0w2010 01 RESUM EJECUTIVO 03 DEFcarta ang

26/10/10

19:49

Página 30

EXECUTIVE SUMMARY 30

Table 2:

United Cities and Local Governments

Intergovernmental System Performance

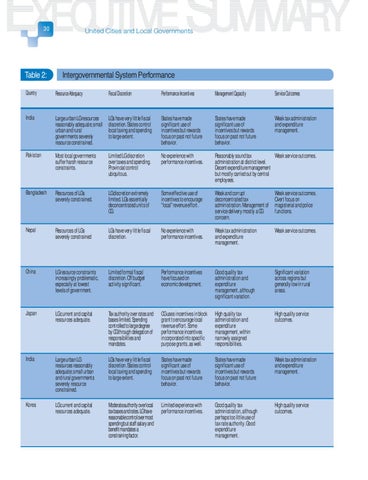

Country

Resource Adequacy

Fiscal Discretion

Performance Incentives

Management Capacity

Service Outcomes

India

Large urban LG resources reasonably adequate; small urban and rural governments severely resource constrained.

LGs have very little fiscal discretion. States control local taxing and spending to large extent.

States have made significant use of incentives but rewards focus on past not future behavior.

States have made significant use of incentives but rewards focus on past not future behavior.

Weak tax administration and expenditure management.

Pakistan

Most local governments suffer harsh resource constraints.

Limited LG discretion over taxes and spending. Provincial control ubiquitous.

No experience with performance incentives.

Reasonably sound tax Weak service outcomes. administration at district level. Decent expenditure management but mostly carried out by central employees.

Bangladesh

Resources of LGs severely constrained.

LG discretion extremely limited. LGs essentially deconcentrated units of CG.

Some effective use of incentives to encourage “local” revenue effort.

Weak and corrupt deconcentrated tax administration. Management of service delivery mostly a CG concern.

Weak service outcomes. Overt focus on magisterial and police functions.

Nepal

Resources of LGs severely constrained

LGs have very little fiscal discretion.

No experience with performance incentives.

Weak tax administration and expenditure management.

Weak service outcomes.

China

LG resource constraints increasingly problematic, especially at lowest levels of government.

Limited formal fiscal discretion. Off budget activity significant.

Performance incentives have focused on economic development.

Good quality tax administration and expenditure management, although significant variation.

Significant variation across regions but generally low in rural areas.

Japan

LG current and capital resources adequate.

Tax authority over rates and bases limited. Spending controlled to large degree by CG through delegation of responsibilities and mandates.

CG uses incentives in block grant to encourage local revenue effort. Some performance incentives incorporated into specific purpose grants, as well.

High quality tax administration and expenditure management, within narrowly assigned responsibilities.

High quality service outcomes.

India

Large urban LG resources reasonably adequate; small urban and rural governments severely resource constrained.

LGs have very little fiscal discretion. States control local taxing and spending to large extent.

States have made significant use of incentives but rewards focus on past not future behavior.

States have made significant use of incentives but rewards focus on past not future behavior.

Weak tax administration and expenditure management.

Korea

LG current and capital resources adequate.

Moderate authority over local tax bases and rates. LG have reasonable control over most spending but staff salary and benefit mandates a constraining factor.

Limited experience with performance incentives.

Good quality tax administration, although perhaps too little use of tax rate authority. Good expenditure management.

High quality service outcomes.