13 minute read

The return of the long-term LNG SPA

Rob Butler, Baker Botts, UK, looks at the data behind LNG contracting activity over the last five years in order to establish whether there has been a resurgence in long-term LNG contracts, and considers what is driving change in LNG contracting behaviour during this period.

In early March 2021, the Marketing Director of a state-owned LNG buyer declared that “the era of the long-term contract is over.” Whilst hindsight is a wonderful thing, it is clear that the world has changed significantly since that statement was made. Many reports and commentators are now declaring the ‘return’ of long-term LNG contracts.

LNG contracting trends

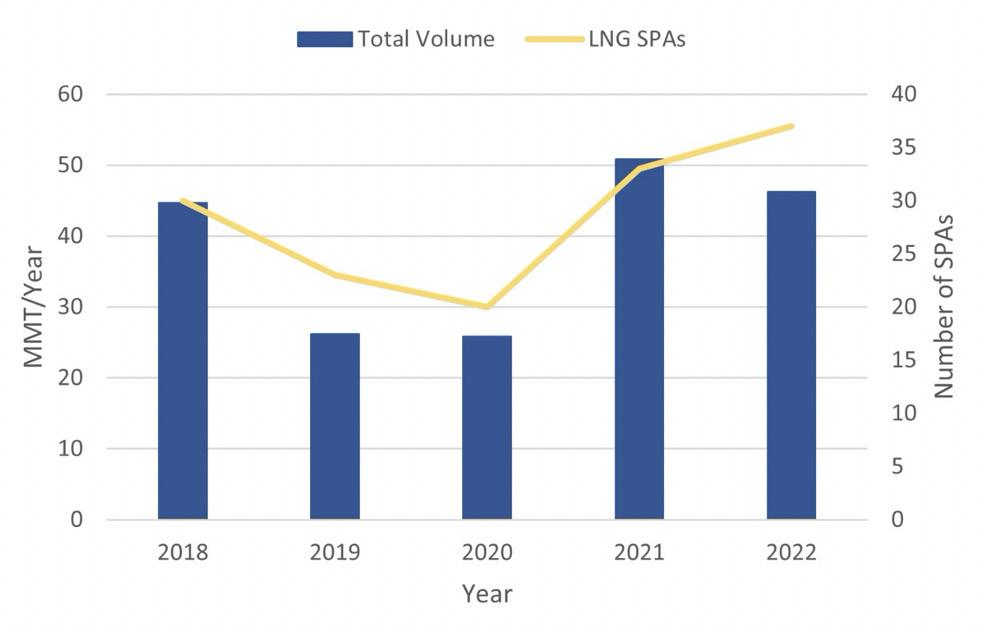

Data from Poten & Partners LNG Contract Intelligence Service shows that 2021 saw a steep rise in both the number of long-term1 LNG sale and purchase agreements (LNG SPAs) that were entered into and the total LNG volumes contracted for under such LNG SPAs (Figure 1). This trend has continued in 2022, with the total number of long-term LNG SPAs signed in 2022 at the time of writing already exceeding the total number of long-term LNG SPAs signed in the whole of 2021.

Whilst this shows that there was an increase in the number and volume of long-term LNG sales contracted for in 2021 and 2022, this could have simply been due to an increase in LNG contracting activity during those years. It therefore needs to be determined whether this represented an increase to the share of long-term LNG sales of the global LNG market.

Data from the annual reports published by the International Group of LNG Importers (GIIGNL) shows that the long-term LNG SPAs2 signed in 2021 represented 64% of the total volume of LNG sales contracted for in 2021. This was an increase from the 47% share that long-term

LNG SPAs had in 2020, but was still nowhere near the 93% share that long-term LNG SPAs had in 2019 (Figure 2). The GIIGNL data only goes up to 2021, however, so does not show whether this trend has continued through 2022.

Looking specifically at 2022, the data from Poten & Partners LNG Contract Intelligence Service shows that the number of mid-term3 LNG SPAs signed in 2022 dropped off significantly from prior years (Figure 3). As of 11 September 2022, only three mid-term LNG SPAs had been signed in 2022, as compared to 20 mid-term LNG SPAs in 2021 and 12 mid-term LNG SPAs in 2020. This therefore represents a significant move away from mid-term LNG sales towards long-term LNG sales. The data therefore supports the claim that there has been a resurgence in long-term LNG contracting, but what is driving this change?

Figure 1. Long-term LNG sale and purchase agreements signed.

Figure 2. Contracts signed by duration.

Figure 3. Mid-term LNG sale and purchase agreements signed.

COVID-19

In order to look at why long-term LNG sales increased in 2021 and 2022, it is first necessary to look at the situation prior to this increase.

