MURRAY GRANT | MANAGING DIRECTOR, CDC GROUP’S AFRICA FUND

MURRAY GRANT | MANAGING DIRECTOR, CDC GROUP’S AFRICA FUND

EDITORIAL TEAM

Associate Editor

Michael Osu

Contributing Experts

Tunde Akodu

Michael Osu

Advertising & Sales

Tola Ketiku

CONTENTS

FEATURED ARTICLES

The extractive industries super cycle has ended – now what?

Short-term uncertainty creates investment opportunities in Africa

Investment in Africa – will the “Africa rising” story continue?

Africa’s long-term growth fundamental is unshaken

Exploring investment potentials in Angola & Mozambique

Fast-moving consumer goods challenges and opportunities in Africa

African Currencies: Economic Challenges and Opportunities

EXCLUSIVE INTERVIEWS

ANN WYMAN

Senior Officer, AfricInvest

FATIMA VAWDA

Managing Director, 27Four Investment Manager

ALISON KLEIN

Manager, Private Equity, FMO

Murray Grant

Managing Director, CDC group’s Africa Fund

Welcome to the April edition of INTO AFRICA, a publication from Capital Markets in Africa, the leading “one-stop” platform for Africa’s fastest-growing Financial, Capital Markets and Wealth Management industry. This publication aims at providing you with fresh insight into Africa’s emerging capital markets where we believe Africa is set for a challenging yet defining year ahead as it continues to build Investor confidence in the wider global community.

This edition of INTO AFRICA focuses on Investment prospects in Africa. Over the past few years, discussion about Africa’s development, prosperity, growth and potential was becoming more optimistic, so Africa seems to have conquered the myth of negative perception. The gained optimism has led to many buzzwords such as Africa rising; Africa the last frontier, Lion on the move etc. As a result, Africa is not hard to sell to investors and many investment pitches highlight the common reason why now is the time to invest in Africa. Africa features abundant mineral wealth, an immense amount of uncultivated, arable land, an improving political landscape and a growing, urbanizing and increasingly educated middle-class population. Consequently, major multinational companies have included Africa as part of their growth strategy keeping it top of mind for foreign business investment.

The recent economic downturn and headwinds that Africa is experiencing, is stimulating debate on Africa’s growth fundamentals and raising questions such as: Is Africa’s rising story real? Can Africa’s growth be sustainable? When China sneezes, does Africa catch cold? Africa could well be a sleeping giant so is the pessimism justified? To contribute to the debate, Robbie Cheadle (Associate Director, KPMG, South Africa) explores Foreign Direct Investment (FDI) trends in Sub-Saharan Africa in her article: The Extractive Industries Super Cycle has ended … Now What?

Maintaining a balanced view as always, we bring further insight into the Investment Outlook for Africa in 2016 with interviews from: Ann Wyman (Senior Officer, AfricInvest); Fatima Vawda (Founder and Managing Director, 27FOUR Investment Manager); Alison Klein (Manager, Private Equity, FMO) and Murray Grant (Managing Director, CDC Group Africa Fund). We put a number of thought provoking questions to them on their strategies for Africa and where they see the next trends. They conclude that current short-term uncertainty creates investment opportunities and Africa’s long-term growth fundamental is unshaken despite recent the slow down.

As with any Investment it is always important to keep an eye on downside risks and Africa is no different. In examining how to navigate investment risk in Africa, Claudine Fry and Gbenga Abosede (Associate Directors, Control Risk) identified major risks for Africa in 2016 and how to mange them in their article: Investment in Africa --- Will the “Africa Rising” Story Continue?

Oil and the extractive industries have long played a significant role in African economies. To give us insight into their effects and governmental diversification efforts Tiagio Dionisio (Chief Economist, Eaglestone Securities), provides a bespoke overview of investment opportunities in Angola and Mozambique. As African Governments therefore look to diversify away from the Oil sector Virusha Subban and Yonatan Sher, (Bowman Gilfillan Africa Group) showcase the potential of the Fast-Moving Consumer Goods (FMCGs) in Africa in the article: Fast-Moving Consumer Goods --Challenges and Opportunities in Africa.

To crown it all, find out what Prasad Dalavai and Vinesh Caumul (Bourse Africa Limited) think about current volatility in African currencies in their masterpiece write-up: African Currencies --Economic Challenges and Opportunities.

Kind regards,

The Editor Capital Markets in Africa

Connect with the Editor on Linkedin.

Follow us on twitter @capitaMKTafrica.

To subscribe to INTO AFRICA, please send an email to intoafrica@capitalmarketsinafrica.com.

Don’t forget to visit our website at www.capitalmarketsinafrica.com for the latest news, bespoke analysis, investment events and outlooks.

DISCLAIMER:

The contents of this publication are general discussions reflecting the authors’ opinions of the typical issues involved in the respective subject areas and should not be relied upon as detailed or specific advice, or as professional advice of any kind. Whilst every care has been taken in preparing this document, no representation, warranty or undertaking (expressed or implied) is given and no responsibility or liability is accepted by CAPITAL MARKETS IN AFRICA or the authors or authors’ organisations as to the accuracy of the information contained and opinions expressed therein.

ENJOY!

MANAGING AFRICAN EQUITY

PORTFOLIOS IN A CHALLENGING ENVIRONMENT

THE EXTRACTIVE INDUSTRIES SUPER CYCLE HAS ENDED.... ...NOW WHAT?

Foreign Direct Investment

During the five calendar years from 2010 to 2014, foreign direct investment (“FDI”) inflows into Africa increased in total by 22% from US$44.1 billion in 2010 to US$53.9 billion in 2014. It should be noted, however, that FDI inflows to Africa peaked at US$56.4 billion during 2012, declining by 4% to US$53.9 billion in 2013 and remaining static in 2014. The distribution of the FDI inflows to the different African regions changed significantly over this five year period, with Southern African’s share increasing from 7.9% in 2010 to 20% in 2014. Other FDI inflow gainers over this period were Central Africa, whose share of total FDI inflows into Africa increased from 18.9% during 2010 to 22.4% during 2014, and East Africa, whose share increased from 10.3% in 2010 to 12.6% in 2014. Those regions that lost out on FDI during this period were North Africa, whose share of total FDI inflows declined from 35.7% in 2010 to 21.4% during 2014 and West Africa, whose share declined from 27.2% in 2010 to 23.7% in 2014.

Key drivers of the FDI trends

The question as to what factors influenced FDI inflows to Africa over the five years to 2014 are well known and include, inter alia, lower growth expectations for the developed countries, a perception that Africa has become more politically mature and easier to access with improved judiciary systems, Africa’s increasing population and rise in consumption and Africa’s vast tracts of unutilised land and significant mineral and other resources.

The reasons for the change in the distribution of FDI inflows into Africa are also fairly obvious – FDI inflows to North Africa and West Africa declined largely due to armed conflict, political uncertainty and security threats in these regions, with Ebola also impacting on FDI inflows into West Africa during this period.

