2 From Would-Be Chef to CPA: Toby Clary Takes the Reins as COCPA Chair

Thirty years ago, you might have been more likely to consult with Toby Clary about how to smoke a brisket rather than how to address a complicated tax matter, but thanks to a collegiate wake up call, the accounting profession has benefited from his insight and leadership for more than 30 years. Meet your 2024-2025 COCPA Chair.

5 Private Equity Investment Comes to Colorado Accounting Firms

Some of the nation’s largest accounting firms are now several years into their investment deals with private equity firms, with two Colorado firms recently announcing their own deals. What are the benefits for the firms and their people?

8 A Look Back at the 2024 Colorado Legislative Session Through the Lens of the Accounting Profession

From sales tax simplification to workforce development and the integration of artificial intelligence in consumer protections, the 74th Colorado General Assembly's second regular legislative session was marked by a variety of noteworthy developments.

10 Bruce Hellerstein’s Quest to Preserve Baseball History

From a boyhood baseball card collector to the founder and curator of one of the most epic collections of baseball memorabilia in the country, COCPA member Bruce Hellerstein is determined to preserve baseball history for future generations.

24 Behind the Curtain: What You Need to Know About ESG Assurance

Organizations are increasingly disclosing ESG information and obtaining assurance for their disclosures, but often lack an understanding of the types of assurance and how to prepare. This article can serve as a resource in helping clients understand the ins and outs of ESG assurance.

NEWSACCOUNT

A publication of the Colorado Society of Certified Public Accountants Vol. 70, No. 1 Summer 2024

Officers

Tobias "Toby" Clary, Chair

Alexandra Tune, Vice Chair Jim Gilbert, Treasurer

Diego Baca, Immediate Past Chair

Alicia Gelinas, Secretary

Directors

Erin Breit, Kevin Gibson, Amy King, Lisa Kutcher, Patrick Lytle, Greg Pfahl, Tiffany Davis

Editorial Board

Isaac Adamu, Jack Allgood, Paul Elggren, Ken Fichter, Laura Theiss, Steve Van Meter, Michael West, Charlie Wright

Kelli Davis, Editor

Sarah Knight, Blue Ocean Ideas, Design

NewsAccount (ISSN #10899952) is published quarterly by the Colorado Society of Certified Public Accountants, 7887 E. Belleview Ave., Suite 200, Englewood, CO 80111. NewsAccount is published in Winter, Spring, Summer and Fall and reports information, news, and trends in the accounting profession. The Colorado Society of CPAs assumes no liability for readers’ business decisions in reference to advertisements or other information included in this publication.

Membership dues include a $5.00 one-year subscription to NewsAccount 303-773-2877 • 800-523-9082 Fax: 303-773-6344

CONNECT WITH COCPA

Follow us on social media and hear about recent news and upcoming events!

COCPA LEADERSHIP

From Would-Be Chef to CPA: Toby Clary Takes the Reins as COCPA Chair

BY NATALIE ROONEY

GThirty years ago, you might have been more likely to consult with Toby Clary about how to smoke a brisket rather than how to address a complicated tax matter, but thanks to a collegiate wake up call, the accounting profession has benefited from his insight and leadership for more than 30 years. Meet your 2024-2025 COCPA Chair.

rowing up in the Western Slope town of Paonia, Toby Clary, CPA, took advantage of every activity for which Colorado is known. “Paonia is a little town where you learn to love the Colorado outdoors, hiking, camping, and fishing,” he says.

But after high school, Clary was ready to head to a larger city and was drawn to Colorado State University (CSU) in Fort Collins, which he says in the mid- to late-’90s still had a small-town feel but with the amenities of a larger metropolitan area.

Thirty years later, Clary is still in Fort Collins, now as a shareholder at Soukup, Bush & Associates, CPAs, P.C.

Clary wasn’t originally an accounting major. He went to CSU thinking he would major in business management before attending culinary school. He had worked in restaurants throughout high school and college and figured that was where his path would lead him.

By his sophomore year at CSU, however, Clary had an epiphany: the restaurant industry is a grind that never lets up, including on weekends and holidays. “I started second-guessing my decision,” he says.

About that time, Clary took his first accounting class, and discovered that not only did he have a natural affinity for the subject, but he also enjoyed it.

“I had no accounting experience prior to that class,” he says. “It was all completely foreign to me, but I liked it, and it made sense.” He did not struggle through that first accounting principles class like his friends and classmates did. “The more I learned, the more I was hooked,” he reflects.

Clary officially changed his major, graduated with his accounting degree (there were a few years of hard work in between those two events), and joined a small firm of just seven people. After six years, he joined Soukup, Bush & Associates, becoming a partner in 2014.

It’s a decision he has never regretted.

Clary says the love for his clients and the relationships he has forged have kept him in the accounting profession, along with the respect and admiration that he has for the firm’s team. “I love what I do on a daily basis,” he says, “and being a trusted resource for our clients, helping them solve complex problems.”

And the firm’s clients love him. One client, who knew Clary was an avid cyclist, purchased him a new bike helmet. “He told me ‘I need to protect your brain,’” Clary laughs. “It was the most unusual gift I’ve ever received, but it meant a lot to me.”

In another example of those strong client/CPA bonds, one client said to another, “You need a Toby on your team.”

“These stories highlight the role I’m trying to fill by being part of a client’s success and their team,” Clary emphasizes. “It’s not about preparing or reviewing tax returns. It’s about helping people. If you don’t like serving others, this profession is going to be a challenge. I love helping, so for me, when I get a client referral, it’s not about the new business. It’s about asking: how can I help them? That’s what I truly love.”

SAILING INTO THE HEADWINDS

Clary says the same things he’s excited about for the profession might also be viewed as challenges.

“The profession has faced some headwinds recently, and while the Society can’t solve them entirely on its own, I’m looking forward to working with the Board to provide guidance as we navigate the road ahead and make a significant impact where we can,” he says.

Learning more about how the COCPA provides value to its members is something else that excites Clary. “How can we enhance what we’re doing?” he asks. “Like many organizations, the Society is facing a tremendous amount of change. Today’s member needs don’t reflect the needs of members 20 years ago. It’s an ongoing challenge to change and adapt the Society’s programming and services to keep pace with member needs, and I look forward to providing insight as we move forward.”

At the top of the list of critical issues that Clary anticipates for the coming year is continuing to address the challenges and opportunities related to the accounting talent pipeline.

“It’s all anyone talks about,” he says. “While there isn’t one magic solution at the state society level, we can support COCPA members as they’re facing talent challenges, be the voice of the members at the national level, and focus on state-level opportunities to influence solutions.”

Also on Clary’s agenda is continuing to explore how the Society can increase its role in impacting legislation that relates to business, tax, audit, and other professional issues that affect COCPA members in service to their clients.

“I’m excited about enhancing the Society’s legislative advocacy,” he says. “Just as the AICPA responds and is well connected to federal tax issues, there is a growing need for more advocacy on behalf of tax professionals at the state level, particularly in the current Colorado political landscape. In recent years, a significant volume of legislation has passed in Colorado. As CPAs, we need to continue to get in front of it, be proactive, and work with stakeholders to not be caught in a reactionary position after legislation has already passed. This is where I see an opportunity to expand the Society’s advocacy efforts.”

A COLORADO FAMILY

Clary and his family – partner Jill, son Miles (13), and daughter Magnolia (10) – love to spend as much time as possible recreating outdoors. The family enjoys skiing and mountain biking together. Clary says biking in any form – road, gravel, mountain –is his personal passion. He has participated in all the quintessential Colorado rides: Triple Bypass, Tour of Steamboat, Iron Horse Classic, and the Copper Triangle. The family has a home in Fraser, and you’ll find them there frequently, especially during ski season, but also during warmer months for hiking, paddleboarding, fishing, and camping. “We try to be outside as much as possible,” Clary says.

CONTINUED ON PAGE 4

Whether skiing with his family, mountain biking, or indulging his love of wine and travel, Clary loves spending time outdoors. Top, he and his partner, Jill, visit Joseph Phelps Vineyard in California’s Napa Valley.

COCPA LEADERSHIP

CONTINUED FROM PAGE 3

And Clary is still cooking, even though it didn’t end up as his career of choice. Now, cooking is how he unwinds at the end of the day. His love of food and wine has remained an important part of his life, and he enjoys experiencing new restaurants, cuisines, and wines. He and Jill have made many trips to California’s Napa and Sonoma areas, and traveled to New Zealand on an outdoor adventure that involved wine tasting.

A PASSION FOR THE PROFESSION

For more than seven years, Clary taught COCPA CPE courses and loved it, not just for the teaching, but for the opportunity to learn about other people. “Some of my most rewarding professional moments have come from sitting in a CPE class and having conversations with incredibly brilliant CPAs throughout the state. Everyone was just trying to be better,” he says.

