BROKERS 2026: WINNERS REVEALED Nearly

Helping first home buyers with the Australian Government 5% Deposit Scheme

ANZ and Brokers.

Working better together.

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

x.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

Brokers facing headwinds head-on

04 Statistics

Less is more for this year’s Top Commercial Brokers as the trend shifts towards fewer but higher-value deals that prioritise quality over volume

BIG INTERVIEW

DAVID SMITH

Liberty’s chief distribution o cer steers brokers through volatile markets with a focus on clarity and consistency

FEATURES COMMERCIAL LENDING

Brokers power through turmoil, exploring bold new territories in commercial lending

Regional markets outperforming the capitals

06 Opinion

Where brokers win in the AI shift

14 Bright spots in commercial

Amid uncertainty, new opportunities emerge for brokers in commercial property

24 SMEs at the coalface

As cost pressures bite, SMEs seek broker advice for fast, flexible funding

28 A new funding frontier

Brokers eye development finance but must tread carefully

12 FEATURES NON-MAJORS ROUNDTABLE

34 A bumpy road for A&E finance

Second-tier lenders look beyond price towards innovation, flexibility and human-centric service

Rocky markets reshape asset finance, putting speed and structure in focus

65 Mastering empathy

How leadership rooted in empathy builds employee trust and loyalty

68 Leading in crisis

Seven leadership traits that are critical when the going gets tough

72 Other life

Virtual reality boxing and cold showers sharpen broker Julian Choo’s focus

50 PEOPLE BROKERAGE INSIGHT

70

Gippsland Finance Solutions steps up for borrowers as banks leave town

Our daily newsletter. Keep on top of property market trends, business strategy, and what industry leaders have to say.

On 20 July 1969, Australians from all corners of the country sat in awe around their black-and-white TV screens as Neil Armstrong became the first man in history to put feet on the moon.

It would take 57 years after that giant leap for mankind for Australia’s 31st prime minister, Anthony Albanese, to bring the country to a collective standstill of such magnitude as his wartime address resounded across the eight states and territories. “ This is a testing time for our nation,” Albanese proclaimed. “The war in the Middle East has caused the biggest increase in petrol and diesel prices in history.”

Channelling the ANZAC spirit, he called on Australia’s fine men and women to make sacrifices for the greater good. Take the bus where possible, he advised. Work from home if you can. Save fuel for the truckies and farmers who keep our nation running.

While Albanese’s broadcast address to the nation – the sixth of its kind on record, with previous instances concerning the outbreak of World War II and the onset of COVID-19 – was maligned for being an overblown status update, it at least threw

Despite the multitude of challenges, the resilience and adaptability of the Australian broking community shine through

into sharp relief the severity of the US-Iran war’s impact on the domestic economy.

Energy price shocks have torn up the script for interest rates; consumer sentiment and business confidence have taken a hit; and house-building targets are under pressure from higher input costs. T hese are all challenges that are set to have a dramatic e ect on the broking community. MPA’s 2026 Commercial Lending Guide shows that business owners are dipping deeper into defensive mode, causing a rethink of the broker-borrower relationship.

But despite the multitude of challenges, the resilience and adaptability of the Australian broking community shine through. It was impressive to hear how brokers are shifting with the times, facing headwinds both new and old head-on to extend their influence over the commercial lending market even further.

The cream of the commercial broking crop is celebrated in MPA’s Top Commercial Brokers 2026 report on page 39. These are the professionals truly pushing the industry forward to deliver the best outcomes for their clients while serving as advocates for the broking community as a whole.

The news cycle might be shifting from hour to hour, but at least one thing is constant – the broking industry is only going from strength to strength.

William Farrington, editor, MPA

EDITORIAL ENQUIRIES tel: +612 8437 4711 william.farrington@keymedia.com

SUBSCRIPTION ENQUIRIES tel: +61 2 8311 5831 • fax: +61 2 8437 4753 subscriptions@keymedia.com.au

ADVERTISING ENQUIRIES claire.tan@keymedia.com

www.keymedia.com

Australia, Canada, USA, UK, NZ and Asia

MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the

AUSTRALIAN BROKER simon.kerslake@keymedia.com T +61 2 8437 4786 NZ ADVISER alex.knowles@keymedia.com T +64 9 200 1319

MORTGAGE

86%

of brokers say AI will be essential within two years

Australian dwelling values rose 9.9% in the year to March 2026, with regional markets (11.7%) outpacing capitals (9.3%). Growth was strongest in Perth, Darwin and the WA and Queensland regions, while Melbourne and regional NT saw comparatively modest gains, Cotality reports.

65% of brokers have no documented AI strategy in place

37% of brokers use AI regularly and confidently in business

CommBank customer data shows today’s typical first home buyer is younger, borrowing more with a smaller deposit and increasingly purchasing with others, as flexible pathways, government deposit schemes and co-buying arrangements help more Australians step into homeownership sooner than they did in 2021.

3%

of brokers have formal AI policies for governance today

Source: Connective, TheStateofAIReadinessinAustralianBroking report

Cotality’s latest Pain & Gain report shows profitmaking resales reached 95.9% in the December quarter, the highest level in more than 20 years, with a record median gain of $365,000 and only a small share of resales selling at a loss.

RESALES: PROFIT VS LOSS

Rising prices are reshaping daily life and eroding Aussies’ financial confidence. New Youi research finds most Australians felt greater cost of living pressure in 2025, with more than two in five worse o financially and over a quarter hit by higher costs every day.

say cost of living pressures increased more in 2025 than in previous years feel the impact of rising living costs daily feel their financial situation has worsened

Source:

Source: Cotality Pain&Gainreport

New research from NGM Group shows regional Australia is drawing skilled workers and city dwellers, with a ordability a key lure and most movers reporting a better quality of life, underscoring the regions’ growing appeal as places to live and work.

AUSTRALIA'S REGIONAL DRAWCARDS

40% 47% 78% of Australians surveyed say the regions are attracting more highly skilled and professional workers of respondents believe more a ordable housing is a key regional drawcard of metro Australians find the idea of regional living highly appealing of movers to the regions report a better quality of life

Source:

AI is upending the broking industry, but brokers will always be the gatekeepers, argues LMG’s Sam White

AT LMG’S recent Growth Summit, we talked about how quickly artificial intelligence is changing the way businesses operate, and the di erent ways people are responding to it. We framed it around three groups:

• Doomers: focused on the risks, the possibility of job losses, and what could go wrong with the rise of AI

• Boomers: using AI where it saves time, but not pushing it further

• Zoomers: who are inspired by AI and rebuilding how they run their businesses with AI at the centre

between brokers who know how to use it and those who don’t.

The ‘human in the loop’

The idea that AI replaces brokers misses the point about why customers choose a broker in the first place: It’s not the back-end e ciency. It’s the support.

Buying a home or making a big financial decision is emotional, complex and often stressful. People want someone in their corner who understands that.

Good brokers don’t just find a loan. They help clients understand what’s possible, what’s

Good brokers don’t just find a loan. They help clients understand what’s possible, what’s smart and what fits their life, not just today but over time

Within the broker industry, I see business owners across all three groups every day. Almost every service-based industry will be reshaped by AI. But I believe brokers are in a unique position compared to most.

At the Growth Summit, we kept coming back to one idea: high-tech, high-touch. AI will change how the work gets done. But the value of a broker isn’t disappearing; it’s becoming clearer. Our future isn’t broker or AI – it’s broker and AI. The real divide will be

smart and what fits their life, not just today but over time.

Customers still want a ‘human in the loop’. Someone who understands their situation and can talk candidly about trade-o s, challenge assumptions and connect lending decisions to real life: family, business, future plans.

For customers with complex lending scenarios, self-employed clients, investors and business owners, brokers are part of the inner circle alongside accountants, planners and

solicitors, so their lending strategy complements a customer’s broader plans.

Trust shows up in the real moments in life – the late-night call about a property they’ve fallen in love with, the deep dive into their numbers to project future earnings from equipment purchases, or the long-term plan to get a family released as guarantors from their son’s or daughter’s mortgage.

