Perspectives on hybrid working

Survey Insights May 2023

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Contents INTRODUCTION ORGANISATIONAL INFORMATION ATTENDANCE MODELS SPACE ALLOCATION TECHNOLOGY COMMUNITY & EVENTS EMPLOYEE VOICE FINAL THOUGHTS CONCLUSIONS 01 02 03 04 05 06 07 08 09 1

Introduction

Perspectives on...

The key takeaways from the previous surveys are given below.

Perspectives on Working from Home (April 2020)

“ … the workplace landscape will be very different from the one we shut down in March 2020. With previous studies showing offices at an average of 45% utilisation and the current situation showing that technology allows us to largely work effectively from home,. Is this the evidence we need to design the future workplace less around individual tasks and more around collaboration and organisational identity?”

Perspectives on Returning to the Workplace (June 2020)

“organisations seem to be heading in the right direction when it comes to … the return to the workplace. The most popular strategies for addressing reduced capacity … are those informed by studying work functions and encouraging staff to continue to work from home wherever possible.

This experience of working from home will have a lasting effect … however, there is still a lot of uncertainty over returning to the workplaces that were vacated several months ago.”

Perspectives on the Future Workplace (March 2021)

“One year into lockdown, and there is still ample evidence that we are ‘people’ people. 90% of participants saw the most positive aspect of the pre-COVID workplace as having access to their colleagues.”

“There is still uncertainty over the attendance model – just over ¼ said they were unsure as to what form the blend would take and who would determine it. 24% stated that a flexible model implemented at team level was their preference.”

01

3 INTRODUCTION

Perspectives on hybrid working

If you go back and look at the introduction to our third survey report “Perspectives on the Future Workplace” , we expressed some surprise at the situation we were in back in early 2021—a vaccine was on the horizon but a lockdown was proving tough to endure. SPACE weren’t sure whether ‘blended’ or ‘hybrid’ was going to be the chosen word to reflect the most common new attendance model. We initially opted for blended, but soon fell into line with the majority.

Fast forward to the present day. The pandemic is almost a distant memory. There are some of our fellow citizens who continue to wear face masks, sales of hand gel have not reduced dramatically and workplace wording and definitions are still causing confusion. While much of society has returned to pre-pandemic norms, there is still a lot of uncertainty surrounding the workplace, and understanding the impact of this is the main focus of this current survey.

SPACE are not in the market of making predictions based on gut feelings; we reflect on data. Your responses will help us make sense of the evolving picture surrounding people, technology and spaces that comes together to form a workplace.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Report Authors

Associate Workplace Consultant

Muir Director of Consultancy & Design

01

Chris Carr

5 INTRODUCTION

Phil

Who replied?

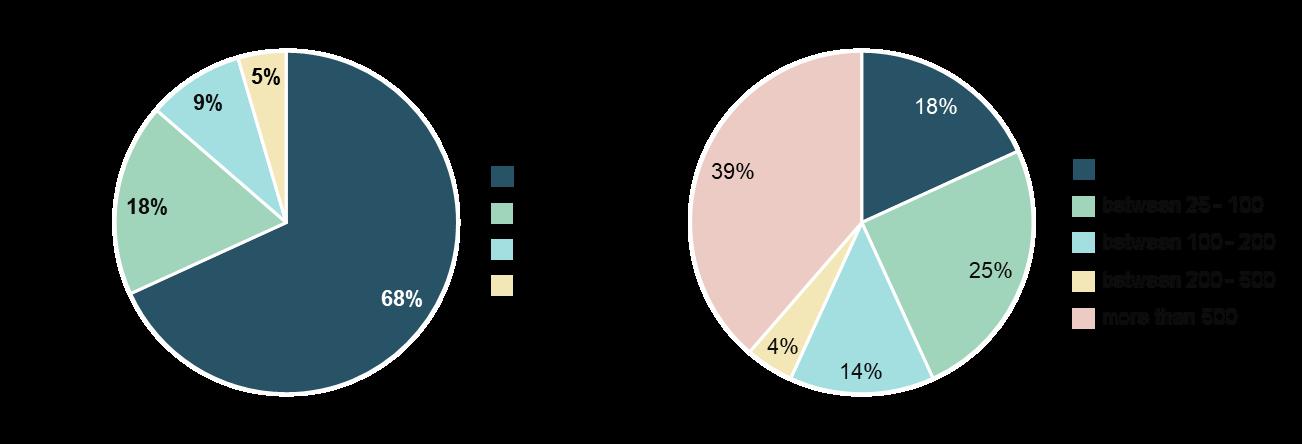

SPACE operates in a wide range of sectors—from education to energy, from small local charities to global organisations. We specifically chose not to ask for more information on sector other than private, public and third (the ‘other’ responses being trade associations).

As we continue to navigate our way out of the pandemic and assist our clients in doing so, we’ve come to the conclusion that there are more similarities than differences amongst our clients. There will always be businesses who provide very specific services, but even within these businesses there are functions that are replicated across sectors. Finance is Finance is Finance.

More than half of the responses are from SMEs—like SPACE. We contemplated asking about the impact of having staff across multiple sites. Although we did not ask this question, some of the free text responses made reference to this—noting the positive and negative impacts.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

01

1. Participants by organisation headcount.

7 INTRODUCTION

2. Participants by organisation sector.

Organisational Information

ORGANISATION 2023

THIRD SECTOR

3. headcount post-pandemic

YES-HAVE LOST SOME PEOPLE

YES-RECRUITED TO REPLACE PEOPLE

YES-RECRUITED NEW STAFF

NO-NEITHER LOST NOR RECRUITED

DON’T KNOW

0 20 40 60

OTHER

% % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Who replied?