The increase in FDI inflows into Southern, Central and East Africa during the five years which ended in 2014, were driven by investment into the extractive industries, in particular, Zambia and Mozambique in Southern Africa; Uganda and Tanzania in East Africa and the Republic of Congo and Chad in Central Africa.

The FDI inflow trends during this five year period highlighted the fact that while high levels of corruption, poor infrastructure and onerous business conditions in certain African countries have always been considerations for potential investors into Africa, these are not overriding obstacles. Countries that have outstanding oil and gas and/or mineral resources

Paul Clark, Portfolio Manager, Ashburton Investments

Robbie Cheadle, Associate Director, Deal Advisory, KPMG in South Africa

attracted FDI inflows despite challenges in other areas, although policy uncertainty and political instability, including terrorism and security issues, do stand out as the biggest barriers to investment.

… while high levels of corruption, poor infrastructure … African countries have always been considerations for potential investors..

Extractive super-cycle has ended

The extractive industries “super-cycle” has come to an end, however, due to lower commodity and oil prices linked, inter alia, to the slowdown of the Chinese economy, and this has impacted heavily on resources seeking FDI. FDI inflows to Africa plunged by 31% during 2015 to US$38.0 billion, led by a decrease of 74% in FDI inflows to South Africa to US$1.5 billion, which is in line with a similar decline of FDI inflows into Australia and even larger FDI inflow reductions into Russia and Kazakhstan. These declines of FDI inflows into resources-based economies are in the context of an overall increase in world FDI inflows of approximately 36.5% during 2015 and an increase in FDI inflows to developing economies of approximately 5.3%. FDI inflows to developing Asia increased by approximately 15.5% during 2015, led by Hong Kong which received FDI inflows amounting to US$163 billion.

Emerging FDI Trends

The downturn in the resources cycle is expected to continue in the short to medium term, and while FDI inflows to African countries with exceptional extractive industries resources will continue, albeit at a materially reduced level, African countries need to strive to diversify their economies away from an over-reliance on the extractive industries. The real question then is, what is going to influence FDI inflows into Africa going forward?

It is interesting to note that while a large portion of the US$88.0 billion value of announced greenfield FDI projects to Africa during 2014 were in the extractive industries, a significant portion of the announced greenfield investment was also into the manufacturing and services sectors. This is an important trend as those African countries that are weathering the reducing FDI inflow storm the best, are those that have a focus on driving growth in the manufacturing or services sectors.

Three keen examples of Sub-Saharan African countries

Ashshbuburtrton on Invnvesestmmennts t

that are successfully starting to shift the focus of their economies are:

• Rwanda in Central Africa, which experienced increases in FDI inflows during 2014 of 4% and whose economy is largely agricultural with a particular focus on tea (9%) and coffee (10%);

• Kenya in East Africa which achieved increased FDI inflows of 96% during 2014 and whose major exports comprise tea (18%), horticulture (14%), manufactured goods (11%) and coffee (4%), and

• Ethiopia in East Africa which experienced increase FDI inflows of 26% during 2014 and whose main exports comprise of collectively coffee, tea, mate and spices (22%), oil seed (18%) edible vegetables (15%) and live trees and plants (5%).

African countries need to strive to diversify their economies away from an over-reliance on the extractive industries.

It is even more interesting to note that Rwanda, Kenya and Ethiopia all have better rankings in the World Bank, Ease of Doing Business Survey, 2015 (“Ease of Doing Business Survey”) and the Transparency International Corruption Perception Index, 2015 (“CPI”) than many of their African peers, although terrorism continues to impact on the Kenya’s security environment.

In review, the potential for the services sectors to develop Africa’s economy is considered to be significant according to the World Investment Report, 2015. In fact, the services sectors accounted for 48% of Africa’s stock of FDI in 2014; comprising of electricity, gas and water, construction, transport, storage, communications and business services, and manufacturing, which contributed 31% of Africa’s stock of FDI in 2014. However, to grow in the services and manufacturing sectors, African countries will need to compete with the world at large and will, therefore, need to improve their business environments. Individually, African countries need to focus on improvements in the areas of corruption, infrastructure, business conditions, policy certainty and security and regionally, Africa as a whole needs to improve in the areas of economic liberalisation and regional integration.

Contributor Profiles

Robbie Cheadle is an Associate Director at KPMG and a JSE accredited approved executive, responsible for KPMG's sponsor service offering and providing advice to JSE listed entities. She also provides guidance on compliance with the corporate governance requirements of King III and the Companies Act as it applies to Fundamental Transactions and the Takeover Regulations. Robbie lead the preparation and launch of KPMG's 2014 "Listing in Africa" publication, as well as the “Listing in Africa – Extractive Industries” publication which was launched at the Ministerial Symposium at the 2015 Mining Indaba, which set out the considerations for listing, listing criteria, processes, documentation requirements and continuing obligations relating to the Botswana Stock

Exchange, Ghana Stock Exchange, JSE Limited, Stock Exchange of Mauritius, Namibian Stock Exchange, Nigerian Stock Exchange, Nairobi Stock Exchange, Zambian Stock Exchange and the Zimbabwe Stock Exchange. Following the success of the “Listing in Africa” publications, a second series “Insights into African Capital Markets” is in progress, with the African Debt Market publication being launched in September 2015 and the What Influences Foreign Direct Investment into Africa publication to be launched during February 2016. Robbie also assisted with the proposed amendments to Section 13: Property Entities of the JSE Listings Requirements and the drafting of the related IRBA Guide for Registered Auditors: Reporting Responsibilities of the Reporting Accountant Relating to Property Entities in terms of the JSE Listings Requirements.

SHORTTERM UNCERTAINTY CREATES INVESTMENT OPPORTUNITIES IN AFRICA

ANN WYMAN

Senior Officer at AfricInvest, responsible for client relations. An internationally recognized economic and geopolitical researcher and manager with two decades of experience in financial services and consulting, Ann has worked as an economist and head of Emerging Markets Research at both Citi and Nomura. Ann also currently serves as a Senior Advisor at Gatehouse Advisory Partners, a geopolitical consulting firm based in London, and contributes analysis to Oxford Analytica, an internationally renown global analysis and advisory firm. Ann is a member of the board of the Tunisian American Enterprise Fund, established by the United States government to help foster stronger investment ties with Tunisia and launch local SMEs as engines for longer-term growth. Ann is a graduate of the University of Pennsylvania (BA), and Columbia University's School of International and Public Affairs (Masters).

CMinAfrica: What do you think will be the biggest potential challenge for global markets in 2016 and its possible impact on African markets?

Ann Wyman: Capital flows out of emerging markets have been a challenge at the start of 2016 for many countries, and have led to the strong depreciation of many EM currencies. The good news for North African countries is that they have been much less affected than places like China and Brazil, or big oil producing countries, because there has been a less dramatic response from foreign investors, many of whom have not placed capital in the region for short-term gains, but rather because of a commitment to the longer-term potential of these economies.

