Against the ongoing soundtrack of protesters loudly chanting “Freeze the Rent! Freeze the Rent!” New York City’s Rent Guidelines Board (RGB) voted June 30 to raise the rent on rent-stabilized apartments by 3 percent for oneyear leases and 4.5 percent for two-year leases.

The debate before the vote, which passed 5-4, contained pointed positions from both sides of the issue.

“Inflation is 4 percent. It should be the starting point for a discussion on one-year leases,” said board member Christina Smyth, who voted against the current raises.

“This board does not value affordability,” countered board member Adán Soltren, who noted that the board had now raised rents 12 percent in total over the last four years, and who also voted against the raises. “There is no way we can come to these decisions four times in a row if we did.”

This latest annual vote likely had more eyes on it than ever before given the prominence of rents as an issue in this year’s mayoral race.

New York State Assemblyman Zohran Mamdani, the Democratic nominee for mayor, famously made freezing rents for the roughly 2 million New Yorkers living in rent-stabilized apartments a key element of his campaign.

Mamdani’s official platform references the incumbent mayor, who is on the November ballot as an independent: “Eric Adams has taken every opportunity to squeeze tenants, with his handpicked appointees to the Rent Guidelines Board jacking up rents on stabilized apartments by 9 percent (and counting) — the most since a Republican ran City Hall. As mayor, Zohran will immediately freeze the rent for all stabilized tenants, and use every available resource to build the housing New Yorkers need and bring down the rent.”

Adams had called for the board to “adopt the lowest increase possible while protecting the quality of housing for millions of New Yorkers” in a statement released on the morning of the vote.

While expounding on the massive rent expense facing so many New Yorkers, Adams, without mentioning his opponent’s name, also took Mamdani to

task for his rent-freeze stance. “Let’s be clear,” Adams wrote, “demands to ‘freeze the rent’ are shortsighted and risk worsening already deteriorating housing conditions — putting tenants’ health and safety in harm’s way.”

Kenny Burgos, CEO of landlord group the New York Apartment Association, agreed.

“Every year the Rent Guidelines Board is put in a horrible position because elected officials do nothing to lower the cost of housing,” Burgos said in a statement. “While we are disappointed that the RGB once again adjusted rents below inflation, we appreciate that they stood

up to political pressure calling for rent freezes that would accelerate the financial and physical deterioration of thousands of older rent-stabilized buildings.”

for hotel-related housing, including SROs and lodging or rooming houses.

Manhattan Office Notches Busiest Half-Year Since 2014

Manhattan’s office market recorded its strongest six months of demand since 2014 during the first half of 2025, despite a decline in leasing activity in the second quarter.

Leasing activity during the quarter slid by 18.9 percent from the previous three months, to 9.23 million square feet, according to numbers last week from Colliers. However, second-quarter leasing activity was still 28 percent above the five-year quarterly average of 7.21 million square feet and 13.9 percent higher than the 10-year average of 8.11 million square feet.

The quarter-over-quarter decline can be attributed to an unusually active first quarter, Franklin Wallach, executive managing director of research and business development for Colliers in New York, told Commercial Observer. Tenants leased 11.4 million square feet in the first quarter of the year.

“Was [the dip] a major surprise? No,” Wallach said. “Because it was such a number to beat from Q1. So that was a very tall order to repeat.”

Overall, the activity in the second quarter highlighted a healthy market with strong demand.

“If you took just the Q2 leasing by itself, which was over 9 million square feet, is that a healthy quarter of activity? Sure is. It beat the five-year average,” Wallach continued. “The overall Manhattan market over the last 25 years averages out around 8 to 8.5 million square feet of leasing per quarter. That’s the typical quarterly Manhattan average over the last quarter century. This was over 9 million square feet. That’s a solid quarter.”

Some of the second quarter’s largest transactions were the 1.08 million-square-foot lease at 770 Broadway by New York University, Amazon taking 330,000 square feet at 10 Bryant Park, and law firm Goodwin Procter inking a 250,000-square-foot lease at 200 Fifth Avenue

Manhattan leasing activity for the first half of the year totaled 20.63 million square feet, a rise of 42.2 percent compared to the same six-month period in 2024. If demand continues at this pace for the rest of 2025, Colliers predicts that full-year leasing could hit 41.26 million square feet, surpassing 2024’s total by 23.7 percent. —Amanda Schiavo

The board also voted for no increases

—Larry Getlen

WHAT THEY SIGNED UP FOR: Zohran Mamdani supporters have rallied behind halting rent hikes.

TUT, TUT, HIKE!

SOARING: Office leasing volume was up 42.2 percent annually.

99TH ANNIVERSARY GALA

We Celebrate the Leading Brokerage Firms Who Have Continued to Shape & Sustain the Avenue of the Americas

NEW YORK MARRIOTT MARQUIS 1535 Broadway, New York, NY 10036 Honoring

THURSDAY, OCTOBER 16, 2025 6:00 PM

Related’s Hudson Yards Expansion Has a Financing Plan

Three weeks after the New York City Council approved necessary zoning changes for Related Companies’ Hudson Yards housing proposal, lawmakers greenlighted a financing structure for a key component of the 4,000-unit development.

The City Council early last week unanimously passed a payment-in-lieu-of-taxes (PILOT) model to fund a $2 billion platform to be built over the Western Rail Yards for Related’s large-scale project consisting of four mixed-use towers.

“This is a historic moment for New York City, and this complex and transformational project would not be moving forward without the strong support and collaboration we’ve had from our city leaders on both sides of City Hall,” Jeff Blau, CEO of Related Companies, said in a statement.

Related’s Hudson Yards project will designate 625 of the 4,000 apartments as affordable housing. The development will also include a 2.4 million-square-foot office tower, a hotel, a new public elementary school and 6.6 acres of public green space.

The council’s zoning approval on June 11 came on the heels of Related striking an agreement with Mayor Eric Adams to boost the number of affordable housing units by 139. Related and Oxford Properties previously planned a casino development at Hudson Yards with Wynn Resorts before the gambling operator pulled out on May 19, citing persistent opposition to the project from local residents. —Andrew Coen

Developer Seeks to Build 1,500 Homes on Brooklyn Waterfront

A developer is seeking approval to build a massive mixed-use development along the waterfront in Brooklyn’s Gravesend neighborhood.

Robert Konig, through the entity Westshore Views LLC, filed a rezoning application with the New York City Department of City Planning to build a 1.6 million-square-foot project on the 737,117-square-foot development site at 4302 Westshore Avenue, which is currently being used for car storage.

The project, which requires zoning approval from the city, would include 24 townhouses and 1,457 residential units across two high-rise buildings — approximately 437 of which would be affordable, the filing said.

The development would also comprise 10,448 square feet of retail, and 80,034 square feet of community facility space, approximately 75,000 square feet of which would be used for a 528-seat school. Plans also call for 143,190 square feet of public open space, including a 74,930-squarefoot public waterfront area, according to the filing. Konig also wants to build a 994-car parking lot and a 48-slip marina for residents.

If the city’s School Construction Authority does not approve the site for a public school, Konig plans to use the space for a private school or residential uses, the filing said.

“Overall, the applicant intends for the proposed project to be based on resiliency features that safely allow the siting of a residential community on the underutilized

development site,” Konig wrote in his application.

Konig, who has owned the Gravesend land through a separate entity since 2012, could not be reached for further comment.

The developer’s proposed zoning

changes related to the project include closing and reducing a portion of Bay 44th Street, reducing the width of Westshore Avenue, and renaming Westshore Avenue as a continuation of Bay 43rd Street, according to the filing. —Isabelle Durso

Sherry Wang Joins Vistria Group as Partner

Former Goldman Sachs executive Sherry Wang is bringing her expertise in deploying investment funds toward affordable and workforce housing to the Vistria Group, where she started a new role as a partner late last month, according to the firm.

“Sherry is one of the most experienced investors in public-private real estate, and is known for her track record of scaling innovative solutions to address affordable housing challenges,” Margaret Anadu, senior partner at Vistria, said in a statement.

Anadu and Wang had worked together at Goldman Sachs for about 15 years, according to Vistria. Goldman Sachs did not respond to a request for comment.

Wang was previously managing director of the Urban Investment Group at Goldman Sachs, where she deployed about $10 billion in funds to low-income housing projects across the U.S., including a $242 million construction loan for the buildout of a 414,000-square-foot facility on 125th Street in Harlem. Wang also led an initiative at Goldman Sachs to invest $10 billion in programs to improve the lives of at least 1 million Black women by 2030.

Also joining Vistria Group as new hires are James Wreschner, formerly of the Jonathan Rose Companies, and Ruby Shi, who is making the transition from Brookfield Properties. —Mark Hallum

HIGH HOPES: The new addition is due to include four towers and 4,000 apartments as well as public green space.

LONG VIEW: Developer Robert Konig has owned the Gravesend, Brooklyn, acreage since 2012.

