Редакционнаяколлегия

UDK 004

Ponomarev Evgenii bachelor’s degree, National Research Lobachevsky State University of Nizhny Novgorod Russian Federation, Nizhny Novgorod

ANALYSIS OF THE IMPACT OF USING MOBILE APPLICATIONS FOR BILL PAYMENTS ON THE TIMELINESS OF PAYMENTS AND FINANCIAL DISCIPLINE OF USERS

Abstract: This article examines the influence of mobile payment applications on the timeliness of bill payments and financial discipline among users. It explores how automatedfeaturesandreal-timefinancialmanagementtoolsenhanceuserengagement with financial responsibilities. The study considers various behavioral and technological factors that contribute to effective financial governance through mobile platforms.

Keywords: Mobile payments, financial discipline, bill management, user behavior, financial technology, payment automation.

INTRODUCTION

The ability to quickly pay bills, transfer funds, and conduct other operations enhances the timeliness of bill payments. This is important not only for preventing late payments and penalties but also for maintaining healthy financial discipline, which is essential for long-term financial stability.

The objective of this study is to analyze the impact of mobile payment applications on the timeliness of bill payments and the financial discipline of users. Theresearchexploresthetheoreticalaspectsoftechnologyadoptionandthebehavioral consequences for individuals.

MAIN PART. THEORETICAL FRAMEWORK

The study of digital payments and their impact on financial behavior is grounded inseveralestablishedtheories.Onefoundationaltheoryisthe TechnologyAcceptance Model (TAM), developed by Fred Davis in 1989. TAM explains how users come to accept and use technology by highlighting perceived ease of use and perceived

usefulness as primary factors influencing an individual's decision to adopt a new technology. In the context of mobile payment applications, these factors translate to the convenience and efficiency perceived by users, which drive their adoption and continueduse.TheUnifiedTheoryofAcceptanceandUseofTechnology (UTAUT), proposed by Viswanath Venkatesh et al. in 2003, expands on TAM by incorporating social influence and facilitating conditions, which also play significant roles in the adoption of digital payments.

Behavioral economics provides another critical lens through which the impact of digitalpayments on financialbehaviorcanbeunderstood.DanielKahnemanand Amos Tversky's Prospect Theory, introduced in 1979, suggests that individuals make financial decisions based on perceived gains and losses rather than absolute outcomes. Mobile payment applications, by offering immediate feedback and easy access to financial information, can alter these perceptions and influence financial behaviors. The ease of tracking expenses and the visibility of financial transactions provided by these applications can lead to more informed and disciplined financial decisionmaking.

Financial discipline is a concept closely related to consumer behavior and is essential for understanding the implications of mobile payment applications. Albert Bandura’s Self-Regulation Theory posits that individuals’ ability to regulate their behavior in alignment with long-term goals is crucial for maintaining financial discipline. Mobile payment applications support self-regulation by offering tools such as expense tracking, budgeting features, and reminders for due payments, which help users align their immediate financial actions with their long-term financial goals.

Consumer behavior theories, such as the Theory of Planned Behavior (TPB), developedby IcekAjzenin1991,suggeststhatintention,attitudetowardsthebehavior, subjectivenorms,andperceivedbehavioralcontrolaredeterminantsofanindividual’s actions. In the realm of mobile payments,users’ attitudes towards digital transactions, the influence of peers and societal norms, and their confidence in using the technology effectively shape their financial behaviors. Furthermore, Richard Thaler and Cass Sunstein’s concept of nudging, derived from behavioral economics, is relevant.

Nudging involves subtly guiding individuals towards desirable behaviors without restricting their freedom of choice. Mobile payment applications can employ nudging techniques by providing timely reminders and alerts, thus encouraging timely bill payments and fostering better financial habits.

The integration of these theoretical perspectives provides a comprehensive framework for understanding how mobile payment applications influence financial behavior and discipline.

TECHNOLOGICAL ADVANCEMENTS AND THEIR IMPLICATIONS FOR FINANCIAL TRANSACTIONS

The advent of mobile payment applications marks a significant milestone in the evolution of financial transactions. This transformation began in the early 2000s with the development of pioneering technologies and has since grown into a vast industry led by major tech firms and innovative startups.

One of the earliest and most influential mobile payment systems was PayPal, founded by Max Levchin, Peter Thiel, and Luke Nosek in 1998. Initially launched as a web-based service, PayPal quickly adapted to the mobile platform, setting the stage for future mobile payment solutions. PayPal's success highlighted the potential of digital payments and paved the way for further innovations.

In 2011, Google introduced Google Wallet, later rebranded as Google Pay, which integrated near-field communication (NFC) technology to enable contactless payments. Google Pay's launch signified a crucial advancement, demonstrating how mobile devices could be used not just for online transactions but also for in-store purchases. Similarly, Apple introduced Apple Pay in 2014, leveraging its vast ecosystem of devices to popularize NFC-based mobile payments. Apple Pay, developed under the leadership of Eddy Cue, has been instrumental in promoting the widespread adoption of mobile payment technology.