Fatima Vawda: The investing environment in Africa has been extraordinarily challenging over the past 12 months. Macro issues such as currency volatility, commodity prices and capital flows have seen a significant deterioration of confidence in the “Africa Rising” narrative. In this environment, it is difficult to extrapolate on generalised, short term opportunities across industries or countries. The short term opportunities at hand tend to be more stock specific in terms of pricing. In the long run, institutional reform, rising productivity and favourable demographics still characterise the Africa opportunity set. If you are of the view that we are close to or at peak USD strength, then now is an excellent time for strategic, long-term orientated investors to consider Africa. Many African stock s are trading at valuations not seen since 2009. Poor sentiment and cheap valuations mostly provide huge opportunity.

CMinAfrica: What are the strongest short-term or long-term opportunities for braver investors interested in North African at the moment?

Ann Wyman: AfricInvest sees opportunities in the region across a number of sectors, including healthcare, FMCG, education, logistics, technology, financial services and

FATIMA VAWDA

FOunder and Managing Director of 27four

Investment Managers, a pioneering South African multi-manager focused on the provision of innovative product solutions for retirement funds and individual investors. She has over 18 years experience in financial markets. Fatima started her career as a lecturer at The University of Witwatersrand in 1995 and also worked at Standard Bank, Peregrine Securities and Legae Capital before establishing 27four. Her areas of expertise include asset allocation and portfolio construction. Fatima has received numerous accolades during her career in asset management.

agribusiness.

CMinAfrica: What challenges do foreign investors have to consider when investing in Africa and how can they navigate these?

Ann Wyman: In some countries, the security environment remains one that concerns potential investors. Nonetheless, once on the ground, many investors realize that businesses day-to-day operations are not impeded by security issues. Moreover, there is a concentrated focus by policy-makers on this area given its importance not only to the business climate, but to the citizens of each country.

Fatima Vawda: China’s slowdown and the commodity bust will impact Africa’s growth prospects. Understanding the full implications of this is something that will challenge foreign investors. Already FX shortages in Nigeria and Egypt are leading to delays in capital repatriations. There are a lot of moving parts. It is important for foreign investors to recognise these and where possible, manage the risks.

CMinAfrica: What impact has the recent pessimism around African markets had on your investment portfolio?

Ann Wyman: We have actually not noticed much in way of pessimism around African markets. Quite the contrary, we have seen many more investors looking at the region than in years past. This means we are even more convinced of our deal-sourcing approach, which focuses on finding and securing exclusive deals, and not entering into bidding wars with our competition for transactions.

Fatima Vawda: Our Fund has a long-only mandate. The pessimism around African markets has resulted in a substantial decline in equity prices and FX rates. Our Fund performance has obviously not been immune to this trend and winning new mandates in this environment is challenging.

INVESTMENT IN AFRICA WILL THE “AFRICA RISING” STORY CONTINUE?

Claudine Fry and Gbenga Abosede, Control Risks

Low commodity prices, the worst drought in Southern Africa since 1982, on-going social unrest, the terrorism threat in East and West Africa - the list of doom and gloom scenarios for many African countries in 2016 is a long one.

But what about positive stories around major urban development projects; M&A deal-making in Africa reaching new heights1; improved anti-corruption legislation and enforcement; or Ethiopia’s emergence as a major FDI target country? What is negative perception only and how optimistic can investors really be?

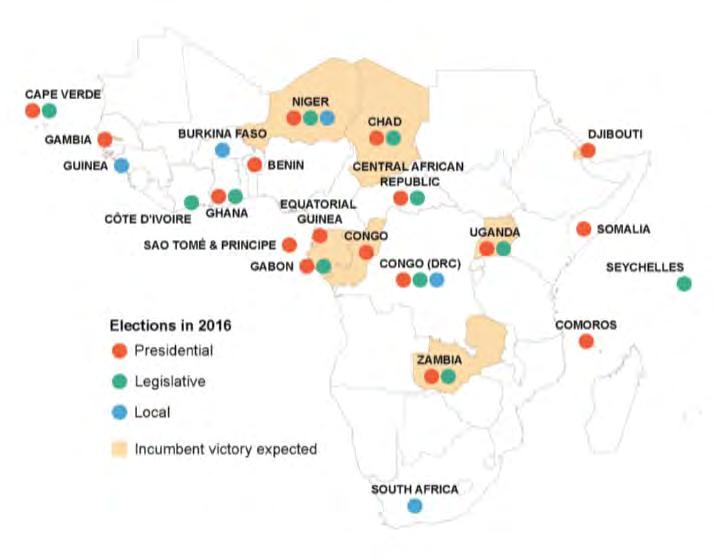

Political Risks and how to manage Grassroots mobilisation in October 2014 in Burkina Faso overthrew President Blaise Compaoré and thwarted a subsequent coup. In March 2015, people power in Nigeria authored a landmark opposition victory. It has also prompted protests from Kinshasa to Kampala against the strivings of long-serving presidents to maintain their grasp on power.

Popular pressure has laid low some establishment parties including the African National Congress (ANC) in South Africa and the People’s Democratic Party (PDP) in Nigeria. Each has fallen victim to power struggles or suffered factional breakaways as prominent party figures have sought to exploit social dissatisfaction to bring about radical change or further their own political ambitions.

False dawn

A total of 22 African countries will see elections in 2016 –17 presidential and 11 legislative polls. Still, we expect incumbent leaders and their parties to dominate electoral dynamics. The outbreak of popular energy will reach their limit.

markets in Africa, even in Burkina Faso and Nigeria, where the excitement generated by Compaoré’s overthrow and Muhammadu Buhari’s election victory will fade in 2016. Moreover, few other countries in Africa nurture the pre-conditions for change driven by the masses, either through the ballot or mass mobilisation.

Across the rest of the continent, social and historic factors are less likely to facilitate political change driven by the will of the masses. Central African countries including Gabon, Chad, and Equatorial Guinea will hold presidential elections in 2016 in which long-standing incumbents will almost certainly secure victories. The recent election in Uganda followed this pattern with the re-election (albeit contested) of President Yoweri Museveni. Some of these elections will be more competitive than in previous years, but they will not overturn the status quo.

Angola’s political system is under strain from worsening socio-economic conditions and rising tension over President Eduardo José dos Santos’s eventual succession. This will undoubtedly influence the tug-of-war within the ruling People’s Movement for the Liberation of Angola (MPLA) over the presidential succession. But there seems to be limited appetite and capability among the masses to challenge the MPLA’s supremacy, not least because of the repressive treatment of dissent and the absence of a credible political alternative.

Muted outlook

In southern Africa, the impact of people power will vary in scale and impact. The ANC’s political dominance will be severely tested in South Africa’s municipal elections, with a very real possibility that it loses its majority in a number of key urban centres. The party’s centre of influence has already been pulled towards its more populist extremes as it attempts to counter the rise in militant movements such as the Economic Freedom Fighters (EFF). A strong municipal election performance by such groups will have concerning implications for how the ANC responds to economic challenges, particularly regarding fiscal and labour policies.

