The Analyst Summer 2025 | GLOBAL MARKETS IN FOCUS: OPPORTUNITES & RISK

Recent world events have placed us in a constant and chaotic news cycle, making it easy to feel overwhelmed by everything happening. Finding the balance between doomscrolling and staying educated on current affairs can be challenging. The theme of this summer’s issue of The Analyst, Global Markets in Focus: Opportunities and Risks, is well-timed as we highlight and glean insights from those making local and global change within the financial industry.

Our feature articles aim to tackle pressing global issues and provide thoughtful insights on how these issues impact investment professionals as we consider the vital role that geopolitics plays in investment risks and gain insight from practitioners on their strategies for managing geopolitical risk. We explore the risks and rewards of investing in emerging markets, foreign currency fluctuations, and hedging international currency.

Our review of Tim Marshall’s thought-provoking book, The Future of Geography: How Power and Politics in Space Will Change Our World, launches us beyond global issues and into the powers and politics surrounding space exploration and its impact on Earth citizens.

This issue’s charterholder profile, Stephanie Poon, CFA, reflects on her progressive career in Canadian financial institutions, diverse academic path in finance and law, commitment to volunteerism, and recent foray into entrepreneurship to expand her family’s business.

For others looking to focus their energy toward making an impact within the financial industry while diversifying their skillsets and expanding their professional networks, the mentorship committee offers a discussion on the benefits of professional volunteering and mentorship to explore alternative career directions and enhance skills.

Finally, we feature coverage from season 1, episode 3 of CFA Society Toronto’s exciting video podcast series, Diverse Dividends, with Wes Hall, activist, founder, and CEO of Kingsdale Advisors and Dragon on CBC’s Dragon’s Den.

In times of global uncertainty, knowledge, education, and insight are solid investments. We certainly hope that this issue delivers.

Board chair message | Brian Madden, CFA

Global Influence, Local Impact

As we explore global markets in this issue of The Analyst, I’m reminded of the unique position we hold here in Toronto, a city at the heart of global finance where professionals blend international perspectives with local insight.

CFA Society Toronto reflects this dynamic. With nearly 12,000 members, we are the largest CFA Society in the world. But beyond size, what truly sets us apart is how we translate global reach into local value.

We are not only a large society, but also a recognized leader. Our Outstanding Society of the Year Award from CFA Institute celebrates our local leadership and global impact. Our work engages regulators, like the Ontario Securities Commission (OSC) and Canadian Investment Regulatory Organization (CIRO), shapes global thought leadership through roundtables and partnerships, and supports critical initiatives like advancing gender equity and improving corporate disclosure standards.

Most importantly, this influence creates meaningful benefits for you, our members. Through our Learning Partner Portal, we offer cutting-edge education on topics like artificial intelligence (AI), data analytics, alternative investments, sustainability, and much more to come to help you stay competitive. Our sold-out conferences demonstrate how we deliver insights that meet you where you are in your career.

But finance is ultimately about people. Across our mentorship programs, volunteer initiatives, and events, our members come together to share knowledge, build meaningful connections, and shape the future of the profession. Together, we are creating a vibrant and inclusive community where members learn, collaborate, and lead.

As membership renewal season approaches, I encourage you to renew your CFA Society Toronto membership at https://www.cfatoronto.ca/membership/renew. By renewing, you secure continued access to the connections, knowledge, and opportunities that drive your career forward.

Thank you for your commitment to CFA Society Toronto and for being part of our vibrant member community. Together, we will continue advancing a globally influential, locally impactful profession, centred on helping members and the industry thrive.

Warm regards,

Brian Madden, CFA, CFP CIO, First Avenue Investment Counsel Inc. Chair, Board of Directors

CFA Society Toronto

TheAnalyst is published quarterly by CFA Society Toronto

120 Adelaide Street West, Suite 2205

Toronto, Ontario M5H 1T1

Telephone: 416.366.5755

Website: www.cfatoronto.ca

General questions: info@cfatoronto.ca

Management Office

Chief Executive Officer Fred Pinto, CFA

Director, Member Events & Experiences Jenny Yeo

Director, Operations Valerie Weddell

Director, Marketing & Communications Kenny Chan

Senior Manager, Education & Events Meredith Lowry IT Manager Alexandra Pegg

Chair, Strategic Content Committee, Walter de Wet, CFA

Chair, The Analyst, Editorial Committee, Joanna Wolff, CFA

Senior Advisor, Member Communications Rossa O’Reilly, CFA

Editorial committee members

Jack Bruton, CFA

Winfred Lam, CFA

Mark Timm, CFA

Jindou Zhang, CFA Kevin Zhao, CFA

Writers Erin Greenfield, CFA

Angha Gupta, CFA

Editor

Sara Maginn Pacella

Art director

Janet Sangalang

Advertisers’ Index

Global X 25 & 30

From the desk of the CEO | Fred Pinto, CFA, ICD.D

Your Voice, Our Commitment

As global markets remain volatile, CFA Society Toronto continues to focus on ensuring you are not only prepared to navigate change, but positioned to lead it.

O ur 2025 Member Engagement Survey offered invaluable insights, and I want to thank the many of you who took the time to share your perspectives. We were especially encouraged to see an almost 60 percent increase in members who are very satisfied compared to the previous survey.

But you also gave us a clear mandate for what comes next. You told us you need more support in critical skills like data analytics, artificial intelligence, and executive communication, with learning that reflects your specific career stage. We are responding by enhancing our programming and educational offerings to focus on these topics and tailor their context to where you are in your career.

You told us you value meaningful and accessible networking and mentorship opportunities. We are expanding our volunteer program to create more opportunities for you to engage with other members, enhancing networking opportunities at our events, and enhancing our mentorship program to benefit even more members.

You told us you want a more seamless experience accessing resources, events, and benefits. We are investing in improvements to our digital platforms to help you quickly find what you need when you need it.

Opinions expressed in The Analyst do not necessarily represent those of the authors’ firms of employment or of CFA Society Toronto and do not constitute a solicitation for the purchase or sale of any financial instruments. Information herein is obtained from various sources and is not guaranteed for accuracy or completeness. The authors’ firms and CFA Society Toronto therefore disclaim any liability arising from the use of information in this publication. The information provided herein is intended only as general information that may or may not reflect the most current developments. The mention of particular companies or individuals does not represent an endorsement by CFA Society Toronto. Although professionals may prepare these materials or be quoted in them, this information should not be used as a substitute for professional services. If legal or other professional advice is required, the services of a professional should be sought. CFA Society Toronto would

Most importantly, you told us that CFA Society Toronto is more than just a professional association. It is a community built on connection, growth, and leadership. We are proud to be seen not just as a network, but as a trusted partner in your professional journey, and we are committed to continuing to support your growth and development at every stage of your career.

These insights and directions will support our Strategic North Star in enhancing and expanding our diverse community and promoting an ethical, dynamic, and vibrant investment and financial services industry. They will guide how we serve you as we advance our three strategic pillars of Member Experience, Influence and Impact, and Operational Excellence.

Thank you for your continued engagement and support. Your insights, energy, and leadership keep our Society thriving and our industry moving forward.

Sincerely,

Fred Pinto, CFA, ICD.D CEO, CFA Society Toronto

Geopolitics: Why It Matters and What to Expect

By Mark Timm, CFA

In fact, geopolitics has been around since ancient Greece, when Aristotle criticized Plato’s concept of a republic because it didn’t account for the impact of the actions of neighbouring states on a society’s welfare. It has waxed and waned as an investment risk ever since.

The Treaty of Westphalia that ended Europe’s Thirty Years’ War in 1648 gave us the modern nation-state. (Previously, European politics had been driven by religion and royal families.) These new states were discrete entities that experienced geopolitical conflicts over access to resources.

After the terrible world wars of the first half of the twentieth century, economic integration was seen as a way to tilt individual countries’ war/peace cost-benefit analysis toward peace. Europe stands out in this effort, but global efforts began with the General Agreement on Tariffs and Trade in 1947 (the predecessor of the World Trade Organization) and the creation of the International Monetary Fund (IMF) and the World Bank.