Reach higher with Ridgewood’s commercial lending solutions. Ridgewood serves the five boroughs, Westchester, Rockland, Long Island, the lower Hudson Valley, Northern New Jersey and Fairfield County, Connecticut. Our real estate experts have extensive experience with multi-family, mixed-use, retail, office and industrial properties. We offer financing up to 75% of the property’s appraised value. Plus, you’ll get personalized service from our all-local team every step of the way.

$14,850,000 $7,500,000$6,950,000$2,800,000

Lease Deals of the Week

Sumitomo Mitsui Banking Corp. Little Big Hospitality

50,000 Expansion 45,000 New

Investment management company Invesco has renewed over 200,000 square feet of office space at Brookfield Properties’ 225 Liberty Street, according to a report from Savills

The duration and exact size of the lease, the broker reps for both parties, and the asking rent were unclear, though a recent listing for space on the building’s 26th floor quoted a price of $72 per square foot.

225 Liberty Street, one of the five buildings that make up Brookfield Place, was formerly known as Two World Financial Center. It contains nearly 2.5 million square feet of rentable space.

Other tenants in the building include fintech firm EquiLend, which signed a lease in March for 19,806 square feet on the 10th floor of the 44-story building; the marketing consulting firm SimonKucher & Partners, which took 27,458 square feet in the building in 2022; and trading firm DRW Holdings, which occupies 17,012 square feet, as Commercial Observer previously reported. The not-for-profit College Board recently took 41,000 square feet in the building, according to the New York Post

Brookfield did not respond to a request for comment, and Invesco did not respond to a request for information.

According to its website, Invesco manages over $91 billion in real estate assets across the globe. —Larry Getlen

The 765,000 square feet that law firm Paul, Weiss, Rifkind, Wharton & Garrison took at 1345 Avenue of the Americas in late 2023 wasn’t enough.

The firm — popularly known as Paul, Weiss — subleased an additional 84,672 square feet on the 29th and 30th floors of the Fisher Brothers-owned building at some point in the second quarter, a market report from Savills stated. The expansion brings the firm’s total footprint to 849,672 square feet.

Terms of the sublease were unclear, but a listing by Noah RE stated that the asking rent is $87 per square foot for a term ending in October 2025.

Brokers from JLL represented the sublandlord, while Chris Mongeluzo, Moshe Sukenik and Brian Cohen of Newmark handled negotiations for Paul, Weiss. JLL and Newmark declined to comment.

The identity of the sublandlord is unclear, but Global Infrastructure Partners is the last known tenant to lease the 29th and 30th floors. The asking rent at the time started at $95 per square foot.

Global Infrastructure Partners could not be reached for comment, while Paul, Weiss did not respond to a request. Paul, Weiss originally moved from 550,000 square feet at 1285 Avenue of the Americas, and has a 20-year lease at 1345 Avenue of the Americas.

Fisher Brothers did not respond to a request for comment. —Mark Hallum

Visual discovery and social media platform Pinterest has signed an 83,000-square-foot lease across the entire 13th floor at SL Green Realty’s 11 Madison Avenue, the landlord announced.

The length of the lease is 11 years and the asking rent was $90 per square foot, a source close to the deal told Commercial Observer. Pinterest is relocating from its office roughly seven blocks away at 225 Park Avenue South, where it currently occupies 40,000 square feet.

“We’re excited to welcome Pinterest to 11 Madison Avenue,” Steven Durels, executive vice president and director of leasing and real property at SL Green, said in a statement. “They join an extraordinary tenant roster.”

Pinterest was represented by Evan Margolin, Justin Haber and Michael Berg of JLL, while SL Green was represented by Brian Waterman, Scott Klau, Erik Harris and Brent Ozarowski from Newmark. JLL did not respond to a request for comment. Newmark declined to comment.

There had been talk of Pinterest taking over the Madison Avenue space back in May, but nothing was finalized at the time.

11 Madison Avenue is a 30-story, 2.34 million-square-foot office tower between East 24th and East 25th streets in Manhattan, just east of Madison Square Park. Other notable tenants of the building include financial institution UBS, media giant Sony, and Japanese beverage company Suntory —Amanda Schiavo

Japanese multinational financial institution Sumitomo Mitsui Banking Corporation expanded its presence at the Stahl Organization’s 277 Park Avenue office tower by 50,000 square feet, bringing its total footprint within the 50-story building to 316,000 square feet.

The length of the lease and the asking rent were not available, but asking rent at 277 Park Avenue can range between $120 and $140 per square foot, according to Cushman & Wakefield Mark P. Boisi, Bryan Boisi and Stephen Bellwood from C&W represented Stahl in the deal, the New York Post first reported. C&W did not respond to a request for comment.

It is unclear who represented Sumitomo Mitsui Banking Corporation in this expansion deal. However, previous Commercial Observer reporting noted that JLL’s Bill Peters represented the tenant when it expanded its footprint at 277 Park Avenue in 2013. JLL and Sumitomo Mitsui did not respond to a request for comment.

The Stahl Organization refinanced its 1.9 million-squarefoot office building at 277 Park Avenue, which is at the corner of Park Avenue and East 48th Street, with a $650 million commercial mortgagebacked securities loan in August of 2024. —A.S.

Little Big Hospitality, a company focused on unique and memorable experiences for families, has signed a 45,000-square-foot lease at CIM Group’s 50 Columbia Heights building in Brooklyn Heights, the landlord announced.

The company is launching a new family-oriented membership club called The Beginning Clubhouse, which is set to open next summer in the building, also known as the Panorama Office The Beginning Clubhouse will offer members curated activities and classes for children, child care, food and beverage options, and coworking spaces, along with fitness and wellness amenities.

“[There are] beautifully designed play areas and enriching programs for children alongside a full-floor lounge for work, fitness and wellness facilities, and incredible F&B options — all under one roof,” Michael Schoen, founder and CEO of Little Big Hospitality, said in a statement.

The length of the lease and the asking rent were not disclosed. However, the average asking rent for retail space in Brooklyn Heights ranges between $80 and $200 per square foot, according to the latest Real Estate Board of New York data.

Marc Schoen from Savitt Partners represented Little Big Hospitality and The Beginning Clubhouse, while Peter Whitenack, Mai Shachi and Andrew Connolly from Newmark represented CIM Group. Neither firm responded to requests for comment. —A.S.

Lease Deals of the Week LEASES

Monroe Capital leased an additional 15,000 square feet of Munich Re’s office building at 320 Park Avenue, doubling its footprint and giving the asset management firm the entire 21st and 30th floors.

The length of the lease was not available, but asking rent was $170 per square foot, a source close to the deal told Commercial Observer. News of the lease was first reported in the New York Post Frank Doyle, David Kleiner and Carlee Palmer from JLL represented Munich Re in this lease, while Greg Taubin from Savills represented Monroe. JLL and Savills declined to comment, and Monroe did not respond to a request for comment.

Monroe had previously leased 15,000 square feet across the building’s entire 30th floor in December, the Post noted, after moving offices from 126 East 56th Street. Asking rent for that first space was $140 per square foot.

Munich took full ownership of 320 Park Avenue, a 35-story office building also known as the Mutual of America Building, for more than $500 million in late 2024 from its joint venture partner Mutual of America, the Post reported at the time.

Other office tenants at 320 Park Avenue include a corporate location of Flagstar Bank, financial institution Fidelity Investments, and wealth management services provider Raymond James —A.S.

Educational development organization Publicolor is extending its stay at 20 West 36th Street

The nonprofit organization, which focuses on at-risk youth, signed a deal with landlord Koeppel Rosen to keep its 6,850 square feet on the ninth floor of the building, which is between Avenue of the Americas and Fifth Avenue. The landlord did not disclose the length of the lease or the asking rent in the deal.

The average asking rent for Midtown in May was $81.62 per square foot, according to a report from CBRE

“The building’s central location in Midtown Manhattan ensures that students from all over the New York area can easily access Publicolor’s headquarters,” Max Koeppel, who represented Koeppel Rosen in-house, said in a statement.

It’s unclear who represented Publicolor in the deal.

Publicolor moved into the 12-story building in August 2015, when it signed a 10-year lease that doubled the size of its previous space. Other tenants include American Friends of Magen David Adom, Martin Brudnizki

Design Studio and packaging and logistics company Pims Incorporated —M.H.

Women’s clothing retailer Free People is moving its Union Square store to a different spot within its building, Commercial Observer has learned.

Free People, which is part of a brand portfolio called URBN that includes Urban Outfitters and Anthropologie, has signed a 10-year lease for 5,500 square feet at the base of Kalimian Properties’ 79 Fifth Avenue, according to a source with knowledge of the deal. Asking rent was $400 per square foot.

Free People moved into its current mid-block space at the Fifth Avenue building between East 15th and East 16th streets in 2007, and it will relocate to the property’s corner retail space as part of the deal, the source said. Its new space spans 4,300 square feet on the ground floor and 1,200 square feet in the basement.

McDevitt Company ’s Tim Duffy and Wade McDevitt brokered the deal for the tenant, while Newmark’s Peter Whitenack and Robert Cohen represented the landlord.

Newmark declined to comment, while spokespeople for Free People and McDevitt did not respond to requests for comment. The landlord could not be reached for comment.

