“I am sure that we will achieve the goal of fortifiying this great enterprise (CFE), for the good of our people, for the sake of workers and for the sake of Mexico”

The publisher has made all reasonable efforts to provide accurate information, and the information contained in this publication is derived from sources believed to be true and accurate. However, the information in this publication should not be considered to be complete or definitive, and may contain inaccuracies or typographical errors. The publisher accepts no responsibility regarding the accuracy of information and use of such information is at your own risk. The publisher will not be liable to any party for any direct, indirect, special or other consequential damages arising out of any use of information in this publication. The publisher provides no representations or warranties, express or implied, including any implied warranties of fitness for a particular purpose, merchantability or otherwise in relation to any information provided by the publisher in this publication.

ISBN: 978-1-7328256-2-8

2019

Mexico underwent a presidential transition in 2018 that rippled across the energy industry, with uncertainty facing the sector. President Andrés Manuel López Obrador’s administration was loud and clear from the beginning about its mandate to boost Mexico’s electricity generation and cope with the country’s increasing energy demand. His ambitious National Electricity Program, executed by Manuel Bartlett, the newly instated Director General of CFE, set a course to revamp the country’s coal-fueled power plants, geothermal plants and hydroelectric installed capacity. One key aspect of López Obrador’s plan that remains unclear is whether or not the new energy model, led by Rocío Nahle, Minister of Energy, will continue using the tools employed by the previous administration to achieve not only the goal of supplying the country’s energy demand but also aligning its energy production to its international commitment of increasing the participation of renewable energy to 35 percent of the total mix by 2024. The first actions taken by the administration suggested it would not be business as usual. Alfonso Morcos, the new Director General of CENACE, announced the suspension of the fourth edition of the long-term electricity auctions in December. These auctions were the prime tool of former President Enrique Peña Nieto’s Energy Reform to award and incentivize the development of large-scale clean energy projects. CRE also saw a massive reduction in its budget for 2019.

Whether López Obrador keeps the door open for future editions of the long-term electricity auctions, 2018 showed that Mexico is already experiencing an open market where new and better technologies are being deployed throughout the country. Mexico Energy Review 2019 looks back at the milestones achieved in 2018, while exploring the role of conventional and renewable power generation technologies as the country copes with the needs of a more sophisticated and informed electricity market.

Grupo Mexico's El Retiro wind farm, Juchitan, Oaxaca

STATE OF THE INDUSTRY

1Three long-term electricity auctions and one midterm auction later, Mexico demonstrated in 2018 that renewables are here to stay. As the energy mix gets greener, the country is further developing its renewable energy value chain and final users will see the impact in their electricity bill if this growth is enhanced in the coming years. In the meantime, Mexico’s industrial segment will be gas-fueled, and a strategy regarding production, transportation and distribution needs to be established for guaranteeing grid reliability, coping with rising demand and transitioning toward a low-carbon future.

By the end of 2018 and with a new federal administration in place, uncertainty reigned and calls for Energy Reform continuity bellowed from all corners of the industry. Important auction processes for developing generation and transmission infrastructure have been put on hold and the new administration will have the final vote in this matter. State of the Industry presents the voices of the key policymakers, regulators and industry leaders who are collaborating on the development of the new energy model to provide a clear picture of the current landscape.

CHAPTER 1: STATE OF THE INDUSTRY

The

12 VIEW FROM THE TOP: Leonardo Beltrán, Ministry of Energy

13 VIEW FROM THE TOP: Fernando Zendejas, Ministry of Energy

14 ANALYSIS: A New Era for Productive State Enterprise

16 VIEW FROM THE TOP: Guillermo García, CRE

18 VIEW FROM THE TOP: Eduardo Meraz, CENACE

20 VIEW FROM THE TOP: José María Cu Cañetas, Energy Agency of the State of Campeche

21 VIEW FROM THE TOP: José Luis Calvo, SEMAEDESO

22 VIEW FROM THE TOP: Christoph Frei, World Energy Council

23 VIEW FROM THE TOP: Odón De Buen, CONUEE

24 VIEW FROM THE TOP: Angélica Quiñones, ANES

25 VIEW FROM THE TOP: Javier Romero, AMFEF

26 VIEW FROM THE TOP: Montserrat Ramiro, CRE

27 VIEW FROM THE TOP: Guillermo Zúñiga, CRE

28 VIEW FROM THE TOP: Alfredo Álvarez, EY

30 VIEW FROM THE TOP: Noé Pascacio, BGBG Abogados

31 VIEW FROM THE TOP: Juan Vargas, Deloitte Consulting

THE YEAR IN REVIEW

2018 was a decisive year for the consolidation of Mexico’s energy model. Added renewable energy capacity and a burgeoning number of market players are some of the results of this model but a new administration is promising to shake things up as the industry calls for continuity

The state of Mexico’s energy industry is strong, even if uncertainty remains the flavor of the day. With regulations shaping up to address nascent needs, the pieces are in place to continue consolidating the Energy Reform. But the election of President Andrés Manuel López Obrador, who has promised to focus on conventional energy sources, has spurred calls from the sector for continuity. The new administration, inaugurated in December 2018, quickly moved to show its hand with the suspension of the fourth long-term electricity auction and the Baja California – National Interconnected System Transmission Line while pushing back the scheduled tender for the key Yautepec – Ixtepec Transmission Line. How AMLO’s plans play out will determine the landscape for the next six years. For now, the president and his government take over an industry that has been internationally acclaimed for the speedy implementation and successes of its reform.

One sure sign of consolidation is the imminent conclusion of the regulatory process that provides all the tools for an operational energy market to be fully functional and increasingly renewable. Looking to find further efficiencies for the transition, the industry’s regulators CRE, CNH and ASEA, materialized their coordination efforts with the creation of ODAC, the Coordinated Assistance Office of the Energy Industry, to facilitate the permitting procedures of market players looking to capitalize on the unlocked opportunities in the energy value chain. Nevertheless, these efforts might be limited by the reduction of budget that regulatory entities have suffered with AMLO’s entrance to office, translating in bottlenecks within their operations. As Mexico’s energy

The Ministry of Energy publishes the Contracting Manuals for Transmission and Distribution Services’ Coverage as well as the Manual for the Development of the Market Rules in the Official Federal Journal

Mexico officially joins the International Energy Agency

CRE presents its 2018-2022 Strategic Plan and also publishes its 2018-2022 Business Plan

CENACE publishes the official results of the first midterm electricity auction

CRE and CENACE publish the call for proposals for the fourth long-term electricity auction

Enel Group inaugurates its 754MW Villanueva PV plant in Coahuila

mix is injected with additional renewable energy capacity, natural gas is expected to play a critical role as a transition fuel, either through continued imports or increased domestic production, which López Obrador is championing. Cheaper and more environmentally-friendly compared to other conventional fuels, access to natural gas can detonate the regional development of Mexico’s economically vulnerable southern region.

The country also took steps in 2018 to prepare its transmission and distribution infrastructure to absorb the intake of the tobe installed 8GW of renewable energy capacity. According to CRE’s database, the state of Oaxaca alone cumulates 2,346MW of operational wind power capacity, as of October 2018, and will welcome an additional 411MW before 2021. While this renewable energy landmark is good news for the country’s clean energy ambitions related to the 2024 horizon, the renewable power generation potential of Oaxaca’s Tehuantepec Isthmus risks facing a transmission bottleneck. To that end, the tender of the Yautepec – Ixtepec Transmission Line project is meant to interconnect the state of Oaxaca with the state of Morelos to transport the state’s power generation to the energy-intensive center region. The project is estimated to require an investment of US$1.2 billion and after several rescheduling announcements, CFE announced it will receive project proposals in February 2019 and the tender winner is set to be announced by March 2019. The other transmission flagship project is Baja California’s interconnection tender to connect both states to the rest of the country’s National Interconnected System. The transmission line is estimated

Pedro Joaquín Coldwell, Minister of Energy, states that Mexico is among the 10 most attractive countries for investment in renewable energy

The energy sector has raised MX$202 billion in the BMV, an amount that represents 14 percent of all CKDs

Public tenders for HDVC lines to connect Baja California with the rest of the country and to dispatch energy from the Isthmus of Tehuantepec to the center of the country attract 22 and 28 participants respectively

to be 1,400km long and will be the first HVDC current transmission line in the country. Conducted by the Ministry of Energy, the tender attracted the interest of 109 companies and counts seven pre-qualified offers. The tender winner is scheduled to be announced by February 2019.

