0w2010 01 RESUM EJECUTIVO 03 DEFcarta ang

26/10/10

19:49

Página 31

Second Global Report on Decentralization and Local Democracy. GOLD 2010 EXECUTIVE SUMMARY

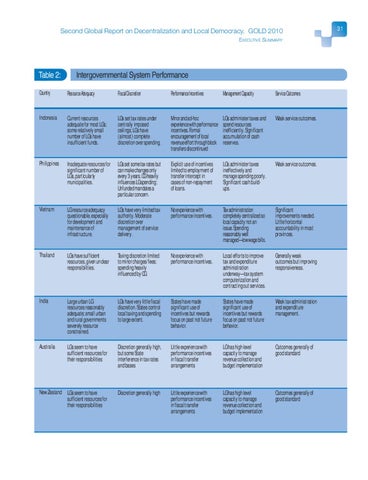

Table 2:

Intergovernmental System Performance

Country

Resource Adequacy

Fiscal Discretion

Performance Incentives

Management Capacity

Service Outcomes

Indonesia

Current resources adequate for most LGs; some relatively small number of LGs have insufficient funds.

LGs set tax rates under centrally imposed ceilings; LGs have (almost) complete discretion over spending.

Minor and ad-hoc experience with performance incentives. Formal encouragement of local revenue effort through block transfers discontinued

LGs administer taxes and spend resources inefficiently. Significant accumulation of cash reserves.

Weak service outcomes.

Philippines

Inadequate resources for significant number of LGs, particularly municipalities.

LGs set some tax rates but can make changes only every 3 years. CG heavily influences LG spending; Unfunded mandates a particular concern.

Explicit use of incentives limited to employment of transfer intercept in cases of non-repayment of loans.

LGs administer taxes ineffectively and manage spending poorly. Significant cash buildups.

Weak service outcomes.

Vietnam

LG resource adequacy questionable, especially for development and maintenance of infrastructure.

LGs have very limited tax authority. Moderate discretion over management of service delivery.

No experience with performance incentives.

Tax administration completely centralized so local capacity not an issue. Spending reasonably well managed—low wage bills.

Significant improvements needed. Little horizontal accountability in most provinces.

Thailand

LGs have sufficient resources, given unclear responsibilities.

Taxing discretion limited to minor charges/fees; spending heavily influenced by CG.

No experience with performance incentives.

Local efforts to improve tax and expenditure administration underway—tax system computerization and contracting out services.

Generally weak outcomes but improving responsiveness.

India

Large urban LG resources reasonably adequate; small urban and rural governments severely resource constrained.

LGs have very little fiscal discretion. States control local taxing and spending to large extent.

States have made significant use of incentives but rewards focus on past not future behavior.

States have made significant use of incentives but rewards focus on past not future behavior.

Weak tax administration and expenditure management.

Australia

LGs seem to have sufficient resources for their responsibilities

Discretion generally high, but some State interference in tax rates and bases

Little experience with performance incentives in fiscal transfer arrangements

LG has high level capacity to manage revenue collection and budget implementation

Outcomes generally of good standard

New Zealand LGs seem to have sufficient resources for their responsibilities

Discretion generally high

Little experience with performance incentives in fiscal transfer arrangements

LG has high level capacity to manage revenue collection and budget implementation

Outcomes generally of good standard

31