Free People’s Union Square store was the retailer’s first location in Manhattan, and it now has four other New York City spots throughout Manhattan and Brooklyn, according to its website —Isabelle Durso

Text messaging platform Sent has signed a lease for 4,609 square feet of office space at 157 West 18th Street

Neil King, Maxwell Tarter and Kelly Tipton with CBRE represented landlord Caspi Development Eric Siegel and Chery Anavian at LSL Advisors represented Sent. The lease first appeared on Traded

The building was recently fully renovated. A CBRE listing page for the building shows that Caspi has been marketing three full floors — the third, sixth and seventh — each spanning 4,609 square feet. All except the seventh are described as “brand-new prebuilt with 10-foot ceilings,” with patterned hardwood floors and glass-front conference rooms. A Google listing indicates that Sent took the seventh floor, which is the building’s penthouse and features double-height ceilings and a private terrace.

Caspi purchased the building in 2019 for $23.2 million from an undisclosed buyer, according to public records

The length of the lease and the asking rent were not disclosed. Asking rents for office space in Chelsea for the first quarter of 2025 averaged $67.82 per square foot overall and $91.40 per square foot for Class A space, according to a report by Cushman & Wakefield. LSL, CBRE and Caspi did not respond to requests for comment.

—L.G.

Medical equipment manufacturer Cranial Technologies is moving into Monadnock Development’s newly built headquarters building in Gowanus, Brooklyn.

Cranial, a non-surgical provider for the treatment of flat head syndrome in babies, has signed a lease for 4,456 square feet on the sixth floor of Monadnock’s sixstory, mixed-use building at 300 Huntington Street, according to landlord broker CBRE

The medical firm has more than 100 clinics nationwide, but its deal at 300 Huntington represents its first office in Brooklyn, CBRE said.

“This commitment by Cranial Technologies speaks to the high-quality office space, highly curated amenities and ideal location of 300 Huntington Street,” CBRE’s Patrick Dugan, who brokered the deal for the landlord along with Joseph Cirone and Jesse de la Rama, said in a statement.

The length of the lease and asking rent were unclear, but office asking rent at the building ranges from $50 to $60 per square foot. Colliers’ Joe Speck and Chad Poff represented the tenant in the deal. Spokespeople for Cranial, Monadnock and Colliers did not respond to requests for comment.

Monadnock’s 136,000-squarefoot development west of the Gowanus Canal was completed in January 2024. The developer itself currently occupies 40,000 square feet on the second and third floors for its headquarters, along with 15,000 square feet in the backyard for its contractor shop. —I.D.

As NYC Builds a New Normal, Business Improvement Districts Lead the Way

How the City’s Business Improvement Districts Help Create

ew York City’s neighborhood associations and business improvement districts (BIDs) are the city’s quiet heroes, keeping our streets clean, fun and lively. From hiring the street cleaners that keep our streets garbage-free, to helping new businesses trumpet their arrival, to establishing pedestrian plazas that provide a needed respite for shoppers, BIDs are the smoothly purring engine that keep the city surging forward.

The past five years were especially challenging for New York City’s BIDs, as navigating COVID and the confusion of the post-pandemic years lent an urgency to their activities and planning.

But these days, the city is entering a new phase. While New York is not without its challenges, our BIDs can now aim their determined focus at enhancements instead of survival.

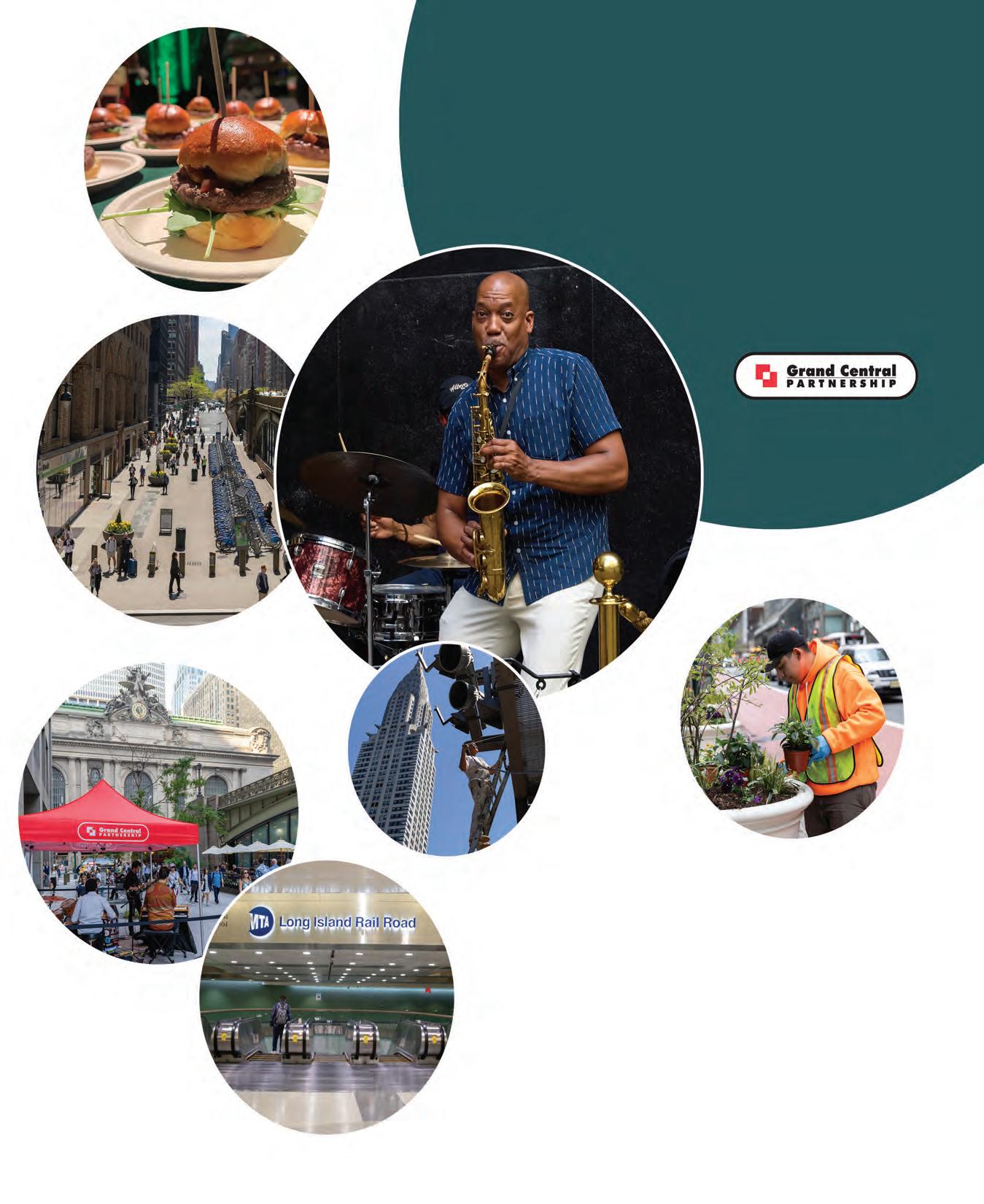

“This was a year of progress,” said Fred Cerullo, president and CEO of the Grand Central Partnership, which covers the area in Midtown bordered by 35th Street, 54th Street, Second Avenue and Fifth Avenue. “It was a year of breathing new life into things and continuous improvement. We’re always looking for ways to do better and, in some cases, bigger.”

The Partnership tripled its pedestrian-counting capabilities in the area, helping it more accurately plan everything from programming to garbage pickup.

Cerullo notes that local pedestrian traffic has averaged around 90 percent of 2019 numbers.

“That’s 90 percent on average, which means there are days where we have 130 percent (over 2019’s numbers) in the district,” said Cerullo. “The people are back. You can tell just by walking down any street in Midtown East. You can barely get in the front door at some of our restaurants.”

One significant reason for this has been the addition of the Long Island Rail Road stop at Grand Central, which has made the area more convenient for Long Island residents.

“We’ve seen a 109 percent increase in people with Long Island ZIP codes coming into the neighborhood,” said Cerullo, quoting data from Placer.ai. “That’s not LIRR usage. That’s Long Islanders in the neighborhood.”

To cater to the growing number of visitors, Grand Central Partnership has increased its free live music programming.

The Pershing Square Sounds series features lunchtime jazz shows on Tuesdays and

a Vibrant New York

happy hour concerts on Wednesdays from May through September at Pershing Square Plaza West, on Park Avenue between 41st and 42nd streets.

The Partnership also partnered with the Arts and Architecture Conservancy at Saint Peter’s, at 601 Lexington Avenue, to host lunchtime concerts on Thursdays from July through September. The Rudin family, owners of 345 Park Avenue, are sponsoring lunchtime shows at their building every Wednesday through August.

“We hosted 63 or so concerts last year. We’re up to 75 this year,” said Cerullo.

In addition to Pershing Square West Plaza, the Partnership has introduced Pershing Square East this year, expanding its car-free street availability for public use.

