The hotel is about 12 miles from the Louisville International Airport. The airport has a designated areas for hired cars to pick up passengers.

Cost: Approximately $25

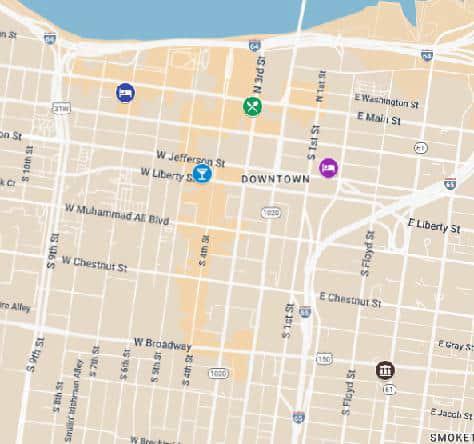

Meeting Locations

The meeting will be held at the Metro United Way, which is approximately a 5 – 10 minute Uber ride from either hotel. (The City of Louisville will be providing Uber codes that members can use to travel from the hotel to the meeting space.)

Tuesday, October 21st, 2025

Coalition Meeting

9:00 AM – 5:00 PM Metro United Way

334 East Broadway

Welcome Reception Hosted by Bank on Louisville

5:00 PM – 7:00 PM Chase Bank

416 West Jefferson St

Wednesday, October 22nd, 2025

Coalition Meeting

8:30 AM – 1:00 PM Metro United Way

Louisville Site Visits

334 East Broadway

1:00 PM - 4:00 PM Various locations

Group Dinner

300 W. Main Street Co-Chairs

5:30 PM – 8:00 PM: BBC Bourbon Barrel Loft

Co-Chairs

San Francisco

New York City

Member Cities

Albuquerque

Boston Dallas Denver

Detroit

Hawai’i County

Jackson Lansing

Los Angeles

Louisville

Philadelphia

Rochester

Sacramento

Saint Paul

San Antonio

Shreveport

Tulsa

Thursday, October 23rd, 2025

Coalition Meeting

8:30 AM – 12:00 PM Metro United Way

334 East Broadway

Co-Chairs

San Francisco

New York City

Member Cities

San Antonio

Shreveport

Tulsa

Tulsa

CFE Coalition Forum Agenda Louisville, KY

October 21st – 23rd, 2025

Tuesday, October 21st, 2025 Metro United Way

334 E. Broadway, Louisville, KY 40202

9:00 – 9:30 a.m. Breakfast

9:30 – 9:45 a.m. Welcome and Agenda

Facilitated by: José Cisneros, City of San Francisco and Nichole Davis, City of New York

9:45 – 10:15 a.m. Louisville City Update & Delta Homes Program Spotlight Facilitated by: Erin Waddell and Ce Garrison, Louisville Metro Government

10:15 - 10:45 a.m. City Updates San Francisco, Dallas

10:45 - 11:00 a.m. Break

11:00 a.m. – 12:00 p.m. Local Elected Officials Championing Financial Empowerment Work Facilitated by: Vicky Selkowe, CFE Fund

Deputy Mayor Nicole George, Louisville Metro Government

12:00 – 1:15 p.m. Working Lunch: CFE Coalition Member City Updates Saint Paul, Denver, Sacramento

1:15 – 1:45 p.m. Rochester City Update & Positive Rent Reporting Spotlight Facilitated by: Angela Rollins, City of Rochester

1:45 – 3:00 p.m. Emergency Financial Empowerment

Facilitated by: Sol Vilera Ramos, CFE Fund

Kasey Wiedrich and Rick Schute, City of Saint Paul

Cruz Correa and Cassandra Wallace, City of Dallas

Angela Rollins, City of Rochester

3:00 – 3:15 p.m. Break

3:15 – 4:00 p.m. Building Legacy Planning into the FEC Model Facilitated by: Courtney Bettle, CFE Fund

4:00 p.m. Adjourn

5:00 – 7:00 p.m. Welcome Reception Hosted by Bank On Louisville Chase Bank 416 W Jefferson St, Louisville, KY 40202

Wednesday, October 22nd, 2025

Metro United Way

334 E. Broadway, Louisville, KY 40202

8:30 – 9:00 a.m. Breakfast

9:00 –

9:30 a.m. CFE Fund Update

Facilitated by: Amelia Erwitt, CFE Fund

9:30 – 10:15 a.m. Los Angeles City Update & FE Support for Immigrant Workers Spotlight

Facilitated by: Veronica McDonnell and Aaron Strauss, City of Los Angeles

10:15 – 10:30 a.m. Break

10:30 - 11:45 a.m. Systems Change & Outcome Identification for OFEs

Facilitated by: Katie Plat, CFE Fund Brandon Coffee-Borden, National Opinion Research Center (NORC), University of Chicago

11:45 a.m. – 1:00 p.m. Working Lunch: CFE Coalition Member City Updates Detroit, Boston, Tulsa

1:00 – 4:00 p.m Louisville Site Visit Options

Louisville Urban League: The Louisville Urban League (LUL) is a non-profit, nonpartisan organization founded in 1921 that works to achieve social and economic equity for marginalized communities in Louisville. As an affiliate of the National Urban League, LUL provides direct services and advocates for change in key areas including jobs, justice, education, health, housing, and black business development. LUL has operated an FEC team since 2022.

Goodwill West Louisville Opportunity Campus: Opened in 2024, WLOC is a collaborative of more than 10 community partners. The opportunity center offers residents regular access to a child-care service, computer labs, dental services, second-chance banking, a business center, restorative justice services, workforce training, behavioral health therapy, meeting rooms, a prayer and meditation room and a café.

Neighborhood Place: Neighborhood Place is a collaborative partnership of public sector agencies that have come together to create a network of community based, “one-stop” service centers. The purpose is to provide blended and accessible health, education, employment, and human services that support children and families in their progress toward self-sufficiency. OFE and FEC is intentionally integrated into services like rental and utility assistance, SNAP, and JCPS parenting supports. This model of social service delivery serves as a nation-wide model with several states looking to Louisville for best practices.

5:00 p.m. Travel to Group Dinner

5:30 – 8:00 p.m. Group Dinner

BBC Bourbon Barrel Loft

300 W. Main Street, Louisville, KY 40202

Thursday, October 23rd, 2025 Metro United Way

334 E. Broadway, Louisville, KY 40202

8:30 – 9:00 a.m. Breakfast

9:00 – 9:30 a.m.

9:30 – 10:30 a.m.

Philadelphia City Update & Consumer Debt Navigator Spotlight

Carolina Rodriguez, Education Debt Consumer Assistance Program (EDCAP)

10:30 – 10:45 a.m. Break

10:45 – 11:15 a.m. New York City Update & Tax Season Spotlight

Facilitated by: Nichole Davis, City of New York and Grace Louis, City of New York

11:15 a.m. – 12:00 p.m. CFE Coalition Member City Updates Albuquerque, Lansing, Jackson

12:00 p.m. Adjourn

Facilitated by: José Cisneros, City of San Francisco and Nichole Davis, City of New York

12:00 p.m. Boxed Lunch (Grab & Go)