It’s this combination of personal guidance, long-term relationships and support that AI can’t replace.

What AI will do is take a bigger share of the admin and analysis. We’re already seeing brokers use AI tools in MyCRM for things like note writing, quality assurance checks and faster turnaround.

Throughout 2026, LMG’s roadmap will have more automation across documents, smarter performance insights, earlier signals on client risk, and tools that help brokers act sooner, not later – all within one platform. By embracing, rather than avoiding, AI, we’ll have less Boomers and more Zoomers. And these tools will give brokers more time to focus on client relationships, strategic guidance and referral partnerships.

Brokers remain the gatekeepers AI works fast, but it’s not perfect. And without human judgement, it can get things wrong quickly.

That’s where brokers come in. Interpreting, challenging and applying it properly – with professional oversight.

Brokers are still the gatekeepers of the finance journey. As one panellist said at our Growth Summit, “If there’s a problem, ASIC will pursue you, not ChatGPT.”

The brokers who win won’t choose between tech and relationships. They’ll be the ones who master both and move faster than the rest of the market.

Chief distribution o cer David Smith is sharpening Liberty’s

TWO YEARS after joining Liberty as chief distribution officer following more than 15 years at Aussie Home Loans, David Smith has made himself comfortable. Having taken the wheel of the broker channel at the prominent non-bank lender, he has become the face of a strategy built on consistency, communication and adaptability – non-negotiables in the cutthroat world of alternative finance.

It helps that he jumped aboard a welloiled machine that has, over multiple decades, established itself as a non-bank powerhouse with brokers at the core of its identity.

With almost 30 years behind it, “Liberty has a clear sense of purpose and curiosity, and that really shows in how people work together,” Smith tells MPA

“Liberty has always represented choice and possibility. From the beginning, our free-thinking mindset has guided the way we approach lending.”

But while he has taken command of a ship with its rudders firmly in place, Smith is not one to sit back and let the tide take its course. He is acutely aware that past success doesn’t guarantee future relevance, particularly in a market where new entrants emerge quickly and customer expectations reset constantly.

Smith has proactively navigated major challenges over the past two years while keeping Liberty’s competitive edge and service proposition at the front of brokers’ minds.

There has been no shortage of challenger brands moving into the alternative lending space in recent years, while an increasingly bullish private credit market is upping the stakes for what was already a competitive environment.

Amid this diversity of financing options, brokers’ and clients’ demands for fast turnaround times, flexibility and high-touch

lending only becoming more sophisticated over the past 24 months.

To supercharge its SME capabilities, Liberty acquired a controlling stake in cash flow lending specialist Moula last year, e ective from 31 December 2025. Smith is excited to see where this relationship goes.

“[Moula’s] digital-first technology and credit expertise complement our own approach and help brokers with business

“Spending more time listening to brokers and focusing on clarity and consistency has been incredibly rewarding”

support from BDM and credit teams are as high as they’ve ever been.

All the while, the macroeconomic environment has been wildly unpredictable, punctured by wild swings in funding costs, consumer sentiment marred by cost of living pressures and, more recently, an energy crisis spurred by Middle East conflict with profound implications for the domestic mortgage market.

For Smith, doubling down on what makes Liberty unique, while implementing improvements where necessary, has been a fine balancing act.

Diversification has become a strong focal point, with o erings across SME, SMSF, commercial, asset finance and personal

clients who need fast and flexible options,” he says.

“For brokers, a diversified o ering means more opportunity. It helps them meet more customer needs, build deeper relationships and grow their businesses with confidence.”

Whether it’s through expanded SME o erings, SMSF lending advancements or updated residential lending policies, Smith stresses the importance of keeping brokers in the know.

“I’ve enjoyed strengthening the way we respond to brokers in a market that’s been moving quickly,” he says.

“Spending more time listening to brokers and focusing on clarity and consistency has been incredibly rewarding. Trust really

Name: David Smith

Role: Chief distribution o cer

Company: Liberty

Years in the industry: 20+

Recent career achievement: Named an MPA 2025 Global 100 Mortgage Leader

comes from consistency. We put a lot of focus on being easy to work with, responding quickly and communicating clearly. When brokers feel they can rely on us, everything else falls into place.”

Smith makes sure his team is laser-focused on actively listening and responding to broker demands. “Whether a broker works with us regularly, or is yet to, their feedback helps shape what we do next. If they tell us they need more speed, more clarity or more support, we take that seriously.

to support them, and earning that trust is something we work on every day.”

Empathy also matters. “When you understand the pressure brokers are under, you can design processes that make their lives easier.”

Australia’s leading lenders use NextGen to accelerate time-to-yes. They’re probably using us.

“We always encourage brokers to reach

Outside of work, Smith understands the virtue of maintaining a balanced approach to life, and he always makes sure to set aside time for other interests.

“Travelling gives me perspective, and I always love to visit somewhere I’ve never been before; even better if there happens to be a Formula 1 Grand Prix there!”

“Liberty has always represented choice and possibility. From the beginning, our free-thinking mindset has guided the way we approach lending”

out early in the process. Our team is great at exploring options, and a quick conversation often opens pathways that aren’t obvious at first glance. Over time, that builds genuine partnership.”

But the challenge isn’t always about keeping up – it’s about continually raising the bar.

“By listening closely and staying adaptable, we make sure Liberty strives to become a leading partner in all environments.”

Reflecting on the personal attributes that allow him to excel in his role, Smith highlights the importance of resilience in a fastmoving industry. He understands the virtue of cutting through the noise and staying focused on what matters, while maintaining a sense of curiosity. Staying aware of industry trends and broker pain points is a must-do.

“In my role, determination, collaboration and communication are essential. You need to bring people together behind shared goals and deliver consistently for brokers. And you need to take accountability. Brokers trust us

Despite the abundance of industry-wide challenges, Smith reckons the future is bright for Liberty and the alternative lending space as a whole. If anything, market pressures have highlighted how important responsibly operated alternative lenders truly are.

“Customers benefit from having choice, and alternative providers play a key role in making that possible,” he says.

“Liberty is in a strong position, with solid momentum across our products and a distribution network that continues to perform well. The focus now is on building on that strength and finding even more ways to improve the experience for brokers and customers.”

As for what’s next, Smith wants Liberty to continue being seen as a trusted and reliable partner – and to reiterate, one that o ers “free-thinking solutions”.

“More broadly, I want our brand to represent accessible finance backed by genuine care for customer outcomes. A brand that continues to evolve while staying true to the values it was built on.”

Commercial applications don’t have to mean a different system, a different workflow, or a different experience for your brokers.

ApplyOnline® is the platform Australia’s brokers already know and trust for residential lending — and it handles commercial loans with the same streamlined, digital process.

Why lenders are extending to commercial on ApplyOnline

One platform

All loan typesresidential, commercial, bridging, and SMSF

Built-in tools available

Digital VOI, Open Banking, and automated document management

Subject to lender activation.

No re-training

Brokers lodge commercial the same way they lodge residential

Fully configurable

Complex entity structures, debt service calculations and lender credit policy

Join the growing network of lenders choosing digital over manual for commercial distribution. Get started today.

Higher funding costs and geopolitical shocks are reshaping commercial finance, yet resilient businesses and savvy brokers continue to drive strong deal pipelines

THIS YEAR’S Commercial Lending Guide comes to you at a particularly uncertain time for the Australian business environment –and the world as a whole.

At the time of writing, a nervous ceasefire was in place between the US and Iran following weeks of conflict that shook markets across the globe. However, with peace talks between the two countries collapsing without a deal, no end to the conflict was in sight.

Meanwhile, here in Australia, energy price shocks have torn up the script on interest rate forecasts, with all major banks increasing their odds on more cash rate hikes to come from the central bank.

This hawkish reassessment of interest rates has fed through to higher funding costs for residential and commercial borrowers alike, while the fallout from higher dayto-day living expenses has yet-to-be-seen consequences for productivity.

Business sentiment was trending lower even before the war escalated, with the NAB Business Confidence Index falling into negative territory in February, ending nine straight months of positive sentiment.

