11

Chapter I. Global economic outlook

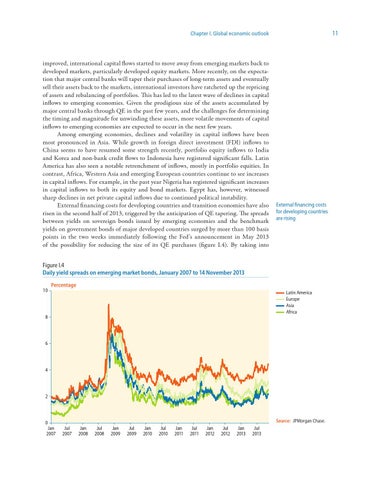

improved, international capital flows started to move away from emerging markets back to developed markets, particularly developed equity markets. More recently, on the expectation that major central banks will taper their purchases of long-term assets and eventually sell their assets back to the markets, international investors have ratcheted up the repricing of assets and rebalancing of portfolios. This has led to the latest wave of declines in capital inflows to emerging economies. Given the prodigious size of the assets accumulated by major central banks through QE in the past few years, and the challenges for determining the timing and magnitude for unwinding these assets, more volatile movements of capital inflows to emerging economies are expected to occur in the next few years. Among emerging economies, declines and volatility in capital inflows have been most pronounced in Asia. While growth in foreign direct investment (FDI) inflows to China seems to have resumed some strength recently, portfolio equity inflows to India and Korea and non-bank credit flows to Indonesia have registered significant falls. Latin America has also seen a notable retrenchment of inflows, mostly in portfolio equities. In contrast, Africa, Western Asia and emerging European countries continue to see increases in capital inflows. For example, in the past year Nigeria has registered significant increases in capital inflows to both its equity and bond markets. Egypt has, however, witnessed sharp declines in net private capital inflows due to continued political instability. External financing costs for developing countries and transition economies have also risen in the second half of 2013, triggered by the anticipation of QE tapering. The spreads between yields on sovereign bonds issued by emerging economies and the benchmark yields on government bonds of major developed countries surged by more than 100 basis points in the two weeks immediately following the Fed’s announcement in May 2013 of the possibility for reducing the size of its QE purchases (figure I.4). By taking into

External financing costs for developing countries are rising

Figure I.4 Daily yield spreads on emerging market bonds, January 2007 to 14 November 2013 10

Percentage Latin America Europe Asia Africa

8

6

4

2

0

Jan 2007

Source: JPMorgan Chase. Jul 2007

Jan 2008

Jul 2008

Jan 2009

Jul 2009

Jan 2010

Jul 2010

Jan 2011

Jul 2011

Jan 2012

Jul 2012

Jan 2013

Jul 2013