INVESTING IN AFRICA’S EQUITY: BALANCING RISK, RETURN & REGRET

TAPPING INTO THE EAST AFRICAN GROWTH STORY VIA KENYA EQUITY MARKETS

INVESTING IN AFRICA’S EQUITY: BALANCING RISK, RETURN & REGRET TAPPING INTO THE EAST AFRICAN GROWTH STORY VIA KENYA EQUITY MARKETS

AFRICA EMERGING: LOOK FOR THE SIGNS TO INVEST

AFRICA EMERGING: LOOK FOR THE SIGNS TO INVEST

BRVM THE AFRICA HIDDEN GEMS: OVERVIEW AND OPPORTUNITIES

BRVM THE AFRICA HIDDEN GEMS: OVERVIEW AND OPPORTUNITIES

AFRICAN FUND MANAGER’S CONTINENTAL OUTLOOK

AFRICAN FUND MANAGER’S CONTINENTAL OUTLOOK

DEVELOPING AN APPROPRIATE BENCHMARK INDEX FOR AFRICAN EQUITY FUND IS THERE ROOM FOR ETFS IN THE AFRICAN CONTEXT?

DEVELOPING AN APPROPRIATE BENCHMARK INDEX FOR AFRICAN EQUITY FUND IS THERE ROOM FOR ETFS IN THE AFRICAN CONTEXT?

EQUITY ANALYST VIEWS: GHANA, MAURITIUS, ZIMBABWE, NIGERIA, AND MOROCCO

EQUITY ANALYST VIEWS: GHANA, MAURITIUS, ZIMBABWE, NIGERIA, AND MOROCCO

EDITORIAL TEAM

Associate Editor

Michael Osu

Contributing Experts

Tunde Akodu

Michael Osu

Advertising & Sales

Tola Ketiku

CONTENTS

FEATURED ARTICLES

Investing in Africa’s Equity: Balancing Risk, Return & Regret

Tapping into the East African Growth Story via Kenya Equity Markets

Africa Emerging: Look for the Signs to Invest

BRVM the Africa Hidden Gems: Overview and Opportunities

Equity Analysts View: Ghana’s stock market outlook and opportunities in 2016

Equity Analysts’ Opinion: Opportunities in Mauritius and Zimbabwe’s Equity Markets in 2016

African Fund Manager’s Continental Outlook

Finding Opportunities in Nigeria’s Equity Gloom

Morocco 2016 Macroeconomic and Equity Markets Prospects

Developing an Appropriate Benchmark Index for African Equity Fund

Is there room for ETFs in the African Context?

Welcome to the May edition of INTO AFRICA, a publication with fresh insight into Africa’s emerging capital markets.

The start of 2016 broke away from the well-known ‘January effect’ – a term coined to describe the seasonal irregularity witnessed in the financial markets over the years: the propensity of stock prices to increase during the first month of the year. In contrary, global equity markets had to navigate an ugly storm, as sell-offs ensued, driven by sentiment rather than fundamentals. As a result of rekindled concerns over global growth and the state of China’s economy, as well as the fresh lows seen in commodity prices, resulted in one of the worst results for global equity markets recorded in the month of January in history. African equity markets were not spared from this global bear sentiment.

In March, major equity markets rose, boosted by a welcome rally in commodity prices although overall in the first quarter of 2016, many equity markets posted declines, dragged down by expected slowdown in global economic --- the International Monetary Fund (IMF) warned that the global economy is at “a delicate juncture where risk of economic derailment has grown”, while the Bank of International Settlements cautioned against a “gathering storm” as investors begin to lose confidence in central banks.

So, the key questions are what is the short-term and long-term African equity outlook (amidst uncertainty) and where does opportunity lie in African equity markets? This edition of INTO AFRICA focuses on investing in African equities and aims to beam a ray of light on African equity fundamentals. In spite of short-term negative outlooks, powerful investment themes are driving the African equity markets for long-term investors and offering diversification potentials.

To analyze this trend further Philippe Koch, Head of Fund Management, iPRO Fund Management talks us through the ‘hybrid private equity approach’ mindset in his article Investing in Africa’s Equity: Balancing Risk, Return & Regret. He highlights what investors in African equities have to focus on to keep achieving the desired returns. Linet Muriungi, Head of Research, Dyer & Blair Investment Bank, Kenya takes a look at regional growth trends in Tapping into East African Growth Story via Kenya Equity Markets. She argues that the Impressive growth in the East African region makes Kenyan equities the continent investment hot spot.

Cavan Osborne, Fund Manager, Old Mutual African Frontiers Fund gives us the clues to this growth spurt in Africa Emerging: Look for the Signs to Invest Demba SOW, Head of Research, Mansa Musa Advisors looks at investing in Francophone West African Countries via the regional stock exchange (BVRM) in his article BRVM the Africa Hidden Gems: Overview and Opportunités. CFG Capital Markets Research Team, provides a bespoke overview of Morocco’s macroeconomic and equity markets prospects in 2016.

To compliment the viewpoints Randy Ackah-Mensah, Head, Trading & Sales, EDC Stockbrokers Limited, Ghana and Nana Kofi Agyeman Gyamfi, Head of Research, UMB Stockbroker Ghana provide commentaries on Ghana’s stock market outlook and opportunities. While Bhavik Desai, Research Analyst, AXYS Stockbroking, Mauritius and Phenias Mandaza, Head Research, EFE Securities, Zimbabwe look at Opportunities in Mauritius and Zimbabwe’s equity markets respectively in 2016.

In African Fund Manager’s Continental Outlook Andy Gboka, Portfolio Manager, Bellevue Asset Management discusses the investment climate as well as the key elements, drivers and dynamics that should inform a Fund Managers Investment Strategy. In the article Finding Opportunities in Nigeria’s Equity Gloom Tajudeen Ibrahim, Head of Research, Chapel Hill Denham Securities Limited determines that Nigerian equities still offer attractive valuations and Lanre Buluro, Head, Investment Research, Primera Africa Securities Limited thinks Nigerian equities are trading at historic lows, hence an opportunity for long-term investors.

To round off Zack Bezuidenhoudt, Head, Sub Saharan Africa and South Africa, S&P Dow Jones Indices walks us through Developing an Appropriate Benchmark Index for African Equity Fund and Pieter de Wet, Head of Research. Novare Equity Partners examines investing in the African equity markets via the Exchange Traded Funds (ETFs)

Kind regards,

Michael Osu Associate Editor Capital Markets

in Africa

DISCLAIMER:

The contents of this publication are general discussions reflecting the authors’ opinions of the typical issues involved in the respective subject areas and should not be relied upon as detailed or specific advice, or as professional advice of any kind. Whilst every care has been taken in preparing this document, no representation, warranty or undertaking (expressed or implied) is given and no responsibility or liability is accepted by CAPITAL MARKETS IN AFRICA or the authors or authors’ organisations as to the accuracy of the information contained and opinions expressed therein.

Connect with the Editor on Linkedin. Follow us on twitter @capitaMKTafrica.

To subscribe to INTO AFRICA, please send an email to intoafrica@capitalmarketsinafrica.com. Don’t forget to visit our website at www.capitalmarketsinafrica.com for the latest news, bespoke analysis, investment events and outlooks.

ENJOY!

MANAGING AFRICAN EQUITY

PORTFOLIOS IN A CHALLENGING ENVIRONMENT

INVESTING IN AFRICA’S EQUITY: BALANCING RISK, RETURN & REGRET

Philippe Koch, Head of Fund Management, iPRO Fund Management, Mauritius

Broad-based performance of African equities in 2015 was something many investors like to forget, if they do not regret their investment decision in the first place. Investors following the herd and buying into the asset class for the first time in the heydays of 2013 can be regularly found in the latter category. Others, who remained on the sidelines so far, can now buy great African businesses at much lower valuations.

The three African equity indices published by MSCI (MSCI Frontier Markets Africa , MSCI Emerging Frontier Markets Africa ex South Africa, MSCI Emerging Frontier Markets Africa) posted total returns in 2015 of -18.0%, -19.2% and -24.5%, respectively. IPRO’s long-only African equity strategy African Market Leaders (i2 share class) returned -21.0% to investors.

Total return of the MSCI Emerging Market Index was -14.6% in 2015, outperforming the MSCI Africa index family and most long-only US Dollar denominated African equity funds. A wedge in performance between the African indices and broader emerging markets can also be observed for longer periods and rolling returns. It looks like elevated risk and liquidity premiums for African equities versus their emerging market peers have regularly weighed on returns of broad indices in the past.

Risk and return of African equities: A macro story in good and bad times?