Business confidence proceeded to collapse to COVID-era lows in March, with April’s print not expected to fare any better.

But all this fear, uncertainty and doubt doesn’t change the fact that commercial finance deals are powering ahead.

The many lenders, brokers, aggregators and technology providers that MPA sat down with to gather insights for this guide said the same thing: businesses are resilient, cunning and highly adaptable to market shocks.

True, the landscape is changing. Alternative lenders are creating waves in the higher-risk end of the pool; SMEs are shifting from expansionary mode to protective mode; commercial property sentiment is highly sector dependent; and asset and equipment finance is becoming concentrated on incomegenerating purchases.

But the broking industry is adapting to the changing winds of commercial lending with vigour. The diversified broker is a well-worn trope by now, but it’s an accurate one. MPA’s first-ever development finance guide highlights how brokers are moving into bolder new territories of the broader commercial lending landscape.

The experts who contributed to this guide universally agreed that commercial lending is a huge opportunity for brokers, and as more business owners look to the broking industry for a holistic approach to their financing needs, market share has only way to travel: up.

Going with the flow is not an option as rising rates, global shocks, surging migration and tech reshape Australia’s commercial market

“FIRM AND PATIENT optimism always yields its rewards,” Mexican oligarch and former world’s richest person Carlos Slim once said. A bit of that wisdom wouldn’t go astray for commercial brokers right now.

Amid falling business confidence, lower capital growth expectations, high CBD vacancy rates and, of course, a Middle East war that threatens to disrupt all corners of the Australian business environment, few would blame you for being jittery about the commercial property outlook.

Yet across Australia’s diverse business landscape, new opportunities are emerging for commercial brokers within certain sectors, regions and demographics.

Speaking with MPA, industry experts across the banking, non-bank lending and technology sectors universally acknowledge that the headwinds are real, but so is Australian businesses’ ability to roll with the punches.

Stuck in the middle

“Right now, we believe the commercial property market sits somewhere in the middle,” says Liberty chief distribution officer David Smith. He notes that the tone is cautious as clients await clarity on how current global events will impact market conditions in the long term.

Chris Thomas, executive commercial broker and equipment finance sales at NAB, phrases the mood as “tilting cautiously towards optimism”, even as parts of the broader economy “remain uneven”. While business confidence softened in the March

quarter, “conditions have broadly held up, sustaining the gains made through 2025”.

Brighten’s head of commercial lending, Ben Mckell, cautions that, with the Reserve Bank of Australia’s tightening cycle bringing the rate back up to 4.1% in March, volatility in valuations and borrowing costs is on the rise. Higher rent, medical and insurance costs haven’t helped, while trade-related volatility “has further weighed on economic confidence and investment planning”.

might be more considered, the activity is still there.”

Thomas is confident that underlying momentum will remain in place, with forward indicators such as capital expenditure plans and orders heading in the right direction.

AT ORDE Financial, director of distribution Lee Prior says, “What we’re hearing from brokers is there’s still plenty of movement, especially from SME owners, and that’s a

“Where the fundamentals are good, confidence tends to follow. Brokers who really understand their local markets will be finding solid opportunities”

David Smith, Liberty

Mckell doesn’t dance around the issues. “No one expected fuel to be hitting $3.50 a litre, and no one thought a rate rise would come again so soon,” he says. “Inflation is unfortunately out of control, and it creates a cyclical impact; tenants, whether residential or commercial, are going to see their rents significantly increase over the next three to six months or at their next rental review.”

That said, Smith is still seeing businesses investing where it makes sense, all the while relying on experienced brokers “to help them navigate risk and structure deals in a complex environment … While the conversations

positive sign.” Business owners are being practical with their lending needs: while conditions are far from perfect, they’re working with brokers to get their businesses in the best position available to them. This can range from buying their premises outright to lock in certainty, to refinancing or restructuring debt to optimise cash flow.

But “it’s certainly not a boom”, adds Craig Stuart, head of commercial at MA Money, “and performance across commercial assets remains highly dependent on asset quality and sector dynamics. The biggest headwinds are likely linked to broader economic uncer-

“Today’s commercial brokers are looking for faster clarity, greater flexibility and deeper relationships with their lending partners – not just sharper pricing”

Chris Thomas, NAB

tainty, particularly given ongoing global events. The impact of Middle East tensions means we’re seeing upward pressure on inflation, leading to cash rate increases and localised rate increases.”

Australia’s industrial powerhouse

The industrial property segment – including warehouses, workshops and mixed-use properties – seems to be a hive of activity in 2026, thanks to a combination of limited stock and strong demand that has driven price appreciation.

NAB data shows that industrial continues

to outperform on sentiment, capital growth and rental expectations, due to low vacancy rates and ongoing demand linked to logistics, warehousing and supply chain resilience.

“That’s translating into sustained borrower confidence and a steady pipeline of highquality deals,” says Thomas.

At MA Money, over 35% of enquiries are currently geared towards the industrial segment, fuelled by growth across e-commerce, logistics and manufacturing.

“Tenant demand appears to remain high in many markets and in some cases is outstripping supply,” says Stuart. He is seeing strong

appetite for vacant land in growth regions on the fringes of metropolitan areas.

Outside of industrial, Mckell has witnessed a renewed interest in some specialist commercial property assets. “We have seen quite a few examples of just your normal residential property investor looking at diversifying and buying boarding houses, which fall in that commercial realm,” he says. Additionally, childcare centres are being seen as an attractive asset class with good rental yield.

‘Silo warehouses’ are gaining traction as a hybrid solution for online businesses, combining storage, light industrial and flexible workspace in one. “Unlike residential, there is still a good supply for commercial assets, hence it represents great opportunities for investors diversifying into the space,” says Mckell.

While office spaces remain in a postCOVID slump, with vacancy rates still higher than expected, there is “selective interest in retail and office assets, particularly in

locations with strong tenant profiles”, says Smith. “Where the fundamentals are good, confidence tends to follow. Brokers who really understand their local markets will be finding solid opportunities.”

Migration redrawing the commercial map

Through ORDE’s work with demographer Bernard Salt, the lender has zeroed in on how migration is reshaping the commercial property market across the country.

Research shows that around 32% of Australians were born overseas and, in many outer-metro and regional corridors, migrant communities aren’t just settling. “They’re starting and growing businesses, which naturally drives demand for commercial property like workshops, warehouses, o ce and clinic suites and mixed-use sites tied directly to the business,” says Prior.

This shift is most evident across the country’s commercial heartlands in the eastern seaboard cities of Brisbane, Melbourne and Sydney, where new employment precincts

“Inflation is unfortunately out of control, and it creates a cyclical impact; tenants, whether residential or commercial, are going to see their rents significantly increase over the next three to six months” Ben Mckell, Brighten

and SME clusters are forming alongside population growth.

Prior says “investment across Australia’s commercial heartlands remains strong, underpinning business confidence, job creation and the growth of new precincts and communities”.

ORDE’s data shows that commercial and industrial building approvals are up around

27% compared to pre-pandemic levels.

“[This] tells us businesses are still planning and investing,” says Prior. “And when you look at segments like tradies (a big driver of SME activity), the numbers continue to grow, with close to two million tradies nationwide, many of them running their own businesses.”

For brokers, those trends translate directly into commercial opportunities as business

owners move from renting to owning, while upgrading to more suitable premises or bringing property into SMSFs.

“These are also the areas where brokers are most active,” Prior says. “Our role as a non-bank is to back brokers in those moments with lending solutions that reflect how these businesses operate. From our perspective, understanding how these shifts play out business by business is what ultimately drives commercial property loan activity.”

As brokers capture an ever-greater share of the commercial property market, technology is becoming fundamental to their growth.

Systems like NextGen’s ApplyOnline platform, the standard bearer of Australian loan application and lodgement, play a pivotal role in driving this expansion. NextGen

Introducing two new home loans packed with features and flexibility for you and your clients.

chief customer o cer Tony Carn says, “NextGen’s role is fundamentally about removing the friction that has historically made commercial lending feel out of reach for brokers who’ve built their practice around residential.”