To say that the past three years have been difficult is an understatement. Government support via the furlough scheme proved to be a lifeline for many employees and employers, but there were still job losses as whole areas of the economy shut down.

For those with a lower headcount than pre-pandemic levels, was that planned (as a result of down-sizing or reorganisation) or did employees leave of their own accord, for a variety of reasons, and were just never replaced?

For those who now have a higher headcount, was it unbroken growth or were there periods of greater than average losses followed by a burst of recruitment?

The data tells us about the clients who have responded, but it is difficult to draw any further conclusions.

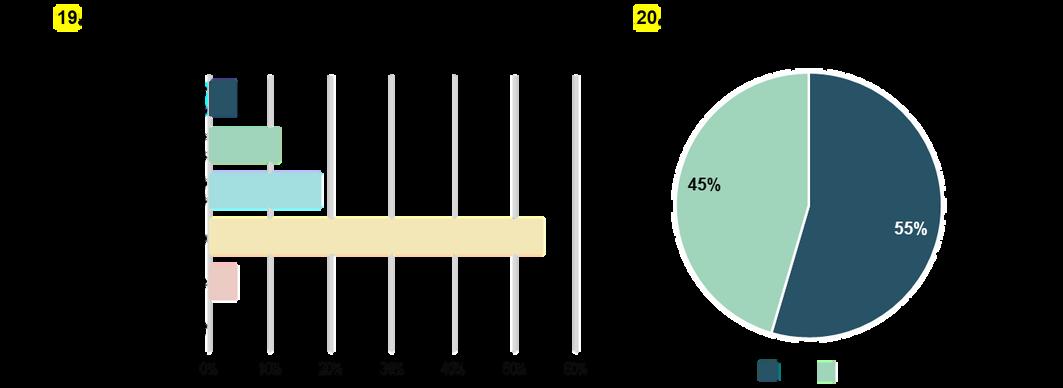

55%

Have seen their workforce grow post-pandemic

If increasing headcount is a measure of success, the pandemic does not appear to have put a significant dent in growth .

02

11 ORGANISATIONAL INFORMATION

Recent Experience

'The Great Resignation' and 'Quiet Quitting' were two phrases discussed repeatedly during the past few years. This was brought on by people reflecting on recent experiences, looking for more and not being too shy about letting you know they weren’t satisfied.

Many studies have shown [1] that reasons for looking for alternative employment were greater flexibility, greater career prospects and better pay and conditions. The responses below show that in amongst this turmoil, just as with the responses to the question on Productivity (next page), once you dig deeper than the headlines, you find that the real picture is not as grim as has been expressed.

VERY NEGATIVE NEGATIVE

NEUTRAL POSITIVE

VERY POSITIVE

VERY NEGATIVE NEGATIVE NEUTRAL POSITIVE

VERY POSITIVE

0 10 20 30 40

N/A

0 10 20 30 40

4. Employee retention over the past 12 months

N/A

% % % % % % % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

5. Ease of recruitment over the past 12 months

The c.25% who have expressed a negative response in Q4 would be wise to understand why retention has been so challenging. If the reasons can be addressed, then that will undoubtedly also help with employee attraction. For some, it may be purely financial and due to the scale of their business and therefore completely outwith their control.

In terms of recruitment, the war on talent continues. The data would tend to support the assertion (repeated in the free text responses on page 17), that the balance of power has currently swung towards the employee. The Chartered Institute of Professional Development (CIPD) reported in July 2022 that there was still a dwindling talent pool [2] though the Office for National Statistics states that vacancy numbers continue to fall, [3] citing “uncertainty across industries, as survey respondents continue to cite economic pressures as a factor in holding back on recruitment” .

EY, How workplace rebalancing is building pressure in the talent pipeline, Liz Fealy & Roselyn Feinsod, April 2022 CIPD, The Battle for Talent Continues, Jonathan Boys, July 2022 Office of national statistics, Labour market overview, UK: April 2023

1. 2. 3. 13 02 ORGANISATIONAL INFORMATION

Recent Experience

Given the current geo-political climate and the degree of general financial uncertainty, the responses in Q6 & 7 show a remarkable degree of resilience within the business community.

Productivity is an oft-heard word in the workplace sector when it comes to discussing the performance of ‘knowledge workers’ . It can be incredibly hard to measure definitively and therefore the correct phrase should be 'perceived productivity' .

There are two sides to every story, but in terms of productivity, the data right would tend to show that the impact of the pandemic has not been the disaster that many commentators report.

The positive impact on productivity follows on to business growth, with a very similar response profile.

The CBI recently reported on a general trend over the past eight quarters of reduced private sector activity, but also highlighted that the expectation is “volumes in business and professional services are set to return to growth” [1].

1.CBI, Latest CBI monthly services sector survey and growth indicator, March 2023

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

6. Productivity during the past 12 months

7. Business growth over the past 12 months

VERY NEGATIVE NEGATIVE NEUTRAL POSITIVE

VERY POSITIVE

0 10 20 30 40 50

N/A

VERY NEGATIVE NEGATIVE NEUTRAL POSITIVE VERY POSITIVE

0 10 20 30 40 50

N/A

% % % % % % % % % % % % 15 02 ORGANISATIONAL INFORMATION

Biggest Impacts

8. What topic has had the biggest impact during the past 12 months?

The survey question did not discriminate between positive and negative impacts, and while some of the responses might be open to interpretation, the number of negative impacts exceeded the number of positive impacts by a factor of c.7:1.

