10 minute read

An ever-changing landscape

Cooper Partners head of SMSF Jemma Sanderson provides the latest update on transfers from the UK pension framework to the Australian superannuation system.

As many readers of this publication will be aware, the UK pension legislation suffers from as many changes as the Australian superannuation system. This author has penned five articles over the past few years regarding UK transfers with the strategies to implement and the areas of which to be aware. The latest update in that regard was in Issue 046 of this publication, with consideration of the view of His Majesty’s Revenue and Customs (HMRC) on lump-sum payments and also the ATO’s interpretation with respect to the calculation of the applicable fund earnings (AFE).

Since that article in June 2024, there has been further public confirmation of HMRC’s position on lump-sum payments and therefore clarity regarding the strategies from the UK perspective.

A refresh of the UK position

Where an individual has a UK pension account, or multiple accounts, once they reach UK pension age, currently 55 but increasing to 57 imminently, they are able to transfer their pension accounts directly to an Australian SMSF that is a recognised overseas pension scheme (ROPS). Where that occurs, the UK will not withhold any tax provided the individual does not exceed their overseas transfer allowance (OTA). The standard OTA is £1,073,100. Some people may have a higher one, however, that is becoming rarer and since April 2025 the opportunity to apply for a higher OTA has now lapsed.

Where a transfer is in excess of the OTA, HMRC will impose a 25 per cent OTA charge on the amount transferred that is greater than the OTA, which is withheld by the pension scheme at the time of the transfer.

UK locals, that is, tax residents, are taxed on any drawdown from their pension as if it is normal income and so it is effectively fully taxable. The underlying assets in their pension account, however, are not subject to tax. So the difference between the UK and Australia is the British pay no tax on the pension earnings, but full tax on the drawdowns. In Australia we pay tax along the way, but in decumulation phase the drawdown itself is tax-free and the underlying assets may benefit from the tax exemption.

UK locals can also receive what is called a pension commencement lump sum (PCLS) up to one-quarter of their domestic pension, or £268,275, whichever is the lesser. This is tax-free. If the individual is no longer a local but a resident of Australia, they are still eligible for the PCLS, which is still tax-free in the UK, but will often not be from an Australian perspective.

The OTA was introduced from April 2024 where previously it was referred to as the lifetime allowance (LTA). The LTA imposed a 25 per cent charge on benefits not only transferred to another jurisdiction, but also on payments received whether local or not. Since April 2024, when the LTA charge was scrapped and the OTA introduced, it has only been overseas transfers potentially subject to the OTA charge, whereas a local could nominate to receive their pension in the form of a lump sum or regular, or irregular, payments without any further charge, save for the local income tax on payments received.

As outlined in previous articles, namely that from Issue 041, there had previously been the opportunity to transfer an amount to an Australian ROPS and remain within the non-concessional contribution (NCC) cap, with any balance then transferred to the individual directly. With consideration for the double taxation agreement (DTA), this had the outcome of the benefits transferred to the individual as a lump sum not being taxed in the UK (given the DTA and HMRC’s treatment of these payments under the pensions article) with no tax in Australia (as such payments were considered lump sums under the Australian provisions and any AFE was already transferred to the Australian ROPS).

In Issue 046, we identified HMRC’s potential change of interpretation on the above with respect to the lump sum payments and the application of the DTA. Lump sum payments aren’t directly referenced in the Australia/UK DTA and our experience, until December 2023 when we first had wind of this interpretive change, had been that where there was more than one lump sum, HMRC would apply the pensions article to such payments. This means Australia would have the taxing right. The change was that where any payments were lump sums, or akin to a lump sum (anything that wasn’t almost an annuity-type payment/regular payment), HMRC would apply a different DTA article where it would assert its taxing right.

Back then (June 2024) that position had not been finalised, although the change of position was becoming evident more practically where nil tax codes were not being issued by HMRC. Since then, on 12 March 2025, HMRC updated its online resources and confirmed the change of interpretation in this regard.

What does this mean?

As a result of these changes, we now can’t rely on the DTA to transfer substantial amounts directly to individual Australian residents without adverse UK tax implications. In practice, this is what it looks like:

1. HMRC is not issuing new nil tax codes, or where it may do, there are substantial delays in one being issued (12 months or more). This is especially the case where the first payment received is a lump sum and not a pension payment.

2. Without a nil tax code in place with the relevant pension scheme, any payments to the individual are subject to withholding by the pension scheme at UK marginal tax rates and often worse.

3. Even having a nil tax code in place doesn’t prevent HMRC from asserting its taxing right to the payment.

Accordingly, there are substantial ramifications with respect to any one-off payments, akin to lump sums directly to the individual, from a UK scheme.

A refresh of the Australian position

Believe it or not, this side of things remains complex and highly dependent on the timing of when the individual set up their current pension scheme in the UK, whether it was before or after they became a resident. In this regard, we are not talking about their period of service that resulted in the accumulation of benefits in the UK pension environment, but rather the date of establishment of the source scheme from where any transfer to Australia is derived.