Modern mobile payment applications offer a range of functionalities beyond simple transactions. Features such as peer-to-peer payments, integration with loyalty programs, expense tracking, and even investment options have become standard. For instance, Venmo, acquired by PayPal in 2014, has gained popularity in the USA for its

social payment features, allowing users to share and comment on transactions within a social feed.

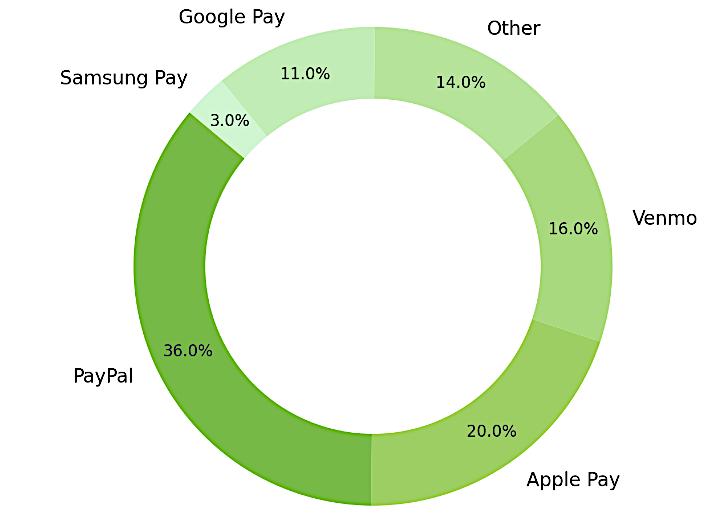

According to digital payment business statistics by Civic Science, the largest digital wallet in the USA in 2022 was PayPal (fig. 1).

Figure 1. Use of digital wallets in the USA, % [1]

The transaction value in the global digital payments market is projected to reach 11.55 trillion dollars in 2024. This figure will show an annual growth rate of 9.52%, leading to a forecasted total of 16.62 trillion dollars by 2028 [2].

According to experts, the leader in the overall ranking of payment services in Russia in 2023 was Sberbank, scoring 72.3 points. This is attributed to the high popularityofthebank'spaymentservicewithintheentrepreneurialcommunity.Similar results were shown by Tinkoff Kassa (68.6) and the payment service YooKassa (66.9). Therankingwasbased onimportant criteriaforevaluatingtheperformanceofpayment services: demand among individuals and entrepreneurs, the variety of payment methods offered to clients, technological features of the payment systems for easy integration and increased conversion on websites, the size of fees for various payment methods, connection speed, and the quality of customer support [3].

The implications of technological advancements for financial transactions are profound. Mobile payment applications enhance convenience and accessibility, allowing users to make payments anytime and anywhere. This flexibility has led to increased consumer engagement with digital financial services. The integration of mobile payments with other financial services, such as budgeting tools and investment

platforms, promotes better financial management and discipline among users. Applications like Mint and YNAB (You Need A Budget) provide comprehensive financial overviews, helping users track spending and plan for future expenses.

Mobile payment applications contribute to financial inclusion by providing services to unbanked and underbanked populations. In regions with limited access to traditional banking, mobile payment solutions offer a viable alternative for managing finances. M-Pesa, launched by Vodafone in Kenya in 2007, is a notable example, providing mobile-based financial services to millions of users who previously had no access to banking.

As the industry continues to innovate, mobile payment applications are poised to play an increasingly central role in the global financial ecosystem, driving further advancements in financial technology and consumer behavior.

USER ADOPTION AND BEHAVIORAL CHANGES

The adoption of mobile payment applications has induced significant behavioral changes among users. They are driven by the unique features andconveniences offered bymobilepaymenttechnologies,whichalterhowindividualsperceiveandengagewith their financial activities.

One of the most notable behavioral changes is the increased frequency and convenience of transactions. Mobile payment applications enable users to make payments quickly and effortlessly [4]. Users no longer need to carry cash or physical credit cards, reducing the friction associated with traditional payment methods. The ability to complete transactions with a simple tap or scan has led to a shift towards a cashless society, where digital payments are preferred for everyday purchases.

Mobile payment applications offer users greater visibility into their financial activities, allowing them to track their spending patterns and identify areas where they can save money. This increased transparency fosters a sense of control over personal finances, encouraging users to adopt more disciplined financial behaviors. For example, users can set spending limits, categorize expenses, and receive alerts for upcomingbillpayments,helpingthemavoidlatefeesandmaintainfinancialdiscipline.

The social aspect of mobile payment applications has also influenced user behavior. Platforms like Venmo and WeChat Pay incorporate social features that allow users to share and comment on transactions. This social interaction around financial activities has led to the emergence of new social norms and behaviors. For instance, splitting bills and sharing expenses among friends has become more streamlined, reducing potential conflicts and enhancing social cohesion.

Mobile payment applications have also contributed to the growth of contactless and remote transactions. The COVID-19 pandemic accelerated the adoption of contactless payments as a safer alternative to cash and card transactions. This shift has led to a long-term change in consumer behavior, with many users continuing to prefer contactless payments even as restrictions ease. The convenience and perceived safety of mobile payments have reinforced their use, further entrenching them in daily financial activities.