In neighbouring Zimbabwe, the perceived weakness of the ruling Zimbabwe African National Union – Patriotic Front (ZANU-PF) is likely to prompt increasingly vocal opposition to the government. Infighting as factions manoeuvre to succeed the 92-year-old President Robert Mugabe, as well as the resulting neglect of a stagnating economy, has emboldened protests and enabled the possible emergence of Zimbabwe People First, a new party led by former vice president Joice Mujuru. These political battles have worrying consequences for business.

Managing the uncertainty is possible

People power, even if contained, sometimes might pose a challenge to business in the form of volatility around key dates such as elections and constitutional reviews. It can also threaten to alter élite power structures and influence policy. For companies operating in politicised sectors, an understanding of the stakeholder environment will be increasingly important to avoid potential interference or contractual instability –particularly when assessing the longer-term outlook. Rising accountability pressures will have a positive impact on long-term governance standards, but also create a more volatile political environment. Businesses will need to navigate this volatility with care to avoid being on the wrong side of a shifting political balance. One option is for companies to develop scenarios for those key markets within their global network that pose a high or extreme risk to their operations from a political perspective. This exercise tends to be most effective when using three scenarios – examples would be a “most likely” scenario, a “credible alternative” and an “outlier” scenario (very low likelihood but high impact). Using these scenarios as a platform, businesses can then identify political developments or “triggers” which increase or decrease the likelihood of a particular scenario taking place, and build in risk mitigation plans based on this model.

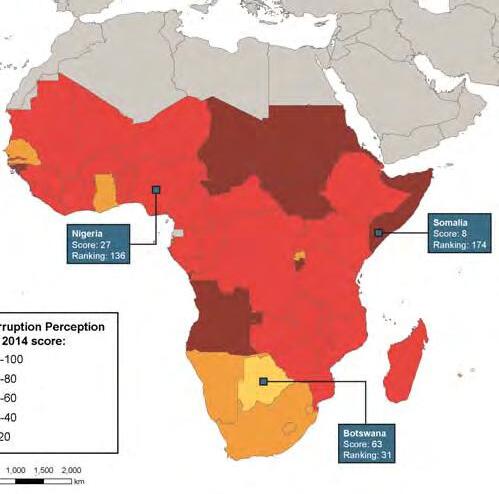

Corruption Risk

A change in government administration is one of the most potent sources of volatility in African markets. It usually represents a critical test of business resilience to sudden shifts in government policy. This is amplified at a time when anti-bribery and -corruption (ABC) enforcement continues to spread around the world and many African governments find themselves under pressure to join this trend.

No longer business as usual

In theory, a renewed political will to tackle corruption can reduce companies’ exposure to corruption. In practice,

however, it also heightens the risk of becoming ensnared in anti-corruption investigations of agreements signed by new and former government officials. Businesses that routinely flout local ABC laws will face higher risks of fines, reputational damage and potential jail terms for staff. Most African countries will remain high-risk jurisdictions through 2016, as vested interests often prevail, impunity persists, and governments fail to make the necessary investment.

Therefore, companies need to take critical steps to review their business operations. Companies should revisit their business strategy, goals and objectives to ensure they would be compatible with a more “compliant” environment and, therefore, have a sustainable business in the new evolving context. This exercise may well raise various questions about the business. For instance, are staff incentives that promote business development sufficiently balanced with incentives that promote compliant behaviour? Are ABC policies on paper actually practised in the field? Is there sufficient leader involvement and anti-corruption accountability?

A company’s reputation is a strategic issue that needs to be managed by its leadership. The tone from the top will naturally affect behaviour in the rest of the organisation. Such a review can be enhanced with an anti-corruption assessment of the business environment. It is important that companies understand the real risks they are likely to face and place these within the specific context of their operations. This should form the basis for developing or enhancing ABC policies and procedures.

Above all, there should be an emphasis on obtaining quality intelligence about activities within and outside the business. It is not uncommon for organisations with sound ABC programmes to find themselves caught out by the unethical actions of negligent staff or partners. This emphasises the need for effective communication lines within the business, as well as quality integrity due diligence programmes covering third parties.

The emergence of genuine local efforts to combat corruption is ultimately a positive story, especially when combined with the existing international enforcement actions of countries like the US and the UK. Removing the “corruption barrier” to business could go a long way towards further unlocking the continent’s vast economic potential. Africa’s leaders still have a lot to prove in this area but it is clear that their followers are running out of patience with “business as usual” practices. Companies should, therefore, take note of this impending change of direction and ensure they are properly aligned to capture the opportunities while managing the associated integrity risks.

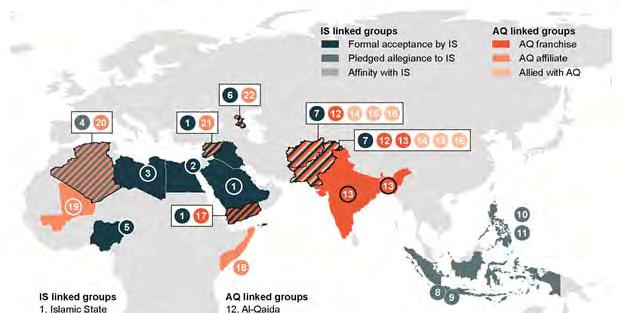

Terrorism and militancy

Terrorism and militancy remain primarily a threat in West and East Africa and tend to be overwhelmingly Islamist. In West Africa, al-Qaida’s shift towards high-impact attacks targeting foreign interests increases the threat facing coastal capitals and economic hubs located outside the Sahel region. Global competition among Islamist militant groups and the continuation of France’s

Operation Barkhane in the Sahel will encourage al-Qaida-linked groups to attempt attacks further from their northern Malian stronghold to demonstrate resilience and expanding reach.

Authorities across the region have realised the seriousness of the threat and are now implementing a

series of security measures designed to protect the most exposed public places. However, questions remain about how the top-level commitment demonstrated by the government and security force hierarchy will translate into rigorous and effective protection at the operational level.

The Nigerian militant Islamist group, Boko Haram, is increasingly likely to splinter in the face of military pressure. The group is likely to evolve into a regional threat, taking advantage of porous border areas and weak state authority around the Lake Chad basin. Although no longer in command of territory to the same extent as in early 2015, Boko Haram will continue to fuel insecurity in the region by combining terrorist and banditry tactics primarily targeting local civilians. It will present more limited threats to foreign businesses, which have few operations in these border areas.

The apparent terrorist attack on a passenger aircraft in Somalia in February could reflect militant fragmentation in Somalia. No group has yet claimed to have staged the attack. Al-Qaida affiliate al-Shabab has repeatedly attacked the heavily protected airport in Mogadishu, which hosts and is secured by African Union (AMISOM) forces, most recently in December 2015. Alternately, splinter factions aligned with rival group Islamic State (IS) and under attack from al-Shabab would have high intent to carry out a high-profile attack, in order to demonstrate resilience and gain supporters.