Even though he is no longer teaching, he still interacts frequently with former attendees of his classes. “I still get questions weekly from CPAs on tax topics, and I love still being able to help,” Clary says.

Clary’s passion and enthusiasm for the accounting profession extend beyond his COCPA leadership. He is also a member of the CSU Accounting Advisory Board, and his roles with both organizations demonstrate how much he wants to see the accounting profession thrive.

“The accounting profession has done so much for me personally and professionally, and I feel strongly about giving back,” Clary says. “That’s why I’m involved with the Society and CSU, because I feel so fortunate and lucky that I’ve been able to have a successful career in this profession. I want to shout from the mountaintop how great it is. It has changed my life and my family’s lives.”

You can help strengthen the COCPA’s future legislative influence through a donation to the CPA-PAC. With the 2024 election year upon us and numerous seats open and uncertain, the CPA-PAC has the opportunity to shape who fills these crucial positions. By contributing, you enable us to back candidates who are committed to listening and supporting issues that matter to CPAs and the general business community. Let’s make sure our voices are heard. Donate today!

FUNDING THE FUTURE

Private Equity Investment Comes to Colorado Accounting Firms

BY NATALIE ROONEY

Some of the nation’s largest accounting firms are now several years into their investment deals with private equity (PE) firms, with two Colorado firms recently announcing their own deals. What are the benefits for the firms and their people?

The investment of PE into accounting firms continues to accelerate, and investor interest has expanded from just PE to sovereign wealth funds, family office, and private capital. Welcome to the new normal, says Allan Koltin, CPA, CGMA, CEO of Koltin Consulting Group.

“These deals don’t come with flashing neon lights because they’re happening so frequently now,” Koltin observes. “The first deals were groundbreaking, but it’s becoming more commonplace.”

Koltin predicts that 2024 will be a catch-up year after higher interest rates caused some dealmakers to hit the pause button last year. “My guess is that deals that didn’t happen in 2023 will happen in 2024,” he says. He also predicts that no less than five more top-25 accounting firms will be involved in a PE deal before the year is over.

Two firms with a significant Colorado presence recently announced their own PE deals.

In March, top-10 firm Grant Thornton LLP announced that it would be receiving a “growth investment” from New Mountain Capital LLC later this year.

“As we approach our 100-year anniversary this summer, Grant Thornton is operating with significant momentum and generating record revenues,” says Lori Davis, market managing partner for Grant Thornton’s Denver office.

“Our investment with New Mountain Capital will empower us to do more of what we’re already doing and make us the industry’s platform of choice. We’ll be able to accelerate our existing strategy and drive additional growth. This is especially true when it comes to providing clients with personalized, high-quality services that span industries and service areas, from audit and assurance to tax and advisory.”

Davis says that New Mountain Capital is the right partner at the right time. “It has a best-in-class track record in terms of growth within its investment portfolio, and it shares our goal of solidifying Grant Thornton’s standing as one of the nation’s preeminent

accounting and consulting firms. Not only is New Mountain Capital experienced in our space, but it shares our standards and vision — particularly when it comes to quality and client service.”

In February, Baker Tilly received a strategic investment from PE firms Hellman & Friedman and Valeas Capital Partners.

A Baker Tilly spokesperson says the firm pursued the investment to bolster capabilities in three key areas. “First, it provides us with additional capital, allowing us to accelerate our competitive edge, invest in our business and talent, and enhance client service. Second, it enables us to attract and retain top talent, offering more opportunities for our team members and securing our position for the future. Third, it facilitates our growth trajectory, both organically and through strategic acquisitions, by enhancing our mergers and acquisitions (M&A) capabilities and positioning us as an appealing buyer for potential targets.”

The spokesperson adds, “This partnership aligns with our commitment to becoming the preeminent mid-market CPA firm and provides the resources and expertise necessary for sustained growth and success.”

While the early PE/accounting firm deals were between some of the largest firms, Koltin says smaller firms are exceeding their own goals thanks to PE money: Parthenon Capital’s investment in top 25 firm Cherry Bekaert LLP; Broad Sky Partners’ investment in Smith + Howard; Lightyear Capital LLC in Schellman & Company, LLC; and Unity Partners LP in NDH LLC.

“Of course, this doesn’t mean that every single one will be a home run, but so far, deals of all different sizes are successes,” Koltin emphasizes, adding that there are plenty of firms that remain fiercely opposed to PE money and are succeeding by figuring out how to create their own capital, which is sorely needed for that trifecta of technology, transformation, and talent.

“Some go to the bank and set up a line of credit, some ask partners to put more personal earnings back into the business, or some just had a

FUNDING THE FUTURE

CONTINUED FROM PAGE 5

head start because they were already offshoring or had built consulting or wealth-management practices. “So, they don’t need as much capital as other firms or they don’t believe in M&A and their growth is purely organic,” Koltin says.

“Not doing it, doing it, or doing it differently is all good. PE isn’t a magic bullet. There’s no one right way, and not doing it doesn’t mean you won’t be successful.”

RETHINKING THE TRADITIONAL MODEL

One of Koltin’s biggest criticisms of the traditional firm model is that the first five to seven years of a young accountant’s career can be spent doing work that isn’t particularly challenging.

“As artificial intelligence (AI) and bots come in and lift that work away, we can push the young professionals into an advisory role at a much younger age,” he says. “That’s exciting. AI will never replace the client relationship or advisory role. It’s lifting you out of the weeds and getting you into the game sooner.”

Attracting and retaining young talent is critical, and Koltin says it’s time to address the elephant in the room: increasing the pay scale. And for that, partners must either find a way to become more profitable or reduce the amount of compensation they’re taking out of the firm.

“We didn’t anticipate that financial services, investment banking, technology, data analytics, and private equity were all going to recruit from the same accounting talent pool,” Koltin says.

Making things great for young professionals is one of the biggest pros of PE investment.

“These kids all talk to each other, so the accounting majors know that their friends are making more. No one wants to talk about it, but we’re going to have to increase the pay scale. And if you increase the pay scale for a new hire, then you’ll have to increase it for the second years, third years, and on up. There’s such a talent drought. If you can’t pay your talent at market rate, they could become a flight risk,” he continues.

Making things great for young professionals is one of the biggest pros of PE investment. “Today’s new, young partners don’t want to wait until age 65 to get their first dollar of goodwill,” Koltin says. “They can get a check today, and again in three to five years if they hit some modest EBITDA and/or growth goals, and then again in five to seven years when the PE firm sells its interest. It will keep these young people around.”

THE ROAD AHEAD

The Baker Tilly team is excited about what the PE money means for the future. “This investment underscores the value we’ve already generated and our potential for substantial future growth, marking one of the largest private equity investments in the U.S. CPA sector to date,” the firm’s spokesperson says, adding, “Having experienced and collaborative capital partners who share our vision is invaluable as we focus on value creation and accelerating growth.”

Baker Tilly remains focused on creating value and driving growth, fueled by an ambitious approach to potential M&A activities. “This strategy not only presents opportunities for wealth creation and

equity participation for our partners, but also promises growth and value for our clients,” the spokesperson adds. “We are dedicated to maintaining a strong and supportive culture, providing a platform for success for our team and clients alike.”

Grant Thornton’s Davis says that New Mountain Capital’s investment means the firm can add scale, resources, and agility, which help Grant Thornton to redefine the competitive dynamic among the top firms. “The investment in our firm immediately strengthens our position amid a highly active landscape and allows us to deploy capital for targeted M&A and integrations,” she adds. “It also helps us offer dynamic professional-development pathways and a singular culture to attract and retain top talent who’ll better serve our clients and continue our focus on quality.”

As well, Davis says the investment offers the opportunity to better invest in technology, infrastructure, and enhanced capabilities for high-quality audit, tax, and advisory offerings.

A GRAND SLAM

But are these PE deals really all they’re cracked up to be?

So far yes, Koltin says, based on performance. “If you asked EisnerAmper/TowerBrook Capital, or Citrin Cooperman/New Mountain Capital, my gut says they’d all say it was a grand slam home run for the PE group and for the partners and associates of both firms.”

Even the earliest PE deals are still relatively young within the accounting profession, but Koltin says the firms involved have already more than doubled their revenue, profitability, and the value of their rollover equity. “And it’s not just partners who are sharing in the equity,” he points out. “This is a rallying call and an opportunity for the younger people in their 30s and 40s to get a piece of the rock at a much earlier age.”

