Ramanan Krishnamoorti is the Vice President of Energy and Innovation at the University of Houston. He has served as chair of the Cullen College of Engineering’s chemical and biomolecular engineering department and associate dean of research for the Cullen College of Engineering. He is a professor of chemical and biomolecular engineering, with affiliated appointments as a professor of petroleum engineering and chemistry. Dr. Krishnamoorti earned his bachelor’s degree in chemical engineering from the Indian Institute of Technology Madras and his doctoral degree in chemical engineering from Princeton University.

Aparajita Datta is a researcher at UH Energy and a Ph.D. candidate in Political Science at the University of Houston. Her dissertation evaluates the policy feedback effects of means-tested home energy assistance programs. Datta holds a bachelor's degree in computer science and engineering from the University of Petroleum and Energy Studies, India, and master’s degrees in energy management from the C. T. Bauer College of Business, in public policy from the Hobby School of Public Affairs, and political science from the College of Liberal Arts and Social Sciences at the University of Houston.

Contributors

The initiative was led by faculty and staff with expertise in energy, sustainability, and carbon management.

CCUS

Charles McConnell and Connor Thompson

Electric Grid

Connor Thompson

Transportation

Dr. Ramanan Krishnamoorti and Aparajita Datta

Workforce Development

Dr. Ramanan Krishnamoorti, Dr. Suryanarayanan Radhakrishnan, and Aparajita Datta

Financial Incentives

Greg Bean

In addition, a multidisciplinary team of 25 undergraduate and graduate students supported this research initiative:

Mindy Abraham

Prajakta Andhale

Rodrigo Carrizales

Pradyumna Ghosh

Claire Gregory

Mohamed Hawter

Eva Jiang

Griffin King

Sheetal Kumar

Carolina Lopez-Herrera

Anam Masood

Ducanh Nguyen

Deborah Nkagbu

Toni Rask

Chandrama Ray

Shelby Riney

Mykyta Rudskyi

Namira Rupani

Rodrigo Salcido

Ellya Saudale

Juan Schlief

Teja Satya Sai Varma

Cydnee Willingham

Sai Udaya Meghana Yella

Hammad Yousaf

The white papers from each focus area are available at: https://uh.edu/uh-energy-innovation/uh-energy/energyresearch/netzero-by-2050/white-papers/

Acknowledgments

The research initiative was generously supported by the Cullen Trust for Higher Education. We thank Corbin Robertson for his continuous engagement, feedback, and support of our work. We are grateful to our UH Energy colleagues – Dr. Deidra Perry, Ed Bailey, Jeannie Kever, Dr. Joe Powell, and Paul Doucette – for their continuous support and feedback. The project could not have been successful without input, engagement, and support from our colleagues across the University of Houston.

We thank Dr. Pablo Pinto, Dr. Sunny Wong, Dr. Gail Buttorff, Margaret Kidd, Dr. Funda Sahin, Dr. Christine Ehlig-Economides, Gina Warren, Dr. Norm Johnson, and Rashda Khan. Our Energy Advisory Board member, Scott Nyquist, has been a great champion of the project. We are also grateful to all the panelists who participated in our Net-Zero Texas by 2050 Symposium in December 2022. An enormous thank you to our colleagues at University Marketing and Communications – Nancy Blair, Shawn Lindsey, Greg Ortiz, Benjamin Corda, and Marcus Allen –for their work on this white paper.

Executive Summary

The cliché is that everything is bigger in Texas, and that is certainly true when it comes to energy. Texas is the nation’s top energy-producing state, the top energy-exporting state, and the largest consumer of energy. It leads the nation in carbon dioxide emissions, responsible for 14% of all U.S. CO2 emissions. Slightly more than one-third of those emissions come from the state’s industrial sector, including refineries, petrochemical plants, and other manufacturing facilities. Another third comes from transportation, including trucks, trains, and ships that move products made in Texas across the nation and the world.

Getting to net zero by 2050 – that is, ensuring all climatedamaging emissions are eliminated or captured and permanently stored – is a daunting goal. It will be expensive, and success is not guaranteed. But Texas is uniquely positioned to lead the energy transition, and cutting-edge research and innovation happening in the state today will shape the net-zero world of the future. Efforts now will allow the state to continue its legacy of advancing U.S. energy security while making progress on national climate goals and building a healthier, resilient, and equitable society.

What will it take to get there? Efforts to decarbonize the state must meet three concurrent goals: ensuring affordable, reliable, and sustainable energy for all; preserving and improving the quality of life for Texans as demographics rapidly change and the state’s population grows to 50 million people by 2050; and maintaining and strengthening the state’s global leadership in the energy industry.

To consider how the state can reach those goals, we focused on four areas: carbon capture, utilization, and storage (CCUS); the electric grid; transportation; and the future workforce. For each, we considered a variety of scenarios, including a business-as-usual approach which assumes no major policy shifts or changes in the energy mix; an approach calling for more renewable energy and curtailing the use of fossil fuels; and an all-of-the-above strategy focused on eliminating emissions regardless of the source.

Policy mandates vary by scenario. The most aggressive approach for the transportation sector, for example, would require all new vehicles sold in the state by 2040 to be zero-emission vehicles. There are viable pathways to reach net zero over the next 25 years, with a price tag that could approach $2 trillion – including investments in new technologies, infrastructure expansions to enable CCUS

Texas is uniquely positioned to lead the energy transition, and cutting-edge research and innovation happening in the state today will shape the net-zero world of the future.

at scale, the installation of charging infrastructure for the anticipated growth of electric vehicles, remediation for gas station sites that are no longer needed, construction of new power generation facilities, and job retraining programs to ensure workers can benefit from the transition. A business-as-usual trajectory will not get us there. In fact, our work suggests the energy workforce will shrink and lead to economic losses for the state under such a scenario. regardless of the policies Texas chooses to pursue. Coal and natural gas-related jobs could drop by 90% as technological changes, shifts in global demand, and the failure to leverage upskilling and reskilling opportunities for the current workforce upend the industry.

Instead, the state stands to gain the most, in terms of lower emissions and more jobs and economic benefits, from an all-of-the above strategy, in which the focus is on reducing emissions through a diversified energy mix rather than favoring one source of energy over another. (Coal is the exception; its share of the energy mix continues to fall under all scenarios.) We found that approach could lead to two million new jobs in Texas by 2050, accommodating growth in the renewables sector, as well as in CCUS, liquid fuels, biomass, and hydrogen.

Efforts to decarbonize the state must meet three concurrent goals:

Ensuring affordable, reliable, and sustainable energy for all

Preserving and improving the quality of life for Texans as demographics rapidly change and the state’s population grows to 50 million people by 2050

Carbon Management

Carbon management through CCUS and other CO2 removal methods like direct air capture will be required to decarbonize the electric grid and industrial sectors. Our research suggests between 212 million tons and 362 million tons of CO2 can be sequestered annually in Texas through the use of CCUS, direct air capture, and changes to agricultural practices.

Importantly, we found about 63% of emissions analyzed in our work can be captured at no additional cost to the emitter, given current capital costs, input costs, and available tax incentives. Nevertheless, obstacles such as access to pipelines, storage fields, storage permitting, labor, and capital could delay these projects. Abating the remaining 37% will cost between $100 and $900 per metric ton of CO2 – on average about $60 billion annually.

