money using ETFs to spread across dif sectors. But it also us a better chance at returns if the stocks we select continue to rise value

For aggressive investors, we add the following question:

So ask yourself: “Do I want to achieve higher or am I comfortable with how things are? Do financial goals cost a lot more than I currentl or am I already on track to achieve them? Am with taking on more risk, or do I prefer to be more conservative?”

So ask yourself: “Do I want to achieve higher or am I things are? Do goals cost a more I or am I already on track to achieve them? Am with taking on more risk, or do I prefer to be more conservative?”

“Am I an aggressive investor?”

“Am I an aggressive investor?”

If the answer is , or even MAYBE, the what I propose. Give us a call at (918) 423-32

Let’s take a few minutes to discuss whether a aggressive strategy is right for you. It’s possib we’ll decide that it’s better to keep the status q isn’t a potential home run worth a few minute phone?

If the answer is , or even MAYBE, the what propose. Give us a call at (918) 423-32 Let’s take a few minutes to discuss whether a aggressive strategy is right for you It’s possib we’ll decide that it’s better to keep the status q isn’t a potential run a phone?

If so, let’s talk. Give our office a call today!

If so, let’s talk. Give our office a call today!

CHECK OUT CHECK OUT CHECK OUT

OUR

YOUTUBE COMPASSCAPITAL MANAGEMENTLLC

SOCIALS

OUR SOCIALS OUR

SOCIALS

INSTAGRAM @COMPASSCAPITALMGT

FACEBOOK

COMPASS CAPITAL MANAGEMENT, LLC

LIKE & FOLLOW OUR SOCIALS FOR EXCLUSIVE CONTENT, UPDATES, BEHING THE SCENES, AND ALL THINGS CCM! WE CAN’T WAIT TO CONNECT WITH YOU!

THANKS F A ! - TH F LAYIN

N FOR PL

Answer Key

FOR PLAYIN

CLIENT

BEHIND THE LENS

A LOOK INTO COMPASS CAPITAL MANAGEMENT’S MARKETING TEAM

OUR MARKETING TEAM

specializes in client appreciation This team works diligently to curate and provide client resources and information in an accessible way While also coordinating with other teams in the office, they take lead in directing community involvement and sponsorships

Alexandria Williams, MA, is our Marketing Director She specializes in digital marketing ranging from photography, videography, social media and graphic design She is a proud graduate of the University of Oklahoma and University of Missouri

Maddie Cooper is our Marketing Assistant She is responsible for assisting our Marketing Director in content creation, graphic design, social media, etc

Working at CCM has been such a great experience. Over the past months, this team has helped me grow in more ways than I could have imagined

Collaborating with Alex has given me a new perspective from my previous marketing experience It is so much fun to see all the moving parts come together to create a big picture

-Maddie Cooper

WHEN LIFE CHANGES SUDDENLY, THE RIGHT GUIDANCE matters

Significant Health Decline Divorce Death

In moments like these, financial decisions can be overwhelming.

As a trusted financial planning firm, we help families navigate these challenging transitions with clarity, compassion, and confidence.

If you know someone facing sudden loss or unexpected changes in their family, please connect them with us.

Your referral could give them the peace of mind and financial security they need during one of life’s most difficult times.

SCAN FOR MORE RESOURCES AND TO EXPLORE OUR WEBSITE