5 minute read

The cryptocurrency push

The interest in cryptocurrency investments is growing among SMSF trustees, particularly those of a younger demographic. LightYear Legal SMSF and family wealth protection strategist Grant Abbott examines how to include these types of electronic assets inside a fund.

SMSFs are getting a big following among the under 45s as they look to invest in property and cryptocurrency. Jump on any social media account, particularly YouTube or TikTok, and you will see SMSFs being highlighted as vehicles to transfer superannuation to invest in speculative digital currencies. But it is not that easy as this detailed case study shows.

Meet the crypto enthusiasts

John and Sally hold a combined $220,000 in their respective industry super funds. They have two young children, Josie, 5, and Sam, 2, and in the event of their death, Sally’s mother, June, will act as their guardian.

Their vision is clear. Following research on social media, they decide to establish their own SMSF to allocate a portion of their retirement savings to Bitcoin (BTC) and Ethereum (ETH). Although the influencers they follow make it sound easy, the compliance reality is different.

To this end, we will look at:

1. SMSF macro context – a review of the surge of industry fund members into SMSFs.

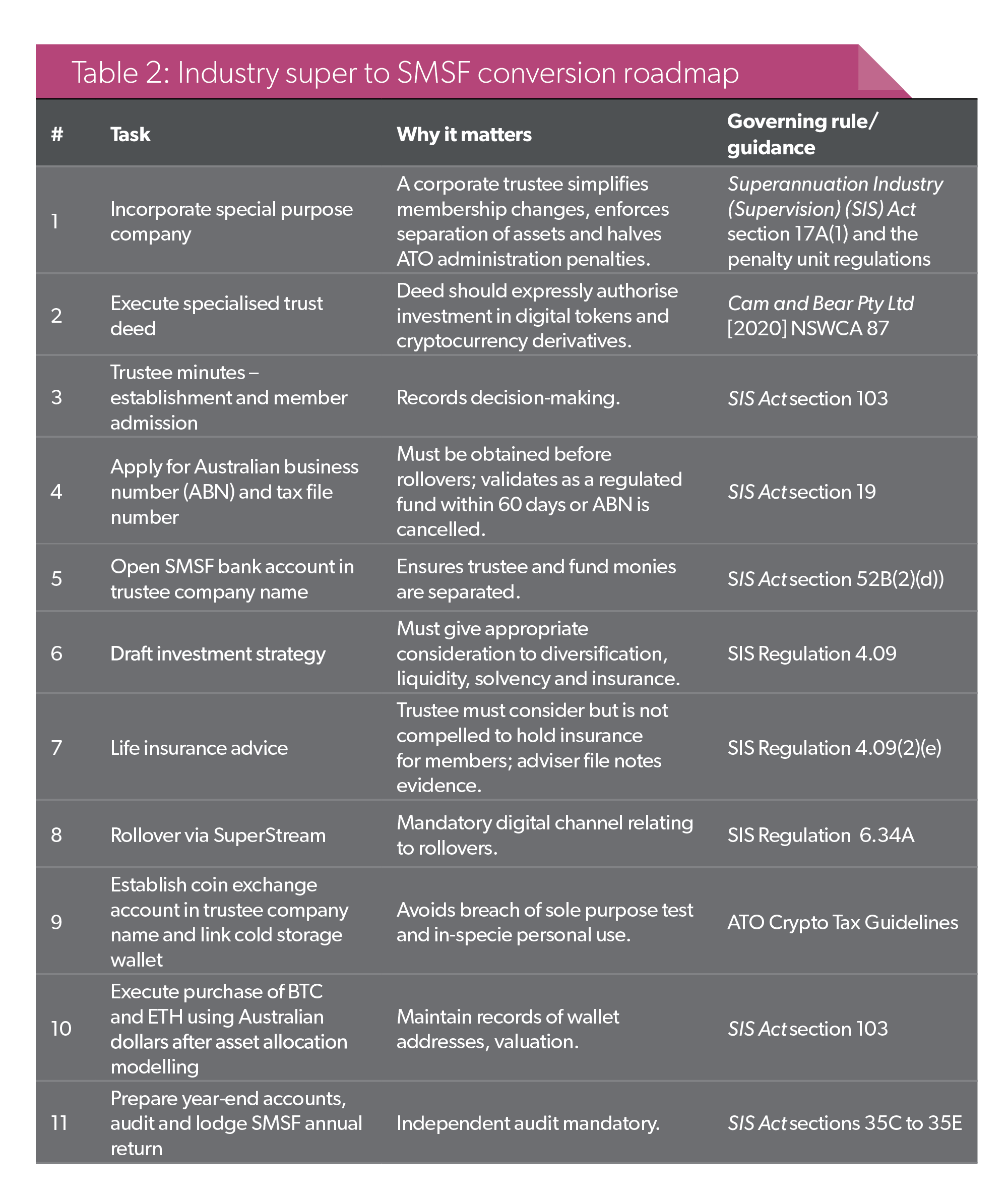

2. The statutory and practical steps to move from an Australian Prudential Regulation Authority (APRA)regulated fund to an SMSF.

3. Why a corporate trustee and a specific trust deed are non-negotiable.

4. How a compliant investment strategy must address digital assets, liquidity, insurance and succession.

5. A data-backed 10-year performance review of BTC and ETH and how it shapes portfolio construction.

6. A project timeline.

7. Comparative case studies regarding relevant advice.

SMSF establishments

Recent analysis and articles show there is a growing trend for the millennial and generation Z cohorts to take more interest in their super than generation X has, reverting to the interest shown by baby boomers. Anecdotally this has been sparked by property and cryptocurrency investments.

According to ATO data, these demographic groups accounted for 24,800 establishments in the 2023 income year and the figure is expected to reach 27,950 in the 2024 financial year, representing 13 per cent year-on-year growth.