MERCHANT PROJECTS, BILATERAL PPAs

With a cumulated pipeline of 58 clean energy projects amounting to 8GW of installed capacity and US$8 billion in investments, Mexico’s long-term electricity auctions have consolidated their status as the success story of the country’s energy transition and its 2024 landmark objective of 35 percent of clean energy generation. Although the fourth-auction has been suspended, the aggressive package prices showcased in previous editions have limited auction participation to a specific player profile. This profile includes utility-comparable companies with the business model and financial capacity to enable an efficient and standardized project development model suitable for utility-scale projects. “I expect a market segmentation in which lower-volume projects can be pursued, opening the door to better offer prices and higher investment returns. But we cannot expect the case of a large market buyer to become a generalized rule for the industry. It would be a mistake to believe that the wholesale electricity market will provide the same conditions to all when not all have the same purchasing power,” says Rubén Cruz, Energy and Natural Resources Lead Partner of KPMG.

The design of Mexico’s energy market avoids cornering project developers to rely on a single scheme. On the contrary, it incentivizes companies with different risk preferences and commercial objectives to look for alternatives in the market. Mexico is consolidating a pool of project sponsors and IPPs that are more comfortable relying on nodal prices and private off-takers rather than auction prices and CFE as the final off-taker. “Merchant projects obtain financing under much shorter terms compared to long-term electricity auction projects, calling for a primarily equity-based financial

structuring. Mezzanine finance can provide a risk-mitigating bridge between attractive short-term yields and long-term uncertainty, characteristic of merchant projects. The ideal scenario is to gradually migrate from project finance to corporate finance based on a sufficiently large critical mass of projects for a strengthened refinancing capacity that provides a capital structure much more adequate for merchant projects,” says Andrés Millán, Chief Investment Officer and Co-Head of the IFC’s China-Mexico Fund. As Mexico’s project finance practice gains sophistication and more financial entities are enticed by this alternative, the country is poised to witness an increased number of merchant projects and bilateral PPAs, fostered both by auction results and the increasing electricity demand from the country’s industrial tissue. “A significant contingent of multinational sponsors that have certain constraints on capital structure were not thrilled or not even able to participate in the long-term auctions because of the low pricing obtained in the coverage contracts. These low levels made certain assumptions about merchant revenues that not everyone was willing to accept, including financial institutions. We believe the emergence of bilateral PPAs to be incredibly positive. For one, it means that more developers are pushing the commercial side of their business and not just relying on CFE. Second, a pool of industrial players willing to sign these PPAs is steadily growing, meaning they are getting more involved so they can enter into commercial conversations with project sponsors. It is a growing trend that will consolidate as we move forward under the new administration,” says Salomón Amkie, Vice President, Head of Power and Utilities for Citibanamex.

FINANCIAL RIGHTS OF TRANSMISSION

According to CENACE’s latest figures, Mexico’s wholesale electricity market counted 140 operational participants and 68 in the process of asset registration. Out of these 72 active participants, 46 are power producers, 17 are qualified suppliers, seven are non-supplying traders, with one intermediation power producer and a basic supply provider. CENACE also

Andrés Manuel López Obrador wins presidential election

CFE ends its efforts to obtain an amparo against CRE’s administrative provisions for distributed generation

The results of the public auction for the construction and operation of the HVDC transmission lines connecting Oaxaca to Morelos is postponed for the fourth time

The biggest wind farm in Mexico, located in Tamaulipas, starts operations with 424MW

CENACE announces plans to inject 12.429GW of new power generation into the grid during 1H19

MORENA’s parliamentary group in the Deputies Chamber presents an Organic Law Proposal for regulatory bodies CNH and CRE to become part of the Ministry of Energy

Mexico’s fourth long-term electricity auction is suspended

AMLO inaugurated as president

AMLO unveils his National Electricity Plan and CRE suffers a budgetary cut of 26 percent

Rocío Nahle enters office as the new Minister of Energy

CENACE announces Alfonso Morcos as new Director General

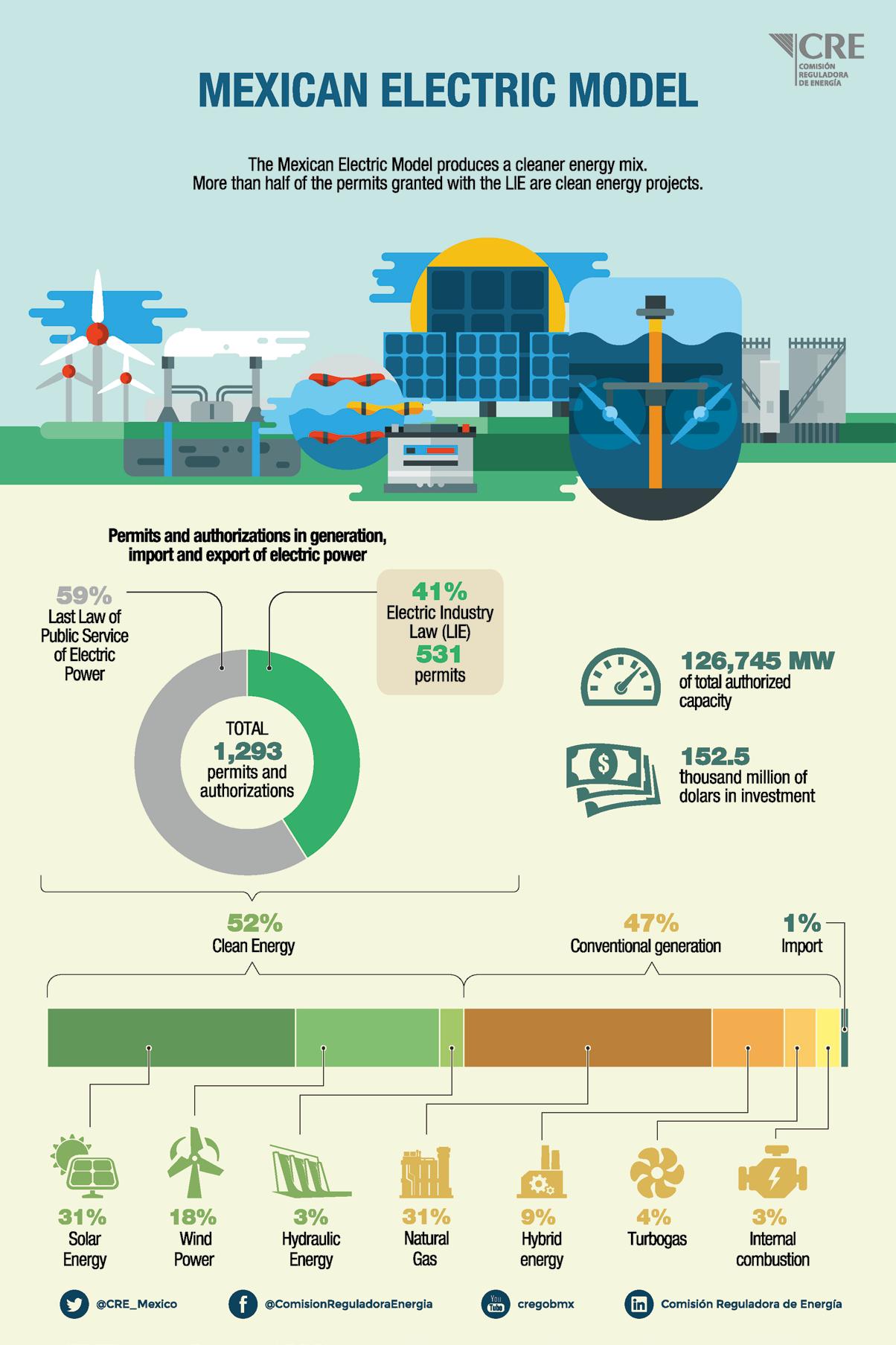

Primary Energy Production in 2017

TOTAL GENERATION (GWh)

329,163

78.9% Conventional

21.1% Clean

Primary Energy Production in 2017

TOTAL CONVENTIONAL ENERGY GENERATION (GWh)

registered energy transactions in the spot, day-ahead and hour-ahead markets, signaling the first steps toward market liquidity and generalized transactions. The road toward market maturity remains lengthy, as observed by Alejandro Blanco, Co-Founder of Tradeon Energy. “The fundamental problem is that qualified suppliers require hedging contracts to operate but have limited capacity to sell their retail products. It helps little that they often overlook the need to get involved in the wholesale hedging market, which provides access to Capacity Bilateral Transactions (TBPot), Energy Bilateral Transactions (TBFin), CELs and financial derivatives, such as swaps. This means the conditions required for new qualified suppliers to be competitive are absent. Without a strong retail segment requiring hedging and bilateral contracts, wholesale cannot prosper,” he says.

