6

. Michigan Golf Course Superintendents Association | www.migcsa.org

Golf Course Taxes B y N o r m S i nc l a i r - F r e e l a nc e Hall of Fame

writer and member of the

Michigan Journalism

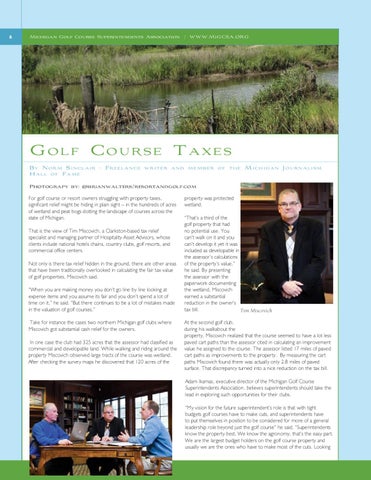

Photograpy by: @brianwalters/resortandgolf.com For golf course or resort owners struggling with property taxes, significant relief might be hiding in plain sight – in the hundreds of acres of wetland and peat bogs dotting the landscape of courses across the state of Michigan. That is the view of Tim Miscovich, a Clarkston-based tax relief specialist and managing partner of Hospitality Asset Advisors, whose clients include national hotels chains, country clubs, golf resorts, and commercial office centers. Not only is there tax relief hidden in the ground, there are other areas that have been traditionally overlooked in calculating the fair tax value of golf properties, Miscovich said. “When you are making money you don’t go line by line looking at expense items and you assume its fair and you don’t spend a lot of time on it,” he said. “But there continues to be a lot of mistakes made in the valuation of golf courses.” Take for instance the cases two northern Michigan golf clubs where Miscovich got substantial cash relief for the owners. In one case the club had 325 acres that the assessor had classified as commercial and developable land. While walking and riding around the property Miscovich observed large tracts of the course was wetland. After checking the survey maps he discovered that 120 acres of the

property was protected wetland. “That’s a third of the golf property that had no potential use. You can’t walk on it and you can’t develop it yet it was included as developable in the assessor’s calculations of the property’s value,” he said. By presenting the assessor with the paperwork documenting the wetland, Miscovich earned a substantial reduction in the owner’s tax bill. Tim Miscovich At the second golf club, during his walkabout the property, Miscovich realized that the course seemed to have a lot less paved cart paths than the assessor cited in calculating an improvement value he assigned to the course. The assessor listed 17 miles of paved cart paths as improvements to the property. By measuring the cart paths Miscovich found there was actually only 2.8 miles of paved surface. That discrepancy turned into a nice reduction on the tax bill. Adam Ikamas, executive director of the Michigan Golf Course Superintendents Association, believes superintendents should take the lead in exploring such opportunities for their clubs. “My vision for the future superintendent’s role is that with tight budgets golf courses have to make cuts, and superintendents have to put themselves in position to be considered for more of a general leadership role beyond just the golf course” he said. “Superintendents know the property best. We know the agronomy, that’s the easy part. We are the largest budget holders on the golf course property and usually we are the ones who have to make most of the cuts. Looking