Further, the statistics indicated 79 per cent of new SMSF members in the 2024 financial year were 45 years of age or younger – a demographic shift potentially driven by digital asset and property appetite.

Member profile and objectives (see Table 1)

John and Sally wish to:

• control superannuation asset selection,

• maximise their retirement savings,

• gain early exposure to crypto inside super to enjoy the capital gains tax concession, and

• maintain appropriate risk cover and build an estate plan with family wealth protection for their children.

Ten-year performance snapshot to 1 June 2025 (see Table 3)

Volatility remains materially higher than listed equities. Hence trustee minutes must evidence stress testing on downside scenarios, for example, one involving an 80 per cent drawdown, to satisfy SIS Regulation 4.09 and audit scrutiny.

Designing a crypto-compatible investment strategy

SIS Regulation 4.09 requires explicit commentary on:

1. Risk/return: Bitcoin 10-year annualised approximately equal to 78 per cent and Ethereum approximately equal to 105 per cent. Position size limited to 40 per cent of total assets ($88,000) to moderate volatility.

2. Diversification: Retain 60 per cent in broad market exchange-traded funds or listed investment companies for balance.

3. Liquidity: Crypto positions can be liquidated 24 hours a day and seven days a week, however, exchange outages and cold storage latency must be documented in liquidity analysis.

4. Member insurance strategy: Replace or exceed existing cover.

5. Valuation policy: Price feeds from CoinMarketCap (UTC 00:00) converted to Australian dollars at the Reserve Bank of Australia spot.

6. Storage and audit trail: Hardware wallet with seed phrase held in bank vault; duplicate held by June (Sally’s mother and children’s guardian) under sealed deed of confidentiality.

A minute template must record each element and should be revisited quarterly due to price volatility and ensure the current position remains within the bands of the investment strategy.

Risk insurance (see Table 4)

SIS Regulation 4.09(2)(e) only requires consideration and Guidance Statement 009 warns auditors to qualify if no documentary evidence exists. A statement of advice by an Australian financial services licensed insurance broker under the Corporations Act must detail premium funding and claims proceeds allocation.