Suddenly, geopolitics has become a key investment risk as the US government under President Donald Trump proclaims its intent to remake the world order with sweeping tariffs, upended alliance assumptions, and outright territorial ambitions. Source: BCA Research

Global integration accelerated after the collapse of the Soviet Union in 1989–90 on the assumption that improved global flows of goods, services, and capital best served the well-being of individual countries. Geopolitics was a slow-moving overarching theme that investors needed to be aware of but not spend much time on.

So globalized had the world become that, by 2015, then brand-new Prime Minister Justin Trudeau described Canada as the world’s first “post-national state.” 1

Globalization ebb tide

The tide was already turning, as highlighted by the first election the very next year of Donald Trump as President of the United States. Today, the early actions of Trump’s second administration challenge comforting assumptions about a quiescent geopolitical landscape.

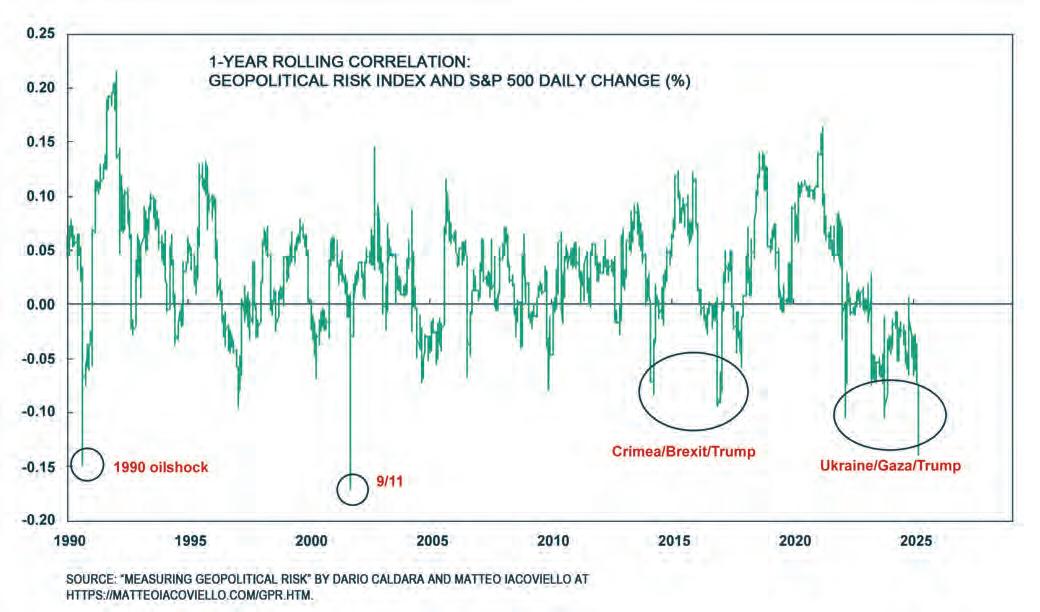

Geopolitical risk—like any risk—measures the probability that outcomes will differ from expectations. One of the most widely

FIGURE 1. CORRELATION BETWEEN GPR AND S&P 500

Geopolitical risk does look set to remain elevated.

used benchmarks is the Geopolitical Risk Index (GPR) devised by Dario Caldara and Matteo Iacoviello.2 It’s a simple measure of the frequency of news media coverage on geopolitical tension.

Figure 1 shows the correlation between the GPR and returns on the S&P 500 Index since 1990. It shows extreme negative correlations (a high GPR accompanied by sharp drops in the S&P 500) during events like the 9/11 terrorist attack, Brexit, and Russia’s invasion of Ukraine. It also shows that negative correlation continuing, with President Trump’s trade war and ongoing great power competition, according to Matt Gertken, Chief Geopolitical Strategist at BCA Research.

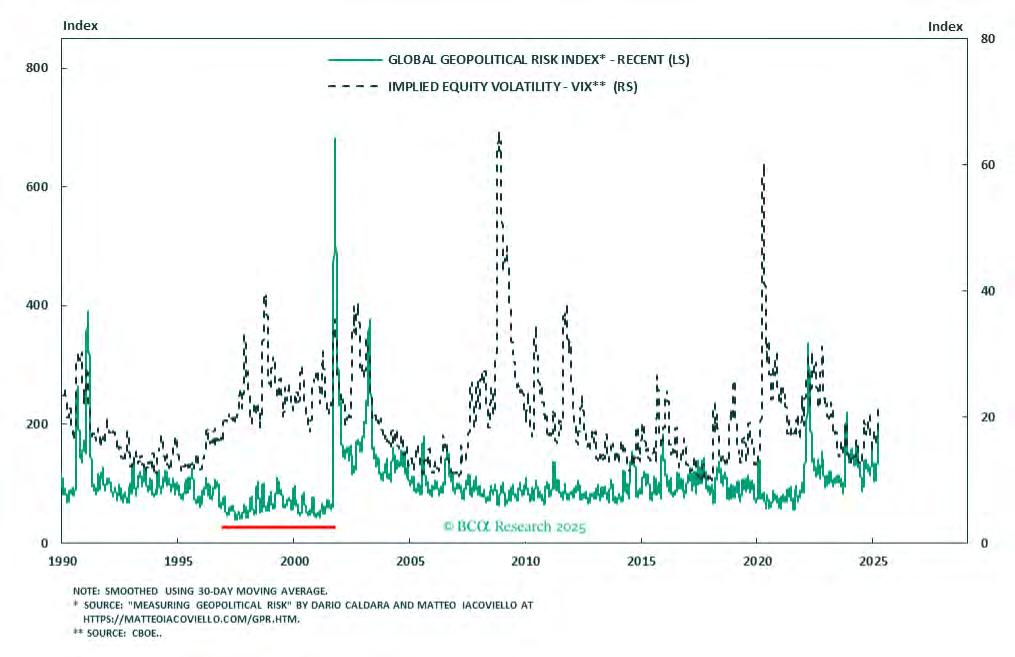

Figure 2 reinforces that the correlation isn’t spurious: although equity market volatility as measured by the Chicago Board Options Exchange (CBOE) Volatility Index (VIX) isn’t always accompanied by a rise in the GPR, since 1990, a spike in the GPR has consistently been accompanied by higher market volatility.

Geopolitical investment risk transmits most directly via currency markets and, relatedly, interest rates. In equities, the key variable is simply the perceived overall risk level, says the former Chief Investment Officer at Alberta Investment Management Corporation (AIMCo), Marlene Puffer, CFA, PhD.

“Markets don’t like uncertainty,” she explains. “When you inject a wider set of outcomes, whether it’s economic growth or profitability of companies, that uncertainty translates into market downturns in the near term.”

Risk premium impacts

Foundational to equity valuation is the equity risk premium and the risk-free rate, historically based on the US 10-year Treasury. Leaving aside speculation about the long-term reliability of US institutions, questions about the near-term impact of US government policies on inflation and monetary policy are putting upward pressure on US Treasuries and the risk-free rate, Puffer notes.

FIGURE 2. GPR (LEFT SCALE) VS. VIX (RIGHT SCALE)

Source: BCA Research Geopolitical Strategy. Data as of March 31, 2025.

Practitioner Strategies for Managing Geopolitical Risk

To succeed in managing geopolitical risk, investors need both quantitative and qualitative approaches, says Matt Gertken.

Markets face geopolitical risk when nonmarket actors (e.g., governments, protest movements, insurgencies) act in ways that influence markets. Gertken advises investors to identify the key non-market actor and that actor’s specific policy priority that affects the investment decision.

To assess the risk, estimate the likelihood that the policy will be implemented, as well as the actor’s own evaluation of the benefits of success and costs of failure.

Research,

scenario planning, and robust debate are irreplaceable

“It’s important to tie a geopolitical risk assessment to an actionable investment conclusion so that you can ask afterwards: ‘Did that assessment improve performance?’” Gertken says.

➜ Do your homework

Marlene Puffer emphasizes that thorough research, scenario planning, and robust debate are irreplaceable.

“Get input from a variety of sources so that you’re not blindsided by some outcome,” she says. “Attach probabilities to outcomes and model your tolerances for the worst tail risks. Add resilience to your portfolio to mitigate the downside risk without sacrificing return.”

