2022 Johnson City Housing Needs Assessment (Bowen Report)

PRELIMINARY HOUSING NEEDS ASSESSMENT

Johnson City, Tennessee

Table of Contents

I. Introduction

II. Executive Summary

III. Community Overview and Study Area

IV. Demographic Analysis

V. Economic Analysis

VI. Housing Supply Analysis

VII. Housing Gap Estimates

VIII. Community Input Results and Analysis

Addendum A – Phone Survey of Conventional Rentals

Addendum B – Community Input Results

Addendum C – Qualifications

Addendum D – Glossary

I. INTRODUCTION

A. PURPOSE

The government of Johnson City, Tennessee retained Bowen National Research in December 2022 for the purpose of conducting a Preliminary Housing Needs Assessment of Johnson City, Tennessee.

With changing demographic and employment characteristics and trends expected overtheyearsahead,itis importantforJohnsonCityanditscitizenstounderstand the current market conditions and projected changes that will influence future housing needs. Toward that end, this report intends to:

• Provide an overview of present-day Johnson City.

• Present and evaluate past, current, and projected detailed demographic characteristics

• Present and evaluate employment characteristics and trends, as well as the economic drivers impacting the area.

• Determine current characteristics of all major housing components within the market (rental housing alternatives and for-sale/ownership).

• Provide housing gap estimates by tenure and income segment.

• Collect input from residents/employees/commuters in the form of an online survey.

By accomplishing the preliminary study’s objectives, government officials, area stakeholders, and area employers can: (1) better understand the city's evolving housing market, (2) establish housing priorities, (3) modify or expand local government housing policies, and (4) enhance and/or expand the city’s housing market to meet current and future housing needs.

B. METHODOLOGIES

The following methods were used by Bowen National Research:

Study Area Delineation

The primary geographic scope of this study, referred to as the Primary Study Area (PSA), focused on the city limits of Johnson City, Tennessee. State and national data was used, when available, as a base of comparison for selected data sets. Maps of the study areas are provided in Section III of this report.

Demographic Information

Demographic data for population, households, and housing was secured from ESRI, the 2010 and 2020 U.S. Census, the U.S. Department of Commerce, and the American Community Survey. This data has been used in its primary form and by Bowen National Research for secondary calculations. Estimates and projections of key demographic data for 2022 and 2027 were also provided.

Employment Information

Employment information was obtained and evaluated for various geographic areas that were part of this overall study. This information included data related to wages by occupation, employment by job sector, total employment, unemployment rates, identification of top employers, and identification of largescale job expansions or contractions. Most information was obtained through the U.S. Department of Labor, Bureau of Labor Statistics. Bowen National Research also attempted to conduct interviews with local stakeholders familiar with the area’s employment characteristics and trends.

Housing Component Definitions

This study focuses on rental and for-sale housing components Rentals include multifamily apartments (generally five+ units per building) and non-conventional rentals such as single-family homes, duplexes, units over storefronts, etc. Forsale housing includes individual homes, mobile homes, and projects within subdivisions. The focus of the rental housing survey for this analysis was concentrated on conventional rental product.

Housing Supply Documentation

During December 2022 and January 2023, Bowen National Research conducted telephone research, as well as online research, of the area’s housing supply. The following data was collected on each multifamily rental property:

1. Property Information: Name, address, total units, and number of floors

2. Owner/Developer and/or Property Manager: Name and telephone number

3. Population Served (i.e., seniors vs. family, low-income vs. market-rate, etc.)

4. Available Amenities/Features: Both in-unit and within the overall project

5. Years Built and Renovated (if applicable)

6. Vacancy Rates

7. Distribution of Units by Bedroom Type

8. Square Feet and Number of Bathrooms by Bedroom Type

9. Gross Rents or Price Points by Bedroom Type

10. Property Type

For-Salehousingdataincludeddetailsonhomeprice,yearbuilt,location,number ofbedrooms/bathrooms,priceper-square-foot, andotherpropertyattributes. Data was analyzed for both historical transactions and currently available residential units, as available.

Housing Demand

Based on the current demographic data for 2022 and projected data for 2027 and taking into consideration the housing data from our phone survey of area housing alternatives, we are able to project the potential number of new units the PSA (Johnson City) can support. The following summarizes the metrics used in our demand estimates.

• Rental Housing – We included renter household growth, the number of units required for a balanced market, the need for replacement housing, commuter/external market support, and step-down support as the demand components in our estimates for new rental housing units. As part of this analysis, we accounted for vacancies reported among all surveyed rental alternatives. We concluded this analysis by providing the number of rental units that the market can support by different income segments and rent levels.

For-Sale Housing – We included owner household growth, the number of units required for a balanced market, the need for replacement housing, commuter/external market support, and step-down support as the demand components in our estimates for new for-sale housing units. As part of this analysis, we accounted for vacancies reported among all surveyed for-sale alternatives. We concluded this analysis by providing the number of units that the market can support by different income segments and price points

C. REPORT LIMITATIONS

The intent of this report is to collect and analyze significant levels of data for Johnson City Bowen National Research relied on a variety of data sources to generate this report. These data sources are not always verifiable; however, Bowen National Research makes a concerted effort to assure accuracy. While this is not always possible, we believe that our efforts provide an acceptable standard margin of error. Bowen National Research is not responsible for errors or omissions in the data provided by other sources.

We have no present or prospective interest in any of the properties included in this report, and we have no personal interest or bias with respect to the parties involved. Our compensation is not contingent on an action or event resulting from the analyses, opinions, or use of this study. Any reproduction or duplication of this study without the expressed approval of Johnson City or Bowen National Research is strictly prohibited.

II. EXECUTIVE SUMMARY

The purpose of this preliminary report is to evaluate the housing needs of Johnson City, Tennessee. To that end, we conducted a Housing Needs Assessment that considers the following:

• Demographic Characteristics and Trends

• Economic Conditions and Commuting/Migration Patterns

• Existing Housing Stock (Rental and For-Sale) Costs and Availability

• Quantified Housing Gap Estimates

Based on these metrics, we were able to identify housing needs by affordability and tenure (rental vs. ownership). This Executive Summary provides key findings of our analysis.

Geographic Study Area

This report focuses on the Primary Study Area (PSA), which consists of Johnson City. Additional information, when available, is provided for Tennessee and the United States for comparison purposes. A map illustrating the study area is provided below An enlarged map is included on page III-4 of this report.

Key Findings

This study included the analysis of numerous topics and data sets. The following summarizes some of the key findings from this study.

Demographic Characteristics and Trends

Johnson City is expected to continue to expand demographically and maintain a relatively even distribution of renter and owner households. Renter household incomes will continue to be primarily concentrated under $50,000 while owner households will primarily earn $50,000 or more through 2027. Household growth projected for several different age segments but will be primarily concentrated among seniors aged 65 and older. Overall, Johnson City has grown andwillcontinuetoexpandfortheforeseeablefutureintermsofbothtotalpopulation and households. Between 2022 and 2027, the Johnson City population is projected to increase by 1,166 (1.6%) while households will increase by 570 (1.9%). Although projected growth rates for the area between 2022 and 2027 will occur at a slightly slower pace than the state of Tennessee, this growth is expected to result in increased demand for housing. Other notable findings of our demographic analysis are as follows:

• More than 20.0% of the Johnson City population is estimated to be living below the poverty line, as compared to approximately 15.0% of the state population.

• Household growth within Johnson City is projected to occur among various age groups, though thelargest growth will occuramonghouseholds aged 75and older and those aged 35 to 44.

• Johnson City households are relatively evenly distributed by tenure (owner vs. renter) as approximately 52.5% of households were renters in 2022 while the remaining 47.5% were renters. Growth is projected to occur among each of these household segments between 2022 and 2027.

• Although the Johnson City median household income is projected to increase by morethan26.0%between2022and2027to $62,681,itisalsoprojectedto remain more than 15.0% lower than the statewide median household income ($74,116) through 2027.

• Household growth among renters is projected to be concentrated among households earning $50,000 or more between 2022 and 2027. However, nearly 60.0% of all renter households are projected to earn less than $50,000 in 2027.

• Similar to renter growth, household growth among owner households is projected to be concentrated among those earning $50,000 or more. Conversely, however, more than three-quarters (76.5%) of owner households are projected to earn $50,000 or more through 2027.

• Johnson City population/household base has potential to increase more rapidly than current demographic projections given the large number of workers that commute to the area from outside of Johnson City. Notably, more than 35,000 workers commute into Johnson City from other surrounding areas. In the event housing which meets the needs of these commuters is built/comes available within Johnson City, it is likely some of these commuters would consider relocating to Johnson City to be near their place of employment.