259,766

63.6% Combined Cycle

16.5% Conventional Thermoelectric

11.8% Coal

4.9% Turbogas

1.7% Internal Combustion

1.5% Fluidized Bed

Primary Energy Production in 2017

TOTAL CLEAN ENERGY GENERATION (GWh)

69,398

45.9% Hydroelectic

15.7% Nuclear

15.3% Wind

10% Efficient Cogeneration

8.7% Geothermal

2.8% Bioenergy and FIRCO

1% Distributed Generation

0.5% Solar

0.1% Regenerative Breaks

Source: Ministry of Energy

The infant market has yet to adjust to the detected imbalance between power energy and CEL prices showcased in the auctions and those reflected in the spot market, determined by node marginal prices. “Qualified users are constantly on the lookout for the best price levels. In our experience, they are aware that their trading price tags will not reach longterm electricity auction levels. I believe the imbalance comes rather from trading terms rather than price levels,” argues Juan Guichard, CEO of Ammper Energía. He also highlights the need for broader financing. “Another pending issue that is needed to boost energy trading is the increased involvement of financial entities. By crafting bankable long-term PPAs with solid warranties, financial entities can contribute to mitigating the inherent long-term risks in energy trading transactions.”

The remaining ingredient for a fully operational wholesale electricity market eagerly awaited by market participants are financial rights of transmission. “It is the only puzzle piece left of fundamental importance for the qualified supply market,” says Marcelino Madrigal, Commissioner at CRE. “In essence, these mechanisms provide the possibility to purchase rights over congestion pricing. This means acquiring the rights, through an auction, obtaining the rights over node price differentials between energy injection and extraction. They essentially act as a shield for power producers and qualified users over electricity price variability over time.”

FUELING ECONOMIC GROWTH

Despite Mexico’s commendable efforts to transition toward renewable energy, natural gas still accounts for 70 percent of fossil fuel demand for power generation purposes. According to PRODESEN 2018-2032, combined cycle generation alone accounts for half of the country’s power generation. Highly cost-effective and environmentally friendly, Mexico’s access to natural gas’ cheapest market, the US, has placed this fuel at the center of the country’s power generation plans to transition toward renewable energy. In 2014, CFE made the decision to adapt its thermoelectric plants to dual combustion

processes to gradually transition from fuel oil to natural gas. This process is ongoing.

Given natural gas’ contribution to the country’s power supply, it comes as no surprise that CENAGAS is looking to use natural gas as a lever for national development and reach greater economic growth rates. The national pipeline administrator, announced a MX$1.75 billion investment on the Yucatan Peninsula. “Part of this investment will be allocated to the reconfiguration of the Zempoala compression station and the interconnection of the Tuxpan pipeline. Another project to be financed by this investment is Engie’s interconnection between the Mayacan system with SISTRANGAS pipelines in the southeastern region of the country to freely transit toward the Yucatan Peninsula. Engie is additionally investing in the Mayacan pipeline to increase compression capacity and possible flow. Its capacity is close to 0.25Bcf/d while flows have yet to surpass the 0.08Bcf/d mark,” says David Madero, Director General of CENAGAS.

To guarantee reliability and safety to natural gas supply for power generation purposes, CENAGAS and CENACE, the electricity system administrator, modified a critical coordination agreement signed in 2015 two years after its initial signature, in September 2017. “Our core objective as control centers is to offer the safest, most reliable and efficient transport system aligned perfectly with CENACE’s mission to offer an electricity system that is equally safe, reliable and efficient. In this sense, part of our work requires us to provide feedback related to project demand growth projections for electricity and natural gas, coupled with ensuring the safety and reliability of natural gas supply to enable a solid electricity industry. When operating with a vision of natural gas as a transition fuel, it is particularly critical to enable the support it can provide to tackle renewable energy intermittency. This is why constant coordination between CENAGAS and CENACE is equally critical. The first fruits of this collaboration have resulted in planning improvements, emergency reaction and management between both control centers as well as administrative efficiencies,” Madero added.

PREPARING MEXICO’S SMART GRID

Distributed generation, decentralized microgrids and energy storage technology are but a few of the technological disruptions called to profoundly transform how Mexico has traditionally produced, transmitted, distributed and consumed its electricity. Extending Mexico’s electricity transmission and distribution infrastructure is but one aspect of how the exponential growth of the country’s electricity consumption can be addressed. “In the case of energy storage, ROIs are averaging five years. For the grid operator, that translates into a reliable power supply, meaning stable frequency and voltage. For power producers, it provides the possibility of storing energy and trading it in the market at a more convenient

time based on electricity rate variability. For final users, it unlocks the possibility to shave the maximum peak demand and significantly reduce electricity bills at a time when they are expected to steadily increase. It also provides long-term certainty over electricity costs,” says Alejandro Preinfalk, Vice President of Energy Management at Siemens Mexico.

For Oscar Miranda, Co-Founder and President of Smart Grid Mexico, smart grids in the country have left the theoretical realm to materialize in the country’s day to day electricity supply. “All the necessary measurements for correct billing in the WEM are fully automated and every operation related to the security and protection of the electricity grid in Mexico is done with telecommunication protocols that are automated. As a matter of fact, for the WEM to work properly every process has to be fully automated. As for DG projects, they also need smart grids for participants to measure bidirectional energy fluxes and to bill clients correctly,” he says.

CRE is redoubling efforts to make sure Mexico’s regulatory framework is entry-barrier free for new technological developments designed to assist the country’s electricity transmission and distribution. “The electricity rates CRE approves for CFE recover the grid’s operation, maintenance and growth costs. CRE has a regulatory mechanism in place where, provided the right rates, CFE, in its role as electricity transmitter and distributor, has the required incentives to improve the grid. On the innovation side, the Ministry of Energy drafted a smart grid plan in 2016, approved by CRE, with information provided from CENACE. CFE’s grid expansion plan therefore includes investments in innovative technologies, such as smart metering,” says Madrigal.

THE AMLO ADMINISTRATION

The wrench in the machinery for the energy industry is the new government presided by López Obrador. His calls to revisit, and potentially revise, the Energy Reform rattled investors throughout 2018 as the presidential campaign unfolded and with AMLO’s victory and subsequent inauguration. Industry insiders have been unified in their calls for continuity in the reform, which they view as mostly successful. The signs so far have been mixed. López Obrador took office with a blistering attack on the Energy Reform, which he said “had only meant a drop in oil production and rise in gasoline prices.” He has vowed to strengthen both PEMEX and CFE as productive enterprises of the state with a mandate to thrive under market conditions, bolstering both their budgets for 2019. The suspension of the fourth long-term auction also helped crack the egg of certainty that had settled over the industry. The new administration has also expressed interest in revamping the country’s hydroelectric assets and has been adamant about securing the continuity of renewable energy’s penetration in the energy mix. For now, the stage is set. The market is only waiting to see how it unfolds.

ENERGY EFFICIENCY AS ENERGY POLICY 2.0

LEONARDO BELTRÁN

Former Deputy Minister of Planning and Energy Transition

Q: How does Mexico’s 2012 energy mix contrast with 2018 and is the country on track to meet its 2024 objectives?

