Western Growers Assurance Trust is now Western Growers Health.

A new day is dawning at Western Growers Assurance Trust, and we’re excited to announce that we are now Western Growers Health!

This evolution reflects our dedication to innovation and our unwavering commitment to serving the agricultural community with excellence.

While our look may be new, our mission remains the same: delivering tailored, innovative healthcare solutions that meet the unique needs of the ag industry.

To learn more, visit wg-health.com.

Prepping For Medicare

July is a great issue, and we enjoy the many article contributions all centered on Medicare. Our next special issue is Group/Employee Benefits and will be the September issue. We appreciate our new advertisers, and we look forward to working with new advertisers and hope each of our subscribers give our advertisers a long look to do business with them in the future. Finally we welcome your client success stories too.

Prepping for Medicare AEP and Employer Open Enrollment

AEP last year was filled with changes, especially last-minute changes. With Wellcare PDP forcing major adjustments made on the fly with PDP clients during AEP many brokers “lost” commission income. To prepare for this year, take a look at Elliott Martin's article. Last AEP, the Martin Agency had success using video to educate clients to self-serve in many cases. The thought this AEP we are hearing from the street is how educating clients to self-direct through the process to get PDP quotes, when possible, can save time. Prerecorded videos made available via email, live Zoom client meetings, and then placed on an agency website seem to be options to get the client work done while using tech to save everyone time. Carrier changes with local marketplace provider changes is something to keep an eye on for all clients. Providers dropping plans due to "cost management” seems to be a real option as looming concerns rise up again. Providers are facing possible cuts to MediCal and an increase in the number of uninsured people landing in the emergency rooms. The response last year was providers either moving hard into managed care plans or hard away from MAPD. Add to this the MediCal trend how some medical groups in rural areas often make changes due to carrier contracting disagreements toward

year end, and this AEP could be a rough ride for brokers. Keep an eye on Med Supp carriers as both increases in premiums and reductions in commissions are being used by carriers to cover their costs.

Focusing on New Business

With many ways to grow your Medicare book, focus first on what your FMO can provide. Then, if you want to find how other FMOs focus on new business look at two articles which offer solutions to grow new business. First Sierra's and Financial Grade's articles on this topic provide tips and valuable tools to add new business. These two FMOs know how to grow new business. While each has unique tools they share in the commitment to their new business model which is focused on how to help brokers with personal support to either enter the Medicare business or grow more business with advanced technology and other tools.

More ways to grow new business can be found in the article covering books of business acquisition, and the outline on how to work with a team of planning experts to grow clients in the future by protecting another broker’s commissions as the Successor - Buyer. Also, for existing clients, read how to find ways to identify problems you can resolve. Most common needs for Medicare clients is to address the cost of long-term care as well as finding a Dental plan with the largest provider network in the US and a $10,000 annual max. You can find these ideas covered in the articles by Marc Glickman, CEO of Buddy Insurance and Sam Melamed, CEO of NCD dental plans.

Hope you all enjoy the summer months and we will see you at the Medicare Summitt in September.

5

PUBLISHER'S NOTE

Prepping For Medicare

TABLE of CONTENTS

AEP last year was filled with changes, especially last-minute changes. With Wellcare PDP forcing major adjustments made on the fly with PDP clients during AEP many brokers worked free and “lost” commission income. To prepare for this year, take a look at Elliott Martin's article. Last AEP The Martin Agency had success with using video to educate clients to self-serve in many cases.

By Phil Calhoun

18

CALIFORNIA POSITIVE

Exploring California Mountain Trips In The Summer Visiting California’s numerous mountains allows visitors to see several natural wonders in one park or area, with plenty of things to see and healthy activities to do. As your clients start making their summer vacation plans, here are a few spots in California that offer mountainous adventures.

By CalBroker Magazine

20

MEDICARE

California’s Aging Population - PART 2

As the baby boom generation ages, California’s older adult population is increasing significantly. Because of advances in health care and improved living conditions, people are living longer, but they are also living through more disabled years.

By

Hans Johnson, Eric McGhee, Paulette Cha, and Shannon McConville, with research support from Shalini Mustala

22

MEDICARE SUPPLEMENT PLANS

Medicare Supplement Plans - The Ins and Outs

For many agents who sell Medicare products, there’s a high likelihood Medicare Supplement products are available in their offerings to clients. But, for those who have not considered selling Medicare Supplement plans, we’ll provide an overview of the products. And, for those of you who do offer Medicare Supplements to your clients, we’ll also discuss some more detailed information you may not have thought about or considered.

By David Ethington

24

ANCILLARY INDIVIDUAL BENEFITS

Insurance Innovation: The NCD Story

In a recent interview, Phil Calhoun—representing California Broker Media with 250,000 California-licensed subscribers—sat down with Sam Melamed, the CEO of NCD, to discuss the company’s mission, product offerings, and the unique value it brings to brokers and clients nationwide.

Via Interview with Sam Melamed CEO of NCD by Phil Calhoun

26

SCAN HEALTH PLAN

Winter Is Coming For California’s Health Insurance Brokers

For brokers measuring their sales numbers, the signs of a decline are evident. Make no mistake: we are entering a bear market. But how can brokers navigate and succeed in this challenging environment? It’s time to rethink our approach to enrollment.

By Michael Blea

28

BUILDING YOUR MEDICARE AGENCY

Playbook: Navigating California’s Evolving Market

In this interview with Phil Calhoun of California Broker Magazine, Pete Blasi, CEO of Financial Grade, shares how he’s helped brokers succeed in the Medicare market for over 20 years. He highlights the importance of education, systems, and client retention strategies to grow and sustain a thriving Medicare business.

Via Interview with Pete Blasi CEO of Financial Grade by Phil Calhoun

30

MEDICARE ADVANTAGE

Best Medicare Advantage Plans In California 2025 Medicare Advantage plans offer more benefits than Original Medicare, and they're often cheaper than paying for Medicare and a Medicare Supplement plan. However, they offer less flexibility since you’ll need to get care from within the plan’s network of providers. Weigh your options to determine what plan best suits your needs.

By Kate Ashford

32

TECHNOLOGY & MEDICARE

Adapting To The New Normal

In the past, re-shopping a client's Part D plan could be a 20- to 45-minute task. Multiply that across hundreds of clients, and it quickly becomes a full-time seasonal job. While we have never entered this field solely for commissions, we also can't ignore the economic reality: it's increasingly difficult to remain profitable servicing a product that doesn't pay.

By Elliott Martin

34

TECHNOLOGY IN MEDICARE

Empowering Medicare Agents Through Technology

Technology is reshaping the Medicare marketplace, drawing on insights from Amanda Hargis of First Sierra. It covers the evolution from paper-based to digital processes, the impact of electronic platforms and AI on agent workflows, changing client expectations, the need for younger agents, and the future of technology in the industry.

By Amanda Hargis

MEDICARE SUPPLEMENTS

Tips & Thoughts About Our Medicare Supplement Market

Many agents today are primarily selling the Medicare Advantage plans and are hesitant to present the Medicare Supplement plans. They are missing a great opportunity for almost half of the Medicare sales in California.

By Margaret Stedt

38

HEALTH & WELLNESS

Your Summer Wellness Guide

Being proactive about our health and making some intentional choices now can help fuel a summer that supports energy, mobility, cognition, stress resiliency and overall vitality. Here are some easy to implement tips for a healthy summer, all based on the wholeperson wellness strategies that we teach every day at St. Jude Wellness Center.

By Megan Wroe

40 MARKETING

Use This Pre-Appointment Routine For More Referral Results

Almost every athlete has a pre-game routine that puts them in the right mental and physical state for the competition. What about you? What is your pre-appointment routine?

By Bill Cates

42 PROFESSIONAL DEVELOPMENT

Letters On Integrity Inspiring Ethical Excellence

Who becomes the face and voice of integrity at home, at work, and in the community? Courageous ones do. They are everyday heroes who face conflicts yet triumph with choices and actions that are viewed by others as serving a greater good.

By Russ Williams

44 LTCI

Annuity Hybrid With LTCi Extension

With the increasing popularity of annuity hybrids paired with LTCi extensions, a modern approach to long-term care planning emerges. This solution blends flexibility, tax advantages, and accessibility. Read on to learn why these innovative products are transforming long-term care planning for clients over 65.