African equities have been mostly marketed as a macro story to potential investors - typical buzzwords are demographic dividend and rising middle class. Coincidentally or not, the downfall starting in 2014 followed also the macro script. Main drivers identified by most observers are (1) the rout in commodities and (2) currencies. Let’s have a look at them.

Regarding commodity rout, a regression of aggregate or country-specific African equity indices over commodity indices, like the Bloomberg Commodity Index, does not reveal a strong linear relationship over longer periods. Correlation increases substantially when using weekly data points as from Q2 2015, but the number of observations is too low to make any meaningful inferences. It looks like African equities have been only affected by the (preliminary) last leg of the commodity bear market, which started in 2011. They are in good company with other asset classes, such as global high yield corporate bonds.

As it is well known, correlation is not causation. Correlation coefficients are volatile and biased through the selection of time period, frequency and number of observations. But the data at hand is clearly indicating that price action in commodity markets is not the main

Paul Clark, Portfolio Manager, Ashburton Investments

driver for African equity prices. The Bloomberg Commodity Index, which is skewed towards energy, dropped by 24.7% in 2015. The fact that this performance is close to the US Dollar performance of a diversified portfolio of African equities in 2015 is mere coincidence in my view. The residual link to commodities is most probably coming from the performance of local African currencies, which brings us to the second driver identified.

We first need to distinguish between currency attribution on the portfolio level and the direct impact of currency volatility on African companies. 2015 was the year of U.S. Dollar strength against most world currencies. The U.S. Dollar Spot Index (DXY) rose by 9.3%, while the trade-weighted US Dollar Index of the St Louis Federal Reserve Bank rose by 10.5%. Negative currency attribution for a diversified portfolio of African equities was higher, particularly for portfolios with a large allocation towards South Africa.

Competitive currency devaluations around the world and the fall in prices for export commodities in specific cases, such as Nigeria and Zambia, were driving African currencies lower in 2015. Negative currency attribution explains between 60% and 80% of the underperformance of African equities against the S&P 500 in 2015, depending on country weights of the respective portfolio. Well understood that this does not give much consolation to (U.S.) investors, but if looking only at the equity delta, African equities have not done too badly. Unfortunately, currency hedging does not make sense for African equities, due to huge negative carry and illiquidity of currency forward markets. There is also a conceptual debate on whether currency hedging should be employed for a long-only equity portfolio, but let’s not go there for now.

Direct implications of currency volatility depends on the business model of the respective company. Most African economies are heavily import dependent. This partly explains the tendency of Af rican currencies to fall, in order to achieve better terms of trade. This is particularly acute for countries depending on export of a single commodity, once prices and/or volumes for the commodity in question decline.

Any regret on investment decisions cannot be alleviated through stop-loss strategies. You need to get it right from the start.

Companies whose costs of goods sold or financing costs are linked to the U.S. Dollar were suffering the most in 2015, as cost increases could not be transferred to the consumer. The consumer staples sector is here the prime example. Other sectors in Africa, such as financial services or real estate, include companies that generate revenues in U.S. Dollars. A lower local currency cost base also helped some of the otherwise struggling African commodity producers.

The macroeconomic vulnerability of African economies, which finds its expression in the value of local currencies, is indeed a problem for African businessmen and foreign investors alike. Here, sound macroeconomic policies and strong institutions, such as independent central banks led by well-educated technocrats, are required. While more needs to be done in that area, nobody can deny the progress Africa has made on that front in recent years. It is also remarkable that many African companies remain profitable throughout the cycle, even under adverse macroeconomic conditions. To make money in such environments requires extraordinary entrepreneurial talent, creativity and resilience. Rather than focusing always on the inherent risks, we have to keep in mind how some well-managed businesses in Africa will take off, once external conditions improve.

Investments into African equities: The ‘hybrid private equity approach’ African stock exchanges, with the exception of the JSE, still offer investors a relatively poor market structure, which leads to elevated liquidity premiums. Investment pools with a certain size have to apply a buy-and-hold strategy. Any regret on investment decisions cannot be alleviated through stop-loss strategies. You need to get it right from the start. We like to call this mindset the ‘hybrid private equity approach’.

The core of this approach is a rigorous bottom-up analysis of the business and regular interaction with management, while macroeconomic and political research serves as a risk-management overlay. Another feature of this approach is adding to promising investment cases on lower valuations, once Mr. Market throws some decent opportunities. Since IPRO has its roots in the niche equity markets of Mauritius and later Botswana, we have internalized this approach and apply it to other African markets.

It is important to align liabilities of the investment pool with underlying assets when investing into illiquid securities. Investors into African equities have to take the long view, ideally 7 to 10 years, and tolerate elevated cash holdings, if market valuations are not compelling. On larger drawdowns, it is advisable to increase capital commitments to improve the entry point and rebalance towards a target allocation. Investors able to hold illiquid assets while taking a very long term view, such as family offices, foundations or endowments, are natural investors for African equities. If investors follow a momentum-driven strategy in African equities, it is often a recipe for disaster.

At IPRO, we focus predominantly on market leading companies in Africa. Such companies are able to compound capital at sustainably high rates throughout the cycle, typically enjoying a quasi-monopoly or having a business model which represents a disruptive force in an otherwise competitive market.

I like to give some examples of how strongly some leading African companies have compounded over the years. Investors who bought shares of Equity Bank at its listing in August 2006 realized an annualized total return of 28.8% in March 2016. Another Kenyan company, East African Breweries, returned 24.6% per annum to investors who bought shares in January 1998. Despite current depressed valuation, Econet of Zimbabwe yielded 10.9% since May 2009. In Botswana, Choppies returned 15.7% annually to investors since January 2012. Sonatel from Senegal produced an annual return of 18.6% since December 1999. To emphasize, all returns stated are in U.S. Dollar and assume no reinvestment of dividends.

Of course this is cherry-picking, so let’s look at some of the more mediocre examples. Nigeria’s Dangote Cement returned only 8.0% since October 2010. Zanaco of Zambia yielded 5.9% to investors who bought shares in November 2008. Maroc Telecom had an annual return of 8.2% since December 2004. It is hard to find stocks of market leading companies in Africa that produced negative returns for investors over longer periods. It is also worth highlighting that practically none of the listed market leaders in Africa went out of business over the years.

We believe that investors into African equities have to focus much more on the intrinsic dynamics of the respective business, rather than focusing overly on macroeconomic and political drivers. It is important to understand those drivers for risk management purposes, and at times refrain from investments into otherwise sound companies when the external environment is rapidly deteriorating. But the most important aspect for investments into African equities remains the understanding of the underlying business, and patience in allowing capital to compound at superior rates of return.

Contributor Profiles

Philippe has over 16 years of experience in the financial services industry. He is responsible for the management of Pan African equity and fixed income portfolios at IPRO Fund Management. Philippe is also the lead Fund Manager of the African Market Leaders fund, a long only Pan African equity fund with a track record of about eight years. Setup in Mauritius in 1992 and present in Botswana since 2007, IPRO manages a small range of investment funds dedicated to the African Continent and its home markets Mauritius and Botswana, both in equities and bonds.

TAPPING INTO THE EAST AFRICAN GROWTH STORY VIA KENYA EQUITY MARKETS

Linet Muriungi, Head of Research, Dyer & Blair Investment Bank, Kenya

A look at regional output growth trends

The East African region’s output growth has outpaced Sub Saharan Africa’s GDP growth over the last 5 years, recording an average of 166bps above Sub Saharan African frontier economies’ 5 year average real output growth of 4.1%, to 2014. The impressive growth was primarily impelled by key structural shifts in broad economic sector contribution to regional output, progressive growth in private consumption as disposable incomes improve and increased public spend and infrastructure investment. The region in turn benefited from increased foreign direct investment (as a % of GDP) that averaged at 40 basis points above the Sub Saharan African average of 2.3% between 2009 and 2014, with key beneficiaries being the Infrastructure, Financial Services, ICT, Consumer services and Agriculture sectors. The East African region has also increased external trade interdependence, with 29% of the region’s exports directed to Sub Saharan economies.

Kenya’s output growth is expected to be driven by further public infrastructure spend and private consumption in 2016.

Kenya; the regional economic darling- expanding accessibility into inland markets via infrastructure investment

Kenya has outpaced neighbouring economies with regards to energy and transport infrastructure investment in the recent years, to see the country emerge as the locus of the East African Power Pool and a strategic access point to the inland export markets. These key investments allude to a shift in supply-side economics, as the country incentivizes further FDI flows via Greenfield and Brownfield projects to boost its slow growing manufacturing sector through provision of lower, more reliable power and route to inland market access for companies keen on establishing a regional footprint. The on-going Standard Gauge Railway (SGR) is set to reduce the freight time from the coastal region to East Uganda by 33% and a reduction in freight costs (per Km) by circa 60.0% to US$8.00 per metric tonne.