A: Since 2012, we have expanded our installed wind power capacity sevenfold and PV generation’s installed capacity grew 48 times, from 34MW in 2012 to 1,677 MW by 2018. The Ministry of Energy laid the groundwork for the legal framework to ensure it was conducive to reaching our 2024 goals. The data is there to assess our progress. The World Bank ranks the sustainability of the energy policies of 111 countries, including renewables, energy efficiency and electricity access. Overall, Mexico ranked 14th in 2017. Bloomberg New Energy Finance placed Mexico in the Top 10 renewable energy investment destinations in 2017. Mexico alone represented over onethird of clean energy investments in Latin America that same year. Mexico went from being among 2012’s Top 30 to 2018’s Top 13 most-attractive countries in EY’s Renewable Energy Attractiveness Index. It is quite encouraging to see Mexico in such good standing on the international stage.

Q: What would you have done differently during your term?

A: In retrospect, energy efficiency should have been considered an essential component of the WEM, comparable to CELs. Energy efficiency should be the Energy Transition Policy 2.0 for the new administration. We also should have paved the way to unlock CFE’s access to capital markets and to list on the Mexican stock exchange. CFE is difficult to compare to a similar fully private and stock marketlisted corporation as it does not operate under the same conditions nor does it have the same corporate mandate. Listing CFE on the Mexican stock exchange has the potential of doing wonders for its corporate governance, financial health and overall competitiveness, both at the national and international levels.

Q: How is Mexico preparing to integrate disruptive technologies such as EV, energy storage and blockchain?

Leonardo Beltrán has 13 years of experience serving in the Ministry of Energy, first as International Negotiations Director from 2005 to 2010. He then served as Director General of Information and Energy Studies until his former appointment in 2012

A: It is a matter of pending regulation, which CRE is in the process of concluding, to make sure it answers to market requirements and can establish a seamless cohabitation between the traditional, centralized power generation model and the growing decentralized system. Going forward, we need to think about preparing the regulatory framework for new, flexible models that can enable the use of disruptive technologies, such as EV, energy storage and blockchain. In terms of electricity transmission and distribution infrastructure, Mexico needs to both extend it and rely on distributed generation systems, as witnessed by the exponential growth in the number of distributed generation interconnection contracts. Mexico’s energy security is based on relying on a mix of optimal options and this administration excluded no possibility as long as it contributed to the energy security goal.

Q: What flagship project showcases the success of Mexico’s energy transition?

A: Coahuila is now home to the second-largest PV park worldwide, located in Villanueva. It is the direct result of the country’s Energy Reform. The next largest Mexican PV park is being built in Tlaxcala, with an installed capacity of 500 MW. Geothermal is also enjoying a second wind with private players developing projectsas a result of the reform. Mexico’s southern region would not have seen wind and solar projects if not for the regulatory framework that fostered their seamless development, including social and environmental impact assessments.

Q: What changes do you expect from the new administration?

A: The new administration has a specific vision and set of actions for what needs to be done to foster the growth of the energy industry. This vision obeys to a moment in Mexico’s history when the country did not have as many trade and investment connections with the international economy as we have today. Now, Mexico has one of the most extensive lists of trade agreements worldwide. As per the World Bank’s latest figures, international trade amounts to 77.56 percent of Mexico’s GDP. As Mexico is a market-driven economy, it makes sense to inject market forces into the country’s electricity industry, such as the design and launch of the wholesale electricity market.

MEXICO WILL KEEP THE SWITCH ON

FERNANDO ZENDEJAS

Former Deputy Minister of Electricity at the Ministry of Energy

Q: How does the Deputy Ministry of Electricity expect the energy mix to evolve in the coming years?

A: Regarding installed capacity, this administration will conclude with 31 percent of clean energy generation. Taking into account intermittency in effective generation, the total is around 21 percent. Nevertheless, with the installation of new plants, the country evolved from 62,000MW in 2012 to 78,000MW in 2018. Half of the additional 16,000MW comes from clean energy sources. If this growth continues, in the next 15 years conventional thermoelectric plants will decrease their participation in the energy mix. Regarding natural gas, this fuel represents half the country’s electricity generation and as long as it remains abundant, has a small carbon footprint and is governed by competitive prices, it makes sense to keep it in the mix. Additionally, there are other technologies that are reliable and consistent, such as nuclear energy. Laguna Verde’s two reactors supply close to 5 percent of the national electricity demand and the PRODESEN aims to duplicate this capacity in the coming years. This will represent a huge investment for CFE as particulars cannot participate in this segment due to national security and constitutional restrictions.

Q: What were the three main contributions of your office to the national electricity industry during this administration?

A: Primarily, we opened an opportunity for the industry to participate directly in transmission and distribution infrastructure projects. At the moment, there are two important tenders on the agenda regarding the construction of transmission line projects. The first will be in association with CFE for the Ixtepec-Yautepec Transmission Line project that will interconnect Oaxaca and Morelos. The second is a private project involving the interconnection between the National Interconnected System and Baja California. The latter will be the first project in the country’s history to install DC lines for electricity transport.

The second contribution was the introduction of the new plant construction model that stands out from the four modalities established in the 1992 Electricity Legislation. These were self-supply, independent power producers, small producers and cogeneration. With the current model,

any company that aims to generate electricity and complies with the requirements stated by CRE and CENACE can do so. Finally, the third contribution is the creation of the qualified supplier figure, which is considered a milestone because it provides certainty for long-term investments and a more dynamic and competitive market.

Q: What three main topics should the next administration prioritize in the electricity industry agenda?

A: First, it should prioritize preventing possible congestions that might take place in the transmission lines, mainly in nodes that are seeing increasing demand, such as the Yucatan Peninsula or Monterrey’s metropolitan zone. Second, it should follow the market rules as established, executing a long-term electricity auction per year. Third, rural electrification is a pressing issue.

Q: Looking at the electricity system as a whole, what energy policies are required to meet the country’s needs?

A: The best thing any future administration can do is to respect the symbiosis between state planning, executed by the Ministry of Energy, administrated by CENACE, regulated by CRE and developed by CFE as the country’s productive enterprise. Complementing this with private investment, long-term planning and the best technology available is mandatory. Despite the political landscape, the country will keep flipping the switch on, and current and future electricity demand will need transmission and distribution infrastructure to supply energy at the required pace.

Regarding CFE, if the government decides it will have fewer than six subsidiaries, that will not pose a problem. The Constitution provides the guidelines for a competitive industry. Having a CFE that is efficient and more competitive every day does not close the doors to other participants. I hope the next administration agrees with this as well.

Fernando Zendejas was appointed Deputy Minister of Electricity at the Ministry of Energy in November 2017. Zendejas’ experience in the energy sector includes roles with PEMEX, CFE, CENACE, CENAGAS, the IEA and INEEL

A NEW ERA FOR PRODUCTIVE STATE ENTERPRISE

CFE looks to the future, armed with a bigger budget and a mandate to again take the leading role in supplying Mexico’s energy needs, following the priorities outlined by President López Obrador in his National Electricity Program

A new era dawned for CFE on Dec. 1, 2018, when Director General Jaime Hernández officially passed the torch to Manuel Bartlett, who wasted little time in outlining the productive state company’s priorities for the next six years of President López Obrador’s term. In line with the government’s priorities and armed with a bigger budget, CFE will pursue coal, geothermal and hydropower as it moves to supply a rising demand for energy.

AMLO intends for CFE to use its muscle, along with fellow state company PEMEX, to put the country on the path to energy self-sufficiency. CFE’s budget for 2019 has been pumped up to MX$434.7 billion, giving it an extra MX$20 billion. Bartlett, a Mexican lawyer who has held various political positions, has announced investments in coal, with MX$10.4 billion pledged to rehabilitate coal plants, and MX$980 million and MX$340 million committed to geothermal and hydroelectric plants, respectively.

