Dr. Joseph J. French (Joe) joined AIT as an Associate Professor in 2024. Before joining AIT, Joe held the position of Professor of Finance at the Monfort College of Business at the University of Northern Colorado. Throughout his 16-year tenure in Colorado, he assumed various roles, including the Department Chair of Finance and the Tointon Chair of Research. Joe currently holds the position of Professor Emeritus at the University of Northern Colorado.

Joe obtained a PhD in financial economics from the University of New Orleans and an MBA from Clemson University. His research interests are in the areas of international finance, corporate finance, and developmental economics, with publications in leading academic journals such as the Journal of Empirical Finance, Journal of Financial Services Research, Emerging Markets Review, and International Review of Financial Analysis. Joe has had the opportunity to conduct research and teach worldwide. He is currently an Extraordinary Professor at the University of the Western Cape in South Africa and has been a visiting professor at universities throughout the world including: Hitotsubashi University, Copenhagen Business School, Shanghai International Studies, University of Trieste, among several others.

Uncertainty and International Fund Flows: A Cross-Country Analysis

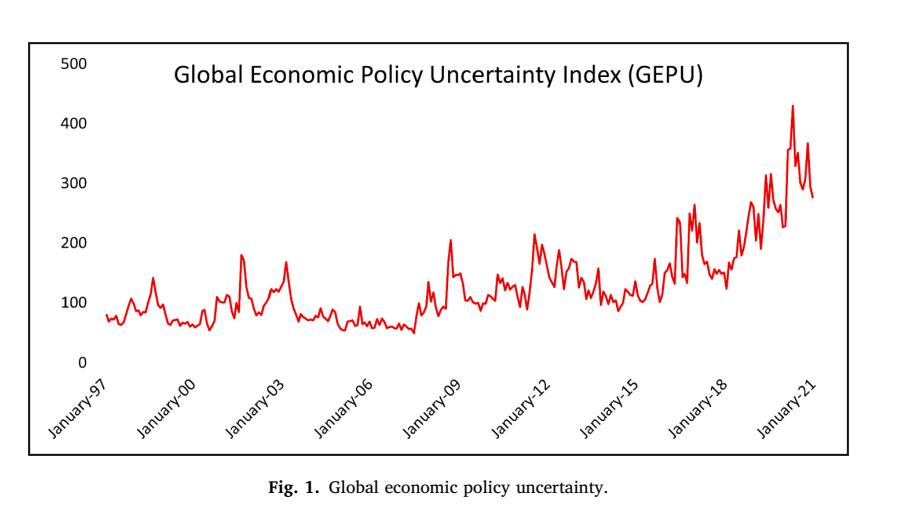

Project Description: Investigates the impact of uncertainty on international fund flows in 27 countries, focusing on the influence of country-level and global uncertainties on equity fund flows

Objectives: Study the effects of economic and geopolitical uncertainties on fund flows and examine fund behavior under various global uncertainty conditions.

Research Outcomes: Demonstrated a positive link between uncertainties and equity fund flows. Identified more pronounced vulnerability to high global uncertainty in emerging markets compared to developed ones.

Social Impact: Provides important information for managing risks in international capital flows, aiding policymakers and investors. Advanced economic modeling to predict global capital movements in response to political and economic changes.