POSITIVE IMPACTS

The responses highlighted the benefits of flexible working patterns and implementing new ways of working. Working from home (within the confines of hybrid working), as a means of addressing the current cost of living challenges, was seen as a positive. The knock-on effect of right-sizing offices to support a reduced daily attendance was referenced.

NEGATIVE IMPACTS

These broadly fell into three categories:

Politics, Economy and Supply Chain

People and Salary

Climate Change and COVID, this category saw only a few responses.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Politics, Economy and Supply Chain

Uncertainty due to inflation, costs and general political upheaval were reported. With many of SPACE’s clients being involved in the North East energy sector, specific issues such as an Energy Windfall Tax and an unclear future for the North Sea were mentioned. Energy cost increases have impacted businesses across all sectors. Efficiencies were having to be investigated as the cost for services and products increased, with project budgets not tracking these increases.

People and Salary

This was the most frequently reported negative impact, reaffirming the data from Q5 regarding challenges with recruitment—not just in terms of finding the right people (with the right skills), but in terms of the time taken to recruit and the expectations over salaries.

The impact of trying to replace European staff with UK-based staff was reported, with an example given of 250 interviewees for positions resulting in only 6 people being hired. In the Third Sector one respondent commented on salary expectations now being 15-25% higher than pre-pandemic levels, making it difficult to recruit into management roles.

While, for some, hybrid working is a positive, others reported that it has been difficult to get the balance right, ensuring that the right people are in the office at the same time.

It is worth noting that the topic with the biggest impact does not necessarily correlate with the most popular current discussion topic which, from our experience, is the journey to net zero.

17 02 ORGANISATIONAL INFORMATION

Attendance Models

“

Office workers are only attending the office 1.5 days a week on average across the data set.”

“Where the declared policy is 3 days a week, people are coming in less (2.3 days a week). ”

Advanced Workplace Associates, Hybrid Working Index, December 2022

19 03 ATTENDANCE MODELS

Workplace Attendance

Hybrid may not be the answer for everyone, but it is the answer at the moment for most, as the responses below testify.

For those who attend the workplace the same days each week, anecdotally it appears that Tuesday–Thursday are, as before, the peak days, with Monday being busier than Friday. This is really no different from the situation pre-pandemic (in terms of measured utilisation patterns, at least).

That the highest response is for attending the workplace when there is a purposeful need to be there, is welcoming.

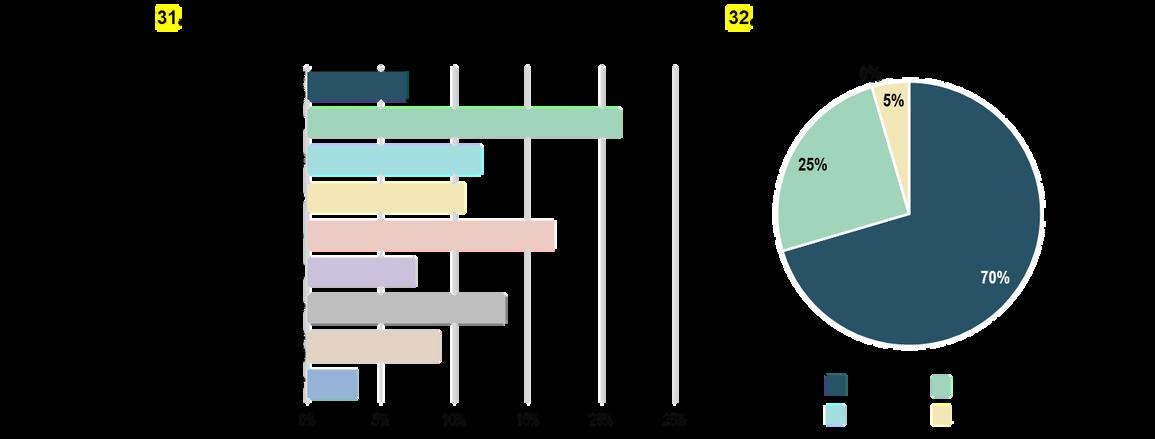

9. Current observations

effectively full time in the workplace

hybrid-people typically working the same days week in, week out hybrid-workplace attendance depends on meetings etc.

predominantly remote with some workplace attendance

don

0 10 20 30 40

’t

know other

% % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

For those who responded ‘other,’ the responses refer to a mix of the two hybrid responses and to variations across the business dependent on the nature of the role. No one size fits all—there we’ve said it.

For some, hybrid working is the natural response to an increased employee expectation of flexibility, where the job function supports a level of flexibility.

For those who have a more operational role, or for whom processes haven’t been developed sufficiently to support hybrid working, being in the workplace full time might not be what they would like, but it is what the job function demands.

It would be interesting to ask the 43% who have no formal attendance policy whether in fact there is a formal policy, it's just that there is no mandated number of days expected in the workplace. SPACE knows of one client whose formal policy was that there is no formal policy.

