4 minute read

MONEY MATTERS

Investment Strategy

The 60/40 portfolio remains a bellweather

GRAPHIC COURTESY OF J.P. MORGAN ASSET MANAGEMENT

After years of falling rates (specifically since the early ’80s), we are now in a rising rate environment. If you understand how bonds work, you know that when interest rates go up, the value of existing bonds decline; when interest rates decline, the value of existing bonds goes up. A good picture for bonds is a seesaw.

You have to go back over 40 years to see a worse bond market than the one we have experienced so far this year. Bonds are traditionally thought of as ballast to a portfolio. When stocks have a tough year, the bonds are there to dampen the volatility. This makes sense in a falling interest rate environment or a stable rate environment, but when interest rates increase at the pace they have this year, that ballast begins leaking and becomes less stable.

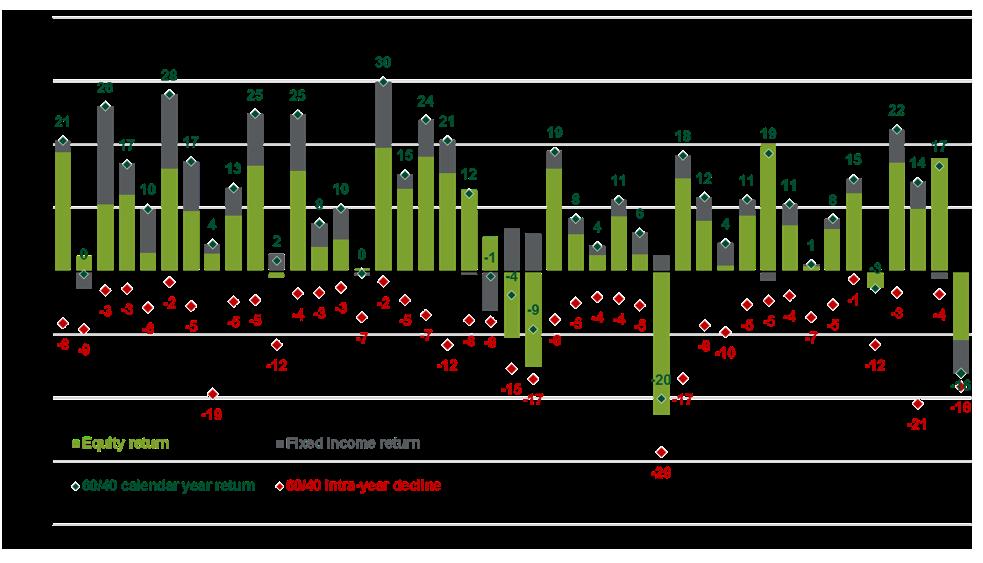

The chart accompanying this article shows the return for a 60/40 portfolio invested 60 percent in the S&P 500 Total Return Index and 40 percent invested in Bloomberg U.S. Aggregate Total Bond Return Index, going back to 1980. The reason this chart was chosen is due to a large number of retirees having similar asset allocation in their portfolios.

Notice first that fixed income return is positive almost every year over this timeframe with decent returns as shown by the blue shading. Secondly, in years where the green part of the bar is negative (stocks), the gray part (bonds) tends to be positive. In 2022, you see both the green and blue severely in the negative.

Going back to 1980, there isn’t another year that looks anywhere near this year regarding equity and fixed income in the negative. Thus far, that makes 2022 one of the worst years in the last 40 regarding returns. The bond portion can be explained with the rise in interest rates, as discussed earlier. Over the last several years, bonds became return-free risk, mainly due to interest rate sensitivity.

Today, not all is bad. After all, the world wasn’t built by pessimists. For the first time in quite some period of time, bonds are actually offering respectable yields with decent yield to maturity. Government bonds, backed by the full faith and credit of the U.S. government, are now yielding over 4 percent for the two-year period, as I write this article. Times have definitely changed quickly. The question then becomes, is now a good time to buy bonds?

The way I would answer this question is: It is a far MONEY better time to buy them than a couple years ago, due to MATTERS where rates are today. The interest rate risk on bonds has decreased. Yields today are far more respectable, and if inflation comes down to the Fed’s target, bonds bought today could have a real return (net return after factoring in inflation), which is something that has been amiss. All in all, the bond market Lee Williams is far better than it was the last several years, and the 60/40 portfolio that has been the bellweather for retirees for so long is looking to be better positioned for future volatility.

On a side note, for those who have insurance products, like annuities and certain life products, cap rates are seeing upward adjustments across many companies, which can favor future returns. Now may be a good time to review these with your advisor. As always, consult your trusted advisor or financial professional for what makes the most sense for your personal plan and know that in financial services, there isn’t a one-size-fits-all model.

~ Lee Williams offers products and services using the following business names: Lee Williams – insurance and financial services | Ameritas Investment Company, LLC (AIC), Member FINRA/ SIPC – securities and investments | The Ascent Group, LLC – investment advisory services. AIC is not affiliated with Lee Williams or The Ascent Group, LLC.

Information gathered from sources believed to be reliable; however, their accuracy cannot be guaranteed. Actual prices may vary. Securities are subject to investment risk, including possible loss of principal. This material is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. While we believe the information provided is reliable, we cannot guarantee its accuracy. Opinions expressed are subject to change without notice and are not intended as investment advice or a solicitation for the purchase or sale of any security. Please consult your financial professional before making any investment decision.