“There are now two beautiful public spaces with tables, chairs and plantings,”

Vibrant pedestrian activity in Midtown East.

The Ron Jackson Trio performing at Grand Central Partnership’s Summer Solstice Music Festival.

Pershing Square Plaza West, and explore the recently completed Pershing Square Plaza East, featuring Citi Bike access , new seating, and plantings. Enjoy exceptional outdoor dining at neighborhood cafés and restaurants, take in art and architecture throughout the district, and experience the color and vibrancy of our seasonal horticulture program. With seamless connections through Grand Central Terminal and Grand Central Madison, getting here and exploring more is simple.

PARTNERINSIGHTS

said Cerullo, who added that Pershing Square East also hosts the city’s largest bike-share program.

In addition to beautification efforts and leisure time initiatives, BIDs can also be political advocates for area businesses.

Jessica Lappin leads the Downtown Alliance, which celebrates its 30th anniversary this year serving the area bordered by City Hall, the Battery, the East River and West Street.

With the Lower Manhattan Relocation and Employment Assistance Program (REAP), a major tax incentive for downtown businesses, set to expire at the end of June, Lappin was laser-focused on persuading Albany to renew the program.

The week before we spoke, she succeeded.

“We spent a lot of time and effort lobbying the legislature to have it renewed,” said Lappin. “Businesses moving here get a $3,000 tax credit per employee if they are growing their payroll by 25 percent or moving here from outside of the state. It was a very nice victory, and something we hope people consider when deciding where to relocate their business.”

This is yet one more factor in the plus

column for business considering a downtown relocation. The area has changed drastically over the past 30 years, evolving from a strictly 9-to-5 business community that became a ghost town at 5 p.m. to much more of a residential and tourist-friendly 24/7 neighborhood.

“We’ve been reflecting on what we’ve accomplished since 1995,” said Lappin. “The neighborhood was on its heels then. That’s why the Alliance was founded, to help revitalize the neighborhood and bring it back.”

Lappin notes that in 2001, the area had six hotels with less than 2,500 rooms total. Today, there are 44 hotels in downtown with over 8,500 rooms available. As for residents, the area covered by the BID had fewer than 15,000 permanent residents in 1995. Today, that number is over 60,000.

“People didn’t have a reason to come downtown in the `90s other than the Statue of Liberty,” said Lappin. “But we have 44 hotels now, which is sort of shocking, and they’re on par with or exceed those in other neighborhoods in Manhattan.”

Lappin notes that concepts pioneered by the Downtown Alliance are now taken for granted, like a widespread composting

program, or a bikeshare program they ran years before Citi Bike. She also makes the case that the Alliance was directly responsible for the area’s growing residential base.

“In the 1990s, the Downtown Alliance had a truly revolutionary idea to create residential housing in the neighborhood. That may be the single most significant thing the Alliance has done,” said Lappin. “Thirty years ago, turning a downtown office area into a residential neighborhood was a revolutionary concept. That’s probably the biggest thing the Alliance has contributed, not just here but across the country.”

To satisfy the needs of its growing constituency, the Alliance has expanded its cultural programming. The BID has been hosting Dine Around Downtown, a celebration and sampling of local eateries, for over 20 years. This year’s event, which took place June 11 and was hosted by James Beard-award winning chef Rocco DiSpirito, was its most popular ever, with over 15,000 people sampling cuisine from over 40 area restaurants.

Another continuing and growing tradition for the Alliance is its free concert series, which ran through June. Two locations alternated in offering performances at lunchtime

on Wednesdays: World Trade Center’s North Oculus Plaza, and 140 Broadway. The series paired with the Alliance’s “Art Is All Around” campaign, which placed public art and performances throughout the neighborhood.

The Alliance also sponsors events such as the panel conversation series LM Live, and New York on Film, where screenings of New York City-related movies are followed by in-depth discussions with critics, historians, and people directly involved with the films in question.

Over in the neighborhoods of Flatiron and NoMad, the Flatiron NoMad Partnership serves an area that is home to more sales tax-contributing businesses than any other, handling the area roughly bordered by 20th Street, Sixth Avenue, 31st Street, and Park Avenue South, as well as the full Baruch College campus extending to Third Avenue.

One major priority for the BID has been further implementation of the Broadway Vision plan, a combined effort among the city’s Department of Transportation and several BIDs to turn much of Broadway into pedestrian plazas.

While the plazas are technically temporary, the BID is working with others to make them

Alliance President Jessica Lappin and staff work to keep neighborhood flowering.

Dine Around Downtown Draws Thousands to Community Food Festival

Downtown Alliance Public Safety Officers on Patrol

PARTNERINSIGHTS

permanent as part of a more than $100 million capital plan, including the addition of new horticultural and security elements and supportive work below ground.

“We’ve seen terrific vibrancy and numbers when it comes to use of the space, as well as filling retail vacancies up and down Broadway,” said James Mettham, president of the Flatiron NoMad Partnership. “We’ve made this one of the premier commercial corridors, infusing pedestrian plazas, bike lanes, distinctive outdoor dining, and respites for people to enjoy their own time.”

Flatiron NoMad has also hosted several successful art installations. After last year’s incredible exhibit of The Portal, which allowed the public to communicate face to face with people in Dublin, Ireland, on the street in real time, the Partnership hosted Winter Glow in January and February, including interactive artworks like “The Diamonds,” a large kaleidoscopic object that produced a vibrant spectrum of ever-shifting light and sound, and “Spectrum,” which converted human speech into a bedazzling array of waves and pulses.

The BID also pulled out all the stops for Pride Month with Start With Love, which the BID describes as “a monthlong celebration of LGBTQIA+ visibility and community” featuring public art displays and musical performances, and spotlighting LGBTQIA+ businesses and voices in the Flatiron & NoMad communities.

“We’re proud to launch Start With Love: Pride in Flatiron NoMad, honoring the vibrancy and diversity of our community as the starting point of the iconic NYC Pride March,” said Mettham.

On the business side of things, Mettham notes that 70 new retail, street-level businesses have opened in the area over the past year, in addition to several hundred more businesses that moved into local office buildings.

The team at the Partnership offers hands-on neighborhood introductions to everything the district has to offer. From keeping the streets vibrant, clean and safe, to spotlighting new businesses across their platforms, they’re all about creating connections and amplifying what makes each business unique in the neighborhood.

“We’re here to integrate new businesses into the pulse of the neighborhood,” said Mettham. “We don’t just tell them about our service. We elevate their presence, feature them across our channels, and plug them into a dynamic community network.”

On top of all this, BIDs throughout the city are preparing for a significant change in the nature of their areas as more and more office buildings convert to residential, meaning that many of the city’s neighborhoods, following downtown’s lead, will need to transition from office areas to full-on 24/7 neighborhoods.

“We have residential development happening at a rate we’ve never experienced before,” said Cerullo. “That has us thinking about how we address that increase in residential population. For example, where else can we develop public space for people to sit and enjoy a cup of coffee on a Sunday morning? Where can we find more spaces for not just recreational activities, but more passive experiences that beautify the neighborhood?”

Of course, it’s impossible to say exactly what New York City will look like 20 or even 10 years from now. But whatever the makeup of this ever-evolving city, our BIDs and neighborhood associations will be keeping pace, doing their best to ensure that New York City’s neighborhoods are clean, safe, vibrant, and as welcoming as possible to residents, commuters and tourists alike.

PARTNER CONTENT

Where New York Meets New York

We are the Flatiron NoMad Partnership, serving the businesses, people, and places that help make this district one of Manhattan’s most iconic and authentic destinations.

Grand Central Terminal

Retail space available

Grand Central Market at Grand Central Terminal

The MTA is soliciting proposals for retail spaces MKT-25 and MKT-26, located in Grand Central Market. Each space is 274 sq. ft., offered individually or combined.

Issued: June 24

Due: August 5

Finance

One regional bank is here to stay

Banks are the new must-have tenants

18 20 24 Blackstone’s megaloan in Jersey City

FINANCE

Debt Deals of the Week Blackstone Provides $515M Loan for Phase 1 of Kushner Companies’ The Journal in Jersey City

U-B-SIGNING REFIS!

Deutsche Bank, UBS Refinance Mixed-Use

Queens Property With $160M CMBS Loan

Rentar Development has landed a $160 million debt package to refinance a Queens mixeduse retail and industrial asset, Commercial Observer has learned.

Deutsche Bank , whose lending platform is led by Dino Paparelli, and UBS originated the commercial mortgage-backed securities loan for the developer’s three-story Rentar Plaza building in Middle Village, Queens.

BayBridge Real Estate Capital arranged the financing.

Located at 66-26 Metropolitan Avenue, the 1.43 million-squarefoot Rentar Plaza was constructed by Garden City, N.Y.-based Rentar Development in 1972. The City of New York is the largest industrial tenant while BJ’s Wholesale Club anchors the retail portion, which is undergoing a renovation as part of a rebranding.

Amazon inked a 10-year lease for 300,000 square feet of warehouse space in February 2020, CO reported at the time.