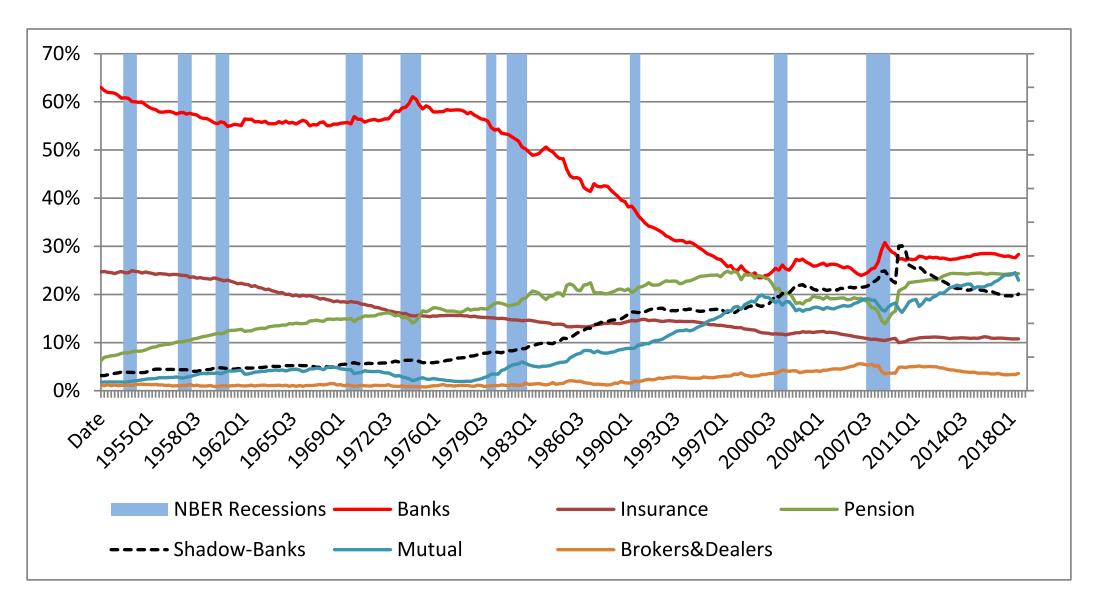

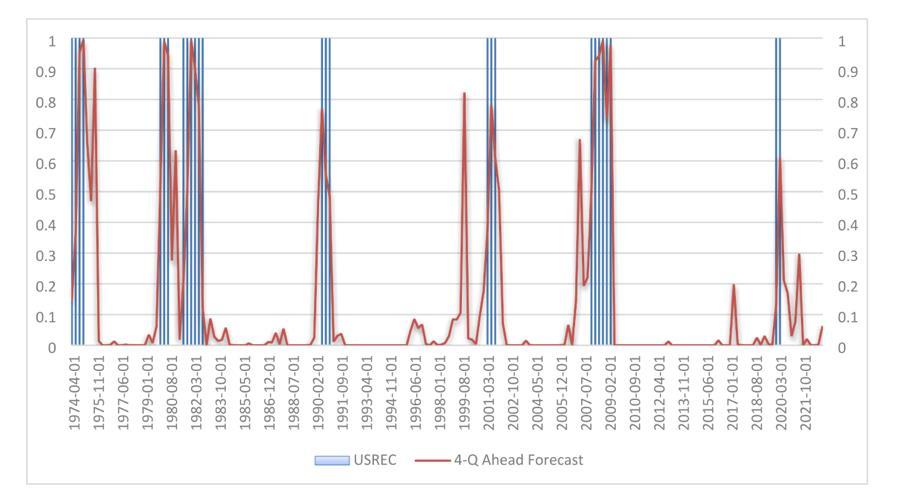

Project Description: The study examines the role of various types of financial intermediaries in predicting business cycles. It distinguishes between traditional banking and emerging market-based intermediaries.

Objectives: To assess the predictive power of various financial intermediaries on business cycles. To Evaluate the impact of different financial intermediaries on economic indicators using multiple decades of data.

Research Outcomes: Demonstrated that aggregate FI assets are a robust predictor of business cycles. While bank and shadow bank assets provide limited predictive power individually, their aggregate contributions are significant.

Social Impact: Provides important insights for policymakers and investors on the significance of FI in economic forecasting and policy formulation. Work supports the development of strategies to enhance financial system stability through better understanding of FI roles.

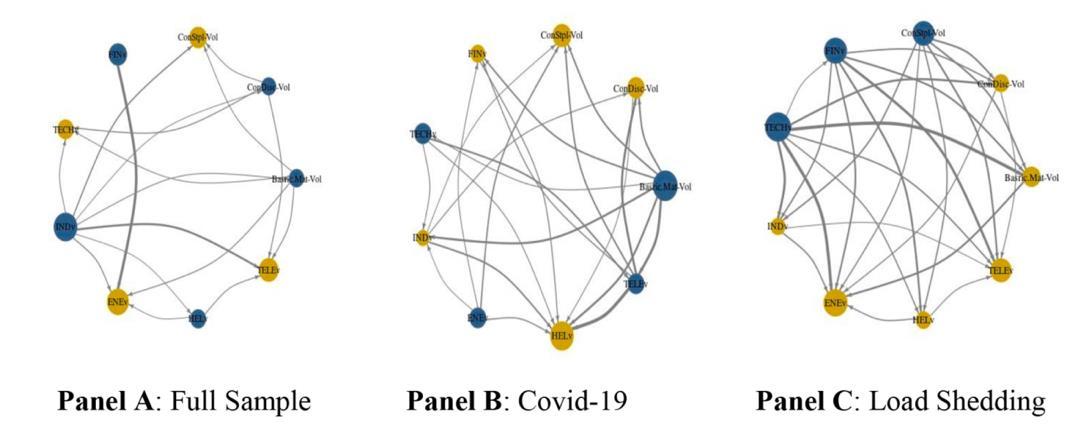

Stock Market Connectedness During an Energy Crisis: Evidence from South Africa

Project Description: This research analyzes the volatility connectivity within the South African equity market during significant domestic and global crises, particularly the local energy crisis (loadshedding) and the global COVID-19 pandemic.

Objectives: Assess the interconnectedness between different sectors within the Johannesburg Stock Exchange during crises. Compare the influence of global and domestic crises on market connectedness.

Research Outcomes: Identified increased market interconnectedness during the COVID-19 pandemic with global markets, while during load-shedding, the JSE showed a detachment from international markets. Results demonstrated the financial and energy sectors as consistent net receivers and transmitters of shocks, showing their systemic importance.

Social Impact: Provides critical insights for risk management and policy formulation, particularly in developing tailored strategies to mitigate financial risks during crisis periods. Work has improved the understanding of the resilience and vulnerability of national markets in the face of both global and localized crises, supporting more informed decision-making by stakeholders.