On the ICT front, an agreement between regional mobile telco giants resulted in a money transfer agreement among Kenya, Tanzania, DRC, Mozambique, Uganda, Rwanda and Zambia via the M-PESA platform further boosting remittance and trade among the countries. Kenya’s impressive growth in service-based sectors has observed a symbiotic relationship, more so in the financial services and ICT sectors averaging at 1.5x and 2.3x GDP growth, as the financial services telecoms sec-tor leverages off the high mobile penetration rate (>80%) to rapidly develop the mobile banking & money

Post 2015 Commodity Price Debacle

2015 saw a widening of twin deficits amongst net commodity exporters, hence currency depreciation, interest rate and inflationary pressures, as the EAC commodity export value was dampened by global commodity price dips and the strengthening of the US Dollar in real terms, prompting a tightening of regional fiscal policies. On the monetary policy front, a trade-off between currency stability and boosting economic output was witnessed, with Central Banks broadly employing short term reactive measures to control extreme currency volatility via money markets intervention.

Fast forward to 2016, the East African Community seems to have weathered the worst of the commodity price storm and Kenya’s economic outlook appears optimistic. The Kenyan Shilling has strengthened 0.8% against the US Dollar year to date on the back of a 24.9% y-o-y trade deficit contraction and shored up official forex reserves to levels above 4.5 months of import cover, as the oil price dip offset the soft commodity dip for the oil importer.

transfer space, which has in turn impelled growth in other sectors such as wholesale and retail trade.

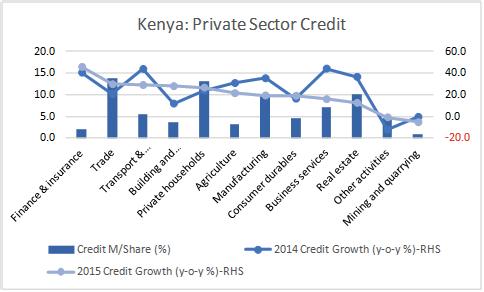

Kenya’s private sector continued to record sturdy credit uptake, despite high interest rates, with the production-centric credit uptake outpacing consumption-based credit uptake in 2015. Private sector credit grew 21% in 2015 and uptake was highest in Financial Services (46% y-o-y), Trade (30% y-o-y), Transport & Communication (29.0% y-o-y), Construction (27.9% y-o-y) and Private Household (26.6% y-o-y) in 2015, against an average lending rate climate of 15.9% (17.2% in November 2015) in 2015, (-68 bps y-o-y).

With protracted healthy credit growth in production driven sectors Kenya is expected to record sturdy growth despite interest rate headwinds. Fiscal deficit financing re-quirements may however create downside risk to interest rate declining in the short term due to increased public spend ahead of the general elections. On the flip side, the high interest rate may see a slowdown in consumption-centric money supply growth in the near term, keeping demand-pull inflation at bay, while the current cost push inflation is expected to remain subdued, as food security and low oil prices account for over 40% of the CPI basket in 2016.

Moving to the Market: valuations, market shocks and general election sentiment

Sub Saharan African Economies Frontier markets typically experience cyclical output growth and market movement attributable to external shocks or election-related shocks, as the private sector and foreign investors attach a political risk premium during election period. Kenya is not exempt to these cycles. However, during the last general election, the equities market actually rallied during the pre and post-election period, with the NSE-20 and NASI indices up 21% and 44% respectively as at year end. We believe this to be indicative of higher foreign investor confidence in the Kenyan economy, relative to other SSA economies, given Kenya’s openness to election monitoring from the international community as well as the country’s strong economic fundamentals. Additionally, there is lower uncertainty attached to the election outcome, given that the incumbent Jubilee Government is running against the other key political party; the Coalition for Reforms and

Democracy (CORD). Optimistic foreign investor sentiment can be further supported by a year-to-date net foreign investor inflow into the equities market, as they currently assume a net buying position.

Kenya has outpaced neighbouring economies with regards to energy and transport infrastructure investment … emerge as the locus of the East African Power Pool.

The market cap-weighted NSE P/E and P/E multiples have declined rather significantly year on year to 11.5x and 4.5x respectively, relative to 15.7x and 6.3x, while the market offers decent dividend yield (4.1%) and impressive Return on Equity (33.9%) rendering the NSE a buyer’s market. Key sectors to watch out for include the banking sector, FMCG and Telcos. We also believe there are packets of value to be unlocked in select stocks in the cement, investments, downstream oil and utilities spaces. The banking industry’s loan book growth reports 21%-24% growth over the last 4 years to 2015. Net Interest Margins (NIMs) remain healthy at approximately 9%. Kenyan banks are currently trading at a discount, relative to African Banks, and current levels therefore provide an attractive entry point. Supported by a growing middle class, we expect private consumption to impel the FMCG sector growth in 2016.

Regarding the mobile telcos space, Kenya’s ICT Sector continues to record strong growth at approximately 2.3 x GDP growths primarily driven by the mobile telecommunications space. Mobile telcos are expected to continue recording double digit bottom line growth on the back of non-voice revenue growth and improved EBITDA margins going forward. While mobile telco trades at a slight premium to the market median on an EV/EBITDA multiple basis, we believe the non-voice revenue growth potential to be unlocked from mobile data and money transfer to compensate for the premium.

Contributor’s Profile

Linet Muriungi joined Dyer & Blair Investment Bank in November 2015 and she is responsible for covering FMCG, Cement, Utilities and Telcos. Prior Dyer & Blair is renowned for topping investment bank rankings, having executed several landmark transactions including transaction advisor for the USD 840m Safaricom IPO, Sole advisor to the USD 180m acquisition of Equity Bank’s 24.99% stake by Helios and USD 317.5mn capital restructuring programme by Kenya Power Company Limited. The brokerage division executes transactions across the equities and fixed income markets and provides access to the Kenya, Uganda, Tanzania and Rwanda markets for both retail and institutional investors. to Dyer & Blair, she worked at Kestrel Capital (EA) for 3 years as an analyst covering Banking, Telcos, Utilities and Cement.

AFRICA EMERGING: LOOK FOR THE SIGNS TO INVEST

Cavan Osborne, Fund Manager, Old Mutual African Frontiers Fund

KEY TAKEOUTS: Strong case for investing in African, Markets quick to respond to recovery. Keep an eye on currencies

As global markets grapple with lower economic growth, the focus has shifted away from Africa as a growth engine of the future. A slump in the oil price, coupled with falling demand for commodities has depressed many African economies. While the global economy shows little immediate signs of recovery, South Africans would do well to remember that the medium- to longer-term arguments for investing in other African countries still stand:

Africa is coming off a low base (as are many other frontier markets).

Africa has one of the youngest and the fastest growing population in the world. This means less old people to care for and more people coming of working age that can contribute to economic growth.

WHEN

African markets, excluding South Africa, are less correlated to world markets and so offer some diversification benefits.

African currencies tend to be more stable than the rand (with Ghana being the exception).

South African pension regulation has allowed a specific 5% allocation to invest in Africa.

IS IT TIME TO INVEST IN AFRICA?

At Old Mutual Equities, our fundamental, valuation-based approach to investing is enhanced by using three other select themes: growth, quality and sentiment. This multi-factor approach to selecting shares is helpful in thinking about timing our investments in the rest of Africa.

1. Valuation

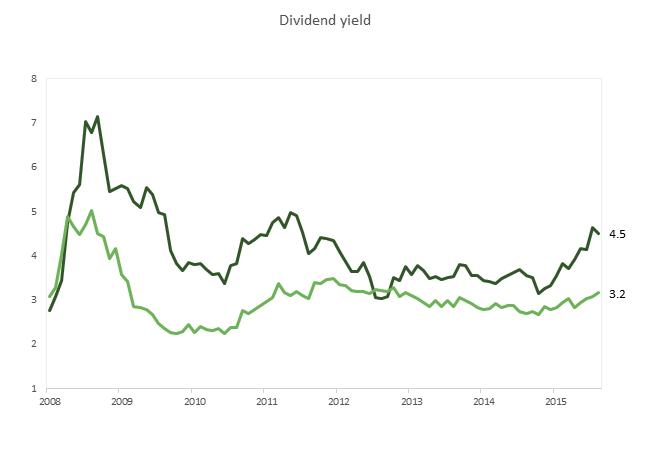

We use the MSCI Frontier Markets Africa Index (excluding South Africa) as our benchmark. This Index peaked in September 2014, but by the end of March 2016 was down around 35% in US dollars terms and nearly 20% in rand terms from this high. At the same time, the dividend yield is sitting at 4.5%, compared with the MSCI South Africa Index’s 3.0%.