While some of the needed infrastructure is already in place, and the state’s geology offers ample options to safely and permanently store large amounts of CO2, substantial additional work and investment are needed if CCUS is to live up to its promise. Systematic efforts at community engagement also will be needed to reduce community

Maintaining and strengthening the state’s global leadership in the energy industry

concerns about long-term safety and other liabilities. Additional policy requirements include supplementing the current federal 45Q tax credits for carbon management, reducing regulatory, societal, financial, and technical barriers to safe transportation and permanent storage, regulatory guidance on ownership rights to subsurface pore space, and the state gaining primary enforcement authority, or primacy, over Class VI wells.

Between 212 million tons and 362 million tons of CO2 can be sequestered annually in Texas.

The Electric Grid

CCUS and other carbon management strategies will be essential to achieving a net-zero electric grid, which in turn will be a critical piece of the state’s path toward an emission-neutral future.

Simply put, efforts by industry, transportation, and other sectors to reduce carbon emissions depend on far higher rates of electrification, produced and distributed on an emission-free grid. This shift – from internal combustion vehicles to electric vehicles, for example, and from gas-powered industrial furnaces to those powered by emission-free electricity – suggests the rest of the economy won’t be able to achieve its net-zero goals if the electric grid can’t deliver.

The grid must be able to reliably deliver more electricity than ever before, without the climate-damaging emissions currently associated with the power sector. (The sector is the third-largest source of greenhouse gas emissions in Texas, accounting for 27% of all emissions in 2021.)

The good news is that a net-zero grid is possible in Texas, using a balanced energy mix including renewables, natural gas, and hydrogen. That all-of-the-above approach is also the least costly option for a net-zero grid, at about $190 billion in levelized system costs.

While the growth of both wind and solar, along with still relatively low levels of battery storage, have gained significant attention in recent years, natural gas-fired generation will remain important to maintain reliability in the face of fluctuating availability from renewables. Coupling gas-fired plants with CCUS technologies will allow Texas to produce the significant amounts of carbonneutral electricity it will need.

Transportation

Even under the most aggressive policy efforts, the Texas fleet won’t reach net zero by 2050, as older cars and trucks will remain on the road for years. We calculate that transportation-related emissions would remain above 80 million metric tons in 2050, even if the state were to require all new sales by 2040 to be zero-emission vehicles. Still, policy decisions could have a significant impact, hastening the adoption of electric vehicles

and reducing emissions, assuming electric vehicles are charged on a net-zero grid. Electrifying the fleet or producing carbon-neutral fuels using carbon-neutral electricity could reduce rail, aviation, and marine freightrelated emissions by as much as 99%. These shifts will, however, significantly increase demand for minerals and other materials required for electric vehicle batteries, including lithium, cobalt, copper, manganese, and graphite.

None of this will be cheap – the cost of a net-zero transportation system will range from $27 billion to $49 billion, including the cost of charging stations and other infrastructure, environmental remediation at suplus gas stations, and the loss of revenue from fuel taxes.

The good news is that a net-zero grid is possible in Texas, using a balanced energy mix including renewables, natural gas, and hydrogen.

Workforce

Energy-related employment in Texas is sure to change, regardless of which policies the state pursues. But the changes needn’t be frightening if leaders from industry, government, education, and related sectors make thoughtful choices about preparing the future workforce for jobs offered by the energy transition while ensuring retraining programs give current workers the skills needed for these new jobs.

The energy transition will offer important opportunities to address current inequities, ensuring that people aren’t left behind. While the coal, oil, and natural gas sectors are expected to lose jobs under all of the scenarios we studied, other emerging sectors could offer a strong net gain in jobs. In fact, by balancing the growth of renewables and storage with advances in liquid fuels, hydrogen, CCUS and other carbon removal technologies, as many as 2.1 million new jobs could be added by 2050.

Many of those jobs will come from capacity growth in the renewables sector, along with liquid fuels, biomass, and hydrogen. But the bulk of new jobs, as many as 1.4 million, will come from the deployment of CCUS. Many workers from the oil and gas sectors will be able to move into those jobs with appropriate reskilling and upskilling opportunities.

The motivation for our analysis has been the Biden administration’s goal of getting to a net-zero electricity grid in the U.S. by 2035 and an aspiration of net-zero by 2050 for all sectors. Our work is based on the policies and laws announced and implemented during the last threeplus years. In light of the recent elections, we anticipate that Trump will reverse most, if not all, Biden-era energy and climate policies.

Trump believes that the U.S. can achieve energy dominance by focusing on fossil fuel production, removing drilling regulations for oil and gas, and lowering reliance on renewable energy. We expect faster growth in carbon capture adjacent to the fossil fuel industry, accelerated permitting for Class VI wells, and pipelines. The infrastructure to support greater uptake for EVs is also expected to continue to grow.

Sweeping policy changes through executive orders are expected, including eliminating the Justice40 Initiative, stalling federal incentives for green hydrogen and direct air capture hubs, and community solar, along with related workforce development and community engagement opportunities. These will be followed by legislative support from the Congress.

In Texas, there will be greater support for Trump’s policies, and upcoming state policies and proposed regulations will be in line with federal policy priorities. Texas’ legislature will adopt more oil-and-gas friendly legislation, including an increase in state funding for oil and gas use and

the state is expected to benefit from federal efforts to encourage CCUS. The growing solar industry will be stifled, and permitting for new grid capacity will be stymied. There will be limited consideration for what these changes will cost consumers in the long term.

The cost of a net-zero transportation system will range from $27 billion to $49 billion.

As many as 2.1 million new jobs could be added by 2050.

Background

UH Energy and the Center for Carbon Management in Energy evaluated pathways and solutions to help Texas achieve carbon neutrality by 2050, a goal known as net zero. The research initiative examined the feasibility and the techno-economic, carbon, and jobs impacts of various plausible pathways to getting there. We evaluated regulatory and policy initiatives and bottlenecks for these pathways and highlighted the most impactful, most likely, and lowest cost opportunities.

Our work centered around four focus areas: carbon capture, utilization, and storage (CCUS); the electric grid; transportation; and the workforce and talent needed to achieve the goals. The focus on the growth of CCUS, accompanied by other carbon removal technologies including direct air capture (DAC), allowed us to understand the opportunities to decarbonize heavy industries, a sector that accounted for 36% of emissions in 2021 (Figure 1). While the industrial sector will decarbonize with the use of alternative fuels and process improvements over the long term, CCUS will be the key driver for accelerated decarbonization in the short term. The electric grid and transportation sector account for another 60% of 2021 emissions.

Our analysis was based on primary energy consumption. Hence, we assumed changes in the grid would be responsive to any changes in the commercial and residential sectors (4% of emissions in 2021).

Figure 1. Sector shares of energy-related carbon dioxide (CO2) emissions in 2021, representing 664 million metric tons per year (top), and the business-as-usual scenario in 2050, representing 772 million metric tons (bottom).

Data source: U.S. EIA

2050 Emissions-Business as Usual Scenario

We focused on five scenarios to describe the state’s anticipated future energy mix in efforts to reach net zero by 2050. The scenarios are based on pathways for infrastructure development, adjacent industrial development, and potential government policies, incentives, and mandates. The businessas-usual scenario is based on the National Energy Modeling System used in the U.S. Energy Information Administration’s 2022 Energy Outlook. The remaining scenarios are relative growth scenarios for end-use electrification and the diversity of the energy mix.