21 03 ATTENDANCE MODELS

10. A formal attendance policy?

Workplace Attendance

11. Current observations of workplace attendance

yes-adherence not strictly enforced

yes-attendance recorded, adherence enforced

0 10 20 30 40 50 1 day / week 2 days / week 3 days / week 4 days / week 5 days / week other

0 20 40 60

no don't know other 12. Is attendance monitored

% % % % % % % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

?

As the comment from Advanced Workplace Associates testifies, what people say and what they do are often two totally different things.

The peak in observed workplace attendance at 3 days per week, and with a greater number of 2 days per week than 4 days ties in with most general observations of slightly less than 3 days per week in the office.

That 5 days per week is reported by almost 25% of the respondents is possibly more of an indicator of SPACE’s client base, where our involvement within the North East energy sector implies more operational roles and therefore an increase in expected daily attendance in the workplace.

For those who didn’t fall into the numbered categories, individual agreements with employees that are dependent on their contract were the main reasons for reporting ‘other’ .

One of SPACE’s clients recently commented that the reason for not having a mandated number of days in the workplace was the desire not to add a level of bureaucracy where it was not needed. That more than 50% of respondents stated their formal attendance policy is a guide and not enforced would seem to be a 'common sense approach' .

Follow-up questions for those who record attendance and enforce adherence might be 'how is this achieved?'—i.e., through a manual checking process or via technology —and 'was this the case pre-pandemic also?'.

23 03 ATTENDANCE MODELS

Workplace Attendance

yes –positiveimpact yes –negativenochangeindon ’tknow other 60 40 20 0

collaborationfocuspersonalpreference betterworkenvironmentsocialisation organisationalpolicyother 25 20 15 10 5 0

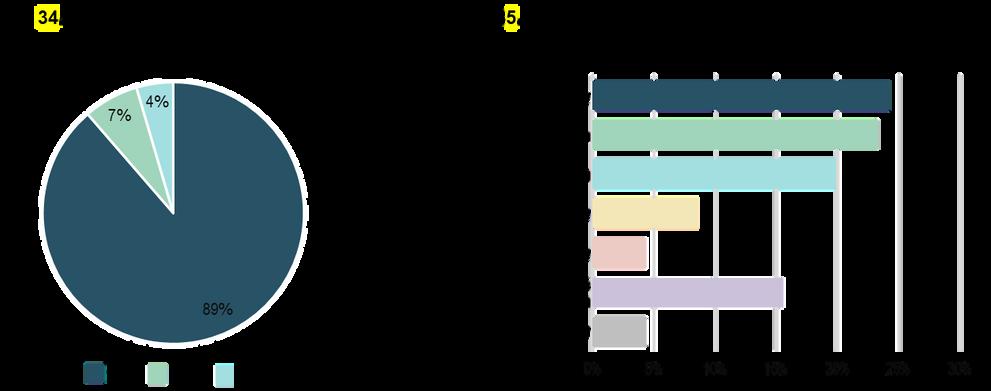

13. Is attendance impacting workplace effectiveness?

% % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

14. Reasons for attending the workplace?

Q13 directly relates to Q6 ('Productivity'). The perception, according to some workplace / corporate real estate commentators, is that there are employers who want everyone back in the workplace 5 days a week (often related to perceptions of reduced productivity, sometimes a barely-disguised 'we’ve a building to fill'). The truth is that people on average were never in the workplace 5 days a week prior to the pandemic, according to utilisation studies conducted by SPACE and others.

The overwhelming majority of respondents have not seen a negative impact from this increased flexibility in when people attend the workplace. This would suggest that while a steady state has not been reached, current attendance levels are not a barrier to organisational effectiveness.

Apart from training (referenced by several in the ‘other’ option), the list of options provided in the survey covers the main reasons why people attend the workplace.

It has long been assumed that focus work would take place at home. This assumes the home environment is appropriate. That is not always the case and the reliance on Teams calls reflects the need for quiet spaces in workplaces.

The two highest scores are for group activities, and this is where the workplace will always be better than the home—with the caveat that such spaces have to really support such communal activities.

The prominence of personal preference and better work environment

possibly

the fact that separation of work and home life was impossible during lockdown. Now restrictions have eased, some are recreating this distinction.

25 03 ATTENDANCE MODELS

reflects

Workplace Attendance

No matter how many surveys are run, how many reports are written, there will be those who say ‘black’ when the data says ‘white’ .

The picture is evolving and will continue to do so. It needs to continue to evolve in order to generate creative thinking and innovative solutions.

A very high-level cutting of the data indicates that responses indicating a formal attendance policy of 4 or 5 days per week in the workplace were all from private or third sector clients.

SPACE’s own perspective— from working with clients and from our interactions across a range of sectors—is that the public sector has been slower to return to the workplace than others.

“If I had asked people what they wanted, they would have said faster horses.” Henry Ford

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

This has consequences for the public sector estate, and we know this is being studied at local and central government level. Whether we anticipated this low level of public sector utilisation or not is difficult to say.

As workplace consultants, we perhaps expected a bit more certainty by early 2023, or at least to be further on the journey towards greater certainty so long after lockdown restrictions have eased.

27 03 ATTENDANCE MODELS

Space Allocation

“

Are we going to see offices (forming part of the total workplace solution along with the home office, the café, the train, the client’s business lounge etc.) becoming more like 75% non-desk, focused and collaborative worksettings with a few token desks for those who don’t need to be as mobile?”

SPACE – FLIP! Is it time (again) to talk about the flipped office?