The threat to aviation assets across sub-Saharan Africa is prominent – the proliferation of anti-aircraft weapons from the Libyan conflict, many of which are believed to be in the hands of Islamist militants, raises the risk to civil aviation in Libya and the Sahel region.

For businesses operating in regions with a significant terrorist or militant threat, having the appropriate crisis and business continuity management structures in place

can do much to mitigate these threats. It is not possible to stop a terrorist incident from happening, but it is possible to build in sufficient organisational resilience to protect your employees and operations from the worst outcomes. Through diligent monitoring of the security environment, horizon scanning and use of incident mapping intelligence to plan movements and locate facilities, businesses can maximise awareness and ensure that crisis management and business continuity plans have the best conditions for successful implementation. A robust crisis management system has a business continuity focus, envisages possible scenarios and targets scenario planning to the ultimate goal of ensuring the survival of the business, its people and operations. This applies at all stages of a crisis, from the immediate security response to matters of operational continuity, insurance and external communications. If teams on the ground and management are aligned in their understanding of the threat and have a rehearsed, coordinated response strategy, businesses can be resilient enough to profit from the risk-reward relationship of complex operating environments.

Contributor Profiles

Claudine Fry, Associate Director, Global Risk Analysis. Claudine provides political and security risk analysis and writes daily analysis for the PRIME political risk service and online Country Risk Forecast, tracking political, economic and security developments across the region and updating clients on their implications for commercial activities. Claudine also produces bespoke consultancy reports. Projects have included security, corruption, political risk analysis and scenario-forecasting on Pakistan for clients in sectors such as manufacturing, oil and gas, defence and retail, as well as comprehensive threat analysis on India for clients in sectors including pharmaceuticals, defence, manufacturing, professional services and oil and gas. Prior to joining Control Risks, Claudine worked as an analyst at Oxford Analytica and at the Institute for War and Peace Reporting. Claudine holds a BA in War Studies and History from King’s College London.

Gbenga Abosede, Associate Director, Compliance, Forensics and Investigations and Technology. As the West Africa Practice Leader, Gbenga specialises in integrity due diligence and providing strategic advice on corruption-related matters and their effects on investment in the region. He has extensive experience delivering business intelligence, reputational due diligence and integrity risk consulting projects across a multitude of sectors, spanning oil and gas, mining, financial services, power , telecommunications and real estate. These services range from pre-transaction due diligence to employee background checks to assessments of corruption-preparedness and gap analysis. Gbenga holds an MBA from the Imperial College Business School and a Bachelor’s degree in Chemistry from the Imperial College London.

AFRICA’S LONGTERM GROWTH FUNDAMENTAL IS UNSHAKEN, AMIDST THE RECENT SLOW DOWN

ALISON KLEIN

Manager at FMO, overseeing private equity investments in Africa and Latin America.

Alison was previously an investment manager at AlpInvest Partners, responsible for private equity fund investments in Europe, Israel and selected emerging markets. Alison helped to design and deploy AlpInvest’s cleantech mandate and represented AlpInvest on the advisory committees of leading buyout and venture capital funds. She previously worked at The Boston Consulting Group, and began her career with both commercial and financial roles with Focus Ventures, USWeb / CKS, and Forrester Research. Alison has an MBA from INSEAD and an AB in Psychology from Harvard College.

CMinAfrica: Some analysts believe that Africa is at a tipping point and its growth story is fading out, what is your view on this?

Alison Klein: For some countries whose economies are highly dependent on commodity exports, the global slowdown, reduced demand from China and lower oil prices are having a substantial impact. At the same time, population growth and urbanization will continue to influence positive growth trajectories, while reduced income from commodities can be a stimulus for governments and the private sector to reduce reliance on these exports and accelerate development of other industries.

Murray Grant: After a long bull run Africa is certainly encountering stronger macroeconomic headwinds. In a historical context this is normal for any region. This does not mean that Africa is not going to grow. Far from it, just look at the demographic fundamentals and GDP per capita numbers.

CMinAfrica: What impact has the recent pessimism around African markets had on your investment portfolio?

Alison Klein: One of the advantages of investing in private equity is that you can time your entry and exits (to some extent). The most concrete impact of pessimism is in valuations, since local currencies can be hard hit by investor sentiment and we value our portfolio in Euros. Over time the currency effect together with a lower valuation environment should create a “buyer’s market” but this takes time to develop as sellers’ expectations tend to lag buyers’ willingness to pay.

Murray Grant: Valuations will adjust in the short term particularly when measured in USD terms. Longer term the growth opportunity will still win out.

CMinAfrica: Presently, which African countries appeal to you the most and why? Do any specific sectors and companies come to mind?

Alison Klein: While cautious in the very short term, we

MURRAY GRANT

Managing Director of CDC Group’s Africa Fund Murray subsequently spent 13 years at 3i in the UK before joining CDC Capital Partners in 2001. When Actis was spun out from CDC in 2004, he was one of the founding Partners of Actis with responsibility for the development of its Africa business and the Africa team.

Murray's investment and NED track record has covered most sectors and regions across Africa. He remains chairman of Vlisco, a pan West African branded fabric business.

Murray has a BSc (Hons) in Engineering from Edinburgh University and an MBA from London Business School.

remain optimistic about political and economic developments in Nigeria. We are actively looking at investment opportunities in the other two most populous countries: Egypt and Ethiopia, each with very different dynamics but where SME and midcap private equity opportunities are only starting to emerge. Beyond these, we continue to be active in the remainder of Africa as well, seeking to build a balanced portfolio of relatively proven and emerging fund managers, and an underlying portfolio of funds and co-investments which is diversified across the continent and sectors. In light of the key growth drivers highlighted above, we are seeing a preponderance of consumer-driven growth models from agribusiness, FMCG to banking and insurance across the continent.

Murray Grant: We tend not to think of country attractiveness at CDC. As an investor in companies over long term equity investment horizon the bit that matters is picking good quality businesses.

CMinAfrica: What is the biggest risk in Africa and how do you handle the risks such as recent currency swings and commodity slumps?

Alison Klein: The biggest challenges are finding quality management, aligning interests between investors and management, and finding fund managers with the right mix of investment acumen and African operating experience to select and manage a portfolio of high-growth companies in these very dynamic markets.

Murray Grant: To answer this question would be too simplistic. Macroeconomic factors such as political stability and currencies certainly matter. At the microeconomic level you cannot underestimate good management and good governance.

After a long bull run Africa is certainly encountering stronger macroeconomic headwinds. …. normal for any region.