CFE’s

Hydropower, in particular, is a mainstay of AMLO’s National Electricity Program, announced in December. At the same time, Bartlett outlined CFE’s strategy to modernize the country’s hydroelectric plants. “In close collaboration with CFE and CONAGUA, we have studied the possibility of increasing hydro-energy capacity in the mix with an additional 3,300MW,” he said. “We have significant feasibility projects to install 2,000MW by taking advantage of 363 hydroelectric structures used for irrigation.”

The beefy budget for CFE was a concern for ratings agency Moody’s, which had improved its outlook for the company in April to stable from negative. Writing in a report following the budget announcement, sovereign analyst Jaime Reusche said the importance placed on CFE and PEMEX in the 2019 budget “generates concern around the possibility that the parastatals become a recurrent burden for the federal government that

potentially deteriorates the sovereign credit profile in the medium term.”

Fernando Zendejas, former Deputy Minister of Electricity at the Ministry of Energy, says, however, that a stronger CFE is not a problem. “The Constitution provides the guidelines for a competitive industry. CFE is the national electricity company and we are proud of it. Having a CFE that is efficient and more competitive every day does not close the doors to other participants."

for his part, Bartlett maintains that the company’s energy capacity and its human organization had suffered during the last few administrations. “Financial limitations, tariff insufficiency and the nontransfer of subsidies for residential and agriculture segments” are some of the reasons he gave. Others include a lack of maintenance and modernization, arbitrary retirements, inconsistent structural reforms and a change in CFE’s mission. “(These factors) have provoked a critical financial situation.”

AUCTION RESULTS FELT

Of concern to the market is the suspension of the longterm electricity auctions after three editions. Although there were no electricity auctions in 2018, benefits of previous editions began to be felt by many – none more so than CFE, according to Héctor Olea, President of the Mexican Association of Solar Energy (ASOLMEX). “Renewable energy sources have dominated every edition. The participant that has most benefited from this scheme is CFE,” he says. “This company has never purchased electricity as cheap as the prices obtained during the auctions. Under this mechanism, the productive enterprise of the state does not invest any money, nor does the state.”

In June 2018, Fitch Ratings gave CFE a AAA rating. Marian Aguirre, Energy Finance Vice President of Bancomext, believes the triple-A status of the country’s biggest offtaker aided the success of the auctions because the thin margins for projects match the equally thin development risk. “As long as CFE maintains a position of leadership as an off-taker, development banking institutions will be able to contribute from a more comfortable position,” she says. However, in November, Fitch downgraded CFE’s Outlook from stable to negative and downgraded

its rating to BBB+ after López Obrador announced the cancellation of the Mexico City airport project (NAIM).

TARIFFS

Also bolstering CFE in 2018 was the tariff regime that allows the company to recover its costs. Prior to the Energy Reform, CFE was mandated with supplying energy to the country, establishing its own tariffs and overseeing its own infrastructure development. However, with the passing of the reform came an independent body, CRE, that would take over the establishment of tariffs. This was done with the expectation that private companies could compete with the state-owned enterprise, effectively increasing competition in the country and reducing electricity costs for final users without the need to provide government subsidies.

Leonardo Beltrán, former Deputy Minister of Planning and Energy Transition at the Ministry of Energy, says 2018 was an interesting year in terms of electricity tariffs. “The tariff we had before 2018 was a closed fee that obeyed to an income objective and that did not recover CFE’s costs, so every year CFE saw its assets reduced,” he explains.

As a result of the LIE, CRE is now responsible for setting tariffs for CFE, and according to Marcelino Madrigal, this was done in a way that allows CFE to recover the grid’s operation, maintenance and growth costs, meaning it can continue to compete with private companies entering the country. “CRE has a regulatory mechanism in place where, provided the right rates, CFE, in its role as electricity transmitter and distributor, has the required incentives to improve the grid,” he says.

THE NATIONAL GRID

The Ministry of Energy drafted a smart grid plan in 2016, approved by CRE. “CFE’s grid expansion plan includes investments in innovative technologies, such as smart metering,” says Madrigal. “CFE even launched a portal within its website for users to determine if the grid has the capacity to absorb a distributed generation system in a specific location, residential or other.”

Mexico’s total installed grid capacity as of September 2018 was 75,685MW. CENACE says that 12,429MW of extra capacity would enter into operation in the National Interconnected System by June 1, 2019. This total capacity will be generated by 84 new power plants that will be installed in 22 entities in Mexico, of which 6,380MW, or 51.3 percent of the new capacity, are renewable technologies and the remaining 6,049MW, or 48.6 percent, are conventional sources.

BALANCING THE BOOKS

As it embarks on a new era, CFE finances remain stable despite losses in the in the year to September 2018.

Revenues from Oct. 1, 2017 to Sept. 30, 2018 totaled MX$361.4 billion, a 0.4 percent increase on the MX$359.8 billion registered in the same period of 2016-17. Sale of energy accounted for the greatest revenue, contributing MX$261.7 billion.

INSTALLED CAPACITY BY MODALITY (MW)

Source: PRODESEN

However, CFE made net losses of MX$37.8 billion during this period, compared to net income of MX$34.5 billion for the same period in 2016-17.

As of Sept. 30, debt had increased by MX$24.5 billion to MX$356.9 billion compared to MX$332.5 billion registered at year-end 2017. In its financial report, CFE indicated that an unfavorable exchange rate, amortization payments and debt repayment amounted to MX$127.1 billion. EBITDA dropped in the third quarter of the year to MX$15.3 billion compared to MX$31.9 billion during the same period in 2017.

Looking to the future, Beltrán believes that, just like PEMEX, the state-owned electricity company would be more profitable and transparent if all or part of it were to launch an Initial Public Offering. “We should have paved the way to unlock CFE’s access to capital markets and to list on the Mexican stock exchange,” he says. “CFE is difficult to compare to a similar fully private and stock market-listed corporation as it does not operate under the same conditions nor does it have the same corporate mandate. Listing CFE on the Mexican stock exchange has the potential of doing wonders for its corporate governance, financial health and overall competitiveness, both at the national and international levels.”

TRANSITIONING TO THE NEW ENERGY POLICY

GUILLERMO GARCÍA President Commissioner of CRE

Q: What were the most relevant developments in the Mexican energy market in 2018 and which CRE achievements during last year make you most proud?

A: In electricity, there was a great advancement in distributed generation, which is the democratization of energy, the possibility that any consumer, regardless of size, can take control of his or her electricity bill. This is something that a few years ago was unthinkable and CRE provided the legal framework for this development, which has many benefits. The first is that consumers can determine how much they will pay for energy use.

Having multiple injections to the distribution network creates a more stable system with frequency regulation and high-power services throughout the day. Moreover, this development is creating employment opportunities and strengthening the Mexican industry, which is a priority for the new presidential administration. Distributed generation has the enormous advantage of requiring a great deal of human capital. For instance, in the US, there are over 100,000 employees in California alone focused on distributed generation. This means that distributed generation has the capability of creating well-paid jobs throughout the country.

It is important to highlight that we finished 2018 with approximately 82,000 solar roofs, which represent around a 70 percent increase from 2017. This increase is the result of the simplified regulation we created for the interconnection, which is a non-permitted activity that requires an interconnection contract with the distribution system. The contract we designed for this purpose, in only two pages, outlines all conditions and users can choose the interconnection modality, which can be net metering, net billing or direct sale. To achieve this, we had a very intense dialogue with CFE, since the company filed for legal protection against distributed generation conditions. Ultimately, we managed to convince CFE that this would be beneficial.

Q: What do you consider to be the main changes in energy policy as Mexico shifted from the Peña Nieto administration

to the AMLO administration and how do you expect these to affect the development of the energy sector?

A: I think the main change, which will be good, is that state-owned companies will be given more strength. It is important to note that the Mexican industry has space for very large and important state-owned companies and also for the private sector; there is no doubt that a strong effort from both sectors is required. The coming focus on strengthening and fixing the finances of the state-owned companies will help to complement the joint effort we have to make as a country.

Q: What opportunities does CRE see for its activities as a result of this policy change?