INFLUENCE ON TIMELY PAYMENTS

The influence of mobile payment applications on the timeliness of bill payments is substantial, with recent advancements and practices significantly contributing to improved financial discipline.

In the USA, PayPal simplifies the payment process through automatic payments for recurring bills, ensuring they are always paid on time without user intervention. It also keeps users informed with reminders and notifications about upcoming bills, which helps in avoiding late fees. The app's design for one-tap payments minimizes the steps involved, enabling users to clear their dues swiftly and efficiently. PayPal offers flexibility in funding sources, allowing users to link multiple bank accounts, credit cards, and maintain a PayPal balance to ensure funds are always available for payments. The mobile accessibility of PayPal means that users can manage and pay their bills anytime and from anywhere, which is crucial for maintaining timely payments.PayPal employs strategic initiatives to enhance its investment attractiveness in the USA market, focusing on expanding its digital payment services and enhancing security measures. These strategies aim to attract a broader customer base and foster

trust, contributing to PayPal's robust financial performance and appealing to potential investors [5].

Cash App, developed by Block, Inc. (formerly Square, Inc.), has seen significant adoption and growth. Cash App, launched in 2013, now includes a variety of features aimed at enhancing financial management. In 2022, Cash App introduced the ability to set up recurring payments and receive reminders for upcoming bills. These features ensure that users can automate their bill payments and receive timely notifications, reducing the likelihood of missed payments. Additionally, Cash App's integration with investment options and Bitcoin trading provides users with a comprehensive financial management tool. As the American manufacturing sector enters a new era characterized by reorganization, risk assessment, and profit analysis, digital financial services like Cash App can play a significant role. By providing innovative payment solutions and fostering financial inclusion, Cash App can help streamline transactions and financial management for businesses adapting to these new manufacturing landscapes [6].

In Russia, Sberbank's app integrates a direct bill payment system that allows users to pay for utilities, taxes, and other services effortlessly within the banking environment. This seamless integration ensures that payments are made promptly. Scheduled payments further automate the process, where the bank handles transactions on predetermined dates, reducing the risk of late payments. Sberbank's app is designed to keep users well-informed with real-time alerts for due bills and provides a comprehensiveviewofallupcomingpayments,whichaidsinbetterfinancialplanning.

Tinkoff, a digital bank founded in 2006, has become a leading provider of financial services. Tinkoff's mobile app offers a wide range of features designed to enhance the timeliness of bill payments. Users can set up automatic payments for utilities, loans, and other recurring expenses. The app provides detailed spending analytics and sends reminders for due payments, ensuring users are aware of their financial obligations. Tinkoff's «Early Salary» feature allows users to access their wages ahead of the scheduled payday, providing liquidity to cover bills promptly.

PROSPECTS FOR THE DEVELOPMENT OF MOBILE APPLICATIONS IN THE FINANCIAL SECTOR

The future development of mobile applications in the financial sector promises to bring significant advancements, driven by technological innovations and evolving user needs (table 1).

Table 1. Prospects for the development of mobile applications in the financial sector [7,8]

Prospect Description

Cybersecurity enhancements

Integrationof neuralnetworks

Blockchain technology

Openbanking

Implementationofadvanced encryption,biometricauthentication, andreal-timefrauddetectionsystems

UtilizationofAIandmachine learningforpersonalizedfinancial advice,predictiveanalytics,and automatedcustomerservice

Adoptionofblockchainforsecure, transparent,andefficienttransactions

Collaborationbetweenbanksand fintechcompaniestoprovide integratedfinancialservicesthrough openAPIs

Impact on Financial Sector

Ensuresuserdataprotection, buildstrust,andmitigatesrisksof cyber-attacks

Enhancesuserexperience, improvesdecision-making,and increasesoperationalefficiency

Reducesfraud,ensures transparency,andfacilitatesfaster cross-bordertransactions

Offersmorepersonalizedand comprehensivefinancialproducts, promotesinnovation,and enhancescompetition

Financial Inclusion

Enhanceduser interfaces(UI)

Developmentofapplicationsaimed atprovidingfinancialservicesto underservedpopulations

Designimprovementsfocusingon user-friendlyinterfacesandintuitive navigation

Sustainable finance Integrationoffeaturesthatpromote sustainableinvestingand environmentallyconsciousfinancial decisions

Expandsaccesstobanking services,reducesfinancial inequality,andfosterseconomic development

Increasesuserengagement, improvesaccessibility,and enhancesoverallusersatisfaction

Encouragesresponsibleinvesting, supportsgreeninitiatives,and alignsfinancialpracticeswith sustainabilitygoals

From the author's perspective, the expansion of functionality and improvement of userinterfacesin mobileapplicationsforbillpaymentscontinuetoattractan increasing number of users, while ensuring a high level of convenience and security. The integration of advanced technologies such as artificial intelligence, blockchain, and big data opens new opportunities for personalization and enhancing the efficiency of operations. Strengthening security measures and compliance with regulatory requirements remain important aspects that require ongoing attention from developers.