By Marc Glickman

46

SUCCESSION PLANNING

Crafting A Powerful Succession Plan

Have you ever had a client look you in the eye and ask, “What happens to me if something happens to you?” Or gently wonder aloud, “Are you ever going to retire?” These are questions that can take any advisor by surprise—but ones that underscore the heart of succession planning. Whether retirement is on the horizon or far off, the time to prepare is now.

By Dr. Daralee Barbera

48 COMMISSION PLANNING

How To Be A Successor – Buyer

Of Commissions

In a recent webinar, Phil Calhoun and David Ethington delved into their proven "Preferred Successor - Buyer" program, designed to help active brokers protect, grow, and eventually sell their health insurance commissions by finding a broker designated as a Successor – Buyer who is part of a team of planning professionals. This article explains how the commission planning process works, the shocking number of health brokers in need of planning, strategies, and a method to help active brokers work with younger brokers to solve the risk of loss when no health insurance commission protection plan is in place. Brokers deserve to secure their legacy, this planning work will protect commissions and help the industry.

By Phil Calhoun and David Ethington

PUBLISHER Phil Calhoun health Broker PuBlishing, llC publisher@calbrokermag.com

PRODUCTION DIRECTOR Zulma maZariegos Zulma@calbrokermag.com

Carmen PonCe Carmen@calbrokermag.com

Peter koZlowski Peter@calbrokermag.com

Zulma@calbrokermag.com

250,000 subscribers 14,000 monthly website visits

health Broker PuBlishing 14771 Plaza Drive Suite C Tustin, CA 92780 714-664-0311 publisher@calbrokermag.com

Print Issue: U.S.: $30/issue

Send change of address notification at least 20 days prior to effective date; include old/new address to:

This information provides an over view on how Medicare sign-up is evolving and what to expect in the near future.

1.

Digital Modernization & AI Integration

• Modernized enrollment systems: CMS is replacing outdated contractor-based systems (like PECOS) with modern in-house, cloud-based platforms for provider and patient enrollment—aiming for faster, smoother processing and better data accuracy. kiplinger.com medtechintelligence.com explore-medicare.org

• AI-enhanced plan selection: Payers and brokers are increasingly using AI to streamline Medicare Advantage enrollment. These tools automate verification, data tracking, and error resolution, and are designed to lead to faster processing and fewer mistakes.

2. Simplified Forms & Structured Data Collection

• Updated enrollment forms: Starting January 1, 2026, CMS is removing voluntary demographic questions (e.g., race, ethnicity, gender identity) from Medicare Advantage (MA) and Part D forms - making enrollment cleaner and easier to navigate cms.gov.

• Clearer guidance: CMS has updated the MA/Part D Enrollment and Disenrollment Guidance - simplifying language, reducing redundancy, and including visuals like graphics and tables to help beneficiaries understand their options. icf.com cms.gov

3. Improved Timeliness and Accessibility

• Faster coverage start: Final rules already allow coverage to begin the month after enrollment, helping close coverage gaps thanks to earlier legislative updates. investopedia.com kff.org

• Expanded Special Enrollment Periods (SEPs): CMS has added or clarified SEPs—such as for dualeligible individuals or after major life events - enabling more flexibility to enroll outside traditional periods.

4. Financial Flexibility with Prescription Drug Costs

• Prescription Payment Plan: As of 2025, beneficiaries can opt for predictable monthly copayments for Part D rather than facing large lump sums - CMS aims in 2026 to offer automatic renewals and explore real-time enrollment over web or phone. natlawreview.com kffhealthnews.org

• Cap on Out-of-Pocket Drug Costs: Starting January 2025, Part D plans will cap beneficiary drug spending at $2,000 annually—helping simplify enrollment decisions and financial planning. apnews.com panfoundation.org investopedia.com

5. Future CMS Proposals (CY 2026 & Beyond)

• AI “guardrails”: For CY 2026, CMS is refining policies around AI in enrollment and plan administration—promoting transparency, equity, and fairness when adopting tech solutions natlawreview.com+1cms.gov+1.

• Coverage Expansion: CMS's proposed rule may add new optional benefits (e.g., weight-loss drugs, broader insulin types), which could influence enrollment materials and selection processes.

How Medicare Sign-Up Is Evolving continued

What This Means for You

Opportunity Benefit

Faster, smoother enrollment

More flexible options

Clearer, more equitable processes

Transparent drug costs

Better informed decisions

What You Can Do Now

Digital platforms and streamlined forms reduce delays and confusion.

Plain-language forms and AI oversight aim to reduce bias and errors.

Annual caps and spread-out payments make costs predictable at sign-up.

Enhanced guidance helps beneficiaries navigate choices with clarity.

• Stay informed: Watch CMS updates, especially for the January 1, 2026 form changes.

• Embrace AI tools: If you're a broker or payer, consider investing in AI-driven enrollment platforms.

• Educate clients: Help them understand new payment options, SEPs, and enrollment flexibility.

• Prepare for new benefits: Monitor upcoming optional coverage options that may affect plan offerings.

In Summary

The future of Medicare enrollment is becoming faster, clearer, more flexible, and tech-driven. Beneficiaries and professionals alike should prepare for smoother processes, smarter planning tools, and expanding benefits. These improvements will help ensure that signing up for Medicare is no longer a bureaucratic burden, but an empowering step toward better healthcare access.

The Medicare Advantage market is undergoing a period of correction after rapid growth in the early part of the decade. Last year showed the first signs of a tempering of this growth, and the cooldown continued into this year.

Prior to the annual enrollment period (AEP), many for-profits signaled their intent to slow growth or even contract membership in response to a “perfect storm” of pressures—including rising utilization, lower-than-expected rate increases, and increased regulatory scrutiny around key financial levers. AEP results show a variety of health plans were beneficiaries of the resulting displaced enrollment.

READ FULL ARTICLE →

Medicare Advantage and Medicare Prescription Drug Programs to Remain Stable as CMS Implements Improvements to the Programs in 2025: Medicare Part D

Today, the Centers for Medicare & Medicaid Services (CMS) announced that average premiums, benefits, and plan choices for Medicare Advantage (MA) and the Medicare Part D prescription drug program will remain stable in 2025. Average premiums are projected to decline in both the MA and Part D programs from 2024 to 2025. Enhancements adopted in the 2025 MA and Part D Final Rule, as well as payment policy updates in the 2025 MA and Part D Rate Announcement, support this stability and increase enrollee protections and access to care for people with Medicare. In addition, the Inflation Reduction Act is reducing prescription drug costs and delivering more comprehensive benefits than ever before, including an annual $2,000 cap on out-of-pocket drug costs. CMS is committed to ensuring these programs work for people with Medicare, that they have access to strong and stable choices, and that they have the information they need to make informed choices about what is best for them. READ FULL ARTICLE →

Medicare Is A Target As Senate GOP Faces Megabill Math Issues

By Jordain Carney, Meredith Lee Hill and Robert King

Republicans have so far kept hands off the politically sensitive program. But senators are now desperate to find additional spending cuts. Senate Republicans are eyeing possible Medicare provisions to help offset the cost of their megabill as they try to appease budget hawks who want more spending cuts embedded in the legislation.

Making changes to Medicare, the federal health insurance program primarily serving seniors, would be a political long shot: It would face fierce backlash from some corners of the Senate GOP, not to mention across the Capitol, where Medicare proposals were previously floated but didn’t gain traction.

But Senate Republicans are now seriously considering it as they race to pass their party-line tax and spending package before a self-imposed July 4 deadline. The idea came up in closed-door meetings this week and, crucially, some Republicans believe President Donald Trump is on board with touching the program as long as it’s limited to “waste, fraud and abuse.”

READ FULL ARTICLE →

Seeing The Bigger Picture: How Payers & Providers Can Find Common Ground In Medicare Advantage: Both Health Systems & Health Plans Face Pressures Like Never Before

In the past year, a growing chorus of disputes has risen between health systems and Medicare Advantage (MA) plans. So far this year, 15 health systems have finalized terminations with MA plans.1 These disputes have ranged from health systems ending a single plan’s MA contract to terminating the entire portfolio of MA contracts. While conflict between payers and providers is hardly novel, the volume is telling and, we believe, a product of a confluence of compounding pressures currently facing both health systems and health plans.