City Updates

Coalition

LOUISVILLE- JEFFERSON COUNTY

METRO GOVERNMENT

Office of Financial Empowerment

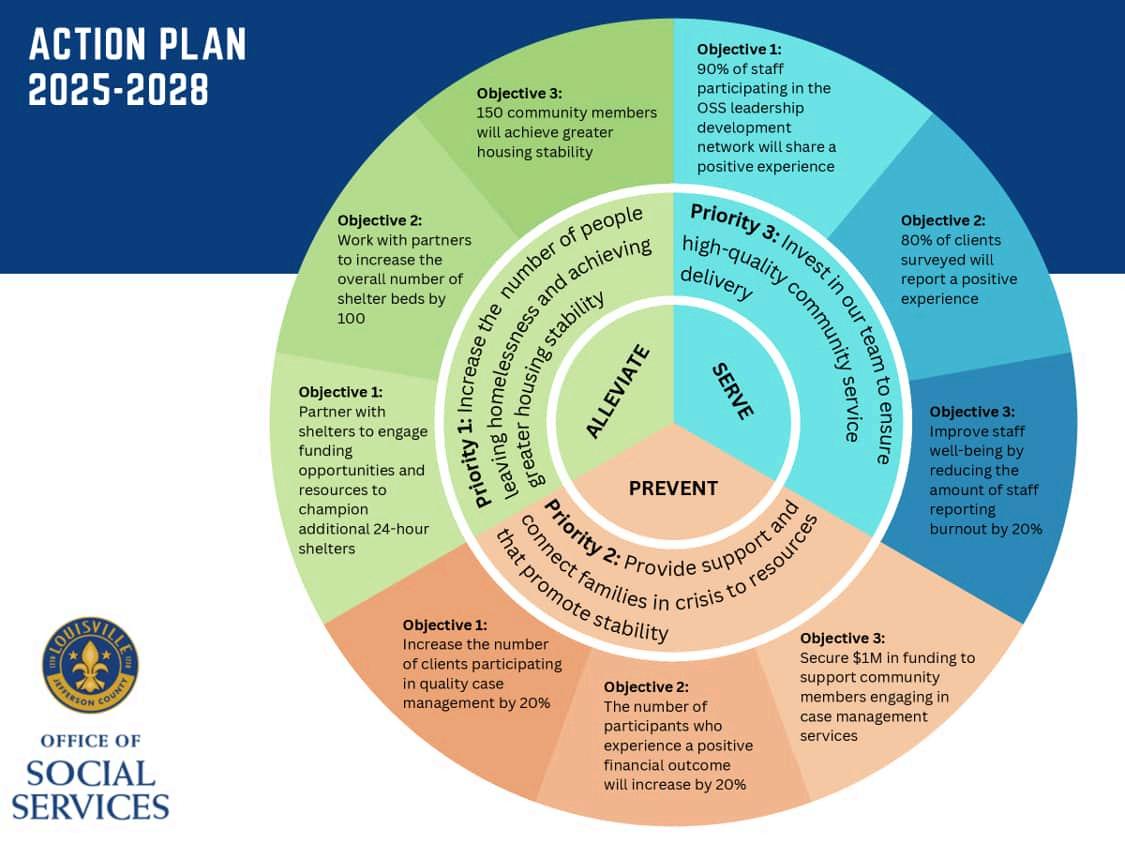

We have a new name and mission statement!

The Office of Resilience & Community Services has officially rebranded as the Office of Social Services. The name change reflects the work of our newly publicized action plan. Community feedback surveys indicated that the old name was confusing and residents didn’t always know what our department does. We are converting branding and hope to have completed by December 2025!

OFE's Mission

To strengthen the impact of OSS through enhanced economic opportunities that build financial resilience, promote economic justice, and provide access to high quality resources regardless of identity or community

OFE's Commitment to Equity

Recognizing the harmful effects of practices such as redlining and lending discrimination on generational wealth building and the systemic injustice faced by black, brown, and indigenous Louisvillians in the financial space, OFE commits to persistent learning, inspiring action, continuous dialogue, challenging systems of power, and transparency.

OFE Structure

Louisville's OFE is a branch of Louisville Metro Government's Office of Social Services, the city's social service department RCS is a public Community Action Agency OFE integrates into department social services such as rental assistance, LIHEAP, and CSBG funded poverty alleviation programs. OFE and OSS also provide financial and administrative support to the Louisville Asset Building Coalition, the local nonprofit that operates VITA. OFE funding consists of general fund dollars, CSBG funds, national nonprofit funding, foundation funding, support from financial institutions and consists of 6 full-time staff and four FEC staff employed through the Louisville Urban League

OFE is a cornerstone of the new action plan in Priority 2. All OFE programs including FEC are indicated as a key prevention strategy. As we continue to embed OFE services into all OSS branches and external partnerships, we have been able to secure sustainable funding and support by weaving our work into all aspects of Louisville’s social services ecosystem.

Strategy Highlight

OSS administers all housing and social services funding to community nonprofits through the External Agency Fund. Beginning in the FY25 year, all 71 agencies who receive funding are contractually required to meet with OFE for a technical assistance session and presented a menu of services that translates into a partnership proposal which is now required to be updated each new funding year. FY26 meetings will begin in November 2025.

LOUISVILLE- JEFFERSON COUNTY METRO GOVERNMENT

Office of Financial Empowerment Branch Highlights

OFE Strategy Areas

Integration into other branches of OSS

HEART Homeless Outreach- ~20% of FEC clients are homeless and receiving services to help boost their income and gain/maintain housing Housing & Support- joint recipient of a Bezos Day 1 Family Fund grant for over $750k to assist unhoused families with a stepping stone rent support with case management and financial counseling Scan the QR code for more information.

Senior Nutrition- Congregate meal sites receive “avoiding consumer scams” placemats with information and resources; homebound meal delivery clients with Meals on Wheels will receive OFE postcards with meal deliveries beginning when we have fully launched and announced legacy planning

Outreach & Advocacy- OSS is taking a major role in supporting residents through benefits changes under the OBBBA, and OFE is leading a workgroup to create a coordinated response Planning & Compliance- integration into external agency funded recipients through contracting process

Neighborhood Place- all clients receiving rental assistance and LiHEAP services can identify “income & asset building” supports which is an immediate referral to FEC counseling as a part of their case plan We are partners in the Single Moms’ Empowerment Series and the Men’s MENtal Health Symposium workshops and case management and have served 75 families so far through these partnerships

Integration into other LMG departments

Public Health & Wellness, Human Resources, Metro Animal Services, Parks & Recreation, Office for Women, Office for Immigrant Affairs, Louisville Free Public Library, Human Relations Commission, Office of Equity, Louisville Economic Development Alliance, Office of Housing & Community Development, LMPD, Metro Corrections, Louisville Fire, Office of Violence Prevention

Strengthening and growing our network of community partnerships with agencies from for and nonprofit sectors to build outreach capacity and sustainability.

OSS is a public Community Action Agency, and OFE is supporting and consulting for National Community Action Partnership’s Collaborative on Economic Mobility and was highlighted in September for this work Scan QR code to go to presentation.

Focusing on an “efforts to outcomes” approach to build capacity and streamline efforts.

LOUISVILLE- JEFFERSON COUNTY METRO GOVERNMENT

Office of Financial Empowerment

Program Highlights

Financial Empowerment Center (launched 2022)

Enhanced Program Assets

Small Business Boost

Financial Health Equity

Protect Borrowers

FEC Leadership Fellows

Fines & Fees/ Eviction Diversion

Delta Home Down Payment Assistance Outcomes

2415 clients served

$3.1 million in non mortgage debt reduced

1293 clients with outcomes

157 community partnerships

Strategy Highlight

Over the summer, LFEC partnered with Center for Accessible Living and Gathering Stength to offer classes and one on one appointments with a focus on the intersection of finances and disability We served over 50 participants with Center for Accessible Living series and nearly 200 participants including individuals with disabilities and service providers across several states with tools and resources locally and connecting providers to other FECs who serve their local population.

Strategy Highlight

Bank On Louisville (launched 2010)

Enhanced Program Assets

Digital Equity partnership

Banking integration with housing authority

Final report for Kroger partnership released

Workforce integration with Chefs for Success Outcomes

175,000 accounts opened

12 financial institution partne

15 years of continuous operat

Bank On Louisville has partnered with Salvation Army for their Chefs for Success program where participants looking to start a career in the culinary field receive hands on training with a chef instructor who teaches ServSafe certification, cooking and plating techniques, and flavor pairing over 6 weeks. BOL teaches a class each week for the first four weeks covering banking and budgeting, consumer rights, asset building, credit and debt, and small business in partnership with LFEC and Small Business Boost

CFE Coalition Meeting City Update, October 2025

OFE convenes, innovates, and advocates to strengthen the economic security and mobility of all San Franciscans

WHAT’S NEW

Youth Accounts

We’ve published a new report on noncustodial youth accounts in collaboration with MyPath. In this report, we dispel common myths and identify several noncustodial youth accounts offered in the SF Bay Area.

In partnership with the SF Juvenile Probation Department, we've expanded banking access for young people in the city's Juvenile Detention Center, allowing them to open free bank accounts and receive financial counseling to manage their money confidently.

“Finances is a lot like riding a bike You can talk about it all day, you could even have a PhD in riding a bike, but you have to ride it in order to learn You also need to actually have a bike to ride in the same way that youth need a bank account to learn how to manage their finances. Youth might make mistakes at first, but those are important to help us learn.”

- Norel, MyPath Youth POWER Leader

Socially Responsible Banking

In a new report, we summarize the findings from our listening session findings and make recommendations for banks to boost financial inclusion

StopScamsSF - An Initiative to Combat Scams

San Francisco's Treasurer's Office is launching the StopScamsSF initiative to protect vulnerable residents and restore confidence in public institutions. This comprehensive program uses five integrated strategies to fight scams:

A citywide, multilingual communications campaign

Develop a monitoring and alert system

"Scam-proof" official messages from the City and creating a 311 Payment Verification Directory

Create a Scam Prevention Partners Table

Create a free StopScams Playbook with alert templates and training

Emergency Preparedness Planning

We’ve published a new toolkit to support San Franciscans prepare for financial emergencies, such as, safeguarding bank accounts, assets, and what to do if a loved one is detained or deported.