CONCLUSIONS

The analysis of mobile payment applications delineates their substantial role in enhancing the punctuality of bill settlements and fostering financial discipline among users. These applications integrate automation of transactions, timely alerts, and comprehensive budgeting tools, which collectively contribute to effective financial management. The capability of these platforms to provide immediate access to financial services, alongside the flexibility of managing finances remotely, significantly aids users in adhering to their financial obligations. The provision of realtime financial visibility empowers users, promoting a disciplined approach to financial decision-making. The continued evolution of these applications suggests a promising trajectory for further innovations in financial technology, with potential to extend even more robust support and functionalities to users globally.

REFERENCES

1. PayPal Leads Among Digital Wallet Adoption, But Cash Stays Relevant // Civic Science URL: https://civicscience.com/paypal-leads-among-digital-walletadoption-but-cash-stays-relevant/ (date of application: 04.04.2024)

2. Digital Payments – Worldwide // Statista URL: https://www.statista.com/outlook/dmo/fintech/digital-payments/worldwide (date of application: 10.04.2024)

3. Rating of Payment Services in Russia 2023 // RBC URL: https://marketing.rbc.ru/articles/14332/ (date of application: 05.04.2024)

4. Ali A., Hameed A., Moin M.F., Khan N.A. Exploring factors affecting mobile-banking app adoption: a perspective from adaptive structuration theory // Aslib Journal of Information Management 2023. Vol. 75 No. 4, pp. 773-795. https://doi.org/10.1108/AJIM-08-2021-0216

5. Abdullina L., Bobovnikova A., Zrazhevskiy A. ESG-factors and CSRstrategy impact on the investment attractiveness of usa companies // Proceedings of the XLIII International Multidisciplinary Conference «Recent Scientific Investigation». Primedia E-launch LLC. Shawnee, USA. 2023.

6. Kudrenko I.The neweraofAmerican manufacturing: evaluating the risks and rewards of reshoring // E3S Web of Conferences. EDP Sciences, 2024. 2024. Vol. 471. P. 05020.

7. Kudrenko I. Adoption of Blockchain in Critical Minerals Supply Chain Risk Management // International Journal of Information Systems and Supply Chain Management (IJISSCM). 2024. Vol. 17. No. 1. P. 1-26. http://doi.org/10.4018/IJISSCM.342118

8. Taherdoost H. Fintech: Emerging Trends and the Future of Finance. In: Turi, A.N. (eds) Financial Technologies and DeFi. Financial Innovation and Technology. Springer, Cham. 2023. P. 29-39. https://doi.org/10.1007/978-3-031-17998-3_2

предсказательной

тенденции.Этастатьяисследует,каккомпаниииспользуютбольшиеданныедля улучшения взаимодействия с клиентами

слова

предсказательная аналитика, поведение

Naianzin Anton co-founder and Chief Marketing Officer, A&K American Educational Consulting USA, Miami

THE ROLE OF BIG DATA IN DIGITAL MARKETING: FROM PERSONALIZATION TO PREDICTIVE ANALYTICS

Abstract: In the era of digitalization, big data plays a key role in shaping marketing strategies. From content personalization to predictive analytics, big data helps brands not only adapt to consumer behavior but also forecast future trends. This article explores how companies use big data to enhance customer interaction and optimize marketing efforts.

Keywords: Big data, digital marketing, personalization, predictive analytics, consumer behavior.

[1].

● В исследовании Chen, M. & Liu, X. (2021) изучает,

● Статья Turner, J. & Shah, R. (2022) изучает

●

Kim, Y. & Park, H. (2023

Alvarez, R. (2022)

● В работе Baker, S. & White, G. (2021) обсуждают

[5].

● Авторы Li, F. & Zhu, L. (2022) как большие

стратегиивзаимодействияивовлечениявсфереонлайн-брендинга,подчеркивая изменения

[6].

● Исследование Greenwood, S. & Scharf, R. (2023) рассматривает различные инструменты

операционную эффективность [7].

● Статья Patel, A. & Kumar, U. (2021) исследует,

большие

продуктов, от идеации до запуска на рынок [8].

● Исследование Thompson, J. & Cheng, Z. (2023) представляет

кейс-стади, демонстрирующий, как

способствовать улучшению

маркетинговые кампании [9]

● Авторы Brown, J. & Lee, K. (2021) описывают, как розничная

и повышения конверсии [10].

● Исследование Hamilton, F. & Carter, S. (2022) показывает, как компанияуспешноинтегрировалаанализбольшихданныхсоциальныхсетейдля

● Singh, A. & Gupta, N. (2021)

●

Morris, L. & Richardson, T. (2022)

● Поведенческие данные: Взаимодействия пользователей с рекламными и образовательными материалами, включая клики, просмотры и время,проведенное на сайте.

● Демографические данные: Информация о возрасте, поле, географическом расположении

● Транзакционные данные: Записи

консультации, которые помогают

рекламных кампаний на 32%, что на 12% выше среднего показателя, отмеченного в исследовании Chen &Liu (2021) [1].