MA plans are facing mounting headwinds to their core business: Rising medical costs driven by increasing utilization are outpacing reimbursement rate increases.

READ FULL ARTICLE →

Medicaid Cuts Ahead: How the Big Beautiful Bill Impacts Care

By Jared Dashevsky, MD

IMedicaid Cuts Ahead: How the Big Beautiful Bill Impacts Care

A patient with COPD misses a few appointments. She runs out of her inhaler. She ends up in the emergency department—again. Why? She lost her Medicaid coverage because she didn’t report 80 hours of work online.

That kind of story could become a lot more common. On May 22, Congress approved the “Big Beautiful Bill,” a $1.7 trillion federal spending cut. Nearly half of those cuts target public health insurance—specifically Medicaid and ACA Marketplaces. In this article, I’ll break down what the bill actually says about insurance, how much it cuts, and what it could mean for patients, physicians, and the hospitals we work in.

The Deets: The Big Beautiful Bill

On May 22, Congress approved the “Big Beautiful Bill” aiming to shave $1.7 trillion off federal spending. Nearly half of that comes from changes to Medicaid and the ACA Marketplaces. According to the CBO, those insurance tweaks alone should save about $793 billion over ten years. READ FULL ARTICLE →

CMS Updates Hospital Price Transparency Guidance Following Executive Order

By Andrew Cass

CMS updated its hospital price transparency guidance May 22, requiring hospitals to post the actual prices of items and services, not estimates. The update comes after President Donald Trump issued an executive order Feb. 25 aimed at boosting healthcare price transparency.

In the updated guidance, CMS said hospitals must display payer-specific standard charges as dollar amounts in their machine-readable files (MRFs) whenever calculable. This includes the amount negotiated for the item or service, the base rate negotiated for a service package and a dollar amount if the standard charge is based on a percentage of a known fee schedule.

CMS also said hospitals should discontinue encoding “999999999” (nine 9s) in the estimated allowed amount data element within the MRF, and instead encode an actual dollar amount.

CMS said it is aware there are “infrequent scenarios” where a hospital has limited historical claims data to derive the estimated allowed amount, such as when a hospital has just negotiated contracts with new payers. In the past, CMS recommended that hospitals encode nine 9s in the data value to indicate there is not sufficient reimbursement history. But after reviewing the MRF files of 68 large hospitals, CMS determined that hospitals are employing the workaround “much more frequently than expected.”

READ FULL ARTICLE →

Medicare Advantage Health Plan Outlook For 2026: Annual Survey Of Health Plan Executives

In this annual survey, health plan leaders share their perspectives on the state of the Medicare Advantage (MA) market, the outlook for the next 5 years, and strategic priorities for the year ahead.

The MA market has faced significant disruption over the last few years (e.g., rising medical cost/utilization, Stars headwinds, risk adjustment model changes, and now regulatory uncertainty)—all of which has influenced priorities. MA leaders are focused on weathering the storm and navigating the disruption. Signs indicate that the forecast is becoming more favorable, and leaders are striking a more optimistic tone for the upcoming year, with increased focus on cost control and financial sustainability.

Leaders also realize they still have to position themselves to take advantage of the future growth opportunity. We offer five core actions for health plans to lay the foundation for future growth.

READ FULL ARTICLE →

Oz Hints At Impending CMS Rule To Force Drug Price Transparency

The Trump administration hopes to issue a rule this year empowering regulators to “very forcefully” go after companies that don’t share information on drug costs, the CMS administrator said Tuesday. The CMS could issue a rule this year requiring healthcare companies to share more information on drug costs, as the Trump administration continues to push for more price transparency in the sector, Administrator Dr. Mehmet Oz said Tuesday.

“If we can do this in an effective way — and we’ll have a rule on this by the end of the year, we hope — then we’ll be able to very forcefully go after folks who are not transparently sharing what it actually costs, or what the transaction prices were, for the drugs that Americans are trying to pick up,” Oz said.

READ FULL ARTICLE →

Getting Care In A Disaster Or Emergency

Being prepared for a natural disaster is crucial to protecting your safety and well-being. Visit Medicare.gov/ emergency to learn how to get the care you may need if an emergency is declared and you have to evacuate to a safe area. Getting your prescription drugs during a disaster or emergency: You can move most prescriptions to another nearby in-network pharmacy, and back to your regular pharmacy when the emergency or disaster ends. Contact your Medicare drug plan if you need to use an out-of-network pharmacy. Seeing a doctor during a disaster or emergency: If you have Original Medicare, you can always see any doctor who accepts Medicare. If you have a Medicare Advantage Plan or other Medicare health plan, contact your health plan about making temporary changes, like using an out-of-network doctor during an emergency or disaster.

Learn more about accessing critical care (like cancer treatments or dialysis) or repairing or replacing equipment (like wheelchairs or walkers that were damaged or lost during a disaster or emergency).

Sincerely,

The Medicare Team.

READ FULL ARTICLE →

New Analysis Rebuts MedPAC’s Claims about Medicare Advantage

Advisory Commission’s (MedPAC) approach and data, calling into question MedPAC’s findings both of so led “favorable selection” into MA and of

Key methodological flaws in MedPAC’s analysis were detailed in a recent report.

MedPAC’s artificial reliance on FFS spending patterns to questions about MedPAC’s approach to evaluating both the differences between MA and FFS populations and the implications for comparing MA and FFS’s

CMS Finalizes 2026 Payment Policy Updates for Medicare Advantage & Part D Programs

Today, the Centers for Medicare & Medicaid Services (CMS) released the Calendar Year (CY) 2026 Rate Announcement for the Medicare Advantage (MA) and Medicare Part D Prescription Drug Programs that finalizes the payment policies for these programs. This release — combined with the CY 2026 MA and Part D final rule that was released on April 4 — makes annual routine and technical updates to the MA and Part D programs.

The actions taken by CMS help protect beneficiaries and taxpayers from waste, fraud, and abuse, while also driving access to high-quality, affordable healthcare through Medicare Advantage. By finalizing these payment policies, CMS is ensuring that Medicare Advantage continues to offer access to critical services in an efficient, accountable manner, further strengthening the program’s ability to serve beneficiaries. READ FULL ARTICLE →

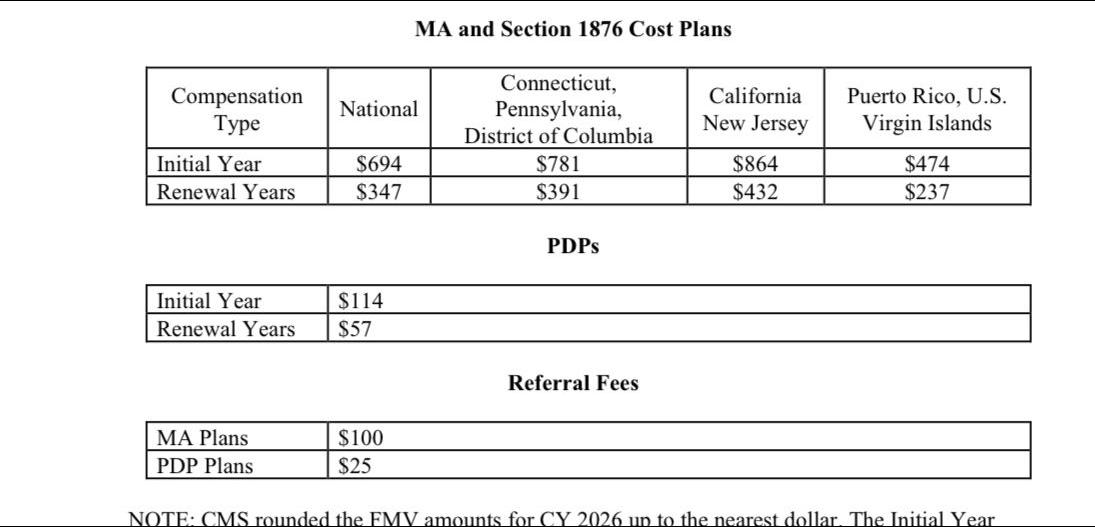

MAPD Commission Increase 2026

New Jersey and California Lead the Way

CMS is proposing the increases in MAPD commission for a certified Medicare Insurance Professional to receive.

