15

Chapter I. Global economic outlook

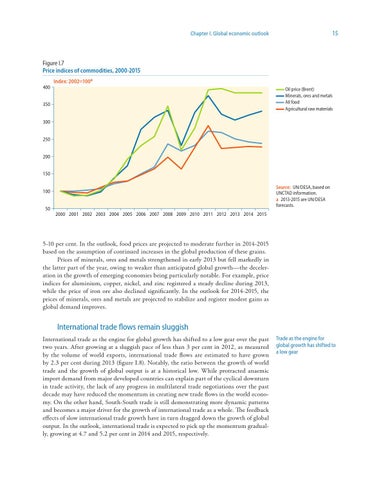

Figure I.7 Price indices of commodities, 2000-2015 Index: 2002=100a 400

Oil price (Brent) Minerals, ores and metals All food Agricultural raw materials

350 300 250 200 150

Source: UN/DESA, based on UNCTAD information. a 2013-2015 are UN/DESA forecasts.

100 50 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

5-10 per cent. In the outlook, food prices are projected to moderate further in 2014-2015 based on the assumption of continued increases in the global production of these grains. Prices of minerals, ores and metals strengthened in early 2013 but fell markedly in the latter part of the year, owing to weaker than anticipated global growth—the deceleration in the growth of emerging economies being particularly notable. For example, price indices for aluminium, copper, nickel, and zinc registered a steady decline during 2013, while the price of iron ore also declined significantly. In the outlook for 2014-2015, the prices of minerals, ores and metals are projected to stabilize and register modest gains as global demand improves.

International trade flows remain sluggish International trade as the engine for global growth has shifted to a low gear over the past two years. After growing at a sluggish pace of less than 3 per cent in 2012, as measured by the volume of world exports, international trade flows are estimated to have grown by 2.3 per cent during 2013 (figure I.8). Notably, the ratio between the growth of world trade and the growth of global output is at a historical low. While protracted anaemic import demand from major developed countries can explain part of the cyclical downturn in trade activity, the lack of any progress in multilateral trade negotiations over the past decade may have reduced the momentum in creating new trade flows in the world economy. On the other hand, South-South trade is still demonstrating more dynamic patterns and becomes a major driver for the growth of international trade as a whole. The feedback effects of slow international trade growth have in turn dragged down the growth of global output. In the outlook, international trade is expected to pick up the momentum gradually, growing at 4.7 and 5.2 per cent in 2014 and 2015, respectively.

Trade as the engine for global growth has shifted to a low gear