● Конверсия в продажи

вработе Turner & Shah (2022) [2].

2. Применение предсказательной аналитики: ● С помощью разработанных

(2021) [8].

1.

Chen & Liu (2021),

значительное улучшение взаимодействия [1].

2. Преимущества предсказательной аналитики. Результаты

Kim & Park (2023), которые указывают

1. Персонализация:

● Внедрение аналитики

рекламных кампаний на 32%, что

улучшения на 20%, описанный висследовании Chen &Liu (2021) [1].

● Улучшенная персонализация привела к повышению

продажина27%,превосходястандартныепоказатели,упомянутыеTurner&Shah (2022), на 7% [2].

2. Предсказательная аналитика:

● Разработанные модели предсказательной аналитики улучшили

планирование кампаний, что привело к увеличению ROI на 43%, значительно превышая улучшение на 28%,обсуждаемое Kim & Park (2023) [3]

● Эффективныестратегиипредотвращенияоттокаклиентовсократили

его на 23%, что на 10% лучше результатов, представленных

& Kumar (2021) [8]

Комментарии к другим

маркетинговых стратегий.

юридические риски. Практические рекомендации:

1. Инвестиции

1. Chen M., Liu X. Big Data in Digital Marketing: Enhancing Business Performance through Data Analytics // Journal of Marketing Analytics. 2021. Vol. 9. N. 3. P. 165-178.

2. Turner J., Shah R. The Impact of Big Data on Consumer Behavior: A Data-Driven Approach // International Journal of Consumer Studies. 2022. Vol. 46. N. 2. P. 324-340.

3. Kim Y., Park H. Predictive Analytics in Marketing: Leveraging Big Data for Strategic Advantage // Journal of Business Research. 2023. Vol. 139. P. 101-113.

4. Alvarez R. Utilizing Machine Learning for Enhanced Market Segmentation // Artificial Intelligence Review. 2022. Vol. 55. N. 3. P. 2075-2099.

5. Baker S., White G. Ethical Considerations in Big Data Marketing // Ethics and Information Technology. 2021. Vol. 23. N. 4. P. 591-606.

6. Li F., Zhu L. Big Data and Online Branding: Interaction and Engagement Strategies // Journal of Brand Management. 2022. Vol. 29. N. 1. P. 22-37.

7. Greenwood S., Scharf R. Data-Driven Decision Making in Marketing: Tools and Techniques for a Competitive Edge // Marketing Science. 2023. Vol. 42. N. 1. P. 88-105.

8. Patel A., Kumar U. Harnessing the Power of Big Data in New Product Development // Journal of Product Innovation Management. 2021. Vol. 38. N. 2. P. 142-159.

9. Thompson J., Cheng Z. Improving Customer Loyalty Through Big Data Analytics: A Case Study Approach // Journal of Consumer Marketing. 2023. Vol. 40. N. 2. P. 234-249.

10. Brown J., Lee K. Optimizing Customer Journey through Big Data Insights: A Retail Case Study // Journal of Retailing and Consumer Services. 2021. Vol. 58. P. 102-115.

11. Hamilton F., Carter S. Big Data and Social Media: Transforming Customer Engagement Strategies // Journal of Digital & Social Media Marketing. 2022. Vol. 10. N. 1. P. 76-89.

12. Singh A., Gupta N. Leveraging Big Data for Improving Product Launch Strategies // Journal of Product Innovation Management. 2021. Vol. 38. N. 3. P. 210230.

13. Morris L., Richardson T. Big Data in E-commerce: Enhancing User Experience and Operational Efficiency // Journal of Business Research. 2022. Vol. 133. P. 57-68.

аудитории и целей проекта. Описываются издательские параметры, формирование

внимание уделяется дизайну, рекламным стратегиям и планированию содержания номера. Рассматриваются

разработки концепции

иллюстраций.

Ключевые слова: Глянцевый журнал,

дизайн,реклама, редакционная деятельность.

Skvortsova Yana specialist’s degree, Kuban State University Russian Federation, Krasnodar

DEVELOPMENT OF A GLOSSY MAGAZINE CONCEPT: BASIC

PRINCIPLES AND GENRE FEATURES

Abstract: The article explores the process of developing a glossy magazine concept, including defining the genre direction, target audience, and project goals. Publishing parameters, the formation of a rubricator, and the features of internal content are described. Special attention is given to design, advertising strategies, and issue content planning. Creative, technical, and commercial aspects of editorial work are considered, as well as the importance of sociological research for creating an attractive and successful publication. The final stage of concept development includes cover and block design, balancing text and illustrations.

Keywords: Glossy magazine, publication concept, rubricator, design, advertising, editorial activity.

Важнымявляетсяикоммерческийуспехиздания.Правильноразработанная концепция, максимально выверенные

концепции и тематики журнала. К основным выходным сведениям

специалистов, действующих

редакционной коллегии издания.

ДЕЯТЕЛЬНОСТЬ РЕДКОЛЛЕГИИ НА

полосе.