A representative for Rentar Development said the rebranded 232,000-square-foot retail portion called The Shops At Rentar Plaza is slated for completion in spring 2026 with current tenants BJ’s, FitNation, Eyeworld and VJ Liquors remaining open during construction. Burlington and Catch Air have also signed leases of 28,000 square feet and 18,000 square feet, respectively, with plans to begin construction of new stores soon, according to Rentar.

Officials at UBS and BayBridge did not return requests for comment. Deutsche Bank declined to comment.—Andrew Coen

Deal volume typically slows down in the run-up to the July 4 holiday, but for Kushner Companies it’s business as usual.

The firm just sealed a $515 million loan from Blackstone for The Journal, its luxury twotower residential development in Jersey City, N.J.’s Journal Square submarket, Commercial Observer can first report.

The three-year loan — originated by Blackstone Real Estate Debt Strategies (BREDS) — includes two one-year extension options and will be used to complete The Journal’s construction and lease-up. It retires previous construction financing on the project from 2022, when AIG provided a $385 million senior loan and Related Credit Funds provided a $130 million mezzanine loan.

“We thank our construction lenders, AIG and Related for their trust in us three years ago, and are excited to open this bright chapter with Blackstone,” Laurent Morali, CEO of Kushner Companies, said in a statement. “We feel blessed to be able to finance our greatest projects with people we call friends.”

Located at 1 Journal Square, the property spans 2 million square feet and comprises 1,723 apartments across two 52-story glass towers, plus a retail podium housing 40,000 square feet that’s 100 percent leased to Target. Phase 1 — just refinanced by Blackstone — encompasses the 12-story retail podium, the development’s 966-unit north tower and 1,000 parking spaces.

“We are pleased to support the completion of this high-quality multifamily property,” a spokesperson for BREDS told CO. “This transaction reflects Blackstone Real Estate Debt Strategies’ ability to deliver creative, large-scale financing solutions and provide certainty to borrowers amidst market volatility.”

Chetrit

Indeed, there’s plenty of market fireworks to contend with at the moment, and closing a half-billiondollar loan in the midst of the volatility is certainly nothing to sneeze at. As if that weren’t enough to celebrate, the building is also off to the races in welcoming new residents.

“The lease-up couldn’t have started stronger, and we look forward to welcoming our first residents this week,” Morali said.

As such, Blackstone’s big loan closed July 1, the day the building opened to residents. Further, The Journal’s leasing center opened on June 12 and already 300 leases have already been executed, making the north tower already more than 30 percent pre-leased.

The Journal features views of the Hudson River and the Statue of Liberty. It’s adjacent to the PATH train, which can be in Manhattan in 20 minutes and which makes The Journal an ideal pick for commuting professionals as well as students.

Amenities include a fitness center, an indoor basketball court, indoor and outdoor pools, a plunge pool, a sauna, a bowling alley, a podcast studio and a yoga studio.

The deal fits nicely into Blackstone’s theme of investing in irreplaceable properties in prime locations across the globe, with Journal Square also experiencing population, household income and job growth greater than the wider New York City metro area over the past five years.

“We believe in the long-term potential of Journal Square and are proud to be part of its continued evolution,” Nicole Kushner Meyer, president of Kushner Companies, said in a statement. “This project is about more than just building homes. It is about creating beautifully designed spaces that inspire connection, elevate daily life, and reflect the unique energy and spirit of the neighborhood.”

Newmark’s Jordan Roeschlaub, Nick Scribani and John Caraviello negotiated the debt.

“The process with Blackstone, orchestrated by Newmark, couldn’t have gone more smoothly,” Nick Maki, head of investment management at Kushner said. “We’re grateful for this great execution.”

The Journal’s second phase is also firmly underway. In June 2024, Kushner Companies landed a $295 million loan from Apollo and RXR to fund its construction, with plans to complete the second phase by the end of this year. (Disclosure: Meyer is married to Observer Media owner Joseph Meyer.)

The Blackstone loan brings Kushner Companies’ financing closings to almost $1 billion in the first half of the year alone.

Cathy Cunningham

Completes Discounted Loan Payoff for 404 Fifth Avenue

The Chetrit Organization has sealed a discounted payoff for the $65 million loan on its former headquarters at 404 Fifth Avenue, Commercial Observer has learned.

The office building’s loan is being paid down as part of a broader recap of the building, in which a new capital partner — which couldn’t be named — is also being brought in.

The loan on the property, also known as the Stewart Building, was originated by the now-defunct Signature Bank in 2016, becoming part of the $17 billion pool of Signature loans acquired by a joint venture involving Blackstone, Canada Pension Plan Investment Board and Rialto Capital in December 2023, with Rialto also the servicer of the loans.

Iron Hound Management ’s Robert Verrone and Will Forbes led the restructuring negotiations with the lenders on behalf of the Chetrit Organization.

“Over the past three months we have closed three large restructuring or discounted payoffs with Rialto; we appreciate them working with us and we look forward to turning these assets around,” Juda Chetrit said in a statement.

Indeed, in April the Chetrit Organization also secured an extension for the $76.5 million CMBS loan on 459 Broadway and 427 Broadway in SoHo, and a month later the firm extended its loan on 393-401 Fifth Avenue. Iron Hound’s Forbes and Verrone negotiated the extensions on behalf of the firm in each instance.

After the 404 Fifth loan missed its maturity date in June 2024, Blackstone filed a lawsuit in January and sought to foreclose to recoup the loan’s outstanding balance of $60.3 million as well as interest, late charges and attorney fees, according to Crain’s New York Business

With the payoff completed, a resolution has formally been achieved and the lawsuit ends, a source familiar with the transaction said.

The eight-story building, acquired by the Chetrit Organization in 1998, per Crain’s, is completely vacant, and the plan is now to start signing new tenants, sources said.

Blackstone and Iron Hound declined to comment. Rialto officials weren’t available for comment.—C.C.

The Journal in Jersey City.

BANK

Wells Fargo’s Peter Cannava.

FINANCE

Bank of America

Refis Micro Industrial Portfolio With $94M Loan

WareSpace and its capital partner Jadian Capital have secured a $94 million loan to refinance a portfolio of micro-bay industrial assets, Commercial Observer has learned.

Bank of America provided the loan for the 20-asset portfolio of smaller warehouses operating under the WareSpace brand.

Newmark arranged the financing with a team consisting of Jordan Roeschlaub, Nick Scribani, and Chris Lozinak

Columbia, Md.-based WareSpace owns small warehouse properties rented out to small businesses all over the U.S., including three locations in Washington, D.C., and Chicago, according to its website. It has been acquiring vacant infill properties over the past three years and converting buildings into industrial suites ranging from 200 to 2,500 square feet, according to Newmark.

“Between strong small business formation and virtually no new infill supply, small bay vacancy is now the lowest in the industrial sector,” Levi Cohen, CEO of WareSpace, said in a statement.

Matthew Hennessy, director at Jadian Capital, said in a statement that the loan from Bank of America “demonstrates how institutional capital providers have come to appreciate the WareSpace value proposition.”

Hennesy added that Jadian is looking to financially back WareSpace’s plans to scale its footprint from 20 to 50 locations over the next “several” years.

Bank of America declined to comment.—A.C.

BFC Partners Closes on $250M Construction Loan for Coney Island Housing Development

Developer BFC Partners has secured a $250 million construction loan to complete the third phase of a major affordable housing development in Coney Island, Brooklyn, Commercial Observer can first report.

The loan, which was provided by Citi Community Capital, will allow BFC to complete the three-building project along Surf Avenue and deliver a total of 1,242 homes to the neighborhood, according to an announcement. Construction is set to be complete in 2028.

The city officially partnered with BFC last week for the project’s Coney Island Phase III, which will bring 420 apartments, roughly 10,700 square feet of commercial space, and about 9,700 square feet of community facility space to 1709 Surf Avenue, as CO previously reported

“Closing on and starting construction of the third and final phase of this transformational development along Surf Avenue in Coney Island marks a major milestone for our team,” Joseph Ferrara, principal at BFC, said in a statement.

“We are proud to continue investing in the future of this vibrant community and are

especially grateful to our city partners and to Citi for their unwavering support and collaboration,” Ferrara added. “Together, we’re building lasting affordability, opportunity and impact for Coney Island.”

The first phase of the project at 2926 West 19th Street was completed in 2021 and created 446 affordable units, while the second phase at 1607 Surf Avenue was finished last year and delivered another 376 units, according to the announcement. BFC worked on both phases.

In addition to Citi Community Capital’s loan, the Coney Island development has received nearly $700 million in investments, including more than $90 million in subsidy

from Mayor Eric Adams’s administration, $116 million in construction financing from the New York City Housing Development Corporation, and funding from the New York City Department of Housing Preservation and Development

“Citi Community Capital is pleased to have been a part of the team that BFC Partners assembled, providing construction debt and long-term equity, that helped finance 1709 Surf Avenue,” Richard Gerwitz, a managing director at Citi, said in a statement.

BFC’s project isn’t the only new development going up on Coney Island’s Surf Avenue.