A: What we see as a great opportunity, but also a challenge, is being able to leverage the energy sector benefits on the social base that the new government enjoys. We believe this will help us to unlock many projects that unfortunately have been halted because of inadequate community engagement. I think the president’s high esteem in many of these communities can help to unlock many problems and construct new projects such as pipelines, energy generation terminals or access wells, which in turn will result in better energy conditions for the country.

If we can capitalize on this prospect for dialogue with society, it will be a great opportunity and at the same time a challenge going forward. For instance, we could have a great deal of gas available for the Yucatan Peninsula, unlock the pipeline from Tuxpan to Tula, provide gas to the region of Sonora with the connection of the pipeline from the south of Sonora to Sinaloa, or install a renewable plant in Yucatan. I think that the possibility for communication with communities that this new administration has is very different from what we saw in previous administrations.

Q: What will be the 2019 priorities for CRE in order to ensure a competitive market while adjusting to the new policy regime?

A: 2018 was an interesting year in terms of electricity tariffs. The tariff we had before 2018 was a closed fee that obeyed to an income objective and that did not recover

CFE’s costs, so every year CFE saw its assets reduced. The change in the LIE, took this responsibility from CFE and sent it to us. The law states that we need to recognize the costs of providing light and energy to different points across the country. We had to analyze their efficiency and then translate these costs to the tariff being paid by users in different regions. In the regions where energy generation is expensive because diesel is used, there was a higher rebounding of tariffs than in other areas that did not have this characteristic. It was important to send this signal because this is what invites investment to locate in certain regions where energy can be offered at a lower cost.

Obviously, the possibility of having these tariffs that recognize the generation cost means that people now think about their electricity bill. When the electricity bill is subsidized, people do not worry about looking for other options, installing solar panels, hiring a supplier, entering a bilateral contract or any other possibility. We are now seeing more businesses worry about having an electricity strategy for their companies. When you realize that 60 percent of manufacturing costs comes from electricity, it makes a lot of sense to put someone in charge of the energy strategy for the company. This gains greater relevance with these alternatives, which is an opportunity that arises from being able to take control of your own energy. The strengthening of CFE is a result of having an adequate cost recovery and investment complementarity in the use of technology from private players.

Also, in 2019, we will see the entrance of a significant number of renewable energy plants. CENACE estimates that by the summer of 2019, there will be 84 new electric centrals that will add 12,429MW to the National Interconnected System; this will allow less dependence on expensive fuels. What is important for the new administration is to continue with the exercises we have been doing, such as long-term and medium-term auctions, and to continue with gas production in the country, so we can have low-cost natural gas. I understand that the new administration wants to make a revision of all the programs, but it would be a really good element going forward to continue with these actions.

Q: What will be CRE’s priorities for the electricity sector in 2019?

A: In the electricity sector, we want to finish the regulation intended for distributed generation. We are missing some pieces, the most important being collective distributed generation. This means that a group of people can set up a renewable electricity installation and share among them all the benefits. This model has already been implemented elsewhere in the world and it is something

that the industry has requested, so we are working on its regulation.

The second priority will be to promote the use of EV charging stations. At the end of 2018, we published the regulation that permits the installation of EV charging stations and to charge for the use of electricity. In previous years, EV charging stations in malls were cost-free and although this might sound like a good thing, for investors it was not an incentive to set up these types of installations.

Today, there are around 2,000 EV charging stations in the country and almost all have been installed by automotive OEMs. The idea of this regulation is to tell them that they can resell electricity and by establishing a regulatory framework that provides certainty to investors, they can now set up EV charging stations throughout the country. This will prove to be important for the country’s energy security. Inasmuch as a country diversifies its use of energy for transportation, we will not depend that much on gasoline and diesel and we will be able to have electric cars as part of the public transportation system.

The third topic that is important to mention for 2019 is related to storage capacities. In this sense we are working on several regulatory pieces and we are in the process of identifying the services that provide storage. We have identified over 18 storage services, such as frequency regulation, transmission in peak periods, generation in peak periods, storage in hours of negative costs and sale in hours of high costs. The first private storage terminals have been installed in Baja California Sur, complementing a solar power plant. Given this experience, I think we will see more energy storage in our country.

Q: What would be CRE’s message for the rest of the industry?

A: The most important thing we need to do is prove why it is necessary to have autonomous regulators. We provide certainty and decisions backed by technical facts. Often, we are seen as a group of bureaucrats that only cost money but the added value is not immediately tangible. We provide an intangible value that banks and investors require and that provides certainty. So, I would extend an invite to the general public to familiarize themselves with the work of the regulators, not only CRE but also CNH, ASEA, COFECE, and IFT. We are all on the same channel and we all provide the value of certainty.

Guillermo García has served as President Commissioner of CRE since April 2016. García took part in the technical and drafting group for the 2013-2014 Energy Reform and conducted support studies for the 2008 Energy Reform

MEXICO’S GRID STABILIZER

EDUARDO MERAZ

Former Director General at CENACE

Q: What type of technologies play a dominant role for CENACE in modernizing the National Electricity System (SEN)?

A: Renewable generation technologies with the capacity to regulate voltage and generation through the application of smart grids contribute in the security of the network. In addition, these technologies support the reduction of congestion and restrictions that could affect efficiency within operations. The transmission of energy based on direct current, energy storage systems and the massive and open use of information for better decision making are all factors that play an important role in the modernization of the SEN.

Q: What challenges does the integration of more clean energy sources to the grid pose to the SEN?

A: It is important to specify that an energy matrix with a greater share of clean energies will make a great contribute to the reduction of polluting emissions compared to other fuels. In addition, it would be ideal if part of this clean energy can come from intermittent sources such as solar and wind energy, which will depend on having enough wind and solar irradiation for adequate production levels. Energy production would very much obey to the weather conditions. However, the fact that these production levels experience constant fluctuations cannot be disregarded. This for the SEN implies that it

must operate compensating the intermittency of this generation to maintain the generation-demand balance.

Q: What have been the measures taken to ensure this intermittency does not act as an obstacle for delivering a continuous electricity supply?

A: CENACE evaluates operating conditions in terms of the participation of these intermittent energy sources and determines the amount of generation that is possible to produce at that moment. It also considers the conditions of the rest of the system in order that these renewable sources do not put at risk the secure and continuous operation of the electricity system. We analyze how to acquire more flexibility and capacity from other energy sources to substitute the variation of intermittent injections. CENACE establishes the availability of flexible sources that can increase and decrease generation rapidly. We contemplate remunerations for the generators that offer these capabilities. For instance, these would include hydro power plants, modern units that have these characteristics and energy storage systems comply with these requirements.

Q: What does CENACE propose to motivate the installation of small-scale clean generation units?

A: Although industry participants have protested that high costs in the interconnection studies for small scale clean generation plants place its development at a disadvantage,

REGULATORY

in the Interconnection and Connection Manual published in 2018, there are significant reductions in these costs for smaller projects. These costs reflect an approved value by CRE, which bases its determination on the resources that are needed to execute this process. It is important to highlight that these studies will always be necessary so that it is possible to gauge the impact that the interconnection of a new generating plant or load on the development of the SEN.

Q: How is CENACE preparing itself for the introduction of distributed generation systems into the grid?

A: Distributed generation has to be introduced based with a more preventive regulation as its foundations so it does not cause future problems in the electricity system. It is important that its entrance complies with the standards and norms that have been applied in other countries where this generation scheme has increased in importance. The grid code outlines the current requisites that are needed for this transition, but future updates have to be contemplated.

Q: What are the main challenges that CENACE has to address in the coming years?

A: Our primary targets are threefold. Firstly, we aim to successfully continue operating the electricity system while promoting the incorporation of much more renewable energy generation. Secondly, we want to ensure a more competitive and sufficient energy market, and we want this efficiency to in turn be reflected in more competitive costs for all kinds of consumers. And finally, we aim to provide adequate information to facilitate smart decision-making for every player involved. Investors, market participants and the energy industry authorities will need this information to determine and evaluate the development of the market mechanisms.

Q: What key elements will represent a step-forward for the WEM looking toward 2019-20?

A: There are several variables that can be measured to gauge the success of the WEM in the coming years. One of the most important indicators will be the rate of new participants entering the market and taking part in electricity-related activities. Another factor is the entrance of new and more competitive generation infrastructure, which will boost the national industry. Finally, the development of infrastructure for the electricity network that will allow us to send the most economic energy to all regions of the country.