разделительные

(Линии, рамки, пробелы, контуры и заливка, интерлиньяж, межстрочные интервалы, отбивка), фон

многообразное обличье

мелкихкеглей(по14включительно)называютсятекстовыми,начинаяс16кегля

Отметимтакже,чтокважнейшимэлементамиздания,формирующиммакет относятся: заглавная (титульная) часть издания (логотип и сопутствующие

компоненты) – обложка, обозначающая начало

Adobe InDesign, Corel

Окончательной

1. ВолковаВ.В., ГалкинС.И.,СитниковВ.П.Дизайнгазетыижурнала: учебное пособие: под ред. В.В. Волковой. М.: Аспект Пресс, 2003. С. 31.

2. Носаев Д. А. Дизайн периодической печати: учебное пособие. Краснодар: КубГУ, 2016. С. 41.

3. ГуревичС.М.ЭкономикаотечественныхСМИ:Учебноепособиедля вузов. М.: Аспект Пресс, 2004. 288 с.

4. Никулина И. А. Верстка, дизайн и допечатная подготовка в полиграфическом процессе: учебник. Краснодар: Кубанский гос. ун-т, 2010. С. 57

5. Кнабе Г. А. Энциклопедия дизайнера печатной продукции. Профессио-нальная работа. М: Издательский дом «Вильямс», 2006. С. 453.

6. Ныркова Л.М. Как делается газета: Практич. пособие. М.: ТОО «Гендальф»,1998. С. 18.

UDK 331.1

Kendjaev Amin PhD, Samarkand Medical Institute Uzbekistan, Samarkand

METHODS OF MOTIVATION AND PERSONNEL MANAGEMENT IN THE MULTICULTURAL ENVIRONMENT OF THE USA

Abstract: This article examines methods of motivation and personnel management in the multicultural environment of the USA. It analyzes the challenges and strategies for inclusive recruitment. The importance of cultural competency training is studied, highlighting its impact on team cohesion and performance. The effectiveness of different leadership styles in managing diverse teams is investigated. Explores how effective management practices can help companies create an inclusive and productive workplace.

Keywords: MC workforce, motivation, personnel management, recruitment, cultural competency, leadership styles, USA.

INTRODUCTION

The USA is known for its cultural diversity, which is reflected in its workforce. As globalization continues to shape business operations, companies are increasingly finding themselves navigating a multicultural (MC) environment. This is particularly evident in distribution companies, which play a crucial role in the logistics and supply chain sectors. The effectiveness of employee motivation and management within these companies significantly influences their operational success and competitive advantage.

In aMCworkforce,employeesbringdiverseperspectives,skills,andexperiences. While thisdiversity can be a source ofinnovation and creativity,it also presentsunique challenges in terms of communication, cultural differences, and varying motivational drivers.

The objective of this article is to explore the methods of motivation and management in the MC workforce of distribution companies in the USA. It will examine the processes of recruitment, training, and retention of employees.

MAIN PART. OVERCOMING CHALLENGES IN MC RECRUITMENT

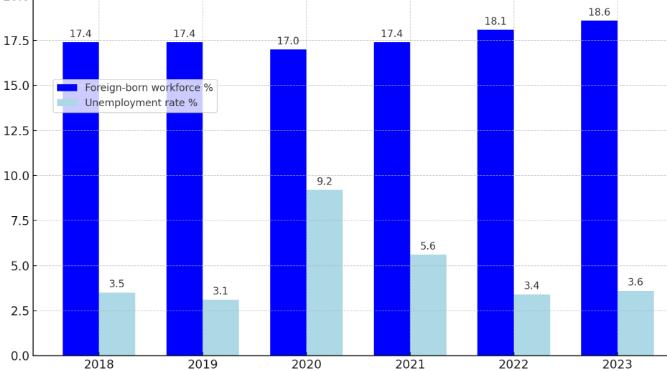

The USA is a MC country, characterized by a diverse population composed of various ethnicities, cultures, and languages. In 2023, foreign-born individuals made up 18,6% of the USA civilian labor force, compared to 18,1% in 2022 (fig. 1).

Figure 1. Number of foreign workers and unemployment rate in the USA, % [1] Hispanic citizens to constitute nearly half (47,6%) of the foreign-born workforce, while Asians accounted for a quarter. Foreignworkerswere most commonly employed in service occupations, natural resources extraction, construction, and maintenance roles;aswellasinproduction,transportation,andmaterialmoving sectors.Themedian usual weekly earnings of foreign-born full-time workers in 2023 were 987 dollars, compared to 1,140 dollars for their native-born counterparts [2].

Recruitment in a MC environment poses several challenges that can significantly impact the efficiency and inclusivity of the hiring process. One of the primary challengesis overcomingunconsciousbiases thatcan influencehiringdecisions.These biases often stem from cultural stereotypes and preconceived notions about candidates from different backgrounds, leading to a less diverse workforce. Language barriers and differing communication styles can hinder effective evaluation of candidates' qualifications and potential. A lack of understanding of cultural nuances can result in misinterpretation of behaviors and responses during interviews, further complicating the recruitment process.