Housing Supply Analysis

Lack of available housing, particularly affordable housing, limits growth within Johnson City as households looking to relocate within or to the area have very few options from which to choose. Limited affordable housing availability also contributes to many Johnson City households, particularly renters, being cost burdened (paying more than 30% of their income towards rent). As part of this analysis, we analyzed American Community Survey (ACS) data as it relates to the Johnson City housing stock. Additionally, we conducted a telephone survey of existing area rental properties and obtained data pertaining to recent home sales (July 2022 to January 2023) and homes available for purchase at the time of our analysis. The results of these analyses revealed that the existing Johnson City housing supply is generally more affordable, though older, than housing throughout the state of Tennessee. Additionally, housing availability within Johnson City is very low as the 49 rental properties surveyed report an overall vacancy rate of just 0.7% and a total of just 51 homes were identified as being available for purchase at the time of this report resulting in an availability rate of 0.3%. Summaries of our survey of area rentals and homes identified as available for purchase are illustrated by the following tables.

Source: Realtor.com & Bowen National Research

Johnson City Available For-Sale Housing by Price

Notable findings of our housing supply analysis are summarized as follows:

• Existing apartment rental product surveyedis relatively evenly distributedamong affordable (Tax Credit and government-subsidized) product generally serving households earning $53,920 or less, and market-rate rentals serving moderate to higher income households. These segments represent 46.0% and 54.0% of the rental units surveyed, respectively. While vacancy rates are low for each of these segments, it is notable that the vacancy rate reported (0.5%) for affordable rental propertiessurveyedisslightlylowerthantheoverallvacancyrate(0.7%)reported for all properties surveyed. This is reflective of just seven (7) vacant units among the 25 affordable properties surveyed. In comparison, a rental vacancy rate generally between 3.0% and 5.0% is considered healthy and allows for a wellbalanced market.

• Waiting lists containing approximately 114 and 484 households combined for the non-subsidized Tax Credit and government-subsidized properties, respectively, are maintained among the affordable rental properties surveyed.

• More than 45.0% of Johnson City renter households are considered to be rent burdened in that they pay more than 30% of their income towards rent, slightly higher than the 42.4% share reported for the state of Tennessee. Further, more than one-fifth (20.9%) of all renter households are considered to be severe cost burdened (paying 50% or more of income towards rent).

• The median rents of the Tax Credit supply are positioned well below (16.5% to 39.0% depending upon unit type) the median rents reported for similar unrestricted market-rate units surveyed in the area. The value of these units has likely contributed to the strong 100.0% occupancy (0.0% vacancy) rate reported for this rental segment.

• A total of just 51 homes were identified as available for purchase at the time of our analysis while 219 homes were known to be sold within Johnson City between July of 2022 and January of 2023. The 51 homes available for purchase are reflective of an availability rate of 0.3%, much lower than the normal range of 2.0% to 3.0% for a well-balanced for-sale/owner-occupied market. The 219 homes sold during the aforementioned time period yield an average sales rate of approximately36 sales permonthduringthis time period.Basedonthis historical sales data, the 51 homes available for purchase represent an available home inventory of less than two months (51 homes / sales rate of 36 homes per month = 1.4 months).

• More than two-thirds (68.6%) of homes available for purchase within Johnson City are priced $300,000 or more. Comparatively, nearly 38.0% of Johnson City homes which sold during the six-month period evaluated (July 2022 to January 2023) were also priced $300,000 or more. Typically, a home of this price point would require an income of approximately $72,000 to be determined affordable (paying no more than 30% of income towards housing costs) to the purchaser. In comparison, only 16 available homes are considered affordable to households earning less than $72,000 within Johnson City.

• A total of 540 (16.3%) of the 3,307 rental units surveyed and eight (8), or 15.7%, ofthe51availablefor-salehousingunitsidentifiedwerebuiltsince2010. Further, just over 13.0% of Johnson City homes sold between July of 2022 and January of 2023 were built since 2010. Comparatively, approximately 35.0% of all rental housingunitssurveyedandbetween49.0%and63.9%ofrecentlysold andhomes available for-purchase were built prior to 1980.

Overall PSA (Johnson City) Housing Needs

Johnson City has an Overall Housing Gap of 4,859 Units for Rental and For-Sale Product at a Variety of Affordability Levels - It is projected that the city has a fiveyear rental housing gap of 2,260 units and a for-sale housing gap of 2,599 units. Both the rental and for-sale housing gap is distributed most heavily among moderate priced (rents of $1,349 to $2,259 and homes priced $179,734 to $301,200) product However, it is important to note that Housing Gap Estimates included in this report show a need for rental and for-sale housing product of all affordability levels within Johnson City. Details of this analysis, including our methodology and assumptions, are included in Section VII.

The following table summarizes the approximate potential number of new residential units that could be supported in the PSA (Johnson City) over the next five years.

The preceding estimates are based on current government policies and incentives, recent and projected demographic trends, current and anticipated economic trends, and available and planned residential units. Numerous factors impact a market’s ability to support new housing product. This is particularly true of individual housing projects or units. Certain design elements, pricing structures, target market segments (e.g., seniors, workforce, families, etc.), product quality and location all influence the actual number of units that can be supported. Demand estimates could exceed those shown in the preceding table if the community changes policies or offers incentives to encourage people to move into the market or for developers to develop new housing product.

III. COMMUNITY OVERVIEWAND STUDYAREA

A. JOHNSON CITY OVERVIEW

This report focuses on the housing needs of Johnson City, Tennessee. Recognizedasacityin1856,JohnsonCityislocatedinportionsofWashington, Carter, and Sullivan Counties in the upper northeast portion of Tennessee near the North Carolina border Johnson City is surrounded by portions of the Appalachian, Blue Ridge, and Great Smoky Mountain ranges. The main thoroughfares that serve Johnson City include Interstate 26, U.S. Highway 19W, U.S. Highway 321, and State Routes 36 and 381. Notably, Interstate 26 connects the Johnson City area with nearby Kingsport, Tennessee to the north, as well as the Asheville, North Carolina area approximately 60.0 miles south of Johnson City.

Johnson City contains approximately 43.0 square miles and is home to 71,046 people based on the 2020 Census, an increase of 10.3% from the time of the 2010 Census. Population density within Johnson City is approximately 1,629 people per square mile in comparison to the Tennessee state average of approximately 164.0 people per square mile. The household base within Johnson City is relatively evenly distributed among renters and homeowners, which comprise 44.5% and 55.5% of households in the area, respectively. Households are also relatively evenly distributed by age. The majority of households (both renters and owners) are comprised of two or fewer persons and more than 42.0% of all households earn less than $40,000 annually.

The city’s largest employment sectors include Health Care & Social Assistance (37.3%), Retail Trade (14.8%), and Accommodation & Food Services (9.1%). Because of the variety of outdoor recreation opportunities available, the area is a popular locale for tourism. This tourism contributes significantly to the local economy and helps to support many of the area’s restaurants, retailers, and lodging businesses. Johnson City serves as a cultural center for the three counties in which it falls, with its Appalachian heritage and small-town charm. The city is known for its picturesque views of the Great Smoky and Blue Ridge Mountains. Notable attractions within the area include Farmhouse Gallery and Gardens, WingedDeerPark,RoanMountain, portionsoftheAppalachianTrail, Tipton-Haynes Historic Site, and several additional parks and museums.

Existingowner-occupiedhomesinthePSA(JohnsonCity)haveamedianhome value of $218,546, slightly lower than the state of Tennessee ($237,721), while the average gross rent for the PSA is $808, also lower than the state of Tennessee ($979). Approximately 45.0% of renters and 17.0% of owners in the PSA are considered cost burdened in that they pay more than 30% of their income towards housing costs. A variety of existing rental housing product is offered within the PSA, in terms of affordability levels, all of which are performing well with vacancy rates not exceeding 1.0% for any individual

rental housing segment surveyed. Similarly, for-sale product has limited availability within the PSA as only 51 homes were identified as being available for purchase at the time of this analysis. This is reflective of an availability rate of just 0.3%. The 51 available homes are representative of less than two months (1.4 months) of supply.

Additional information regarding the city’s demographic characteristics and trends, economic conditions, housing supply, and other factors that impact housing are included throughout this report.

B. STUDY AREA – MARKET AREA DELINEATION

Thisreportaddressesthe residentialhousingneeds ofJohnsonCity.Tothis end, we focused our evaluation on the demographic and economic characteristics, as well as the existing housing stock, of the Johnson City area. In order to provide an additional base of comparison, we provided data on the overall state of Tennessee and/or the United States, when applicable.

The following summarizes the study area used in this analysis.

Primary Study Area – The Primary Study Area (PSA) includes the entirety of the established limits of Johnson City, Tennessee. No secondary markets or submarkets were included in this analysis.

Maps delineating the boundaries of the study area are shown on the following pages.

IV. DEMOGRAPHICANALYSIS

A. INTRODUCTION

This section of the report evaluates key demographic characteristics for the Primary Study Area (PSA, Johnson City) and Tennessee (statewide). Through this analysis, unfolding trends and unique conditions are often revealed regarding populations and households residing in the selected geographic areas. Demographic comparisons between these geographies provide insights into the human composition of housing markets Critical questions, such as the following, can be answered with this information:

• Who lives in Johnson City and what are these people like?

• In what kinds of household groupings do Johnson City residents live?

• What share of people rent or own their Johnson City residence?

• Are the number of people and households living in Johnson City increasing or decreasing over time?