Baker Tilly says the increased access to capital will allow the firm to position itself as an appealing buyer for potential acquisitions, expanding its reach and capabilities. “This capital infusion enables us to continue investing in our ongoing large-scale tech transformation projects and future initiatives aimed at enhancing client offerings and streamlining internal processes. In essence, the investment sets the stage for significant growth and innovation within our organization, allowing us to better serve our clients and remain at the forefront of our profession.”

Davis says the PE investment will position Grant Thornton for both organic and inorganic growth opportunities. “And it will help us ensure that our current and future teammates have the skills to continue solving our clients’ increasingly complex challenges,” she adds. “Likewise, we’ll be able to adopt and scale technology and infrastructure — and launch new offerings. This will create an even more engaging experience for a range of stakeholders. All the while, we will be focused on quality and service, which are hallmarks of Grant Thornton’s client-centric model.”

At the end of the day, Koltin says professional and financial growth are the levers that matter to today’s young professionals. “If you don’t grow, you die a slow death at a professional services firm,” he says. “You have to continuously create growth to advance people through the system.”

It’s a great time to be in public accounting, Koltin says. “It’s a time of celebration, but we need to raise the starting pay. We need to attract the stars with a competitive wage and more challenging work. You need capital for that, which is why you’ll see these deals continue.”

Member Benefit Provider

CPACharge has made it easy and inexpensive to accept payments via credit card. I’m getting paid faster, and clients are able to pay their bills with no hassles.

Trusted by accounting industry professionals nationwide, CPACharge is a simple, web-based solution that allows you to securely accept client credit and eCheck payments from anywhere. – Cantor Forensic Accounting, PLLC

22% increase in cash flow with online payments

65% of consumers prefer to pay electronically

62% of bills sent online are paid in 24 hours

A Look Back at the 2024 Colorado Legislative Session Through the Lens of the Accounting Profession

BY ALICIA GELINAS, CPA

The May 8, 2024 adjournment of the 74th Colorado General Assembly's second regular session creates an opportunity to look back on the session's strides and challenges, and the implications for Colorado accounting professionals. From sales tax simplification to workforce development and the integration of artificial intelligence (AI) in consumer protections, the legislative session was marked by a variety of noteworthy developments.

SALES & USE TAX SIMPLIFICATION

Progress was made on the long-term effort to simplify the Colorado sales and use tax system. The COCPA has been a dedicated member of the Coalition to Simplify Colorado Sales Tax since 2015, advocating for streamlined processes. This year, legislators passed four pivotal bills, which COCPA CEO Alicia Gelinas, CPA, and other Society members supported through committee testimony:

• HB24-1041 Streamline Filing Sales & Use Tax Returns

• SB24-024 Local Lodging Tax Reporting on Sales Return

• SB24-025 Update Local Government Sales & Use Tax Collection

• SB24-023 Hold Harmless for Error in GIS Database Data

While some legislators responded to requests for simplification, others aimed to use the sales tax system to accomplish affordability objectives through proposed bills to offer sales tax exemptions and sales tax holidays focused on children’s products and college textbooks. These initiatives, which would have been the first in Colorado, ultimately failed to pass through the appropriations committee due to budgetary concerns.

WORKFORCE DEVELOPMENT ACROSS INDUSTRIES

Workforce development remained a top priority among legislators, with initiatives aimed at building a skilled workforce to meet the evolving demands across various sectors. Many bills included funding, expansion, and ongoing support of apprenticeship programs.

While the accounting profession seeks to address its own talent pipeline challenges, Colorado has prioritized industries such as healthcare, construction, transportation, education, engineering, and technology. Various other sectors worked to expand flexibility through interstate mobility and licensure compacts, a privilege from which the accounting profession has benefited for more than a decade. While not challenged in 2024, the COCPA continues to monitor impacts to the CPA mobility privilege as the profession navigates potential updates to the licensure process.

ENVIRONMENTAL LEGISLATION AND

POTENTIAL

FUTURE ACCOUNTING IMPLICATIONS

Environmental legislation gained traction during the session, with a focus on defining long-term effectiveness and clarifying climate goals. Although no broad environmental reporting mandates were introduced, potential implications for CPAs may arise during subsequent legislative sessions or rule-making processes. The COCPA aims to monitor these developments to ensure that CPAs are prepared to navigate new reporting requirements and seize opportunities as service providers for affected businesses.

REGULATING ARTIFICIAL INTELLIGENCE FOR CONSUMER PROTECTIONS

The rapid advancement of artificial intelligence in consumer protections captured legislative attention. The COCPA adopted a monitoring position on SB24-205 Consumer Protections for Artificial Intelligence, intended to protect consumers from discrimination in the use of AI, voicing concerns with other business stakeholders about definitions and potential unintended consequences.

While the general assembly acknowledged the business community's tentativeness, the bold intention to be the first state to issue legislation of its kind in the use of AI was reiterated. In his bill-signing letter, Gov. Polis applauded the sponsors for good intentions and encouraged engagement with stakeholders to make improvements to the bill before its effective date of February 2026.

Legislation at the state or federal levels concerning AI could have significant implications for CPA firms involved in AI development, deployment, and technology risk-assessment services.

TABOR REFUND MECHANISM CHANGES

The Taxpayer’s Bill of Rights (TABOR), established in 1992, remains a unique feature of Colorado’s fiscal landscape, capping government revenue. In response to the record-high $3.73 billion TABOR surplus for the 2021-2022 tax year, legislator debates on refund mechanisms continued through 2023 and into 2024.

Despite a failed attempt to increase TABOR revenue limits through Proposition HH on the November 2023 voter ballot, legislators convened a special session to address immediate refund decisions. Ultimately, legislators agreed to maintain the existing statutory TABOR eligibility and administration for 2023, while only temporarily overriding the tiered income-based refund amounts for flat-rate refund amounts.

The work continued in the last week of the 2024 session, when SB24-228 TABOR Refund Mechanisms was introduced and passed, temporarily reducing the income tax rate for 2024 from 4.40% to 4.25%, permanently changing deadlines for 2024 and beyond TABOR refund claims to Oct. 15 for all individuals, and triggering a new TABOR refund

mechanism of sales tax rate adjustments upon reaching certain surplus levels.

In partnership with the Department of Revenue, the COCPA played a crucial role in recommending changes to filing deadlines, simplifying compliance for taxpayers and their tax preparers in future years.

AFFORDABILITY THROUGH THE USE OF TAX CREDITS

Given the revenue constraints imposed by TABOR, legislators leveraged income tax credits to promote affordability for targeted Coloradans. In its role to support policy makers, the Department of Revenue evaluated roughly 85 proposed bills this session that held potential tax impacts, with approximately half passing. As a result, new and revised line items to Colorado tax returns are anticipated, which is now the focus of the Department in its implementation.

Notable tax credit initiatives included:

• HB24-1211 Family Affordability Tax Credit

• HB24-1134 Adjustments to Tax Expenditures to Reduce Burden –impacting child care and earned income credits

• HB24-1312 State Income Tax Credit for Careworkers

• HB24-1052 Senior Housing Income Tax Credit

Stakeholders across various sectors must engage in the rule-making process that will unfold as these legislative actions take root, adapt to ensure compliance, and seize opportunities for growth.

The COCPA not only tracks and engages with proposed bills but also monitors issues from other states that could impact Colorado. Potentially harmful proposals such as fees on services, threats to CPA licensure, and heavy regulations were successfully avoided this session.

CPA-PAC

Support the COCPA’s efforts to build productive legislative relationships and promote a collaborative advocacy landscape by donating to the CPA-Political Action Committee.

In this election year, your contributions are crucial for equipping and mobilizing our future advocacy efforts. Together, we can shape a future that supports our profession's growth and resilience.

SUPPORT THE CPA-PAC Donate today!

MORE INFO

To stay informed about the bills monitored by the COCPA during the legislative session, visit the COCPA’s Bill Tracker on the COCPA advocacy page.

To learn more about bills and related case law challenges, consider attending the CPE series, “Navigating the Legislative Maze: Keeping You Informed, One Bill at a Time.”

Up next: Aug. 22, 2024

CPE: 2 ea.