MAPD Commission Increase 2026: New Jersey & California

Lead the Way

CMS is proposing the increases in MAPD commission for a certified Medicare Insurance Professional to receive.

Democrats Introduce Bill To Establish A Medicare 'Part E' Public Option

By Paige Minemyer

Democrats in the House and Senate have introduced new legislation that would establish a "Part E" for Medicare, which would allow people to opt into the program.

Reps. Jimmy Gomez, D-Calif., and Don Beyer, D-Va., on Monday put forward the Choose Medicare Act. Under the proposal, a potential Medicare Part E would have the program compete with private insurance. Democratic Sens. Jeff Merkley, of Ore., and Chris Murphy, of Conn., introduced a companion bill in that chamber.

Medicare Part E as outlined in the bill would sustain itself through premiums, with enrollees able to sign up through any state or federal insurance marketplace. Any existing subsidies available for Affordable Care Act (ACA) plans would be applicable to Part E coverage.

The bill would also allow employers to choose to provide Part E coverage to workers.

Mental Health & Substance Use Disorders

Medicare covers many mental health services to support you, including depression screenings, individual and group therapy, and family counseling. You may be able to get mental health counseling and treatment, including addiction recovery, from home via telehealth. If you're feeling isolated, it can take a toll on your mental health. Get tips on caring for your mental health, and learn when to seek professional support.

Sincerely,

The Medicare Team

READ FULL ARTICLE →

A Remedy For Missed IRA Distributions

By Eric Rasmussen

The IRS slaps big penalties for retirees who miss the required minimum distributions from their qualified retirement plans. But what if the person has a good excuse? For example, what if they started suffering symptoms of dementia or Alzheimer’s and miss their distributions for a couple of years?

In fact, there’s a form for that. Form 5329 allows taxpayers to report additional taxes and make up shortfalls in their required distributions so that hopefully they can avoid penalties if there was a reasonable cause, and tax experts say that Alzheimer’s would likely be one of those.

“In the circumstances where we’ve been approaching the IRS with the discovery that our RMDs have been missed I’ve always found that they’ve been pretty lenient,” said Thomas C. West, a senior partner at Signature Estate & Investment Advisors in McLean, Va., who deals with estate and longevity issues. “The big thing that I always try to do is I try to solve all of the problems before I contact the IRS with my clients.”

READ FULL ARTICLE →

Social Security Cost-Of-Living Adjustment May Be 2.5% In 2026, New Estimates Find

By Lorie Konish

Key Points

Social Security beneficiaries may see a 2.5% increase to their monthly checks in 2026, based on new government inflation data released Wednesday. Those estimates may be subject to change, since there are four more months of data before the official cost-of-living adjustment for next year is announced. Here’s what experts are watching. Millions of Social Security beneficiaries received a 2.5% boost to their benefits in 2025, thanks to an annual cost-ofliving adjustment that went into effect in January.

In 2026, Social Security checks may go up by the same amount — 2.5% — based on the latest government inflation data, according to new estimates from both The Senior Citizens League and Mary Johnson, an independent Social Security and Medicare policy analyst.

That is up from the 2.4% increase for 2026 that those sources forecast last month. A 2.5% cost-of-living adjustment would be “about average,” according to Johnson.

READ FULL ARTICLE →

California’s Deficit Dilemma: Cut Spending, Borrow Money Or Raise Taxes?

By Dan Walters

The California Legislature has just a few days to pass a 2025-26 state budget to meet the state constitution’s June 15 deadline. The deadline will be met, if for no other reason than legislators would, at least theoretically, have their salaries suspended were they to miss it. However, the budget they enact may bear only a passing resemblance to what will eventually, perhaps many months later, become a complete fiscal plan.

The revised budget that Gov. Gavin Newsom proposed a month ago projects that general fund tax revenues for the year would be about $20 billion short of covering the spending that he has proposed — and that’s after counting the billions of dollars in reductions, primarily in health care and other services for the poor, he’s asked the Legislature to swallow.

READ FULL ARTICLE →

California Hospital Prepares for Surge in Patients

By Anna Skinner, Senior Reporter

At least one California hospital is preparing for a surge in patients presenting with heat-related illness as a heat wave brings abnormally warm temperatures to the Golden State this weekend.

Why It Matters

National Weather Service (NWS) meteorologists are already issuing guidance ahead of a surge in temperatures this weekend, with inland areas across much of the state expecting temperatures to hit triple digits.

Since it is one of the first heat waves of the season, people might be unprepared for the hot temperatures, putting them at a greater risk for heat-related illness.

READ FULL ARTICLE →

RFK Jr. Says Food And Pharma Are Poisoning Americans: His Big Report Says A Fix Is Coming

By Carmen Paun, Chelsea Cirruzzo, Marcia Brown and David Lim

The Make America Healthy Again Commission that Robert F. Kennedy Jr. leads will release a strategy to combat chronic disease by summer’s end.

A much anticipated report led by Health Secretary Robert F. Kennedy Jr. says that children’s health is in crisis and that it’s likely the result of ultraprocessed food, exposure to chemicals, lack of exercise, stress, and overprescription of drugs. But the report, from the Kennedy-led Make America Healthy Again Commission, shies away from the strident language Kennedy has used in the past in demonizing the food, farming and pharmaceutical industries, and leaves for another day proposals for how to improve kids’ health. The accused industries have been lobbying furiously to persuade Kennedy to tone down the rhetoric.

Solutions for the health crisis will come within 100 days, Kennedy promised reporters during a call Thursday

READ FULL ARTICLE →

2025 JULY CONFERENCES

June 28 - July 1 NABIP: Future Foreward: Annual Convention @ Miami, FL

EVENTS

July 7 @ 2:30-4pm EPI: The Five Conversations That Drive Business Succession Planning @ SF, CA

July 9 @ 2:30-4:30pm EPI: Investigating Exit Options From Various M&A Expert Perspectives @ San Diego, CA

July 10 @ 2:30-4:30pm EPI: Investigating Exit Options From Various M&A Expert Perspectives @ Costa Mesa, CA

July 16 @ 11am-1:00pm EPI: Disaster Preparedness & Contingency Planning For Exit-Ready... @ Westlake Village, CA

July 17 @ 9am-12pm NAIFA CA: Inland Empire’s Mastering the Course: Insights for Industry Leaders @ Corona, CA

July 23 @ 2:30-4:30pm EPI: Coaching Business Owners To Maximize And Grow The Value Of Their Business @ LA, CA

July 24 @ 11:30am-1:30pm EPI: The Ripple Effect: How Tariffs Influence Business Valuation In A Global... @ Norco, CA

Benefit Mall / CRC Benefits February Compliance Update Webinar w/ Misty Baker & Carol Taylor

Benefit Mall / CRC Benefits March Compliance Update Webinar: RxDC Explained w/ Misty Baker & Carol Taylor

Benefit Mall / CRC Benefits April Compliance Update Webinar: MLR & 5500 w/ Misty Baker & Carol Taylor

Benefit Mall / CRC Benefits May Compliance Update Webinar w/ Misty Baker & Carol Taylor

Benefit Mall / CRC Benefits June Compliance Update Webinar w/ Misty Baker & Carol Taylor Commission Solutions 2025 Webinars Commission Solutions January 8, 2025 Webinar: Mary’s Journey To Protect, Grow and Sell Her Commissions Commission Solutions January 16, 2025 Webinar: How to Sell Your Health Insurance Book of Business Commission Solutions February 12, 2025 Webinar: Rick’s Journey to Protect, Grow, and Sell his Commissions Commission Solutions February 20, 2025 Webinar: How To Use Advanced Tax Planning/Maximizing Retirement Income Commission Solutions March 12, 2025 Webinar: How Health Commissions Were Protected and How the Plan... Commission Solutions March 20, 2025 Webinar: How to Use Advanced Tax Planning for Maximizing Retirement Income Commission Solutions April 9, 2025 Webinar: Broker Succession Planning and the Impact on Loved Ones Commission Solutions April 17, 2025 Webinar: Help Baby Boomers as their Preferred Byer and Successor

Covered California: Important Tax Information: How to get a Small Business Credit

IEHP: Health Education for Members Join no-cost health education classes just for IEHP members. Pinnacle: Announcing Healthview, Refreshed: Simply A Better Experience

Sutter Health Plan: Prioritizing Mental Wellness

Exploring California Mountain Trips In the Summer

By Cal Broker Magazine

California is a land of towering trees, sweeping seascapes, and rugged mountains, so it’s no wonder that it attracts visitors from all over who want to experience its beauty firsthand. Visiting California’s numerous mountains allows visitors to see several natural wonders in one park or area, with plenty of things to see and healthy activities to do. As your clients start making their summer vacation plans, here are a few spots in California that offer mountainous adventures. Knowing the terrain and activities involved in these spots can help them understand the right insurance coverage they need to give them peace of mind during their getaway.