Advancing CalAccount Implementation

In collaboration with the CalAccount Community Coalition, we are engaging on implementation planning for CalAccount. This program will offer no-fee, no-penalty, federally-insured transaction accounts with debit cards, direct deposit, automatic bill pay, and recurring payment options. It also includes credit-building tools to help users establish or improve their credit history. The program will prioritize outreach to communities disproportionately impacted by financial exclusion, including Black, Latino, and immigrant households, as well as individuals experiencing homelessness or housing instability We are developing a template for regional roll-out strategy

CFE Coalition Meeting City Update, October 2025

OFE convenes, innovates, and advocates to strengthen the economic security and mobility of all San Franciscans

HIGHLIGHTS

Kindergarten to College

Successfully encouraged SF students to claim their K2C and CalKIDS college savings. The multi-lingual effort utilized diverse communication channels, including in-person outreach at graduations The campaign also leveraged an Instagram Reel featuring the Mayor and Treasurer to boost participation

To date, K2C has disbursed more than $2.8M to over 4,600 San Francisco graduates (Classes of 2023, 2024 & 2025) to use continuing their education after high school.

K2C program evaluation continues with qualitative findings released. We highlight students’ and parents' experiences with K2C in a new published report.

FEC

During this past year, San Francisco has served over 1,000 clients in 2,892 sessions since becoming an FEC in Sept 2024 That's a 67% increase in new clients

San Francisco's adoption of FECBOT has enabled counselors to collect more accurate data on the client impact they've had. For example, they've supported clients to achieve 1,195 official outcomes in the past year, which is about twice the number of outcomes they've been able to capture in previous years. This includes supporting clients to:

Increase savings by $946,374

Reduce more than $1M in non-mortgage debt

Working with County Assessor’s Office on rolling out the legacy planning module. They collaborate with a legal services provider to provide free estate plans for low-income homeowners.

Collaborating with Mayor’s Office on economic justice integration into RV Buyback Pilot, including financial counseling, banking access, and debt relief

Financial Justice

San Francisco contributed to a newly released strategy guide by Results for America on fine and fee reform

The Financial Justice Project has partnered with Results for America and the Fines and Fees Justice Center on Cities and Counties for Fine and Fee Justice (CCFFJ), a national leadership network of local places committed to meaningful fine and fee reform. In the last fiscal year, there were 203,594 San Francisco Museums for All admissions, or 8% of all SF museum admissions

In the last fiscal year, we issued about $640,700 in direct payments to over 2,000 jurors, through our Be The Jury program.

SF Lends

Since its launch in December 2023, SF Lends has helped 10 small businesses access over $2 million dollars in working capital ($1.56 million in loans and $500,000 in lines of credit) from four banks.

SF Lends banks are also actively referring small business owners to CDFIs and technical assistance providers for support

CFE Coalition Meeting City Update, October 2025

OFE convenes, innovates, and advocates to strengthen the economic security and mobility of all San Franciscans

NEW REPORTS

K2C Qualitative Results

This new qualitative evaluation of San Francisco’s K2C program reveals that early college savings accounts have a meaningful impact on students and families

Youth Banking Financial Emergency Guide

In a partnership with the SF Office of Community Engagement and Immigrant Affairs, we released a guide to promote economic security and financial resilience during times of uncertainty

This new brief advocates for expanding access to noncustodial youth bank accounts, which allow individuals under 18 to open and manage accounts independently

Socially Responsible Banking

In this new 2025 report, we outline San Francisco’s efforts to promote equitable access to financial services through its Socially Responsible Banking initiative

CFE COALITION UPDATE

OCTOBER

2025

Coming Soon: Drivers of Opportunity

The Office of Community Care and Empowerment is now the Office of Housing and Community Empowerment! As a part of the City of Dallas's focus on reimagining service, several departments were consolidated to create this new office, which will oversee the City's housing, homelessness and social services program. The new Office has been charged with advancing a new "Drivers of Opportunity" framework to advance financial empowerment and upward economic mobility for all Dallasites.

The FEC program was temporarily paused for strategic realignment during much of 2025. HCE is finalizing a new contract with a nonprofit to serve as a Financial Empowerment Center for FY26, whichwillrelaunchourprogram.Simultaneously,HCEis piloting internal service delivery in alignment with our re-entry services strategy, with staff completing training asofnow.

Volunteer Income Tax Assistance (VITA)

- 1,749 Dallas residents served

- 6,004 counseling sessions completed

- $514,102 total increased savings

- $1,168,715 total decreased non-mortgage debt

The City has continued its partnership with Foundation Communities for the Community Tax Centers. For the 2025 tax year, x returns were filed, with x EITC filers and $ in total refunds claimed

Other Programs

HCE has added two new partners, Housing Connector and Volunteers of America, in our reentry programming. This helps us to realize an updated to our programmatic model which is to align housing support, job training and placement, financial coaching and wraparound case management for clients.

City of Saint Paul Office of Financial Empowerment October 2025 Update

The Office of Financial Empowerment (OFE) advances economic democracy by ensuring that all Saint Paul residents have access to tools, resources, and opportunities that help them thrive financially. Our department leads innovative, community-rooted efforts to share in the city’s economic prosperity, supporting families in building wealth, accessing opportunity, and living with dignity and stability.

OFE’s work is guided by a Results Framework that seeks to achieve the following outcomes:

• Result 1: Saint Paul residents achieve financial health.

• Result 2: Saint Paul neighborhoods achieve community wealth.

• Result 3: Saint Paul residents live in stable, accessible, fair, and equitable housing.

• Result 4: Families with children in Saint Paul have a city that cares about their future.

• Result 5: Saint Paul residents are engaged in public decision-making.

Together, these results reflect OFE’s commitment to both individual opportunity and systemic change, ensuring our work meets people where they are, while building toward an inclusive and resilient local economy.

Recent Department Successes

CollegeBound Saint Paul

CollegeBound Saint Paul is the city’s children’s savings account program. The first “at-birth” citywide college savings account program of its kind, CollegeBound Saint Paul helps families build a strong foundation to invest in their children’s education and future.

The oldest CollegeBound Saint Paul participants will be starting Kindergarten this fall, 2025!

COLLEGEBOUND BY THE NUMBERS

• Launched on January 1, 2020

• 18,000+ babies enrolled in CollegeBound Saint Paul

• $3,600,000+ saved in seed deposits and other savings

• 20+ Community Outreach, Referral and Engagement Partners

• 24 Community Ambassadors

Other successes:

- Hosted fourth year of Money Action Day in partnership with Saint Paul nonprofit, Prepare + Prosper, where we connected over 300 people to financial health resources in the community and a day of fun for families.

City of Saint Paul Office of Financial Empowerment October 2025 Update

- Family Deposit Days: CollegeBound has been offering three Family Deposit Days a year for families to come to Bremer to make deposits for the first time in their children’s accounts. We have had 2 events in 2025 so far with over 200 families who made deposits totaling over $11,000

- Tax Promotion: CollegeBound Saint Paul promoted tax time savings through outreach efforts and mailers by offering an extra incentive to families who saved part of their tax refund into their child’s CollegeBound account; families made 517 deposits during the tax time in 242 unique accounts. Have started to think with our VITA partner about how we might use our tax-time promotion to inform families about IRS phasing out paper checks and connecting to bank accounts and to Bank On Minnesota.

CollegeBound Saint Paul Elementary

CollegeBound Saint Paul Elementary is entering its second year of partnership with Saint Paul Public Schools. As CollegeBound Saint Paul’s oldest participants enter Kindergarten, CollegeBound Elementary will continue to serve all enrolled Pre-K students, as well as all enrolled Kindergarten students in SPPS, adding 5 schools and more than doubling the number of students impacted. We are excited to continue our partnership with Saint Paul Public Schools to boost child savings, increase whole family wealth, and increase College and Career readiness opportunities for children and families. CollegeBound Elementary will be exploring potential partnerships with non-SPPS schools in an attempt to make sure all of Saint Paul’s children have access to the program.