04

29 SPACE ALLOCATION

Ownership

15. Have desk numbers changed post pandemic?

16. Are there defined workplace neighbourhoods?

yes-reducedsignificantlyyes-reducedmarginallynochange yes-increasedmarginally yes-increasedsignificantlydon

’

50 40 30 20 10 0

tknow other

% SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

One of the defining ideas of Smarter Working is the move from owned to shared space. An extreme case of Smarter Working is that all desks, regardless of their open plan location, are bookable. For some organisations (e.g., the Registers of Scotland office in Glasgow, designed before the pandemic) this model works and supports a greater mixing of disciplines.

For others, encouraging people back into the workplace (if that is the desire) is assisted by having some defined area to return to, where local storage may be located, or where privacy may be more controllable. SPACE’s recent project with the Scottish Prison Service was built around flexible neighbourhoods for each team.

One of the ‘other’ responses talks of areas set aside for quiet working but with all desks being bookable. A recent layout SPACE proposed for a client echoes this idea, having a small, quieter area (but still open plan) and a larger area where there is less of an expectation of silence.

As the picture continues to evolve, many clients are waiting for things to settle down a little more and, for this reason, the highest response is that there are no changes to the number of desks.

This is not surprising.

The challenge will be that, if utilisation remains low, how long asset managers will allow spacing to remain unchallenged.

31 04 SPACE ALLOCATION

Utilisation & Changes

17. Are you measuring desk utilisation?

yes – utilisation is higher than pre-pandemic levels

yes – utilisation is about the same as pre-pandemic levels

yes – utilisation is lower than pre-pandemic levels

18. Have you remodelled your workplace post pandemic?

don’t know other

0 20 40 60

no

% % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Workplace utilisation studies were not carried out on a regular basis pre-pandemic. They were usually commissioned by Finance or Facilities Managers who had change in mind but needed data to back up their own observations. Some organisations have invested in sensor-based systems for providing real-time utilisation data, but costs dictate that this has not become standard practice.

Thus, just as with the 'Productivity' question, we are likely here to be discussing perceived workplace utilisation. Reported changes in utilisation have to be taken with a pinch of salt.

If utilisation is not being measured by the majority, and the numbers of desks are more or less staying the same, remodelling of workplaces must be down to changing layout to increase functionality.

Where there is an opportunity to move to smaller, better workplaces (the ‘espresso office’ [1]) the down-sizing, or more accurately, the right-sizing, allows organisations to respond to their ESG (Environmental, Social and Governance) commitments.

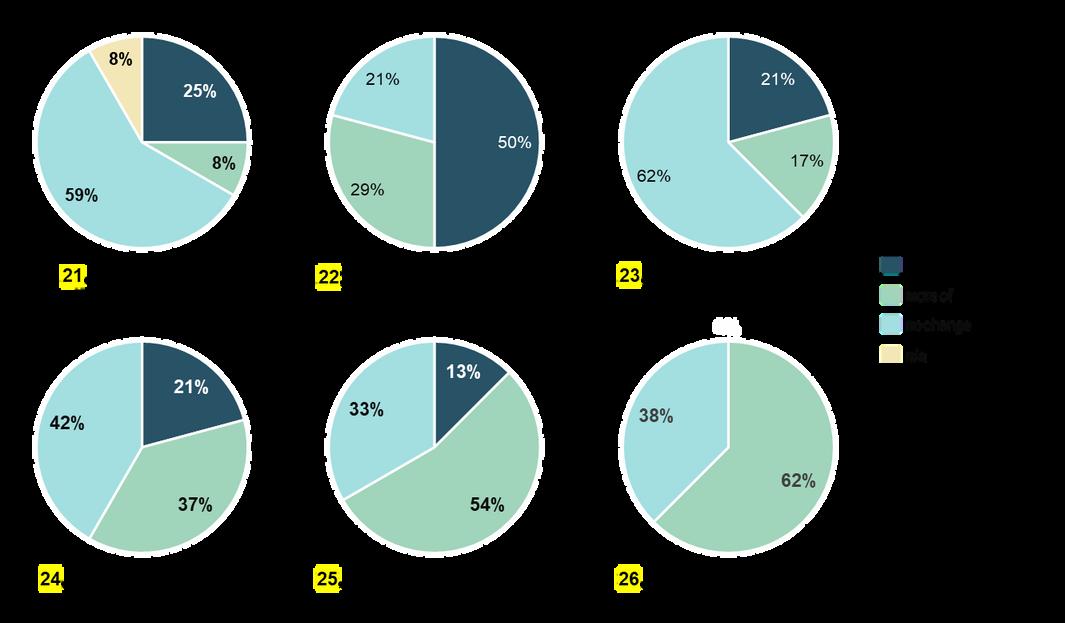

In our 2021 Perspectives on the Future Workplace survey, nearly 70% of respondents said they would reconfigure space to better align with new working practices. The responses left would suggest that many have followed through on this promise.

