9 minute read

Passing the baton

Knowing who is responsible for certain SMSF obligations after a change of individual trustees is critical and complicated. SuperCentral superannuation special counsel Michael Hallinan examines the legal approach to these circumstances.

Circumstances can occur during the life of an SMSF whereby a change needs to be made to the make-up of the fund trustees. When this situation arises, it needs to be determined who is then responsible for the SMSF annual return (SAR), the tax return and any resulting ATO liability. This article will address this issue.

General legal rules

There are general legal rules that are relevant to this issue. First, unlike companies, or more generally corporations, SMSFs are not legal persons. This means an SMSF cannot own property, enter into or be bound by contracts, commit torts and sue or be sued. It is the trustee of the SMSF that owns the property, it is the trustee of the fund that enters into or is bound by contracts and commits torts and it is the trustee of the SMSF that sues or is sued.

Despite the legal position, in everyday discourse the SMSF is treated, at least grammatically, as if it is an entity. For taxation and accounting purposes, the SMSF is treated as a taxation entity and as an accounting entity.

As the SMSF is not a legal entity, it is the trustee that incurs fund liabilities. Trustees have a right of indemnity in respect of properly incurred trust liabilities so they can either pay the tax from personal funds and then be reimbursed from the assets of the SMSF or pay the debt directly using fund assets. While they have a right of indemnity, this does not necessarily mean they will be indemnified as there may simply be insufficient SMSF assets to cover the costs in question. Nevertheless, they have the right.

In terms of liabilities incurred by the trustees, it is the trustees at the time the liability is incurred that are personally liable for it. In relation to income tax liability, this liability arises immediately before the end of the financial year.

Having a right of indemnity means the trustees have proprietary interest in the SMSF’s assets because the interest is property and can be assigned to third parties, and that this interest is only recognised in equity and enforceable by equitable proceedings. So in a way the trustees are beneficiaries of the SMSF.

However, the interest relating to the trustees is different from that of an SMSF member. Members have the most complete and superior beneficial interest, while the interest the trustee has due to the right of indemnity is a lesser beneficial interest. This interest of the trustee arises by reason of and to the extent required to satisfy right of indemnity. If the liability giving rise to the right of indemnity ceases, for example, if the liability is discharged by payment from the fund or the trustees have discharged the liability and they have been reimbursed from the assets of the fund, then the equitable property interest also ceases. The equitable interest arises by reason of the liability and once the liability is satisfied, the interest is extinguished.

Further, the right of indemnity continues to exist even if the trustee has retired or been removed as trustee. However, the right of indemnity will cease if the current trustees discharge the liability.

In relation to super funds, taking income tax liabilities as an example, the trustee that incurs the tax liability in respect of the 2025 financial year will be the trustee immediately before the end of the 2025 financial year, that is, the trustee at 11.59pm on 30 June 2025 for this year. The argument is that, at the close of the 2025 financial year the income tax liabilities of the super fund immediately arise, the liability may not then be known or may not even be quantifiable, however, the amount of tax due in the 2025 financial year will, in due course, be determined and expressed as a specific dollar amount. This is the view of the ATO as set out in paragraph 7 of Practice Statement Law Administration (PSLA) 2012/2 (revised 16 January 2025). In relation to other taxation liabilities that may apply to SMSFs, such as goods and services tax (GST) liabilities and payas-you-go (PAYG) imposts, a similar position would occur. In relation to GST, it is the trustee at the end of the relevant reporting period that incurs the liability. In relation to PAYG, it is the trustee at the time of payment to which the withholding should have occurred.