Furthermore, Africa (excluding SA) is trading at a price: earnings multiple of 9.7 times – almost half that of SA at 17.4 times (admittedly, SA is distorted by highly rated Naspers).

Source: Bloomberg, MSCI

2. Quality

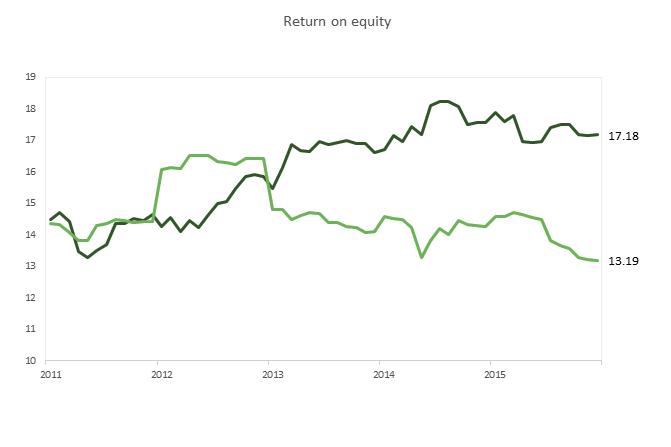

While this doesn’t have much to do with timing, it is worth a quick mention. While competition is increasing in some areas, many African companies actually enjoy monopoly status, which allows for attractive returns, highlighted below with ROE’s higher than the SA market.

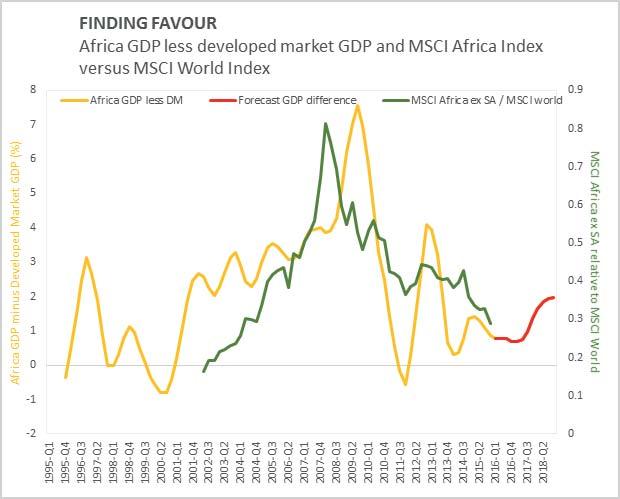

FINDING FAVOUR

3. Growth

This is probably the most important factor to consider. Share prices are ultimately driven by supply and demand. For the past few years, emerging markets have been unloved, so it is very important to think about when they will come back into favour.

What this graph tells us is that in early 2000’s, as the GDP growth difference between African countries and developed countries was widening, at the same time MSCI Africa Index outperformed the MSCI world Index. Since 2008, the gap in economic growth has been narrowing and African stock markets have underperformed. Based on forecasts from Global Insights, the growth difference is expected to remain stable in 2016 and then start widening again in 2017. Of course, markets usually react ahead of time, so it is important to keep on top of this chart.

4. Sentiment

When looking at sentiment within Africa, we define it as the currency outlook. While currency movements have historically accounted for around 25% of returns in emerging markets, over the past year this has accounted for closer to 90% of returns. Rand investors will know all about this. It is best to invest after currency devaluation.

2015 was a terrible year for many African currencies (in fact, all frontier and emerging market currencies struggled)but, given that some Africa currencies are managed, it could have been worse. The worst performing currencies in Africa were the rand and the Zambian kwacha. With many currencies having weakened, this exchange rate risk has reduced. That said, we would wait for further devaluation of the two most important African currencies (ignoring the rand).

The Egyptian pound devalued by 15% in mid-March 2016, but there could be further devaluation. Nigeria, Africa’s largest economy, still needs its currency to devalue.

IS “REST OF AFRICA” ATTRACTIVELY PRICED?

We believe it is, but before investing we would suggest waiting until after a Nigerian naira devaluation and

possibly also a further downward movement of the Egyptian pound. However, we think that the real positive returns will transpire once global economic growth accelerates and the “deep pocket” investors from the developed markets start looking to take advantage of what Africa offers.

Finally, when thinking about investing in the rest Africa, you have to remember… there are over 50 countries on the continent and they are not all about commodity prices. While overall growth on the continent is being restrained by the two largest economies, South Africa and Nigeria, there are still a good number of countries that are continuing to deliver economic growth in excess of 5% particularly in East Africa, an area that benefits from lower oil and other commodity prices.

THE STIRRING SIGNS OF CHANGE

As global growth slows, Africa has become the forgotten continent. However, market sentiment turns quickly and Africa will, undoubtedly, regain favour with investors. We are constantly looking for those zephyrs of change on behalf of our clients. Investing in Africa is not without challenges, but can a long-term investor risk not having exposure to one of the growth engines of the future?

Contributor Profile

Cavan joined Old Mutual Investment Group in April 2007 and has managed the Old Mutual Pan Africa Fund (OMPAF) and Old Mutual African Frontiers Fund (OMAFF).

Since 2012 he was the analyst for JSE-listed industrial companies and portfolio manager of the Old Mutual Industrial Fund, a South Africa based mutual fund.

During this time he was rated in Financial Mail Analysts’ survey in six categories: diversified industrials; support services; transport, building and construction; hotels, gaming and leisure and small and mid-cap companies.

Cavan has 15 years of work experience in the investment industry.

BRVM THE AFRICA HIDDEN GEMS: OVERVIEW AND OPPORTUNITIES

Demba SOW, Head of Research, Mansa Musa Advisors

BRVM, the year 2016 started on a bearish note, with most international stock exchanges indices stumbling Global equity markets began 2016 on a bearish note and most international stock indices stumbled, as a result of concern with slowdown in China economy and commodity slump. The West African region stock exchange, BRVM, also witnessed a slowdown, but not for the same reasons. The bearish witnessed by BRVM slowdown was largely due to sell-off as a result of investors cashing in their profits. Indeed, in 2015 BRVM was African stock exchange best performer with its all-share index (the BRVM composite) returning 17.8% in local currency (4.7% in US dollar), while all other African stock exchanges, with the exception of Botswana, recorded negative returns. Although, in early February, momentum seemed to return and the BRVM Composite index reached a 4.50% year to date performance, as at end of April 2016.

What are some key highlights of 2015?

Back in 2015, the latter index has been bullish most of the year with a great pick-up during the month of July, thanks to first semester dividends earnings reinvestment. Telcos (SONATEL Senegal and ONATEL Burkina Faso) and other large cap companies (Societe Generale Cote d'Ivoire and Total Cote d'Ivoire) were the usual suspects in the trading volumes category. When it comes to performance, mid and small cap companies gained more attention and thus recorded a strong price growth. Indeed, while the BRVM 10 index (including the 10 most liquid stocks) was up by 8.5%, the BRVM Composite recorded a 17.8% performance, compared respectively to 8.6% and 11.23% in 2014. The best performing sectors were Distribution (95.1%), Transport (25.7%) and Logistic & Utilities (16.0%). The laggard was the Agriculture sector, which was down by 27.7%, hit by a global fall in commodities prices, especially rubber and palm oil that affected financial results of Societe Generale Cote d'Ivoire, PALM Cote d'Ivoire and SAPH Cote D'Ivoire. It is important to note that despite strong concerns coming from the Ebola crisis, security issues in the Sahel and 2015 elections in Côte d'Ivoire and Burkina Faso, which both took place peacefully, the WAEMU zone managed to keep a strong growth of 6% led by Côte d'Ivoire's continued economic expansion.

What makes the BRVM a hidden gem?

The blue chips (SONATEL Senegal, ONATEL Burkina Faso, ECOBANK Transnational Incorporated Togo, Societe Generale Cote d'Ivoire), despite increasing in value, experienced a tough year as shareholders try to diversify their portfolio allocation and opting for fresh new opportunities, especially within medium and small cap companies. Cote d’Ivoire, which accounted for 82% of

the listed companies, has been witnessing a strong recovery in domestic consumption, hence sent a strong message towards international and local investors thus increasing their appetite for BRVM stocks and bonds, and of course boosting FDIs. In addition the government of Côte d'Ivoire improved their communication efforts through conferences and summits to promote the country's improved business climate and present investments opportunities. Indeed, projection figures are positive for the country, which expects to score the strongest GDP growth in Africa in 2016 with 7.7%, according to the Economist’s Intelligence Unit. The government renewed investors' appetite issuing several international bonds in USD and EURO denominated bonds, as well as Sukuks, Islamic bonds.