• How do Johnson City residents and those of the state compare with each other?

This section is comprised of three major parts: population characteristics, household characteristics, and demographic theme maps. Population characteristics describe the qualities of individual people, while household characteristics describe the qualities of people living together in one residence. Demographic theme maps graphically show varying levels (low to high concentrations) of a demographic characteristic across a geographic region.

It is important to note that 2010 and 2020 demographics are based on U.S. Census data (actual count), while 2022 and 2027 data are based on calculated estimates provided by ESRI, a nationally recognized demography firm These estimates and projections are adjusted using the most recent available data from the 2020 Census count, when available. The accuracy of these estimates depends on the realization of certain assumptions:

• Economic projections made by secondary sources materialize.

• Governmental policies with respect to residential development remain consistent.

• Availability of financing for residential development (i.e., mortgages, commercial loans, subsidies, Tax Credits, etc.) remains consistent.

• Sufficient housing and infrastructure are provided to support projected population and household growth.

Significant unforeseen changes or fluctuations among any of the preceding assumptions could have an impact on demographic estimates/projections.

It should be noted that some total numbers and percentages may not match the totals within or between tables in this section due to rounding.

B. POPULATION CHARACTERISTICS

Population bynumberandpercent change(growthordecline)forselectedyears is shown in the following table:

Source: 2010, 2020 Census; ESRI; Urban Decision Group; Bowen National Research

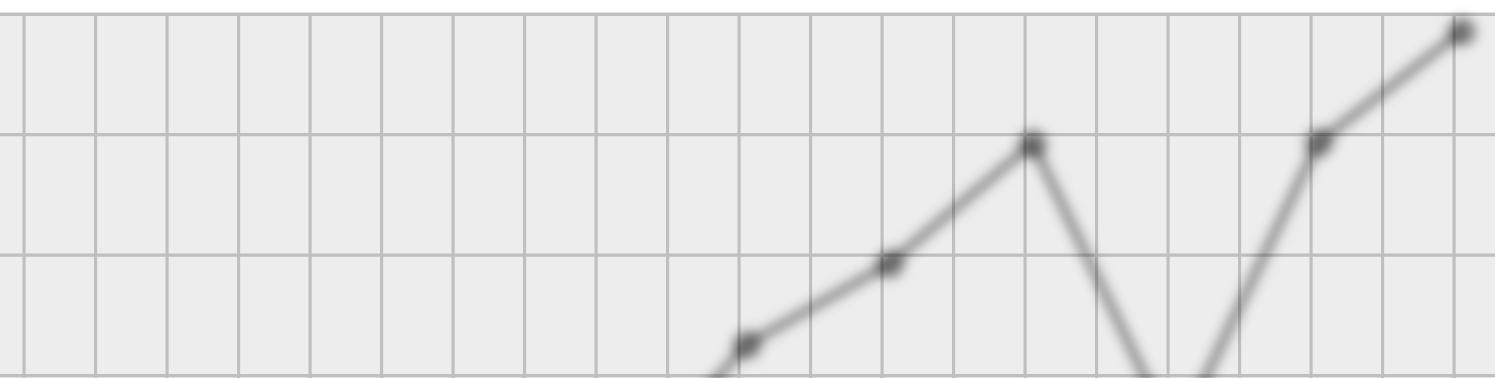

Between 2010 and 2020, the population within the PSA (Johnson City) increased by more than 10.0%, outpacing population growth experienced throughout the state of Tennessee (8.9%) during this same time period. In 2022, the total population of the PSA was estimated to be 72,127, which represented a 1.5% increase in population from 2020. This ongoing population growth is projected to continue through 2027 as the total population within the PSA is projected to increase by 1,166 (1.6%) between 2022 and 2027. The rate of population growth reported between 2020 and 2022, and that projected for between 2022 and 2027, within the PSA is lower than that reported for the state of Tennessee. Nonetheless, the Johnson City area is expected to continue to expand in terms of total population for the foreseeable future.

The following graph compares the percent change in population since 2010 and projected through 2027 for the PSA (Johnson City) and the state of Tennessee.

Population Trends (2010-2027)

Johnson City Tennessee

Population by age cohorts for selected years is shown in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research N/A – Not applicable

In 2022, the median age for the population of the PSA (Johnson City) was 39.0 years. This represents a 5.1% increase over the 2010 median age (37.1 years). In 2022, the median age for Johnson City was slightly lower than that reported for the state of Tennessee (40.0 years) The median age for the PSA is projected to increase to 40.1 years by 2027, remaining similar to the median age for the state of Tennessee.

In 2022, nearly one-third (31.2%) of the PSA population, the largest share of the PSA population, is within the age cohort of less than 25 years of age. This is not surprising considering this cohort encompasses a wide range of ages. Aside from this younger cohort, the distribution of population by age is relatively well balanced among the remaining cohorts. With the exception of the age cohort of 75 years and older (9.3%), all other cohorts have shares between 10.8% and 14.0% of the population. Population shares by age within the PSA are also relatively similar to those reported for the state of Tennessee, which is reflective of the similar median age reported for these two study areas.

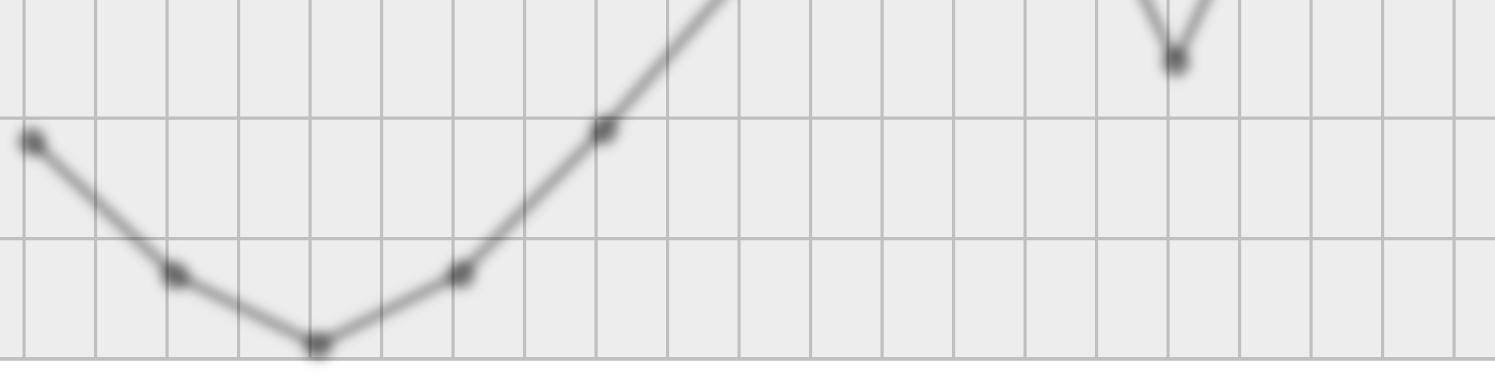

Projections for 2027 indicate that population growth within the PSA will occur among several different age cohorts, though the most notable growth is projected to occur among the age 75 and older and age 35 to 44 populations. Given the projected population growth among several age cohorts, population shares by age will remain relatively stable between 2022 and 2027, as will the median age projected for the area.

Thefollowing graphcompares theprojectedchangein population byagecohort between 2022 and 2027 for the PSA (Johnson City).

Johnson City Change in Population by Age (2022-2027)

Population by race for 2020 is shown in the following table:

Source: 2020 Census; ESRI; Urban Decision Group; Bowen National Research

In 2020, 80.7% of residents within the PSA (Johnson City) identified as “White Alone,” which is a notably higher share than the state overall (72.2%).

Approximately 6.7% of residents within the PSA identified as “Black or African American Alone”, whereas nearly 16.0% of residents in the state overall identified as this race. The remaining distributions of population by race in the PSA are relatively similar to those reported for the state overall.

Population by marital status for 2022 is shown in the following table:

Source: ESRI; Urban Decision Group; Bowen National Research

In 2022, nearly half (44.1%) of the population in the PSA (Johnson City) was married, a lower married rate than that reported for the state of Tennessee (52.1%). More than one-third (37.4%) of PSA residents have never married, 11.6% are divorced, and 6.9% are widowed. Unmarried persons, including divorced and widowed persons, are more likely to live in a one-wage-earner household with alowerincomecompared to amarriedhousehold which is more likely to have two sources of income. As more than half (55.9%) of the PSA population is unmarried, this portion of the population is likely to live within a household with a single source of income. It should be noted, however, that there is a high probability that many of the individuals that have never married are between the ages of 15 and 25 and live with a parent or guardian.

The following graph compares the shares of the population by marital status for the PSA (Johnson City) and the state of Tennessee.

Population by Marital Status (2022)

Johnson City Tennessee

Population by highest educational attainment for 2022 is shown below:

Source: ESRI; Urban Decision Group; Bowen National Research

Earning capacity generally has a high correlation to educational attainment. This is to say that a low share of post-secondary degrees and/or a high share of individuals lacking high school diplomas can limit the incomes and affect the affordability of housing for the population within a given area.