1.https

1. 33 04 SPACE ALLOCATION

://issuu.com/aberdeenchamber/docs/april bulletin online (p.19)

Utilisation & Changes

22. The number of small meeting rooms

23. The amount of informal meeting space

22. The number of small meeting rooms

23. The amount of informal meeting space

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

24. The amount of social/welfare space

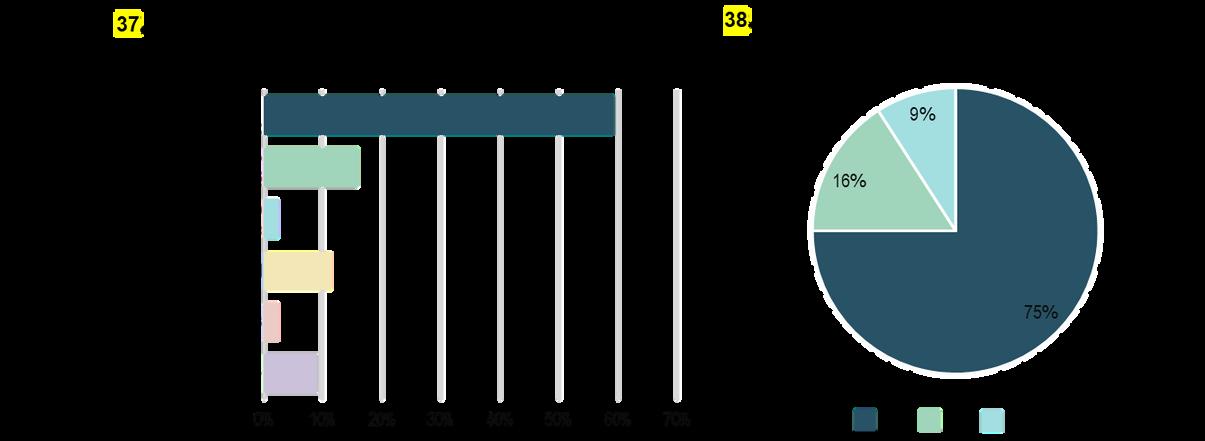

Where changes have been made, the results show that the office has indeed ‘flipped,’ with primary workspace (offices and desks) being reduced and the area won back given over to spaces that support group activities.

The biggest change is in the provision of spaces to support informal activities and employee socialisation. Both of these are seen as being vitally important for encouraging employees back to the workplace in greater numbers.

While, from Q14, we have reported that achieving focus is not one of the most important reasons for attending the workplace, the increase in the number of small meeting rooms could be attributed to providing spaces away from the desk for Teams calls or for private phone calls.

35 04 SPACE ALLOCATION

Technology

The IT Crowd, Channel 4

05

off

”

“Hello, IT. Have you tried turning it

and on again?

37 TECHNOLOGY

Work From Anywhere

very poorly poorly neutral well very well

very poorly poorly neutral well very well

0 20 40 60

n/a

25. Supporting desk work in the workplace

0 10 20 30 40 50

26. Supporting remote work

n/a % % % % % % % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

SPACE are not AV or IT consultants, but we hear a lot from our clients about technology—mainly reporting that it doesn’t work. Thus the responses left are pleasing to see.

However, the overwhelmingly positive response to Q25 shouldn’t mask a complaint we hear repeatedly from the clients: the time wasted setting up your laptop when you arrive.

Fewer desks and a desk booking system, coupled with a range of computing technologies and personal preferences, can result in five minutes every morning being spent hunting for cables or adjusting monitors. This is one of the many reasons why some prefer to have their own desk.

Three years following the first lockdown, it would be surprising, and somewhat worrying, if remote work was still a problem for a large number of respondents.

One of the reasons we have heard from clients (and from some of our own employees) as to why the office is so popular is that it offers fast and reliable connectivity.

Combining the themes of desk work and remote work, the home environment for many replicates their workplace experience as best as possible. Where multiple monitors in the workplace are seen as being essential, but are not available at home, can productivity be compared?

39 05 TECHNOLOGY

Meeting & Collaboration

very poorly poorly neutral well very well

very poorly poorly neutral well very well

0 10 20 30 40 50

n/a

27. Supporting hybrid meetings

0 10 20 30 40 50

28. Supporting work away from your desk

n/a % % % % % % % % % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

For many organisations, having the entire team present in the same meeting room is not logistically possible. Colleagues can be in different cities or different time zones and the ability to collaborate through technology has been a massive bonus.

When it works.

The data left would tend to suggest that it is working well and, certainly, there has been considerable investment in AV technology within SPACE in recent months.

Whether hybrid meetings are truly as collaborative as possible is questionable. The technology functionality might exist, but the knowledge and experience to make the most of this functionality may be lacking with some employees (and this inexperience or lack of confidence was masked previously with having support on hand at all times).

Having an IT department who might also be working hybrid places an emphasis on training, on having intuitive technology and on some people standing on their own two feet.

Activity Based Working (ABW)

A key component of an ABW environment is the ability to quickly move from one task in one location to a new task in (perhaps) a different location.

Where technology is involved, this 'dock ‘n go' approach is the holy grail. That a significant proportion of responses say there is a poor experience means, in general, workplace technology has not yet reached a settled solution for everyone.

41 05 TECHNOLOGY

Community & Events

& DUKE 2022

BELLA

Spreading the word

hardcopye-mailintranetTeams WhatsApp,

25 20 15 10 5 0

Messengeretc.TownHalls-virtualTownHalls-face-to-facecompanyawaydays other

29. Communications methods

%

30. Do you have a formal ‘Events’ group?

With many organisations seeing hybrid working as the norm, more emphasis is placed on keeping staff who are not in the workplace every day informed and updated on a range of organisational issues affecting them.