Example:

Luke, 58, has been a resident of Australia for 17 years. He has £450,000 in a UK pension scheme. Luke derived that benefit from working for 20 years at a single employer, and when he left 17 years ago, he moved his benefits to a new UK scheme (Scheme 1). He set up the current UK scheme before he was an Australian resident.

When Luke then seeks to transfer his benefits to an Australian ROPS, section 30575 of the Income Tax Assessment Act 1997 (ITAA) will apply to the calculation of the AFE for Luke. Let’s say the ultimate breakdown of his benefits is as per Table 1.

If Luke didn’t want to exceed his NCC, and was happy to drip feed his benefits to Australia (refer to Issue 040 for more details on this option, which is often not preferred as there are superior options), then he might look to transfer the equivalent value of his AFE component, £150,000, plus an amount up to his NCC, let’s say £175,000. Luke would have to transfer the £325,000 to a separate UK scheme (Scheme 2) before transferring to a ROPS, otherwise the £150,000 AFE would be taxable to him.

Where Luke transferred the £325,000 from Scheme 1 to Scheme 2 to the ROPS, he would then have AFE of £150,000 and NCC of £175,000, as intended.

In the situation that Luke had transferred his employment benefits to a new scheme (Scheme 1) after becoming an Australian resident, say right now he moves from the employer defined benefit scheme to a new scheme, the position is quite different when the above strategy is implemented, due to a different provision of section 305-75 of the ITAA.

Luke’s transfers would be as follows:

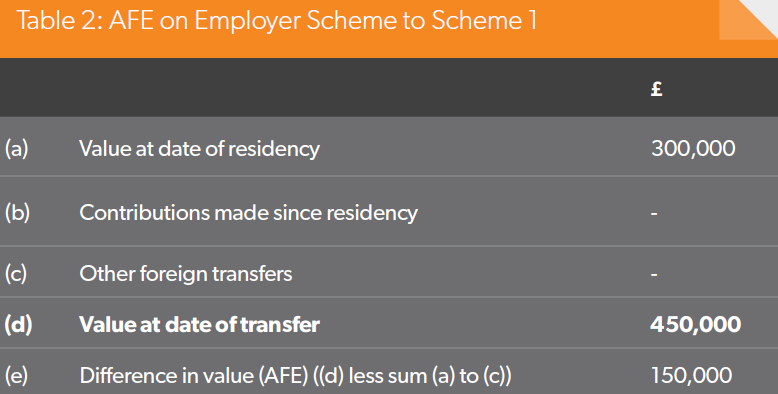

Employer Scheme to Scheme 1: £450,000

Scheme 1 to Scheme 2: £325,000

Scheme 2 to ROPS: £325,000

If Luke transferred £325,000 from Scheme 1 to Scheme 2 to then subsequently transfer to the ROPS, the AFE on the ultimate transfer would be £275,000, calculated as in Table 2.

As the above AFE amount of £150,000 is deferred as Luke has transferred his benefits from a foreign scheme to another foreign scheme, it is then classified as previously exempt fund earnings (PEFE) within Scheme 1.

When £325,000 is transferred from Scheme 1 to Scheme 2, the AFE on that transfer is as per Table 3, where that transfer by itself has an AFE calculation undertaken, as well as the addback of any PEFE.

Item (f) in Table 3 is then the PEFE in Scheme 2. When Scheme 2 is then transferred to the ROPS, the numbers are as per Table 4.

The above arises due to the timing of when Luke sets up his UK schemes and undertakes any transfers once he is a resident of Australia. As per the previous article in Issue 046, this is a change in interpretation by the ATO and as is evident can have a substantial impact on the transfer to the ROPS as there would be a much higher assessable component and a lower NCC component (now only £50,000). This is not as intended.

The ATO’s view with respect to the above is as outlined in several private binding rulings and appears to be the approach the author has experienced since being aware of this interpretation by the regulator in December 2023.

The outcome

Given the above HMRC and ATO positions, highly summarised above (and the application of the provisions to every individual is different, depending on their circumstances), we recommend caution is exercised with respect to any partial transfer of benefits from the UK to Australia as the expected AFE calculation, and therefore the tax payable, could be substantially higher than expected. In Luke’s situation it amounts to a $37,500 additional liability in his ROPS.

Further, we would suggest any transfers of benefits to Australia are undertaken to ROPS from the UK scheme, and not to the individual, as one or more lump sums directly. This includes those with respect to a PCLS as, although that might be tax-free in the UK, it could be fully taxable in Australia.

Let’s say Luke wanted to take a PCLS from his account prior to any transfer. He would be eligible to withdraw £112,500 (one-quarter of £450,000) that would be tax-free in the UK. However, that entire amount ($225,000 equivalent) would be taxable in Australia in his own name at his marginal tax rate. If that was his only income in Australia, that is still about $72,000 in tax to be paid.

Strategies – a new hope

There are some strategic opportunities with respect to the above positions to contemplate, however, they come with timing, taxation and transaction cost considerations. Specialist advice is recommended and the application of the provisions of the ITAA will be different for each individual.

Notwithstanding that the above is confusing, there is clarity on the position on both sides to enable transfers with some certainty.