Successes

• Held an in-school Deposit Day event in every Saint Paul Public Schools Pre-K classroom, serving over 1500 students and contributing $19,460 to CollegeBound accounts

• Brought on 8 Parent Champion volunteers to serve as CollegeBound Elementary liaisons at their child’s school

• Hosted its first Family Deposit Day specifically for Saint Paul Public School families

Priorities

City

• For the remainder of 2025 the CollegeBound Elementary Team will be focusing on:

o Generating awareness and excitement among school staff and parents

o Scaling up In-School Deposit Days to include Pre-K and Kindergarten

o Enrolling all Saint Paul Public Schools’ Pre-K and Kindergarten students in CollegeBound

o Kicking off and supporting Deposit Days in 5 more SPPS elementary schools

o Recruiting Parent Champions as each SPPS elementary school

• In 2026 the CollegeBound Elementary team will be:

o Piloting a 1st grade field trip to a bank

o Integrating CollegeBound Elementary curriculum into student Personalized Learning Plans

o Exploring partnerships with non-SPPS schools to expand the impact of CollegeBound Elementary

Guaranteed Income: CollegeBound Boost & Advocacy

• The City completed the monthly income payments to the 333 families that were selected to receive guaranteed income through CollegeBound Boost. As of August 15, 2025, families received $4,079,250 in unrestricted, regular income ($4 M in ARP funding, and the remaining was funded through private donations and a grant from MN DHS). We also deposited $789,000 into the CollegeBound accounts of the 789 children participating in Boost (who received quarterly progressive deposits totally $1,000 each).

• Research with the University of Michigan is ongoing, and the team have been collecting 24-month surveys from families. We have been providing offboarding services for participants: informing participants of their options to remove any remaining funds from their ReliaCard, referrals to partner organizations for financial counseling or coaching, and optional benefits counseling to review if there are additional resources for which families qualify that can help them with the transition of no longer receiving the monthly income.

• We are also working with partners to promote guaranteed income in Minnesota and at the national level:

o Mayor Carter leads national advocacy efforts as a co-chair of the Mayors for a Guaranteed Income network. The Office of Financial Empowerment is a member and on the steering committee of the Minnesota Financial Opportunity Coalition, which has advocated for state-funding for guaranteed income and cash assistance in the Minnesota legislature. We are also working with other basic income programs in the state to tell the story of cash transfer programs in Minnesota and lift up the stories from participants in the programs.

o The Coalition held a webinar on September 18 during US Basic Income Week to highlight impact of guaranteed income and the success stories from pilot programs across Minnesota. Also featured State Representative Athena Hollins and Mayor Carter.

o The City is also working with the Saint Paul & Minnesota Foundation to secure additional funding for additional guaranteed income programs locally. This year, we helped the Interfaith Fund secure funding from the Kresge Foundation to expand guaranteed income to a new cohort of 25 American Indian participants in their Economic Mobility Hub, an initiative to support economic stability and opportunity for American Indian families in the East Metro.

Medical Debt Reset Initiative

The City of Saint Paul is partnering with Undue Medical Debt to acquire and cancel medical debt from local health systems. Undue Medical Debt, a national, independent nonprofit organization, acquires medical debt portfolios from health systems. The City is allocating $1.1 million in American Rescue Plan funds to erase an estimated $100 million in medical debt for eligible Saint Paul residents with incomes below 400% FPL. Residents can not apply for debt cancelation, they will be notified by Undue Medical Debt through the mail if their debt has been canceled as a part of the initiative. To date, we have purchased medical debt from Fairview Health Services, and is working with Undue Medical Debt to expand the initiative to the other health systems and hospitals in Saint Paul so that we can bring debt relief to more Saint Paul residents.

Undue Medical Debt collected testimonies from some of the residents who had their debt relieved:

• The debt that was paid off by Undue Medical Debt was from 2015, when I was only 19 years old. I was battling drug addiction at that time and was in and out of the hospital for various reasons due to my addiction. I am now sober and work at a treatment facility helping people that are still struggling. I am so thankful for the relief that Undue Medical Debt has given me. – Jenna

• I am a single mother of five children, and this program has definitely relieved some stress and anxiety from my life. This program covered a medical debt of mine (about 10 years old) that I was not able to afford to pay off. I am above and beyond appreciative for this debt relief. – Anissa B.

Emergency Financial Empowerment Opportunity

Saint Paul is one of the cities participating in the CFE Emergency Financial Empowerment Initiative to embed financial stability strategies into the City’s existing emergency and disaster preparedness and response work to better support residents in prioritizing

City of Saint Paul Office of Financial Empowerment

financial concerns and mitigating financial disruptions during disasters. OFE is partnering with our Emergency Management Department to implement the project. We are working in partnership with the City’s Office of Technology & Communications to build a Financial Health Resource Hub that will include financial empowerment programs available to Saint Paul residents, but also emergency preparedness resources. We hope that the Resource Hub can also serve as a central communication hub for the City during an emergency.

LOCAL Fund: Worker & Community Ownership programs

As part of a Citywide strategy to build institutional commitment to community wealth building, the City created the LOCAL Fund which comprises of two programs: Worker Ownership and Community Ownership. The LOCAL Fund uses shared ownership models as approaches to build community wealth, anchor jobs locally, and grow the local economy and tax base. The Worker Ownership program offers grants and technical assistance for worker co-op startups, conversions of existing businesses, and existing co-ops. The Community Ownership program supports community-owned entities with grants and technical assistance for predevelopment, acquisition, demolition, and rehabilitation of commercial properties.

Successes

• The Worker Ownership program has given out four grants totaling $420,000 to four worker owned cooperatives in Saint Paul.

• Both the Worker Ownership and Community Ownership programs continue to provide technical assistance to interested small businesses and community groups that want to explore whether shared ownership models are the right fit.

Priorities for remainder of the year and 2026

• Continue to raise awareness and promote the LOCAL Fund and shared ownership models as forms of economic development.

• Award up to 3 more grants to small businesses that want to start up and/or transition into a worker owned cooperative.

• Award up to 6 grants to community owned groups that are interested in developing commercial real estate investment cooperatives.

FAIR HOUSING

Tenant Protections was passed in May 2025 by Saint Paul’s City Council. OFE and the Department of Safety and Inspections team are planning towards the implementation in May 2026.

October 2025 CFE Coalition City Update

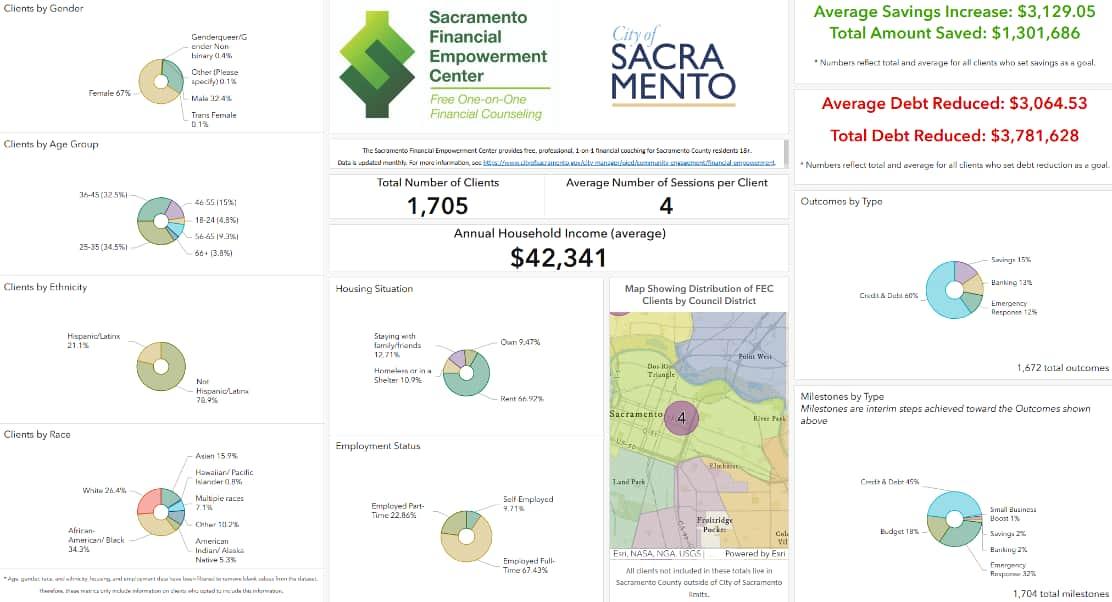

In line with our City’s policies around contract relationships, in early spring we put our Financial Empowerment Center lead partner role out for bid. The RFP process resulted in a decision to diversify our FEC partnerships. We have kept on our original and previously only partner, the Sacramento office of International Rescue Committee, and have added Health Education Council, a 35-year-old local organization with very stable leadership (the founding Executive Director is still at the helm) that focuses on the various social determinants of health, including financial wellbeing. We are working with HEC to get their coaching service up and running hopefully by the end of this year, and are excited about the potential of this new partnership while maintaining our original one as well.

IRC’s student loan counselor, who has become an integrated part of the FEC team thanks to Student Loan Empowerment Network funding from the California Department of Financial Protection and Innovation, continues to significantly boost the FEC’s debt reduction numbers, which are now approaching $4 million. Given the ongoing ever-changing landscape of student loans, we hope the state will be able to continue the SLEN program after current funding is set to end in January. Below are our FEC stats as of September 30, 2025.

