APPENDIX B SELECTED TOPICS TOPIC 1: INVESTMENTS ASSIGNMENTS B1–1 Held-to-maturity, trading, and available-for-sale securities

B1–2 The primary objective of investing in held-to-maturity securities is to earn interest revenue and collect the face value of the security at its maturity date.

B1–3 Cost method

B1–4 Held-to-maturity securities that will mature within one year are reported as current assets. Securities maturing beyond one year are reported as long-term assets.

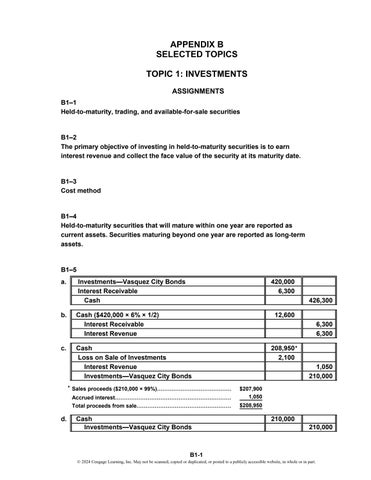

B1–5 a.

b.

c.

Investments—Vasquez City Bonds Interest Receivable Cash

420,000 6,300

Cash ($420,000 × 6% × 1/2) Interest Receivable Interest Revenue

12,600

Cash Loss on Sale of Investments Interest Revenue Investments—Vasquez City Bonds

208,950* 2,100

426,300

6,300 6,300

1,050 210,000

* Sales proceeds ($210,000 × 99%)……………………………………

$207,900 1,050 Accrued interest………………………………………………………… $208,950 Total proceeds from sale………………………………………………

d.

Cash Investments—Vasquez City Bonds

210,000 210,000

B1-1 © 2024 Cengage Learning, Inc. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.