Diversification is always the key

The equity offering is well diversified by sector, covering financial services, telecoms, hydrocarbons, logistics, transportations, services, construction and agro-industries. There is also an active Bond Market displaying promising growth trends. According to latest data available, an estimated 270 bonds, worth XOF 2.91 trillion (EUR 4.9 billion), had been issued between 1998 and December 2014, of which 53% were in the form of sovereign issues offering a safe R.O.I. (Return On Investments), with offered yields varying from 3% to 7%. Being a regional stock market also has its perks, as investors can not only diversify their stock allocation by capitalisation size, sectors and financial products but also by countries, with 7 active countries out of 8 (Guinea Bissau not having listed companies yet). The regional currency’s peg to the Euro currency frees investments in the WAEMU zone from foreign exchange risk. It also greatly explains why the BRVM has not suffered from foreign exchange rates fallout in 2015, contrary to several other African stock exchanges.

A new impulse from the bourse

Beyond the outreach and promotion efforts from the Côte d'Ivoire government, the Stock Market entities themselves, in particular the BRVM, went on a promotional tour to attract more international investors with roadshows in Paris (2014), London and New-York City (2015). The latest edition has just taken place and was led by the newly elected BRVM President, architect Atepa Goudiaby, and the current Benin Prime Minister Lionel Zinsou, former PAI Partners CEO. It was a strategic move at a moment when BRVM stocks were gaining more visibility and recognition from international markets with S&P Dow Jones Indices (SPDJI) and Morgan Stanley Capital International (MSCI) launching indexes dedicated to the BRVM in 2014 . The "S&P BMI Index Côte d'Ivoire (Broad Market Index)" contains all shares listed on the BRVM, while the "MSCI Index WAEMU" index values 3 of

its major companies, SONATEL, ONATEL and SGBCI. This year, the BRVM and regional brokers through APSGI their professional association, are focusing their promotion and education efforts on targeting local investors within the region via their BRVM Days workshops sessions.

The equity offering is well diversified by sector, covering financial services, telecoms, hydrocarbons, logistics, transportations, services, construction and agroindustries.

Reforms to boost liquidity and BRVM 3.0

In the past years, two major reforms led to improved liquidity. The first came in 2012 with the revision led by the Stock Market regulator (CREPMF) allows share splitting to cater for smaller investors. This paved the way for stock splits on Sonatel (1/10 in November 2012), Onatel (1/10 in November 2013), Total CI (1/20 in April 2015) and Uniwax CI (1/5 in August 2015). This revised regulation had an immediate impact on liquidity, even though these shares already were featured amongst the five most traded stocks. The second major reform was implemented in mid-September 2013, when the market switched from the auction method to a continuous trading model. This has fostered greater trading to arbitrage price movements and has had an immediate impact on trading activity.

In December 2015, the BRVM inaugurated their brand new trading room in compliance with international standards in finance. This new setting will allow rolling out in a same place all operations related to trading, clearance and markets surveillance.

Innovation also came from market actors such as Impaxis Securities, a brokerage firm based in Dakar, which launched the first online trading platform of the WAEMU zone, available on both their website and mobile app, the first app developed in connection with the BRVM. These welcomed innovations fill a gap for information on the market and enable investors to follow up the BRVM market and their portfolio in real-time as well as placing buy and sell orders.

What is Next?

On the longer run, the BRVM is participating in the West Africa’s Capital Markets Integration (WACMI) initiative with Sierra Leone, Ghana and Nigeria exchanges that aims to boost intra-regional trading. The first phase of integration has already been rolled out, allowing reciprocal sponsored access for Accra and Lagos-based brokers. A second one will allow brokers to access the four West African financial markets (BRVM, Lagos SE, Ghana SE and Sierra Leone SE) as well as a common trading platform, scheduled for completion by 2020.

Investors craving for more IPOs and splits

The BRVM is expecting 20 new companies to list over the next three years, increasing attraction and boosting liquidity of the stock exchange. This could increase the number of listed companies in the equity compartment to 59 companies. In 2015, there was only one company listing and one capital increase on the stock exchange.

Municipal

bonds

Last year, in March 2015, the BRVM almost launched its first municipal bond for the city of Dakar, backed by USAID, the World Bank and the Bill & Melinda Gates Foundation, a sure achievement when South Africa is the only country to have done it on the whole continent. Unfortunately, a last minute decision coming from the national government of Senegal aborted the USD 40-million bond issue. As it is the case in many countries in Africa, many laws and regulations bar cities from issuing long-term debt, preventing local authorities to look for innovative ways to finance their development projects. Thankfully, public actors and financial players will gather in Dakar in April 25th this year at the Africa Municipal Bonds Forum to discuss the tremendous potential of municipal bonds as a tool for financing African cities' development.

To conclude, increasing interest from international investors is definitely putting the BRVM on the map and proving it is the new African financial market to consider thanks to not only its long-term high returns but also a great portfolio diversification opportunity. It is becoming a destination of choice for many international investors, eager to diversify their asset portfolio plus prospects are comforting and suggest good upcoming years.

Contributor’s Profile

Demba Sow is co-founder and head of research of Mansa Musa Advisors, a portfolio management firm based in Dakar, Senegal. He is the former partner francophone Africa at Asoko Insight Ltd. Demba combines 8 years of experience in investment management in Canada and Senegal, private banking in Switzerland and market research covering francophone West Africa. He holds a BBA in Finance and e-Commerce from HEC Montréal business school.

EQUITY ANALYSTS VIEW: GHANA’S STOCK MARKET OUTLOOK AND

OPPORTUNITIES IN 2016

Randy Ackah-Mensah, Head, Trading & Sales, EDC Stockbrokers Limited.

The market has not had a great run for the first quarter of 2016 as both indices, GSE Composite [GSE-CI] and GSE Financial stocks Index [ GSE-FSI] reported -4.16% and 5.50% respectively. This is as a result of uncertainties surrounding inflation and interest rates as well as and policy direction from Government among other concerns in a challenging operating environment for businesses in the country. However, the local currency has managed to remain fairly stable for the quarter, down only 1% making it possible for foreign investors to continue to fund inflows into Ghana’s capital markets especially within the fixed income space. A pending $ 1 billion Eurobond issue by Government within the second quarter is also expected to support the strength of the Ghana cedi and a continuous fall in treasury rates will likely bring investors back to the equity market.

With Ghana’s presidential elections being seven (7) months away in November, the market should be expecting more increased but guided spending by Government and a consequent increase in consumer spending. Listed companies within FMCG, oil marketing and distribution sectors will benefit from this growth and consequently attract investor interest on the GSE. Companies such as Fan Milk, Unilever, Benso Oil Palm, Ghana Oil and selected banks such as CAL Bank, GCB Bank and Ecobank Ghana are expected to boost the GSE’s composite index positively to close the year at an average YTD of 6% [GHS]. However, a strong quarter-on-quarter demonstration in significant improvements in impairment charges from listed banks can significantly bolster investor interest and subsequently increase returns beyond our expectations.

The market is also set to witness a number of capital raising programs via rights issues throughout the second and third quarters as Guinness Ghana, Ghana Oil and Societe General have all announced rights issue actions. Other possible issues could come from UT bank and Produce buying company. Profile

Contributor’s Profile

Randy Ackah-Mensah is the Head of Trading and Sales at EDC Stockbrokers Limited (a member of the Ecobank Group). Randy joined the Ecobank team in June 2012 and has so far been instrumental in deepening relationships with clients across the globe. Prior to joining EDC Stockbrokers Ltd, Randy was the Head of Africa Trading at Databank Brokerage Ltd. and actively repositioned the trading desk to grow its local market share to 40% amongst 19 competing brokerage firms in the industry. He built strong relations with partner brokers in Africa and global markets to drive the foreign trading business.

Nana Kofi Agyeman Gyamfi, head of Research, UMB Stockbroker Ghana. Investors on Ghana’s bourse may endure another challenging year with the persisting macroeconomic challenges specifically, the fragile local currency, high interest rates and utility rates expected to have an effect on the bottom-line of listed firms.

Additionally, as usual, the anticipated election fever, which will peak during the second half of this year, may also be another downside brake on risk taking.