In April our report included information about a potential new local Sacramento chapter of the Asset Funders Network, but that road came to a dead end when an insufficient number of funders were able to commit to the AFN membership fees. The FE Manager and a few colleagues at the City are working on an alternative no-cost entity around asset building work that we are calling Sac LIFT (Local Impact Funders Table), which would consist of quarterly funder gatherings of financial institutions and other philanthropic entities, at which members would share information and strategies and potentially build collaborative efforts. We plan to integrate conversations about implementing our CityStart and Financial Empowerment Cities strategic plans into this soon-to-emerge dialogue.

Our City’s Economic Development Department, in which the FE work is housed, is also embarking on a strategic plan for the first time in quite a while, and this dovetails well with both the recent appointment of a new City Manager who will start in January and a recent City Council priority-setting workshop in which Economic Development scored highest in the voting process. The new City Manager, Maraskeshia Smith, will be the first Black woman to ever hold the job in the City, coming to Sacramento from the same post in Santa Rosa and bringing experience from a long public service career that has included a focus on equity. Preliminarily this all bodes well for good potential FE progress in 2026.

After years of ultimately fruitless efforts to encourage Sacramento County to partner around Financial Empowerment, we had a breakthrough recently thanks to one of the members of our Economic Mobility Ambassadors team, through which we pay stipends to trusted local leaders to promote financial coaching, workforce, and small business support resources of the City and community partners, and to help people connect with those directly. At press time for this report the FE Manager was a few days from a key meeting with some County executives on this subject, and will hopefully have more to report in person at the Coalition convening.

After the subject came up in recent conversations with both the FEC coaching team and in a presentation that the FE Manager did for some new staff at Legal Services of Northern California, there is a fledgling effort to build local capacity for a campaign and associated assistance regarding fraud and scams. Hopefully more to come on that next time!

City of Rochester October 2025 Update

Rochester Financial Empowerment Center (FEC) provides free, 1-1 professional financial counseling as a public service.

• Small Business Boost: The City of Rochester was selected to participate in CFE Fund’s Small Business Boost Initiative. Originally piloted in 2022, we are excited to expand our financial counseling into the small business resources offered by the City of Rochester.

• Legacy Planning: We will be integrating financial counseling into estate planning services, including the new “Legacy Planning” component of FEC services and our existing estate planning program with the local legal aid nonprofit, Just Cause.

• Homeownership Pipeline: The FEC has been integrated into the City’s homeownership grants process, where clients who are not ready for homebuyer grants are referred to the FEC.

Bank On Rochester will improve access to safe and affordable bank products for communities who've been historically excluded from financial institutions.

• In talks with three financial institutions to become Bank On Certified: Canandaigua National Bank, Five Star Bank, and Community Bank

• Working with our local VITA program to offer Bank On account openings with Thompkins Bank on site for a 2nd year in a row

• Convening a community engagement committee to create an outreach strategy for the Modernizing Payments Executive Order, which will end paper checks for federal programs

• Special focus on youth banking access in partnership with our Department of Recreation & Youth Services. Participating in a variety of outreach events to engage youth and their families in financial education and account openings

Emergency Management Financial Empowerment: Rochester was selected to participate in CFE Fund’s first ever Emergency Management Financial Empowerment cohort. We are partnering with the Rochester’s first ever Emergency Manager to build financial preparedness into the City’s emergency management plan for the City of Rochester.

• We will begin offer a train-the-trainer series to local emergency management and lowincome service providers to train them on financial preparedness and recovery. We will offer 10 trainings over the next 12 months with the goal of reaching approximately 300 directservice professionals across the City. Participants will include partners such as 211, 311, local nonprofits, and government service providers.

R-Future Fund: Children Savings Account programs are growing in popularity across the United States. Research shows that $500 or less in the pockets of moderate and low income children increases their likelihood of attending college by three times, and graduating college by four times. RFuture Fund is aimed to reduce the disparity in wealth among Rochester youth - particularly for Black and Brown, low-income residents.

• After an extensive design and planning process, we are set to launch a 2 year pilot program, “R-Future Fund” in early 2026

• Children in Kindergarten who are signed up for existing City of Rochester Recreation Services will be automatically enrolled in the program. We are working with our charter schools and city school district to establish data sharing which would allow automatic enrollment for the 2nd year of the pilot. Automatic enrollment with our district seems unlikely at this point.

• R Future Fund will offer every Kindergartner a savings account with a $15 seed deposit, an additional $15 equity bonus for children living in poverty, and up to $30 a year in bonuses for eligible activities. Once the children finish school they will be able to use their savings account for anything related to increasing their economic mobility.

Positive Rent Reporting provides opportunities for residents with poor or no credit history to improve their credit scores and make progress towards mortgage readiness.

• In January we kicked off our partnership with the Credit Builders Alliance, who provided 6 months of comprehensive training and implementation guidance to three local housing providers: The Rochester Housing Authority, Hart Homes, and Rosey Property Management.

• We will be partnering with the Rochester Housing Authority to offer rent reporting and financial counseling to up to 400 public housing tenants in 2026

Homeowners Guide to Building Generational Wealth was launched this summer to consolidate information and resources for new homeowners related to preserving the wealth within their home. This includes tax and foreclosure resources, home repair and maintenance support, and estate planning.

• Guide is being distributed across City service centers and nonprofit housing counseling agencies

• We are hosting a Generational W ealth Summit this November to provide onsite resources related to home repair, maintenance, tax exemptions, foreclosure prevention, banking access, and more.

• We continue to partner with Just Cause, a local legal aid nonprofit, to provide free estate planning services to 100 income eligible homeowners

Kiva Rochester Small Business Loans are 0% interest small business loans from $1,000-$15,000 and crowdfunded $25 at a time. Since its launch in 2016, the City has funded over $1.2 million to over 200 small and micro businesses. Kiva is truly the first step of the capital ladder for these businesses.

• The OFE partners with over a dozen entrepreneurial programs to embed and advertise Kiva loans

• Kiva loan recipients are offered financial counseling, business coaching, and connected to larger financing options such as local CDFIs or the City’s Neighborhood and Business Development

Prepare to Prosper Business Academy has served 50 small minority owned businesses and will serve an additional 25 in 2026.

• This training provides participating businesses marketing plans, tax filing, bookkeeping training, MWBE certification, cash flow and projections, and business plans to thoroughly prepare them to take the next steps to grow and sustain their businesses. This program emphasizes relationship building among participants and more mature businesses in the community to develop authentic opportunities for mentorship.

• In 2026 we will add Human Resource & Branding services to the next cohort of participants

CFE Fund Updates – Fall 2025

Bank On

The Bank On movement has reached a significant milestone: there are now more than 500 publicly available accounts certified as meeting the Bank On National Account Standards (with many more on the way!) The Bank On team continues to work to bring new financial institutions into the movement, with extensive targeted outreach to credit unions and smaller financial institutions.

In August, we released two RFPs for coalition partners interested in building or strengthening their banking access efforts. Applications just closed for Bank On Academy (for prospective coalitions or coalitions with new leadership seeking foundational training) and the new Bank On Integration Accelerator Grant (for active coalitions). We received close to 20 applications for the Bank On Integration Accelerator opportunity; evaluations are underway with decisions to be announced later this month. We’ll also enroll a cohort of approximately 35 new and relaunching coalitions through Bank On Academy. Technical assistance to these new cohorts will begin in November, with a multi-phased approach of cohort-based learning and individual technical assistance. We also extended invitations to a select group of coalitions for the fifth cohort of the Bank On Fellowship, with grantees to be finalized this month. We select 5 organizations from this invitation-only opportunity to hire full-time Bank On coalition leadership. These technical assistance and grant opportunities are enhanced by our broader learning community offerings available to all active and prospective Bank On coalitions throughout the year.

Additionally, the Bank On team continues to expand our work building programmatic banking access integrations, including supporting partners building banking access moments into workforce, transit, unemployment, and prisoner reentry systems. Bank On team members are implementing creative new approaches to support coalitions in pivoting their efforts towards scalable integrations. In August, two team members traveled to Albuquerque, NM to facilitate a day-long strategy session with NM Department of Workforce Solutions officials and the three New Mexico-based Bank On coalitions This inperson session represents a new and promising approach to supporting state-level partners in integrating banking access into their public benefit and workforce systems. Summer Jobs Connect

In its 12th year, the Summer Jobs Connect initiative continues to support youth workforce programs in embedding banking access and financial education into their programs. The CFE Fund has welcomed the fourth cohort of SJC Academy, our Summer Jobs Connect entry point, in which we engage summer youth employment programs and other types of youth workforce programs with robust technical assistance to help them develop a plan for integrating banking access and financial empowerment services into their programs. The fourth cohort of SJC Academy includes Bronx, NY (which represents four workforce boards and four summer youth employment programs); Houston/Galveston, TX; Hopkins, MN; Hutchinson, KS; Long Beach, CA; Monroe, LA; San Diego, CA; and Tampa Bay, FL.