EXPLORING INVESTMENT POTENTIALS IN ANGOLA & MOZAMBIQUE

The sharp drop in oil prices since mid-2014 has had a major impact on the Angolan economy. Real GDP growth is projected to have slowed to 2.9% in 2015 from 4.8% in the previous year. This is significantly lower than the average annual growth rate of 10.2% recorded during the decade of 2004-14 that made Angola one of the fastest growing economies in the world. The current slowdown in economic activity is attributable to a hard landing in the non-oil sector, which recorded the lowest growth rate since the end of the civil war (1.5% vs. 8.2% in 2014). The oil sector is projected to have expanded 6.3% (from a contraction of 2.6% in 2014). Overall, lower private consumption and public spending levels in an existing backdrop of more limited availability of foreign exchange in the local economy all led to a significant adjustment in the industry, construction and services sectors last year.

GDP Structure (2015E)

Source: Angolan authorities.

The Angolan authorities currently forecast a 4% growth rate for 2016. The oil sector is expected to advance 4.5% while the non-oil sector is projected to pick-up to 3.8%. Our real GDP growth assumption of 3.2% for 2016 is more conservative than the government’s forecast though. We believe further downside risks could emerge and continue to weigh on economic activity, namely persistently low oil prices and a slowdown in some of Angola’s main trading partners, particularly China.

Meanwhile, inflation has climbed back to double-digits in recent months, reflecting in large part the impact of the depreciation of the kwanza, which the BNA is trying to contain through tighter monetary policy measures. The central bank has used international reserves to defend the local currency and limit inflationary pressures, but has not prevented the kwanza from depreciating nearly 31% against the dollar in 2015 and a further 20% so far this year. It is worth noting that annual inflation had kept a downward trend in recent years and stayed in single-digits from mid-2012 until July 2015. However, it

has reached 20.26% in February of this year, its highest level recorded since January 2006. This recently led the Angolan authorities to revise upwards their 2016 inflation forecast to 15.8% from 11% in the 2016 budget.

Exchange Rate vs. Inflation

Source: BNA.

International Reserves vs. Exchange Rate

Source: BNA.

On the fiscal front, the government is aware that in the current low oil price environment it remains crucial to rationalize public expenditure levels and imperative to accelerate the efforts to increase non-oil related revenues. This starts with reducing the public wage bill to levels more consistent with a new revenue reality. Another area is the reform of fuel subsidies, which started in September 2014. The lower international oil prices together with the several domestic fuel price increases since the reform began have reportedly led to the elimination of subsidies on most fuels while the ones still subsidized are done at much lower levels than in the recent past. The plan is to reportedly eliminate fuel subsidies completely by 2020. At the same time, the local authorities aim to improve social assistance to the poor in order to lower the impact of the gradual elimination of fuel subsidies. Moreover, public investment projects need to be better prioritized and their execution more carefully monitored.

There are several sectors that are likely to be on top of the local authorities’ agenda going forward. The aim is to gradually diversify the economy away from the oil sector and reduce import levels. These are sectors that are likely to support real GDP growth in the future. However, the impact from these increased diversification efforts is going to take time to materialize.

First, agriculture is the second non-oil production sector and has resources that can make Angola one of the richest agricultural countries in Africa. Less than 10% of arable land is still exploited and very little of irrigation land is developed. Some of the country’s most successful crops include coffee, bananas, timber, tobacco and sunflowers. Angola’s climate is diverse and provides for the growth of both tropical and semi-tropical crops. The fishing sector has recently shown improvements but its full potential has yet to be realized.

Second, diamonds represent the lion’s share of Angola’s mining sector. The country also remains an extremely attractive target for the discovery and development of world class ore deposits such as iron, gold, copper, phosphate and even zinc. The government has created a new legislation for mining exploration and is assessing the best way possible to attract new investors into the sector.

Third, the post-war reconstruction boom and resettlement of displaced persons has led to high growth rates in the construction sector. Although the appetite for housing and large scale projects has recently slowed (in most part due to the fall in oil prices), it is worth noting that the expected strong population growth and increasing urbanization levels in the country should continue to support the expansion of the construction sector.

Fourth, the government remains committed to improving the country’s energy facilities, namely hydroelectric, in order to improve and expand its power generating capacity and network grid. Solar and wind power energies are also at an early stage of development.

Other areas of interest are likely to come in the manufacturing, retail and services sectors such as telecoms and banking where Angola still remains underdeveloped. And finally, it is worth highlighting the potential of the country’s tourism sector. The business segment is currently the main segment that visits Angola. However, there is still a long way to attract other types of tourists. Problems related to bureaucracy (visa requirements), lack of infrastructure, a weak focus on the visitor and no institutional marketing are critical for the development of the tourism sector of the country.

Mozambique’s long-term prospects remain upbeat

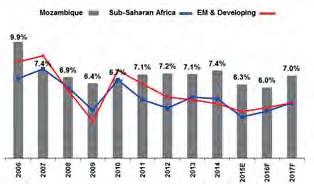

Mozambique’s latest GDP figures showed that economic activity in the country slowed to 5.6% YoY in the last three months of 2015 and that real GDP growth for the year stood at 6.3%, below the 7.4% in 2014 (which is near the average growth of the last decade). This

slowdown was mainly due to the sharp drop in commodity prices, namely aluminium and coal (the country’s main exports) and lower foreign direct investment (FDI) inflows. However, real GDP growth remained well ahead of the IMF’s latest 3.5% average growth projection for Sub-Saharan Africa in 2015.

Real GDP Growth

Sources: Mozambican authorities, IMF and Eaglestone Securities.

Inflation also picked up recently after recording a constant downward trend in recent years. Prices are expected to remain under pressure chiefly due to the sharp depreciation of the metical against other currencies like the US dollar and South African rand. Inflation is more than likely to remain above the official target of 5.6% this year.

The extractive industry has been responsible for a significant part of the FDI inflows in recent years (other inflows have gone to the transport, storage and communication sectors). Large investments have initially been made in the coal sector, but more recently attentions have turned to the vast natural gas reserves in the Rovuma basin, in the north of the country. This has boosted other sectors such as construction, utilities and real estate. Mozambique is nowadays a more diversified economy but remains highly dependent on the agriculture sector, which still accounts for nearly a third of its GDP.

Net Foreign Direct Investment (US$ million)

Sources: Mozambican authorities and IMF

Despite the recent slowdown in economic activity, the country’s long-term prospects remain upbeat as a result of the natural gas projects expected to come on stream later this decade. Local officials reportedly expect more

than US$ 30 billion will be invested initially in the sector, with the first exports of LNG due to start no sooner than in 2020. This is huge for a country whose GDP currently stands at more than half of that amount.

Real GDP growth could pick-up once again to nearly 8% in 2017-20 on the back of the anticipated investments in natural gas. The country is also expected to benefit from international loans like the ones recently agreed with the IMF (US$ 286 million over an 18-month period) to help bring some stability to the economy following the sharp drop in commodity prices and the European Union (US$ 740 million over the next five years) to support development projects.