ApplyOnline is already ubiquitous in the Australian broking industry, which means most brokers can manage commercial applications on a platform they’re already familiar with.

“Importantly, as brokers work through commercial applications on the platform, the structured workflows and lenderspecific requirements built into ApplyOnline actively help them understand how commercial loans are put together – so the platform itself becomes part of the learning curve,” says Carn.

ApplyOnline supports brokers by outlining each lender’s policies and requirements while o ering dynamic checklists that change from deal to deal and lender to lender.

But tech can only take brokers so far. Commercial lending is inherently more complex, and involves considerably more variables, than residential lending.

Carn regularly sees brokers approaching commercial applications with a similar mindset to residential lending, which can frustrate and delay the loan application process. This underscores the importance of user-friendly systems and portals at the lender level.

“[Brokers’] demands haven’t just changed; they’ve crystallised,” Carn explains. “Commercial brokers now expect the same guided, structured lodgement experience they have for residential, and lenders are increasingly recognising that providing that experience is a competitive advantage in attracting broker business.”

Thomas attests to this. Brokers’ expectations of their lending partners continue to rise, “and rightly so”, he says. “Today’s commercial brokers are looking for faster

clarity, greater flexibility and deeper relationships with their lending partners – not just sharper pricing.”

Brokers are looking for early, informed conversations that quickly surface whether a deal is feasible, so they can manage client expectations with confidence. They also value lenders who can tailor solutions around a customer’s broader goals, rather than taking a one-size-fits-all approach.

NAB is meeting these demands “by leaning into our relationship-led model”, says Thomas. He explains how bankers retain lending authorities, enabling real-time credit discussions and faster decision-making.

NextGen and integrated with ApplyOnline, allow brokers to collect data straight from banks, which reduces the risk of AI-altered or fraudulent documents. It also removes the back and forth of manual document collection that slows down the application process and frustrates clients.

“For business borrowers, having transaction data that accurately reflects cash flow and income patterns – rather than relying solely on what can be captured in tax returns – can make a genuine di erence to both the speed and the outcome of a credit decision,” says Carn. “That’s a real value-add a broker can o er their commercial clients.”

“Commercial property decisions today are rarely standalone … Brokers who stay close to their clients – and build strong working relationships with accountants, advisers and other intermediaries – tend to create deeper, longer-term opportunities as needs evolve” Lee Prior, ORDE Financial

NextGen plays its part by working with its lender partners to build out commercialspecific configurations within ApplyOnline “so that the platform does more of the heavy lifting in guiding brokers through what each lender actually needs, at the point of submission”.

Open banking is also becoming increasingly relevant to the commercial lending conversation, “particularly for the selfemployed and small business borrowers that commercial brokers typically work with”, notes Carn.

Systems like Frollo, which is owned by

From banks to non-banks and tech providers, all commercial property experts agree on one thing: the sector represents a massive opportunity for brokers.

Current estimates put broker share of the broader commercial lending space somewhere between 30% and 40% (unlike residential, there is no cold, hard data), but the only way is up.

Mckell estimates that the share has risen from the upper 20% range just two years ago to the mid 30% range today and is expected to hit 50% over the next two to five years.

“Brokers are becoming increasingly confident in the commercial lending space, and we’re seeing a noticeable shift in mindset,” says Mckell. If anything, Brighten’s substantial growth over the past 24 months, expanding its distribution team from six to 20, with dedicated commercial BDMs in

more strings to their bow, multiplied by clients having more confidence in the broker market to help with their business and commercial needs, naturally we can expect greater participation,” predicts Stuart.

“We expect more mortgage brokers to step into commercial lending by drawing on

“Our commercial product range shares similarities with our residential product suite, ensuring a more simplistic approach that most brokers can resonate with” Craig Stuart, MA Money

Victoria – and New South Wales and Queensland soon to follow – proves that brokers are increasingly influencing the commercial landscape.

Stuart believes education plays a big role in advancing brokers’ influence in the commercial space, with industry bodies the MFAA and FBAA performing “excellent work” in educating and training brokers on commercial property opportunities.

“Combine the fact brokers are looking for

the relationships they already have,” adds Smith. “It often starts with a simple conversation about future plans, such as moving into self-employment or expanding operations. It’s all about asking the right questions. Liberty works closely with brokers to build their knowledge and confidence so they can identify these commercial opportunities and workshop scenarios with us.”

As uncertainty around growth, inflation and interest rates has increased, “brokers

have become more central to helping customers navigate trade-offs between timing, structure and risk, and are increasingly supporting customers to plan for a wider range of potential outcomes”, says Thomas. He is seeing brokers move beyond transaction execution into a more advisory, end-to-end role by supporting clients earlier in the journey, shaping funding strategies and helping customers weigh up risk, timing and structure.

“At the same time, the quality of brokers entering commercial lending has lifted,” says Thomas. “More experienced professionals are stepping into the space, raising the standard of deal preparation and customer engagement.”

“Commercial lending isn’t new, but the opportunity for brokers has never been clearer,” continues Prior, who describes a holistic approach to growth.

“Commercial property decisions today are rarely standalone. They sit alongside broader business and personal considerations for the client, which is why brokers who stay close to their clients – and build strong working relationships with accountants, advisers and other intermediaries – tend to create deeper, longer-term opportunities

as needs evolve … Brokers are far more central to these conversations now.”

Despite the increasingly diverse needs of borrowers, Smith says it’s a common misconception that commercial loans are too complex. “While some applications do require more detail, many are more straightforward than brokers expect … With the right support, brokers can start to see possibilities in the commercial space, rather than challenges, which in turn strengthens their own o ering to their clients,” he says.

Prior believes complexity often comes from business owners’ “layered financial situations”. He explains, “They might have strong turnover and solid businesses but also ATO debt, legacy lending structures or short-term facilities that were put in place during tougher periods and no longer make sense.”

While that can look risky, “in reality, it often just needs the right structure and the right lender”, says Prior. He notes that commercial lending has been central to ORDE’s growth over the six years since it opened its doors. Today around 80% of ORDE’s book supports SME owners and operators. “This isn’t niche or fringe lending. These are everyday business owners who keep the economy moving – employing people, investing locally and adapting as conditions change.”

As a relatively new player in the commercial world, MA Money is “mindful that awareness is paramount”, says Stuart. To build awareness, MA Money has recruited a national BDM team to meet brokers where they operate. Simplicity is the name of the game at MA Money. “Our commercial product range shares similarities with our residential product suite, ensuring a more simplistic approach that most brokers can resonate with. The aim is to not overcomplicate the process,” says Stuart.

Brighten, meanwhile, is meeting broker demands “by continuing to invest heavily in our people, our processes and the way we

support brokers”, says Mckell. “Brokers value responsiveness and clear scenario guidance, so we have expanded our team to ensure we can respond quickly and provide meaningful support at every stage of a deal. We are also simplifying our internal.”

NAB is also investing heavily in broker capability, education and support – from credit skills workshops to dedicated banker coverage across Australia – so brokers know exactly who they’re dealing with and where to go for help. In 2025 alone, NAB delivered 29 commercial credit skills workshops to

“We are watching global political developments closely and considering how they may impact financial markets, inflation and energy prices,” says Smith. “Shifts in these areas typically flow directly through to commercial confidence. For brokers, understanding how customer needs change in this environment will be key. The more tailored the solution, the better the outcome could be for the borrower.”

For now, uncertainty reigns. As Mckell explains, “When we look at market interest at the moment, it really is hard to predict. Locally

“NextGen’s role is fundamentally about removing the friction that has historically made commercial lending feel out of reach for brokers who’ve built their practice around residential”

Tony Carn, NextGen

around 650 brokers, alongside a further 10 bespoke sessions tailored to key aggregator partners. “The focus is simple: reduce friction, improve certainty and support brokers to deliver better outcomes for their customers,” says Thomas.

There remain some pretty sizeable question marks hanging over the commercial property outlook. Despite well-documented resilience among Australia’s small business community, there’s no way of knowing how the ripple e ects of the Iran war will play out.