In February, the New York City Economic Development Corporation (EDC) issued a request for proposals to build a 500-unit project called Coney Island West on an 80,000-square-foot, city-owned site between West 21st and West 22nd streets, CO reported The EDC will select a developer for that project by the end of the year.

Mayor Adams also has plans to renovate the summer tourist hot spot’s Riegelmann Boardwalk and Abe Stark Sports Center, as well as update the neighborhood’s streets and sewers.—Isabelle Durso

Kushner Companies, PTM Seal $87M Loan From Corebridge for Miami’s 2000 Biscayne

Kushner Companies and PTM Partners have locked in a fresh round of financing for 2000 Biscayne, the partners’ luxury apartment building in Miami’s Edgewater neighborhood, Commercial Observer has learned.

The developers just sealed an $87.3 million, eight-year loan from Corebridge Financial, closing 2000 Biscayne’s development and construction chapter with permanent, fixed-rate financing.

The financing was structured to be coterminous with the $52 million in debt on the building’s fee simple interest — which also was provided by Corebridge (a spinoff of AIG). Together, the two components bring the total debt on the building to $139.3 million.

Walker & Dunlop’s Aaron Appel, Jonathan Schwartz, Keith Kurland, Adam Schwartz, Michael Stepniewski, Jordan Casella, Christopher de Raet, Stanley Cayre and Dustin Stolly negotiated the financing, which retires the previous leasehold mortgage on the building that Valley National Bank provided in 2021

“2000 Biscayne represents the highest standard for modern living in one of Miami’s most dynamic neighborhoods, combining exceptional design, premium finishes and unmatched amenities,” Laurent Morali, CEO of Kushner Companies, said. “This successful financing is a clear testament to the strength and quality of the asset, and we’re grateful to our friends at Corebridge for their trust and confidence.

Thank you to the Walker & Dunlop team for their unwavering support and expertise through another great execution.”

PTM Partners CEO Michael Tillman said the refinancing is a testament to the project’s success. “The 2000 Biscayne development team’s meticulous attention to detail and design has realized itself in a brisk 75 percent lease-up in a very short period,” he said. “Not only does this demonstrate the demand for high quality assets but also shows the continued strength of the Miami rental market, particularly within Edgewater.”

Kushner and PTM delivered the 36-story, 420-unit apartment building in October 2024 and was designed by Kobi Karp Architecture Leasing launched in July 2024, and today

the building is 75 percent leased, with amenities that include coworking spaces, community dining areas, a children’s play area and a dog park. (Disclosure: Kushner president Nicole Kushner Meyer is married to Observer Media owner Joseph Meyer.)

“2000 Biscayne delivers unmatched quality, convenience and lifestyle offerings, firmly establishing it as the leading multifamily property in the Miami market,” Stepniewski, senior director of New York capital markets at Walker & Dunlop, said in a statement. “Miami continues to see strong demand for well-located, high-quality housing, driven by a rapidly growing population and sustained economic expansion. We’re proud to have been part of this exceptional project and look forward to its continued success.”—C.C.

A rendering of the Coney Island development.

Laurent Morali (top), Michael Stepniewski (bottom) and 2000 Biscayne.

A WareSpace storage location.

ost people in finance remember where they were when they heard Silicon Valley Bank had collapsed. And, if you were in New York City, the failures of Signature Bank and First Republic Bank were likely even more palpable. Both were major players in financing the city’s commercial real estate over the years, but ultimately became the secondand fourth- largest bank failures, respectively, in U.S. history.

Signature Bank, in particular, had been a consistent, go-to lender in the five boroughs, and a top three multifamily lender. At the helm of its lending activities was Joseph Fingerman — also the highest-profile, most visible member of the team. At the time of the bank’s demise, he and his team had accumulated a $33 billion commercial real estate loan book — executing $4 billion across 632 loans in 2021 alone — along with a reputation for being relationship lenders that borrowers could rely on, and trust.

When Signature Bank failed on March 12, 2023, CRE loans weren’t the cause of its demise. Rather, the fatal blows came from the bank’s $16.52 billion of cryptocurrency coupled with contagion from SVB’s failure, which kick-started a quick outflow of deposits.

Peapacking Heat

Peapack Private Bank & Trust seized on an opportunity the regional banking crisis presented to add Signature Bank’s Joseph Fingerman and Andrew Corrado to its roster as its business expanded into New York City.

By Cathy Cunningham

“It was never in our minds that we would fail,” Fingerman said. “We were quite solvent when the FDIC seized us, so the thought of this happening was surreal. In our opinion, it was a definite overreach of [the FDIC’s] authority, and we just couldn’t understand how this could be possible. The first thing you think about are your clients and employees and what to say to them. Unfortunately it takes time to gain some clarity, especially during times of turmoil and unanswered questions.”

The bank run on Signature escalated on Thursday afternoon, March 9, and by Friday several members of the lending team, including Fingerman, were called in to review and prepare loans for pledging to the Federal Reserve. “We spent the weekend working tirelessly in the office, wrapping up around 3 p.m. Sunday before I went home to relax with my kids,” Fingerman said.

While he was watching the NCAA tournament with his family, news broke on CNBC that the bank had been seized, and Fingerman’s cellphone immediately lit up with messages. “It was a surreal moment,” he recalls. “By Monday, we were operating under an FDIC bridge bank, and a week later it was announced that only deposit operations were sold to NYCB/Flagstar, while the CRE and fund banking portfolios were retained by the FDIC. After 16 years [working at Signature] in CRE, it hit me hard that I wouldn’t be part of the acquiring bank’s future.”

There are many theories around what eventually led to the seizure, and Fingerman has his. “Texts and tweets can make a bank run a reality in minutes in this day and age,” he said. “In order to have a systemic failure

Photographs by Evelyn Freja Joseph Fingerman.

you need two banks, and we had a somewhat similar business model to Silicon Valley Bank — so we were in the wrong place at the wrong time.”

First Republic was next. It may have been headquartered in San Francisco, but its loan book had heavy exposure to New York City real estate, adding to the void that Signature left behind. An over-reliance on uninsured deposits coupled with continued loss in depositor confidence was also key in First Republic’s demise on May 1, but so was its book of lowinterest mortgages, fatally impacted by a series of rate hikes that reduced the market value of those assets.

While the world watched in stunned silence as the banking crisis unfolded, wondering whether a more widespread run was next, for some, the institutions’ failures didn’t just open a window of opportunity — it took that window clean off its hinges.

“The opportunity when Signature and First Republic closed their doors was to run into New York City — not walk,” said Doug Kennedy, president and CEO of New Jerseyheadquartered Peapack Private Bank & Trust.

Indeed, opportunity came sprinting through the door, with Peapack having the ability to hire teams from both of the failed banks, notably two of Signature Bank’s most wellknown, respected players — Fingerman and Andrew Corrado. In order to fully capture the opportunity left behind in New York, Peapack would also need a Manhattan location, and a plan to fill the immediate, abrupt and gaping regional bankshaped void.

“When Signature failed, people would call me and say, ‘Joe, you don’t understand what a loss it is to have Signature go out of the market,’ ” Fingerman said. “They’d say, ‘I’m sure it was a big loss to you, but it was a huge loss for the real estate community.’ I’m really excited to be able to bring that back at Peapack.”

They say you don’t know what you’ve got until it’s gone, and so Fingerman is also confident.

“There are two types of real estate people: those that are banking with Peapack, and ones that will be banking with Peapack,” Fingerman said. “Our goal is to put the Peapack brand in front of people, show them who we are, and continue to execute.”

104 years young

If you’re Googling “Peapack” right now, you might not be alone. Although the bank has been around for more than a century, many outside of its home territory are unfamiliar with the New Jersey bank. (Fingerman said he often chats with his peers today, and only at the end of the conversation will they say, “Wait, where are you now?!”)

Kennedy describes Peapack as a “104-year-old startup” — one that he joined 12 years ago when the bank was the ripe old age of 92. Previously Peapack-Gladstone Bank, the company reorganized and combined its banking and wealth management divisions in 2024, rebranding as Peapack Private Bank & Trust.

When he joined Peapack in 2012, the bank had a great reputation around client service but wasn’t overly sophisticated on the lending side, Kennedy said. It was a $1 billion balance sheet bank with a $2 billion wealth management business. Kennedy looked to other successful boutique organizations he thought Peapack could emulate — specifically the regional banks that had a single point of contact and a hyper-focus on client and borrower experience.

Oddly enough, Signature and First Republic were two of those banks.

“What they had in common was a single point of contact handling the transactional and operational needs as well as the lending, and doing it not only at a corporate level, but also on a personal level,” Kennedy said.

His team put together a 200-page document analyzing the two banks’ business models, how they were structured and how they paid their people, and began to adopt

POWER PLAYER

a similar client- centric business model at Peapack in New Jersey. When Signature and First Republic vanished from the market starting in March 2023, Kennedy saw the chance to bring what he had been building across the Hudson River to Manhattan.