The positives are that having witnessed declines in the last two years we do not anticipate another year of negative return on the stock market. Prices have bottomed out generally while the end to the energy challenges has been a boost to businesses. Furthermore, with the government’s activities under the keen eyes of the IMF we project economic fundamentals to witness some improvement going forward.

With regards to market opportunities, most of the banking stocks look attractive. Additionally, petroleum distribution stocks and insurance stocks appear to be great long term plays. Others that can also be thrown into the hat include Unilever Ghana, Fan Milk and Benso Oil Palm.

In the last twelve months, banking stocks have shed on the average 22% of their share prices inspite of the fact that majority of them posted resilient results in 2015. True, banks like UT Bank and HFC recorded loses in 2015 while Stanchart saw profit whittled down significantly by higher provisions but others like CAL Bank, GCB Bank and Ecobank Ghana saw impressive profit growth.

Fan Milk and Unilever, two manufacturing blue chips which suffered from the depreciating Cedi in 2013 -2014, and the unavailable power supply have seen a turnaround in fortunes.

Contributor’s Profile

Nana is the Head of Research at the investment division of Universal Merchant Bank, with main activities involve extensive financial analysis of listed and unlisted equities in Ghana. Nana also undertakes in-depth analysis of the Ghanaian economy and other investment vehicles.

Nana Kofi holds an MBA (Finance) from Stratford University in the USA. He also earned a B.A. Degree in Economics and Sociology from the University of Ghana, Legon, and holds a Dealer’s Representative License under the Securities Industry Law (SIL). He is a board member of a group that runs hotels and hostels in Accra.

EQUITY ANALYSTS’ OPINION: OPPORTUNITIES IN MAURITIUS AND ZIMBABWE’S EQUITY MARKETS IN 2016

Bhavik Desai, Research Analyst, AXYS Stockbroking, Mauritius

Mauritius has experienced a rough 2015. In addition to policy shifts under a freshly elected Government, the collapse of a conglomerate added uncertainty as well as adverse spill-over effects which explain why economic growth hovers at ~3.5%. Looking ahead, Government is trying to kick-start construction, and diversifies the economy through improved connectivity – both aerial and maritime – and taking advantage of marine resources.

On the Mauritian bourse, boosted by enhanced connectivity, we think the hospitality industry is poised to record another excellent year as average room rates are expected to increase. LUX (NRL MP) is this sector’s top pick as other hotel groups are highly leveraged and going through transition phases.

The shift from global sugar over-supply to under-supply is driving sugar prices higher. We therefore expect Sugarcane Conglomerates (ALTEO {ALT MP}, TERRA {TERA MP}, OMNI {MTMD MP} & MEDL {MSE MP}) to benefit from the 2016/2017 crop.

After five successive years of contraction, we think the construction sector has bottomed out and poised to register small growth. Therefore, we think building materials producers such as UBP (UBP MP). The financial industry is likely to have to undergo an evolution in coming years as a result of increasingly stringent reporting requirements (think FATCA) and diversifying business away from just a few specific jurisdictions. Therefore while we do not expect a stellar performance for the sector, we believe it is poised to register low-single digit growth.

Contributor’s Profile

Bhavik Desai leads the equity research and valuations department at AXYS Stockbroking which he joined in 2010. His primary foci are Mauritian equities and the burgeoning Mauritian fixed income market. Prior to joining AXYS, Bhavik worked on the implementation and monitoring of corporate strategies for the Office of the CEO at SAP Labs LLC in California. Bhavik holds a Double Bachelors in Arts in Physics and Astrophysics from the University of California, Berkeley.

Phenias Mandaza, Head Research, EFE Securities, Zimbabwe

The Zimbabwe Stock Exchange is one of the oldest exchanges on the African continent despite the lower level of development relative to others though the recent improvements have been quite commendable. Notable amongst these was the automation of the trading platform a development which in other markets generally implied improved trades and activity. Alas, for the ZSE the developments coincided with global emerging markets selloffs thus depressing activity while the local macroeconomic environment rendered the equities unpalatable. On the back of this background of foreign selloffs and low local investor participation on depressed liquidity most of the stocks on the bourse have seen themselves extending their discounts to their regional peers beyond what we would consider country specific discounts. As a consequence we are more than convinced that the ZSE has a lot of gems in the rough that have the potential to become powerhouses in the region while offering a good return on investment to those that will consider exposure to same. It is worth noting that the market’s top capitalized stocks have been the major casualties of the foreign selloffs and unsurprisingly they dominate our stocks to watch going forwards more-so with significant improvements in financials filtering in as companies adapt to stay afloat.

The recent reporting season has proven beyond reasonable doubt that most of the Zimbabwean companies have been adapting well to match the operating environment with most reporting improved bottom lines despite lower top lines due to the deflationary pressures. While prices are unlikely to recover the full year on year losses, most will certainly offer decent returns on investment to those who dare to tap into the unsuspected treasures of the ZSE.

Contributor’s Profile

Phenias is the head of research at EFE Securities having joined the company in 2009 as a research analyst. His career kicked off in 2008 at Imara Capital Zimbabwe as a clerk in the Asset management division and later moved to join the dealing team at the Stock broking arm of the same company in the same year. Phenias holds a B. Com (Hon) Finance Degree from the National University of Science and Technology awarded in the year 2008

AFRICAN FUND MANAGER’S CONTINENTAL OUTLOOK

Andy Gboka, Portfolio Manager, Bellevue Asset Management

Confident in the positive prospects embedded into Africa’s long term development, our team has been working on the best way to access the latter for almost a decade. In this purpose, one should be aware that intrinsic risks related to the region’s political and economic situation make the definition of an investment strategy relatively complex, especially when taking into account the features of the continent’s capital markets such as liquidity or FX volatility, to name a few. Consequently, our philosophy as institutional investors is to secure our exposure to Africa’ buoyant growth by basing our decisions on reforms which are likely to turn “a great potential” into tangible earnings.

From infrastructure investments, to social, fiscal and macro-economic policies, there are a wide range of measures needed to insure the fast growing-population and natural resources locally available become reliable drivers for sustainable growth in the long run. Thus, when assessing investment opportunities, we pay a particular attention to countries whose economic development appears structurally viable whilst we look for companies well positioned to benefit from fundamental changes in their respective industry. Although there is an obvious cyclicality driven by global markets dynamics, risk appetite for EM / frontier markets and commodities, our approach has been successful in both bullish and bearish cycles when we look at our LT performance.

More recently, the fall in commodities prices of the recent years has been a clear reminder to African nations that they have no choice but implement reforms should they wish to (1) shield themselves from external shocks but also (2) answer their own social and economic needs. This is well illustrated by the difficulties Nigeria, Angola and Ghana are facing today, and unveils how fragile the so called “growing middle-class” story is. Indeed, we have always been concerned by the misinterpretation of growth potential and subsequent risks of disappointment once markets realise the boost to domestic earnings over 2010/2013 (mostly based on consumption) is not sustainable once the “easy money” from the commodity rally disappears. In our opinion, the latter theme has acted as a double-hedged sword by turning investors’ perception of the continent to over bearish today, from over bullish back in 2010/11, whilst fundamentals have always pointed to a more balanced approach. This is exacerbated by political instability, poor visibility on the regulatory environment, unwillingness to push for “painful” macro adjustments that, overall, constitute a source of concerns for any investor willing to deploy capital into the region.

The mismatch between growth realities and equities valuation backed by the markets will continue to be part of the environment we invest in and remain a threat to our short term performance. However, we believe it also offers attractive returns in the medium to long term should one focus on “reform-led growth stories” whilst keeping an eye on conjectural developments affecting returns. For this year, we expect the dynamics seen in 2015 to continue to play out: on the one hand, net commodities exporter suffering, with business troubles spreading to most sectors of their economy; on the other hand, net importers benefiting from the low commodity price environment. Nonetheless, countries which have moved faster in social and economic measures aiming at driving a turnaround should perform much better than those not having done their homework. That said, our base case could be materially impacted by the pace and extent of any recovery or further weakness in commodities prices.

To sum it all up and finish on a constructive picture we think is real, African markets are going through a tough period which started in late 2014 – early 2015. Although the situation changes significantly from one country to another, we believe the upcoming months are likely to show new developments that will unlock some opportunities - not available a few years ago - which we are ready to seize in order to strengthen our portfolio.

Contributor’s Profile

Andy Gboka's roots lie in West Africa and therefore, having grown up in Ivory Coast as a dual French citizen, he has intricate knowledge of the local business environment. The experienced Sub-Saharan expert joined Bellevue Asset Management as a senior analyst / portfolio manager for the BB African Opportunities Fund at the beginning of 2015.