Northern California

Northern California has a mild, Mediterranean climate that can be damp and foggy in the cooler months and hot and dry during the summer. The terrain includes rugged mountains throughout the Sierra Nevada Mountains, as well as giant redwood forests, where travelers can hike, bike, camp, and explore.

Shasta-Trinity National Forest

Shasta-Trinity National Forest is a must-visit in Northern California. It’s home to Mount Shasta, the second-highest mountain peak in the Cascade Range. The park itself covers more than two million acres and has five different

wilderness areas. There are plenty of trails around the area where trekkers can get different viewpoints of the surrounding area, camp, and hike. Another feature of the park that attracts visitors is Shasta Lake. The lake’s placid waters are an ideal spot to try all kinds of water sports, like boating, swimming, fishing, and paddling. Visitors can camp in the area, explore the hiking trails around the lake on bike or foot, and relax in the eating and rest areas.

Lassen Volcanic National Park

Lassen Peak, in the Cascades, is the world’s largest plug dome volcano. The park is home to several volcanoes that helped to create the slopes and cliffs that visitors enjoy hiking today. Hikers can explore 150 miles of trails that loop around lakes, meadows, volcanic peaks, and even hydrothermal zones. Some fun, healthy activities your clients can try after hiking include boating, fishing, and swimming in the park’s lakes. This park is also a popular spot for stargazing, horseback riding, and even parkcaching.

Central California

Central California has a unique climate that is influenced by the San Francisco Bay. When it comes to nature, this part of the state has mountain ranges, giant sequoias, and several lakes and rivers for water activities.

Sequoia National Park

Sequoia National Park is located in the southern part of the Sierra Nevada range. Visitors can come for a day hike, or plan to stay for a few days and set up camp. One thing to keep in mind is that the weather changes with the elevation, so visitors need to be prepared for all kinds of weather. The top activity here is wandering the trails and sequoia groves. Other parts of the park have areas to enjoy a picnic and spot wildlife. Sequoia National Park also has spots for adventurous activities like fishing, rock climbing, and horseback riding.

Yosemite National Park

Yosemite National Park contains a mix of landscapes, like cascading waterfalls, deep valleys, and rolling meadows. This park also has towering sequoia trees, but is famous for its distinctive mountains, like El Capitan, Half Dome, and Mount Lyell. There are plenty of hiking trails to discover different lookout points and landscapes. However, there are other ways to discover the park besides just on foot. Visitors can roam the trails on horseback or even on mules. Something else that’s great about this park is that there are 12 miles of paved paths for bikes and e-bikes. People who like water sports can go floating or rafting on the Merced River, as well as swimming and paddling on Tenaya Lake.

The key to a safe and fun trip to the California mountains is being prepared. “ “

Southern California

Southern California is a magical mix of arid deserts, rolling mountains, and beautiful forests, all of which offer great opportunities for hiking and camping. Southern California has a Mediterranean climate, but it is warmer than northern and central California. The deserts can reach scorching temps, so hikers and campers should be prepared with the right gear and supplies.

Joshua Tree National Park

Joshua Tree National Park is the unique meeting place of two of Southern California’s deserts: the Mojave and the Colorado. This park, which covers nearly 800,000 acres, is home to the Little San Bernardino Mountains, ancient rock formations, and the curious trees from which the park gets its name. The park has 300 miles of trails and nine campgrounds available for visitors to see some of its most emblematic sights. Within the park, hikers will find cactus gardens, a variety of rock formations, and nature trails that highlight the park’s flora and fauna. The Joshua trees are a natural wonder that definitely can’t be missed.

Mount San Jacinto State Park

Mount San Jacinto is the highest peak in the San Jacinto Range. The park covers 14,000 acres and 50 miles of trails for hiking and biking. The trails vary in difficulty so that visitors can enjoy both different views and challenges. As hikers loop the trails, they can see pine forests, meadows, and deserts. Mount San Jacinto is home to all kinds of wildlife and is a popular spot for birdwatching, in particular. One thing that visitors shouldn’t miss is a ride on the Palm Springs Aerial Tramway, a cable car that has impressive panoramic views of the park.

Preparing for a California Mountain Trip

The key to a safe and fun trip to the California mountains is being prepared. With the right gear and equipment, travelers can be better prepared for the terrain and elements that await them. It’s also important to look into factors like the level of difficulty of the hikes, if the activities offered in the area are family-friendly, and if equipment is available to rent, if necessary. Knowing exactly where they’re going and what to expect can also help when it comes to choosing the right insurance coverage for the trip. Being prepared for any and all situations means your clients will have better peace of mind as they enjoy their vacation.

Sources:

1. https://www.fs.usda.gov/r05/shasta-trinity

2. https://www.nps.gov/jotr/index.htm

3. https://www.nps.gov/lavo/index.htm

4. https://www.nps.gov/seki/index.htm

5. https://www.nps.gov/yose/index.htm

6. https://www.parks.ca.gov/?page_id=63

ANTICIPATING DRAMATIC GROWTH IN THE NUMBER OF OLDER CALIFORNIANS

By Hans Johnson, Eric McGhee, Paulette Cha, and Shannon McConville, with research support from Shalini Mustala

The Population of Older Californians Will Continue to Grow and Diversify. The significant shifts in California’s demographic landscape over the past two decades are projected to continue and even accelerate through 2040. Several key factors are driving these changes: the aging of the baby boom generation, increased longevity, and the long-term effects of past immigration patterns.

The baby boom, from 1946 to 1964, created exceptionally large population cohorts that are now entering older ages. The youngest baby boomers are now 60 years old while the oldest are 78. In 2040, the youngest will be 76 and the oldest will be 94. As this generation ages, the older adult population is increasing significantly. Because of advances in health care and improved living conditions, people are living longer, but they are also living through more disabled years (Tesch-Römer and Wahl 2016).

It is important to note that the COVID-19 pandemic caused a brief— and traumatic—deviation from the long-term pattern of increases in life expectancy. The latest estimates suggest that life expectancy has resumed its pre-pandemic trend of gradually increasing longevity. (1) The Department of Finance projects moderate increases in life expectancies through 2060.

California’s Older Adult Population Will Increase Dramatically By 2040. California’s older adult population (aged 65 and over) is projected to increase by a remarkable 59 percent, from 5.7 million to just over nine million. This growth stands in stark contrast to the projected changes in other age groups. The working-age population (20–64 years old) is expected to increase only three percent, while the population under age 20 is anticipated to decrease by 23 percent. California is projected to have 3.4 million more older adults aged 65 and over, and 1.7 million fewer residents less than 65 years old.

This disproportionate growth in the older population will lead to a significant shift in the state’s age structure. Almost one-quarter of Californians (22%) will be age 65 or older by 2040, a substantial increase from 14 percent in 2020. The old-age dependency ratio (the number of older adults per 100 adults of working ages) is projected to

grow from 24 to 38.(2) In other words, there will be 38 older adults for every 100 working adults in the state.

The most dramatic growth is projected among the oldest age groups— or the oldest old (Figure 1). The population aged 80 and over is expected to more than double, increasing by nearly 1.8 million in 2040. This rapid growth in the oldest age groups, driven by both the aging of baby boomers and increases in longevity, is especially significant because of this group’s relatively high personal care and health care needs. The dramatic population increase for this group overwhelms any improvements in well-being. For example, there will be so many more very old Californians that reductions in the share with self-care limitations will not counterbalance a dramatic increase in care needs.

Declines in the state’s child population reflect low birth rates. Like the rest of the United States and most developed countries in the world, California has experienced a sustained decline in birth rates. In California, the total fertility rate—the average number of births in a woman’s lifetime—has fallen from 2.15 in 2008 (just above the level needed to replace the population) to 1.47 in 2020. The Department of Finance (DOF) projects that these low levels of fertility will persist into the future.