To develop alternative energy and decarbonization pathways, we considered government policies, including previously employed production and investment tax credits, renewable portfolio standards, renewable energy credit trading programs, and investment in Competitive Renewable Energy Zones (CREZ) and transmission infrastructure, which enabled the growth of the state’s onshore wind capacity over the past two decades.

We assumed the federal and state governments would similarly incentivize the growth of pumped storage; hydrogen production, storage, and its use in fuel cells; solar; thermal; offshore wind; and CCUS and carbon dioxide removal (CDR) systems. In our analysis, these technologies followed the growth pattern of onshore wind. It was assumed that capacity additions of new technologies would become available in 2026, and the scenarios would begin to diverge from the business-asusual (BAU) scenario. Growth rates were adjusted based on relative technology penetration in each scenario compared to the business-as-usual case (Table 1 and Table A1 in Appendix A).

In addition to the business-as-usual case, the scenarios include:

• Scenario 2, which assumes the accelerated conversion of end-use systems that rely on fossil fuels to those powered by carbon-neutral electricity, combined with high growth for all sources of energy and decarbonization technologies. This is the all-of-the-above scenario.

• Scenario 3, which assumes accelerated conversion to electrification, with a moderate to low growth rate for renewables and storage.

• Scenario 4, which also assumes accelerated rates of end-use electrification, with the highest possible growth rate for renewables and storage.

• Scenario 5, which assumes the lowest rate of end-use conversion of fossil-based systems to electricity, coupled with limited diversification of the energy mix and the highest growth for liquid fuels including petroleum, natural gas liquids, and gas-to-liquids, accompanied by commensurate growth in decarbonization technologies like CCUS and CDR.

In these scenarios, grid capacity by 2050 ranged from 207 gigawatts (GW) to 361 GW (Figure 2 and Appendix A).

Table 1. Technology penetration, energy supply scenarios, and year-on-year growth rates relative to the business-asusual scenario (Scenario 1) of the U.S. EIA’s 2022 Energy Outlook.

(Scenario 2)

(Scenario 3)

High End-use Electrification, Unconstrained Renewables and Storage (Scenario 4)

Figure 2. Grid capacity growth between 2022 and 2050 for the represented scenarios: Business-as-usual (scenario 1), High End-use Electrification, Unconstrained Energy Supply (scenario 2), and Low End-use Electrification, Constrained Energy Supply (scenario 5).

Carbon Removal through CCUS and DAC

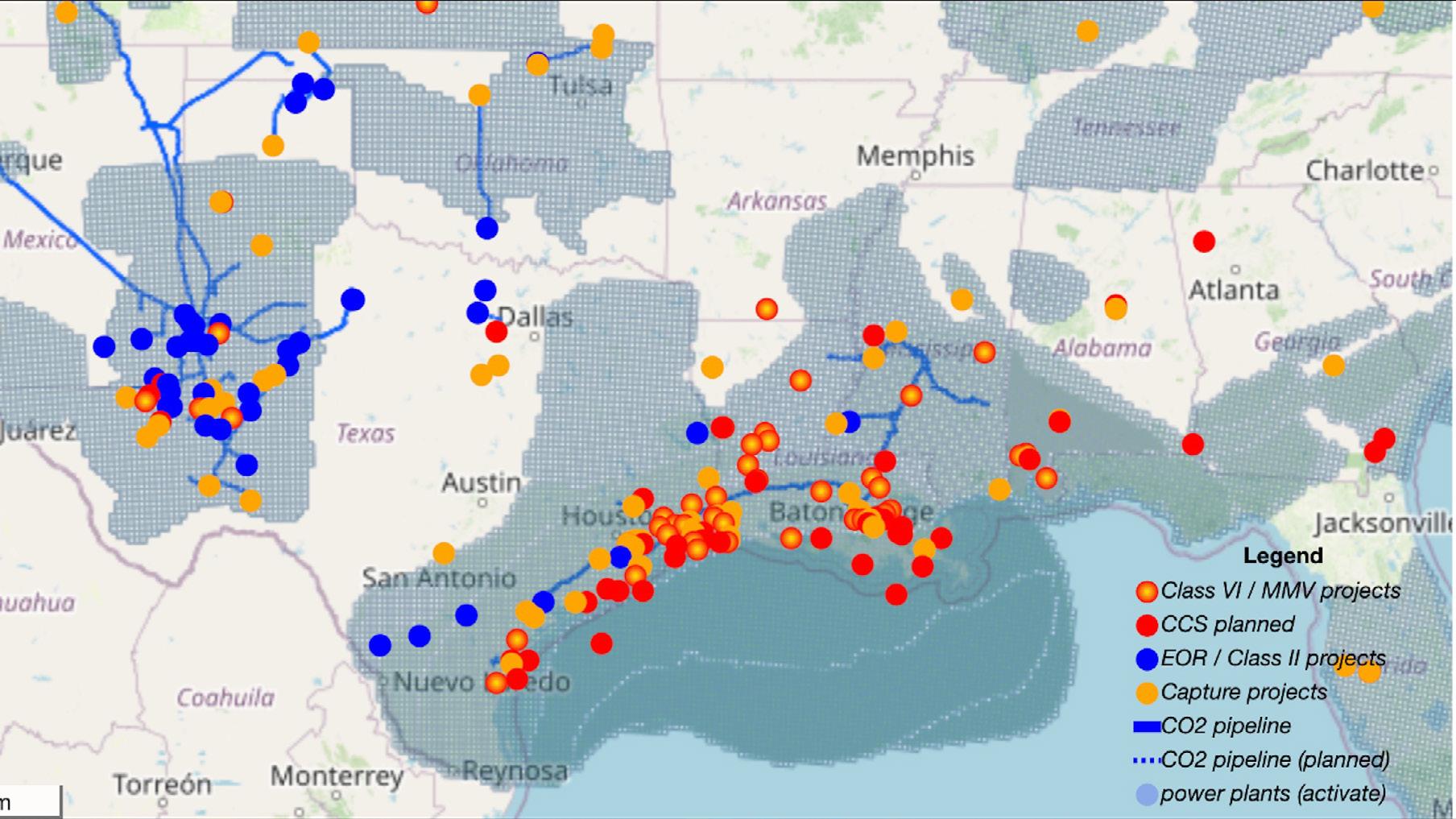

Texas can serve as an opportunity zone for the growing carbon removal industry. We assumed that different CCUS technologies would improve in cost and performance at varying rates under each scenario. We identified proximal sources and sinks for CO2 storage and lowest-cost transportation options based on growth potential in Texas and the provisions of the Inflation Reduction Act (Figure 3). We find that an estimated 212 million to 362 million tons of CO2 can be sequestered annually in Texas with CCUS, DAC, and changes to agriculture processes.

Our key findings are:

• Approximately 255 million tons of CO2 (63% of the emissions analyzed in our work) can be captured without cost to the emitter given current capital costs, input costs, and tax incentives like 45Q. While these projects are economically feasible, obstacles such as access to larger transport pipelines, storage fields, storage permitting, labor, and capital could result in delays.