From 2011 to 2014 Andy Gboka was with Exotix LLP in London as a Senior Analyst covering listed African companies in the brewing, cement and industrial sectors. Prior to that, he spent three years at Société Générale's Corporate and Investment Banking unit as an Equity Analyst. Andy Gboka earned a Master's degree in finance from the Bordeaux Management School BEM and he is a Chartered Accountant

FINDING OPPORTUNITIES IN NIGERIA’S EQUITY GLOOM

Tajudeen Ibrahim, Head of Research, Chapel Hill Denham Securities Limited

Lanre Buluro, Head of Investment Research, Primera Africa Securities Limited

Nigerian equities offer attractive valuations says Tajudeen Ibrahim, Head of Research at Chapel Hill Denham Securities Limited

The Nigerian stock market offers attractive valuations relative to its global emerging and frontier market peers. The performance of the market (down c.10% YTD) is broadly reflective of external factors such as the falling crude oil prices and the strong US$ against many EM and FM currencies around the world. To put the valuations in context, the current P/E ratio of 16.4x for the Nigerian stock market compares favourably with the average P/E of 22.1x for the SCRIN (South, China, Russia, India, and Nigeria) and the average P/E of 20.8x for the MINT (Mexico, Indonesia, Nigeria, and Turkey). These valuations indicate that stocks are trading on the Nigerian Stock Exchange (NSE) at a 26% and 21% discount to the stocks trading on the SCRIN and MINT countries on average.

and MINT countries respectively. Thus, on a one-year forward basis, stocks are trading on the NSE at a more attractive PEG of 0.71 compared with the average PEG of 1.30 and 1.19 for the SCRIN and MINT countries respectively.

Nigerian Stock Exchange (NSE) at a 26% and 21% discount

to the stocks trading on the SCRIN and MINT

countries on average

The sectors we believe are appealing include the banking and industrial sectors in the short-to-medium term. For the banks, we see opportunities in the tier 1 segment as valuations appear cheap at the moment. It is also worth highlighting that bank stocks are liquid. We like GTBank (Rating: BUY, TP: N28.53), Zenith (Rating: BUY, TP: N22.70), UBA (Rating: BUY, TP: N6.55). We believe these banks are well-positioned to take advantage of emerging opportunities even the currently challenging operating environment. We also expect the banks to remain prudent in the creation of risk assets and maintain below-industry-average non-performing loan ratios. These banks are also expected to gain market share in e-banking to support non-interest income and centralize their operations for improved cost efficiency.

The valuation of the Nigerian stock market is also more compelling than the average of the SCRIN and MINT countries as indicated by the PEG ratio. The one-year earnings growth for Nigeria is more compelling at 23% compared to the average of 19% and 18% for the SCRIN

In the industrial sector, we are positive on Lafarge Africa (Rating: BUY, TP: N118:35) and Dangote Cement (Rating: BUY, TP: N209.00). We believe the two cement producers will benefit from government spending on infrastructure in 2016 and beyond. We see the construction and renovation of concrete roads, bridges, stadia, and houses among others as the driver of growth in this regard. The expansion story of Dangote Cement to other African countries remains a catalyst for volume growth in the short-to-medium term. For Lafarge Africa, the offering of extensive products such as Ready-Mix, concretes, and aggregates bodes well for earnings outlook.

Contributor Profile

Tajudeen is the Head of Research at Chapel Hill Denham Securities Limited. He has over 10 years’ experience in investment research and asset management. Prior to joining Chapel Hill Denham in 2012, he was an equity research analyst within the Standard Bank Group. He also managed the pension and gratuity funds of multinational companies within the Standard Bank Group. Tajudeen holds an MBA from University of Lagos and an M.Sc. and a B.Sc. in Mathematics from University of Ibadan.

Nigerian equities trading at historic lows, an opportunity for long-term investor - Lanre Buluro, ead, Investment Research, Primera Africa Securities Limited

It is a difficult time on the macro front, and this has led to the whole capital markets to be under selling pressure. Nigeria is oversold and stocks are trading at historic lows. On fundamentals, some listed companies are strong with sound business models, adaptable balance sheets and management capable of navigating the economic headwinds. But the inconsistent monetary policy, uncertainty around the exchange rate, and unclear fiscal policy has prompted investors, particularly foreign investors, to exit the equities market. Stocks are cheap, and this should be an opportunity to pick up blue chip companies at good prices.

We should note that the Nigerian equities market is not as deep as other developed markets, but opportunities exist for the prudent long term investor. Overall, 2016 will remain a volatile and challenging year as companies continue to deal with the effects of falling oil prices, FX illiquidity, and waning consumer demand. Investors should focus on companies with strong market share, diversified income streams, focus on cost leadership, strong balance sheet, and positioned to benefit from the government’s investment in infrastructure and agriculture. For the banks, we like GTBank, Zenith, UBA, and Access Bank for their liquid balance sheet, capitalization, risk management, profit outlook, and strong dividend. In the consumer space, our picks are

Nestle, Guinness, Dangote Sugar, Okomu Oil, and Presco. Dangote Sugar, Okomu, and Presco are in the agric/intermediate consumer space with product offerings in high demand and opportunity to earn FX via exports. In oil & gas, Seplat remains a stand out. Amidst the fall in oil prices, the long term outlook for Seplat is positive – increasing oil production, rising contribution from the gas business, and profitable. Finally, we like the building materials sector with Lafarge Africa and Dangote cement as our key picks. We see government infrastructural initiatives driving up cement demand and enhancing top and bottom-line of cement manufacturers. Capacity initiatives by both companies will capture the resurgence in cement demand. Also, their ex-Nigeria operations are a positive to cashflow and FX needs.

Contributor Profile

Lanre Buluro is Director at Primera Africa and in charge of the investment research platform at Primera. He has extensive global experience across investment banking, corporate finance, and equity research. He was a pioneer equity research Analyst at Bloomberg LP, covering the Biotechnology and Pharmaceutical industry. Prior to this, he worked as a corporate finance associate at Roche Pharmaceuticals focusing mainly on global in-licensing and acquisition opportunities. He began his professional career as a biochemist at Orchid Biosciences. Lanre is a Henry Rutgers Scholar with a BA in Molecular Biology & Biochemistry and Economics from Rutgers College and an MBA from Rutgers Business School.

MOROCCO 2016 MACROECONOMIC AND EQUITY MARKETS PROSPECTS

CFG Bank Capital Market Research Team

Macroeconomic prospects unfavourable but positive momentum

Prospects for the Morocco economy in 2016 are mixed with very weak economic growth on the one hand and, on the other, an on-going contraction in the twin deficits, which will help restore the long-term health of the country’s public finances and balance of payments.

As far as the growth outlook is concerned, expectations of weak GDP growth in 2016 should once again highlight the economy’s sensitivity to the agricultural sector and the vagaries of the weather, despite the considerable progress made in recent years under the Green Morocco Plan. In addition to the volatile character of the country’s GDP, the fact that non-agricultural GDP has registered only moderate growth has undoubtedly been the stand-out factor in since 2013. This is likely to remain so in 2016. Non-agricultural GDP is expected to grow by about 3%, well below the growth rate registered between 2004 and 2012.

This slowdown can partially be explained by the prevailing global economic situation which remains hesitant, particularly among the country’s main trading partners as well as a less expansionary fiscal policy. Such a slowdown is particularly symptomatic of Morocco’s economy entering a transition phase, resulting in the gradual emergence of new high value-added industries as drivers of the country’s economic development, at the expense of a number of ‘traditional’ sectors. The rapid development of the latter over the past decade has provided a strong boost to non-agricultural activity but the slowdown seen in recent years has been particularly marked.

The future flagship sectors of the Moroccan economy have been broadly identified as automobiles, aeronautics, food-processing and renewable energy while more ‘traditional’ sectors include tourism and phosphates. These sectors have performed remarkably well in recent years. However, their contribution to GDP growth and the knock-on effects on the country’s productive capacity are still inadequate to raise the general level of non-agricultural GDP. Given the likelihood that this situation will continue for a few more years, the scenario of persistently moderate growth of the non-agricultural component is the most likely one for the domestic economy over the coming years.

