TEST BANK FOR ACCOUNTING PRINCIPLES, VOLUME 2, 10TH CANADIAN EDITION JERRY J. WEYGANDT, PAUL D. KIMMEL, JILL E. MITCHELL, VALERIE WARREN, LORI NOVAK CHAPTER 9-18

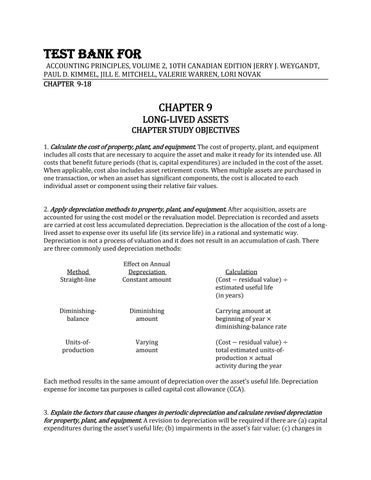

CHAPTER 9 LONG-LIVED ASSETS CHAPTER STUDY OBJECTIVES 1. Calculate the cost of property, plant, and equipment. The cost of property, plant, and equipment includes all costs that are necessary to acquire the asset and make it ready for its intended use. All costs that benefit future periods (that is, capital expenditures) are included in the cost of the asset. When applicable, cost also includes asset retirement costs. When multiple assets are purchased in one transaction, or when an asset has significant components, the cost is allocated to each individual asset or component using their relative fair values. 2. Apply depreciation methods to property, plant, and equipment. After acquisition, assets are accounted for using the cost model or the revaluation model. Depreciation is recorded and assets are carried at cost less accumulated depreciation. Depreciation is the allocation of the cost of a longlived asset to expense over its useful life (its service life) in a rational and systematic way. Depreciation is not a process of valuation and it does not result in an accumulation of cash. There are three commonly used depreciation methods:

Method Straight-line

Effect on Annual Depreciation Constant amount

Diminishingbalance

Diminishing amount

Carrying amount at beginning of year × diminishing-balance rate

Units-ofproduction

Varying amount

(Cost − residual value) ÷ total estimated units-ofproduction × actual activity during the year

Calculation (Cost − residual value) ÷ estimated useful life (in years)

Each method results in the same amount of depreciation over the asset’s useful life. Depreciation expense for income tax purposes is called capital cost allowance (CCA). 3. Explain the factors that cause changes in periodic depreciation and calculate revised depreciation for property, plant, and equipment. A revision to depreciation will be required if there are (a) capital expenditures during the asset’s useful life; (b) impairments in the asset’s fair value; (c) changes in