Puffer notes that investment managers, especially those evaluating private market deals, need a culture that integrates geopolitical considerations.

“You need the right internal structure and challenge mechanism so that the macro view and the voice of the risk team are taken into account,” she says.

“For people inside the deal, there can be a tendency to downplay those risks. It’s important to come back up and out of the deal and ask whether you can justify the risk premium,” Puffer concludes.

➜ Unique private wealth considerations

For high-net-worth individuals or family offices, geopolitical risk management presents unique challenges, says Brian Madden, CFA, CFP, Chief Investment Officer at First Avenue Investment Counsel Inc. and Board Chair of CFA Society Toronto.

“Every client thinks about risk in their own unique way,” says Madden. “Before we invest a single dollar, it’s crucial that we understand both their risk appetite and risk tolerance— and those aren’t always the same thing.”

Unlike institutional investors, private clients may lack a formal geopolitical view, placing more responsibility on wealth managers to account for such risks.

“ We have to assess their total risk budget and be really clear about the nature of all risk—including geopolitical—that our approach may encounter.”

Behavioural nuances also loom larger in wealth management. Some geopolitical risks may provoke a particular emotional, patriotic, or cultural response for clients. Madden says that managing those reactions is all part of the client relationship, but there’s a duty not to let them override the cold calculus of investment decision-making.

“If a client doesn’t have staying power for a given position, it means we’ve done something wrong at the outset,” he says. “We’ve misjudged something about their risk preferences, tolerance, or appetite.”

“Sometimes, it’s easier to just avoid the really hot potatoes,” Madden concludes.

It’s not so much the level of risk as the uncertainty about the direction that is kryptonite for markets, though. To illustrate, a rise in global tariffs affects the profitability of different industries and investee companies. But if tariffs are just used to extract concessions and then rolled back, those profitability effects may be undone.

“So much of the investment outlook currently is policy-driven; investment decisions are difficult,” says Puffer. “Because the drivers and range of possible outcomes have become broader, we may have entered a thematic zone characterized by under-investment and muted global returns.”

Geopolitical risk does look set to remain elevated. The GPR has never revisited the multi-decade low it hit at the turn of the millennium with the collapse of the Soviet bloc.

A changing landscape

Despite widespread commentary that current White House trade policies are misguided and aimed mainly at financing both new and renewed domestic tax cuts, deeper trends more broadly underlie both the tariffs and heightened geopolitical risk.

First, rapid globalization has prompted populist movements in many countries, fueled by economic, social. and political inequalities, notes BCA Research’s Gertken.

“Now that states have started to enforce borders and impose trade taxes, there’s an entire class of media and society that had a distorted sense of the importance of commerce and finance and that’s now frustrated and bewildered because it didn’t understand that states and borders still matter,” he says.

Second, economic relations have become intertwined with broader national security interests. After the COVID-19 pandemic exposed the risks of globalization by interrupting supply chains, government policy swung back toward securing domestic supplies. At the same time, dominance in key industries and control of strategic materials is seen as offering leverage in increasingly adversarial geopolitical relationships, notably between the US and China.

“Economics is no longer purely about the financially beneficial flows of goods, services, and capital,” says Jonathan Fried, a retired Canadian diplomat and fellow at the Canadian Global Affairs Institute. “Today, economic security and national security are increasingly intertwined in government policy and business planning alike.”

Third, US policy has been increasingly shaped by its relative decline in material power.

“The large US material advantage over other states has declined, and the US has awakened to the need to be competitive rather than cooperative with other nations,” Gertken says. “That and the strategic-technological challenge posed by China really revolutionize the geopolitical context that we live in.”

The question is what new geopolitical order will emerge.

“Even though the current US administration may yet try to restore it, a global order solely dominated by the US seems to be dissipating,” says Fried, also a Senior Advisor at the Washington-based DGAAlbright Stonebridge Group global advisory firm. “The world is more heterogeneous, and we’re on our way to some new configuration, but no one yet knows what shape it will take.”

Mark Timm, CFA, is an independent financial writer with more than three decades of experience in Canada and abroad as a journalist, equity analyst, and Director of Institutional Marketing for a leading Canada-based global asset manager. Mark is a volunteer with CFA Society Toronto’s Digital Content Committee.

1 Foran, Charles. “The Canada experiment: Is this the world's first ‘postnational’ country?” The Guardian, January 4, 2017. https://www.theguardian.com/world/2017/jan/04/the-canadaexperiment-is-this-the-worlds-first-postnational-country

I believe in investing globally because it increases opportunities and permits better diversification. That said, global investing comes with risks, including foreign currency fluctuations.

In the short term, foreign currency fluctuations can materially impact reported investment performance, both positively and negatively. Clients rarely ask about this impact when it is positive. However, it can be concerning for them when the impact is negative, which happens when the Canadian dollar appreciates.

Despite the risk, our firm generally does not hedge the foreign currency exposure arising from our equity investments even though our combined exposure to foreign

currencies such as USD, EUR, GBP, HKD, etc. is more than 75 percent of our equity portfolios at present.

Why does our firm not hedge foreign currency risk arising from our equity positions? Below are four reasons.

1. Hedging reduces diversification

Much of the concept and study of hedging foreign currency risk comes from the US. Despite this, currency hedging is not

Some may ask, “But all my retirement expenses will be in Canadian dollars, so shouldn’t I have all my assets and income based in Canadian dollars?” The simple answer is “No.”

Swiss Franc

Icelandic Krona

Israeli Shekel

US Dollar

Danish Krone

British Pound

Australian Dollar

Swedish Krone

Norwegian Krone

New Zealand Dollar

European Euro

Japanese Yen

Korean Won

Czech Koruna

Polish Zloty

Mexican Peso

Hungarian Forint

South African Rand

Russian Ruble

Turkish Lira

popular among US institutional investors. Cheema-Fox and Greenwood found only 21 percent of USD-based institutional equity investors hedge their foreign currency exposure, and those investors only hedge 35 percent of their exposure. 1

So, currency hedging is not popular in the US, and, in my opinion, it should be even less popular in Canada. Why? Because for investors in countries with smaller economies such as ours, hedging can actually increase risk. When Americans hedge foreign currency, they increase their exposure to the US dollar, the world’s most important currency, often referred to as the world’s “reserve currency.” On the other hand, when Canadians hedge currency, they are increasing their exposure to our Canadian dollar, and therefore to our relatively small, undiversified economy.

Some may ask, “But all my retirement expenses will be in Canadian dollars, so shouldn’t I have all my assets and income based in Canadian dollars?” The simple answer is “No.”

While retirement expenses will be denominated in Canadian dollars, the items purchased and consumed will be priced off international markets. Your coffee might come from Brazil, your pasta might contain European wheat, your fuel might come from American refineries, your clothes might be made from cotton grown in India, your vehicle might contain Japanese steel, the shows you watch might be produced in the US, the plastics around your home might be from China, your bananas might be from Costa Rica, you might take a cruise to Argentina, and your purse might be made from Italian leather. The chances of being able to afford global goods is better if your assets are spread across important global currencies than if you take a gamble putting everything into our loonie. In other words, diversification away from the Canadian dollar should insulate purchasing power.

2. Determining how much to hedge is guesswork

Calculating how much foreign currency to hedge involves considerable guesswork because it is impossible to determine precise exposures. For example, Toyota is based in Japan, but 39 percent of its revenue comes from North America. Their annual report does not split this between the US, Canada, and Mexico. So, how would a Toyota shareholder hedge the underlying currency exposures? Microsoft’s annual report says that when they sell software to giant US multinational companies, they record all the corresponding revenue in their American segment, even though the software is purchased and used by subsidiaries and workers worldwide. So, what proportion of revenue should be attributed to which currency?

To make good hedging decisions, one must also understand where each investee company’s costs, profits, and cash flows are derived, and understand the foreign currency hedging each company is already undertaking themselves, if any. Companies disclose almost none of this, and even if they did, the details are constantly changing.

3. Currency movements tend to cancel out over time

Currency movements should largely cancel out over the medium to long term. This can be illustrated with an example. Imagine you own shares in a Japanese company that makes and sells beverages in Japan. Then, imagine the Yen depreciates.