Energy shortages are a pervasive threat that risk causing price shocks in all corners of the Australian economy – commercial property included. If the most hawkish of RBA rate predictions play out, alongside persistent supply chain pressure, there could be challenging times ahead.

in Australia, the current mood is shaped by the fuel crisis, the rising cost of living and rising interest rates, along with what’s happening overseas.”

Stuart also cautions that tighter disposal income among Australian households “could lead to softer consumer spending and potentially temper momentum in certain sectors”.

But this uncertain economic climate only serves to reinforce the importance of brokers in delivering personalised solutions for business owners.

As Prior says, “SME owners need support across property, debt and growth, and brokers who understand di erent borrowing structures – and work with lenders that can accommodate them – are well placed to support clients as their needs evolve.”

Is it business as usual right now? Perhaps not, but nor is it as bleak as the news cycle would have you believe.

8042 reviews on

Amid rising costs and compliance pressures, SMEs turn to faster, flexible funding options and full-scope broker advice to protect cash flow resilience

WITH SMES making up 97% of all Australian businesses and employing 42% of the national workforce (per official government data), they are often the first to feel the turbulence when the economy hits a stormy patch.

Such is the situation today as business owners weigh headwinds blowing in from both home and abroad.

Amid the geopolitical strife that has muddied the outlook on interest rates, along with wobbly consumer sentiment and tightening lender risk appetites, SMEs are being particularly strategic with their financing needs. This is rapidly reshaping the brokerSME relationship as the market shifts from a growth mindset to an aware stance – but within this fast-evolving landscape lies an opportunity for the broking community to truly prove its worth.

“SMEs aren’t just looking for funding; they’re looking for speed, someone to help them through the process and a structure that matches how they actually operate” Roberto Sanz, Prospa

SME credit demand can be best described as “steady overall”, according to Prospa general manager sales and partnerships Roberto Sanz. While large-scale purchases aren’t rolling in en masse, they’re in need of more “operational” financing. “We’re seeing many businesses seeking funding to smooth cash flow and stay flexible, rather than borrowing purely to chase growth,” says Sanz.

It’s no secret why this is the running theme of SME finance right now. Cost pressures –chiefly payroll and bills – remain high, and suppliers are taking their time to pay receivables.

“When businesses don’t have large buffers, they seek certainty and access to capital to keep trading with confidence,” says Sanz. “We continue to see strong demand across flexible, revolving funding solutions, which

reflects the broader SME need for certainty and adaptability, particularly during busy periods like EOFY [end of financial year].”

These are certainly not new struggles for SMEs, but they are becoming more pronounced in a more demanding macroeconomic environment. Compliance obligations have never been higher for businesses, and interest rates are playing havoc with funding costs. SMEs tend to be at the coalface of these headwinds.

Global economic uncertainty – like the little matter of the USIran war – is also playing a role. “What happens on the world stage continues to impact Australian inflation, and SMEs – the backbone of the economy – often feel that pressure first,” says Sanz.

As they face up to these challenges, SMEs are demanding speed and certainty from their lending partners. Unfortunately, this often comes up against rigid credit settings that don’t align with how small businesses tend to operate.

Anmol Dhingra, director and mortgage broker at WIN Financial Group, says it’s becoming “selectively harder” for SMEs to access funding from the major banks. “Banks are tightening credit appetite and risk models, meaning more SMEs fall outside policy, despite being viable,” he says. Amid increased regulatory pressure and strict capital requirements, their preference is for propertybacked, lowerrisk lending, as opposed to cash flow lending without strong security.

“It’s not that banks don’t want to lend to SMEs, but you have to be clean. Your story needs to make sense,” says Dhingra.

Irregular and seasonal revenue fluctuations – a wellknown bugbear across the entire SME space – can throw up additional hurdles in the application process and lead to unpredictable deal outcomes, especially if a business looks unconventional on paper.

While traditional lenders play a dominant role in providing finance for businesses that match their risk appetite, SMEs are increasingly using nonbank lenders “because these

of SMEs say they can remain cash flow positive over the next 12 months

2.7 months of expenses on average Businesses hold

30%

allows them to maintain control over their financing requirements,” he adds.

The move towards alternative lending options “is one of the biggest shifts I’ve seen in my career”, says Dhingra. “Nonbanks are no longer ‘lenders of last resort’; they’re becoming first choice for many SMEs, especially for shortterm and working capital needs. Faster turnaround times are also a big win with nonbanks.”

Dhingra believes this upheaval of the SME lending landscape is “positive and revolutionary. It will increase competition, which means more products will come into the market to support SMEs. It will also have better pricing”.

But as more lenders pile into the space, the onus is on brokers to properly educate themselves on the funding options at their clients’ disposal. “The more you know the better,” says Dhingra.

14%

of SMEs only have one month or less of expenses in reserve of SMEs have no reserves at all of SMEs plan to access external finance in the next 12 months (up from 31% in September 2025)

Payday super is shaping up as the next big compliance crunch for Australia’s small businesses – and a pivotal opportunity for brokers to step in as strategic partners.

Source: Prospa SMESentimentReport/YouGov SME Sentiment Research (Feb 2026)

providers offer the certainty, speed and relevance essential to business continuity”, says Sanz.

“SMEs are seeking solutions that meet their highyield needs, combining funding with speed and a service proposition that

From 1 July 2026, employers will need to pay super at the same time as wages rather than quarterly, effectively removing a key shortterm liquidity buffer from SMEs’ cash flow.

While the change may sound incidental, it’s causing a stir in the SME lending community. Many business owners are already grappling with higher costs and softening demand, yet Prospa research shows that nearly a third of SMEs are completely unaware of the change, and a significant cohort are unsure they can meet the new schedule.

With 30% holding one month or less of expenses in reserve and 14% with no reserves at all, the margin for error is thin.

“The compliance changes to payday super will have a massive impact on SMEs’ cash flow,” says Sanz. “For businesses with thin buffers, moving super payments forward

compresses working capital. The risk isn’t the rule itself; it’s being caught unprepared and being non-compliant.”

Sanz emphasises that cash flow planning is going to be key for businesses. “If you don’t have or can’t create the reserves to fund this new change, it’s time to plan a funding line to support your cash flow through this change.”

super payments a year to paying super every pay cycle, which reduces flexibility and leaves far less margin for error – particularly for businesses with variable payrolls or uneven revenue.

“With cash reserves already low for many SMEs, this makes active cash flow management and access to flexible funding more important than ever.”

“It’s not that banks don’t want to lend to SMEs, but you have to be clean. Your story needs to make sense” Anmol Dhingra, WIN Financial Group

For brokers, this is a timely trigger to broaden conversations beyond rate and product. Payday super is an obvious entry point to review payroll timing, cash bu ers and upcoming obligations, then align flexible funding solutions with real operating needs such as wages, BAS and supplier payments.

As Sanz notes, “The main risk with payday super is not higher costs but the change in payment cadence. It impacts SME cash flow right away by forcing businesses to increase the number of super payments, adding extra pressure on already-tight cash positions.

“Many SMEs will move from making four

Lift awareness: particularly for the 41% of SMEs who either don’t understand the change or aren’t aware of it at all

Whether it’s about payday super, cash flow management or operational matters, brokers continue to play a quintessential role in guiding SME clients through the full spectrum of financing needs.

Dhingra believes brokers should move away from a purely transactional mindset to give clients a more personal touch. “It is not transactional and rate focused any more. It’s more advisory focused where a broker will not just focus on the transaction in hand but on long-term growth of their clients, which involves funding strategies, cash flow planning and navigating di erent lender options.”

Strengthen liquidity and cash flow planning: especially for businesses holding less than three months of cash reserves

Because of this shifting broker-SME dynamic, it’s becoming increasingly important for brokers to work alongside SMEs’ wider professional services partners to effectively coordinate applications.

“A lot of businesses I meet have a great turnover, but they fail to understand that banks rely on what’s left over,” says Dhingra. “I have started involving clients’ accountants more often [it helps that Dhingra comes from an accounting background]. The best brokers are becoming long-term business advisers, not just deal writers.”