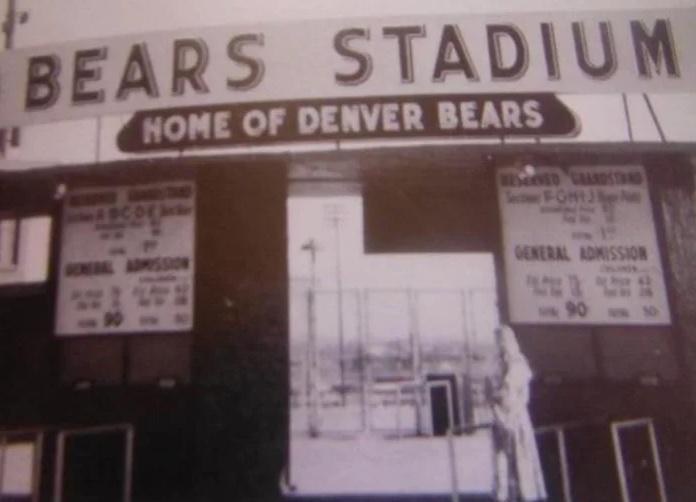

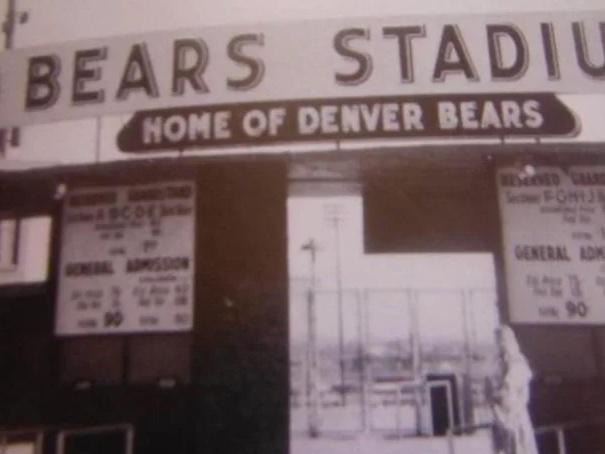

BRUCE HELLERSTEIN’S QUEST TO PRESERVE Baseball History•

BY NATALIE ROONEY

From a boyhood baseball card collector to the founder and curator of one of the most epic collections of baseball memorabilia in the country, COCPA member Bruce Hellerstein is determined to preserve baseball history for future generations.

Hellerstein and his wife, Judy Frieman, attend the 2019 World Series in Washington, D.C. The Washington Nationals defeated the Houston Astros in the Series, four games to three.

Many people collect things for fun, but Bruce Hellerstein, CPA, has taken that concept to a new level. What began as a museum in the basement of his home has grown into the National Ballpark Museum in LoDo, and now it’s one of the most extensive collections of baseball history in the United States.

Hellerstein operates his CPA practice and the museum out of the same building. “I can see the museum from my office,” he says. That proximity is important, because sometimes he dashes down the hall to give a tour of the museum in the middle of the day. It’s a little hectic, but he doesn’t mind.

What drives Hellerstein is the magic that he says surrounds baseball. “When people ask me why I’m so attracted to baseball, it’s because it’s magical. There isn’t a day that goes by that I don’t think about it.”

That magic sets the stage for what Hellerstein calls his love affair with baseball and the classic, old baseball parks. In 1968, he made his first official visit to a classic ballpark: Crosley Field in Cincinnati. “I still dream I’m there. I’m in love with her, and my wife isn’t jealous,” he laughs.

A GIRL NAMED CAROL

The path from boyhood baseball fan to baseball museum proprietor all began thanks to a girl named Carol. Hellerstein’s family didn’t even go to baseball games at that point, but during second grade show and tell, Carol shared that her family had been to see a Denver Bears baseball game at Bears Stadium, and that was pretty much it.

Hellerstein ran home and begged his parents to take him to see this magical place for himself. “As quick as you could say ‘Denver Bears Stadium,’ I was out the door and ready to go,” he recalls. He still remembers feeling awestruck when he saw the team’s name painted on the stadium wall. “I truly believe this was the start of a calling.”

He began making frequent visits to Bears Stadium, not just to see the players, but to experience the stadium itself. Entering the field area by the Bears’ bullpen, he would talk to the players during warmups. His favorite player was Tony Bartirome, a second-string baseman. “I’d wave and say, ‘Hi, Tony,’ and he’d wave back and say, ‘Hi, Bruce.’ That was big-time excitement. I followed his whole career.”

After the games, Hellerstein would head to the locker rooms; he says his autograph requests were never turned down.

He became a lifelong baseball player himself and took part in the game from little league through high school, the semi-pros, and the “old-timers league.” He loved pitching and how the pitcher controls the game.

He says his perfect day is still going to any ballpark in the country to see a baseball game.

FROM COLLECTOR TO CURATOR

Like a lot of young kids, Hellerstein’s collection began with baseball cards. “The cards, without a doubt, were the biggest draw,” he says.

As he grew up, so did his collection, which includes autographed bats and balls, programs, photos, and game jerseys, and even bricks, mortar, and the actual seats from different stadiums.

The eclectic collection was housed in Hellerstein’s basement for years, and he operated as an official 501(c) (3) organization, following every IRS rule to the letter. That meant making the collection public and allowing people into his home to see it during posted hours.

But very few people came to the house, and Hellerstein wanted to share his collection with the world.

In 2006, a realtor was helping Hellerstein find a space that could house both his accounting practice and his collection. Amidst Hellerstein’s hope that the property would be near Coors Field, baseball worked its magic again, and the realtor found 1940 Blake St. – just a stone’s throw from the Colorado Rockies’ home plate. “It was the perfect space for my office and the museum,” he says.

Moving into the new office and museum space was a huge project that took the better part of two years, “and I still had to make a living during all of this,” Hellerstein says.

While other museums focus on the game itself, Hellerstein’s museum is the only one dedicated to the old, classic ballparks like Fenway Park and Wrigley Field. “These are our American treasures,” he says.

For that reason, he always wanted the museum to feel like an old ballpark, even when it was still in his basement. Now he had the opportunity to make that vision a reality in the bigger space on Blake Street.

Today, visitors are treated to pieces of history from the 14 classic ballparks: original signage, old seats, turnstiles, and wrought iron carvings of logos are displayed alongside jerseys, hats, balls, and bats. The museum contains more than 1,000 items.

If patrons are lucky enough to have Hellerstein himself lead their tour, he’s got stories and anecdotes galore. He’ll definitely share his opinions on baseball today because, yes, he’s a baseball purist. The artificial turf, the enclosures and domes, and the clocks – he gives it all a hard pass.

His thoughts on Babe Ruth? “I’ll argue with anyone that the growth of baseball fandom can be attributed to one person,” Hellerstein says. “Babe Ruth made this game, and anyone who wants to argue that with me can be my guest,” he challenges, pointing out that there were no power hitters prior to Ruth, who traveled the country touting baseball as the greatest game on earth and America’s national pastime.

CONTINUED FROM PAGE 11

This museum is the only place where you can relive the best of the old ballparks.

IT’S A CELEBRATION OF BASEBALL and the classic old ballparks.”

– Bruce Hellerstein

“He single-handedly was the representation of baseball. He captured the youth of this country,” he adds.

A highlight of Hellerstein’s tour is how the song “Take Me Out to the Ballgame” originated. You could probably Google the history, but it would be a lot more fun to head to LoDo and have Hellerstein tell you, with great enthusiasm, himself. “I love all of the offbeat stories and the magic of baseball,” he says.

The museum’s five-star rating on TripAdvisor demonstrates that Hellerstein’s opinions, insights, and stories are what makes the museum a success, right alongside his epic collection.

PRESERVING THE FUTURE OF BASEBALL’S PAST

Even though his office is located nearby, don’t think that Hellerstein is sitting in the museum taking tickets all day. “I still work full time,” he says. Volunteers help in the museum, but more often than not, Hellerstein himself fields calls from members of the public who want to come in and see the museum, a process that makes work challenging. “But this is so important to me because of what it represents as a gift to the community,” he explains.

It’s Hellerstein’s goal to preserve the past, because while new ballparks can also be great, “You can’t just build a classic ballpark, because it’s about the ambiance of the location,” he says. “The neighborhoods are so interwoven into the fabric of the ballpark itself.”

“This museum is the only place where you can relive the best of the old ballparks. It’s a celebration of baseball and the classic old ballparks.”

Here’s the rub: All of this preservation and presentation comes at a price. Rent, insurance, and HOA fees are all becoming cost prohibitive, and Hellerstein has been personally supporting the museum nonprofit since its inception. It has required some sacrifice, including the sale of some of his most treasured – and very valuable –baseball cards, along with other items, including two signed Babe

Ruth balls, an Ebbets Field usher’s cap, a piece of the original Yankee Stadium façade, and an on-deck circle from Wrigley Field.

How will he keep the museum going in the future? “That’s the $64,000 question,” Hellerstein says.

While he has an impressive network of baseball connections, no one from that circle has committed to being on the museum nonprofit’s board. “We need money to survive. I can’t keep bankrolling it.”

So Hellerstein continues to look for a long-term funding plan. His CPA brain knows that the answer could lie in his own area of expertise: estate planning. He hopes that someone – or many someones – might find it in their heart and tax return to donate part of their own estate to the museum.

“Baseball is such a passion for people in this country. This is our national pastime,” Hellerstein says. “It’s so important to me. It’s just a big love affair with the game. We’ll just keep working on it.”