Significant challenge is ensuring that the recruitment process is accessible and appealing to a diverse pool of candidates. To address these challenges, distribution companies can implement several strategies for inclusive recruitment:

•organizations should invest in training for hiring managers and recruiters to recognize and mitigate unconscious biases.

•employingastructuredinterviewprocesswithstandardizedquestionscanreduce the influence of personal biases and ensure that all candidates are evaluated based on the same criteria.

•broaden the recruitment channels to reach a more diverse candidate pool.

Companies should review their job descriptions and requirements to ensure they are inclusive and do not inadvertently exclude qualified candidates.

TRAINING AND DEVELOPMENT

Cultural competency training is crucial in a MC work environment, addressing the need for employees to effectively navigate and thrive in diverse cultural settings. Such training is essential for fostering an inclusive workplace, enhancing team cohesion, and improving overall business performance. By equipping employees with the necessary skills and knowledge, organizations can reduce cultural misunderstandings, promote better interpersonal interactions, and create a more harmonious and productive work environment (table 1)

Table 1. Methods of cultural competency training [3,4]

Aspect

Understanding andappreciation

Enhanced team cohesion

Better customer service

Personal and professional growth

Commitment to diversity and inclusion

Description

Helpsemployeesunderstandandappreciate diverse backgrounds and perspectives, reducing cultural misunderstandings and conflicts.

Fosters a harmonious and productive work environment by improving interactions and respectamongemployees.

Enhances the ability to serve a diverse customer base by understanding cultural preferences and dietary restrictions, leading tohighercustomersatisfactionandloyalty.

Encourages open-mindedness, adaptability, and empathy, driving innovation and problem-solvingwithinteams.

Demonstrates the company’s dedication to diversity, enhancing its reputation and attractivenessasanemployer.

Methods

Workshops on cultural awareness, cross-cultural communication training, interactiveseminars.

Team-building activities, roleplaying exercises, intercultural dialoguesessions.

Customer service training focused on cultural sensitivity, scenario-based training, feedbacksessions.

Diversity training programs, mentoring, and coaching from diverse leaders, cultural immersionprojects.

Regular DEI (Diversity, Equity, Inclusion) workshops, inclusive leadership training, policyreviews.

Improved employee retention Creates an inclusive environment where employees feel valued and respected, leading to higher job satisfaction and retentionrates.

Competitiveedge Providesbettercustomerserviceandfosters innovation, givingcompaniesacompetitive edgeinthemarket.

Costsavings Improves employee retention, reducing turnover costs and contributing to operationalstability.

Continuous learning opportunities, inclusive workplace policies, employee resourcegroups.

Innovation labs, crossfunctional teams with diverse members,marketanalysisfrom diverseperspectives.

Regular assessment and feedback mechanisms, comprehensive onboarding programs,retentionstrategies.

From the author's perspective, cultural competency is an important component of successfully managing a MC work environment. Cultural competency not only fosters harmonious and productive interpersonal interactions but also plays a key role in enhancing customer service quality, stimulating innovation, and improving employee retention. Effectively implementing methods of cultural competency allows organizations to create an inclusive work environment where all employees feel valued and respected.

FACTORS AFFECTING EMPLOYEE ENGAGEMENT IN MC TEAMS

Employee engagement in MC teams is influenced by various factors that can either enhance or hinder the overall productivity and satisfaction of employees. These factors include:

•Cultural awareness and sensitivity: employees who feel that their cultural background is understood and respected are more likely to be engaged. Cultural awareness training helps in building this understanding, which in turn fosters a sense of belonging and acceptance [5].

•Communication styles: effective communication is crucial for engagement. MCteamsoftenfacechallengesduetodifferentcommunicationstyles,includingdirect versus indirect communication, high-context versus low-context communication, and varying preferences for verbal and non-verbal communication.

•Leadershipapproach:inclusiveleadershipthatvaluesdiversityandencourages open dialogue is essential. Leaders who demonstrate cultural competence and

adaptability can significantly enhance employee engagement by creating an environment of trust and respect.

•Recognition and appreciation: regular and culturally sensitive recognition of employees’ contributions can boost morale and engagement. Employees feel valued when their work is acknowledged in ways that are meaningful to them culturally.

•Career development opportunities: Providing equitable access to career advancement and professional development opportunities is vital. Employees are more engaged when they see a clear path for growth within the organization.

Retention of employees in a MC work environment requires strategies that address the diverse needs and expectations of the workforce. Fostering an inclusive organizational culture where diversity is celebrated, and everyone feels they belong is crucial. This involves not only policies and practices that promote inclusion but also everyday interactions and behaviors that reinforce it.

Establishing mentoring programs and support networks for employees from diverse backgrounds can help them navigate the organizational culture and advance theircareers [6].Theseprogramsprovideguidance,support,andasenseofcommunity, which are important for retention.

Ensuring that all HR practices, including recruitment, promotion, and compensation, are fair and transparent helps in building trust. Employees are more likely to stay when they perceive fairness and equity in the workplace. Providing ongoing training and development opportunities that cater to the diverse needs of employees helps in retaining talent. This includes cultural competency training, leadership development programs, and skill enhancement workshops.

