• In June, the National Bank of Hungary maintained its benchmark interest rate at 6 50% for the ninth straight meeting, matching market forecasts. This decision signals a continued cautious approach, given that inflation remains near the upper threshold of the bank’s target range

• Hungary’s annual inflation rate edged up to 4.6% in June 2025 from 4.4% in May, aligning with market expectations This was the highest level since March, mainly due to rising prices for food, as well as electricity, gas, and other fuels. In contrast, core inflation which excludes volatile components like food and energy fell to 4 4%, marking its lowest level in seven months.

• In May 2025, the volume of construction output was 3.6% higher than a year earlier based on raw data, and 5 5% higher when adjusted for working days. Among the main construction groups, the output of building construction decreased by 9.3%, while that of civil engineering works increased by 26 0% Based on seasonally and working-day adjusted indices, construction output was 2.5% higher than in April 2025.

• In May 2025, the volume of industrial production was 2.6% lower than a year earlier. Most manufacturing subsectors experienced a decline; however, production volumes increased in the two largest-weight sectors: motor vehicle manufacturing (+6% yoy) and the manufacture of computer, electronic, and optical products (+1.1%). Based on seasonally and working-day adjusted data, industrial output was 1.3% lower than in April 2025.

• In May 2025, the volume of retail trade was 2.1% higher than in the same month of the previous year. Calendar-adjusted sale volumes expanded by 0.5% in specialized and non-specialized food shops, by 4.0% in non-food retailing and fell by 1.1% in automotive fuel retailing. According to seasonally and calendar adjusted data, the volume of retail sales was 1.3% down on the previous month. In January–May 2025, the volume of sales was 3.1% higher than in the corresponding period of the previous year.

• As of July 22, Hungary’s 10-year government bond yield was 7.06%, reflecting a stable base rate environment amid continued market uncertainty.

• European natural gas futures rose to €34/MWh on 07. 21, amid new EU sanctions on Russian oil, potential U.S. tariffs, and stabilizing Asian LNG demand Improved Norwegian supply and strong German wind forecasts are easing pressure, while flexible EU storage targets reduce competition for LNG.

• Brent crude oil futures fell to around $68 3 per barrel on 07 22, extending losses for a third straight session amid growing concerns over global demand. Uncertainty around EU–US trade negotiations ahead of the August 1 deadline, when President Trump has threatened 30% tariffs on EU exports, is weighing on sentiment The EU is also preparing retaliatory measures in case talks fail On the supply side, pressure is mounting as OPEC+ continues to unwind production cuts, with Saudi Arabia’s crude exports hitting a threemonth high in May. Meanwhile, Iran announced it will resume nuclear talks with European powers, aiming to revive the 2015 deal and avoid renewed international sanctions.

• ECB officials delivered an eighth consecutive rate cut in June to support inflation expectations and avoid financial tightening, amid ongoing global uncertainty and trade tensions. ECB stressed the need for flexibility and avoided firm forward guidance A pause in July is now likely, as most officials prefer to wait for clearer data. Inflation is expected to dip below the 2% target later this year and stay low into 2026, driven by a strong euro, cheaper energy, and low-cost Chinese imports Markets now anticipate just one more cut in 2025, with possible tightening in late 2026.

• Eurozone inflation was confirmed at 2% yoy in June 2025, slightly up from May’s 1.9% and matching the ECB’s target. Services inflation edged higher to 3 3%, while the drop in energy prices slowed to 2.6% from 3.6%. Core inflation held steady at 2.3%, its lowest since January 2022.

• Germany’s industrial production rose by 1.2% in May 2025, outperforming expectations and rebounding from April’s 1 6% decline The increase was led by strong gains in automotive sector (4.9%), pharmaceuticals (10.0%), and energy (10.8%). On an annual basis, output grew 1.0%, marking a turnaround from April’s 2.1% drop and indicating a modest recovery in the manufacturing sector.

• U S annual inflation rose to 2 7% in June 2025, the highest since February and up from 2.4% in May, driven by rising food, transport services, and used car prices. Energy costs declined more slowly, with smaller drops in gasoline and fuel oil, while natural gas prices remained elevated. Inflation eased slightly for shelter and new vehicles. Monthly CPI rose 0.3%, the largest increase in five months. Core inflation ticked up to 2.9% annually, below expectations, while monthly core CPI rose 0 2%, also softer than forecast

• The U.S. unemployment rate dipped to 4.1% in June 2025 from 4.2% in May, beating expectations of a rise to 4.3% and maintaining a year-long range of 4.0%–4.2%, indicating labour market stability However, the labour force shrank by 130,000, pushing the participation rate down to 62.3%, the lowest since December 2022. The employmentpopulation ratio remained at 59.7%, the weakest since January 2022. The broader U-6 jobless rate which includes discouraged workers and those employed part-time for economic reasons edged down to 7 7% from 7 8%

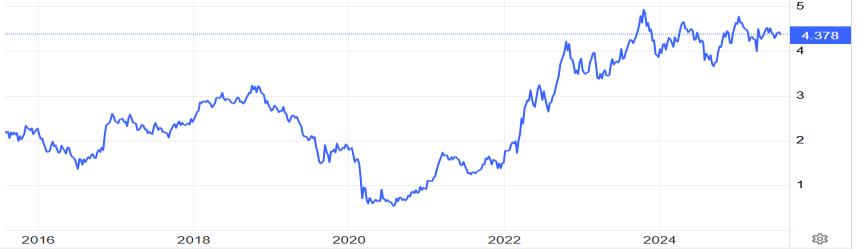

• The U.S. 10-year Treasury yield held steady around 4.37% on 07.22 after four days of declines, as investors stayed cautious ahead of the August 1 trade deal deadline. Treasury Secretary Scott Bessent emphasized that deal quality matters more than timing, leaving open the possibility of deadline extensions. Markets are also watching for comments from Fed Chair Jerome Powell for hints on rate policy, as President Trump continues to push for rate cuts, though markets have not fully priced in a move this month.