In addition to being the president, curator, and founder of the National Ballpark Museum, Bruce Hellerstein, CPA, is the owner of Bruce Hellerstein, CPA, P.C. To learn more about the National Ballpark Museum, visit ballparkmuseum.com . Reach Hellerstein at bruce@hellersteincpapc.com or 720-351-0665.

Has your CPA designation taken you down an unusual career path? Do you have a unique hobby, interest, or side gig that’s become a passion? CPAs do all kinds of interesting things both professionally and personally, and we’d love to shine the spotlight on members' unique endeavors.

Please email Kelli Davis at kelli@cocpa.org to indicate your interest in being interviewed for an article or to let us know of a fellow COCPA member who has a story to tell.

Share your story today!

The COCPA 100% Membership Program helps save your team time and money. At the same time, it demonstrates your organization’s commitment to the profession. Together, we are 100% strong.

Benefits include:

CONCIERGE-STYLE attention from COCPA’s membership team

RECOGNITION of your firm and team (both online and in print)

DISCOUNTS towards training that helps make your team smarter

STREAMLINED dues processing

So much MORE!

Causey Demgen & Moore, PC

Cherry, Ogle & Quinn, PC

Eide Bailly

FORVIS, LLP

Grant Thornton LLP

Haynie & Company

Johnson and Associates, CPAs, PC

Kundinger, Corder & Montoya, PC

Marrs Sevier & Company LLC

MGPM, PC

Moss Adams LLP

Plante Moran LLP

Reese Henry & Company, Inc.

Rubin Brown, LLP

Soukup Bush & Associates

CPAs, PC

WhippleWood CPAs, PC

TECHNOLOGY Beyond the Ledger: Pragmatically Enhancing Cybersecurity in Accounting Firms

BY MIKE ELLERHORST

Atop the daily stresses of “busy season” within the public accounting sector, imagine a scenario in which your laptop gets hacked, your company systems are inaccessible, or your client data have been stolen, with critical filing and client deadlines meanwhile quickly approaching.

In today’s interconnected, digitally enabled world, all businesses face a landscape of growing cybersecurity threats, with no industry or company size immune. For accounting professionals working in public accounting firms, many of which are smallor medium-sized businesses (SMBs), safeguarding sensitive financial, personal, and client data is paramount.

In this article, we explore cybersecurity risks specific to CPA firms and offer practical solutions to improve your posture in this area.

CYBERSECURITY RISK IS A VERY REAL BUSINESS RISK

While small- and medium-sized business owners are aware of and worry about cyberattacks, there is often a disproportionate investment or response to this existential threat.

A recent Global Small Business Study by McAfee/Dell Technologies found that 73% of organizations [say cybersecurity] is one of their biggest risks or vulnerabilities, but that less than half (48%) “were fully confident in the ability of their business to prevent cyberattacks.”1

Despite this lack of confidence, there is also a lack of action. The National Small Business Association’s 2021 Report found that “just 34% of small businesses reported completing a technology audit.”2 In today’s threat landscape, this is the proverbial “death wish,” as you cannot secure what you don’t know is out there, and attackers only need to find one way in to compromise your systems.

Unfortunately, this fear and lack of confidence by small business owners is not unfounded, with a Hiscox Small Business Cyber Report finding that 47% of small businesses suffered at least one cyberattack in the past 12 months. Within that group, 44% suffered more than one attack.3

CPA and accounting firms are at increased risk of these catastrophic events due to their business model of obtaining and interacting with highly sensitive data and the potential reputational impact with existing and future clients – often carrying high revenue concentration with a limited number of clients.

WHERE TO START WHEN YOU DON’T KNOW WHERE TO START

Unlike many articles that provide technical “tips and tricks” that everyone should follow, I recommend a slightly different approach: start with the business, then with the people and technology.

1 Establish and maintain a risk register.

A corporate risk register serves as a critical tool for SMBs and can enable partners and business owners to more systematically evaluate the risks that could impact the organization. By including cybersecurity risks in this register, companies acknowledge that protecting data is not just an IT concern – it’s a strategic business imperative.

Furthermore, an intentional discussion of all risks with a cybersecurity lens can identify how seemingly innocuous cybersecurity risks could result in a non-technology risk being realized.

Key steps in building and maintaining a risk register include the following:

Identify risks. Collaborate with key stakeholders (including strategic advisors, board of directors, and trusted industry representatives) to identify potential cybersecurity risks

to the business. Consider external threats (e.g., cyberattacks, data breaches) and internal vulnerabilities (e.g., employee negligence, outdated software). Consult industry reports, contracts recently signed, and the latest regulatory updates.

Assess impact and likelihood. Evaluate each risk’s potential impact on the business and the likelihood of occurrence. Consider utilizing a risk quantification methodology such as FAIR or OCTAVE to estimate financial impact. Prioritize risks based on severity.

Determine risk treatment and mitigation strategies. Develop specific treatment strategies for each risk. For cybersecurity, this can range from risk transference (increasing a cyber insurance policy), risk avoidance (do not open an office in [state] due to privacy obligations), or risk mitigation (such as implementing firewalls, encryption, and access controls).

Assign ownership to the risk treatment and check in on progress at least quarterly.

2 Inventory your systems, data, and contracts.

Just as one of the most important steps in setting up your home security system is counting your doors and windows, understanding your technology footprint (or the surface area exposed to external attack) is essential to a comprehensive and trustworthy cybersecurity program.

At a minimum, I recommend starting with the three inventory types listed below and focusing on creating a process and level of detail that you can sustain. It's better to have a less detailed inventory, but one that is up to date and – to the best of your knowledge – complete.

System inventory: Document the physical and virtual systems or assets that your company owns or has accountability for, as well as the software that is running on those devices. For

hardware, this could include servers, workstations, mobile devices, routers, firewalls, and cloud instances. For software, keep track of installed applications and their versions. You can start with software licenses that you have purchased on either a one-time or subscription basis. Tools such as configuration management databases (CMDBs) and asset management products can help collect this information or periodically validate it, but most SMBs struggle to sustain the sophistication of these options.

Data inventory: Categorize data based on its sensitivity (such as public, internal, confidential) and document where the more sensitive data exist. As a starting point, list the data repositories (e.g., laptops, SharePoint, file server, AWS S3 Buckets, Box.com) and the most sensitive type of data that is stored there.

Then document the individuals or roles who are approved to have access to that information. For the most sensitive data, or where you have specific contractual or regulatory obligations, you may need to maintain a more granular accounting of data (such as database name, folder, or file name).

Third-party inventory: Establishing and maintaining an inventory of all of your third parties is critical for understanding “upstream” and “downstream” risk as well as fulfilling data privacy obligations. Understand which vendors/suppliers have access to your systems or handle/store your sensitive data. Understand with what third parties (including clients, affiliates, partners, or subcontractors) you share your sensitive data. Perform periodic reviews and due diligence to assess their security practices and contractual obligations to you, as well as your contractual obligations to your clients. Sometimes there’s a gap!

By understanding your assets, data, and third-party relationships, you lay the foundation for a robust information security program. Regularly update your inventories and adapt security controls as needed.

3 Employ and reinforce pragmatic cybersecurity hygiene.

I like to highlight the many parallels between maintaining one’s physical health and reinforcing a company’s cybersecurity health. Physical health is made up of a series of factors that all work together in concert for how you look and feel on a given day: your sleep habits, your diet, your exercise patterns, your environment/the climate in which you live, your genetic predisposition.

No single factor by itself is going to make you “healthy,” and you’re never “done” with any one of the factors – it requires daily/monthly/ yearly intention and effort (and it's realistic to know that you’re never going to be perfect in all dimensions).

Some of the good “healthy cyber habits” to remind and reinforce/encourage with your employees, team members, and clients include:

EMPLOYEE AWARENESS AND EMPOWERMENT

• Policy awareness: Review and discuss your company’s and/or your client’s information security policy.

• Phishing awareness: Train staff to recognize phishing emails and avoid clicking suspicious links. Know how and to whom to report suspicious emails.

• Password hygiene: Encourage strong, unique passwords and regular rotation/changes, and whenever possible, use a password manager to securely store your passwords so that you don’t have to remember them.

DEVICE MANAGEMENT

Software updates: Keep operating systems and applications up to date to address known vulnerabilities. Follow the schedule provided or communicated by your information technology (IT) department, or if there isn’t a defined schedule, turn on automatic updates.

Regular reboots: It may be easier to keep your many open browser windows or tabs and just close your laptop at the end of the day, but a regular restart of your operating system/device helps to ensure that background system changes take effect.

ACCESS CONTROLS

Least privilege: Limit access rights to only what’s necessary for each role. If you have more access than you think you need, raise your hand and let your IT or information security team know. Don’t maintain access “just in case,” and consider how you can implement separation of duties (SOD) principles.