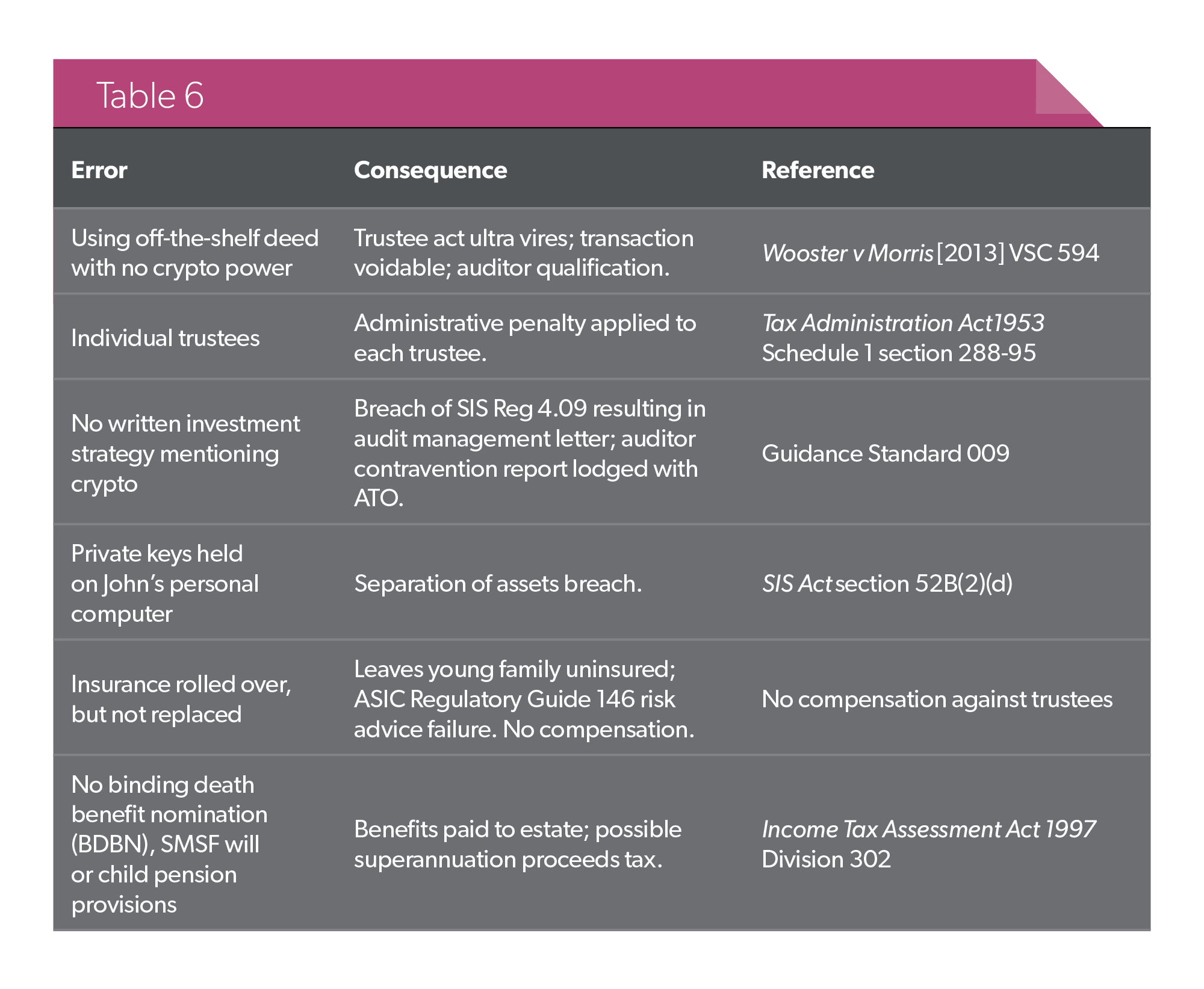

Disaster of doing it yourself (see Table 6)

Penalties resulting from these errors could eventuate in the forced sale of crypto-assets at depressed prices and poor outcomes for the family.

SMSF specialist differentiation

Table 7 illustrates how Level 2 provides holistic protection, preserving value and governance continuity if John and Sally die together.

Conclusion and strategic imperatives

Establishing an SMSF to invest in BTC and ETH is not necessarily a fringe activity, but is becoming a mainstream, regulatorrecognised pathway when executed within the SIS framework and documented under a deed that expressly empowers digital assets. A corporate trustee structure, a cryptoenabling deed, a rigorously documented investment strategy and properly replaced risk cover form the backbone of compliance.

John and Sally’s long-term success and the security of Josie and Sam hinges on professional guidance that extends beyond mere set-up.

With more of the younger generation exiting industry funds in the past few years, John and Sally are joining a surge of trustees who refuse to outsource their investment edge. The regulatory pathway is clear; the strategic upside is compelling; the risks, while real, are entirely manageable when governance is built first and trades come second.

Further, trustees must realise trying to execute any SMSF strategies themselves is a pathway to guaranteed trouble.