Regular engagement surveys and feedback mechanisms can help organizations understand the needs and concerns of their employees. Acting on this feedback shows that the organization values its employees' input and is committed to continuous improvement [7].

Employee engagement in MC teams is influenced by various factors that either enhance or hinder productivity and satisfaction. Retaining employees in a MC team requires fostering an inclusive organizational culture, establishing mentoring

programs, ensuring fair HR practices, providing ongoing training, and implementing regular engagement surveys. These strategies collectively create a supportive and engaging work environment, enhancing employee commitment and reducing turnover.

ROLE OF LEADERSHIP AND MANAGEMENT

Different leadership styles can have varying impacts on team cohesion, motivation, and performance. In MC settings, leaders must navigate a complex landscape of diverse cultural norms, communication styles, and expectations.

Transformational leadership, characterized by the ability to inspire and motivate employees, is particularly effective in MC teams. This leadership style encourages innovation and creativity by promoting a culture of trust and collaboration [8]. In MC settings, transformational leaders can bridge cultural gaps by emphasizing common goals and values, thereby enhancing team cohesion and overall performance.

Transactional leadership relies on rewards and penalties to motivate team members, providing a clear framework for performance. While it may not foster the same level of intrinsic motivation as transformational leadership, transactional leadership can offer stability and clarity, which are valuable in managing culturally diverse teams. It is crucial for transactional leaders to be culturally sensitive when applying rewards and penalties to ensure they are perceived as fair and equitable by all team members.

Laissez-faire leadership, which involves a hands-off approach, allowing team members to make decisions independently, can be challenging in MC teams. This style assumes a high level of autonomy and self-motivation among employees, which may not align with the expectations and work habits of all cultural groups. In MC settings, laissez-faire leadership can lead to confusion and a lack of direction, negatively impacting team performance. It is generally less effective in managing diverse teams unless supplemented with strong support and communication structures

Democratic leadership, which involves participative decision-making, is highly effective in MC teams. This style values the input and perspectives of all team members, fostering a sense of ownership and engagement. By encouraging open

dialogue and inclusive decision-making, democratic leaders can harness the diverse insights and experiences of a MC teams, leading to better problem-solving and innovation. This approach also promotes a culture of respect and equality, which is crucial for maintaining high morale and commitment in diverse teams.

The effectiveness of leadership styles in MC teams depends on the ability of leaders to adapt and respond to the diverse needs of their team members. Transformational, democratic, and servant leadership styles tend to be more effective in fostering an inclusive andcollaborativeenvironment. Transactional and laissez-faire leadership styles may require additional cultural sensitivity and support mechanisms to be effective. Successful leadership in MC settings hinges on the leader’s cultural competence and commitment to promoting diversity and inclusion.

CONCLUSIONS

The study of methods of motivation and personnel management in the MC environment of the USA highlights several critical insights. Effective recruitment in a diverse workforce requires strategies to mitigate unconscious biases, ensure inclusivity, and broaden recruitment channels. Cultural competency training is essential for fostering an inclusive workplace, enhancing team cohesion, and improving overall performance. Various leadership styles, such as transformational, democratic, and servant leadership, prove effective in managing MC teams by promoting inclusivity and collaboration. Successful management in MC settings hinges on cultural competence and a commitment to diversity and inclusion.

REFERENCES

1. Gross Domestic Product, Fourth Quarter and Year 2023 / Bureau of Economic Analysis USA Department of Commerce // URL: https://www.bea.gov/news/2024/gross-domestic-product-fourth-quarter-and-year2023-advance-estimate (date of application: 15.06.2024)

2. GVR Report cover USA Packaged Food Market Size, Share & Trends Analysis Report By Product / Grand View Research // URL: https://www.grandviewresearch.com/industry-analysis/us-packaged-food-market (date of application: 16.06.2024)

3. Bukhtueva I. Enhancing Customer Experience with AI-Powered Personalization Techniques // Innovacionnaya nauka. 2024. № 4-1. P. 114-119.

4. Gareev I.F., Valiullin A.A., Gubeev E.P., Khakimova T.S., Farkhullin R.R., Semko D.V., Potapov I.V., Volkov V.S. Development of measures to activate the territories of historical settlements // Russian Journal of Housing Research. 2023. Vol. 10. N. 4. P. 403-424. doi: 10.18334/zhs.10.4.119968

5. Lee J. Foreign lobbying through domestic subsidiaries // Economics & Politics. 2024.Т. 36. №. 1. P. 80-103.

6. Federal income tax rates and brackets / IRC // URL: https://www.irs.gov/filing/federal-income-tax-rates-and-brackets (date of application: 18.06.2024)

7. Minimum Wage U.S. / USA DEPARTMENT OF LABOR // URL: https://www.dol.gov/general/topic/wages/minimumwage (date of application: 19.06.2024)

8. Fogleman V. Environmental liabilities and insurance law in the United States // Managing Environmental Risks through Insurance: Legal and Economic Aspects. Cham : Springer Nature Switzerland 2024. P. 169-216.