Wind and solar sources injected 4,413MW to the grid in 2017 while distributed generation added 434MW

Q: What is CENACE’s contribution to the maturation process of the WEM?

A: CENACE greatly promotes the widespread diffusion of the market mechanisms, which grant many more options to those who buy and sell energy. Knowledge of the options available to them is always beneficial for the consumer. In addition, the responsibility this entity has a responsibility to serve the network with honesty and transparency through an attitude of service that takes into account every market participant. Finally, supply reliability will be obtained by having a market with sufficient competitive offer of supply and demand that can respond to the system management based on prices and demand control incentives.

CENACE is a decentralized public entity that was founded in 2014 to act as Mexico’s independent grid operator. It sprouted from CFE’s former intelligence unit and now acts as manager of Mexico’s National Electricity System.

PREPARING CAMPECHE FOR GREATER SUCCESS

JOSÉ MARÍA CU CAÑETAS

Director General

of the Energy Agency of the State of Campeche

Q: What is the story behind the creation of Campeche’s Energy Agency and what are its attributions and long-term objectives?

A: The agency was created by executive agreement published on July 28, 2017. Our mission is to manage and promote the development of energy projects in a safe, reliable, profitable and sustainable manner and to generate employment and welfare opportunities for the people of the State of Campeche. Our priority is to detonate and take advantage of the opportunities brought by the Energy Reform. In this regard, Campeche has prepared to become the most important oil and gas hub in Mexico. We were the first state to evaluate its energy balance, considering the strength of the state in terms of energy. It is important to note that we have hydrocarbon reserves and large areas suitable for renewable energy generation, positioning our entity as a producer and natural generator of energy. Campeche has conducted an unprecedented in-depth study in which it identified a broad portfolio of projects in the field of energy. The agency also has a business model designed to foster national and international alliances between the public, social and private sectors, for the development of strategic energy projects.

Q: What clean energy technologies is Campeche best suited to develop?

A: After analyzing the results of our energy balance evaluation, we concluded that Campeche has a series of business opportunities in the field of energy. Although the first place is occupied by the hydrocarbons sector, it should be noted that, in turn, Campeche has optimal areas for the development of clean energy projects, including a wind farm, a solar park and two biodigesters. The geographical location of the state and its potential in natural resources allow us to continue evaluating other probable sources of renewable energy such as hydroelectric turbines since we

The Energy Agency of the State of Campeche was created in June 2017 to focus on the state’s strategy for energy development, coupled with the promotion, research and development of energy projects

have four hydrological regions, seven basins and 2,200km2 of coastal lagoons.

Q: How is the agency aligning to the new administration’s agenda?

A: We know that the new administration plans to increase Mexico’s oil and gas production through PEMEX’s top-tier assets and this policy will give national and local service companies the opportunity to participate in the NOC’s plans. With respect to local content, Campeche has more than 30 years of experience providing offshore services to the oil fields of PEMEX. The government of the State of Campeche is working on programs to promote, develop and train local companies to receive and offer new services to new operators. The government of the State of Campeche is working on the modernization of state ports, considering Ciudad del Carmen’s role as the base of operations and logistics of PEMEX for more than 30 years.

In terms of renewable energy, Campeche is prepared to incorporate the development of wind farms, solar parks and even offshore wind farms with state-of-the-art technology and skilled labor. We are also assessing the opportunity to develop onshore and maritime pipelines along with storage facilities to become a focal point for hydrocarbons and fuels logistics.

Q: What are the key ingredients to attract investment in clean energy projects for the state?

A: The state has a potential for proven reserves of hydrocarbons and large areas of renewable energy generation. Having the natural resource for the generation of clean energies is the main asset and ingredient for the development of these projects. Aside from the energy wealth of the state, Campeche is in a strategic location as the gateway to the south-east of the country and the bridge between the center and the peninsular region. That is why the new energy development strategy of the state identifies specific cases of business initiatives that consolidate a portfolio of investments in the order of about US$1.25 billion, consisting of 16 specific projects that will allow the comprehensive development of our state.

OAXACA LEADING RENEWABLE POWER GENERATION CHARGE

JOSÉ LUIS CALVO

Minister of Environment, Energy and Sustainable Development of the State of Oaxaca (SEMAEDESO)

Q: How does SEMAEDESO contribute to the development of Oaxaca’s energy industry?

A: Oaxaca is the country's most biologically diverse state and SEMAEDESO manages its environmental affairs. Regarding the energy sector, Oaxaca is Mexico’s leader in renewable power generation, with the highest installed capacity from wind energy power in the country. It hosts 28 wind farms that supply more than 62 percent of the wind energy in Mexico. This represents 1,583 turbines with a total of 2,750MW. In 2018 alone, we increased this capacity by 17 percent.

An example of this successful management is the culmination of the Eólica del Sur wind farm. This project was developed by FONADIN, Mitsubishi Corporation and Balam Fund. It has an installed capacity of 396MW and is composed of two substations and 132 wind turbines. This project represents the mitigation of 566,967t/y of CO2 equivalent, which is the same as removing 300,000 vehicles from the roads. Additionally, it represents social benefits for the region. For instance, more than 6,142 lightning systems were installed and the electricity tariff experienced a reduction of 30 percent.

Oaxaca hosts the largest wind farm in Latin America. This is a product of generating legal certainty for investment. We want to demonstrate our commitment to the development of the state, which is why the Oaxaca Energy Council was created. This initiative groups the three levels of government, companies and owners to discuss proposed projects and the associated social benefits for each community involved.

In the solar arena, the state also offers significant levels of solar irradiation and related projects are becoming tangible. An example of this is the construction of a solar plant at the Universidad Tecnológica de la Mixteca. This project will support the education of 2,200 students and academics. The hydroelectric segment will become a reality too, mostly in Oaxaca’s coastal region.

During Cué Monteagudo’s administration there was no investment in renewable technologies from the government.

But since 2016, when the new administration entered, the state has attracted investment of more than US$2 billion.

Q: Which projects best illustrate SEMAEDESO’s interest in and efforts to develop Oaxaca’s renewable energy industry?

A: EDF Renewables is developing a project with a total investment of US$600 million that will supply 300MW and mitigate 360,797t/y of CO2 equivalent. This project will be located in the municipality of Union Hidalgo. Additionally, Siemens GAMESA will invest US$400 million in the construction of another wind farm. For this project, six assemblies were held to achieve community consent for the construction works.

The Ixtepec-Yautepec transmission line that will interconnect the states of Oaxaca and Morelos is a priority as well. Along with the governor, SEMAEDESO is intensively lobbying for its development. This project will open the door for more investment and will incentivize the development of not only more wind energy projects but also the introduction of new industries, such as automotive manufacturing plants or even wind infrastructure components facilities.

Regarding the solar segment, the state is developing a project in collaboration with the Energy Ministry to introduce thermo solar technology to hotels located in the city of Oaxaca. One of Oaxaca’s main economic activities is tourism and if we install solar heaters in the city's 6,000 hotel rooms, we will boost the city’s economic development while decreasing CO 2 emissions. These projects could not be developed without skilled local human capital. Now, international companies bring their own personnel with them. Oaxaca’s Universities System (SUNEO) has 10 universities and 18 campuses across the state. We want to promote training of technical professionals in the renewable energy arena by investing in this system as well.

SEMAEDESO is Oaxaca’s Ministry of Environment, Energy and Sustainable Development. Created on Dec. 1, 2016, it oversees the protection, conservation and sustainable use of the state’s natural resources, preserving its ecological balance

SCORING THE REFORM: TRIPLE-B WITH ROOM FOR IMPROVEMENT

CHRISTOPH FREI

Secretary General and CEO of the World Energy Council

Q: What tools has the World Energy Council developed to understand the present and future world energy scenarios?