• Costs to abate the remaining 37% (150 million tons of CO2) of emissions will range from $100-$900 per metric ton of CO2. On average, this would result in a total cost of $60 billion annually.

• Changing agricultural practices could have a significant decarbonization impact, sequestering about 60 million tons of CO2 annually.

• Some of the needed infrastructure for CCUS and DAC is already in place, which would reduce up-front costs and allow projects to collectively share access to infrastructure. However, based on our previous analysis, detailed in CCUS Infrastructure: Preparing for the Future of Houston, stakeholders lack a shared visioni

Other key enablers require action now:

A. Pipelines: Utilization of the Denbury Green Line to connect cluster sources to storage; regulatory support and certainty for onshore and offshore pipeline development; obtaining right of way and permits well in advance for construction projects; and regulatory certainty for CO2 private and common carrier systems.

B. Storage: Texas achieving primacy for Class VI wells; well characterization of announced CCUS projects to determine actual capacity; clarity for offshore storage regulations; and acquisition of offshore land for potential future storage.

C. Electricity: Enhanced utilization of current assets; key investment decisions and strategic planning for future decades; preliminary work for new power plant construction in the next decade. Cogeneration facilities may be necessary by the 2040s, but consideration for development must begin within this decade.

D. Water: The existing water supply should be sufficient for CCUS deployment during the first decade. New water resources, especially surface water reservoirs, will be required in future decades, and work to gain approval must begin early.

• The state’s geology is unmatched for long-term carbon storage, both onshore and offshore. The primary path for large-scale utilization in Texas today is the use of CO2 in enhanced oil recovery (EOR) operations, where an estimated 90%-95% of injected CO2 can be expected to be permanently stored. EOR operations in Texas alone could store up to 4.9 billion metric tons of CO2, while geological sequestration in saline formations may be able to accommodate the storage of an additional 1.4 trillion metric tons of CO2. The combination of EOR and pure storage opportunities gives Texas the capacity to store twice as much carbon dioxide as any other state.

• Challenges remain in terms of the legal and regulatory framework. These include the lack of guidance on ownership rights to subsurface pore space and state primacy over Class VI injection wells. The lack of a price on carbon emissions creates additional challenges.

• Texas needs greater investment in CCUS and DAC. Investment will ensure new projects are launched and infrastructure is developed in the short term, resulting in continued deployment of at-scale emissions reductions and new markets for lowcarbon products over the long term. Investment also will be required to meet the increased energy demands associated with carbon removal technologies.

CO2 Storage Sites

Figure 3. The CO2 storage sites, existing and planned CO2 pipelines in the Permian Basin and along the Gulf Coast, ongoing and planned Class VI or geological sequestration projects, Class II or enhanced oil recovery (EOR) projects, ongoing and planned CCUS projects, and saline aquifers used for the analysis. Image source: CCUS Maps. ii

A Net-Zero Electric Grid

A net-zero future depends on a decarbonized grid that can provide affordable and reliable electricity to Texans. Currently, the electric power sector is the third largest source of greenhouse gas emissions in Texas, accounting for 27% of all emissions in 2021.

Onshore wind is the second largest source of electricity in Texas, behind natural gas. Since early 2024, wind output has dropped several times compared to the same time last year. As a result, many utilities have had to increase generation from baseload sources to meet system needs. An unusual drop in wind speeds, combined with record high demand and challenges posed by worsening grid congestion, underscore concerns that the state may not always be able to rely on wind to meet its electricity generation needs. Solar capacity is expected to continue to grow (39,500 MW by mid-2025); while solar’s rapid growth has allowed it to provide a significant share of power on the Texas grid at times this year, the overall share of solar remains small.

Using the Regional Energy Deployment System (ReEDS), a model developed by the National Renewable Energy Laboratory, in combination with our scenarios, we find that grid capacity will range between 207 gigawatts (GW) and 361 GW by 2050, while lifecycle emissions, including the albedo effect (direct emissions discussed in Figure 1), will range between 478 million and 507 million metric tons of CO2eq (Table 2). Fuel switching and advances in storage and hydrogen production will lower the perunit lifecycle impact of capacity additions to the grid. Moreover, CCUS and DAC, if incentivized appropriately, can scale sufficiently in all alternative scenarios to mitigate the direct and lifecycle emissions impact of the grid.

While a net-zero, resilient, and reliable grid is possible, the transition will be complex. Our key findings are:

