FIGURE 1

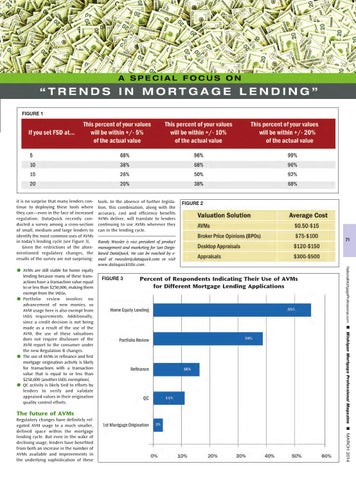

it is no surprise that many lenders continue to deploying these tools where they can—even in the face of increased regulation. DataQuick recently conducted a survey among a cross-section of small, medium and large lenders to identify the most common uses of AVMs in today’s lending cycle (see Figure 3). Given the restrictions of the aforementioned regulatory changes, the results of the survey are not surprising:

Randy Wussler is vice president of product management and marketing for San Diegobased DataQuick. He can be reached by email at rwussler@dataquick.com or visit www.dataquicktitle.com. FIGURE 3

Percent of Respondents Indicating Their Use of AVMs for Different Mortgage Lending Applications

71

n Michigan Mortgage Professional Magazine n MARCH 2014

The future of AVMs Regulatory changes have definitely relegated AVM usage to a much smaller, defined space within the mortgage lending cycle. But even in the wake of declining usage, lenders have benefited from both an increase in the number of AVMs available and improvements in the underlying sophistication of these

FIGURE 2

NationalMortgageProfessional.com

l AVMs are still viable for home equity lending because many of these transactions have a transaction value equal to or less than $250,000, making them exempt from the IAEGs. l Portfolio review involves no advancement of new monies, so AVM usage here is also exempt from IAEG requirements. Additionally, since a credit decision is not being made as a result of the use of the AVM, the use of these valuations does not require disclosure of the AVM report to the consumer under the new Regulation B changes. l The use of AVMs in refinance and first mortgage origination activity is likely for transactions with a transaction value that is equal to or less than $250,000 (another IAEG exemption). l QC activity is likely tied to efforts by lenders to verify and validate appraised values in their origination quality control efforts.

tools. In the absence of further legislation, this combination, along with the accuracy, cost and efficiency benefits AVMs deliver, will translate to lenders continuing to use AVMs wherever they can in the lending cycle.