Declines in the population aged 16 to 64 are driven primarily by interstate out-migration. For several decades, California has experienced substantial net outflows to other states, particularly among less-educated Californians. International immigration to the state counterbalanced some of this population decline, but the flow of immigrants has been modest in recent years.

Growth in the Older Adult Population Will Vary Across Counties. While all regions of the state will be impacted by growth in the older adult population, regional differences are a key consideration for planning and policy. The DOF population projections provide information at the county level, which we use to provide a high-level picture of how older adults will be distributed across the state.

California’s Aging Population - Part 2

Increases in the population of adults 65 and older in the Far North region of the state will be much lower than the statewide average. Several counties near the northern border are projected to see little or no growth—including Shasta, one of the largest counties in the region. Many Bay Area counties—including Alameda, Santa Clara, and Contra Costa—will see growth rates in the 70 to 80 percent range. In contrast, counties in the Central Valley (e.g., Kern, Stanislaus, Fresno, and Kings) are projected to have lower than average growth (about 40%), as are Central Coast counties including Santa Barbara and San Luis Obispo. Most large Southern California counties, including Los Angeles, will see increases around the state average (60%); this is not surprising, given that such a large share of the state’s population resides in that region.

When we look at growth among adults aged 85 and older, the regional patterns shift somewhat. Northern California regions stand out with some of the largest increases; in a few counties—including Mendocino, Trinity, and Plumas—the over-85 population will more than triple by 2040. Most large Bay Area and Southern California counties will see their populations age 85 and older more than double. Although counties such as Fresno and Stanislaus will have lower than average increases in older adults, they will see considerable growth (80%) in this age group.

California’s Older Adult Population Will Be Diverse.

The racial/ethnic composition of California’s older adult population is projected to become increasingly heterogeneous, with no single racial or ethnic group constituting a majority of the older adult population. The number of Latino, Asian, and Black older Californians is expected to double or nearly double by 2040, while the older white population will increase by 30 percent. While whites are projected to remain the largest racial/ethnic group of older adults, their relative share will decrease as other groups grow more rapidly (Figure 3).

A key driver of diversity among older adults is the dramatic increase in immigrants from Latin America and Asia in the 1980s. Upon arrival most were young adults, primarily in their 20s and 30s. Those early large cohorts of immigrant arrivals from the 1980s are now in their 50s and 60s, beginning to fundamentally alter the ethnic composition of California’s older population.

It is worth noting that in recent years, migration of older adults, both international and domestic, has not been a primary driver of the growth and diversity of California’s older population.(3) Instead, the growth in the state’s older population is primarily driven by the aging of existing residents, including those who immigrated decades ago, and their increased life expectancy.

There will also be variation across the state in racial and ethnic changes in the population of older adults (Figure 4). In 2020, only 12 counties did not have a majority-white older adult population; by 2040 that number doubles to 24 counties. As previously discussed, the population of adults 65 and older who identify as Latino and Asian and Pacific Islander will more than double by 2040 and the older Black population will nearly double (90% increase). Counties that will see the highest growth rates in Latino older adults include relatively smaller counties like Mendocino and Marin, along with larger counties such as Monterey and Orange. Among Asian older adults, Santa Clara County will have one of the highest increases, with the number of adults aged 65 and older of Asian and Pacific Islander descent growing from about 98,000 to nearly 225,000.

The share of older adults who are foreign born is expected to increase to over 40 percent by 2040 (compared to 29% in 2020), again reflecting immigration patterns from decades ago. The largest increases will be among 65 to-74-year-olds (Figure 5). The majority of Latino older adults (59%) will be foreign-born, similar to levels today. Almost 9 of 10 Asian older adults will be foreign born. Again, these levels are similar to those of today.

For many agents who sell Medicare products, there’s a high likelihood Medicare Supplement products are available in their offerings to clients. But, for those who have not considered selling Medicare Supplement plans, we’ll provide an overview of the products. And, for those of you who do offer Medicare Supplements to your clients, we’ll also discuss some more detailed information you may not have thought about or considered.

Medicare Supplement Plans, also known as Medigap, are private insurance policies that help pay for out-of-pocket costs not covered by Original Medicare (Parts A and B), such as:

• Copayments

• Coinsurance

• Deductibles

There are several standardized Medigap plans (labeled A through N), and each offers different levels of coverage. While Medigap policies are sold by private insurers, all plans with the same letter offer the same basic benefits, regardless of the company.

Key Features:

• You must have Medicare Part A and Part B to buy a Medigap policy.

• Medigap does not cover prescription drugs—you’ll need a separate Part D plan for that.

• It only covers one person; spouses need separate policies.

• Medigap doesn’t work with Medicare Advantage plans.

These plans can help reduce unexpected healthcare expenses and provide more predictable costs in retirement.

Why is it important for Medicare beneficiaries to consider these plans?

• Typically, beneficiaries only have one opportunity to join this type of plan with Guaranteed Issuance and that is when they first become eligible for Medicare.

° If that opportunity is missed, then they must go through Medical Underwriting. If they have any pre-existing health conditions, there is a chance their application will be denied.

• This type of Medicare product allows beneficiaries to see any medical provider that accepts Medicare, with some exceptions.

• Beneficiaries will avoid the pitfalls of Insurance providers and Medical Group providers coming to contract disagreements. These disagreements can lead to disruptions in care if they are covered under a Medicare Advantage plan.

Why is it important for Agents to offer these products?

• The simple answer is that you become more appealing to Medicare beneficiaries when you can speak to ALL of their plan options.

• The retention rate is high. According to the Kaiser Family Foundation, one in five Medicare enrollees choose a Medicare Supplement product. And of those that choose this product, 90 percent retain their policy.

° This means that retaining your clients requires less time, which allows you to spend more time gaining new business.

• Commissions: many of the carriers pay at least a 20 percent commission in the first year of the policy.

° We’ll provide additional information on this later in the article.

For those of you who already market Medicare Supplement products, you might find some of the upcoming information very helpful for you when considering which carriers you’d like to offer to your clients. Please note that not all carriers are represented in this article. There are over 20 carriers in California. Please reach out to the carrier in question to verify the information as information frequently changes.

Rate locks are important to consider as this can protect your client from rate increases for six to 12 months depending on the insurance carrier. For example, Blue Shield and Humana have 12-month rate locks. This is important because when you are advising your client on the lowest rate option, you may not be thinking about the rate increase that’s lurking around the corner.

If you decide to enroll a new client into a Medicare Supplement prior to that carrier’s annual rate increase, it’s possible that your new client will get hit with an unexpected rate increase. But, if you put them with a plan like Blue Shield or Humana, your client will avoid this pitfall for the first 12 months they are on their policy. You can mention this to your new client to further show that you are the subject matter expert of these Medicare products all while strengthening the trust your client has with you.

United Healthcare, Anthem Blue Cross (Elevance), and Health Net all have rate locks built into their plans. Please speak to your carrier representative to get more information.

Plan changes often come up when your client wants to “shop” for alternative options due to rate increases or they want to change their benefit level. However, they are not always able to do this. If a client is healthy, they can facilitate this change through submitting an application that requires medical underwriting. If the member is unhealthy, they will need to wait until their birth month in order to use the “birthday rule” that allows them to make a plan change regardless of pre-existing health conditions. Alternatively, if your client is with United Healthcare/AARP’s Medicare Supplement plan, the member can move freely from plan to plan anytime throughout the year.

Commissions are always at the forefront of an Agent’s mind. Although we’re all going to do what’s right for the client, it is important to know the details of the insurance carriers we’re representing. Based on today’s information, below is a list of some of the carriers in California and how they pay.

• Anthem Blue Cross (Elevance): will pay lifetime commissions for those members that are underwritten or enroll due to being new to Medicare. Alternatively, they will only pay up to 10 years if a member is written using a Guaranteed Issue, such as, the “birthday rule”

• Blue Shield of CA: will pay lifetime commissions in all cases, unless the member is under 65 years of age. Commissions are reduced after Year 1 of the policy.

• Health Net: will pay lifetime commission in all cases, unless the member is under 65 years of age. Commissions are reduced after Year 1 of the policy.