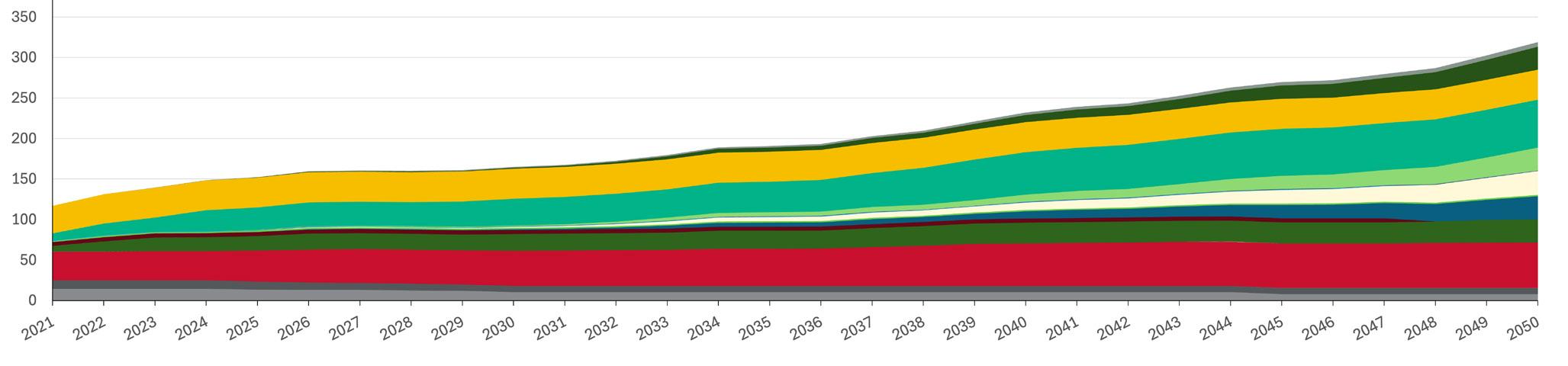

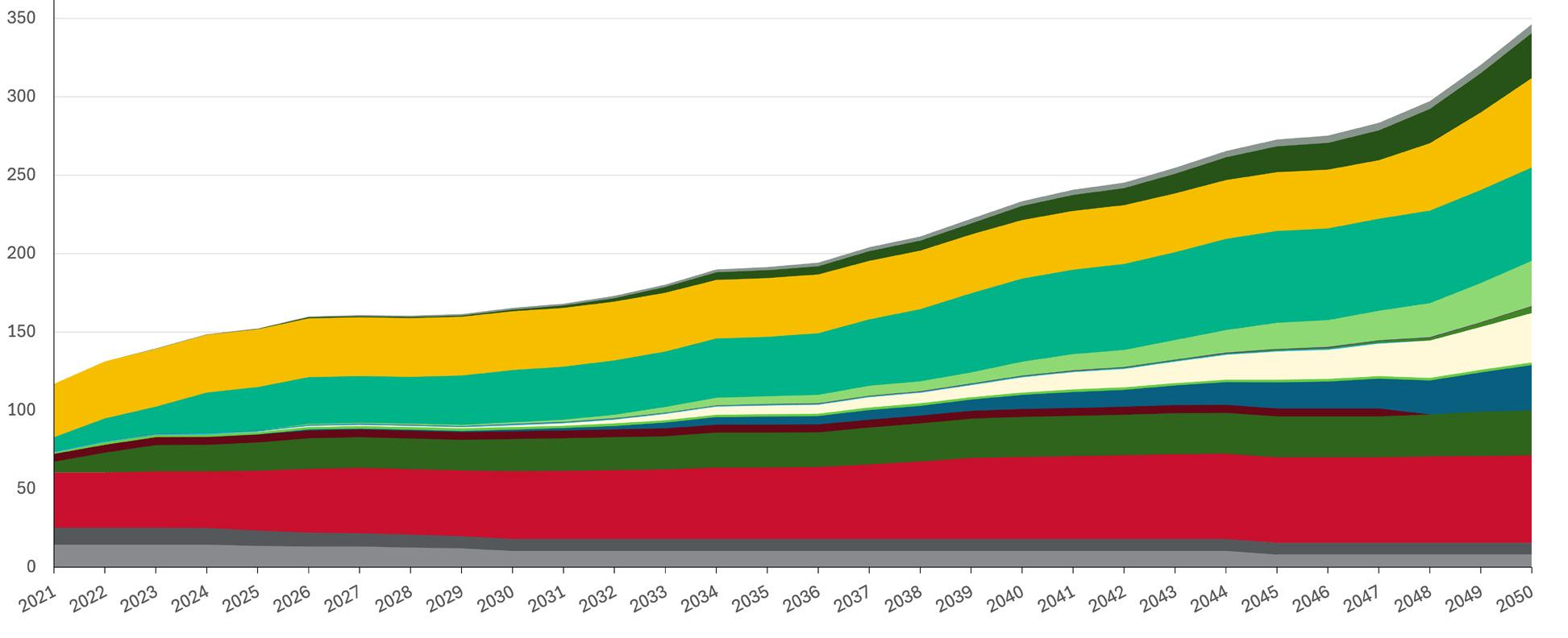

• The lowest cost option will be an all-of-the-above pathway, with high end-use electrification (Scenario 2). This would grow the baseload capacity from natural gas and couple it with CCUS, hydrogen, and the simultaneous growth of renewable generation and storage (Figure 4). The total levelized system cost of this scenario would be about $190 billion (Table 2).

• The levelized system costs of the other scenarios range from $211 billion to $318 billion (Table 2).

• CCUS would improve grid reliability, allowing net-zero baseload capacity addition without added emissions, along with the ability to maintain higher reserve margins and operational flexibility during extreme weather.

• Provisions in the federal Inflation Reduction Act will be crucial if Texas is to achieve net zero. These include a broad range of incentives for nuclear generation, blue hydrogen production, storage projects, hydro, geothermal, wind, solar, CCUS, and DAC.

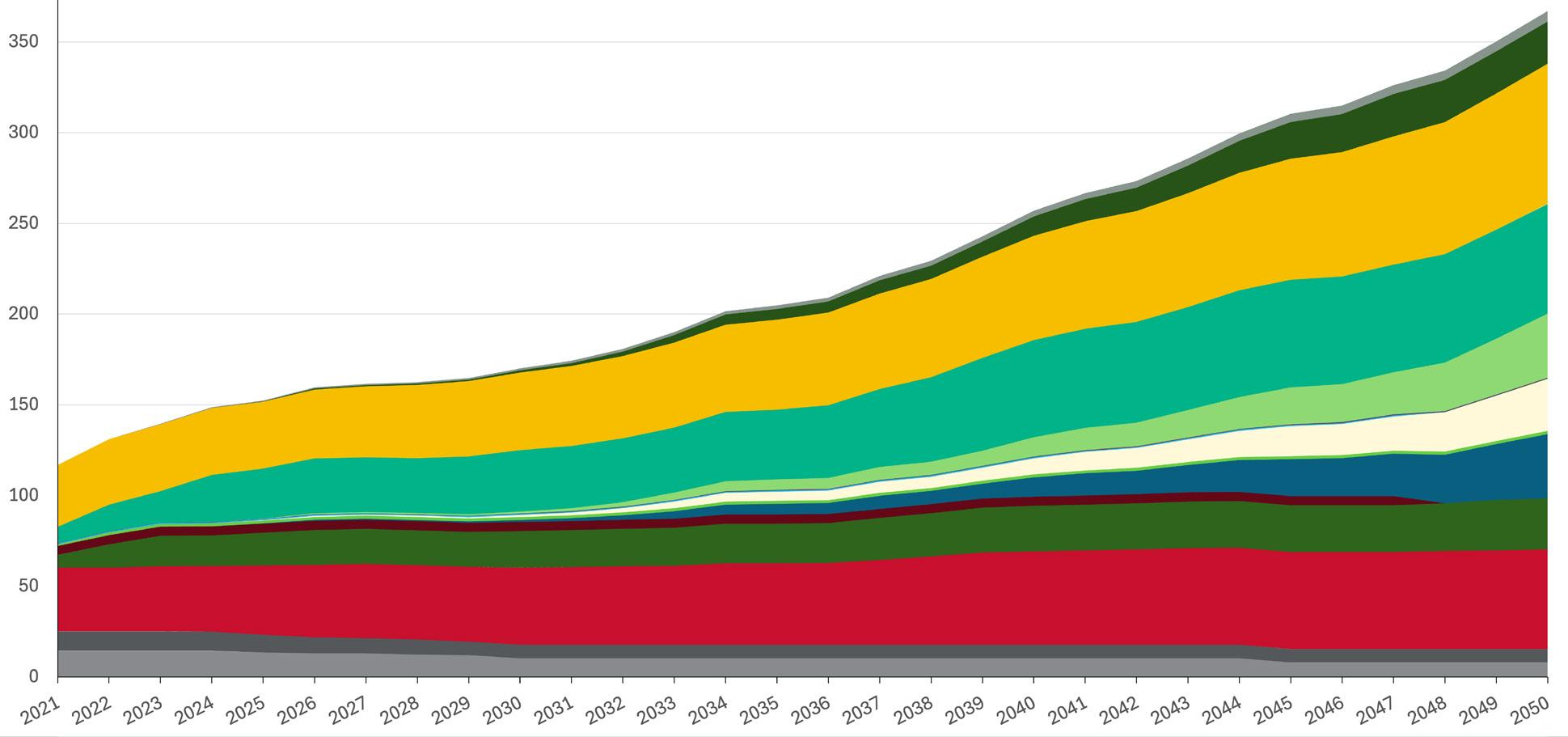

Figure 4. The energy mix of the current (2021) Texas grid (Bottom), the business-as-usual grid in 2050 (Top Right), and the lowest cost net-zero grid, i.e. Scenario 2, the High End-use Electrification, Unconstrained Energy Supply scenario (Top Left). Shares below 4% are not highlighted.

Pumped and Diurnal Storage

Hydroelectric

Geothermal

Wind Onshore and Offshore

Municipal, Wood, and Other Biomass

Fuel Cells

Table 2.