Electronic communication is still the key, with e-mail, unsurprisingly, still being the front-runner. What is interesting is the prominence of third party messaging platforms such as WhatsApp and Messenger. Within many teams, WhatsApp groups sprang up during lockdown as a means of keeping morale up—less about work-related issues and more about general chat. That this is still popular is good news (keeping up the information flow) and bad news (relying on an unofficial, and commercial platform).

Face-to-face Town Halls being more popular than the virtual alternative is possibly related to a desire to create more in-person events to encourage workplace attendance.

Of the ‘other’ responses, two alternatives are audio files and a regular newsletter. The high prominence of company away days shows that some businesses are happy to invest significantly in keeping employees informed and engaged.

Within SPACE, we have a Wellness Group who are tasked with curating a range of events and initiatives across our locations. One of the frequent criticisms made against such groups and campaigns is the difficulty in calculating the benefits. That being said, diverse organisations have reported that for every £1 spent on employee wellness (and this can take many forms), the benefits can be as much as £7. With 70% of respondents saying they have a formal group tasked with addressing the staff experience, there is definitely value to be gained.

06

45 COMMUNITY & EVENTS

Developing a community

There is no clear winner in the 'what makes a good workplace community?' stakes. Rather, it seems to be a combination of having the right mix of people with a space they can congregate and feel comfortable in. In-person events seem to be favoured over virtual events.

Where smaller organisations have geographically dispersed teams, there will always be two levels of community—one at a local (office) level and one at an organisational level. The two have to work hand in hand as there needs to be an over-arching culture (with some room for local influences to permeate).

Reading some of the corresponding free text comments relating to this question, there are those who feel that a community can only be built through having people in the same physical space.

There are numerous organisations globally who have a 'remote first' approach and who have been extremely successful at creating a (virtual) community—it requires ingenuity and new ways of developing relationships, but is not impossible.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

31. Community building factors

wellbeing / community group available budget diversity right type of physical space virtual team building experiences regular team meetings in-person social events collaborative projects

engaged and passionate employees considering team dynamic when recruiting

Free Text Comments

“It is important to maintain a culture in the business which is collaborative and innovative. This is only possible by recruiting the right people and providing the right tools and working environment.”

“I believe people used to take their workspace for granted, not coming into an office has made people realise there is a real social element to meeting up with colleagues, for many working from home was a very lonely experience.”

"We have remodelled our office to encourage a greater one-team approach; increased collaborative working. We have also established a social committee which has encouraged and arranged increased social / charity events etc."

0 5 10 15

% % % % 47 06 COMMUNITY & EVENTS

Employee Voice

Scottish Government, Fair Work First

“Fair Work … offers effective voice, fulfilment, opportunity, respect and security.”

49 07 EMPLOYEE VOICE

Contributing Ideas

32. Avenue for contributing ideas

33. Most popular employee issues

0 5 10 15 20 25 sustainability technology integration innovation accessibility neurodiversity equality, diversity & inclusion other

% % % % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

Engaged and passionate employees ranked high in the factors contributing to a workplace community. Engagement needs to be more than cake sales, however, and having an avenue for contributing ideas that benefit the entire organisation is important.

With nearly 90% of respondents reporting that avenues do exist for promoting ideas people feel passionate about, the key is what then happens—are the topics developed further or just placed into a bank of good ideas and not actioned. The latter will quickly result in disengagement.

In late 2020, SPACE initiated a Think Tank programme where employees came together and discussed issues that were important to them. The top two themes were sustainability and technology—echoing the data left.

Sustainability has become the number one talking point in just a few short years, and, we believe, will continue to dominate discussions for years to come. As mentioned at a seminar recently, organisations or products that are not sustainable will not survive.

It could be argued that the ‘people’ issues (accessibility, neurodiversity, and equality, diversity & inclusion) taken as a whole, are the single most important topic based on numbers alone. Neurodiversity is perhaps still a niche discussion topic at this point in time, for specific HR & OD professionals and design teams only.

Given that the majority of respondents to the survey were private sector, it is perhaps no surprise to read the ‘other’ responses focusing mainly on areas such as new ideas for income generation, opportunities for saving money and making efficiencies, and for encouraging entrepreneurial activities.

51 07 EMPLOYEE VOICE

Employee Survey

34.

0 20 40 60

no surveys conducted don’t know other

annual survey (within last 12 mths) one-off survey (within last 12 mths) within first 6 mths of the pandemic

Regularity of employee surveys

% % % % SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

35. Are survey results reported back?

The first lockdown sparked an avalanche of surveys. We were all suddenly keen to hear opinions.

Three years on, while we are possibly no nearer to the clarity we all desire; we are able to report trends based on frequent snapshots, such as this survey.

Not listening to the voice of employees is a recipe for disaster. The pendulum will continue to swing back and forth between employee and employer as we go through economic cycles. In the past, it was very heavily weighted towards the employer, but those times have possibly gone for good.

That the majority of respondents are reporting an annual survey of employees being conducted is positive. As one of the ‘other’ respondents mentioned, continuous feedback is also important. 12 months is a long time to wait before you get feedback, so avenues need to exist for issues to be raised at any time—those might be local office committees, formal appraisals or Q&As with senior leadership.

Once you have asked the questions or provided the avenues for feedback, where is the worth in not reporting back? Having a significant number of organisations who choose not to inform their employees of the findings of a survey seems like a missed opportunity to really show you are listening by having a 'you said, we did' report.

Unless those organisations who don't report back are 100% perfect, in which case, we salute you.