“I knew we had to run into the city and start a business that looked and felt like both of those banks in order to fill the massive void they had left,” Kennedy said, speaking from Peapack’s shiny new Manhattan offices at 300 Park Avenue. “I knew that the banks that were already here [in Manhattan], even the smaller ones, couldn’t fill that void because that high level of service wasn’t part of their business model, whereas it was already very much part of our DNA.”

Not that this plan of action was quite as immediate as more timely concerns in the midst of the banking crisis.

“For the first two weeks [after Signature failed] I wanted to make sure that there wasn’t going to be a run on us, and that we weren’t going to fail,” Kennedy said. “Once I became certain it wasn’t going to happen, it was a run into New York City. We recruited a team, principally out of First Republic. Six months later I called Andrew [Corrado] and said, ‘Andrew, I’m coming into New York City to start a business. Can you coach me on what I should do?’ He said, ‘It’s funny you called, because I’d be interested in joining you, and I have a whole team of other individuals who might be interested as well.’ ”

Peapack hired 100 people in total from the two banks, the majority from Signature. There was just one rule as Kennedy went about putting his plan in motion: “We don’t hire jerks — strictly no assholes.”

‘We don’t hire jerks — strictly no assholes.’

‘A little like Van Halen’

Corrado, previously an executive vice president and head of commercial and private banking at Signature Bank, was working as a group director at Flagstar Bank when he got the call. Flagstar had acquired a large portion of Signature’s assets (and liabilities) post-failure.

“There wasn’t the ability to navigate the market as we once had,” Corrado said of his time at Flagstar. “Having interacted with Doug historically, and having the same, client-centric thought process, I felt that there could be a good match here.” He joined Peapack in March 2024, roughly a year after Signature failed.

Meanwhile, Fingerman had taken a role at a nonbank —A&E Real Estate’s lending arm —but his banking roots were calling.

“I felt like my highest and best use — to use an appraisal term — was back in a bank,” he said. “It was just a question of finding the right bank.”

Fingerman met with several banks before Peapack, and — for good reason — felt he was interviewing those banks just as much as they were interviewing him. “I wanted to know their headaches, and what I’d be getting myself into,” he said.

But Peapack, he already knew. The bank had been a formidable competitor of Signature’s for years in New Jersey. It had a large real estate portfolio, the two banks would often trade deals back and forth, and they had several clients in common. “It gave me comfort that they were able to produce a $2 billion- plus mortgage book and had a general idea of

what was going on in commercial real estate — as not everyone does,” Fingerman said, adding that he felt Peapack was the best fit for him, given its culture, client focus and position in the market.

Further, Kennedy, Corrado and Fingerman had similar beginnings, having all worked at North Fork Bank at various times. When Fingerman was a young analyst at the bank, Kennedy was running the bank’s New Jersey operations and Corrado was running the Long Island region. When Capital One bought North Fork in November 2008, Fingerman left for Signature Bank.

“We eventually dragged Andrew to Signature [in March 2014],” Fingerman said. “We’d also tried to drag Doug to Signature over the years, and so what was I going to say to this [Peapack] offer? It feels a little like Van Halen — the band’s back together again.”

The Signature fallout — from the bank’s failure to the shedding of its staff to the bank’s loan portfolios auction process — had been the industry’s obsession and must-read news, and Fingerman’s moves were keenly watched.

Keeping a secret in New York City real estate is like trying to nail jelly to a wall, however, and Fingerman’s interview setting at Peapack didn’t help too much. “I was sitting in this glass fishbowl of a conference room with people I’d known for years walking by and texting me while I was still in the interview,” Fingerman recalls, laughing.

When he accepted Peapack’s job offer, he already had a plan to help build the brand.

“Peapack didn’t have a retail location in New York to garner deposits previously,” Fingerman said. “When I took the role, I thought I’d be able to either go after the existing clients that have loans with us for deposits or — over the next few years — replace that book with my existing clients. Now, I’m doing a little bit of both of those. We’re working to make our book more relationship-focused, where we can go after clients for deposits, wealth, cash management, home mortgages, whatever they need — and it’s been really well received by the New York marketplace.”

In March 2024, when Corrado joined Peapack, the bank’s headcount was around 500 people. A little over a year later, it’s risen to 670 and the bank has grown its staff by more than 30 percent. Peapack has a $6 billion loan book today, of which roughly $2.5 billion is commercial real estate loans in the New York metro area and New Jersey. Its primary clients are family offices that own around 10 properties, have been in the business for typically decades, and place importance on a personal touch — a dedicated person to speak with who can handle both their deposit and lending needs.

“With all the change in the landscape in the banking world, clients are yearning for what they had pre-2023, so we’re providing tailored solutions to each one of the clients,” Fingerman said. “On the commercial real estate side, we’re lending on multifamily, retail, industrial and mixed-use properties throughout the New York metro area. While we have the capacity to lend on a much higher number, we’re trying to keep the loans under $20 million.”

The end of the gun

Many theories exist around what ultimately led to the untimely demise of the banks that failed in 2023. Kennedy, Corrado and Fingerman agree that a bank’s culture is key to its success, while pressure to feverishly grow can be a killer.

“I’ve never subscribed to ‘You have to close $300 million of loans per quarter,’ ” Fingerman said. “You have to find good business first, because I think when you’re given quotas, you end up making really bad decisions.”

In addition to its crypto book, and funding its activities through largely uninsured deposits, Signature aggressively grew from $50.6 billion to $110 billion in assets between 2019 and 2022 — without adequate risk management practices in place to match that growth, according to a FDIC report.

Kennedy, a member of the New York Fed’s board of

directors since 2020, carefully studied the FDIC postmortems on SVB, Signature and First Republic.

“All three of those banks were trying to fuel a growth story,” Kennedy said. “What they shared in common in their culture —which I think is wrong —was to grow at any cost.”

It’s a mindset that Peapack is steering well clear of.

“The lesson learned, and what we’ll not do, is drive this company for a number,” Kennedy said. “That’s not our preamble. I don’t care if we grow or don’t grow, let’s just go out and get the client. Let’s please them like we can like nobody’s business. Let’s get paid fairly for what it is that we do, and whatever the size that comes out of that, that’s fine.”

The big takeaway for Kennedy is “don’t focus on growth, focus on the client, focus on executing superbly for that client, and let the rest of it all take care of itself,” he said. “If you do that with really good people — who are not assholes and work collaboratively — the growth and the shareholders, all of that will follow. And this is a deep enough pond in the New York metro area, with $2.8 trillion in deposits. That’s the fuel that we need to lend, and just crumbs in this market is enough to make Peapack successful.”

Banking on Manhattan

To get those deposits and truly fill the void left by Signature’s exit, Peapack needed a location and retail branch in New York City. Kennedy had managed teams in New York City during his time at Capital One, and he knew Midtown was where Peapack had to be. In January 2024, it announced plans to open at Tishman Speyer’s 300 Park Avenue, officially opening its doors in March 2025.

The location houses 6,000 square feet for its private banking center and an additional 18,000 feet of office space on the 13th floor.

“We’re not just a New Jersey bank opening up a branch in Manhattan,” Kennedy said. “This is a transformational

change, and we’re here for the long haul.”

Kennedy views the bank’s new retail location — which includes a quarter-million-dollar horse statue in the lobby window that’s illuminated at night — as an announcement of sorts. It’s certainly caught the eyes of some of Peapack’s competitors, who have been taking selfies with the horse as they pass and sending them to Fingerman.

“It doesn’t say typical retail bank,” Kennedy said. “It’s really there as a billboard, a showplace, a sign of our commitment.”

The bank may not be hyperfocused on growth, but it’s happening anyway. Peapack thought it could bring in around $400 million in deposits in 2024 through Corrado and the New York teams they’d hired. It ended the year at $1.2 billion.

As it expands its business in New York, the team is focused on building out Peapack’s business diligently, but in partnership with clients.

“The client experience is changing. We’re saying to clients, ‘If you want to use that side of the balance sheet and be borrowers, we would like to have some deposits from you,’ ” Fingerman said. “My core group in New York, together with the legacy team in New Jersey, basically went through both books, Signature and legacy Peapack, and said, ‘These are the clients that we want to go after, and these are the clients that are perfectly fine. But if they’re more transactional and not willing to give us deposits, we would like to either convert them to a client, or be paid off.’ And, so, we’ve been going after the city’s top borrowers and saying, ‘Hey, we’re Peapack and this is what we could do for you. Give us a shot.’ ”

Most of those conversations are going well, Fingerman said: “Most people say, ‘It’s so good to hear from you,’ because they have personal relationships with me, with Andrew, with the staff that we brought on, with Peapack’s legacy staff.”

As such, Peapack’s pipeline is shaping up nicely. “It’s being

carefully managed to make sure that we’re getting the right loans, the right deposits, the right ratios,” Fingerman said.

Given that the run on regional banks a couple of years ago scared the bejeesus out of most, Peapack is focused on giving clients plenty of reassurance that their deposits are safe.