A: At the World Energy Council, we have developed several tools to understand the global energy landscape. One is the World Energy Trilemma Index, a report that evaluates 125 countries on a yearly basis in the three most relevant aspects related to energy: energy security, energy equity and energy environment. The ranking measures the performance of a country’s policies in achieving a sustainable energy mix and the balance score highlights how well the country manages the trade-offs. AAA is the best balance score and DDD is the worst. Another significant tool developed by the World Energy Council is a policy-based approach on future world energy scenarios that can be classified into three genres: modern jazz, unfinished symphony and hard rock. Modern jazz depicts a market-driven approach to achieve energy accessibility and affordability through economic growth. Unfinished symphony is based on a government-driven approach to achieve sustainability through internationally coordinated policies and best practices. Lastly, hard rock implies a fragmented approach driven by a desire for energy security and independence in a world with low global cooperation. For all these scenarios, policy is a key driving element.

Q: How would you score the latest transformations of Mexico’s energy environment according to these tools?

A: Modern jazz is a liberalized, competitivity-enabling and technology-based approach. This means that the market framework favors trade agreements that allow for investment as well as greater imports and exports that result in better technologies. Symphony, on the other hand, achieves progress on climate change by selecting specific technologies and promoting them even if they are not the cheapest. Modern jazz has mastered trade agreements while symphony has mastered carbon agreements. Lastly, hard rock is very focused on national content for the

The World Energy Council is the main network of energy leaders and practitioners worldwide. The organization has a coordinated Secretariat based in London and under the direction of the Secretary General, who reports to the Council’s board

development of energy technologies and therefore misses important opportunities. From the World Energy Council’s perspective, the Energy Reform has jazzy elements that introduce technology competition while, at the same time, it has symphonic elements promoting energy efficiency, renewable energy and carbon-mitigation technologies. This means that the Energy Reform lays in a symphonic-jazz area. Looking at the trilemma, Mexico earns a BBB score, which is very balanced. The first thing we strive for at the World Energy Council is balance, as its absence generates policy risk. This drives investors away and without them we cannot manage any transition. The balance reflected in Mexico’s BBB score is good overall but there is certainly room for improvement and the Energy Reform aims to keep improving, which should increase the country’s score.

Q: What role do innovations like digitalization, storage, IoT and blockchain play in Mexico’s energy transition?

A: Digitalization offers many opportunities and its capacity to create a future uberization in the energy industry is one of the most exciting. Providing hotel-like services without having a hotel or driving people from one place to another without owning a taxi is what Airbnb and Uber have achieved. Uberization therefore means the capacity of taking a capitalintensive sector and coming up with business models that bring additional value to existent assets via digital processes. What this means for the energy industry is that companies can become energy storage providers without owning an energy storage facility, for example.

In Mexico, a clear example of what digitalization can do is depicted in a shift of the baseline of energy consumption. There are 40 million households in Mexico. Considering that every household has a fridge that consumes 100W then there are 4GW of power being consumed just from fridges. On an average day, Mexico has an energy demand peak of 45GW, which means that fridges represent 8 percent of the peak load. If you could digitally enable all the fridges to be turned off during peak demand and then turn them on after the peak ends, 8 percent of the total peak load from the system could be shifted, therefore relieving the energy network.

MUCH STILL TO BE DONE TOWARD ENERGY EFFICIENCY

ODÓN DE BUEN

Former Director General of CONUEE

Q: What were CONUEE’s priorities during your administration?

A: CONUEE’s program with the greatest scope and impact is the one related to energy efficiency standards (NOM) and we worked to increase its reach and to strengthen the compliance system.

We have supported the development of energy-efficient lighting projects in more than 40 municipalities and we have contributed to the implementation of best practices following our NOM, giving more formality to a market where there is much improvisation. In terms of final use of energy, we have generated discussion among several players in the transportation, construction and industrial sectors in best practices and technology to improve energy performance. We also completed our National Energy Efficiency Monitoring Report in collaboration with the Economic Commission for Latin America and the Caribbean and the French Development Agency. This report helps the general public and policymakers understand the evolution and present levels of efficiency by sector in great detail. This is now the most complete report in all of Latin America addressing this topic.

Q: How have regulations advanced to promote energy efficiency in buildings?

A: There has not been much progress. As electricity in the housing sector is heavily subsidized, the greatest benefits of NOM-020 go to the Ministry of Finance. We have a proposal to economically support compliance with certain standards but this is a conversation that must be established with the new federal government. We also face challenging conditions due to the lack of interest from mayors and municipal leaders since energy-efficiency projects do not usually yield largely visible results. We have approached administrations in Mexico City, Villahermosa, Merida, Mexicali and Hermosillo, among others, but we have not succeeded in making energy efficiency a key element in local construction rulebooks.

Q: What were the main conclusions reached through the National Energy Efficiency Monitoring Report?

A: We found that electric energy intensity in the industrial sector has decreased by 15 percent over the past 20 years. This is mostly a result of high energy and gas tariffs rather than government policies. In the residential sector, on the other hand, public policies have had a significant impact with an estimated 45 percent reduction in electric energy intensity and a decrease of 20 percent in energy use per capita. The analysis covers the entire value chain of the energy sector, highlighting opportunities in supply as well. PEMEX’s drop in efficiency has also impacted national indicators, which shows a need to improve processes for fossil fuels.

Q: What pending priorities should the new administration focus on?

A: We are still missing an energy efficiency standard for heavy vehicles. We already have one for light vehicles but CONUEE must still work together with SEMARNAT to draft its heavy-vehicle counterpart. There is also a gap in the implementation of norms NOM-008 for nonresidential buildings and NOM-020 for residential buildings in the construction sector, which should be a requirement in the permit process at a municipal level.

The SME sector also represents an area of opportunity. Promotion and financing among these players are not simple and our strategies should be rethought to make them more effective. There is also a change needed in the mindset of public officers at a municipal level, so they are more knowledgeable regarding energy projects and the best way to implement these.

Going forward, support for CONUEE should continue and there should be ongoing innovation in support toward SMEs and municipal projects. There should also be stronger collaboration with the environmental sector to ensure healthy progress toward national goals.

The National Commission for the Efficient Use of Energy (CONUEE) is a public entity that promotes efficiency and the sustainable use of energy resources through the adoption of best practices

WHERE INDUSTRY MEETS ACADEMIA

ANGÉLICA QUIÑONES President of ANES

Q: What is the main contribution that ANES offers to the solar energy market in Mexico?

A: The National Association of Solar Energy (ANES) has participated for more than 40 years in the Mexican energy arena. It brings together the interests of more than 800 members from academia and industry. I believe having this academic and institutional support is one of our biggest strengths. Some of our strategic allies are the Renewable Energy Institute (IER-UNAM), the Mexican Center of Solar Innovation (CeMIE-Sol) and the German-Mexican Energy Partnership. ANES’ work is focused on the democratization of energy. This means that not only big consumers benefit from its generation but small users in remote areas as well. Another important value that ANES brings to the table is the technical certainty and normalization of the industry’s guidelines. For instance, I represent the Solar Committee of the Mexican Society of Normalization and Certification (NORMEX). ANES has worked for several years on regulatory topics. We acknowledge that the market would not evolve without having strong ground rules.

Q: What will be the priority topic on ANES’ agenda during the new administration’s term?

A: Solar heat for industrial processes is a very important topic for the association. This was addressed by the previous administration and resulted in the creation of two programs. The first is the Solar Heat Initiative, an interinstitutional platform in collaboration with CONUEE and GIZ. The program aims to unite parties interested in generating solar heat temperatures between 150-400°C for its application in various sectors.

The second program is Solar Payback, an initiative developed with CAMEXA where its main focus relies on solar heat generation for industrial processes. With both programs, we conducted market research and now we have strong facts

and data that justify heat demand in the country. In Mexico, 70 percent of the energy used in industrial processes comes from heat and the remainder comes from electricity. The study also determined the niche industry segments where this technology could be applied. During this administration, one of ANES’ main goals is to improve our communication strategy to empower the final user. Successful case studies are what is missing for the industry to take over thermosolar technology. At the same time, this generates major consciousness. With supporting data, we can motivate the construction of a better policy strategy for the industry.

Q: What is missing from a regulatory standpoint to motivate the solar industry’s growth?