• UnitedHealthcare/AARP: Beginning June 1, 2025 they will no longer pay lifetime commissions for new business written going forward. They will only pay up to year 10 of the policy.

• Humana Achieve: pays lifetime commissions but commissions are reduced the longer the policyholder remains active. They will pay on members who are under 65 years of age.

There are many more carriers to consider. Please reach out to your contracted carriers to learn more about their commission structures.

Guaranteed Issuance (GI) Guidelines are important to know and understand so that you can better assist your clients. The purpose of knowing the “GIs” is so you can address certain situations that would allow your client to make a plan change without having to go through medical underwriting. Here are some of the more common “GIs”:

• New to Medicare: the member is new to Medicare because they are either turning 65 or they are enrolling into Part B for the first time. In order to qualify, they must enroll within six months for the Part B start date

• Birthday Rule: For members that are currently enrolled in a Medicare Supplement plan, they have 30 days prior to their birthday and 60 days after their birthday to make a change to their policy. They can make a change as long as the benefits offered are equal or lesser value to their current plan.

• Loss of Employer Coverage: if a member loses their employer sponsored coverage, they can enroll in a Medicare Supplement plan. They must provide proof of notice of termination.

° Some carriers may require that it be an involuntary termination.

A lesser known but very useful “GI” applies to those clients that are enrolled in a Medicare Advantage plan. If the Medicare Advantage reduces benefits or increases the amount of cost-sharing or premium or discontinued a contract with a provider currently furnishing services then the member has the opportunity to enroll in a Medicare Supplement.

• If the member’s current Medicare Advantage plan offers a Medicare Supplement, they may have to enroll in that carrier’s Medicare Supplement. If the carrier does not offer a Medicare Supplement option, they may be able to shop other insurance carrier options. Please verify this information with each of the carriers as their definitions may be slightly different.

Household Discounts are an excellent tool for clients to take advantage of in order to save money. Typically, when more than one policyholder lives at the same address, they may be able to qualify for the household discount that reduces their monthly premium responsibility. Below are some of the carriers that offer household discounts:

• Anthem Blue Cross (Elevance): five percent discount for each member

• Blue Shield of CA: seven percent discount for each member, must be on the same plan

• Humana Achieve: 12 percent discount for each member

• Cigna: six percent discount for each member

• Physicians Mutual: 10 percent discount for each member

• United Healthcare/AARP: seven percent discount for each member

There is so much to know about Medicare Supplements. I encourage you to speak to your uplines, your carrier representatives, and your colleagues. Share your stories with one another as that is how we grow. If you’re looking for a group of agents, look no further than the California Agent and Health Insurance Professionals (CAHIP). Most counties have a local chapter that you can get involved with.

Check out https://cahip.com

Happy Selling!

David Ethington is VP of the Medicare Division and director of Broker Relations with Commission Solutions, part of Integrity Advisors. His work has excelled due to his commitment to providing the best service to both health clients and health brokers. David respects the hard work it takes to build a book of business and enjoys working with retiring brokers and their families. David has participated in the commission protection process for seven years. He’s also involved in acquisitions, especially in the broker relationship transfer of commissions. David lives in Orange County with his wife and their cats. He is an avid runner and completes several long-distance events annually.

David@commission.solutions 714-664-0605

Insurance Innovation: The NCD StoryConsidering NCD for Medicare Clients

Via Interview with Sam Melamed CEO of NCD by Phil Calhoun

The insurance industry is filled with stories of unconventional career paths and innovative business models, but few are as intriguing as the journey of Sam Melamed, who transitioned from rabbinic studies to become a leader in supplemental health benefits. In a recent interview, Phil Calhoun—representing California Broker Media with 250,000 California-licensed subscribers—sat down with Sam Melamed, the CEO of NCD, to discuss the company’s mission, product offerings, and the unique value it brings to brokers and clients nationwide.

As CEO of NCD, Melamed has been instrumental in shaping the company’s direction and facilitating industry dialogues. Calhoun and Melamed discussed the driving force that helped Sam into his product development and regulatory strategy work leading up to NCD.

As CEO of California Broker Media, Calhoun enjoyed learning how Melamed’s extensive background in insurance leadership brings a broker-centric perspective to the discussion. “It is ensuring the conversation addresses the real-world needs of agents and agencies across California and beyond,” stated Calhoun.

Sam Melamed’s Unconventional Path

Sam Melamed’s route to insurance leadership is anything but typical. He spent years studying to become a rabbi then realized he preferred another career path.

After getting married young, a neighbor introduced him to insurance sales—a field he initially found challenging. “I was just terrible. I couldn’t figure out how to do it,” Melamed admits, highlighting his early struggles with prospecting and closing.

Driven by curiosity, Melamed launched Insurance Forums, an online community for agents and brokers. He chose this path in a bid to understand his own sales difficulties. The forum grew into a small business, complete with an insurance magazine, giving Melamed firsthand insight into the challenges brokers face and the importance of quality industry content.

His career advanced when he joined ABC Insurance Trust, where he learned the nuances of association health plans, ancillary benefits, and employee benefits. Rising through the ranks to become CEO, Melamed honed his expertise in dental, vision, disability, and supplemental benefits.

NCD’s Mission and Market Approach

Four years ago, Melamed took the helm at NCD, a company specializing in dental and vision insurance, with plans to expand into other supplemental products. Under the leadership of CEO Liam Collopy, NCD carved out a unique space in the market by focusing on the underserved individual segment—a group often overlooked by major carriers like MetLife, which traditionally prioritize large group plans.

NCD operates as a Managing General Agent (MGA) and product development company, partnering with national carriers to create custom plans for individuals. Their flagship offering, developed with MetLife and the National Wellness and Fitness Association, was the first $10,000 annual maximum dental plan available to individuals—a benefit previously reserved for large group plans. These products are built on an association chassis and feature escalating benefits, including major services and implants, designed to be “the last dental plan you ever have to buy,” as Melamed puts it.

Broker-Centric Distribution and Support

NCD’s distribution model is designed with brokers in mind. Agents can contract directly with NCD or through major Field Marketing Organizations (FMOs) such as Integrity, Spark, Amara Life, and others. This flexibility allows brokers to choose the contracting path that best fits their business needs, whether that means consolidating for better bonuses and marketing support or working directly for personalized service.

One of NCD’s hallmarks is its obsession with customer and agent experience. The company boasts over 10,000 five-star reviews and is recognized as one of the highest-rated insurance plan administrators in the country. “We answer every phone call from agents in 30 seconds or less, every email in an hour or less, every text in 10 minutes or less,” Melamed explains, underscoring the company’s commitment to responsiveness and support.

“We answer every phone call from agents in 30 seconds or less, every email in an hour or less, every text in 10 minutes or less.”

Products for All Ages and Needs

NCD’s plans are available to any adult age 18 and over, with no upper age limits or price differences based on age. The company serves a diverse clientele, including retirees and residents of nursing homes, who continue to value dental and vision care well into their later years.

The dental network, powered by MetLife, is among the largest in the country and particularly strong in California. Members benefit from broad access to both general dentists and specialists, with significant savings when using in-network providers. Out-of-network coverage is also available, though members may pay more due to balanced billing and claims adjudication.

Culture and Mission: Spreading the Smile

NCD’s internal culture is shaped by its mission to “spread the smile.” This ethos is reinforced through initiatives like the “smile feed,” where team members share positive customer feedback throughout the day, keeping the focus on delivering exceptional service and fostering a positive work environment. Melamed credits this culture with attracting top talent and driving the company’s success, even when traditional ROI metrics might not fully capture the value of such an approach.

Relevance for California Brokers

With over 250,000 licensed life and health insurance professionals in California—many of whom are nonresidents but licensed to do business in the state—NCD’s offerings can be a perfect fit for Medicare and individual clients who often have limited options many of which are DHMO plans. NCD’s national reach, regulatory expertise, and broker-friendly approach, combine to make for a valuable partner for many agencies.

Calhoun suggested “Many brokers operate across group, individual, and Medicare markets. NCD’s products are designed to fit seamlessly into these varied books of business. Brokers look to provide high-value supplemental options that can be offered at key touchpoints in the client’s health coverage journey and NCD plans are a great fit.”