“We made the strategic move when we came into New York to lead the discussion and take any angst off the table around ‘Who is Peapack and how stable are you?’ ” Corrado said. “So, even though our balance sheet and capital ratios are some of the highest in the country and we’re one of two or three banks in the country that have a Moody’s investment-grade rating, our clients need to be able to rest at night and go to sleep knowing that the monies that they’ve invested are safe.”

As such, Peapack leads with a product called ICS — essentially a reciprocal arrangement where deposits are held with other FDIC banks across the country in order to pass through the FDIC coverage.

“Customers aren’t capped at $250,000 [in FDIC insurance coverage] — there’s up to, I think, $220 million that they could be covered for in today’s environment, based upon the number of participants across the country,” Corrado said. “It’s a cost to us, but we bear that cost because we felt it was the right thing to do from a business perspective, to give those clients peace of mind, and, you know, as part of our entree into New York.”

As Peapack works to fill the lending void Signature and First Republic left behind, Fingerman knows he has a long road ahead as the bank establishes a longer track record and more familiarity in New York, but he’s just getting started.

“I was at Signature for 16 years, and that platform wasn’t built overnight,” he said. “It was constant work and we went through several market highs and lows, but we were there for our clients. We want to have that same lender-borrower relationship here.”

MAKING THE BAND: (From left) Andrew Corrado, Doug Kennedy and Joseph Fingerman at Peapack’s 300 Park Avenue offices.

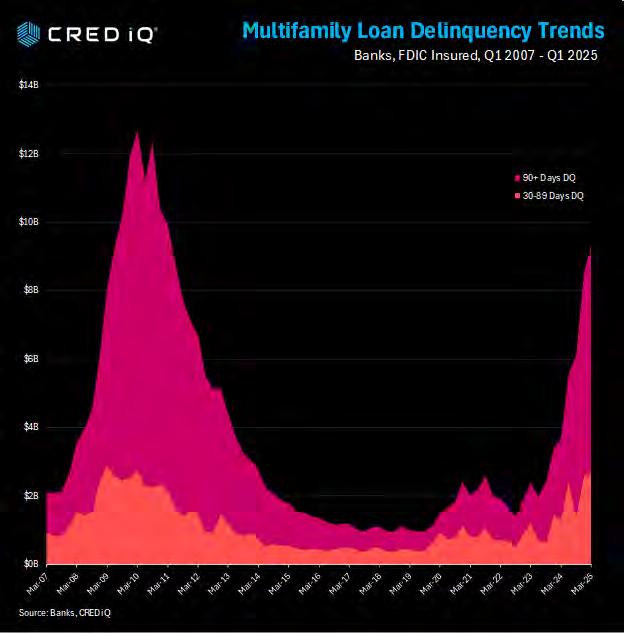

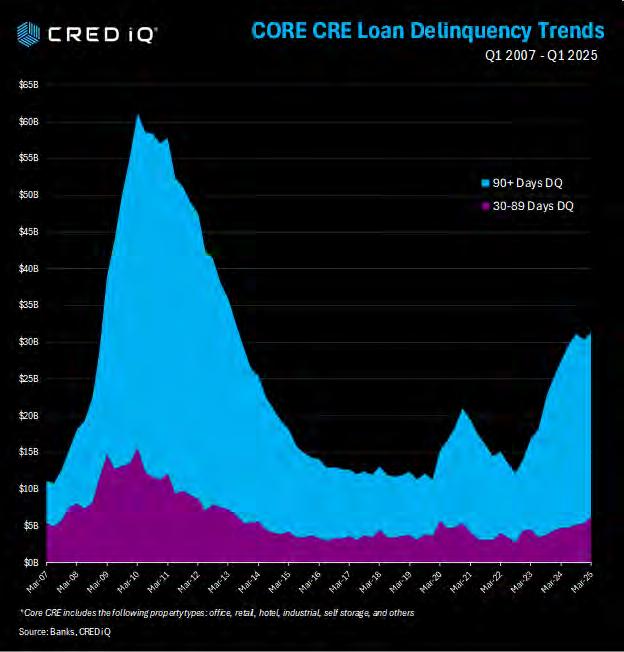

Chart Finance

Tracking Delinquency Trends From the GFC to Q1 2025

By Mike Haas

At CRED iQ, our mission is to provide commercial real estate professionals with the data and insights needed to navigate an ever-evolving market. This week, our research team took a deep dive into loan delinquency trends, expanding our lens from the Global Financial Crisis (GFC) to the present day. By focusing on FDIC-insured commercial banking and savings institutions, which includes community banks, we’ve uncovered critical patterns in CRE loan performance, offering a clearer perspective on today’s marketplace.

Two key segments and what they tell us

Our analysis spans from March 2007 to March 2025, shifting focus from securitized and agency markets to FDIC-insured institutions. We examined two key segments: multifamily properties and “core” CRE, which includes office, retail, hotel, industrial, self-storage and other property types.

This approach builds on our earlier research, providing a comprehensive view of delinquency trends and their implications for the CRE industry.

Key findings from Q1 2025

Our analysis revealed several trends in loan performance:

• Core CRE lending growth slows: The long-term average annual growth rate for core CRE lending balances is 4.55 percent. The first quarter of 2025, however, saw an annualized growth rate of just 1.22 percent, the lowest since 2012, signaling a cautious lending environment.

• Core CRE delinquencies rise: Total delinquencies across core property types reached $31.4 billion in Q1 2025, equating to a 1.7 percent overall delinquency rate. Of this, $25.1 billion are loans 90-plus days delinquent, while $6.3 billion are 30 to 89 days delinquent.

• Net losses decline for core CRE: Net losses in the core sector totaled $3.9 billion in Q1 2025, down from $5.9 billion in the prior quarter, suggesting some stabilization.

• Multifamily losses peak: Multifamily properties reported net losses of $767 million in Q1 2025, the highest quarterly total

since 2012, highlighting growing challenges in this sector.

Comparing March 2020 to March 2025

To contextualize recent trends, we compared delinquency metrics from March 2020 to March 2025:

• Multifamily delinquencies surge: Delinquent loan balances in the multifamily sector grew from $1.5 billion (0.3 percent delinquency rate) in 2020 to $9.4 billion (1.5 percent) in 2025. Loans 90-plus days delinquent increased dramatically, from $560 million to $6.71 billion.

• Core CRE delinquencies double: Delinquent loan balances in the core segment rose from $15.4 billion (1 percent) in 2020 to $31.4 billion (1.7 percent) in 2025, with 90-plus day delinquencies climbing from $9.7 billion to $25.1 billion.

These shifts underscore the increasing pressures on CRE loan performance, particularly in the multifamily sector, where rising delinquencies and losses signal heightened risk.

Mike Haas is the founder and CEO of CRED iQ.

CREDIQ

More banks are tapping the equity in their branch locations

By Jeff Ostrowski

alk about branching out. SouthState Bank grabbed headlines earlier this year when it agreed to a saleleaseback of 165 of its branches across the Southeast for $467 million, and it’s not alone. In a structure typically more common for industrial and logistics properties, banks are increasingly offloading their branches to third parties, and Florida-based SouthState executed the biggest such deal in recent memory.

“We’ve looked at this type of transaction several times over the years, and felt like the stars aligned now,” John Corbett, CEO of SouthState, said during an April earnings call.

When it comes to financial institutions tapping the equity locked up in their branch networks, the stars are aligning for others, too. According to an analysis by SLB Capital Advisors of New York, the pace of sale-leasebacks of bank branches has accelerated. SouthState’s deal alone outpaced the entire volume of bank sale-leasebacks in 2023 and 2024 combined.

Beyond SouthState, which is headquartered in Winter Haven, Fla., and has $65 billion in assets, Harborstone Credit Union of Tacoma, Wash., also this year closed on a sale-leaseback totaling $79.3 million. SLB Capital Advisors points to half a dozen other institutions around the country that have executed smaller deals.

So, why the sudden popularity of sale-leasebacks?

The trend is driven by a combination of rising interest rates and midsize banks’ need for capital, said Stewart Riggs, principal at SLB Capital Advisors.

“It is a very attractive source of capital for banks and credit unions,” Riggs told Commercial Observer. “They can execute a sale-leaseback and put cash back on the balance sheet. The whole banking system is predicated on taking one dollar and lending out five — but you need the one dollar.”

Bankers have shifted their mindset around property ownership. While the best branches once were seen as prized possessions, bankers have begun to view physical locations differently, Riggs said.

“Bricks and sticks is not what drives the profitability of a branch,” he said. “It’s the people inside the location.”

Other companies with retail locations long have done sale-leasebacks, and bankers are coming around to the benefits of an asset-light strategy.

“They need real estate, but they don’t need to own it,” said Tzvi Rokeach, partner at New York law firm Herbert Smith Freehills Kramer. “In my mind, this is the perfect asset for a sale-leaseback transaction. I would not be surprised if there were more.”

Another factor driving deals: Despite the fading importance of bank branches for everyday transactions, the locations remain in favor among investors, said Andrew Sandquist, vice chairman at Newmark in Chicago.

“Today, bank branches are quite valuable,”

Sandquist said. “Bank branches are viewed favorably by investors, so the timing is good for banks to do these transactions.”