Multi-factor authentication (MFA): Implement MFA for critical systems and processes. This could include human-based processes such as calls with a managed service provider (MSP/MSSP) requiring a verbal passphrase to make substantial and/or security-impacting changes.

Remember, cybersecurity is an ongoing process and is everyone’s responsibility. Regular risk assessments, continuous monitoring, and proactive measures are essential to safeguarding sensitive firm and client data. By following the guidelines outlined above, accounting professionals can better protect their firms’ data and help lessen the chance of a data-related interruption to doing business.

ADDITIONAL CYBERSECURITY RESOURCES

→ COCPA blog post: "Free WISP Template: Protection for Your Clients and Your Firm"

→ On-demand CPE course: Complying with IRS Publication 4557 and FTC Safeguards Rule: Step-by-Step Guidance for Firms of All Sizes

→ Webinar (various dates): Cybersecurity 101 for CPAs

→ National Cybersecurity Alliance CyberSecure My Business webpage

→ Cybersecurity & Infrastructure Security Agency (CISA) Cyber Guidance for Small Businesses webpage

Mike Ellerhorst is the founder and CEO of NTM Advisory, a cybersecurity consulting firm based in Lafayette, Colo. Reach him at mike.ellerhorst@ntmadvisory.com. Click here to watch his webinar, “The Pragmatic CISO,” delivered at a May 12 COCPA Technology Users Group (TUG) event. To learn more about or to join the COCPA Technology Users Group, contact Stacy Svendsen at stacy@cocpa.org.

Did That Just Happen Uncovers Truths on Common Workplace Inclusivity Challenges

BY JUDY A. THOMAS, CPA, MBA

Did That Just Happen?! Beyond “Diversity” – Creating Sustainable and Inclusive Organizations, by Drs. Stephanie Pinder-Amaker and Lauren Wadsworth, offers a well-written account of not only the authors’ personal experiences with diversity, equity, and inclusion (DE&I) in the workplace, but also those of others, from the everyday to the shocking. The stories come alive for readers, who are encouraged to draw parallels to their own lives, improve their own cultural awareness, and seek to be more equitable in their personal and professional lives.

UPDATING THE LANGUAGE

The authors emphasize the importance of diverse teams in the workplace, noting that groups with this type of makeup contribute richly to organizational success. The book introduces updated terminology such as “rising identities” as a replacement for more traditional language such as “minorities,” “diverse populations,” and “cultures,” and notes that the ever-changing landscape of the DE&I space increases the complexity of specifying identities. Thus, the term, “rising identities” more comprehensively reflects the often-seen combination of multiple identities.

While readers might think that this book addresses many of the same issues as other DE&I literature, its experiential content takes things to the next level.

As well, a more inclusive alternative for the term, “microaggressions” – the everyday slights, invalidations, and offensive behaviors that people experience from generally well-intentioned individuals who may be unaware of the demeaning

nature of their interactions – is “identity-related aggressions” (IRAs).

While the reader might question the necessity of this updated terminology, the authors explain the subtle differences among the various terms and why the newer ones are more appropriate.

DIVERSITY EXPERT BY DEFAULT

Drs. Pinder-Amaker and Wadsworth discuss the role in which employees with rising identities often find themselves within organizations: Filling the role of “diversity expert” simply because of their identity rather than any particular expertise that they may have related to diversity issues.

While these employees may be enthusiastic about the role, its responsibilities often come atop their normal workplace duties and are uncompensated.

Drs. Pinder-Amaker and Wadsworth have each found themselves in similar situations and are quick to point out the pitfalls of such an arrangement for both the employee and the organization.

The authors share the experiences of others who have found themselves in the “diversity expert” position and suggest alternative solutions and compromises that address the weaknesses of many DE&I programs. They suggest that management dedicate specific resources and expertise to these programs in order for them to succeed.

CHECK YOUR BAGGAGE

As the authors point out, participants must “check their baggage” at the door when they become involved in DE&I activities, whatever that baggage may be, and abandon the perspective of “me.”

Readers may become defensive when they first read this commentary; after all, they only have the best of intentions or are only seeking fairness for all. However, too often, in making their points, well-intentioned employees are blinded by the “rightness” of their position and the need to share it with others. A willingness to accept honest feedback and criticism helps both the team and the organization function more effectively.

It is important to note that whether intentional or inadvertent, the impacts of IRAs are equally difficult for the affected person(s). The question is how they are handled. Do the affected individuals or the group speak out, address the situation later, or ignore the incident altogether?

The book addresses the various responses to these types of scenarios. The authors bring readers along as the aggressions become progressively escalated, such as a George Floyd situation, and describe how people reacted to this incident. Drs. Pinder-Amaker and Wadsworth accelerate the narrative to emphasize the need for diverse teamwork and commitment to DE&I.

SEEKING SOLUTIONS

Throughout the book, Drs. Pinder-Amaker and Wadsworth offer narratives based on real experiences, followed with possible solutions. They highlight the pitfalls and benefits of the solutions, as well as the consequences for those involved. They emphasize that solutions must include management, rising identities, and all employees and team members. Not all solutions fit all organizations, but all follow a similar trajectory.

While readers might think that this book addresses many of the same issues as other DE&I literature, its experiential content takes things to the next level to uncover “truths” in new ways. These truths combine to give readers insight into how to function successfully in a world filled with rising identities.

The next time you ask yourself, “Did That Just Happen?”, you will be better able to address the questions that ensue.

Recently retired as chair of Regis University’s accounting department, Judy Thomas, CPA, MBA continues as an affiliate faculty member of Regis’ Anderson College of Business and Computing, and serves as vice chair of the COCPA Diversity, Equity, and Inclusion Committee. Reach her at jathomas@ix.netcom.com. To learn more about the committee’s activities, contact Stacy Svendsen at stacy@cocpa.org.

Everybody Matters: Championing a Different Measure of Success

BY TOM HALL, CPA, CFA

Iread lots of books and listen to lots of audiobooks. About a year after I started working at Deloitte’s Denver office, I began writing down the name of every book I read or listened to. I counted them up recently and discovered that I have read or listened to almost 1,250 books since 1996. While many of these are absolutely forgettable and unremarkable, occasionally I come across a book that changes me, that leaves a lasting impression, that screams, “You need to read me again – and again!”

Everybody Matters, by Bob Chapman and Raj Sisodia, is one such title.

In fact, if there were one book that I think should be required reading for every university business student, this is the book. And its relevance extends beyond the business-student crowd; it’s relevant for anyone who leads an organization or even a small team, for educators who lead students, and for anyone who deals with people.

One of the authors, Bob Chapman, is chief executive officer of a company that you’ve likely never heard of – the St. Louis-headquartered Barry-Wehmiller (BW), a diversified manufacturing and service company involved in the global packaging industry. That doesn’t sound exciting at all, but the book is not about Chapman’s company; instead it details the revolutionary way in which it operates.

The tagline of the book says it all: “The Extraordinary Power of Caring for Your PEOPLE Like FAMILY.” This is a book about leadership – the right kind of leadership.

I’ve now read this book three times, and each time I’m amazed at the simplicity of its message. This style of leadership now seems obvious to me, but it runs counter to likely anything that is taught in business school.

Chapman graduated with an undergraduate degree in accounting, going on to earn his MBA from the University of Michigan. After graduating, he worked for Price Waterhouse for a couple of years before going to work at BW, his family’s business, which was on the verge of bankruptcy. After his father passed away in 1975, the younger Chapman became the CEO and helped to right the ship. But again, this isn’t a book about the history of BW.

Here are Chapman’s own words:

“I started out as one of those leaders who put profits before people, who always thought about costs, never about caring. Eventually, I realized it is all about leadership – but not the kind of leadership I had learned in business school.”

WHY YOU SHOULD LISTEN TO CHAPMAN

Before I tell you about the company’s leadership approach, let me tell you why you should listen to what its CEO has to say. Chapman’s company has been successful by every definition of the word. Since 1987, BW has invited more than 120 companies to join the BW family, growing it from a $20 million business into a diverse $3 billion-plus global leader in industrial manufacturing.

According to KPMG, 77% of acquisitions fail to meet their objective. The record of BW, however, is exactly the opposite: the organization has not sold a single acquisition. (BW likes to call them “adoptions.”). All of the acquisitions, or adoptions, have been successful. Furthermore, it’s easy to find value in a company that is already profitable, but nearly all of the acquisitions that BW made involved companies that were floundering, many on the verge of bankruptcy themselves, where productivity was low and employee morale even lower.

And in all the acquisitions, BW fired or laid off almost no one, which is unheard of after 120 acquisitions. The BW strategy allowed the organization to deliver 16% compounded returns to its investors for more than 16 years, when the S&P returned only 4% during the same period.