07

53 EMPLOYEE VOICE

Final Thoughts

PIPER SANDLER 2022

Optimism

As is customary in our projects, comments are broken down into the three key themes of people, technology and space.

PEOPLE

There will be a greater focus on flexibility, wellbeing initiatives and on collaborative working. Hybrid working will encourage new employees (with potentially non-geographic recruitment) and is already having a benefit on some employees, with a better work/life balance resulting in higher levels of job satisfaction, performance and staff retention.

As well as increased productivity, hybrid working and greater flexibility in general have the opportunity to allow employees to work across a range of sites, experience a range of workplace cultures and communities and (hopefully) to bring in new ideas. It might need some refinement and the benefits of hybrid working (and office working) need to be well communicated.

On the flip side, there are those who are optimistic about being back in the office full time, due to their perceived boost in terms of productivity, collaboration and the learning and development benefits for younger members of their teams. For them, a return to pre-COVID ways of working and there being no expectation of home working would be a positive move. And it would increase office utilisation.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

There is an awareness that there needs to be a focus on sustainability, with workplaces and the people who use them tackling climate challenges. There is positivity that, within a specific respondent’s sector (and the wider business community we would hope) that quality wins out over the cheapest solution.

TECHNOLOGY

There is general optimism over fixing the hybrid meeting experience, alongside general improvements in technology integration to support communication and greater flexibility. Moving out of the office, one organisation is buoyant about the future since they have invested in new machinery that will allow organic growth into a new plant.

SPACE

When creating improved facilities that contribute towards a modern working environment, supporting informal collaboration is a goal for some. Some see this is an opportunity to tailor the workplace to their needs, freeing up space for other areas of the business. This will involve thinking about issues such as 'How many desks do we really need?' or 'How many informal working areas do we need?' and creating the type of environments that will attract and retain employees.

The integration of technology into the workplace may change the role of the workplace, turning it into more of a training and collaboration hub.

08 57 FINAL THOUGHTS

Pessimism

The number of comments relating to concerns was approximately the same as the number of positive comments.

PEOPLE

Just as some praised and some mourned the advent of hybrid working, a concern raised was about the return to inflexibility. A balance does need to be reached—one comment read 'we gave an inch and they took a mile' .

However, most of the concerns raised related to new and young employees not learning from their peers and seniors, not learning professional behaviours, hampering their professional development and breaking the bond between employee / employer by not being in the office.

Reduced productivity was reported as being a concern arising from hybrid working, while some lamented it being a permanent solution that was essentially an emergency response to a specific and pressing issue.

An extension of hybrid working is the opportunity for non-geographical recruitment —this is an opportunity and a threat, with the potential for work going to cheaper locations.

As was referenced in Q8, salary expectations and the ability to compete in the jobs market are a concern for many. The cost of living also has an impact on people’s ability to attend the workplace

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

The 4-day week by stealth was raised as an issue—this will very possibly impact support staff who rely on delivering commercial services. A catch-all term 'concerns about the unknown' possibly reflects a wider feeling— some businesses thrive on certainty.

TECHNOLOGY

The threat to the status quo from AI and technology, with regard to jobs, was raised as a concern, as was more general technology issues around security, rising costs and having the spaces to support the ever-present Zoom / Teams calls.

SPACE

Access to reasonable-cost, small, suitable, and flexible office space made one respondent pessimistic; a different perspective was having redundant office space or facing the closure of offices as business go through a process of reorganisation. Access to appropriate space to support growth was also reported as being a concern.

Workplaces are vital parts of our cities and towns—their economies rely on people attending and generating footfall in local businesses. The threat is of permanent closures and job losses.

OTHER

The fact that the last lockdown is not too distant a memory causes some to fear a return to the cycle of lockdowns we had previously, with enforced working from home.

59 08 FINAL THOUGHTS

Conclusions

SPACE sent this survey out to our client contacts, who, for the most part, are at a more senior level within businesses and organisations. This has to be borne in mind when reading the responses.

On a day-to-day basis, we deal with our colleagues, with our clients and read reports of studies others have conducted. Through these different channels we hope to gain a rounded (and grounded) picture of where we currently are and where we might be going.

What is clear is that technology and the physical environment are not the main issue —and they never really were.

Every workplace solution is essentially a people-solution and since people come and go within organisations, since teams are born, grow and are often disbanded, it can be nigh on impossible to devise the perfect solution. We aim for the best solution at that time and trust the flexibility of any design to cope with most change on a sensible timescale.

It is clear that recruitment has been, and continues to be, a major issue. Costs— from salaries to services—are also an issue. There is hopefully light at the end of the tunnel in terms of stability of costs. Whether costs will drop will be determined by the market—appropriately enough given that it is the 300th birthday of Adam Smith.

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

The hybrid working experiment continues, and will continue to evolve. Judging by the responses, some are not warming to this increased flexibility, preferring pre-pandemic levels of influence over the 'what, where, and when' of work, rather than building on the trust established during the days of enforced home working.

Thank you to all participants of the survey.

If you have any questions, please contact:

Phil Muir: philip.muir@spacesolutions.co.uk

Chris Carr: chris.carr@spacesolutions.co.uk

61 08 FINAL THOUGHTS

Additional Insights

SPACE SURVEY – PERSPECTIVES ON HYBRID WORKING

ABERDEEN DUNDEE EDINBURGH GLASGOW LONDON e: philip.muir@spacesolutions.co.uk w: www.spacesolutions.co.uk