Within the PSA (Johnson City), the share of individuals with a post-secondary degree (48.2%) is notably higher than the share for the state of Tennessee (39.0%). Additionally, the share of individuals within the PSA lacking a high school diploma (9.1%) is lower than the statewide share (10.7%). While the PSA population has a higher share of educational attainment than the state of Tennessee, it is important to note that more than one-quarter (26.5%) of the population has not obtained a high school diploma or college degree. This population is most likely to be in need of affordable housing options within the market.

The following graph compares the populations of the PSA and state of Tennessee by educational attainment.

Population by Educational Attainment (2022)

Johnson City Tennessee

Population by poverty status is shown in the following table:

Source: U.S. Census Bureau, 2016-2020 American Community Survey; Urban Decision Group; Bowen National Research

Approximately 20.5% of the population in the PSA (Johnson City) suffer from poverty, a higher rate than that reported (14.6%) for the state of Tennessee. The poverty shares reported for the under 18 and the 65 and older populations are similar to those reported for the state of Tennessee. While the population age 18 to 64 reports the highest poverty share within both the PSA and state, this share within the PSA (13.8%) is more than five full percentage points higher than that reported for the state (8.4%). Overall, approximately 12,747 individuals live in poverty in the PSA, more than two-thirds (67.3%) of which are between the ages of 18 and 64

The following graph compares the poverty rates by age/overall for the PSA (Johnson City) and the state of Tennessee.

No High School Diploma High School Graduate Some College, No Degree

Associate Degree Bachelor Degree Graduate Degree

Poverty Rates by Age/Overall (2022)

Johnson City Tennessee

Population by migration (previous residence one year prior to survey) for years 2016-2020 is shown in the following table:

Source: U.S. Census Bureau, 2016-2020 American Community Survey; ESRI; Urban Decision Group; Bowen National Research

As the preceding table illustrates, more than three-quarters (77.5%) of Johnson City residents remain in the same house year over year. This is a lower rate than that reported (85.8%) for the state of Tennessee. Among all Johnson City residents, 10.9% moved within the county, 6.5%moved from a different county within the state, and 5.2% moved from a different state or from abroad. It is notable that the share of individuals in the PSA moving from a different county withinthestateismorethandoublethecorrespondingshareforthestate(3.2%). These statistics indicate a relatively stable housing market with a moderate degree of mobility within the PSA but also demonstrate a higher transiency rate within the PSA as compared to the state. The housing supply of the PSA is examined in detail in Section VI of this report.

Population densities for selected years are shown in the following table:

Source: 2010, 2020 Census; ESRI; Urban Decision Group; Bowen National Research

The population density of Johnson City has increased by nearly 12.0% since 2010. This increased population density is projected to continue as it will increaseby1.6%between2022and2027.Similartrendshavebeenexperienced and are projected to continue statewide, as the population density for the state of Tennessee is projected to increase by 2.6% between 2022 and 2027.

C. HOUSEHOLD CHARACTERISTICS

Households by number and percent change (growth or decline) for selected years are shown in the following table:

Source: 2010, 2020 Census; ESRI; Urban Decision Group; Bowen National Research

There are approximately 30,362 households within the PSA (Johnson City) in 2022 The number of households in the PSA increased by 7.7%, or 2,144 households, between 2010 and 2020. Household growth within the state of Tennessee outpaced growth within Johnson City during this time, as the state household base increased by 10.0%. Household growth continued within both the PSA and the state between 2020 and 2022, a trend which is projected to continuethrough2027.Specifically,thetotalnumberofhouseholdsisprojected to increase by 570, or 1.9%, within the PSA between 2022 and 2027. Ongoing household growth within the PSA is expected to increase demand for housing within the area for the foreseeable future. Further, the housing needs of many existing households will likely change in the next five years. This can result from seniors aging in place that choose to downsize, or seniors that relocate to a single-story floorplan due to health considerations. Additionally, some younger households may increase in size which may necessitate relocation to housing with more bedrooms. As such, household composition should be considered along with household numbers.

The following graph compares the percent change in households between 2010 and 2027 for the PSA (Johnson City) and the state of Tennessee:

Household Trends (2010-2027) Johnson City Tennessee

Household heads by age cohorts for selected years are shown in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

With the exception of the under age 25 age group, households are relatively evenly distributed by age within Johnson City. However, household heads between the ages of 55 and 64 comprise the largest age cohort (16.7%), similar to the state of Tennessee. Household heads between the ages of 25 and 34 (16.2%) and 65 to 74 (16.1%) comprise the next largest shares of the overall household base. Senior households (age 55 and older) comprise nearly half (47.3%) of all households within the PSA, while those between the ages of 25 and 54 comprise 45.6% of all households. Household growth between 2022 and 2027 is projected to be greatest among elderly households age 75 and older, though notable growth is also projected for younger households between the ages of 35 and 44. Household growth trends have been and are projected to continue to be similar to statewide trends/projections. The preceding factors demonstrate a good base of potential support for both family and seniororiented housing alternatives within the Johnson City area.

The following graph illustrates the projected change in households by age for the PSA (Johnson City) 2022 and 2027.

Johnson City Change in Household Heads by Age (2022-2027)

Households by tenure for selected years are shown in the following table:

Source: 2010 Census; 2020 Census; ESRI; Urban Decision Group; Bowen National Research

In 2022, slightly more than half (52.5%) of households in the PSA (Johnson City) are owner households, while the remaining 47.5% are renter households. The distribution of households by tenure within the PSA is more even than that reported for the state of Tennessee as more than two-thirds (66.9%) of all households within the state are owner households and approximately 33.0% are renter households. Both the number and share of owner and renter households is projected to remain stable within the PSA between 2022 and 2027. It is important to note that limited available housing inventory can limit future household growth. Therefore, sufficient housing stock in the market is crucial for the PSA to accommodate additional households. Notably, rental product surveyed within the PSA at the time of this report has an overall vacancy rate of just 0.7% while just 51homes were identified as available for purchase. This is detailed in Section VI and demonstrates limited available housing stock within the PSA.

Thefollowing graphillustrateshousehold tenurewithin the PSA(Johnson City) for various years:

Johnson City Households by Tenure (2010-2027)

Owner-Occupied Renter-Occupied

Renter households by size for selected years are shown in the following table for the PSA (Johnson City) and the state of Tennessee:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National

With an average renter household size of 2.01 in 2022, one- and two-person households comprise nearly three-quarters (71.2%) of all renter households within the PSA. This is a larger share of such households compared to those within the state (66.2%), which results in the state having a slightly larger average renter household size (2.22 persons). Over the next five years, the overall numberof renter households in thePSAis projectedto remain relatively stable, with some growth projected among three- and five-person households. One- and two-person households will continue to comprise more than 70.0% of all renter households within the PSA in 2027.

The following graph shows the projected change in persons per renter household for Johnson City between 2022 and 2027:

1-Person

Johnson City Change in Persons per Renter Household (2022-2027)

2-Persons

3-Persons

4-Persons

5-Persons

Owner households by size for Johnson City and the state for selected years are shown in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National

With an average owner household size of 2.31 in 2022, one- and two-person owner households comprise more than two-thirds (68.9%) of the PSA’s owner households. This is a higher share of such households compared to the state (63.1%), which has an average owner household size of 2.42 persons. Over the next five years, owner households in the PSA are projected to increase by 572 households, or 3.6%, overall. This growth is projected to occur among most household sizes, with the exception of three-person households. Considering the growth projected among most household sizes, the average household size among owner households is expected to remain stable through 2027.

The following graph illustrates the projected change in persons per owner household for Johnson City between 2022 and 2027:

1-Person

Johnson City Change in Persons per Owner Household (2022-2027)

2-Persons

3-Persons

4-Persons

5-Persons

The distribution of households by income is illustrated in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

The PSA (Johnson City) in 2022 has a diverse mix of households by income level; however, there is a notably higher share of households in the PSA (42.3%) earning less than $40,000 annually than that of the state (35.3%). Although the number of lower-income households is projected to decrease by 2027 for the PSA,the share of such households (34.7%) will remain higher than that of the state (24.7%) for this time period. While this may signal a moderate shift in housing oriented toward middle- and higher-income households over the next five years in the county, the need for affordable housing will remain critical as more than one-third of households in the PSA will continue to earn less than $40,000 annually.

Median household income for selected years is shown in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

The median household income of the PSA (Johnson City) for 2022 is estimated to be $49,576, which is approximately 20.8% below the Tennessee median income of $62,567 From 2010 to 2022, the median income of the PSA increased by nearly 40.0%. Though notable, this is a smaller increase than the state (48.9%) during the same time period. The median household income for the PSA is projected to increase by an additional 26.4% by 2027, at which time the median household income for the PSA will be $62,681 annually. This projected increase is greater than that projected for the state (18.5%). Nonetheless, the median household income will remain below that projected for the state of Tennessee for the foreseeable future.