While most acquisitions are made solely for a financial return, the BW slogan is, “We measure success by the way we touch the lives of people.” And that means all people: employees, customers, vendors, even bankers. Its leadership approach starts with the statement, “There are no underperforming teams, only underperforming leaders.”

TREAT EMPLOYEES RIGHT AND PROFITS WILL FOLLOW?

BW believes that if you simply treat your employees like you would your own family, the profits will take care of themselves. But to be clear, BW never speaks of profits as the main goal. Employees report that BW’s leadership training is not about increasing profits, decreasing waste, reducing overhead, or boosting productivity. Not one word is mentioned on how this approach is “good for business.” The main goal is instead to help every employee be excited about working, feel safe, and reach his or her full potential.

Chapman was once interviewed for two hours by a professor of organizational development. Afterward, the professor said he’d never spoken with a CEO who didn’t talk about his company’s products. Chapman said, “We have been talking about our products for two hours. It’s our people.” Indeed, despite having read this book three times, I'm still largely unclear on exactly what products BW manufactures (besides people, of course).

Every one of them testifies that their lives – their whole lives, both at work and at home – have experienced a 180degree turnaround, and they all credit this to finally feeling valued, appreciated, and heard.

Simon Sinek, the best-selling author of Leaders Eat Last and Start with Why (and who also wrote the foreword to Everybody Matters), said, “The thing that makes us love our jobs is not the work that we’re doing, it’s the way we feel when we go there. We feel safe; we feel protected; we feel that someone wants us to achieve more and is giving us the opportunity to prove to them and to ourselves we can do that.”

In the United States, 88% of the workforce – 130 million people – go home every day feeling that they work for an organization that doesn’t listen to or care about them. That’s seven out of every eight people! BW is trying to change that. Its primary purpose is not to make profits. Rather, BW is in business so that all its team members can have meaningful and fulfilling lives. Yes, it builds capital equipment and offers engineering solutions, but that is simply the vehicle – the economic engine – through

which the organization can improve its team members’ lives.

OUR WORK IS LITERALLY KILLING US

According to a Gallup poll, only 22% of U.S. employees are engaged and thriving at work. But the healthcare costs for that group are 41% lower than for employees who are disengaged, and 62% lower than for the one-fifth or so of U.S. employees who report hating their jobs.

The number-one factor in the rise of chronic disease is elevated chronic stress, with an estimated 73% of Americans having unmanageable stress in their lives. We are stressing people out at work, then sending people home to their families.

It’s a vicious cycle that will continue as long as we treat people as objects to be used to “meet our numbers.” In contrast, employees who feel listened to, cared for, and treated superbly will feel better about themselves and thus have better relationships with their families. Put simply, the way we treat people at work affects the way they feel and, in turn, how they treat everyone else in their lives.

RESPONDING LIKE A CARING FAMILY WOULD

If you are a parent, you want your children to be safe, healthy, happy, and cared for, and for them to lead lives of meaning and purpose. Each employee is someone’s son or daughter. Good leadership and good parenting both boil down to taking care of the people entrusted to you. Just as parents feel a deep sense of responsibility for their children, we should feel the same about the people whom we are privileged to lead.

When a firm downsizes, it has a lasting negative impact on its employees, in the form of both damage to self worth and a dramatic loss of income. Eighty percent of people report a negative impact on their health within a year of getting laid off, and their risk of dying goes up by 44%. The frequency of sick days doubles in downsizing companies.

For those reasons, perhaps the single-best example of how BW lives its culture is what happened during the Great Recession of 2008 and 2009. In 2008, Citicorp laid off 73,000 people, Bank of America 35,000, General Motors 34,000, and Hewlett-Pack-

LESSONS IN LEADERSHIP

CONTINUED FROM PAGE 19

ard 25,000. In January 2009 alone, Fortune 500 companies laid off almost another 164,000 people.

BW thought its backlog of customer orders would get it through this crisis without layoffs, but backlog orders started to evaporate, with few new orders placed. However, true to BW’s principles, Chapman asked, “What would a caring family do when faced with such a crisis?” The answer was obvious: you wouldn’t lay off one of the children. (“Sorry, Timmy, Mommy and Daddy lost their jobs, so we unfortunately have to let you go!”)

Instead, everyone would pitch in with a sense of shared sacrifice so that no one member would have to experience dramatic loss. BW implemented a furlough, and every employee was required to take a month off without pay. In addition, the company’s 401(k) match was suspended for a time. Executive bonuses were also suspended, and Chapman’s own annual salary dropped from $875,000 to $10,500 – his starting salary in 1968 at Price Waterhouse.

BW team members responded well to these initiatives. Employees had been walking on eggshells for months, fearing employee layoffs. In an instant, that fear was gone, replaced with positive feelings of security and gratitude. Morale rose immediately, and most people were happy to offer up four weeks of income to help them (and their coworkers) keep their jobs. Some employees who could afford to take off more unpaid time did so to help others who couldn’t afford to take off four weeks. Not one person was laid off because of the recession.

The company rebounded faster than the regular economy. In fact, 2010 was BW’s best year ever for earnings, and that was after it had fully repaid the lost 401(k) match for all employees. BW has since enjoyed one record year after another.

PERSONAL STORIES

Everybody Matters is filled with stories of employees, mostly at struggling BW acquisition companies, who suffered from low morale and experienced extreme cynicism when BW swooped in and promised “this time, things will be different.”

These employees had all “seen it before” and had been told by countless previous owners that things were going to change. But eventually, they came to see that the BW way of doing business and treating people like family was authentic. Every one of them testifies that their lives – their whole lives,

both at work and at home – have experienced a 180-degree turnaround, and they all credit this to finally feeling valued, appreciated, and heard. Oh, and by the way, their original companies (now part of BW) are as successful financially as they’ve ever been.

WHY YOU SHOULD READ THIS BOOK

The reason this book resonates so deeply with me is because I’ve seen the cost of poor leadership. Ask any group of people if they’ve ever quit a job they kind of liked because they disliked their boss, and many will raise their hands. In college, I quit one of those jobs myself.

I read recently that people don’t quit their jobs, they quit their bosses. The resulting lost productivity in the United States is close to a trillion dollars each year. It is so much cheaper and more efficient to keep an employee happy and satisfied than to suffer the inefficiencies of an unhappy one, only to have to find, hire, and retrain someone else when your employee quits. Just treat your people right the first time! I have worked at large, well-known companies where the policy was “rank and yank” – “rank” every employee each year and then “yank” (i.e., fire/lay off) those at the bottom (so you can replace them with supposedly “better performers”), even though the “bottom” employees might be performing satisfactorily and fulfilling some important functions.

It was such a challenge to lead teams in that kind of environment. How much better would my own experience have been if instead, every employee were valued as having infinite potential and if upper management would have had the patience to help each employee achieve it. Unfortunately, the focus was always on cost cutting, profitability, and efficiency rather than people. That’s the way it is in almost every modern organization.

I am now an accounting professor. I no longer lead corporate teams like I did for more than 20 years, but that is of no consequence. While my sphere of influence is different than it used to be, I can absolutely apply the principles of this book to my classroom and to my students. I have always cared for my students, but this book inspired me to up my game!

I see my students as well-rounded human beings with infinite potential who have been entrusted into my care for a short

time – perhaps only a 10-week quarter. As such, I have a responsibility to help them feel safe and valued.

That doesn’t come at the cost of academic integrity or rigor in my classroom. Every student must still meet the requirements of the course to receive credit, and to receive an A in my class, you must earn it. My classes are sometimes viewed by students as “hard,” with lots of material to learn and lots of assignments and exams by which to demonstrate that learning. But, importantly, my courses are also described as fair.

I don’t want it to be said at my funeral that I was “a really smart and effective accounting professor.” Rather, I want it said that I was kind, caring, patient, and understanding, and that I was a good steward to those students in my care.

Everybody Matters doesn’t just show the right way to lead people that will help companies achieve financial success as a byproduct … although it does do that. Beyond that, it shows that caring for others and helping people feel fulfilled fosters a spirit of altruism: if I genuinely care about you, you will genuinely care about Ray, and if you genuinely care about Ray, he will genuinely care about Sara, and so on.

It all begins with you.

Tom Hall, CPA, CFA, is an associate professor of the practice with the University of Denver School of Accountancy. Reach him at tom.hall@du.edu. Watch for his new semi-regular column, “Career Chronicles: Advice for Emerging Professionals,” debuting in the fall 2024 issue of NewsAccount

The Emerging Professionals Initiative Committee (EPIC) unites students and other emerging professionals through special events, resources, and programs to support your professional growth. Visit COCPA's EPIC homepage to learn more

Your COCPA membership includes exclusively negotiated discounts and program enhancements with leading providers in the accounting and business space.