Over the coming months, Sanz expects low cash reserves, global economic conditions and inflationary pressures to reshape how SMEs prepare for the rest of 2026. For many, this is likely to increase demand for cash flow solutions to help them plan for future uncertainty.

“From our side, we expect to continue investing in our partner and customer propositions, enhancing products and services that help SMEs navigate volatility with confidence,” says Sanz. “The focus remains on flexibility, relevance and supporting real-world business needs.

“Taken together, 2026 is less about chasing big growth and more about resilience, timing and staying in control, with less room for error.”

Match funding solutions to real operating needs: including products that provide flexible, on-demand access to capital

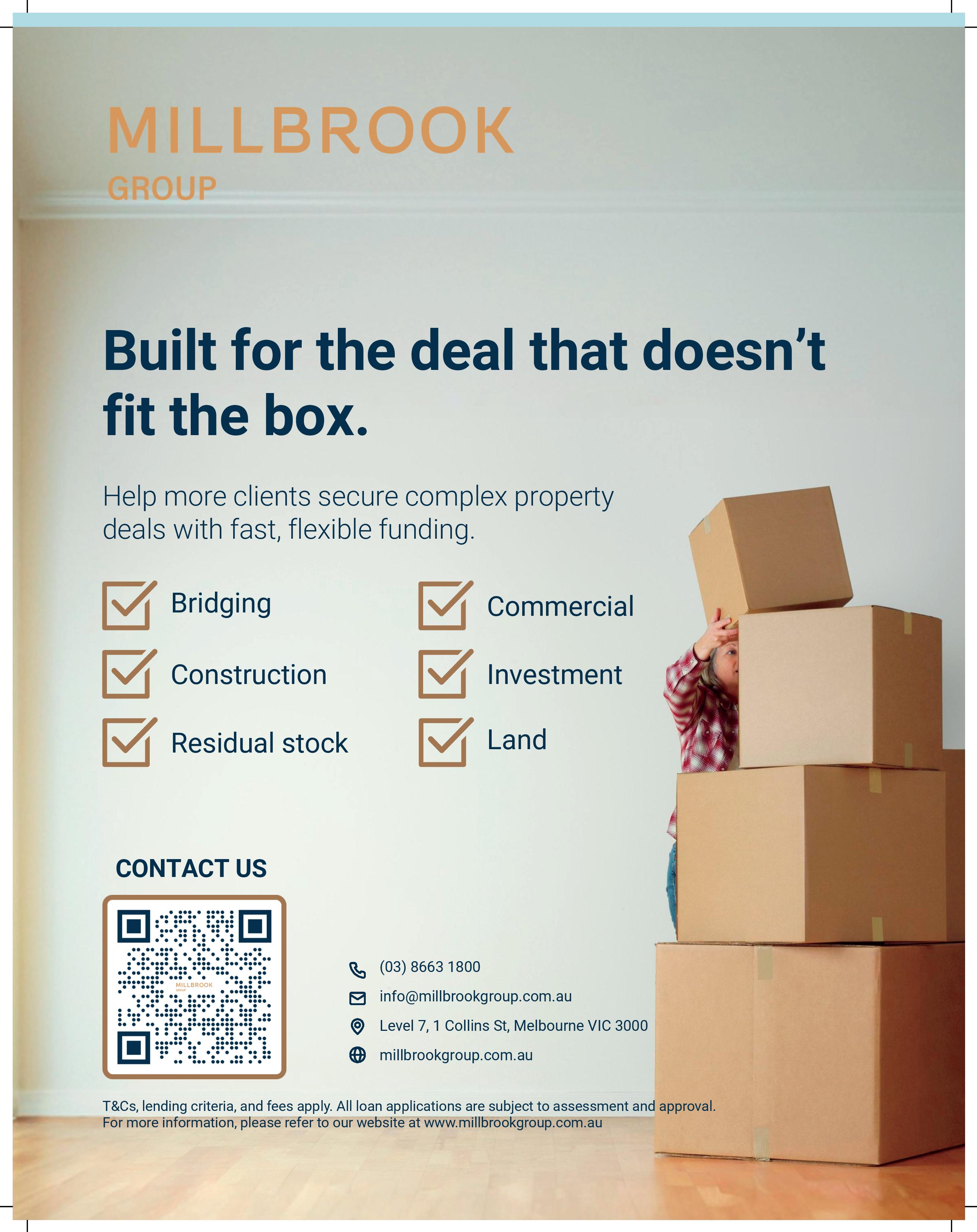

As brokers diversify into brave new territories, development finance is moving into their crosshairs – but brokers must tread with caution

be the next great growth opportunity for brokers?

In world where broker market share of the residential lending space is nearing its terminal limit, brokers have become adept at transferring their skill sets into brave new territories. This has led to rapid growth in broker market share of the commercial lending market; within that broad umbrella lies development finance, encompassing land acquisition and construction of residential, mixed-use and commercial projects.

Development finance is still a niche, technically demanding space, full of complexities and trip hazards for the ill-prepared. It requires firm knowledge of project feasibility, exit strategy and presale require-

“With Australia’s housing requirements over the next five years, brokers have the opportunity to play a much larger role in facilitating funding for developers” George Lyall, Millbrook

ments. Yet that hasn’t stopped a growing cohort of brokers from eyeing the sector with zeal, drawn by larger deal sizes and deeper client relationships.

To get the lowdown on where the space is going – and how brokers fit into the equation – MPA caught up with a panel of leading development finance specialists

for this edition’s inaugural development finance pulse check.

Amid shifting risk appetites, both traditional and non-bank lenders play an important role in the development finance sector. Banks are highly active in this space where

it fits their credit parameters, but they can be hobbled by issues like presale requirements and leverage limits.

“That’s where non-bank and private credit lenders have been playing an increasingly important role,” says James Munn, commercial and development finance expert and director of Sydney-based brokerage Chifley Securities. “They can often offer more flexibility around structure or parameters, and in situations where timing is critical they can move more quickly.”

One such non-bank lender is La Trobe Financial, whose chief lending officer, Cory Bannister, says it can assess credit “holistically, rather than purely through rigid covenants and policy settings”. This allows La Trobe Financial to support viable projects

that fall outside the metrics required by some major lenders, which is “of critical importance in addressing the housing supply gap in this country, now and in the future”.

Risk appetite varies from project to project and from asset class to asset class, while private lenders often stick to a particular niche. So the challenge isn’t necessarily accessing capital but “understanding which lender is best suited to a particular deal”, says Munn.

Millbrook Group general manager George Lyall has seen the market become more “tiered”, with banks funding lower-risk projects and alternative lenders supporting projects that require more flexibility. “The major banks remain active but are generally more selective and focused on experienced sponsors, strong presales and lower-leverage structures,” says Lyall.

Pallas Capital group executive Jason Arnold has seen a clear increase in both loan volumes and loan sizes in the private credit space. “A major driver has been the continued retreat of banks from higher-risk segments –particularly construction finance, higherleverage transactions and projects with lower levels of pre-commitments such as presales or pre-leases,” he says.

Arnold also explains how the growing participation of institutional capital in Australian private credit has materially expanded the sector’s capacity, supporting growth in both settled loan volumes and the size of individual facilities.

“We’re also seeing many borrowers gravitate towards a single, flexible lender who can provide the entire capital stack, whether that’s first mortgage, second mortgage or preferred equity,” adds Arnold. “The ability to offer higher leverage and faster execution is contributing to both higher deal volumes and larger loan sizes across the space.”

Between a rock and a hard place Development finance is a unique challenge for banks. On the one hand, they have a regulatory obligation to tightly manage

risk. On the other hand, they have the unregulated private credit space breathing down their necks. Could this lead to a rethink on risk appetite among the major Australian banks?

In the UK and US markets, where private credit is substantially more mainstream, Munn has seen the banks gradually reassess

running. This does vary depending on the project type, with broadly appealing projects like high-density, affordable residential apartment complexes more likely to attract more easy-going presale requirements than, say, a luxury complex in Darling Point. It is, however, early days. Lyall explains that banks are still generally looking for 50%

“As market conditions remain somewhat uncertain, developers are increasingly turning to brokers for access, structuring expertise and lender navigation”

Cory Bannister, La Trobe Financial

their lending appetite and approach to remain competitive.