The distribution of renter households by income is illustrated in the following table:

Renter Households by Income

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

In 2022, the largest single cohort of renter households by income within the PSA(JohnsonCity)earns between$10,000 and$19,999(18.8%).Additionally, nearly two-thirds (61.2%) of renter households within the PSA earn less than $40,000 annually. This is a higher share of such households compared to that of the state (49.4%). Although the number of renter households earning less than $40,000 annually is projected to decrease within the PSA between 2022 and 2027, the share (52.8%) of such households will remain much higher than thatofthestateoverall(39.4%).Conversely, allincomecohortsinboth the PSA and state earning more than $50,000 are projected to experience renter household growth over the next five years. The continued majority share of lower-income renter households and the increase of higher-earning renter households within Johnson City through 2027 indicates the importance of providing a wide range of rental housing alternatives.

The following table shows the distribution of owner households by income:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

In 2022, nearly 60.0% of owner households in the PSA (Johnson City) earned $60,000 or more annually Between 2022 and 2027, the PSA is projected to experiencegrowth amongownerhouseholds earning$50,000ormoreannually, with thegreatest growthexpectedto occuramong households earning $100,000 or more All owner household income cohorts under $50,000 in the PSA are projected to experience declines. However, owner households earning less than $40,000 will continue to comprise nearly 20.0% of all owner households in 2027.

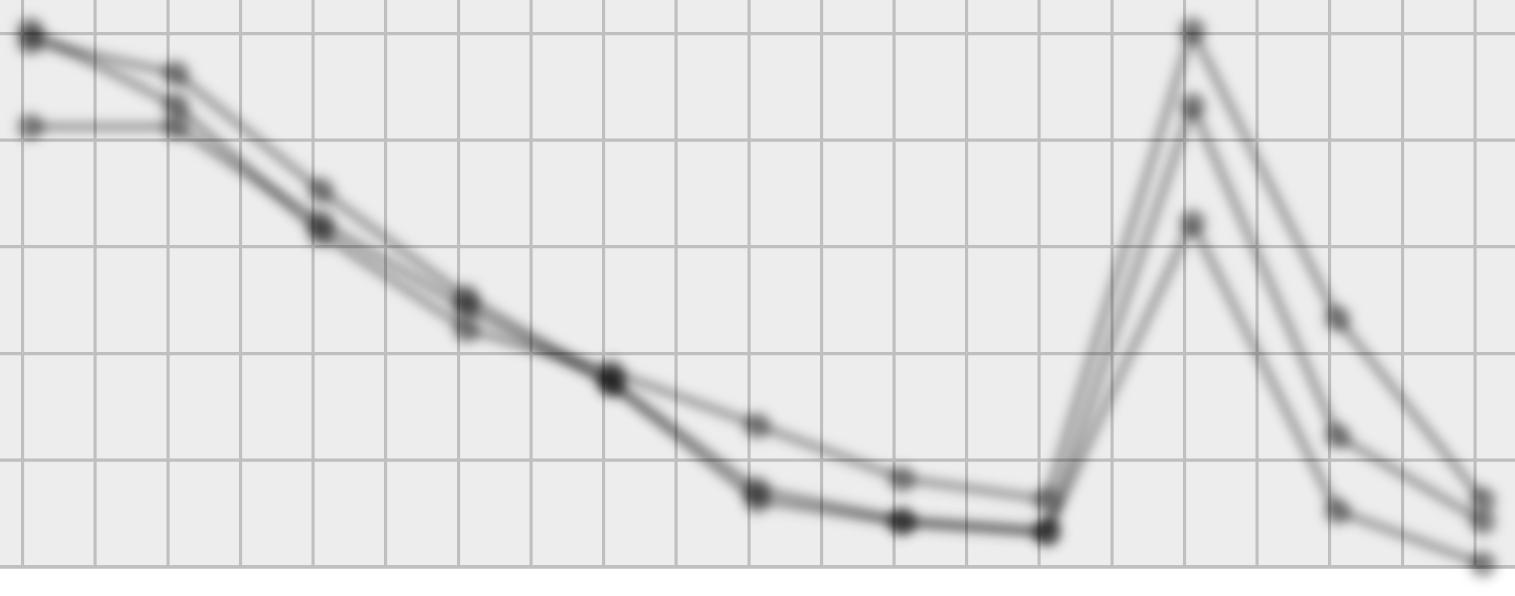

The following graph illustrates household income growth by tenure between 2022 and 2027 for the PSA (Johnson City)

Johnson City Change in Households by Tenure & Income (2022-2027)

Renter Owner

<$20,000

$20k-$29,999

$30k-$39,999

$40k-$49,999

$50k-$59,999

$60k-$99,999

$100,000+

In 2022, there were 14,367 senior households (age 55 and older) in the PSA which represent nearly half (47.3%) of the total households in Johnson City While households between the ages of 55 and 64 are projected to decrease in the PSA by 2027, households age 65 and older are projected to increase by 993 households, or 10.7%. Overall, this will result in an increase of 684 households, or 4.8%, among senior households (age 55 and older) between 2022 and 2027. As such, senior households represent a significant share of the demographic base that contributes to the overall current and future housing demand in the PSA. In an effort to better understand the housing needs for senior households, additional analysis follows.

Seniorhouseholds bytenurefor selected years are shownin the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

In 2022, nearly 70.0% of all senior households (age 55 and older) were owner households while nearly one-third (30.6%) were renter households. In comparison, the PSA (Johnson City) has a higher share of senior renter households as compared to the state of Tennessee (19.9%). These shares for the PSA and state will remain stable through 2027 as the number of both owner and renter households age 55 and older within these geographies is projected to increaseslightlybetween2022and2027.Thesearegoodindicationsofongoing demand for senior-oriented housing alternatives within the PSA, a trend which is also expected to continue throughout the state during this time period.

The following table shows the distribution of senior (age 55+) renter households by income:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

As the preceding illustrates, more than half (56.0%) of senior renter households (age 55 and older) in the PSA earn less than $30,000 annually. This is not surprising given that a large portion of these households are likely retired and live on a fixed income. This is a slightly higher share of very low-income households compared to that reported for the state of Tennessee (49.5%). While the number of senior renter households earning less than $30,000 is projected to decline by 2027, this income cohort will still comprise 49.3% of all senior renter households in the PSA. Conversely, growth is projected among senior renter households earning $50,000 or more annually over the next five years. The large share of very low-income senior renter households and the projected increase among the higher income cohorts should be considered in future housing needs.

The distribution of senior (age 55+) owner households by income are in the following table:

Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research

Comparedto seniorrenterhouseholds in thePSA,thedistribution ofsenior (age 55 and older) owner households is much more weighted toward the higher income cohorts. Senior owner households earning less than $40,000 annually comprise less than one-quarter (22.7%) of all senior owner households in the PSA. This is a much smaller share compared to the senior renters in the PSA (56.0%). Between 2022 and 2027, all growth among senior owner households is projected to occur among households earning $50,000 or more annually. This collective income cohort is projected to increase by 1,506 (26.3%) households over the next five years, while senior households earning less than $50,000 are projected to decline by 878 (20.6%).

D. DEMOGRAPHIC THEME MAPS

The following demographic theme maps for the study area are presented after this page:

• Median Household Income

• Renter Household Share

• Owner Household Share

• Older Adult Population Share (55 + years)

• Younger Adult Population Share (20 to 34 years)

• Population Density

The demographic data used in these maps is based on U S Census, American Community Survey (ACS) and ESRI data sets.

V. ECONOMIC ANALYSIS

A. INTRODUCTION

The need for housing within a given geographic area is influenced by the number of households choosing to live there. Although the number of households in Johnson City at any given time is a function of many factors, one of the primary reasons for residency is job availability. In this section, the workforce and employment trends that affect the PSA (Johnson City) are examined and compared to the state of Tennessee and the United States

B. WORKFORCE ANALYSIS

The PSA (Johnson City) has an employment base of over 66,000 individuals within a broad range of employment sectors Industries of significance within the PSA include health care & social assistance, retail trade, accommodation & food service, and manufacturing Each industry within the PSA requires employees of varying skill and education levels. The following evaluates key economic metrics within Johnson City. It should be noted that based on the availability of various economic data metrics, some information is presented only for select geographic areas, which include the PSA (Johnson City), the Johnson City MSA, Washington County and/or the state of Tennessee, depending upon the availability of such data.

Employment by Industry

The following table illustrates the distribution of employment by industry sector in the PSA (Johnson City) and the state of Tennessee:

*Source: 2010 Census; ESRI; Urban Decision Group; Bowen National Research E.P.E. - Average Employees Per Establishment

Note: Since this survey is conducted of establishments and not of residents, some employees may not live within the study area. These employees, however, are included in our labor force calculations because their places of employment are located within the study area

The labor force within the PSA (Johnson City) is based primarily in four sectors: Health Care & Social Assistance (37.3%), Retail Trade (14.8%), Accommodation & Food Services (9.1%), and Manufacturing (6.7%). Combined, these four job sectors represent over two-thirds (67.9%) of the PSA employment base. Notably, these top four sectors are the same for the state of Tennessee. However, the share of the total employment base among these sectors within the PSA (67.9%) represents a greater concentration of employment within the top four sectors than the state (48.7%). Areas with a heavy concentration of employment within a limited number of industries can be more vulnerable to economic downturns with greater fluctuations in unemployment rates and total employment. While the distribution of employment within the PSA is more concentrated than that of the state, the primary sector (Health Care & Social Assistance) in the PSA is considered a critical service and is typically less susceptible to economic fluctuations.