Net-Zero Transportation

The transportation sector is the state’s economic engine, reflecting both the personal travel of a fast-growing population and the commercial truck, rail, air, and marine transit required to move both the goods the state produces and those it imports. That adds up to about one-third of the state’s CO2 emissions.

We modeled interactions between the transportation system, travel demand, and socioeconomic conditions to quantify the emissions, infrastructural, environmental, and socioeconomic impact of the Texas transportation sector under three scenarios: business-as-usual; one in which all new sales are required to be zero-emissions vehicles by 2050; and one in which that requirement takes effect by 2040. The electrification of the fleet was based on the grid capacity scenarios discussed above.

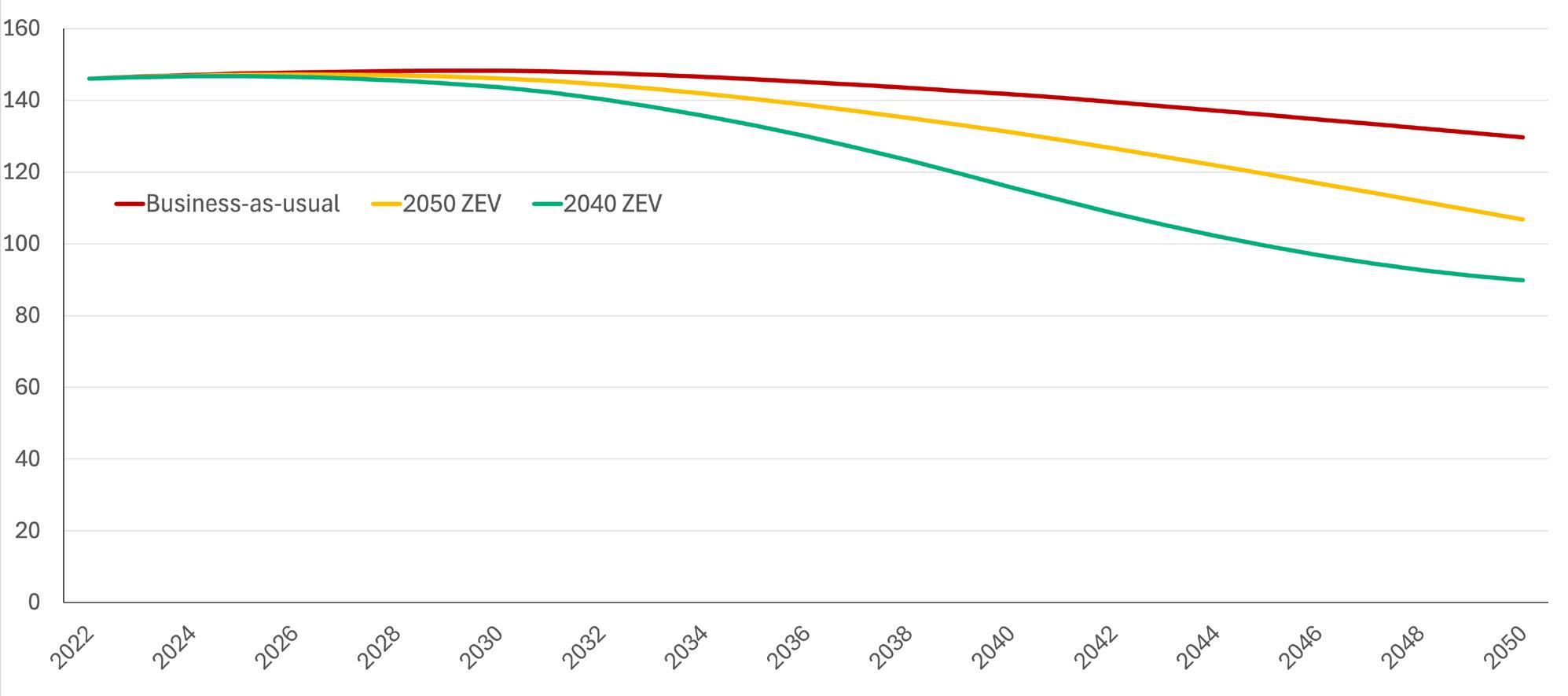

We find that even under the most aggressive policies considered, which would require all new vehicles sold in Texas to be zero-emission vehicles by 2040, and assuming the electric grid has converted to net-zero generation, the transportation sector will not be carbon-neutral by 2050, in part because older vehicles will remain on the road (Figure 6). Other key findings are:

• There will be an additional 2.5 million light-duty vehicles (LDVs), and 82,000 medium and heavy-duty vehicles (M/HDVs) on Texas roads by 2050 due to population growth and other factors (Figure 5).

• Depending on the scenario, EVs in the light-duty fleet are expected to grow to between 63% and 100% of new car sales, while the percentage of internal combustion engine vehicles (ICEVs) will vary from 7% to 60% of the total fleet.