Financial Empowerment Center (FEC) Replication Initiative

The FEC Public movement continues to gain momentum; a total of 97 cities and counties have engaged in FEC Public, including 38 cities and counties who have already launched active local FEC public counseling initiatives. Recently, Jefferson County (WI) launched their FEC; Charleston (SC), Howard County (MD), and St. Louis (MO) also submitted Implementation proposals and have been approved to move into the “build phase.” An new cohort of FEC Academy began in October 2025 (Albuquerque, NM: Madison, MI; and Riverside County, CA).

The second phase of the Small Business Boost (SBB) FEC partnership program is underway. Participating FECs in this phase include: Akron, OH; Aurora, IL; Columbus, OH; Louisville, KY; Polk County, IA; Rochester, NY; and Sacramento, CA. Small Business Boost was initially piloted in 2022 with five cities to explore how FEC counseling could help entrepreneurs and small business people to stabilize and improve their personal finances as a foundation for building and growing a sustainable business. This second phase of SBB integrates FECs with small business development and entrepreneurship programs in an additional set of municipalities, while also diving deeper into the impact of FECs on the financial health and small business journey of early-stage entrepreneurs. The second phase of the pilot kicked off in December 2024. After an initial planning and training period, FECs launched targeted services for small business clients in March 2025. To date, financial counselors have facilitated over 700 sessions with 352 clients. The CFE Fund also was invited to present a workshop about the SBB pilot and the intersection of personal and business finances at the Prosperity Summit in Washington, DC earlier this month.

The CFE Fund also received funding from the Wells Fargo Foundation to create a new professional development opportunity for FEC Local Government Managers to further advance their FEC management skills: FEC Leadership Fellows. Selected Local Government Managers include those from Aurora, IL; Baltimore, MD; Greenville County, SC; Louisville, KY; and Polk County, IA. This new opportunity launched in May 2025 with an

in-person convening at the CFE Fund’s New York City office; after a series of additional cohort learning calls, the cohort convened one final time in-person in September 2025.

Finally, with funding from the Bloomberg Philanthropies’ Greenwood Initiative, the CFE Fund is continuing to work to incorporate legacy planning counseling services into the national FEC Public initiative. We are implementing legacy planning into the FECs across two cohorts in 2025; the first cohort of 13 FECs had their kickoff convening in New York in March, began training in May, and began providing legacy planning services in July 2025.

The second cohort of 18 FECs had their kickoff convening in New York in June 2025, began training in July, and launched services in September 2025. To date, more than 2,200 clients have been introduced to legacy planning and over 300 clients have begun working on legacy planning activities. The CFE Fund will coordinate a national and local announcement about this new legacy planning service as a core component of the FEC model at the end of October.

Financial Empowerment Cities

The CFE Fund continues to support local leaders through our FE Cities initiative as they work to launch and lead new local Offices of Financial Empowerment. While the first cohort of FE Cities (Jackson, TN; Pittsburgh, PA; Rochester, NY; and Tulsa, OK) have finished the core FE Cities grant engagement, we are continuing to work with Tulsa through an “accelerator fund” grant to supercharge a discrete project that supports OFE operations. Rochester and Jackson have wrapped up their accelerator fund projects, both focused on fundraising for CSA programs in their respective cities.

The second FE Cities cohort (Albuquerque, NM; Dallas, TX; Los Angeles, CA; and Sacramento, CA) has begun its second year of the engagement. All four have hosted the CFE Fund for site visits and are working to synthesize site visit findings and information from their landscape analysis to begin crafting their strategic plan, a key tool for launching the OFE in the second year of the grant. Each also used their site visit to build OFE momentum: for example, Albuquerque hosted a public launch of their OFE featuring the Mayor and other key stakeholders, and Sacramento combined it with their CityStart blueprint launch and their inaugural OFE Advisory Group meeting. The CFE Fund brought on five CFE Coalition members (Boston, MA; Denver, CO; Lansing, MI; New York, NY; and St. Paul, MN) to serve as expert mentors to FE Cities grantees, advising on topics such as program development, communications, and public funding strategies. We also are excited to welcome our third cohort of FE Cities (Little Rock, AR and Nashville, TN). Both cities joined our most recent CFE Coalition convening in Lansing. While Little Rock has their FE Leader in place and is in the process of conducting their landscape analysis and planning their site visit, we are playing an active role in guiding Nashville through their hiring

process. We plan to host all active FE Leaders for an in-person convening in New York in mid-January.

An RFP for fourth cohort of FE Cities grantee was released last month with applications due November 14th .

Consumer Financial Protection Initiative

The CFPI team is currently focused on developing new resources to support the local consumer financial protection movement. We recently received a new grant from the Annie E. Casey Foundation to support a new approach to our national convenings. We will host the first of two workshop-oriented convenings January 21-22 in Baltimore, MD focused on litigation and enforcement strategy; formal invitation with registration information will be available soon. The second convening, anticipated for late Spring, will focus on strategic communications that can amplify the impact of consumer protection efforts. We also highlighted essential local consumer protection work in Cuyahoga County, OH and Denver, CO in the most recent issue of our Skyline newsletter; both will participate in deep dive webinars in October and December.

CityStart

The CityStart team continues to work with local governments around a structured approach to identify financial empowerment goals, convene relevant stakeholders for sustainable success, develop actionable strategies, and ultimately craft a blueprint rooted in local insights and opportunities to consider and expand access to wealth and build wealth equity. The CityStart team is working closely with grantees to identify how best to speak about racial wealth equity work under the current political climate.

All partners from our fourth CityStart cohort with a wealth equity focus (Kansas City, MO; Memphis, TN; Milwaukee, WI; Savannah, GA; and St. Petersburg, FL) have completed their site visits. During each site visit, the CFE Fund facilitated roundtable discussions with a range of stakeholders as well as individual meetings with senior officials, including mayors and heads of departments, to gain a deeper understanding of the localities’ priorities and opportunities. This cohort will now build their “story of wealth,” which includes collecting data on current local wealth disparities and identifying data gaps, exploring local policies and practices that currently or historically have impacted wealth accumulation and extraction, and engaging residents to collect their input on these issues. To support this phase of their work, the CFE Fund convened the cohort in New York City on October 15th and 16th. The convening was an opportunity for grantees to share learnings and themes that

arose from their site visits and set up their story of wealth work. The convening also included a resident engagement session led by Third Space Labs and a narrative change session led by Race Forward.

Previous cohorts are focusing on finalizing their “story of wealth” as part of their eventual municipal financial empowerment blueprint and identifying actions to which the municipality can sustainably commit. Others are working to finalize their blueprints and release strategies to release this fall. As one example, Newark, NJ released their blueprint in July and created a framework highlighting a “financial well-being continuum.” Their framework and actions included:

• Stabilize: Focuses on a residents’ financial health by increasing their earning and income to cover essential living expense and improving their access to financial institutions, financial knowledge, and financial services

• Secure: Focuses on residents’ financial resilience by expanding access to programs, resources and services to increase their savings and net worth

• Sustain: Focuses on residents’ financial longevity by increasing their access to, knowledge of, and utilization of wealth building and estate-planning tools and on building residents’ power to accumulate and transfer wealth to their communities and future generations.

Emergency Financial Empowerment

The CFE Fund’s Emergency Financial Empowerment (EFE) initiative continues to work with Offices of Emergency Management, or the emergency management entity in a given locality, to build and expand emergency preparedness and recovery infrastructure to support the financial stability of residents and streamlined deployment of financial empowerment resources as part of their emergency response procedures.

All grantees from our first cohort (Dallas, TX; Gainesville, FL; Rochester, NY; St. Louis, MO; and St. Paul, MN) are currently developing Implementation Plans, which will include their ideas to integrate and enhance financial empowerment opportunities within local emergency processes and plans; galvanize or create partner networks (possibly launching local Financial Empowerment Networks); provide disaster preparedness trainings for community partners already doing financial empowerment work; and deploy public awareness tools and resources.

The CFE Fund team is currently accepting proposals for the second cohort of grantees, with applications due November 10.

Administrative Updates

Since the last CFE Coalition meeting, the CFE Fund has hired a new Senior Associate to support Financial Empowerment Center work; Zach Etzin joined the team in April.

In the fiscal year ending June 30, 2025, 2,754 households were referred to financial coaching services. Through personalized coaching sessions, 1,491 households improved their financial well-being, increasing their household income by $4,607,416. This was achieved through:

80 households successfully lowered their debt-to-incomeratioby$31,076. 80householdsimprovedtheircreditscore.