Much of the company’s input costs, such as sugar, packaging, and fuel, are priced off international markets and will rise in Yen terms. So, the company will raise its prices in Yen to compensate. Over time, the company’s revenues and profits, measured in Yen, will rise. However, when measured in terms of other major currencies, it is probable that the profit will be relatively unchanged. Therefore, the value of your investment, measured in Canadian dollars, will also be roughly unchanged. If you had hedged Yen exposure, it might have helped investment returns in the very short term, but hedging would likely have been largely unnecessary over the medium term.

4. Hedging has costs

Hedging is almost always accomplished through entering forward foreign currency contracts with an investment dealer. The dealer earns a spread between their clients selling protection and their clients buying protection. The more liquid the

currency, the tighter the spread, meaning hedging is cheaper. Besides this spread earned by the dealer, hedging can also involve carrying costs, which are most easily illustrated by considering emerging markets. Emerging markets often have high inflation and therefore high interest rates. The differential between the interest rate in the emerging market and the interest rate in Canada can be quite high. This differential is built into forward currency contract prices and represents a cost of hedging.

If an investor always hedges foreign currency as a policy, the costs are incurred continuously, and they can add up to a significant amount over time. The investor will regularly pay dealers a spread, and they will continuously pay the interest rate differentials buried in forward contract pricing. However, the sizeable unanticipated currency volatility they are trying to protect against might never materialize or might not materialize

for many years. So, just as with buying extra house or car insurance, one must evaluate if hedging is worth it. Since I believe currency fluctuations will likely be a wash over the long term, I feel investors can afford to self-insure by not hedging. Instead, they can reduce risk by diversifying their equity portfolio by country, industry, and market capitalization.

Should we ignore macro?

As a global investor, I feel it is wise to pay attention to international politics, economics, and regulations. I consider these when deciding whether to avoid or expose clients to certain countries and currencies. Despite not hedging, I do pay attention to foreign currencies, which can become overvalued or undervalued, especially in the short to medium term. A metric to help determine this over/ undervaluation is Purchasing Power Parity,

which compares the price of goods in different countries and currencies. When a currency is undervalued, it can be a good time to consider buying or adding to stocks from that market. Conversely, when a currency is overvalued, it may be time to sell, trim, or avoid equities from that market.

Just one approach

The approach to foreign currencies described in this article is not uncommon. Like many long-term equity investors, I feel the best way to deal with risk caused by inflation, politics, tariffs, and currency wars is to own stocks of strong companies.

These include companies that can pass on higher prices and that have essential, non-cyclical products in high demand. Often, these are larger companies with global operations. Such companies can often manage risks by moving production

and supply chains around. They frequently fund their operations in local currencies and use other techniques to manage foreign currency risk internally.

All that said, the philosophy I have outlined is just one approach. For investors who do not have the appetite for foreign currency risk, there are many funds and securities available in Canada that hedge exposure to currencies.

Erin D. Greenfield, CFA, is President of Greenfield Investment Management Limited.

1 Cheema-Fox, Alex, and Robin Greenwood. “How Do Global Portfolio Investors Hedge Currency Risk?” Harvard Business School. Working Paper, October 2024. https://www.hbs.edu/faculty/ Pages/item.aspx?num=66598

largest bank to deliver reliable investment servicing and data to more than 1,000 Canadian asset managers and pension plans so they can focus on what matters most – helping their clients and members achieve their aspirations.

TheFutureofGeography:HowPowerand PoliticsinSpaceWillChangeOurWorld by Tim Marshall

Rossa O’Reilly, CFA

Journalism has long been called the first rough draft of history. Tim Marshall’s book on politics and space suggests that journalism can also sketch the future geography of our world. Marshall is a very successful best-selling writer, and he explains in everyday terms the science of humanity’s exploration of space. Most effectively, he shows how power and politics in space will likely change our world.

Geopolitics—the geography, politics, and international relations on Earth—have shaped our world up to this point, but now astropolitics—the geopolitics of outer space— are beginning to matter. There are contrasting views concerning the political future of space. One view is that space belongs to humankind and is inherently beyond politics; hence, any benefit that comes from space exploration should be shared by all nations. Opposing this optimistic view, realists maintain that, without changes to human nature and an end to the widespread pursuit of nationalism, space cannot be protected from military use.

In the modern era, Marshall argues, there are three main independent spacefaring nations:

• United States of America

• China

• Russia

How they choose to proceed will affect everyone on Earth. Soon, what happens in space will shape human history as geography and international politics have on Earth.

Rocket diplomacy

A decades-old space partnership between the US and Russia is beginning to unravel, ending a relationship that has benefited both science and détente between the two powers. Even before the war in Ukraine, Russia’s Western partners complained about Russian incompetence and behaviour. In 2018, the Russian News Agency TASS

accused, with no evidence, US astronaut Serena Auñón-Chancellor of having a mental breakdown aboard the International Space Station (ISS) and drilling a hole in a docked Soyuz capsule.

In 2021, a Russian space laboratory docked with the ISS, but shortly thereafter, its thrusters began firing and caused the ISS to spin uncontrollably until they ran out of fuel. As the Ukraine war intensified, Dmitry Rogozin, head of the Russian space agency, Roscosmos, called US astronaut Scott Kelly a “moron” and threatened to leave Americans stranded on the ISS.

With increasing sanctions hitting the Russian economy and its growing isolation from world science and commerce, Roscosmos finds it difficult to compete. The war in Ukraine has made it more likely that Russia will step away from space exploration and, with China, focus on military applications in space.

Russia is still ahead of China in many facets of space technology, but China has the financial resources, the scientists, and the ambition to succeed in space. Russia and China plan to build an International Lunar Research Station on the surface of the moon and/or in the moon’s orbit by 2035.

Up-and-coming space nations

Russia, China, and the US are now being joined by other aspiring explorers in space.

While the "Big Three" are the main players in space, many others are looking to increase their presence and have established space agencies. Marshall refers to European countries, the UK, Japan, South Korea, India, Australia, and countries in the Middle East and Africa, but notes that none of them look “anywhere near ready to challenge the status of the Big Three space powers.”

Marshall details the potential contributions of these up-and-comers to knowledge and human welfare. But he also outlines ways in which their competition in space could trigger wars that endanger all of humanity. However, we may not have much choice in the matter. As Stephen Hawking said, “I am convinced that humans need to leave Earth. Spreading out may be the only thing that saves us from ourselves.”

The Future of Geography is a very serious and engaging book. Everyone interested in understanding the future role of space would do well to read it.

Marshall, Tim. The Future of Geography: How Power and Politics in Space Will Change Our World. Elliott and Thompson, 2024.

Rossa O’Reilly, CFA, is a Past Chair of CFA Institute, Past President of CFA Society Toronto, and former Managing Director of Institutional Equities at CIBC World Markets Inc.

Emerging, But Not Earning: Why Emerging Markets Require an Active Mindset

By Walter de Wet, CFA

The emerging markets (EM) investment thesis, at least in the late 1990s and early 2000s, was built on the structural growth premium. Due to structural factors such as population growth and urbanization, economies of scale are expected to be available. These trends should drive improving infrastructure and rising productivity. Indeed, in the early 2000s, the BRIC countries—Brazil, Russia, India, and China—were the poster children as significant emerging markets.

In addition to the structural growth premium, EMs often have some exposure to long-term secular themes within a region, such as the demographic dividend in Africa or the growth of e-commerce and technology manufacturing in parts of Asia. These secular themes should provide attractive, long-term growth opportunities for specific companies.

Lastly, in EMs, there is growth in public markets, where informal capital markets become formal and mature, leading to improved corporate governance and access to higher-quality assets at potentially more attractive valuations.

Despite becoming a standard theme, performance has been disappointing

Since the 1990s, EMs have become a standard theme in global investment portfolios, albeit still relatively small. However, the experience over the past decade suggests that a simple passive approach to EM investing doesn’t guarantee higher returns, despite what the structural growth premiums and secular trends would suggest and despite what are often seen as attractive valuations.