The following graph illustrates the distribution of the top five employment sectors for the PSA compared with the state.

Top 5 Employment by Industry

Johnson City Tennessee

Employment Characteristics and Trends

Typical wages by job category for the Johnson City Metropolitan Statistical Area (MSA) are compared with those of Tennessee in the following table:

Health Care & Social Assist. Retail Trade Accom. & Food Services Manufacturing Construction

Most annual blue-collar salaries range from $22,950 to $45,020 within the Johnson City MSA. White-collar jobs, such as those related to professional positions, management and medicine, have an average salary of $75,524. Wages within the area are typically lower (9.4% on average) than the overall state wages. Within the MSA, wages by occupation vary widely and are reflective of a diverse job base that covers a wide range of industry sectors and job skills, as well as diverse levels of education and experience. Because employment is distributed among a variety of professions with diverse income levels, there are likely a variety of housing needs by affordability level. As a significant share of the labor force within the PSA is contained within health care & social assistance, retail trade, accommodation & food service, and manufacturing, many workers in the area likely have typical wages ranging between $20,000 and $75,000 annually This further demonstrates an ongoing need for a variety of housing products, in terms of affordability, within the PSA.

Total employment reflects the number of employed persons who live within the county regardless of where they work. The following illustrates the total employment base for Washington County, the state of Tennessee and the United States for the various years listed.

Source: Department of Labor; Bureau of Labor Statistics *Through November

Total employment within Washington County increased between 2015 and 2019, prior to the impact of the COVID-19 pandemic in 2020. Notably, the county employment base declined by 2,466 jobs, or 4.2%, in 2020 as a direct result of the pandemic. This rate of decline, however, was lower than those reported on the state level (5.3%) and nationally (6.1%) during this same time period. Since 2020, the county employment base has added nearly 3,400 jobs through November of 2022. Notably, this recent growth replaces all jobs lost during the initial impact of the pandemic and the most recent total employment figure (59,924) reported is the highest annual total reported over the past decade within the county. This demonstrates that the county employment base has fully recovered from the initial impact of the pandemic, in terms of total employment.

Washington County Total Employment (2012-2022*)

*Through November

Unemployment rates for Washington County, the state of Tennessee and the United States are illustrated as follows:

Source: Department of Labor, Bureau of Labor Statistics

*Through November

The annual unemployment rate within the county declined each year between 2013 and 2019 but spiked by nearly three full precentage points in 2020 as a direct result of the COVID-19 pandemic. Despite this increase, however, the annual unemployment rate within the county (6.3%) was below both state (7.4%) and national (8.1%) levels. Further, the unemployment rate within the county declined by more than three full percentage points since 2020, to a rate of 3.1% through November of 2022. This is lower than pre-pandemic levels reported for the county and remains below both state and national levels.

Unemployment Rate (2012-2022*)

Washington Co. Tennessee U.S.

*Through November

In order to get a better sense of the initial impact the COVID-19 pandemic had on the local economy and the subsequent recovery; we evaluated monthly unemployment rates. The following table illustrates the monthly unemployment rate from January 2020 to September 2022 in Washington County.

Source: Department of Labor, Bureau of Labor Statistics

As the preceding illustrates, the monthly unemployment rate within the county spiked by nearly ten full percentage points during the initial impact of the pandemic, reaching a high of 13.5% in April of 2020. While elevated, monthly unemployment rates within Washington County were lower than those experienced in many markets during this time, some of which reported monthly unemployment rates of 20.0% or higher. Further, monthly unemployment rates within the county quickly began to decline starting in May of 2020. Notably, the most recent monthly unemployment rate reported for November of 2022 was just

3.2% and monthly unemployment rates within the county have remained below 4.0% each month since July of 2021. Recent monthly unemployment rates have also been lower than pre-pandemic levels.

WARN (layoff notices):

The Worker Adjustment and Retraining Notification (WARN) Act requires advance notice of qualified plant closings and mass layoffs. WARN notices were reviewed on January 18, 2023. According to the Tennessee Department of Labor & Workforce Development, there have been no WARN notices reported for Johnson City over the past 12 months. This is a good indication of the stability of the local economy.

In-place employment reflects the total number of jobs within the county regardless of the employee's county of residence. The following illustrates the total in-place employment base for Washington County.

Source: Department of Labor, Bureau of Labor Statistics *Through June

The preceding table illustrates in-place employment (people working within Washington County) increased by 5.2%, or 3,032 jobs, from 2013 to 2018. While the greatest single decrease over the past decade occurred in 2020 (3.2%) and can be largely attributed to the COVID-19 pandemic, it is notable that the county experienced a similar rate of decline in 2013 and another slight decline in 2019, just prior to the impact of the pandemic in 2020. Despite the significant decline in 2020, the county experienced an overall net increase of 2,847 jobs, or a 4.7% increase, from 2012 through June of 2022.

Employment Outlook

The ten largest employers within the Washington County area are summarized in the following table: Employer

Ballad Health

East Tennessee State University

James H. Quillen Veterans Hospital

Citi Group

Advance Call Center

Johnson City School District

AO Smith

Frontier Health

General Shale Headquarters

Mullican Flooring

Source: The Chamber Johnson City; 2022

Six of the top ten employers within the Washington County area are within the healthcare and manufacturing industries, two of the prominent industry segments within the PSA, as detailed earlier in this section. The remaining top employers are within the education, financial, and technology industries. Based on the preceding factors, the area’s largest employers are within industry segments which are generally considered to offer critical services and therefore are expected to contribute to economic stability within the Johnson City/Washington County area.

A map delineating the location of the area’s largest employers is included on the following page.

According to a representative with The Chamber Johnson City, the Johnson City and Washington County economy has been experiencing dynamic growth.

One key driver for growth is East Tennessee State University (ETSU) investing in several projects including the renovation of the student center and the Martin Performing Arts Center, which opened in 2020 as part of a $46 million investment.

The following table summarizes some additional recent and/or ongoing economic development projects within the Johnson City/Washington County area as of the time of this analysis:

Winged Deer Park

Caliber Collision

10

$17.4 million N/A

$2 million N/A

Completed: Opened an entertainment venue in 2022; Within three months of opening, expanded by 3,000 square feet; Also made Johnson City their corporate headquarters

Completed: New 25,000 square-foot location for operations center

Under Construction: New 24,000 square-foot financial center; ECD mid-2024; New Interactive Teller Machine to be completed spring 2024

Under Construction: 40-acre expansion; Plans include adding six baseball fields and an umpire locker room; ECD summer 2023; Estimated economic impact $4 million

Under Construction: Auto body repair shop consisting of 16,345 square feet; ECD early 2023

Under Construction: Plans include adding three new floors for perinatal and neonatal care center and pediatric specialties; ECD 2024 West Walnut Street Redevelopment

Approved: Expansion of existing facility; Manufacturer and developer of high-temperature heat pumps

Under construction: Will include a distillery, brewery expansion and museum ECD 2023 Stone Mountain Technologies (Anesi)

Completed: A 175,000 square-foot building located in Washington County Industrial Park; Expecting to expand again in 2024

Completed: A 375,000 square-foot auto part manufacturing building for General Motors; Positions expected to pay $17/hour; May add a second phase with a $29 million investment which could create 90 new jobs from 2026 to 2027

Under Construction: Began multi-phase project for fiber buildout in 2022; Once completed approximately 61,000 residents/businesses will have access to broadband services

In addition to the preceding economic development projects, East Tennessee State University has several projects planned or under construction. These projects are summarized as follows: Project Name & Address

Integrated Health Services

Brown Hall (Phase 1 & II)

Academic Building

$44 million

$94 million

$52 million

University Innovation Park N/A

ECD: Estimated completion date

N/A: Not available

Under Construction: Renovation of Lamb Hall has begun; ECD fall 2023; Entire project ECD fall 2025

Planned: In design phase; Renovation of existing building

Planned: Campus Center Building to be demolished; New building to consist of 60,000 square feet; ECD fall 2025

Proposed: City board approved master plan of mixed-use research park in 2021; Still in concept stage; Being developed by ETSU and Johnson City; High paying jobs expected to be created; Infrastructure estimated at $10 million

The following summarizes recent and/or ongoing infrastructure projects within the Washington County area. Project Name

Peoples Street

West Walnut Street Redevelopment

Knob Creek Road

University Innovation Park

Added traffic light at four-way intersection; Increased number of right-turn lanes from Greenline Road to Peoples Street; Increased the number of left-turn lanes from Peoples Street to Greenline Road

New power and utility lines, streetscapes, sidewalks, landscaping

Five-lane roadway (two are bike lanes) on State Road to Franklin Road

Demolition of exiting building; Adding roadways and stormwater retention pond

University Innovation Park Additional infrastructure needed for research park

ECD – Estimated Completion Date

N/A – Not available

N/A Completed: In spring 2022

$30 million (All phases) Under construction: ECD 2023

$15-$20 million Under Construction: ECD 2025

$3 million

$350,000

Proposed: Part of the University Innovation Park being developed by ETSU and Johnson City

Approved: City board approved master plan in 2021

C. PERSONAL MOBILITY

The ability of a person or household to travel easily, quickly, safely, and affordably throughout a market influences the desirability of a housing market. If traffic congestion creates long commuting times or public transit service is not available for residents without a vehicle, their quality of life is diminished. Factors that lower resident satisfaction weaken housing markets. Typically, people travel frequently outside of their residences for three reasons: 1) to commute to work, 2) to run errands or 3) to recreate.