The conversation between Calhoun and Melamed offers a window into the values and vision driving NCD’s growth in the supplemental benefits pace. Melamed’s career journey through his continued focus on insurance innovation, combined with NCD’s broker-centric focus, highlights how thoughtful product design, relentless customer service, and a mission-driven culture can set a company apart in a crowded market. For brokers and agencies seeking high-value dental and vision solutions for their clients, NCD stands out as a partner committed to both excellence and empathy.

Sam Melamed is the CEO of NCD, a leading provider of supplemental health benefits for the Medicare Advantage and ACA markets. With a background in insurance innovation and digital community building, he guides NCD in delivering tech-driven, broker-friendly solutions. Sam is also a frequent voice in industry podcasts, sharing insights on ancillary products and healthcare trends. His leadership focuses on simplifying benefits while supporting carriers, brokers, and members alike.

Winter is Coming for California’s Health Insurance Brokers

By Michael Blea, Chief Growth Officer at SCAN Health Plan

I've spent three decades in this industry, and I’ve witnessed the cyclical nature of the market. I remember the Balanced Budget Act of 1997, which created the Medicare+Choice Program, which became known as Medicare Advantage.

I recall the economic downturn of the late 2000s, when one of the largest insurers abruptly downsized. One morning they sent busloads of sales and telesales representatives to a hotel, told them their positions had been eliminated and promised to ship their belongings to their homes. It was a stark reminder of the volatility inherent in our profession.

Since then, a new generation of brokers has entered the field. Most of them have experienced nothing but boom times. However, for those of us who have weathered the busts, ominous clouds are gathering on the horizon, signaling potential trouble ahead.

Market Shifts and Financial Pressures

Insurers are beginning to exit the Medicare Advantage (MA) markets. Some carriers aren’t paying commissions on stand-alone prescription drug plans.

Others have removed their MA plans from online enrollment platforms. The Inflation Reduction Act has introduced changes that lower reimbursement rates and increase financial pressures on insurers. It’s not just insurers feeling the strain; at least 15 hospitals and health systems have also pulled out of Medicare Advantage.

For brokers measuring their sales numbers, the signs of a decline are evident. Make no mistake: we are entering a bear market. But how can brokers navigate and succeed in this challenging environment? It’s time to rethink our approach to enrollment.Here’s how:

Focus on Quality Sales

Dumping clients into an MA plan without considering their long-term health needs does little to benefit them. Insurers are looking for members who are connected with the right doctors and who will remain loyal to both, in return for supporting their health. Brokers should adopt this focus as well. Quality sales, where clients are matched with plans that truly meet their needs, will lead to better health outcomes, more satisfied customers and longer-term stability for everyone.

Look to the Long Term

Our current system allows for annual enrollment and disenrollment in plans, leading to significant churn. However, this churn does not benefit either the member or the insurer. Health costs decrease and health outcomes improve when insurers, physicians, and members can make long-term investments in health. Brokers should seek out plans with provider networks that will support members for years to come, fostering stability and continuity of care.

Support Your Community

Some brokers go above and beyond by helping clients find care, navigate medical bureaucracies, locate the best prices on medications, and even connecting them with life-saving social services. These brokers are not just salespeople; they are trusted members of their communities. By leveraging this trust, they help clients access a range of health solutions that may not be provided by an insurer. Brokers have a role to play in better health, and this is a powerful way for them to fulfill it.

Brokers who

focus

on health and serve that purpose will find that they not only survive this period

but also come out on top

Be a Trusted Advisor

Each year, thousands of people enroll in plans and are randomly assigned providers. When these mismatches occur, members often drop out of the plan. The lack of stability leads to missed preventive care and can lead to health declines. Brokers have a special role to play as trusted confidantes. By serving as a link to the right providers, brokers can help ensure smoother relationships between carriers and physician groups. This, in turn, yields better long-term health outcomes and more enduring customer relationships. Greater member satisfaction and improved health outcomes also lead to higher star ratings, which are vital for plans, providers, and patients alike.

Choose Higher-Rated Plans

Amid these market shifts, it’s crucial that brokers steer clients toward higher-quality plans. Pay attention to plan ratings; if a plan’s ratings decline, it’s a sign that it’s probably not the best option for your client. On the other hand, high-quality plans with high star ratings have more resources to support your clients’ health. Enrolling them in these plans is an easy way to ensure long-term satisfaction and customers who will be as loyal to you as they are to their doctor and carrier.

Navigating Stormy Waters

Yes, we are in stormy waters, and there are signs of problems ahead. However, this does not mean we are heading for collapse. Medicare Advantage remains the best plan option for most seniors, providing the coverage and benefits they need to lead healthy lives in their later years. Brokers who focus on health and serve that purpose will find that they not only survive this period but also come out on top.

Michael Blea leads SCAN’s Medicare growth operations across five states—California, Arizona, Nevada, New Mexico, and Texas. With over 25 years in the health insurance industry, he has deep expertise in scaling Medicare distribution channels. Previously, he was Vice President & General Manager at Golden Outlook, where he built one of the nation’s largest field marketing organizations. He also held leadership roles at Health Net and Secure Horizons/PacifiCare.

Financial Grade’s Playbook for Medicare Brokers Navigating California’s Evolving Market

Via Interview with Pete Blasi CEO of Financial Grade by Phil Calhoun

For two decades, Pete Blasi has been quietly shaping the Medicare brokerage landscape in California and beyond.

As the CEO, and president of Financial Grade, Blasi brings a rare blend of hands-on sales experience, strategic vision, and a deep commitment to broker education. In a recent conversation with Phil Calhoun, CEO of California Broker Magazine, Blasi opened up about his journey, the evolving needs of brokers, and the actionable strategies that have made Financial Grade a trusted partner for hundreds of California insurance professionals.

Financial Grade is a leading Medicare-focused field marketing organization (FMO) based in California. The company partners with independent insurance brokers to provide access to top Medicare Advantage, Medicare Supplement, and ancillary health products, while also delivering robust training, compliance support, and business development resources.

From Financial Advisor to Medicare Market Pioneer

Blasi’s entry into the Medicare space was serendipitous but quickly became a calling. “About 20 years ago, I founded Financial Grade after helping a client unravel Medicare,” Blasi recalls. “There was limited knowledge and resources to really get Medicare—especially all the different products that could serve clients’ needs. I saw the future, with Baby Boomers coming and increasing complexity, and jumped in as one of the first distributors in the Medicare market in San Diego.”

This foresight proved prescient. The Medicare market has since exploded, with California’s aging population and regulatory environment creating both challenges and opportunities for brokers and agencies.

The Broker’s Pain Points: Organization, Education, and Retention

Having worked with hundreds of brokers over the years, Blasi has a clear-eyed view of their biggest needs. “Brokers are great conversationalists and salespeople, but being organized is often a challenge,” he notes. “They need tools and processes to manage the client journey—from initial engagement and enrollment to ongoing follow-up, reminders, birthday cards, and annual policy reviews. A system is essential.”

This focus on systems is more than operational—it’s about building trust and delivering consistent value. “Systems and processes prove you’re a trusted advisor,” Calhoun observes, and Blasi agrees: “You really want to gain, but you also want to retain those clients year after year.”

Education as a Differentiator

Blasi emphasizes that successful Medicare brokerage starts with education, for both brokers and their clients. “Medicare is different from other types of insurance. Whether a broker comes from under-65 health, P&C, or another line, proper education is key,” he says. Financial Grade offers a structured track for agents,

covering both “Insurance 101” and “Medicare 101,” ensuring they understand not only the basics but also the nuances of the client journey as needs change over time.

He also highlights the importance of understanding ancillary opportunities: “Beyond Medicare, there are add-on products—dental, hospital indemnity, and more— that can serve clients and expand the broker’s value proposition.”

Touchpoints and Client Engagement: The Financial Grade Formula

One of Blasi’s core philosophies is that enrollment is just the beginning of the client relationship. “You want to call clients three days after enrollment, engage with them several times a year, and provide additional education. The idea is to serve them well, year over year,” he explains.

This approach is especially crucial in California, where strict Department of Insurance regulations require brokers to maintain clear records and demonstrate ongoing service. Regular touchpoints not only support compliance but also foster loyalty and retention—key drivers of long-term revenue.

Scaling Up: Supporting Growth-Oriented Brokers