The experience over the past decade suggests that a simple passive approach to EM investing doesn’t guarantee higher returns, despite what the structural growth premiums and secular trends would suggest and despite what are often seen as attractive valuations.

The equity returns of EMs as a collective asset class have been disappointing over the past decade. Reasons are plentiful, such as political and policy uncertainty in EMs and slower commodity demand growth, especially from China. However, a dollar-bull market that started in 2012 made investments in local currency EM assets less attractive, especially for dollar-based investors.

To put some numbers on performance, according to Bloomberg, the MSCI EM Index shows that over the past ten years, up until the end of the first quarter of 2025, EMs had an annualized total return of 4.1 percent in US dollars when dividends were reinvested in the index. This compares to the Developed Markets (DM) Index, which returned 10.1 percent over the same period. For EM equities to outperform DM on a more consistent basis, one must go back to the early 2000s before the global financial crisis.

One could argue that DM equity returns are skewed to the upside by the US, but even European equities outperformed, with an annualized total return of 6.3 percent in US dollars. Furthermore, the returns generated in EM were more volatile than those of DM and the European market.

EM is not a homogenous asset class

However, EM is not a homogenous group of countries that provide similar returns, and these markets differ significantly. When considering individual EM economies, it becomes apparent that there is a broad dispersion of returns. Once again, over the past ten years up until the end of the first quarter of 2025, according to Bloomberg, the MSCI Taiwan Index had an annualized total return of 12.5 percent in US dollars, while India returned 8.1 percent, Brazil returned 4.1 percent, China returned 2.7 percent, and Mexico returned 1.5 percent.

There needs to be a selective bias in EM, just as in DM. This is even more the case, given that the volatility, or standard deviation of returns, in the MSCI EM Index has consistently been higher than in DM.

Arguably, after the experience since 2009, only when risk is managed adequately can structural trends still be the source of potential higher returns.

The stylized risks to consider in EM

Investments worldwide tend to face the same types of risks. However, in EM, many risks that carry less weight in DM tend to be highly pronounced and are often more challenging to quantify. These risks are part of why EMs tends to appear cheaper on a price-to-earnings-ratio (P/E) multiple than DMs. For example, over the past ten years, the MSCI EM Index traded at an average P/E ratio of 13.7x compared to the DM Index at 18.5x. The opposite also holds: if risks can be managed, assets can be purchased at lower valuations. These risks that would need more attention can broadly be grouped into five buckets:

1. Political and regulatory uncertainty:

In recent months, Canada has experienced firsthand the negative impact of policy and regulatory uncertainty on investor confidence, trade, and economic growth expectations. In many EMs, this uncertainty is standard. A political clampdown on sectors of the economy or capital controls is a regular theme that can rapidly lead to a repricing of local assets. Political stability, rule of law, and institutional independence can be challenging to quantify but must be constantly assessed.

2. Sovereign and corporate credit quality:

Closely tied to greater policy and regulatory uncertainty, EM sovereign and corporate debt markets offer yields, but often with elevated credit risk. There is often a greater connection between asset performance, fiscal policy, external debt obligations, and political will relative to DM economies. Although less frequent, the risk of restructuring or selective default remains present in several EM sovereigns.

EM risks may be complex, but they can also be mitigated through a wells tructured framework

3. E xposure to global macroeconomic events:

EM assets can be sensitive to changes in global macroeconomic conditions. Their prices often respond in a more pronounced way under global market stress than DM assets. For example, a stronger US dollar, rising global rates, or a downturn in commodity prices are all factors that can generate significant performance divergence.

4. Currency volatility:

The decision to hedge FX risk when investing in EM could have a considerable impact on the dollar return of that asset. As a result, the broad dollar cycle plays an important role. Furthermore, many EMs are small, open economies subject to global capital flows, making FX volatility a key risk driver in EM asset returns. EM FX is subject to local inflation, fiscal policy dynamics, political dynamics, and, ultimately, the resultant portfolio flows. It is also the case that some frontier EM economies often experience dollar (or hard currency) shortages, which force the implementation of capital controls. This means that even if a local asset return was high, an investor may be unable to repatriate assets, should that be required. As a result, when it comes to EM local markets, the challenge is not just directional risk, but also tail events—such as sudden stops, currency devaluations, or capital flight episodes.

5. Liquidity and market structure:

Many EMs tend to have relatively shallow market structures, which implies that trading volumes can vary significantly between days. Alongside currency risks, this can limit allocation size to investments and also limit the ability to exit a market when necessary.

Global growth, mitigating local risks to protect returns

EM risks may be complex, but they can also be mitigated through a well-structured framework. Often, five key considerations can go a long way to address the risks.

1. Local knowledge and research:

Information flow in EMs tends to be less than in DMs and is often asymmetric due to market inefficiencies, policy uncertainty, and political influences. As a result, local context is often a key advantage that enables investors to benefit through bottom-up analysis and on-the-ground research teams, which usually generate significant informational advantages.

2. Regional and country diversification:

EMs are not homogeneous, so excessive diversification can lead to inferior performance, as historical returns suggest. But diversification across regions, such as Southeast Asia or Eastern Europe, can also mitigate region-specific risks. Within areas, further limits on individual country exposure could be implemented. This diversification framework can also address sectoral diversification to mitigate cyclical and structural risks.

When it comes to EM local markets, the challenge is not just directional risk, but also tail events—such as

3. Local vs. hard currency debt allocation:

Slightly away from equities, but when it comes to EM fixedincome markets, an important choice is whether to invest in local or hard currency debt. Local currency debt instruments offer higher yields and potential for currency appreciation but at greater FX risk. Hard-currency debt (e.g., sovereign or corporate USD bonds) is typically less volatile but subject to dollar liquidity in the domestic market and is also more correlated with US rates and global credit markets.

4. G overnance screening:

Screening for governance quality at the government and company levels is critical in equity and credit markets.

Underlying risks must be managed, and investment should be made accordingly

5. Scenario planning:

Although long-term structural themes often exist within EM economies, these themes unfold within a cyclical global economy. Incorporating risk models and stress testing for themes such as US dollar strength or commodity price shocks can support cyclical hedging or rebalancing decisions.

Conclusion

The past ten years have shown that investing in an economic thesis, such as BRICS, is insufficient to guarantee performance. Underlying risks must be managed, and investment should be made accordingly. If risks are managed effectively, then the chance of a greater return could increase rapidly. A simple passive approach is not enough.

small and

Walter de Wet, CFA, is a Senior Research Strategist at Nedbank CIB Global Markets. Walter is the Chair of the Strategic Content Committee at CFA Society Toronto.

Celebrating $20 Billion in ETF AUM

The first Exchange-Traded Fund (ETF) in the world was created in Canada in 1990, transforming the investment industry. ETFs have come a long way since starting as a passive index tracking investment. Today, ETFs cover everything from broad market indexes to different asset classes, industry sectors, geographic regions and highly specialized strategies to give investors greater flexibility to customize their portfolios.

On a mission to innovate

Over the past eight years TD Asset Management Inc. (TDAM) has launched more than 50 ETF investment options and grown its ETF assets under management (AUM) from under $300 million to over $20 billion1 - a significant milestone as TDAM continues to build a strong foundation of strategies and solutions to offer investors flexibility, while seeking to advance its mission to offer innovative investment solutions.

“Our talented investment teams at TDAM continue to push the envelope through their expertise and collaboration, offering investors greater flexibility to meet their financial goals. The popularity of our TD ETF solutions is evident in the rapid growth of our ETF assets under management in an increasingly competitive market,” said Bruce Cooper, Chief Executive Officer, TDAM and TD Epoch, Executive Vice President, TD Bank Group.

“We are pleased to reach a new milestone of $20 billion in ETF AUM and are deeply grateful to our investors who have chosen us as their ETF provider, and whose needs drive our commitment to continued innovation.”

Breadth of expertise

TDAM is known for its broad solution suite featuring its expertise in fixed income, fundamental equity and pioneering low volatility strategies in Canada, among other capabilities. Our deep and experienced Asset Allocation, Public Equities, Fixed Income, Alternative Investments and Commodities teams draw on the strength of many investment professionals to build disciplined portfolios that aim to meet our investors' needs.