Hypothetical situation

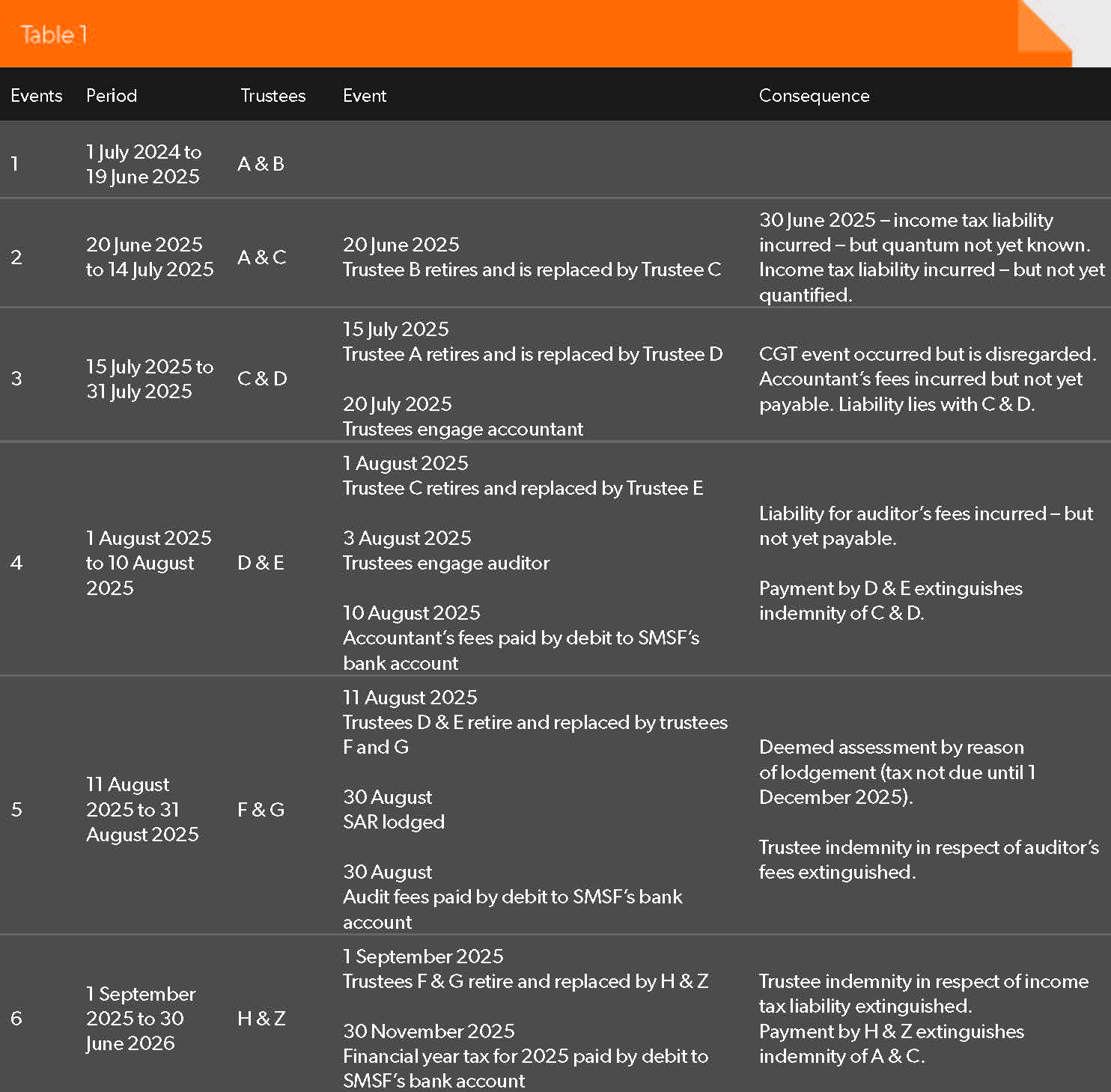

Table 1 shows an SMSF that has experienced a sequence of changes to the individual trustees of the fund in relation to the 2025 financial year and the following months until 31 December and the following months until 31 December 2025 to deal with the post-balance event arising from the 2025 financial year.and the following months until 31 December 2025 to deal with the post-balance event arising from the 2025 financial year.

The unnamed SMSF has not engaged a tax agent and so must lodge the SAR in respect of the 2025 financial year by 31 October2025 and must pay the income tax arising in respect of the 2025 income year by 1 December 2025. Any relevant CGT implications have been ignored in this example.The unnamed SMSF has not engaged a tax agent and so must lodge the SAR in respect of the 2025 financial year by 31 October2025 and must pay the income tax arising in respect of the 2025 income year by 1 December 2025. Any relevant CGT implications have been ignored in this example.

Application of general rules to hypothetical situation

Event 2 – The income tax liability for the 2025 financial year has been incurred by A and C. Even though A and B were trustees for 90 per cent of the financial year, they bare no liability.

Event 3 – C and D engage the accountant. A contract for services exists between C and D and the accountant. C and D incur liability for the fees payable pursuant to the accountant upon completion of the contracted services.

Event 4 – D and E engage the auditor. A contract for services exists between D and E and the auditor. D and E incur liability for the fees payable pursuant to the auditor upon completion of the contracted services. D and E also paid the accountant’s fees. The accountant is indifferent as to whether C and D pay the fees or whether D and E pay the fees. The payment has discharged the liability of C and D. The accountant’s fees are a proper trust expense and so D and E can pay the fees even though they are not a party to the contract. If the accountant sued C and D for non-payment of fees, C and D would have a full defence to the claim by reason of D and E’s payment based upon either no damage being incurred by the accountant or on the basis the accountant accepted the payment by D and E as a full discharge of the debt.

Event 5 – F and G lodge the SAR and pay the auditor’s fees. While A and C were the trustees immediately before the end of the financial year, once they ceased to be trustees, they also ceased to have any authority to act on behalf of the SMSF. F and G were the trustees at the time the SAR was lodged and they therefore had authority to do so. F and G also authorised the payment of the audit invoice, even though they are not parties to the contract engaging with the auditor, and as the auditor’s fee is a proper trust expense, they have authority to pay the expense. Payment by F and G discharges the liability of D and E under the contract with the auditor and the right of indemnity that arose on the auditor being entitled to the fee is extinguished by the payment of the fee by F and G.

Event 6 – H and Z pay the income tax due in respect of the 2025 financial year on 30 November. This payment discharges the liability of A and C that arose immediately before the end of the 2025 income year. The right of indemnity of A and C in relation to the 2025 income tax debt continued despite the various changes of trustees set out in events 3 to 5 and is now extinguished and A and C cease to have an equitable propriety interest in the assets of the SMSF.

Practical responses

While the system works and delivers the right outcome, life is so much easier with a corporate trustee.

All the membership changes required to make the above example work would still occur, but would not have any practical impact at the taxpayer level. The company would incur the tax liability. At financial year end the company would be liable for the accounting and audit fees and the company would discharge its own income tax liability.

As the properly incurred but not discharged liabilities of the retiring trustees do not automatically transfer to the incoming trustees, the retiring trustees should consider including the following in the documentation effecting retirement and appointment:

• an acknowledgement the retirement of trustees does not extinguish or adversely affect the retiring trustees’ rights of indemnity in respect of properly incurred trust liabilities,

• an express undertaking the incoming trustees will duly and properly attend to the lodgement of the income tax returns of the SMSF,

• the newly appointed trustees will duly and properly discharge all outstanding liabilities incurred by the retiring trustees as and when they are due and payable (possibly the principal liabilities are identified in the documentation) and the incoming trustees agree to impose a similar condition on any future trustees,

• the retiring trustees have rights of access to trust documents and financial statements for the purpose of defending any claim made against them and for the purpose of exercising any right of indemnity they may have, and

• that the above provisions do not limit or prejudice any legal or equitable rights the retiring trustees have by reason of general or statutory law.