COMERICA, INC. (CMA) Comerica Incorporated, through its subsidiaries, provides financial, products and services primarily in three major US markets. The company operates in three major US markets. The company operates in three segments: Business Bank, Retail Bank, and Wealth Management.

Key Statistics (As of December 2014) P/E (TTM) 14.14 Fwd P/E 13.3 P/S 3.3

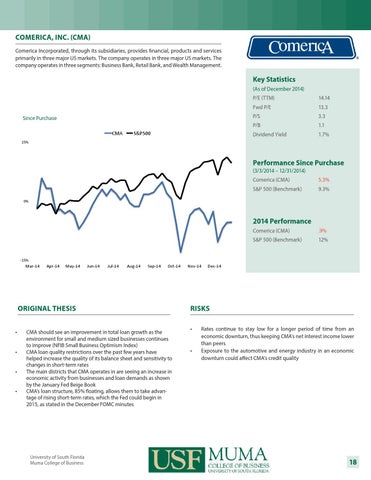

Since Purchase

P/B 1.1 CMA

S&P500

Dividend Yield

1.7%

15%

Performance Since Purchase (3/3/2014 – 12/31/2014) Comerica (CMA)

5.3%

S&P 500 (Benchmark)

9.3%

0%

2014 Performance Comerica (CMA)

.9%

S&P 500 (Benchmark)

12%

-‐15%

Mar-‐14

Apr-‐14

May-‐14

Jun-‐14

Jul-‐14

Aug-‐14

Sep-‐14

Oct-‐14

ORIGINAL THESIS • • • •

CMA should see an improvement in total loan growth as the environment for small and medium sized businesses continues to improve (NFIB Small Business Optimism Index) CMA loan quality restrictions over the past few years have helped increase the quality of its balance sheet and sensitivity to changes in short-term rates The main districts that CMA operates in are seeing an increase in economic activity from businesses and loan demands as shown by the January Fed Beige Book CMA’s loan structure, 85% floating, allows them to take advantage of rising short-term rates, which the Fed could begin in 2015, as stated in the December FOMC minutes

University of South Florida Muma College of Business

Nov-‐14

Dec-‐14

RISKS •

•

Rates continue to stay low for a longer period of time from an economic downturn, thus keeping CMA’s net interest income lower than peers Exposure to the automotive and energy industry in an economic downturn could affect CMA’s credit quality

18