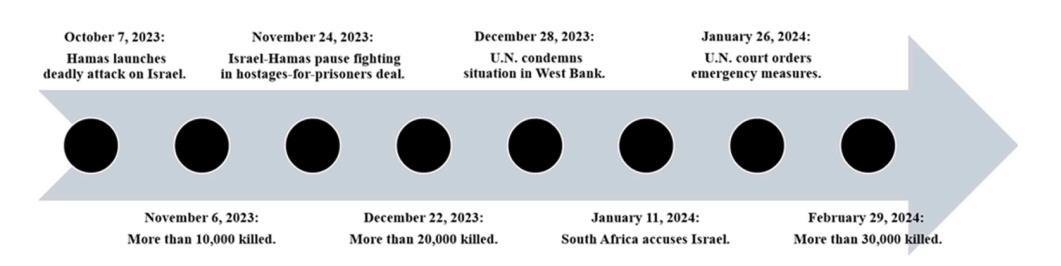

Project Description: This study investigates the impact of student protests and geopolitical events on firms targeted for divestment during the 2023–2024 Israel–Hamas conflict. Using event study methodology, it analyzes the cumulative abnormal returns (CARs) of these firms during key conflict periods, capturing market reactions to activism and geopolitical upheavals.

Objectives: Quantify the market's response to divestment actions against firms with connections to geopolitical conflicts. Evaluate the temporary versus sustained impact of public protests on corporate value.

Research Outcomes: Findings show positive CARs for targeted firms at the onset of the conflict but significant negative CARs as student protests escalated. Evidence suggests a recovery in CARs post-protest, indicating a limitation to the sustained impact of activism on firm valuation.

Social Impact: Offers insights into the tangible impacts of public pressure campaigns on corporate valuations. Aids stakeholders in understanding how market perceptions are influenced by social and political movements, potentially guiding more informed corporate and investment strategies.

Reassessing the Inversion of the Treasury Yield Curve as a Sign of U.S. Recessions: Insights from the Housing and Credit Markets

Project Description: The study reassesses the predictive power of the Treasury yield curve inversion for U.S. recessions by incorporating additional indicators like house prices, residential investment, bank liquidity creation, and corporate credit spreads.

Research Outcomes: Found that house prices and credit spreads are reliable predictors of recessions, with declines in house prices and rises in credit spreads preceding recessions. Demonstrated that residential investment is less robust as a recession predictor compared to house prices.

Social Impact: Improves the understanding of recession forecasting, aiding policymakers and financial analysts in developing more effective economic strategies. The finds support the formulation of monetary policies that consider a wider range of economic indicators beyond the traditional yield curve.

This work examines how economic uncertainty and market power influence the intermediation efficiency of Indonesian banks, measuring inefficiency through the Net Interest Margin (NIM). Utilizing a stochastic frontier approach on data from 91 banks between 2012 and 2023, preliminary findings show that economic uncertainty and market power collectively increase inefficiencies, especially during the COVID-19 period. Larger banks exhibit a stabilizing effect amidst financial stress, albeit at the cost of heightened inefficiencies during stable periods. The study implies significant inefficiencies within government banks compared to private ones, emphasizing the need for policies that enhance competition and manage economic uncertainty effectively.

This ongoing research explores the risk management capabilities of energy hedge funds amidst various market uncertainties using GARCH-family models. The preliminary analysis reveals a consistent negative relationship between the idiosyncratic volatility of these funds and economic, climate, and energy market uncertainties, demonstrating their effective hedging abilities. Additionally, trendfollowing strategies in bond and commodity markets exhibit significant risk reduction properties, particularly during periods of high uncertainty, which shows their role in stabilizing fund performance against market volatilities.

This work explores how government-guaranteed loans affect banks' loan loss provisions in Japan, highlighting a decrease in provisions with increased use of guaranteed loans due to their risk-reducing effects. Conversely, higher payouts from guaranteed loans indicate future increased default risks, leading banks to increase provisions. The preliminary analysis, focused on data from Japanese banks between 2012 and 2023, demonstrates the contrasting effects of guaranteed loans and their payouts on bank behavior, particularly during the expansion of these programs following the COVID-19 pandemic.

This ongoing research investigates the impact of the 2022 Russian invasion of Ukraine on stock market performance, focusing on firms with varying levels of environmental, social, and governance (ESG) commitments. Surprisingly, early results show that firms with low ESG scores that remained passive during the conflict outperformed the market, while those with high ESG ratings underperformed, regardless of their response strategy. The research suggests that the market rewarded non-responsive low ESG firms due to reduced competition and lack of penalties for inaction, whereas high ESG firms were penalized for their responses, viewed as redundant or negatively impacting cash flow. The findings highlight a shift in how geopolitical risks influence market dynamics, challenging traditional views on ESG investment during crises.

We examine the critical role of domain knowledge in improving the predictive accuracy of machine learning (ML) algorithms for forecasting bank failure rates. Through a quasi-natural experiment, it was found that ML algorithms generally outperform traditional predictive OLS models using specific predictors. Incorporating key variables identified by ML into predictive models shows statistical significance, though caution is advised as some ML predictions may contradict economic intuition. Our preliminary work shows the importance of combining domain expertise with ML predictions to make informed policy decisions and investment choices, particularly in complex financial environments.