We also place risk management at the core of everything we do. TDAM has a large and dedicated risk management team with a disciplined and objective research process which focuses on thorough analysis of company and industry fundamentals.

Why invest with TDAM

We Create

Our solutions are often first-to-market and may even appear unconventional because we believe it takes real creativity and invention to help solve your most important challenges.

We Innovate

TDAM is committed to applying the new thinking necessary to help address investors most important challenges. We take a collaborative team-based approach, focus on quality and employ a comprehensive risk management discipline.

We Perform

By many measures – from the performance of our strategies to the size of our business and the loyalty of our clients – we are an exceptionally strong, disciplined and successful asset manager.

We Listen

To you, and to one another. Conversation with our clients and collaboration among our investment professionals provides the spark for our very best thinking.

Additional information about our complete suite of TD ETFs including the prospectus and ETF Facts can be found at www.TDAssetManagement.com.

DISCLAIMERS

*As of January 31, 2025

1Source: TD Asset Management Inc. as at January 17, 2025.

2Source: TD Asset Management Inc. as at March 7, 2025.

Commissions, management fees and expenses all may be associated with mutual fund and/or exchange- traded fund (”ETF”) investments (collectively, “the Funds”). Trailing commissions may be associated with mutual fund investments. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns. Please read the fund facts or ETF facts and the prospectus, which contain detailed investment information, before investing in the Funds. The Funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated.

TD Mutual Funds, TD ETFs and the TD Managed Assets Program portfolios are managed by TD Asset Management Inc., a wholly-owned subsidiary of The Toronto-Dominion Bank, and are available through authorized dealers.

® The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

About TD Asset Management Inc.

TD Asset Management Inc. (”TDAM”), a member of TD Bank Group, is a North American investment management firm. TDAM offers investment solutions to corporations, pension funds, endowments, foundations and individual investors. Additionally, TDAM manages assets on behalf of almost 2 million retail investors and offers a broadly diversified suite of investment solutions including mutual funds, professionally managed portfolios and corporate class funds. Asset management businesses at TD manage $487 billion in assets. Aggregate statistics under management as of December 31, 2024 for TDAM and Epoch Investment Partners, Inc. TDAM operates in Canada and Epoch Investment Partners, Inc. operates in the United States. Both entities are affiliates and are wholly-owned subsidiaries of The Toronto-Dominion Bank.

CFA Charterholder Profile – Stephanie Poon

Where Finance Meets Vision: One Leader’s Role in Bridging Capital Markets, Entrepreneurship, and Community

By Angha Gupta, CFA

Throughout her career, Stephanie Poon, CFA, GPLLM, MBA, has held progressive roles in prominent financial institutions. Her experience includes working at RBC Capital Markets as a VP for ten years, where she managed the credit analysis, onboarding of trading facilities, portfolio management for hedge funds and regulated funds, and conducted due diligence meetings with global alternative asset managers.

transactions. Given this, I enrolled in the Global Professional Master of Laws (GPLLM) program at the University of Toronto. It was not an easy task to work and study simultaneously. However, my drive and time management skills helped me achieve both, and I was profiled on the cover page of the university’s Faculty of Laws’ program brochure.

You’ve worked across global financial hubs and different areas of finance and investing during your various roles. Did each role add a layer of skill or perspective to your toolkit?

Before that, Stephanie spent three years with Scotiabank, working closely with the prime brokerage group on hedge fund onboarding transactions, and four years in corporate banking with HSBC. Currently, she leads an expansion initiative for her family’s business, growing it into a longterm success story. She intends to return to the financial industry to focus on her career upon the completion of the expansion project. In the meantime, Stephanie is serving as the Chair of the Next Gen Program with CFA Society Toronto.

What motivated you to pursue a diverse academic path (e.g., GPLLM, MBA)? How did each degree or credential contribute to your professional perspective beyond technical knowledge?

From an early age, my parents taught me the importance of continual learning and acquiring new skills. Each academic path

I pursued provided me with additional skills a nd diverse perspectives. I strongly desired to pursue a career in finance and capital markets. To achieve this goal, I majored in accounting at the University of British Columbia to build my foundation in financial statement analysis, followed by an MBA at Simon Fraser University, where I majored in finance and graduated with the Dean of Graduate Studies Convocation Medal for academic excellence.

After completing my MBA studies, I immediately enrolled in the CFA Program, reflecting my strong commitment to the finance industry. I was also fortunate to receive a scholarship for Level I of the CFA Program, and I completed all three exam levels on my first attempt.

While working on structured transactions, I saw the importance of acquiring critical analysis skills and legal knowledge to help me better understand these complex

Each role gave me valuable complementary experience and transferable skills to expand to the next level. At RBC Capital Markets, I developed expertise in alternative asset manager due diligence. I managed the credit onboarding of trading facilities and portfolio management for asset managers and hedge fund clients. I also helped build out the Portfolio Management and Analytics team during the COVID-19 pandemic as one of the founding members. This experience built and expanded my people management, strategic thinking, and team-building skills, which are highly relevant in capital markets.

My role with Scotiabank’s Global Banking and Markets provided me with good exposure to the asset management industry. I partnered with prime brokerage and trading desks and managed the credit onboarding for new hedge funds, pension funds, and broker-dealers.

At HSBC Corporate Banking, I built expertise in syndicated loans, structuring and executing

acquisition financings, and loan facilities in diversified industries. I also gained relationship management skills, working with multinational corporations on their financing, trading, and treasury needs.

Has developing broad skills and knowledge (such as soft skills, legal understanding, risk management, mentorship, and leadership) helped you open unexpected doors?

Certainly! Developing a diverse skill set (technical and soft skills) has been pivotal in unlocking unexpected opportunities in the industry. My ability to integrate credit analysis with in-depth alternative fund due diligence allowed me to take on leadership roles, including at RBC Capital Markets, where I led a team of six members. My legal skills from the Global Professional LLM degree provided a strong foundation to analyze complex hedge fund structures and cross-border transactions. My strong mentorship and leadership skills enabled me to develop high-performing teams and drive efficiencies. Additionally, my volunteer engagements, including serving as one of the committee chairs at CFA Society Toronto and speaking at key events, have expanded my professional network, strengthening my career trajectory.

What would you say are the key skills you cultivated? Are soft skills and leadership capabilities just as critical as technical know-how? How can emerging professionals develop these skills in their roles?

While technical skills are critical, soft skills make employees well-rounded and valuable to employers. People with soft skills a re often seen as having unique and broad backgrounds that can help employers run their companies more effectively and efficiently. Soft skills are acquired over time, so it is crucial to start developing them early in your career.

I encourage emerging professionals to take the initiative to participate in team projects and coach junior team members or intern students, which can provide great opportunities to acquire some soft skills early on.

I also emphasize the importance of professional relationship-building, both inside and outside of where you are working, and developing a strong two-way network where you give and receive.

In addition, CFA Society Toronto and other professional organizations offer a variety of industry events, workshops, and networking functions that can help improve technical and soft skills. I have attended many conferences and volunteer social functions. I enjoyed all of them.

How are you leveraging your finance background and relationship-building skills to lead and build your family’s entrepreneurial practice? Are there aspects of capital markets that surprisingly transferred well to running an entrepreneurial venture?

While I enjoyed my job, I decided to take a short break from work to lead an important expansion project for my family’s dental business. The project requires me to apply my business and financial acumen to scale up the practice. The initiative includes building new operatory rooms and recruiting new dentists, providing capacity for us to take on more new patients.

The skills I learned from the CFA Program and my work apply well in capital markets and the entrepreneurial setting. The financial analysis and investment knowledge gained from the CFA Program continue to apply well as I design the investment strategies for the business portfolios for risk/return and budgeting. My research and due diligence skills, strategic thinking, and leadership skills from my work roles transfer very well when I work with dental equipment providers to acquire new patient chairs and interview candidates for new dentists. This project has strengthened my strategic thinking, problem-solving, and entrepreneurial skills—skills that align well with leadership roles in the financial industry.