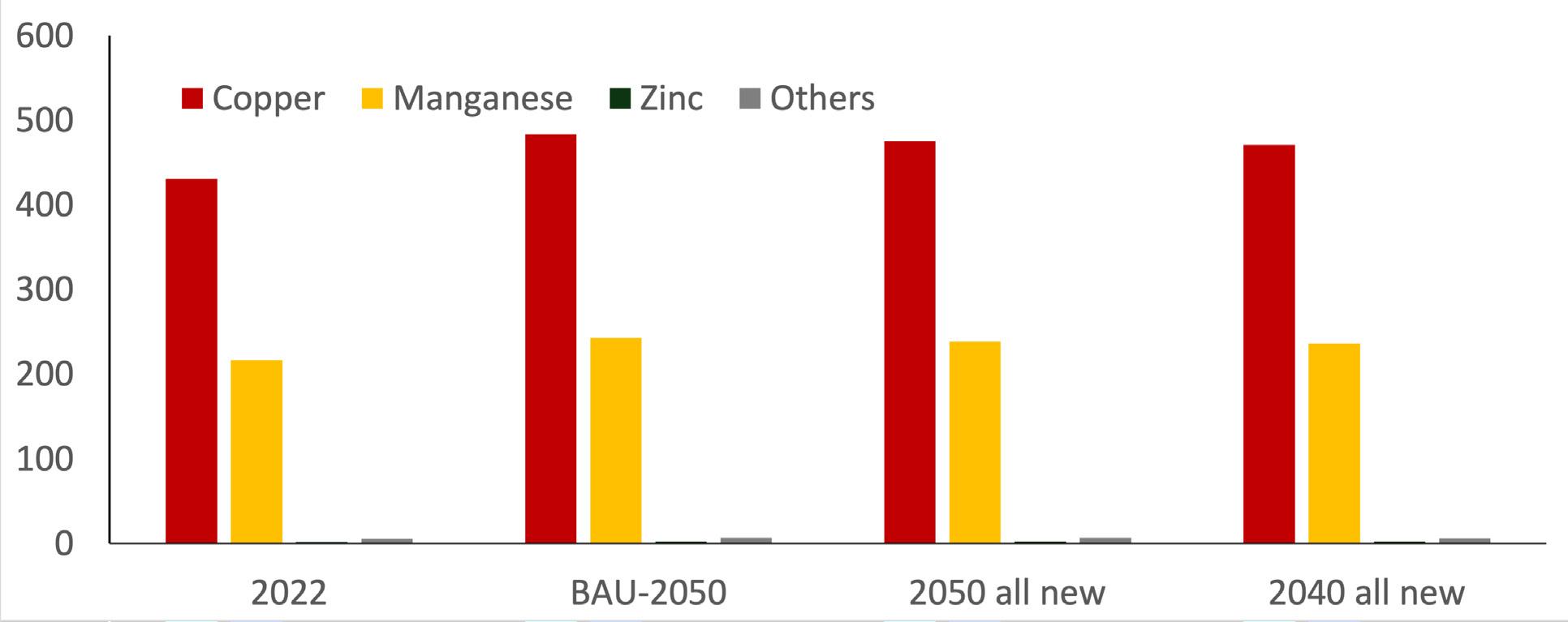

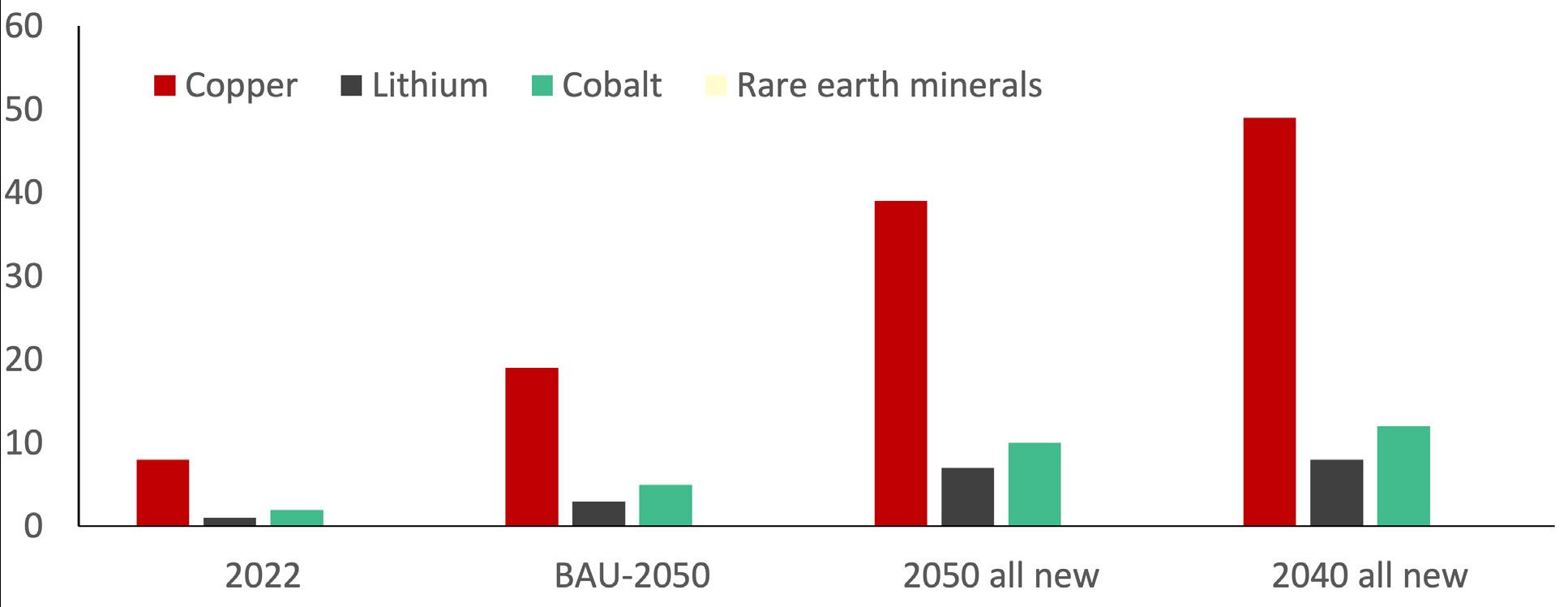

• The move to electric vehicles will have a significant impact on the need for minerals. The volume of lithium and cobalt necessary for batteries to power the expected number of EVs in the state by 2050 would exceed the current worldwide production of both minerals and lead to a significant increase in demand for materials including copper, manganese, and graphite (Figure 7).

• Electrifying the fleet or producing carbon-neutral fuels using carbon-neutral electricity could reduce rail, aviation, and marine freight-related emissions by as much as 99%.

• The costs of a net-zero transportation system will range from about $27 billion to $49 billion. This includes the cost of installing charging stations and other infrastructure, the cost of environmental remediation at gas stations that will be retired, and the loss of revenue from fuel taxes that no longer will be collected.

• It does not include the cost of vehicle replacement through 2050. These costs will be borne by the public and average about $80,000 per person.

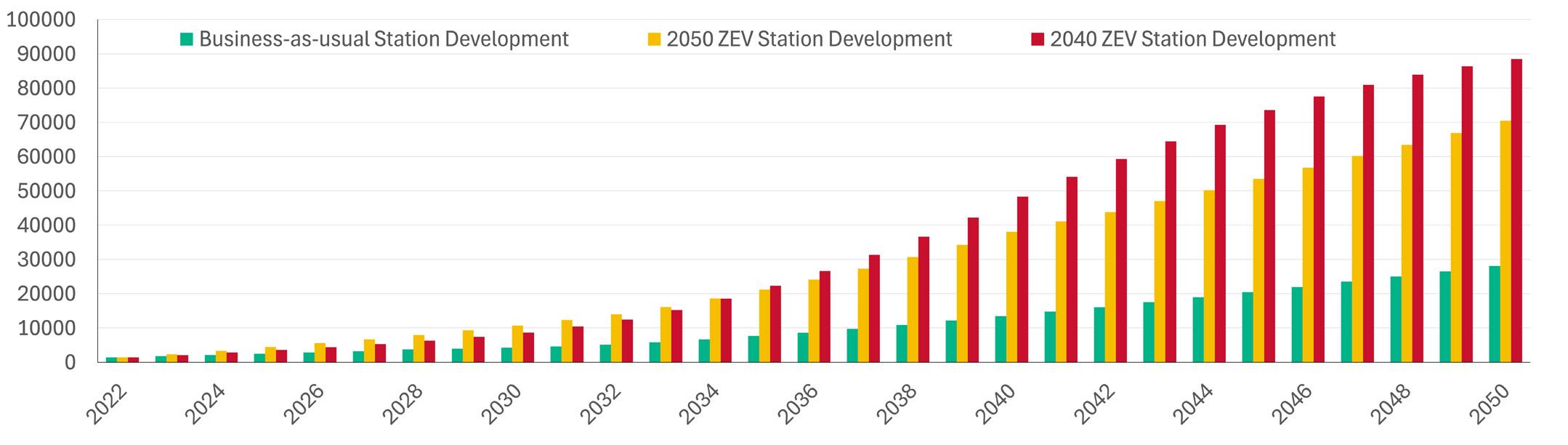

• While jobs will be lost in the traditional auto sector, between 130,000 and 180,000 new jobs in the lowcarbon transportation, electricity, advertising, retail, data and networking, and maintenance sectors will be added (Figure 8).

• New jobs will need to be supported by reskilling and upskilling opportunities, pay parity with the traditional auto sector, and the ability to organize.

Number of Vehicles In Millions

Figure 5. The total number of EVs and internal combustion engine vehicles (light-duty and medium and heavy-duty vehicles) in millions on Texas roads for the three policy scenarios.