DepartmentalConsolidation

During this year ' s budget season, Mayor Karen Bass recommended consolidating the Department of Aging, Economic and Workforce Development Department, and Youth Development Department into the Community Investment for Families Department (CIFD). CIFD was instructed to present a roadmap for creating an integrated department that will deliver coordinated, equitable, and outcomedriven services to the residents and businesses of Los Angeles This effort is not simply a costsaving measure; it is driven by the need to streamline services by leveraging shared administrative infrastructure across departments with similar functions, freeing up resources to focus on service impact and outcomes.

CIFD leadership presented this report to the City Council in August, and the City's Chief Administrative Officer and Chief Legislative Analyst are preparing reports on the proposed consolidation'sfiscalandprogrammaticimpact.

Abigail R. Marquez General Manager

IPV/TAYGuaranteedIncome (STAYSAFE)

CityCouncilapprovedCIFD’sprogramdesignfor a new $2 million Guaranteed Income program, STAY SAFE - Supporting Transitional Aged Youth and Survivors Achieve Financial Empowerment. The program will provide 84 participants - 42 from Council District 9 and 13, the two funding Council Districts - with $24,000 in unconditional financial assistance distributed over two years Participants will choose between 24 months of $1,000 per month or a $6,000 lump sum payment accompanied by 18 months of $1,000 per month. We will also connect participants with workforce opportunities via the Los Angeles Hospitality Training Academy and other vital resources such as financial coaching, housing navigation, and more. Our goal is to release the program application in October and issue the first round of disbursements before the end of theyear.

ULAIncomeSupportProgram

CIFDispartneringwiththeLosAngelesHousing Department to administer a $14.6 million income support program for households with seniors and/or people with disabilities. Our joint report to the City Council is in its final stages. It will outline the proposed program design, priority populations, contracted partners for outreach and implementation, recommended staffing positions, and other key components necessary for successful programlaunch

RegionalEmergencyFund

In response to aggressive, ongoing federal immigration enforcement actions in Los Angeles, the Mayor’s Office worked with the LA Dodgers Foundation and the California Community Foundation to raise $1 million for emergency assistance for families financially impacted by immigration enforcement CIFD was responsible for program design, including eligibility criteria, the flow of funds, and the disbursement mechanism, and has worked with FamilySource Centers and other immigrant-focused community organizations to identify families and distribute funds efficientlyandeffectively.

CD13EmergencyFund

Councilmember Hugo Soto-Martinez has identified $350,000 of his discretionary funding to support additional families living within Council District (CD) 13 who have been financially impacted by immigration enforcement. CIFD is coordinating with the district, MoCaFi, and several FamilySource Centers on program design and creating a referral program to serve some of the most vulnerableCD13constituents

CIFD administers Opportunity L.A., one of the countrys largest universal Children's Savings Account programs.Itopensacollegesavingsaccountforeveryenrolledfirst-gradestudentatover500Los Angeles Unified School District public schools and affiliated charter schools, serving between 26,000 and 32,000 students annually. To get parents started, families receive a seed deposit of $50uponregistration. They can add their own savings, ultimately contributing to post-secondary expenses.

Therearecurrently 116,000 studentsintheprogram.Weareinthemidstofaregistrationdrivewith contract partners at the YMCA of Greater Los Angeles and Agency M Media, leveraging in-person interactions, community events, bus benches and shelters, neighborhood poster and flyer placements, and digital out-of-home advertisements. Our registration rate increased from 4.7%to 6.6%betweenJuneandAugust,puttinguswellonourend-of-year10%registrationgoal.

The program is also facing two significant operational challenges Due to ongoing budget constraints,neithertheCitynortheCountyofLA hasidentifiedadditionaldollarsforseeddeposits, resulting in our new approach that offers funds to parents only once they have registered This does not notably change the participant experience and allows us to sustain the program for multiple years while we seek new philanthropic and restored municipal funding. Furthermore, Citibank, our current banking partner, is exiting the Children's Savings Account space in 2026. Therefore,CIFDisinconversationwithseveralotherfinancialinstitutionsinanticipationofreleasing aRequestforProposallaterthisyear.

Seebelowexamplesofourprogramoutreachmaterials.

Free Tax Prep Los Angeles

CIFD oversees the Free Tax Prep (FTPLA) coalition with County and FTPLAisapublicawarenesscampa to educate working Angeleno available federal and state tax provides free tax preparation ser earningunder$67,000annually.All FamilySource Center (FSC) locat Volunteer Income Tax Assistance whichtheCIFDteamhelpstocoord

The 2025 tax season was extended due to the January wildfires As o FTPLA Coalition has assisted over 15,000 households in filing their taxes, resulting in over $15.4Minreturns,includingtaxcredits.

CIFD also participated in a kickoff press conference, facilitated nine pop-up events in partnershipwithelectedofficesthatreachedover 200 clients and resulted in returns of $240,000, and placed five student interns with FSCs to expandtheircapacity.

Ensure that all FamilySource Centers are preparedtodeliverVITAservicesviatrained stafforsubcontractors

Plan a new series of community pop-up eventswithelectedofficesinVITAdeserts Expand the intern placement program basedonavailableMayor’sOfficefunding Advocate for policies that meet the needs ofITINholderswhoareafraidtofile

Darchelle Strickland Love, Local Government Manager - City of Detroit.

Previously, it was reported that two additional staff members were assigned to Detroit’s FEC and Bank On programs. We are working together to bring more visibility to both programs and are off to a good start.

1. We have begun the process of informing Detroit City Council Members about Bank On and FEC and how it connects to the councilmember’s existing committee, the Generational Wealth Taskforce.

2. During Estate Planning Month, a press release will be published to highlight the city’s existing Free Will and Estate Planning Program and how Bank On and FEC can complement family efforts to become financially solvent and establish a foundation for future generations.

3. Planning to refresh content on the city’s webpage for both programs is underway. The goal is to launch program updates and how Detroiters can connect to Bank On and the FEC using testimonials and social media posts.

4. We are considering ways to use FECBOT data to communicate the impact the FEC has on Detroiters who take advantage of the program. Opportunities exist to tell the story of someone who has successfully gone through the financial counseling process, reduced debt and accumulated savings. This info can also be adopted for social media posts.

5. We are also working with community non-profit organizations to develop a process to refer their clients to the FEC. These non-profits currently offer first time homebuyer workshops. The FEC could be helpful to those who want to own a home, but they are not financially ready to manage the responsibility of owning a home. More discussion is required to determine if this is a viable option to pursue.

Cities for Financial Empowerment Coalition

Update from the City of Boston, Fall 2025

Previously known as the Mayor’s Office of Financial Empowerment, the Center for Working Families (CWF) has completed more than three years as part of the Worker Empowerment Cabinet, which aims to advance the well-being of all Boston workers in the public and private sectors.

CWF’s mission continues to be to identify and implement programs and strategies that connect Boston residents with skills and resources to improve their economic wellbeing and financial empowerment. This includes providing access to financial empowerment through workforce development, so employment and related services are a key component of the assistance we offer.

Our current initiatives include:

o Boston Saves – Boston Saves, our Children’s Savings Account program, enrolls a new K2 class citywide every year, as well as adding students who have moved into the Boston Public Schools in grades 1 through 6 (about 3500/year). Our mission is to empower families to save and plan for their children’s future with the support of their city, schools, and community, and our vision is a citywide culture that supports the educational and career aspirations of Boston’s children and their families.

o 81 participating elementary schools, K2-Fourth Grade

o 21,500+ active accounts (this will increase in November when we add another group of Kindergartners)

o 33% of households have logged in at least once

o $50 seed funding held by the City of Boston until graduation

o Opportunities for families to earn $65 incentives in the first year to their COB account through saving in their own linked account, reading aloud, tax preparation, etc.

7 Palmer Street, Boston, MA 02119 (617) 918-5239 Boston.gov/Working-Families

o $1,449,800 allocated in seed and $466,605 in incentive funds as of June 30, 2025

o Most recently, a special promotion with families living in public housing allocated $500 each to the accounts of 485 Boston children.

o Evaluation being conducted by Dr. Willie Elliott, Summit Lab. Part 2 should be completed by end of year.

Boston Tax Help Coalition

The Boston Tax Help Coalition (BTHC), the CWF’s largest and best-known program, will be in its 25th year of serving Boston and surrounding areas. Its mission is to provide free tax preparation to LMI residents, ensuring that the fee they would have paid to commercial preparers goes back into their pocket/into the community, preventing them from being victimized by predatory organizations that would overcharge and possibly also provide substandard work, and to maximize access to the Earned Income Tax Credit. The goal is also to serve low-to-moderate income residents, limited-English proficiency residents, and disabled residents. Most households making $70,000/year or less are eligible. For the past two years, we served 12,000+ households in Greater Boston. The average annual income of our taxpayers is $30,000; 85% are people of color and 20% have limited English proficiency.