Economic growth should also remain supported by the rehabilitation of the country’s transport infrastructures (roads, railways, ports and airports), which is a strategic priority for the local authorities. The development of hinterland corridors also serving neighbouring countries is critical for the future of Mozambique, providing easy access to the sea for mineral projects, agricultural projects and industry.

Other areas of interest include agriculture and fisheries. Mozambique provides strong potential in a variety of

crops, namely for the local market and export of cereals, fruits, flowers and vegetables. The Zambezi valley is a prime area for agriculture. Moreover, the country’s vast coastline is very rich, as Mozambique currently exports prawns and the sector is being developed through local and foreign investors.

Meanwhile, the potential for hydroelectric power plants is considerable and the need for a reliable power transmission infrastructure urges. Mozambique also has the potential to explore renewable energy (wind, solar and photovoltaic). It is a capital intensive sector, but with several investment opportunities.

The telecoms market is also underdeveloped with relatively low penetration levels while a significant part of the local population does not hold a bank account. Telecoms and banking are two sectors where foreign players remain quite interested and hold strategic positions.

Finally, we also highlight the strong potential in terms of tourism. The ongoing investments in infrastructure development will allow access to new locations with touristic potential, also benefiting from the country’s large coastline and natural parks.

FASTMOVING CONSUMER GOODS CHALLENGES AND OPPORTUNITIES IN AFRICA

Virusha Subban and Yonatan Sher, Bowman Gilfillan Africa Group

Africa represents a large and growing opportunity for fast-moving consumer goods companies and retailers with the rapid expansion of Africa’s consumer class. At an average 5% growth, African countries’ booming consumer demand outspans the developing world.

The average GDP per capita in Africa over the last five years has grown by over 11%. According to a report by McKinsey, GDP per capita is the single most important driver of global growth in the consumption of fast-moving consumer goods, and Africa’s consumer-facing industries are expected to grow by more than $400 million by 2020.

While the potential of the African market is very real, there remain many challenges for FMCGs and trade in general on the continent. It is mainly incoming multinationals that are maximising the potential of African markets. African countries and companies are largely missing out on the consumer boom on their proverbial stoep.

According to UN statistics published in the report “Economic Development in Africa Report 2013 –Intra-African Trade: Unlocking Private Sector Dynamism”, the average African country exports just over 10% of its total merchandise within the continent, this is compared to 50% in developing Asia, 21% in Latin America and the Caribbean and 70% in Europe over the same period.

This problem is compounded by regulations imposed across the spectrum of African jurisdictions that actively inhibit regional trade. In a recent speech delivered at the World Trade Organisation round table in Nairobi, Senior Director of the World Bank Group Global Practice on Trade and Competitiveness, Anabel Gonzalez, stated that while regional trade integration has long been a strategic objective for Africa, and despite some success in eliminating tariffs within regional communities, the African market remains highly fragmented. A range of non-tariff and regulatory barriers still raise transaction costs and limit the movement of goods, services, people and capital across borders throughout Africa. She bemoaned the fact that barriers to trade continue to limit the growth of trade throughout all African regional groupings. By imposing unnecessary costs on exporters these barriers raise prices for consumers, undermine the predictability of the trade regime, and reduce investment in the region.

The nascent Tripartite Free Trade Area Agreement which

has been on the cards since 2008, and the AU dream of an eventual Continental Free Trade Area, promises some hope for an up-tick in intra-Africa trad. So far, however, African leaders have been dragging their feet, with only 16 out of 26 countries having signed the Tripartite Free Trade Area Agreement and none having ratified it.

Another risk for the growth of the FMCG industry is that many African customs authorities, such as SARS in South Africa, are increasing the use of risk profiling procedures in order to speed up time delays at borders and merchants in the FMCG industries have been earmarked as being high risk from a customs and trade perspective.

In mid-2015, SARS issued a stern warning to the FMCG industry after identifying extensive non-compliance within the formal and informal cash merchants’ environment. SARS uncovered many forms of non-compliant behaviour, such as customs fraud; the illicit expatriation of funds off-shore; and VAT fraud, including the claiming of undue VAT refunds; and so called ‘Ghost Exports’. SARS has further identified the involvement of organised syndicates with sophisticated organisational structures that further this non-compliant behaviour.

What this means from a trade and customs perspective is that the turn-around times of cross border trade of FMCGs may be significantly slower than other trade, considering the new and ever more sophisticated risk profiling systems being rolled out at the borders in South Africa and other African countries.

It is mainly incoming multinationals that are maximising the potential of African markets. African countries and companies are largely missing out on the consumer boom on their proverbial stoep

AFRICAN CURRENCIES: ECONOMIC CHALLENGES AND OPPORTUNITIES

Prasad Dalavai and Vinesh Caumul, Bourse Africa Limited.

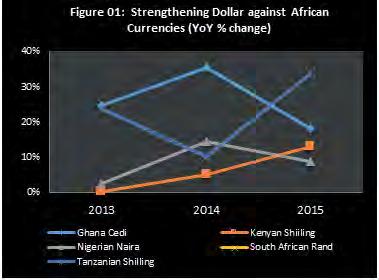

Concerns about China’s economy, worries about the US Federal Reserve interest rate policy, nervousness about the impact of negative interest rates on banks, and worries about drop in prices of commodities such as crude oil and base metals make a toxic mix for any emerging economies. As a result many emerging market currencies are falling as investors move their money from emerging countries’ financial markets (Table 1). Even African currencies are not completely insulated from the toxic mix. In Africa, the early effects of a stronger dollar have been extensive (figure 01). From Ghana and Nigeria in the west

Table 1: Emerging Markets Currencies against

(YoY)

* - Considered data as of 19 February in 2016 Source: Bloomberg

to Kenya in the east and South Africa in the south, currencies have all fallen against the dollar.

Why African currencies are weakening?

African currencies are tumbling amid a rout in commodities, slowing Chinese economy and the prospect of higher interest rates in the US. Things took a turn for the worse in mid-2014 when prices of crude oil and minerals, the export mainstay of many African economies, plunged largely due to a sharp slowdown in one of the biggest consuming countries, China.

Falling Commodity Prices

Although price decline of major commodities such as crude oil and base metals has been less precipitous than during the global financial crisis in 2008-09, it could be worse for commodity dependent African countries since state finances have failed to recover from the last turmoil. In Africa, plunging crude oil prices (Table 2) have hit hard major oil exporters such as Nigeria and Angola while lower oil have hit oil exporting countries across the globe. Since lower oil prices typically result in depreciation of the oil exporters’ currencies, the dramatic plunge of oil prices has severe implications for the oil exporting countries. This conveys that Africa should not become overly reliant on commodities.

Source: Bloomberg

Looming Fed Interest Rate Hike

Last year, African currencies woe were compounded by speculations over a possible interest rate hike by the Fed in over ten years that made the dollar strengthen globally. The Fed finally increased rates in December for the first time in nearly a decade, strengthening the dollar even further. This accelerated a flow of funds out of frontier markets as investors anticipated a further hike in U.S. interest rates later this year.