Munn has already seen some Australian banks start to ease up on presale requirements, which have historically been a major bottleneck for getting projects up and

• Usually short-term, ranging from 6 to 36 months

• Capitalised interest during construction

• Generally up to 70–80% LVR of total development costs or gross realisable value (GRV)

• Staged drawdown funding based on construction milestones

• Repaid upon project completion through the sale of units or refinancing

presales by debt coverage, while alternative lenders may be willing to work with lower thresholds in exchange for stronger equity or pricing. Millbrook doesn’t have a presale requirement at all.

Traditional banks are also becoming more open to providing residual stock facilities, previously a domain largely controlled by private credit. Chifley Securities recently handled a project that saw a property developer refinance away from a private construction funder to provide the developer with sufficient time to partially sell down and lease up the project’s residual stock.

But Bannister doesn’t see the major banks meaningfully re-entering the development finance space any time soon. “Pullback from development finance by major lenders began some time ago and has been a consistent feature of this cycle, rather than a recent shift,” he says.

Although recent headlines have suggested banks may be pivoting back into the space, prevailing geopolitical uncertainty and broader macro volatility are likely to keep them cautious for longer.

Higher interest rates and elevated labour and construction costs “are undermining

• 58% of property developers planning new projects within the next six months (above series average of 47%)

• 49% of developers targeting residential projects (53% in Q3)

• 20% of developers targeting industrial property (up from 19% in Q3)

Just 4% of developers targeting offices (down from 17% in Q3)

8% of developers targeting retail (up from 3% in Q3)

effects of the Iran war are yet to be fully quantified), “but the legacy of volatility means lenders remain cautious”, says Lyall.

He adds, “Developers who have locked-in contracts with reputable builders and conservative feasibility assumptions are still able to access funding, but the margin for error is much smaller than it was a few years ago.”

Nonetheless, overall development finance activity remains strong across all lender categories, and appropriate funding terms can be found across all asset types – as long as the broker knows where to look.

Industrial remains a highly financeable asset class due to robust tenant demand, while institutionally backed build-to-rent and affordable social housing projects are going well. Data centres are also emerging as a specialist asset class.

project feasibility and increasing perceived lender risk”, notes Arnold. In response, lenders are taking steps to derisk transactions, whether by reducing LVRs or implementing higher-contingency and interestreserve allowances.

As a result, “credit appetite remains constrained”, says Bannister. He calls it a “bifurcation” of the market. While presale requirements remain tight at the majors, non-banks like La Trobe Financial “are taking a more pragmatic approach, assessing the entirety of the project, including sponsor strength, asset quality and exit strategy, rather than relying solely on pre-funding commitments”.

Lyall is seeing lenders require larger contingencies and more rigorous quantity surveyor oversight “to ensure projects remain viable if costs shift during construction”.

On the bright side, construction costs appear to be stabilising (although the ripple

on gearing levels and the lender’s confidence in the developer’s ability to meet key milestones throughout the loan term,” he adds.

“The determining factor is rarely the asset class itself, but rather how the project aligns with a lender’s specific credit parameters,” explains Munn.

“Lenders ultimately assess a range of factors, including feasibility, market demand, sponsor capability, construction risk, exit strategy and other factors. However, each lender weighs those factors differently and has its own internal requirements around leverage, presales and project structure.”

A warning to the curious

While diversification is all the rage in the broking space, development finance is not somewhere to tread lightly. The skill set required is vastly different from the residen-

“Development finance is inherently complex and significantly more involved than traditional lending … a number of issues can arise if these complexities are not managed carefully”

James Munn, Chifley Securities

Residential projects, such as townhouses, apartments and land subdivisions, “remain the most attractive from a financing perspective”, says Arnold. “This is largely driven by Australia’s significant housing undersupply, strong population growth and sustained demand.”

Lenders are also showing greater flexibility around presale requirements for projects in metro or high-demand locations. According to Arnold, this is most evident in stronger segments such as residential build-to-sell and industrial.

“That flexibility is still highly dependent

tial property space, involving knotty issues like feasibility assessments, construction risk, capital structuring and arcane lender credit parameters.

“Development finance is inherently complex and significantly more involved than traditional lending,” says Munn. “In our experience, a number of issues can arise if these complexities are not managed carefully.”

Munn has seen situations where builders needed to be replaced mid-project, construction contracts including variations were not reflected in the original feasibility, and developers faced delays due to labour or trade

shortages. He says, “Projects can also stall when lender requirements are not fully understood or key information is provided late in the process. In other cases, previously undisclosed liabilities emerge during due diligence, or valuation and quantity surveyor reports come back materially di erent from early feasibility assumptions.”

Although the sector presents a great opportunity for broker diversification, “I strongly encourage brokers to invest in the right training and education before stepping into development finance,” says Arnold.

To those new to the sector, he suggests partnering with an experienced broker for the first few transactions or working closely with a specialist construction lender who can guide them through the process. “The right lender will collaborate with both the broker and the client to ensure a smoother process and help build confidence as you take on more complex deals.”

Bannister often sees brokers engaging their business development manager too late in the deal process. “Development finance rewards early structuring,” he says. “Not all lenders assess risk the same way, and selecting the wrong partner can materially impact execution. It’s for this reason that all La Trobe Financial BDMs are trained in development finance, meaning brokers spend less time chasing answers and more time structuring a submission.”

• Traditional banks taking on lower-risk projects

• Non-bank lenders o ering flexibility for non-standard projects

• Private credit taking on more complex, higher-risk projects

“I strongly encourage brokers to invest in the right training and education before stepping into development finance”

Jason Arnold, Pallas Capital

Lyall agrees that the complexity of development finance is not always understood, although he believes it can be a valuable diversification strategy for brokers who want to expand beyond traditional residential lending.

However, Lyall stresses the importance of approaching the sector with the right level of education and support. He advises partnering with experienced development finance specialists or capital advisers who can help brokers understand deal structuring and lender expectations.

“For brokers starting out, the best way to find opportunities is by building relationships with property developers, builders, planners and commercial agents within their network,” says Lyall.

While there is no precise data to estimate broker share of Australia’s development finance market, it’s undeniably a nascent space with ample room to grow as developers increasingly recognise the value that brokers bring to the table.

“Broker market share of development finance is very unclear,” says Bannister. “What is clear, however, is the increasing number of brokers becoming active in the space. As market conditions remain somewhat uncertain, developers are increasingly turning to brokers for access, structuring expertise and lender navigation. That trend is only likely to accelerate as projectspecific complexity increases.”

Lyall agrees. “With Australia’s housing requirements over the next five years, brokers have the opportunity to play a much larger role in facilitating funding for developers,” he says. “As the lending landscape becomes more fragmented, I expect broker participation in development finance will continue to increase.”

Arnold explains that brokers are most active in the mid-market development finance segment, handling deals between $5 million and $50 million. He estimates that that broker share of the bandwidth now sits somewhere between 50% and 60%, although it could increase to 70% over time.

After a brief rebound, asset and equipment finance faces geopolitical shocks, shifting credit appetites and rising demand for speed and flexibility

SOMETIMES WHEN things are looking up, a dip in the road to recovery emerges to mess everything up again.

Take the current state of asset and equipment (A&E) finance. Following a rather drab 2025 potholed by high interest rates, weak consumer confidence and a slowdown in the construction sector, a turning point was up ahead. As a new year emerged on the horizon, volumes were trending higher and brokers were reporting a resurgence in enquiries. Then along came the little matter of the US-Iran war, and A&E finance is now facing the fact that recovery was merely fleeting after all.

If this were the stock market, an analyst might call it a dead cat bounce – a rather ugly term for a false recovery in a downwardly trending market.