Even before the onset of the COVID-19 pandemic, during 2019 and early 2020 the LNG industry was experiencing a period of over-supply and historically low prices. The COVID-19 pandemic greatly accelerated these issues. In 1H20, with governments across the world imposing lockdowns on the public and on businesses, global demand for natural gas dropped by an estimated 4% y/y;4 this was the largest fall on record. This demand destruction resulted in a significant decrease in LNG production, as buyers scrambled to cancel or reschedule cargo deliveries, and global LNG exports fell by 17% between January – June 2020.4

The resulting over-supply in the LNG market led to huge drops in LNG and natural gas spot prices, with spot prices hitting record lows in April and May 2020. The Japan Korea Marker (JKM), the LNG benchmark price assessment for spot physical cargoes delivered ex-ship into Japan and South Korea, dropped to a record low of US$1.80/million Btu on 28 April 2020. This was down from US$5.26/million Btu at the start of 2020. Spot natural gas sales at the Dutch Title Transfer Facility (TTF) fell to a record low US$1.13/million Btu on 28 May 2020, down from over US$5.00 at the beginning of 2020.

Lockdowns resulted in delays to LNG projects already under construction, with project developers forced to reduce the number of workers on site to the bare minimum. In addition, even once workers could return to site, the knock-on effects of delays throughout the global supply chain further pushed back the expected start-up dates for new LNG export projects.

COVID-19 also delayed the taking of a final investment decision (FID) on a number of proposed LNG export projects. In 2019, six LNG export projects took FID on nearly 71 million tpy of additional LNG production capacity – a record year for the approval of new LNG export projects. A similar number of FIDs was predicted for 2020 but, due to the effects of the pandemic, Sempra’s Energía Costa Azul

project in Mexico was the only LNG export project to take FID in 2020.

The drop in LNG contracting activity in 2020, and the pushing back of FID on all of these delayed projects, has contributed to the increase that has been seen in long-term LNG contracting activity in 2021 and 2022. Despite not having taken FID, project sponsors had invested heavily on these projects and, for many of these projects, it was a question of ‘when’ not ‘if’ they would proceed to FID once market conditions improved.

Buyer opposition to long-term contracts

Due to historically low spot LNG prices in 2019 and 2020, and the resulting price differentials against traditional long-term LNG SPA contract price formulas, many LNG buyers had begun to rely heavily on spot LNG purchases for an increasing share of their LNG demand.

Whilst some LNG buyers saw an opportunity to lock-in low-cost LNG supplies during this period, many LNG buyers were reluctant to commit to long-term LNG SPAs, which they viewed as inflexible and expensive (as against then-current spot LNG prices). This can be seen in the decline in the number of long-term LNG SPAs signed in 2019 and 2020 (Figure 1), and in the increase in spot cargo sales as a share of the global LNG market over the same period (Figure 4). The statement quoted in the opening paragraph of this article was made against this backdrop of historically low prices and relative over-supply.

Even amongst the long-term LNG SPAs signed in 2019 and 2020, it can be seen that there was a growing tendency towards shorter contract terms. Data from GIIGNL shows that the weighted average duration of the LNG SPAs signed in 2019 and 2020 was far shorter than those signed in 2018 (Figure 5).

Historically, long-term LNG SPAs had tended to be for terms of at least 20 years, as stable long-term revenues were required to support the high capital costs involved in developing LNG liquefaction projects. In addition, project lenders would typically require that the term of each LNG SPA covered the full tenor of the project loans plus a ‘tail’ of 10 – 50% of the term. This tendency for shorter duration LNG SPAs can be demonstrated by the Mozambique LNG project, which managed to secure approximately US$15 billion in project financing in July 2020, backed by LNG SPAs for 75% of its total production with terms of just 13 – 15 years.

Price recovery and volatility

Figure 4. Share of spot and short-term vs total LNG trade.

Figure 5. Volume weighted average duraton of long and medium-term contracts in years. Following the record-low LNG and natural gas spot prices in April and May 2020, prices gradually recovered. Cancellations of cargoes from US liquefaction projects initially helped to balance the market and, as the world slowly emerged from lockdown, energy demand slowly recovered and US LNG cargo cancellations had all but disappeared by the end of 2020.

This price recovery was further driven by a number of production issues at LNG export projects around the world in 2H20. This included shut-ins at US LNG export projects between August and October 2020 due to hurricane activity; the long-term shutdown of Norway’s Hammerfest project in September 2020 following a fire; and production issues in Qatar, Malaysia, and Nigeria in November 2020. Adding to the supply constraints, extreme cold weather in North-East Asia in December 2020 and January 2021 led to increased gas consumption, and JKM hit a new record level of US$32.5/million Btu on 13 January 2021.

Whilst LNG spot prices quickly fell off after this record high, spot prices gradually rose during 2021, and JKM hit a new record high of US$56.32/million Btu on 6 October 2021. This was driven on the supply side by unplanned shutdowns at LNG export facilities, including the continued shutdown of Hammerfest LNG in Norway. This was also driven on the demand side by droughts in hydro-rich countries, such as Brazil, increased demand in the Asia-Pacific region, and competing demand in Europe due to reductions in Russian pipeline deliveries.

By the end of 2021, spot LNG prices were at historically high levels and were in excess of Brent or Henry Hub-based long-term

contract formulas. This pricing differential, as well as the volatility of an 18-month period that had seen both record highs and record lows in LNG spot prices, provided a strong incentive for buyers to look to lock-in long-term LNG supplies.