Commuting Mode and Time

The following tables show two commuting pattern attributes (mode and time) for the PSA (Johnson City) and the state of Tennessee:

Mode

Source: U.S. Census Bureau, 2016-2020 American Community Survey

Source: U.S. Census Bureau, 2016-2020 American Community Survey

Noteworthy observations from the preceding tables follow:

The share (90.0%) of commuters in the PSA that either drive alone or carpool is comparable to the share (90.7%) of the same commuting modes in the state of Tennessee. Shares of other commuting modes are also similar between the PSA and state.

Generally, commute times to work in the PSA are shorter than those on the statewide level. Nearly three-quarters (76.4%) of PSA commuters have travel times of less than 30 minutes to work, which is a much higher share of short commute times when compared to the state (60.2%). More than 41.0% of Johnson City residents have travel times of less than 15 minutes and more than one-third (34.9%) have travel times between 15 and 29 minutes. Only 2.9% of PSA commuters have travel times of 60 minutes or more, which represents a smaller share when compared to the state (6.3%).

Based on the preceding analysis, it is clear that a significant share of PSA (Johnson City) residents has relatively short commutes and they rely on their own vehicles or carpools to commute to work. A drive-time map showing travel times from the geographic center of the PSA (Johnson City) follows this page.

Commuting Patterns

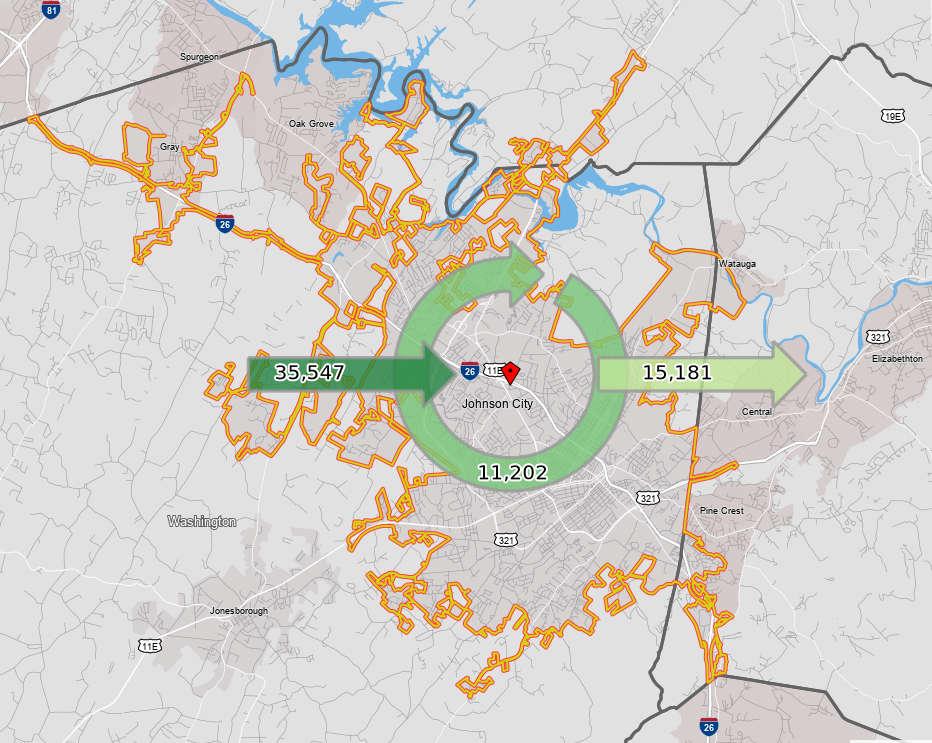

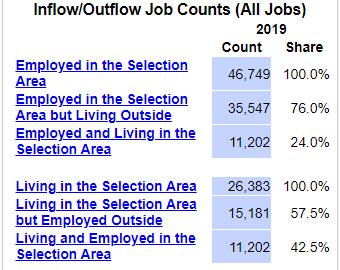

According to 2019 U.S. Census Longitudinal Origin-Destination Employment Statistics (LODES), of the 26,383 employed residents of Johnson City, 11,202 (42.5%) stay in the city for work, while the remaining 15,181 (57.5%) are employed outside the city. In addition, 35,547 people commute into Johnson City from surrounding areas for employment. These 35,547 non-residents account for more than half (57.4%) of the people employed in the city and represent a notable base of potential support for future residential development. The following illustrates the number of jobs filled by in-commuters and residents, as well as the number of resident out-commuters.

Source: U.S. Census, Longitudinal Origin-Destination Employment Statistics (LODES)

Characteristics of the Johnson City commuting flow in 2019 are illustrated in the following table.

Johnson City, TN: Commuting Flow Analysis by Earnings, Age and Industry Group (2019, All Jobs)

Source: U.S. Census, Longitudinal Origin-Destination Employment Statistics (LODES)

Note: Figures do not include contract employees and self-employed workers

Based on the preceding data, people that commute into Johnson City for employment are more likely to be middle-aged (30 to 54 years), earn moderate wages, and work primarily in the services industries. Of the county’s 35,547 incommuters, more than half (51.3%) are between the ages of 30 and 54 years, nearly two-thirds (64.0%) earn $3,333 or less per month (less than $40,000 annually), and nearly three-quarters (70.3%) work in the services industries. Resident outflow workers tend to be similar in age as compared to inflow workers, earn comparably more, and are less likely to work in the service industry. By comparison, resident workers have the highest share of workers ages 29 or younger (28.0%), are more likely to earn lower wages (between $15,000 and $40,000 annually), and a vast majority work in the services industries (76.4%).

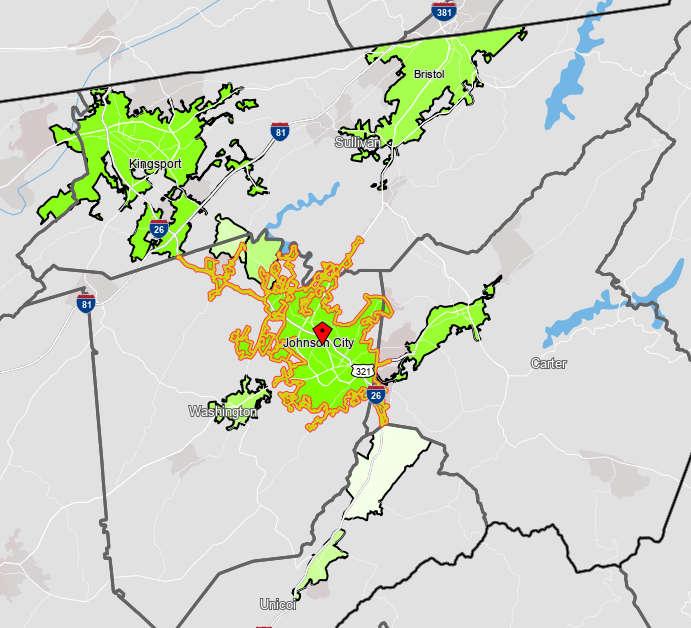

The following map and corresponding tables illustrate the physical home location of people working in Johnson City, as well as the concentration of jobs within Johnson City and the surrounding region.

Source: U.S. Census, Longitudinal Origin-Destination Employment Statistics (LODES)

Statistics provided by LODES indicate that nearly one-quarter (24.0%) of the Johnson City workforce are residents of the city Kingsport (6.1%), Elizabethton (3.1%), and Bristol (2.4%) contribute the next largest shares of Johnson City workers. This is not surprising given the proximity of these areas from Johnson City. It is of note, however, that more than half (57.3%) of all Johnson City workers commute from areas not listed in the preceding table/figure. This is reflective of the many smaller towns/cities throughout the more rural areas surrounding Johnson City, as the Johnson City area serves as an employment center within the region. In terms of commute distances, nearly half (49.4%) of the Johnson City workforce has commute distances less than 10 miles, while nearly 81.0% have commutes of less than 25 miles. Thus, the majority of Johnson City workers reside within a reasonable commute of their place of employment. However, nearly 9,000 workers commute into the city from 25 miles or more, with the majority (65.3%) of these workers commuting from 50 miles or more to their place of employment. These inflow workers with lengthy commutes represent a base of potential support for future residential development, as it is likely/possible that some of these workers would prefer to

reside more near their place of employment if housing which was affordable to them was available. It should be pointed out that from previous surveys our firm has conducted of commuters in areas similar to Johnson City, it is not uncommon for 20% to 40% of non-residents commuting into a market to have interest in moving to the same market in which they work.