Both funding and support from the IRS were a challenge in 2025. The IRS cut our funding by 60% without explanation and several of our key contacts at IRS Spec have lost their jobs. There were a lot of rumors about immigrant families being afraid to file; however, our numbers are the same vs. last year. We operated 30 sites (including one at our main office in Roxbury), plus eight weekend sessions specifically for the disabled.

o The Financial Check-Up (FCU) continues to be a key asset building tool for CWF both during the tax season. The FCU is part of Mayor Wu's city-wide empowerment strategy to help LMI Boston residents receive financial coaching to build their credit and savings. During the 2024 tax season, we completed 1200 FCUs but interest in 2025 was less, which we attribute both to easier access to credit scores via Credit Karma, etc. and more tax sites doing drop off service (people just want to get in and out).

o The FCU is a cost-efficient, light-touch strategy, and financial tool. It is a one-time, approximately 20-minute session, intended to provide education, knowledge, and behavioral change about easy to implement activities that may improve an individual’s credit score and financial well-being. The FCU provides services in six core areas: credit review, credit advising, service referrals, voter registration (if applicable), financial products, and offers options for spending/saving the tax return.

7 Palmer Street, Boston, MA 02119 (617) 918-5239 Boston.gov/Working-Families

o Bank On Boston – Bank On Boston is part of a nationwide movement of Bank On programs led by the CFE Fund, which has supported our work over the last several years. Bank On Boston, like many of its peer programs around the country, works to raise public awareness, expand access to financial education, and help connect residents to other asset building initiatives, not merely our own programs but also this year we are focusing on summer youth partnerships. When we began Bank On Boston, the only account in Boston that met the Bank On National Standards was Bank of America and, distressingly, clients we sent there to open accounts received puzzled looks from staff unfamiliar with the concept or designated account. Since then, Chase established a banking presence in Boston with its Secure Banking account. In addition, the efforts of our Bank On Boston team has resulted in accounts being established at Berkshire Bank, Citizens Bank, Dedham Savings, Lending Club, The Cooperative Bank, Metro Credit Union, Reading Cooperative, and Wakefield Cooperative Banks. Capital One, Santander, Lending Club, and Webster also provide certified accounts now.

o We were finally able to hire a new Bank On Boston Manager, Norah Boyle. She has experience at Fidelity and Bank of America, and hit the ground running working on a ROTH IRA project to encourage 18 year olds to understand the importance of retirement. Northeastern University and J-PAL are partners on this project.

o Bank On Boston and Summer Jobs Connect

The City’s Youth Employment and Opportunity (YEO) Department manages and develops Boston’s future workforce and is part of our Worker Empowerment cabinet. We worked closely with them leading up to and during summer 2024 and 2025, with great support from the CFE Fund. Approximately 9,000 students received some type of paid summer job through the City both years, and we connected with nearly every summer employer to promote direct deposit and safe bank accounts. We estimate that 34% of our summer youth do not have a bank account, especially those who are 14 and 15.

Four local financial institutions offered non-custodial no-fee accounts for youth under 18 during Summer 2025. There were still challenges to overcome in account opening – primarily the lack of identification by many students although Metro Credit Union was willing to accept nearly anything reasonable, but we were extremely busy. We did not have metrics for summer available at press time but our work included opening accounts, providing workshops, and supporting the Summer Jobs program at events.

o Rachel Rodri, our indomitable grants manager, was inspired by Chicago and New York to create a new program we launched in April, Young Money Mentors. This was a stipended program for high school juniors and seniors in which they learned personal finance topics during the spring, chose a topic in which to become expert, and presented to students in our Learn & Earn community college program. Students also shadowed some of our banking

7 Palmer Street, Boston, MA 02119 (617) 918-5239 Boston.gov/Working-Families

partners, visited colleges, learned about financial aid, and became regulars in our office. One even serenaded us on his cello on their last day!

o Boston Builds Credit – This innovative citywide credit building initiative was created by our office and United Way to help Boston residents attain a prime credit score through financial education and coaching. Targeting LMI residents, small business owners, immigrants, youth, and large employers, we are using a place-based strategy to reach neighborhoods identified as high need and collaborate with community-based organizations to expand our reach. This program moved to a new partner in early 2025, Working Credit, although CWF continues to partner in this work.

Financial Empowerment

o Our office, in the heart of Boston’s Roxbury neighborhood, led by Alan Gentle, includes four financial coaches, and one outreach coordinator – and provides coaching in English, Spanish or Haitian Creole. We provide one-onone long-term financial and employment coaching to about 400-600 clients annually. The office also serves as one of the City’s busiest VITA tax sites so much crossover promotion takes place. We built some new partnerships over the past year, particularly in our work with Returning Citizens, a challenging but very important target group.

o Bridge to Hospitality Program – Preparing Boston residents for the 21stcentury workplace is a priority for Mayor Wu and the Center for Working Families. In the past, we have offered Culinary, Digital Literacy, and Green Jobs training programs. Our current collaboration is a Commercial Driver’s License “Bridge” and training program for ESOL individuals to augment the Office of Workforce Development’s traditional CDL training.

o Homebuyer Readiness – Several years ago, the City of Boston’s Home Ownership division asked us to work with them by offering workshops to help residents interested in home ownership but who did not know where to start – and were intimidated by or simply not ready for the City’s Home Ownership 101, which is required for home financing programs. We created a workshop curriculum that incorporates both credit building and home ownership strategies. Those interested are recruited to become financial coaching clients which helps them focus on the savings strategies needed to amass a down payment and the credit score needed to get a good mortgage rate.

o Summer Learn & Earn

The Summer Learn & Earn (SLE) program was created during the pandemic as a virtual, stipended opportunity for rising high school juniors and seniors to earn academic credit at local community and four-year colleges. Courses included Marketing, Communications, Web Design, and Criminal Justice. We

7 Palmer Street, Boston, MA 02119 (617) 918-5239 Boston.gov/Working-Families

moved to in-person classes on Tuesdays and Thursdays and “academic readiness” with OWD staff on Wednesdays. Students earn $250/week if they attended all sessions and our Bank On Boston staff worked with as many participants as possible to get them banked. This program is funded by the summer jobs division of Worker Empowerment so in 2025 SLE and its staff moved under Youth Engagement and Opportunity, which is still part of our Cabinet.

I am sorry to miss seeing everyone in Louisville!

7 Palmer Street, Boston, MA 02119 (617) 918-5239 Boston.gov/Working-Families

ConstanceMartin

www.cityoftulsa.org/ofe

BacKground

The City of Tulsa has embedded financial empowerment programs and policies into City services to improve individual and family financial resilience and stability. Financial empowerment is part of several strategic initiatives that the City of Tulsa has implemented to fulfill its mission to build a foundation for economic prosperity, improved health, and enhanced quality of life for all Tulsans

Tulsa launched its Financial Empowerment Center (FEC) planning process in February of 2020, just a few weeks before the pandemic shut down Tulsa and much of the world. Despite this challenge, the city continued to convene a large cross sector group of stakeholders to submit an implementation proposal that year to launch the Tulsa FEC before the end of 2020. The FEC operates within the Office of Financial Empowerment and Community Wealth (OFE), which was officially launched in January 2023. The Office now falls under the Department of Resilience and Equity.

In Tulsa, financial empowerment initiatives are an integral part of the department that oversees the city’s resilience strategy, Resilient Tulsa and New Tulsans Welcoming Plan, which include goals and actions to improve financial health and reduce economic disparities. Financial empowerment and resilience were embedded in the city’s COVID-19 response and relief efforts including grants that were distributed to over 60 local nonprofits as well as through emergency rental assistance integration.

The Tulsa OFE has successfully leveraged both public and private funding to support its operations, including Community Development Block Grant, Coronavirus Aid, Relief, and Economic Security Act, American Rescue Plan Act (ARPA), private foundation grants, and grantsfrom financial institutions.

office of financial empowerment and community wealth

The Office of Financial Empowerment and Community Wealth is the City of Tulsa’s centralized approach to provide programs and resources for Tulsans to achieve financial stability and resiliency. Through partnership development, strategic coordination, policy and advocacy, and long-term financial empowerment strategies, the OFE will optimize public and private funding streams while leveraging new financial investments to support its initiatives.

$330,000 arpa funding for fec operations

Institutionalizing the Work:

$95,000 funding from private local foundations

$150,000 additional funds for fiscal year 2026-27