Emissions In Million Metric Tons of Carbon Dioxide Equivalent

Figure 6. The emissions impact of the fleet (LDVs and M/HDVs) under the three policy scenarios based on the current electricity mix in Texas.

Critical Minerals For ICEVs In Thousand Tons

Critical Minerals For EVs In Thousand Tons

Figure 7. Growth in the demand for critical minerals (in thousand tons) for LDVs- ICEVs (top) and EVs (bottom) from 2022 to 2050, under the business-as-usual, 2040, and 2050 scenarios.

Workforce and Talent for a Net-Zero Texas

The energy industry has an outsized impact on the Texas economy, and any changes to the industry during the drive to net zero will directly impact the current and future workforce. Using the Jobs and Economic Development Impact (JEDI) and Impact Analysis for Planning (IMPLAN) models, our work suggests the energy workforce will shrink and lead to economic losses for the state under a business-as-usual scenario. The greatest impact will be on jobs in the coal and natural gas sectors, with a 90%-95% drop in related jobs and economic impact.

• Alternatively, the highest workforce benefits will come from a balanced strategy, focusing not on specific types of energy but on strategies to reduce emissions regardless of the source. These gains are achieved when moderate capacity additions in the renewables sector are balanced with growth in liquid fuels, biomass, hydrogen, CCUS, and CDR. Under this scenario (Scenario 3), about 2.1 million jobs will be added by 2050.

• CCUS will be a key employer in a net-zero Texas, growing to five times the state’s current oil and gas workforce by 2050 (Table 3). This sector can be supported with a highly skilled workforce from the coal, oil, and natural gas sectors, which will lose jobs. Ensuring the transferability of skills and the availability of reskilling and upskilling opportunities will be critical for an equitable transition.

• Current federal and state policies are geared towards the workforce needs of a changing industry, growing middle-skill jobs and presenting Texans with real pathways for upward mobility. More coordinated efforts from the workforce, educators, employers, and policymakers will be required to leverage these benefits.

The greatest impact will be on jobs in the coal and natural gas sectors, with a 90%-95% drop in related jobs and economic impact.

2.1 million jobs will be added by 2050

Table 3. The number of full-time equivalent jobs added during construction and operations based on the electricity grid in each scenario, the growth of CCUS and CDR, and the number of jobs projected to be lost in coal, oil, and natural gas sectors for each scenario by 2050. All impacts are cumulative, across the economy, and include indirect and induced effects beyond the energy industry. Numbers rounded to the nearest hundred.

Business-asusual

High End-use Electrification, Unconstrained Energy Supply

High End-use Electrification, Constrained Renewables and Storage

High End-use Electrification, Unconstrained Renewables and Storage

Low End-use Electrification, Constrained Energy Supply

Number of Jobs

Figure 8. Total employment from station development and station operations for Level 2 (L2) (top) and Direct Current Fast Charging (DCFC) stations (bottom). Jobs include direct, indirect, and induced jobs for the stations, and in the electricity, advertising, retail, data and networking, and maintenance sectors. All impacts are across the economy and include indirect and induced effects beyond the energy industry.

Implications for a Net-Zero Texas

A net-zero Texas is possible, but we are unlikely to get there by 2050. The financial costs will be enormous, perhaps in excess of $1.7 trillion. Transitioning to net zero will strain the economy and the people who live here, adding about $60 billion in costs per year for electricity, new infrastructure and products, environmental remediation, and spillover effects across all sectors of the economy.

Anticipated technological improvements and new federal and state policies will aid the state’s decarbonization efforts but are unlikely to bring down costs substantially. Some sectors, including the on-road transportation fleet, won’t be fully decarbonized by 2050 even under the most aggressive policy measures.

The 2024 rule, Order 1920, which allowed the Federal Energy Regulatory Commission to direct transmission providers to plan for future demand and increase grid reliability, is expected to be blocked, even though the final rules are based on comments from 200 stakeholders from the electric power industry, environmental organizations, state and other government agencies, and consumers.

The new government will weaken efforts for long-range planning and minimize FERC involvement in regional interconnections. The provisions of FERC’s new rule are expected to be challenged in court, and with a conservative judicial majority on the Supreme Court, its future is threatened. The Trump government is also likely to reverse two recent Biden programs that focus on investments in increased transmission and faster interconnection for lowcarbon energy and financing for rural electric cooperatives to increase energy access for rural communities.

The Trump government is likely to stall the Southern Spirit transmission line, which has recently received DOE funding to connect the Texas electric grid to the U.S. Southeast interconnection. This project is characterized by 320 miles of transmission lines that will have the capacity to carry 3,000 MW between the Texas-Louisiana border, northern Louisiana, and Mississippi. A Trump government is expected to argue that the project will infringe on states’ rights of being able to decide what is best for them.

At the state level, due to repeated challenges to infrastructure resilience and despite citizens’ demands to ‘fix the grid,’ we anticipate further increases in the cost of energy for all Texans.

Ultimately, the cost of any transition will be shouldered by the public, even as Texans’ ability to pay for a net-zero future will be challenged by rising income inequality in the state. At the same time, current emission levels already are adversely affecting residents in terms of public health, socioeconomic mobility, and quality of life.

Despite the pricetag and the hard choices that will have to be made, doing nothing is not a viable alternative. Smart decisions will have outsized impacts. A balanced net-zero strategy for new capacity additions to the electricity grid, for example, will provide Texas with the most benefits in terms of decarbonization, the economy, and the workforce.

Carbon removal through CCUS, direct air capture and other technologies will be critical to the decarbonization effort. The sector also has the potential to become a key employer in the state, helping offset jobs lost through the energy transition and continuing Texas’ global energy leadership.

Despite the pricetag and the hard choices that will have to be made, doing nothing is not a viable alternative.

Appendix A

Table A1. Assumed annual growth rates for different energy sources relative to the base case for existing technologies and relative to the growth rate for onshore wind in Texas for new technologies.

Grid Capacity in GW

High End-Use Electrification, Constrained Renewables and Storage

High End-Use Electrification, Unconstrained Renewables and Storage

Figure A1. Grid capacity between 2022 and 2050 for the remaining scenarios: High End-use Electrification, Unconstrained Energy Supply (scenario 3), and High End-use Electrification, Constrained Energy Renewables and Storage (scenario 4).

References

i UH Energy White Paper Series. CCUS Infrastructure: Preparing for the Future of Houston. No 4. 2023. ii CCUS Maps. 2024. https://ccusmap.com/markers/map/

About UH Energy

UH Energy is an umbrella for efforts across the University of Houston to position the university as a strategic partner to the energy industry by producing trained workforce, strategic and technical leadership, research and development for needed innovations and new technologies. That’s why UH is THE ENERGY UNIVERSITY®

Editorial Board

Ramanan Krishnamoorti

Vice President, Energy and Innovation University of Houston

Greg Bean

Executive Director, Gutierrez Energy Management Institute

Ed Hirs

Lecturer, Department of Economics BDO Fellow for Natural Resources

Christine Ehlig-Economides

Professor

Hugh Roy and Lillie Cranz Cullen Distinguished University Chair

Pablo M. Pinto

Professor, Hobby School of Public Affairs Director, Center for Public Policy

Produced by University of Houston Marketing and Communications