At the turn of the year, Blake Buchanan, general manager of mortgage aggregator SFG, witnessed a momentary uptick in demand from SMEs that had delayed capital expenditure decisions in 2025. But “there’s now more caution in the market again due to international affairs”, he says. “Businesses considering reinvestment in productivity and efficiency, which is a strong leading indicator for A&E demand, will pause and reassess. Prior to this it has not been a sharp rebound, but a steady, more sustainable recovery was underway.”

Amid these choppy conditions, prominent A&E finance lenders are being strategic with their financing activities.

Resimac, for instance, has kept its settlement volumes on an even kilter. “In the first half of 2026, settlements were broadly in

“In 2026, brokers are expected to have a deeper understanding of industries, not just products. Speed still matters, but so does the ability to guide clients through increasingly complex credit and policy settings” Blake Buchanan, SFG

line with the first half of 2025, which was a deliberate decision by us,” Michael Stavroulakis, Resimac’s head of product, asset and equipment and SBLs, tells MPA. “We prioritised higher-quality deals over volume, and we targeted applications from more resilient sectors.”

In the current lending environment, Stavroulakis stresses the need to be clear on where Resimac stands, policy-wise. “We price strongly on well-documented deals, with quality assets and experienced borrowers. We’re not in the market for deals that need aggressive pricing, and while we focus on

portfolio performance, we’ll always support brokers and customers where the numbers stack up.”

Stavroulakis adds, “We seek the right business for the risk we take. This means refining our credit appetite for current conditions and keeping customer outcomes front of mind.”

Lenders are also having to accommodate greater demands for flexibility, particularly for SMEs with variable cash flow. Stavroulakis highlights the popularity of balloon payments, while he is also seeing a high volume of refinancing and consolidation requests.

continually invest in broker CRM direct lodgements to speed up efficiencies,” says Buchanan. Alternative lenders have become more prominent in the A&E space for the simple reason that their flexibility, faster credit processes and willingness to look at more complex or outside-policy deals “make them highly competitive”, Buchanan says.

He notes that the prime space remains the forte of the big banks and traditional lenders, “but their growth is more measured due to tighter policy settings and longer turnaround times”.

“Customers want choice and speed, and brokers play a critical role in advising on structure and lender choice to land the right solution” Michael Stavroulakis, Resimac

One of the biggest emerging trends – perhaps because no one really knows what tomorrow will bring these days – is the emphasis being placed on deal speed.

In A&E finance, where asset availability and business timing are critical, speed has become “a non-negotiable”, says Buchanan. This has led to significant investments into automation and credit decisioning among the lenders, he notes, “and we’re seeing strong improvements in turnaround times as a result”.

Resimac, says Stavroulakis, knows how critical speed is for A&E customers, “and that’s why we are investing in improving the broker and customer experience, making the credit assessment more efficient to meet that expectation. We know delays in financing can cost revenue or business contracts and can also reduce productivity. That’s why time to yes matters”.

However, performance isn’t exactly uniform across the market – and brokers are making their voices heard by favouring lenders that can marry speed with consistent settlement follow-through. “Lenders would do well to

If anything, the volatile nature of the business environment has thrown into contrast the increasingly important role brokers are playing in A&E finance.

“The relationship is becoming more advisory-led,” says Buchanan. “Clients are no longer just asking ‘can I get finance?’; they’re asking ‘what structure makes the most sense for my business?’ ”

Stavroulakis strikes a similar tone. “Brokers are increasingly acting as an adviser for their business customers,” he says. “Their deep understanding of a client’s business allows them to offer better guidance and seek out lenders who they can work closely with.”

Clear communication and timely feedback from a lender are essential, adds Stavroulakis, as they enable brokers “to present lending options that best suit their clients’ needs, with confidence”.

In 2026, brokers are expected to have a deeper understanding of industries, not just products, continues Buchanan. “Speed still matters, but so does the ability to guide clients through increasingly complex credit

and policy settings. The brokers who win will be those who can combine responsiveness with genuine commercial insight.”

Brokers are clearly up to the task, as their share of the A&E market goes from strength to strength.

“Broker share in the asset and equipment space is likely to keep increasing,” Stavroulakis predicts. “Customers want choice and speed, and brokers play a critical role in advising on structure and lender choice to land the right solution.”

While precise figures are not readily available, Buchanan estimates that brokers originate somewhere in the vicinity of 70% of new A&E volumes, and as brokers expand their capabilities, that share is trending higher. “The complexity of deals and the need for lender choice plays strongly into the broker value proposition,” he says.

It helps that diversification in the broking industry is a trend that’s only getting stronger. More brokers – particularly those with a residential lending background – are expanding into A&E finance to diversify their business revenue and deepen client

Australia Business Confidence Index (points)

relationships. Concurrently, more A&E brokers are diversifying their businesses into residential lending.

“Broker diversification is absolutely continuing, and in many ways it’s a positive development,” says Stavroulakis. “It expands market reach and brings more borrowers into the A&E space.” However, he stresses the importance of lenders educating brokers about the unique nuances of A&E finance, including deal structuring and credit expectations.

Diversification “is a positive for the industry overall, but it does raise the bar in terms of capability”, adds Buchanan. “A&E finance requires a di erent level of credit understanding and commercial awareness. Aggregators and lenders have a role to play

in supporting brokers with education, policy clarity and deal structuring guidance to ensure quality advice remains high as participation grows.”

A clear trend is emerging in the market: demand is being driven by incomegenerating assets, as both Stavroulakis and Buchanan have noted.

Commercial vehicles remain a standout, particularly in the logistics, trade and services sectors where utilisation is high. Electric and hybrid vehicle finance is also growing but from a smaller base, and it’s still influenced by cost and infrastructure considerations.

Demand is strong “where the asset is essential to day-to-day operations”, explains

Stavroulakis. Construction, maintenance and field equipment has shown early signs of improvement after a softer period, while commercial vehicles remain relatively resilient.

“Overall, clients are prioritising assets that either directly increase revenue or reduce operating costs,” says Buchanan.

As 2026 progresses, the road is likely to remain bumpy for A&E finance, but the journey will power on regardless.

“Broker and customer experience has become more important than ever,” says Stavroulakis. “Simply providing an approval is no longer enough to stand out. What truly di erentiates is clarity and speed in funding. While price remains a factor, it’s not the only consideration.”

placing

Brokers are writing fewer

and making

THE COMPLEXITY of commercial broking in Australia continues to rise, with greater choice of funding structures and higher borrower expectations. This has changed how performance is defined and what separates the Top Commercial Brokers from the rest.

MPA’s latest data reinforces a pattern that emerged last year and shows what now defines performance at the top end of the market. Median loan values have continued to rise –from $122.8 million in 2022 to $190.5 million in 2025 – pointing to a move towards larger

transactions. Top-end volume peaked in 2024 and remained elevated in 2025, with the leading broker settling more than $1.1 billion, well above volumes of earlier years.

Deal counts have declined, with the top broker writing 61 loans compared to 98 in 2024 and 130 in 2023. The spike of 547 loans in 2024 didn’t carry into 2025, with volumes returning to a more typical range. Across the four-year period, performance remained anchored to larger deal sizes rather than higher transaction counts.

At the firm level, Stamford Capital Australia stands out, with five individuals ranked among this year’s top performers.

“Funnily enough, we haven’t done much differently,” says managing director Peter O’Connor. “We’ve stayed true to our core values, invested in our team’s growth and development and fostered strong relationships with lender partners and clients. We’re proud that our top five brokers represent every Stamford office around the country and a mixture of positions in the business.”

La Trobe Financial congratulates MPA’s Top Commercial Brokers for 2026.

This year’s list recognises the industry’s highest-performing commercial brokers, professionals who consistently deliver strong outcomes for their clients and play a vital role in supporting Australian businesses and communities.

In a market defined by ongoing economic uncertainty, heightened credit selectivity and increasing regulatory and funding complexity, this year’s award recipients have demonstrated exceptional leadership, adaptability and execution. Their ability to cut through complexity, structure tailored solutions and deliver certainty when it matters most continues to set the benchmark for excellence across the commercial broking industry.

At La Trobe Financial, we believe that strong broker partnerships are