Amidst falling currencies, African countries provide certain opportunities and challenges.

What are the challenges?

Many African economies are struggling to cope with falling commodity prices and a slump in investor confidence.

Growing Current Account Deficit

The transmission of the commodity price shock will be felt through the current account. The lower crude oil prices will reduce export earnings of oil exporters and put pressure on the current account balance and the exchange rate. However, lower oil prices will reduce pressure on the current account of oil importers. Most of Africa’s economies, beyond commodities, import more than they export. This has meant that the region tends to have significant current account deficits with falling local currencies. The International Monetary Fund (IMF) stated that many African economies current account deficit has remained at a very high level of GDP.

Falling Forex Reserves Reserves are shrinking for many African countries amid

falling exports (Table 3). With foreign-exchange reserves of less than a tenth of the emerging-market average, sub-Sahara African countries increasingly find it difficult to stop their currencies from plummeting. Nigeria saw its foreign exchange holdings plunge around 20 percent in 2015 thereby forcing trading restriction.

Source: The World Bank and Trading Economics

Impacts on FDI

Note: For 2015, in the case of Ghana & Kenya, the data was till September & October res[ectively.

Source: The World Bank and Trading Economics

Cost of Imports to go up

As the dollar strengthens, all dollar-denominated goods and commodities imported become expensive. For importers of energy products denominated in dollars, when the domestic currency weakens against the dollar, energy products such as petrol become more expensive. In South Africa, with a weaker rand, maize and wheat imports, which are more than half of its domestic wheat and maize production, become expensive.

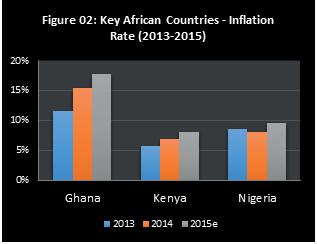

Spiraling Inflation

Higher import costs due to weakening local currency will lead to a higher inflation and eventual higher interest rates (figure 02). In Angola, the central bank of the country raised interest rates as a big drop in Angola’s kwanza pushed inflation to almost a three year high.

Note: For 2015, its estimated figures

Source: The World Bank and Trading Economics

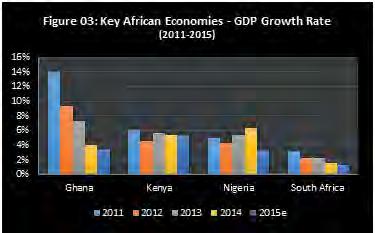

Slump in GDP

Growth in sub-Saharan Africa has weakened after more than a decade of solid growth (figure 03). Africa, home to a third of the world’s mineral reserves and a tenth of global oil reserves, particularly dependent on revenues from commodity exports, is worst hit. In fact, IMF estimated average sub-Saharan economic growth of 4.4 percent for 2015, down from the 5.8 percent forecast in 2014.

For investors, good business performance could be illusory with significant currency depreciation. Hence, depreciation of local currencies may discourage foreign investors’ new investment. According to UNCTAD publication ‘Global Investment Trends Monitor’, foreign direct investment (FDI) inflows to Africa fell by 31 percent (YoY) in 2015 to an estimated US$38 billion, largely due to a decline of FDI in Sub-Saharan Africa. Any curtailment in foreign capital inflows could seriously affect growth and poverty reduction in Africa. Hence, a reversal of or slowdown in these flows from foreign investors is the last thing the continent needs.

What are the opportunities?

Africa known for its abundance and opportunity is attracting increasing interest from the international financial community. Amidst weakening currencies, African countries still provide certain opportunities.

Inexpensive Investments

The search for returns has led foreign investors to the African continent. The fall in commodity prices that has seen most African currencies fall against the dollar presented an investment opportunity for foreign investors. Hence, fund managers and investors should look out for opportunities for inexpensive investments on the continent.

Benefit for Importers

Not all African countries are equally affected by weaker commodity prices. Of course, plunging crude oil prices are not bad to all African economies. In effect, oil importers like South Africa, Tanzania and Kenya will be the perceived winners. However, the overall risks to the continent’s economic outlook are currently tilted towards negative due to falling commodity prices.

Exports become more Competitive

In today’s integrated global economy, where international trade is a necessity, exchange rates can enhance or diminish a country’s competitiveness and make investments in the country more or less attractive. No doubt, a weaker exchange rate will make exports more competitive. However, it will also make it more expensive for countries to service their external debt.

Table 3: FOREX Reserves of Key African Countries

Contributors’ Profile

Year Nigeria - Naira South AfricaRand Ghana - Cedi KenyaShilling Tanzania - Shilling

2013 5.70% 13.69% 7.48% 4.43% 5.06%

2014 10.71% 11.28% 24.92% 2.73% 6.71%

2015 9.15% 15.60% 24.75% 4.77% 23.59%

Source: Bloomberg

Structural and Market Reforms

Government spending and policy initiatives will have an impact on the direction of a currency. For instance, effective import policies promote import substitution that will lead to current account surpluses resulting in currency appreciation over a period of time. Most of the markets in the continent lack transparent forex and commodity markets. Many African currencies witnessed high volatility last year due to global economic uncertainty (Table 4). Establishing a vibrant futures market provides a transparent hedging platform for all the stakeholders who wither currency and commodity price volatility.

What is the way forward?

The way forward, and to sustain rapid growth the region will need to move away from being commodity dependent economies by increasing export sophistication and integrating into global value chains. For this, Africa needs to set aside its intra-continental differences and bring-in necessary economic reforms in order to maximize the opportunities available from growing foreign interest.

Dalavai G. Prasad, Senior Manager, Bourse Africa Ltd. Mr. Prasad is a well-known personality in economic research, commodity market, derivatives markets, economic policies and trade issues. Mr. Prasad, who is Masters in Economics (MA) and Management (MBA), had many publications related to commodities and financial derivatives market. Several of his write-ups received international acclaim.

Vinesh Caumul, Asst. Manager, Bourse Africa Ltd. Vinesh Caumul is an expert in financial arena with over 8 years experience in Market Surveillance, Valuation & Risk Management of Exchange Traded Derivatives, Management of the Exchange Trading Platforms, Capital Market Regulatory Framework and Complex Statistical Analysis. He holds Masters in Applied Financial Statistics from University of Mauritius and did his graduation in Statistics, Mathematics and Computer Science from Bangalore University, India.

References

1. “Global Investment Trends Monitor”, UNCTAD publication, 20 January 2016

2. “Regional Economic Outlook: Sub-Saharan Africa - Dealing with the Gathering Clouds”, IMF world economic and financial surveys, October 2015.

3. “Africa's currency markets face major slump” by Nye Longman, August 13, 2015.

4. “On the Adequacy of Monetary Arrangements in Sub-Saharan Africa” by Agnès Bénassy-Quéré and Maylis Coupet, March 14, 2005.

5. “Oil, Toil and Trouble”, The World Bank, February 16, 2016