COCPA has vetted each one of these companies for you. The Member Savings Program is just one more way COCPA creates value for you, your clients, and your organization.

PROFESSIONAL SERVICES

Payment processing

Cost segregation

HR Solutions/payroll/multi-state compliance new

”White labeled” wealth management services new

Managed IT/cyber security services

Private, secure, and air-gapped network connectivity new

”.cpa” web domains

Shipping, printing, and office supplies

Car rental/travel services

Background checks

Insurance

Professional liability insurance

Long term care insurance

SOFTWARE/CLOUD SERVICES

Cloud accounting software

Lease/NetSuite accounting solutions

AI-powered expense management new

Secure file sharing/unlimited document signing

Email marketing systems

Messaging, video, phone services

LEARNING RESOURCES

Tax and accounting books

CPA exam review courses

WE WALK THE TALK.

CAMICO knows CPAs, because we are CPAs.

Created by CPAs, for CPAs, CAMICO’s guiding principle since 1986 has been to protect our policyholders through thick and thin. We are the program of choice for more than 8,700 accounting firms nationwide. Why?

CAMICO’s Professional Liability Insurance policy addresses the scope of services that CPAs provide.

Includes unlimited, no-cost access to specialists and risk management resources to help address the concerns and issues you face as a CPA.

Provides potential claim counseling and expert claim assistance from internal specialists who will help you navigate the situation with tact, knowledge and expertise.

Does your insurance program go the extra mile? Visit www.camico.com to learn more.

Welcome, New COCPA Members

The COCPA welcomes the following new members, who joined between March and May 2024.

FELLOW MEMBERS

Allison Beyl

Kelly Buck

Jason Call

Ryan Comstock

Jennifer Dombek

Tim Ford

Leah Gillaspy

Lucas Godber

Aimee Grech

Michael Huskey

Jessica Johnson

Katie Kallenberger

Maria Kelly

Michaela Knox

Katherine "Kalee" Koval

Lauren Kuykendall

Bilal Lulu

Terri McGehee

Bryan Meisenzahl

James Miller

Matthew Minteer

Jie "Jen" Pan-Maddis

Daniel "Duster" Pevonka

Connor Pickering

Juan Rayo

Austin Regan

Sara Royster

Nicole Swift

Jaya Tripathy

Simon Vakili

Tijana Vukovic

Andrew Walton

Ashley Wiitala

Trenton Yamashita

Shanshan "Sam" Yang

STUDENT MEMBERS

Nayeli Aguirre

Joanne Anderson-Wooley

Annabelle Barkoff

Ellis Brenneman

Derik Castillo

Ashley Cisneros

Terry Faulkner

Jake Folsom

Noah Haselby

Darcy Jardine

Ryann Koobs

Jason LaBau

Madeline "Madie" Main

Zahra Mammadova

ASSOCIATE MEMBERS

Jenny Arias

Stephanie Box

AnnaMarie "Anna" Bugosh

Madison "Madi" Callahan

Myles Campo

Krystal Cook-Matson

Samuel Dennington

Herbert "Lowell" Dillon

James Fox

Matthew Friedberg

Riley Hand

Karly Haugen

Alexandrea Hennessy

Dustin Kaufmann

Asya Kosolap

Ashley Kyle-Johnson

Joelle Laundy

Ashley Matthews

Jasmine Passanante

Rebecca Pierson

Bryce Raines

Gabriela Rendon Hernandez

Katie Sanchez-Cortez

Michelle Schultz

GET INVOLVED GET CONNECTED

Know any of these members? Reach out and welcome them to our community!

Visit the COCPA Member Directory at cocpa.org/member-directory.

Lucinda Macias

Lorena Martinez Sanchez

Sophia McConnell

Lupita Nagireddy

Dawn Nobilio

Joshua Park

Emmett Pelissier

Cassandra Shetler

Angela Simon

Nelli Simons

Samona Skidmore

Cordell Soderquist

Michael "Mikey" Stoddard

Andrea Turbak

Victoria VanVorst

Caitlin Shaughnessy

Evan Sheehan

Andrea Stout

Juan Vasquez

Rylee Vilhauer

New members, are you looking for a way to get involved, meet others, and connect with your new professional community? Whether your passion is serving on a committee, participating in a special-interest group, or bettering your community, find the opportunity that speaks to you and join in! For more information on volunteering, contact Stacy Svendsen at stacy@cocpa.org.

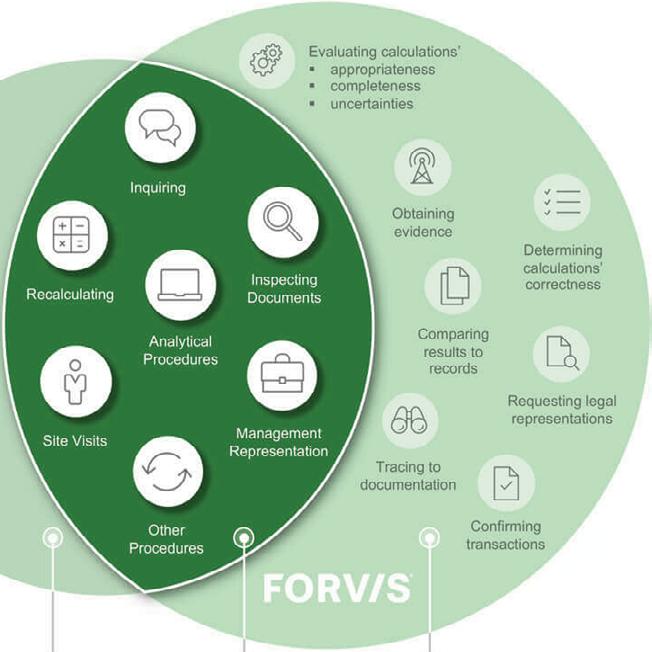

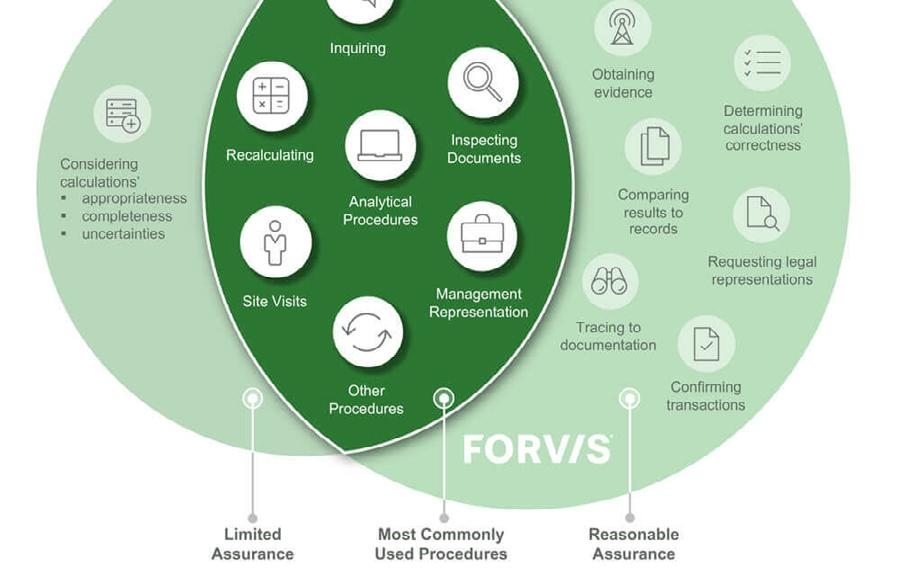

Behind the Curtain: What You Need to Know About ESG Assurance

BY DIRK COCKRUM AND STEVE WILKERSON, CPA, CFSA

As CPAs work to educate their clients on the increasing relevance of environmental, social, and governance (ESG) disclosures and assurance, the following can serve as a valuable resource in helping clients understand what ESG assurance is, the difference between and applications of its two types, and how best to prepare for an ESG assurance engagement.

Organizations are increasingly disclosing environmental, social, and governance (ESG) information and obtaining assurance for their ESG disclosures; however, they often lack understanding of the types of assurance and how to prepare. Organizations seek assurance of ESG information to show their senior executives, board members, investors, customers, suppliers, regulators, and other stakeholders that the ESG information

being reported is reliable and credible. Organizations have been especially interested in obtaining assurance for their greenhouse gas (GHG) emissions disclosures to comply with the U.S. Securities and Exchange Commission (SEC) final climate disclosure rule, which was approved on March 6, 2024. The SEC rule includes requirements for large accelerated and accelerated filers to obtain assurance on GHG emissions disclosures if emissions are material.