We must put all the skills developed over the years to good use, and we never stop learning. My passion remains in the financial industry. Upon completion of the

While technical skills are important, soft skills provide people with well-rounded and valuable backgrounds.

expansion project, I look forward to returning to the industry to focus on my career, b ringing new and improved skills with me.

You have been Chair of the Awards & University Relations Committee (Next Gen Program) for several years. How has volunteering with CFA Society Toronto complemented your professional growth, and how does it impact your industry perspective?

My volunteer roles with CFA Society Toronto started with being a mentor in the mentorship program and a panel judge for the Undergraduate Finance and Economics Awards and the CFA Institute Research Challenge. I am the Chair of the Next Gen Program, working with twelve investment

FUN FACTS:

What is your personal motto?

My favourite motto is “In faith go forward.” This is the motto of my high school. It represents a driven, resilient professional who confidently embraces challenges, builds trust, and pushes for continual growth.

If you could travel anywhere, where would it be and why?

If I could travel anywhere, I would travel to Austria. I have always been drawn to destinations rich in musical and cultural heritage, and Austria offers both in a unique way. Vienna and Salzburg are two cities where we can hear live classical music and stroll down nice streets. I have been playing the piano since elementary school, so visiting the places where Mozart and Schubert resided would be especially meaningful. Furthermore, the cuisine is fantastic, featuring dishes such as schnitzel and fresh-baked pastries at historic coffee houses.

professionals to organize competition events to empower others and nurture the next generation of investment professionals. In addition, I was honoured that CFA Society Toronto invited me to serve as the speaker for the 2023 CFA Charterholders Graduation Ceremony. I am very grateful to the Society for providing me with these valuable opportunities.

I have gained a lot through my volunteer experience, including developing leadership, presentation, and communication skills. I especially enjoy working with the fantastic team at the Society. Volunteering provides a great opportunity for us to apply what we have learned through the CFA Program, partner up with peers throughout the industry, and leverage each other’s talents to help give back to others. I strongly encourage CFA members to consider volunteering with the Society to broaden their skill sets and widen their exposure.

What trends are you seeing in the next generation of charterholders?

The next generation of charterholders is technologically adept, with an increased interest in environmental, social, and governance (ESG) and sustainable investing, alternative investments, and entrepreneurial ventures. The finance industry is becoming more tech-driven, a nd young professionals are developing stronger quantitative and programming skills. In addition, while traditional asset management and equity research remain core areas, there is increasing interest in entering private markets, private wealth, and fintech. The CFA Program has evolved to keep pace with the industry. This year, the CFA Level III Program is expanding to introduce two new specialized pathways, including private markets and private wealth, in addition to the existing portfolio management pathway.

Where will you focus your energy over the next five years? Are there any broader industry shifts you anticipate?

I anticipate we will continue to grow in private markets and alternative investments. Private equity, venture capital, private credit, and real assets will play an increasingly important role in portfolio diversification. Artificial intelligence-powered analytics will continue to evolve, and AI-driven portfolio management and automated trading will gain more traction. In addition, ESG and sustainable investing will accelerate, with stricter regulations on ESG reporting and climate-related disclosures. I plan to return to the financial industry upon completion of my dental expansion project. Over the next five years I aim to deepen my current expertise and to broaden my learning in areas such as strategy, private markets, and AI-driven analytics.

This article was edited for length and clarity.

Angha Gupta, CFA, is a Senior Analyst in S&P Global Ratings. She holds an MBA from Ivey Business School and is an FSA Credential Holder from International Financial Reporting Standards. She is a member of the Corporate Finance Committee at CFA Society Toronto.

From Mailroom to Dragon’s Den: Wes Hall on Resilience, Leadership & Legacy

(Editor’s Note: This article is based on Season 1, Episode 3 of Diverse Dividends, CFA Society Toronto’s video podcast

When Wes Hall immigrated to Canada from rural Jamaica in 1985, he could not have imagined how far he’d travel: Chancellor at the University of Toronto, founder and CEO of Kingsdale Advisors, Dragon on CBC’s Dragon’s Den, and passionate activist through the BlackNorth Initiative. Along the way, however, a humble mantra has guided him: Take one “baby step” after another, embrace each failure, and never rest on your laurels.

The power of baby steps

“It all started in a mailroom at a downtown law firm,” Hall recalls. “I’d never been above the second floor of a building before. My ears literally popped on the 13th floor.” This early career opportunity changed his life because it broadened his vision of what he could accomplish and allowed him to open the door to others. ”I saw what was possible,” he says, and he started to replicate those small successes: crawls into steps, steps into runs, and runs into flights of entrepreneurial enthusiasm. “A baby doesn’t stop walking when it falls. It just gets up and tries again,” Hall reminds us. Advice as applicable to business presentations as to bedtime routines.

Solution-oriented leadership

For Hall, genuine leadership is assuming responsibility for each outcome. “When things go wrong, point no fingers. Instead ask, ‘What decision led us there, and how do we fix it?’” That problem-solving attitude has been rewarded whether he’s leading clients through proxy battles or advising prime ministers on trade wars. When you are a leader and something goes wrong, take the time to reflect on why a decision was made and to create a plan to make a better decision next time without pointing fingers. It’s important to fix what went wrong or pivot. "Blame kills momentum. Accountability fuels progress."

If you can land an elephant, it will be so much easier to catch a gazelle

Twenty-two years ago, Hall created something that he didn’t see in the Canadian landscape: a space for activist investors. After having his vision turned down by investors, he placed a mortgage

on his house and Kingsdale Advisors was born. Vision and ambition have been cornerstones of Hall’s career, and his first “elephant” client was Sun Life Financial, which had the largest retail shareholder base in the day. Since then, his successes with Sun Life drew other clients in.

series featuring Wes Hall.)

Diverse Dividends

Diverse Dividends is CFA Society Toronto’s new video podcast series from The Analyst, which aims to explore the rich mosaic of the finance and investment industry. Each month, Diverse Dividends features candid, in-depth interviews with industry leaders across the finance and investment world as they share their insights on mindsets, strategies, and lessons that drive their success.

Why listen?

• Actionable insights: Gain concrete ideas to boost resilience, leadership, and innovation.

• Unfiltered dialogue: Learn how industry pioneers navigated setbacks and seized opportunity.

• Community connection: Join fellow members in thoughtful discussions that spark inclusive change.

Where to find us

Listen during your commute, enjoy it at home for a deep-dive session, or watch Diverse Dividends for a richer, more immersive experience. Join our growing community and take away actionable ideas that can transform both your mindset and your bottom line.

• Podcast apps: Subscribe on Apple Podcasts, Spotify, SoundCloud, or YouTube

• Online: Stream full episodes at cfatoronto.ca

Don’t miss a single episode! Tune in to Diverse Dividends wherever and however you love to listen and reap the dividends of diverse experience!

“That win became our CV,” he says, proving that sometimes you need to go big or go home. “Once we’d won Sun Life’s trust, every other door opened.”

Own your seat at the table

When you’re the only person in the room who looks like you, “It’s a message to say, ‘well, you don’t belong here,’” says Hall, acknowledging the societal influence of imposter system. “Use the spotlight,” he advises, “and remind people precisely why you belong.” If he had let seeing people who didn’t look like him in positions of power affect him, he never would have seen the success he enjoys today. “I always say that my Blackness is my superpower,” Hall laughs. “People automatically underestimate your abilities until you start to show what you’re capable of doing. By the time they figure it out, you have the upper hand.” Explaining how to reframe mindset around imposter syndrome, Hall explains, “When we want to get to the next level, we automatically assume that everyone there is better than us… until we get there and realize it’s just like society: some people are smarter, and others are not.”

Understand the value of unconventional champions

Hall recalls that one of the best jobs he ever had was when he was 25 years old and working at Canwest Global. The General Counsel was a 35-year-old white man who was incredibly hard on him, and he didn't understand why. “I couldn't understand why he was so tough on me. And he explained

it to me later on: ‘I saw your talent, and when I didn't see you living up to it, it was disappointing to me because I know life is going to be hard for you, so I'm making it tough for you… When you leave this place, and you will because you're ambitious, you’re going to be okay and withstand all the storms coming your way in the future.’”