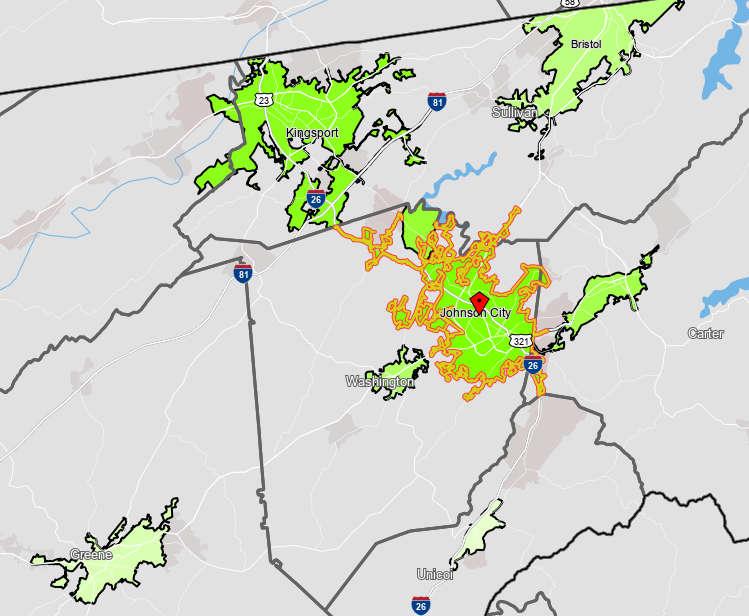

The following map and corresponding tables illustrate the physical work location of Johnson City residents, as well as the commute distances for these workers.

Source: U.S. Census, Longitudinal Origin-Destination Employment Statistics (LODES)

Of the 26,383 employed residents of Johnson City, nearly 43.0% are employed within Johnson City Kingsport (9.3%), Oak Grove (6.1%), and Elizabethton (3.5%) employ the next largest shares of Johnson City residents. As the data illustrates, nearly 80.0% of Johnson City residents commute less than 25 miles to work, with the majority (75.5%) of these residents commuting less than 10 miles to their place of employment. A slightly larger share (16.4%) of Johnson City residents commute more than 50 miles to work as compared to the 12.5% share of inflow workers commuting to Johnson City from areas more than 50 miles from the Johnson City area.

D. MIGRATION PATTERNS

Unlike the preceding section that evaluated workers’ commuting patterns, this section addresses where people move to and from, referred to as migration patterns. For the purposes of this analysis, the Census Bureau’s Population Estimates Program (PEP) is considered the most reliable source for the total volume of domestic migration. To evaluate migration flows between counties (city level data not available) and mobility patterns by age and income at the county level, we use the U.S. Census Bureau’s migration estimates published by the American Community Survey (ACS) for 2020 (latest year available). It is important to note that while county administrative boundaries are likely imperfect reflections of commuter sheds, moving across a county boundary is often an acceptable distance to make a meaningful difference in a person’s local housing and labor market environment. The data provided by the PEP is intended to provide general insight regarding the contributing factors of population change (natural increase, domestic migration, and international migration), and as such, gross population changes within this data should not be compared among other tables which may be derived from alternate data sources such as the Decennial Census or American Community Survey (ACS).

The following table illustrates the cumulative change in total population for Washington County between April 2010 and July 2020. Note that Washington County data was considered as components of population change data is not available on a city (Johnson City) level. However, as Johnson City is the primary population center of Washington County, data presented for Washington County is likely reflective of trends within Johnson City as well.

Estimated Components of Population Change for Washington County, Tennessee April 1, 2010 to July 1, 2020

Source: U.S. Census Bureau, Population Division, October 2021 *Includes a residual (-14) persons unaccounted for it total estimates.

Based on the preceding data, the population change within Washington County from 2010 to 2020 was primarily driven by natural decrease (more deaths than births) and domestic migration. The data illustrates that, without the positive influence of domestic and international migration (net increase of 8,359), the population of Washington County would decline significantly as a result of natural decrease (decrease of 1,041). Natural decrease typically occurs in areas where there is a comparably high share of older population, or within areas where the younger population migrates from the area prior to establishing a family. While domestic migration accounts for more than three-quarters (81.5%) of the total net migration in the PSA, a notable share (18.5%) of the net migration can be attributed to international migration. Regardless, both domestic and international migration are vital to the overall population change

in Washington County. As such, it is important that an adequate supply of income appropriate rental and for-sale housing is available in the future for the area to continue benefiting from positive net migration.

The following table details the shares of domestic in-migration by three select age cohorts for Washington County from 2011 to 2020.

Washington County, Tennessee

Domestic County Population In-Migrants by Age,

Source: U.S. Census Bureau, 2015 & 2020 5-Year ACS Estimates (S0701); Bowen National Research

The previous table illustrates that from 2011 to 2015, 42.0% of domestic inmigrants to Washington County were under the age of 25, while 52.9% of domestic in-migrants were between the ages of 25 and 64. By 2020, the share of in-migrants under the age of 25 increased to 45.0%, while the share of domestic in-migrants between the ages of 25 and 64 decreased to 44.7%. The share of domestic in-migrants ages 65 and older also increased from 5.1% to 10.3% during this same time period. Median age figures for both periods indicate that domestic in-migrants that originated from a different Tennessee county were younger by approximately three to four years than in-migrants that originated from out of state.

To further illustrate Washington County migration patterns, the following table summarizes the top 10 counties from which Washington County both attracts and loses residents. Note that the table only lists regional counties contained within Tennessee and the bordering states. Washington County: County-to-County Net

Source: U.S. Census Bureau, 2019 5-Year American Community Survey; Bowen National Research

As the preceding table illustrates, the top 10 regional in-migration counties account for 62.0% of the total inflow for the county, while the top 10 regional out-migration counties account for 69.7% of the outflow. Notably, the top two counties (Carter County and Sullivan County) for both in-migration and outmigration are adjacent to Washington County and nine of the top ten counties for each segment are located within the state of Tennessee. Mecklenburg County, North Carolina (Charlotte) and the independent city of Winchester, Virginia represent the only two regional out-of-state areas within the top ten in/out migration segments. In total, Washington County experienced a positive net migration of more than 1,100 persons regionally, based on the preceding data. This means that Washington County draws new residents from a number of counties, not only within the state of Tennessee, but also from the surrounding region. In order to sustain these positive migration trends within the county, it is important there is a sufficient supply of housing available in the market at a variety of affordability levels.

Maps illustrating immigration flow by county to Washington County and emigration flow by county from Washington County for 2020 are shown on the following pages.

While the data contained in the previous pages illustrates the overall net migration trends of Washington County and gives perspective about the general location where these individuals migrate to and from, it is also important to understand the income levels of in-migrants as it directly relates to affordability of housing. The following table illustrates the income distribution by mobility status for Washington County in-migrants.

Geographic mobility by per-person income is distributed as follows:

Source: U.S. Census Bureau, 2020 5-Year American Community Survey (B07010); Bowen National Research

According to data provided by the American Community Survey, a significant portion of the population that moved to Washington County earned less than $25,000 per year. Note that this data was provided for the county population (not households) ages 15 and above. It is likely that a significant share of the population earning less than $25,000 per year consists of children and young adults considered to be dependents within a larger family. This population segment also includes those that earned no income.

Specifically, this lower income segment (<$25,000) represented 56.7% of the Washington County population that moved within the county, 69.4% of the people moving to the county from another Tennessee county, and 57.6% of people moving to the county from a different state. A far lower share of the population that moved within the past year earned more than $50,000 annually.

Based on our evaluation of the components of population change between 2010 and 2020, Washington County benefits from domestic and international migration, while natural changes (births vs. deaths) detracts from the county population change. A majority of these in-migrants are between the ages of 25 and 64 years, although there has been a notable recent increase in migrants age 65 and older. The top 10 regional counties account for the majority of both inmigration (62.0%) and out-migration (69.7%). Nonetheless, this indicates that Washington County also benefits from in-migration even beyond the regional area (Tennessee and bordering states) evaluated within this section. Washington County also experiences a net in-migration of more than 1,100 persons, based on data contained within this section. In addition, a vast majority of in-migrants earn low to moderate wages. As such, future housing supply will need to account for both the age and income levels of these migrants.

VI. HOUSING SUPPLYANALYSIS

This housing supply analysis includes a variety of housing alternatives. Understanding the historical trends, market performance, characteristics, composition, and current housing choices provide critical information as to current market conditions and future housing potential. The housing data presented and analyzed in this section includes primary data collected directly by Bowen National Research and secondary data sources including American Community Survey (ACS),U.S.Censushousinginformation,anddata providedbyvariousgovernment entities and real estate professionals.

While there are a variety of housing options offered in the Primary Study Area (PSA, Johnson City), we focused our analysis on the most common housing alternatives. The housing structures included in this analysis are:

• Rental Housing – Rental properties consisting of multifamily apartments (generally with five or more units within a structure) were identified and surveyed.