Russian invasion of Ukraine

Even prior to the Russian invasion of Ukraine on 24 February 2022, the LNG market was expected to remain tight throughout 2022. Spot LNG and natural gas prices were also at historically high levels, with both JKM and TTF well in excess of US$20/million Btu immediately before the invasion. The Russian invasion exacerbated these issues, and has resulted in LNG and natural gas spot prices remaining both high and volatile throughout 2022. JKM and TTF hit record highs in March 2022, with JKM peaking at US$84.76/million Btu on 7 March 2022.

The Russian invasion resulted in an immediate response from the UK, the US, and the EU, with the imposition of a wide range of sanctions targeting Vladimir Putin and his allies. On 8 March 2022, the EU also announced its ‘REPowerEU strategy’, which aims to reduce the EU’s demand for Russian gas by two-thirds by the end of 2022 and to make Europe independent from Russian fossil fuels by 2030. Given that the EU received roughly 40% of its natural gas from Russian pipelines in 2021, this is an ambitious goal. 2022 has therefore seen countries across Europe, in particular Germany and the Netherlands, accelerating plans for new LNG import capacity. A number of these are utilising pre-built FSRUs, which allow for extremely quick start-up of operations. Two FSRUs commenced operations in September 2022 at Eemshaven in the Netherlands. Two further FSRUs are expected to commence operations in Germany, and one FSRU is expected to commence operations in Finland/Estonia, before the end of 2022.

In connection with this ramping up of LNG import capacity, 2022 has seen European energy companies and utilities seeking long-term LNG supplies in order to replace Russian gas volumes. Whilst the long-term LNG SPAs signed in 2019 and 2020 were for the most part entered into by Asian buyers, the long-term LNG SPAs signed since February 2022 include a number of European buyers. In September 2022, Uniper entered into a 16 year LNG SPA with Woodside, and, in June 2022, EnBW entered into two 20 year LNG SPAs with Venture Global for supply from its Plaquemines and CP2 LNG export projects. Most noteworthy is the entry by ENGIE in May 2022 into a 15 year LNG SPA from NextDecade’s Rio Grande LNG export project. This deal had reportedly been cancelled back in October 2020, as US LNG was viewed as “not aligned with France’s environmental project and environmental vision”.5 The fact that this deal was subsequently entered into following the Russian invasion of Ukraine means that either the environmental concerns of the French government had been addressed, or those priorities had shifted (or perhaps a bit of both). Either way, LNG supply to France became relevant once more.

Whilst the sanctions imposed by the UK, the US, and the EU do not currently prevent the purchase of Russian LNG or natural gas, many countries and buyers outside of the EU are no longer willing to purchase LNG from Russia. Russia accounted for 7.9% of global LNG supply in 2021, so this move away from Russian LNG by many buyers has further added to the tightening of the global LNG market and has led to many buyers looking for new long-term LNG supplies from alternative sources.

Energy security

Recent events have led to energy security, and in particular security of gas supply, becoming much more of a concern for governments, gas suppliers, and gas buyers alike. A long-term LNG SPA provides the certainty of stable supplies of LNG at an agreed contract price formula. Prices under long-term LNG SPAs will still vary in accordance with changes to global oil and gas reference prices (depending upon the applicable pricing basis), but they protect buyers from the extreme volatility that has been seen in the LNG spot market over the last few years.

However, energy security is not simply a concern about the ability to obtain affordable supplies of LNG/gas, but often more critically about the ability to actually procure sufficient supplies of LNG/gas to satisfy demand. During 2022, both Pakistan and Bangladesh repeatedly failed to procure any offers in respect of their LNG tenders. Both countries had to subsequently introduce gas rationing in order to address the resulting shortfall in supply. When markets are tight, LNG supplies will go to the highest (and most creditworthy) bidders. For many countries, long-term LNG SPAs may therefore be the only means of guaranteeing stable supplies during periods of volatility.

Cyclical nature of LNG market

Whilst all of the matters discussed above have contributed to the increase in long-term LNG sales entered into over the last two years, such a ‘return’ to long-term LNG sales was inevitable to some extent due to the often cyclical nature of LNG markets. 2019 and 2020 represented a period of over-supply and low prices in the LNG market, and the market was bound to tighten eventually.

The events discussed above, in particular the Russian invasion of Ukraine, have clearly led to a significant increase in LNG prices, but such an increase was likely in any event given the inevitable tightening of supply after a sustained period of under-investment in LNG export facilities. These events can therefore be seen as the catalyst, rather than the cause, of this increase in long-term LNG contracts.

References

1. Except as provided in Footnote 2, for the purposes of this article, ‘long-term’ is defined as contracts having a supply period of 10 years or more. 2. Please note that, solely for the purposes of this GIIGNL data, ‘long-term’ was defined as contracts having a supply period of 11 years or more. 3. For the purposes of this article, ’mid-term’ is defined as contracts having a supply period of four years or more but less than 10 years. 4. ‘Global Gas Security Review 2020’, International Energy

Agency, (12 October 2020). 5. WHITE, S., and DISAVINO, S., ‘France halts Engie’s U.S.

LNG deal amid trade, environment disputes’, Reuters, (2020), www.reuters.com/article/engie-lng-franceunitedstates-idUSKBN27808