In the short to medium term, Morocco’s non-agricultural growth is likely to be between 3% and 4% with the top end of the range only achievable if the global economy were to show signs of a much more robust pick-up and if domestic fiscal policy were to become more expansionary. However, this scenario would seem to be highly unlikely over the short to medium term given the government’s current priorities. Despite the fact that the 2016 and medium-term economic growth forecasts hardly warrant anything more than cautious optimism, it is worth highlighting the significant contraction in the country’s twin deficits, after reaching worrying levels in 2012. This positive trend towards restoring equilibrium on the budgetary and external trade fronts paves the way for a number of major reforms. Therefore, it enables the government to focus on bringing about further reform in sensitive areas such as pensions reform, particularly with regard to civil servant and state corporation employee pensions with concerns growing over their viability. In addition, it provides the Central Bank with

the conditions needed to make a gradual and successful transition towards a floating exchange rate system.

Given the relatively sluggish state of the domestic economy, it is essential that Morocco tackles the shortcomings of its existing growth model and undertakes the structural reforms required to move towards a development model based on productivity growth rather than one governed by accumulating factors of production.

Opportunity for both aggressive and conservative … Despite an unfavourable macroeconomic outlook along with the expectation that earnings should not grow substantially in 2016, the CFG25 is up by 0.8% year-to-date. Indeed, as of February 19th, the market was up 3.2% to 19,718 pts after breaking its previous resistance at 19,400 pts. This was followed by a fall of the index by 2.3% which eroded the gains realized during the first weeks of the year. It is very noticeable that the market is hesitating after an early rally this year as a result of the uncertainty engendered by the heterogeneity of the factors impacting its prospects.

The antagonism inherent to the plurality of factors expected to impact the market in year 2016 create a lot of uncertainty regarding the trajectory that the market could follow. What we can quite confidently assert is that the performance of the market will be moderate should the market increase or decrease. Indeed, we believe that the market should increase by 5% at most (best case scenario) or also ebb by at most 5% (worst case scenario).

Amid the uncertainty that characterizes the market, we recommend two investment strategies that investors should elect based on their risk aversion, their expected returns and their investment horizon:

For an aggressive investment strategy with an investment horizon that hovers around 2-3 years, we recommend buying the stocks that are the most undervalued. As we believe for most of these stocks that the upside should start to materialize starting 2016, as a result of their current low valuation levels, and their high dividend yields which provides a downside protection.

On the contrary, for a conservative investment strategy, we recommend focusing on defensive stocks that offer high and sustainable dividend yields (i.e. dividend yields above the median dividend yield of the market). This strategy should yield the same return as a money market bond, i.e. a mild increase that would provide some protection in case the market remains in a bearish territory this year.

On a final note, we do believe that the performance of the market should be moderate regardless of whether the market ends the year in the green or the red. This conviction arises from the fact that the factors impacting this year are antithetic. In fact, on one hand, the market could suffer from an unpromising macroeconomic environment along with a mild growth of the aggregate earnings. On the other hand, the market should benefit from the decrease in bond yields, the attractiveness of the Moroccan market for foreign investors who perceive it as relatively defensive, as well as the recovery of certain sectors that have been extremely oversold in our opinion such as the real estate sector.

DEVELOPING AN APPROPRIATE BENCHMARK INDEX FOR AFRICAN EQUITY FUND

Zack Bezuidenhoudt, Client Coverage: Sub Saharan Africa and South Africa

Although most investors have adopted a preferred benchmark or index to measure or track the performance of developed markets, agreeing on benchmarks for emerging and frontier markets still needs to be established. The International Finance Corporation (IFC) coined the terms emerging markets and frontier markets and was the pioneer in creating equity indices in these markets. S&P Dow Jones Indices (SPDJI) acquired Africa Indices from the IFC in 2000 and now offers the most comprehensive index suite available with live history dating back to 1998. Selecting the most appropriate benchmark for an Africa Equity fund has been one of the most challenging, taking various factors into account as these markets develop and grow.

The two main factors to consider when developing or selecting any benchmark or index is the tradeoff between representativeness and tradability. As one increases the universe of stocks that represents an index, one typically finds that the tradability or use of the index becomes less efficient. Similarly, when only selecting highly liquid or tradable stocks one does not capture the true representation of the market.

Most index providers will construct indices by maintaining a good balance between liquidity of stocks and capturing a large percentage of the market. Reading the methodology documents supplied on index providers websites is always a good start to understand how the indices are constructed.

Indices are mainly used for two reasons, benchmarking and index products. Indices used for benchmarking purposes tend to be broader indices where fund managers can select stocks they expect will outperform the market, while indices used for index products tend to be more liquid indices and concentrated indices. Due to the lack of stocks in Africa, one naturally finds that most of the liquidity is concentrated in the largest stocks.

S&P Dow Jones Indices coverage for Africa includes South Africa, Egypt, Morocco, Tunisia, Botswana, Ghana, Côte D’Ivoire, Nigeria, Kenya, Mauritius, Namibia, Zambia, Zimbabwe as well as African companies listed on developed exchanges like Australia, Canada, France, UK, Switzerland and the USA. (African companies listed on developed exchanges need to derive a significant portion of their earnings and operations out of Africa to qualify for inclusion.)

Broad indices like the S&P Pan Africa and S&P All Africa indices offer a full universe of stocks without applying extremely strict liquidity, size and capping adjustments to the universe. These indices as well as similar indices from other index providers with less coverage, have however been criticized for the fact that sector and country exposure is not well diversified due to African economies still growing into mature well diversified economies. Outside of South Africa one will find that financial and telecommunication companies dominate listings. Most Africa equity funds aim not to invest more than 30% to 40% in a particular country or sector, and some adhere to a 5/10/40 rule whereby no stock can be more than 10%, and the sum of all stocks larger than 5% can’t be more than 40% in a fund. SPDJI addressed these concerns and requirements by introducing capped versions, where the index is capped on a country, sector and stocks level to minimize being over-exposed to a particular sector or geographical area.

Although having capped indices seem to have addressed diversification concerns, a larger concern relates to liquidity in Africa, as many exchanges excluding South Africa still only have a small number of equity listings as seen in the above tables. Primary listed Africa stocks excluding South Africa only represent 16% of the S&P Pan Africa BMI Index.

Another important factor to take into account when looking at Africa Indices, is the inclusion of a free-float factor. Free-float methodology excludes closely held shares such as those held by pension funds and governments. The percentage of closely held shares is rarely traded and should not be included in the available universe.

SPDJI have introduced indices that incorporate addition liquidity criteria and these indices are typically referred to as “SELECT” indices. The constituents selected for these indices not only have to meet specific average or median trading values per day, but also trade a specific amount of days out of all trading days. The Select indices also follow a capping approach in order to maintain the desirable representation and diversification. Indices like the S&P South Africa 50, S&P North Africa 15, S&P East Africa 10, S&P West Africa 25 and S&P Southern Africa ex SA 10 represent the largest and most liquid stocks for each of the main geographical areas.

Investors with a particular investment strategy or objective that is not aligned to a standard Africa index can look to work with index providers to construct a custom index. Custom indices can be constructed to incorporate regional, size, liquidity, turnover, rebalancing, currency, tax and many other unique requirements a client might need.

Investors seeking fair and equitable measurement should be aware of the various indices available to Africa Equity Funds, and make sure that their fund manager has selected a benchmark with similar representation and liquidity requirements, as well as risk-return characteristics. Having to pay performance fees against a cash plus-target, like LIBOR, should no longer be seen as appropriate for an Africa equity investment with the wide range of free float capital market benchmarks available.

Contributor’s Profile

Zack Bezuidenhoudt is head of client coverage, South Africa and Sub-Saharan Africa, at S&P Dow Jones Indices. The group focuses on business development, sales, and ongoing client relationship management. Zack

works proactively with existing and prospective clients in the region to deepen their knowledge of equity, fixed income, and strategy indices and to better understand their future indexing needs.

Prior to joining S&P Dow Jones Indices, Zack worked at Old Mutual Investment Group as a business development executive with a focus on business and product development for Old Mutual Global Index Trackers. Zack also worked at Alexander Forbes Asset Consultants and Barclays Africa as an asset consultant and head of performance surveys, after starting his career at ABSA Asset Consultants in 2005.

Zack has a BSc in Financial Mathematics from the University of Pretoria, as well as a CIPM from the CFA Institute and a Claritas® Certification from the CFA Institute.

IS THERE ROOM FOR ETFS IN THE AFRICAN CONTEXT?

Pieter de Wet, Head of Research. Novare Equity Partners

In the third quarter of 2015, financial commentators were abuzz when industry research group ETFGI announced that the global Exchange Traded Fund (“ETF”) market has surpassed the Hedge Fund industry in terms of size for the first time ever. With assets under management of $2.971 trillion as at the end of Q2 2015, its quarterly growth of $45 billion during the same quarter made it surpass the Hedge Fund industry’s $2.969 trillion.