Many such mentors have been allies to Hall over his career, despite looking nothing like him, focusing their efforts on him realizing his potential and inspiring him to do the same.

Legacy: The power of generational thinking

Nowadays, victory is not quantified by Hall in terms of accolades but in the world he leaves behind for future generations. “I’m no longer just thinking about my children, but about their children,” he asserts. “How can I do better to bring life improvement for those who are coming?” He describes the difference between the Canada he came to in 1985 at just 16 years old, with his father, who worked in a factory and fought to bring him opportunities. He asserts that every generation should think one to two generations ahead and consider how they can make it better as their own personal legacy. It’s a call to construct much beyond individual ambition.

Whatever you have can be gone in minutes, or even seconds, so focus on what’s important

Hall emphasizes the value of your principles, family, and close relationships. “I kind of live my life on the basis that,

He asserts that every generation should think one to two generations ahead and consider how they can make it better as their own personal legacy.

whatever I have, it can be gone within minutes or seconds. But there are certain things in your life… your principles, your family, and really close relationships. It doesn’t really matter if you’ve lost your wealth. It doesn’t matter if you lost your influence. Those people will always be there to support you. And those are the people that I focus my life on.” If you have these things, it doesn’t matter if you’ve lost a prestigious position, wealth, or influence.

Wes Hall's journey from the mailroom to the pinnacle of Canadian finance is a testament that greatness is rarely bestowed: it's earned one step at a time. From rising analyst to seasoned partner, his insights to finance and investment professionals seeking to advance their careers is:

➥ Stay hungry. Satisfaction kills motivation.

➥ Own every outcome. No blame, only solutions.

➥ Aim high. Land your elephant, then the gazelles follow.

➥ Think generationally. Build for those who come next. Use your difference. Your uniqueness is your advantage.

In every challenge and triumph, Wes Hall’s story exemplifies how perseverance, vision, and community can transform both personal journeys and the broader industry.

Subscribe & Listen Now on Your Favourite Channel:

Under Diverse Dividends: Under CFA Society Toronto:

Crafting an Alternative Career Path Through Professional Volunteering

By Eve Makarova, CFA

In today’s fast-paced and ever-evolving job market, professionals often seek ways to diversify their skills, expand their networks, and make a meaningful impact beyond their day-to-day roles. Professional volunteering is one of the most powerful yet underutilized avenues for achieving this. More than just an opportunity to give back, volunteering allows individuals to build an entirely separate career path that can either complement their existing profession or take them in a completely different direction.

Beyond giving back: Redefining professional volunteering

When most people think about volunteering, they picture charitable work or giving back to their professional community. While that is certainly part of it, professional volunteering offers so much more. It provides a structured platform to influence industry change, cultivate leadership skills, and establish a p resence in areas that may otherwise be difficult to access. By taking on volunteer roles, professionals can craft an alternative career trajectory—one that opens doors to opportunities they may have never considered before.

Driving

industry change in a meaningful way

Volunteering within a professional organization can be more than just contributing time; it can be a chance to shape the future of an industry. Many volunteer-led initiatives focus on policy advocacy, mentorship programs, and diversity projects that drive substantial change. Professionals who engage in these efforts are not only strengthening their resumes but are

also leaving a lasting impact on their field. Volunteers play a crucial role in the evolution of best practices and thought leadership by working on initiatives that address industry challenges.

Embracing creativity

Corporate roles often come with defined responsibilities, constraints, and hierarchical structures. Volunteering, on the other hand, offers a unique creative outlet where professionals can experiment with ideas, develop innovative programs, and explore alternative problem-solving approaches in a low-risk environment. Whether it’s planning industry events, curating thought leadership content, or designing new mentorship f rameworks, volunteers have autonomy to innovate in ways they might not have the opportunity to do in their primary careers.

Testing and refining leadership styles in a safe environment

One of the biggest advantages of professional volunteering

One of the biggest advantages of professional volunteering is the opportunity to develop an d refine leadership skills in a safer and more flexible setting

is the opportunity to develop and refine leadership skills in a safer and more flexible setting. Unlike corporate roles, where leadership promotions can be slow and incremental, volunteer positions often allow individuals to take on leadership responsibilities more quickly. This makes professional volunteering an ideal testing ground for different leadership styles—whether leading a project team, managing committee members, or influencing strategic decisions within a professional society.

Brian Madden, CFA, CFA Society Toronto Board Chair, shares his perspective:

“I began volunteering with CFA Society Toronto in 2010, serving on the Membership Committee before eventually moving into the Vice-Chair and Chair roles. In 2015, I joined the Society’s Mentorship Program and its committee. By 2020, I was elected to the Board of Directors and now serve as Chair. Beyond CFA Society Toronto, I volunteer on the University of Toronto’s Governing Council and the User Advisory Committee of the Accounting Standards Board. For all the hours I spend volunteering, I firmly believe I get back as much or more in benefits. The exposure to leadership, strategy, and governance has significantly enriched my perspective as an investor and industry professional. Leadership, in my view, is not just hierarchical—it’s about service. Volunteering has accelerated my career into an executive role, thanks in no small part to these experiences in my ‘parallel career.’”

Expanding your network by opening doors to new opportunities

Networking is one of the most critical aspects of career growth, yet many professionals struggle to connect beyond their immediate circle. Professional volunteering offers a unique way to engage with a diverse range of professionals across various sectors of the capital markets. These connections often lead to meaningful engagements, collaborations, and even career advancements that might not have been possible through traditional networking events alone.

Paul Hamilton, CFA, Mentorship Committee member, shares his journey:

“Like many people, my initial motivation to volunteer stemmed from my desire to give back and expand my professional network. I started volunteering with CFA Society Toronto in 2014, joining the Professional Development Committee. Over time, I took on greater responsibilities, eventually chairing the committee and later serving on the Board of Directors as Programming Chair during the challenging COVID-19 crisis. This experience gave me exposure to strategic planning, risk management, and finance in a not-for-profit setting. I learned how to ask better questions, think critically, and demonstrate leadership in a dynamic environment. If you’re on the path of professional development, there’s no better way than to volunteer. Volunteering is synonymous with learning.”

A first step: Volunteering with CFA Society

Toronto’s Mentorship Program

For CFA charterholders and candidates looking to start their volunteer journey, the CFA Society Toronto Mentorship Program provides an excellent starting point. Established in 2007, this program provides meaningful professional development opportunities and mentorship from experienced practitioners. Recognized by CFA Institute for its innovative approach, the Mentorship Program offers participants the chance to develop leadership skills, expand their networks, and contribute to the professional growth of others.

As senior adviser to the Mentorship Committee, professional volunteering has been a powerful tool for career growth, skill development, and community impact. My journey with the CFA Society Toronto Mentorship Program is a testament to this. I first joined as a protégé, seeking guidance and industry insights from experienced professionals. That experience not only shaped my career but also inspired me to give back. I transitioned into a mentor role, helping others navigate their professional paths. Eventually, I took on the challenge of leading the committee as Chair, overseeing the program’s growth and impact. This progression not only strengthened my leadership, communication, and strategic skills but also expanded my professional network and credibility in the industry. Volunteering in professional organizations is more than just giving back—it’s an opportunity to learn, lead, and grow in ways that directly enhance career success.

How to get involved

If you're interested in joining CFA Society Toronto’s Mentorship Program as a mentor or protégé, applications open annually in August. To learn more about the program structure, key dates, and application requirements, visit www.cfatoronto.ca or contact mentorship@cfatoronto.ca.

Final thoughts

Professional volunteering is more than just an altruistic endeavor—it is a strategic career move. Whether you are looking to build new skills, expand your network, or make a meaningful impact, getting involved in professional volunteering can be the first step toward crafting an alternative career path.

If you’re considering volunteering but aren’t sure where to begin, why not start here? The next chapter of your career journey could be just one volunteer opportunity away.

Eve Makarova, CFA is a seasoned investment professional with over fifteen years of experience in asset management, strategic advisory, and institutional client solutions. She currently serves as a Client Portfolio Manager at Mercer Canada and is a past Chair and current Senior Advisor of CFA Society Toronto’s Mentorship Committee.

Canadian Advocacy Council Quarterly Update

What’s new with the CAC?