ASSUMPTIONS VS. REALITY: CONSIDERING INCOME RIDERS ANNUITY

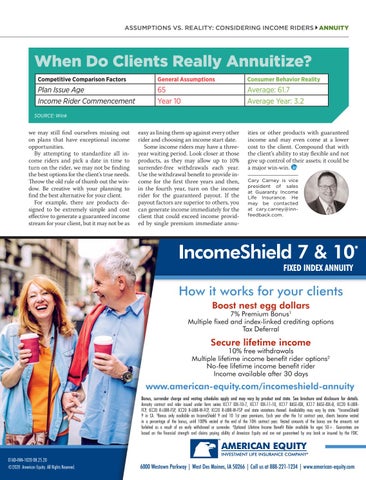

When Do Clients Really Annuitize? Competitive Comparison Factors

General Assumptions

Consumer Behavior Reality

Plan Issue Age Income Rider Commencement

65 Year 10

Average: 61.7 Average Year: 3.2

SOURCE: Wink

we may still find ourselves missing out on plans that have exceptional income opportunities. By attempting to standardize all income riders and pick a date in time to turn on the rider, we may not be finding the best options for the client’s true needs. Throw the old rule of thumb out the window. Be creative with your planning to find the best alternative for your client. For example, there are products designed to be extremely simple and cost effective to generate a guaranteed income stream for your client, but it may not be as

easy as lining them up against every other rider and choosing an income start date. Some income riders may have a threeyear waiting period. Look closer at those products, as they may allow up to 10% surrender-free withdrawals each year. Use the withdrawal benefit to provide income for the first three years and then, in the fourth year, turn on the income rider for the guaranteed payout. If the payout factors are superior to others, you can generate income immediately for the client that could exceed income provided by single premium immediate annu-

ities or other products with guaranteed income and may even come at a lower cost to the client. Compound that with the client’s ability to stay flexible and not give up control of their assets; it could be a major win-win. Cary Carney is vice president of sales at Guaranty Income Life Insurance. He may be contacted at cary.carney@innfeedback.com.

IncomeShield 7 & 10* FIXED INDEX ANNUITY

How it works for your clients Boost nest egg dollars

7% Premium Bonus1 Multiple fixed and index-linked crediting options Tax Deferral

Secure lifetime income

10% free withdrawals Multiple lifetime income benefit rider options2 No-fee lifetime income benefit rider Income available after 30 days

www.american-equity.com/incomeshield-annuity Bonus, surrender charge and vesting schedules apply and may vary by product and state. See brochure and disclosure for details. Annuity contract and rider issued under form series ICC17 IDX-10-7, ICC17 IDX-11-10, ICC17 BASE-IDX, ICC17 BASE-IDX-B, ICC20 R-LIBRFCP, ICC20 R-LIBR-FSP, ICC20 R-LIBR-W-FCP, ICC20 R-LIBR-W-FSP and state variations thereof. Availability may vary by state. *IncomeShield 9 in CA. 1Bonus only available on IncomeShield 9 and 10 1st year premiums. Each year after the 1st contract year, clients become vested in a percentage of the bonus, until 100% vested at the end of the 10th contract year. Vested amounts of the bonus are the amounts not forfeited as a result of an early withdrawal or surrender. 2Optional Lifetime Income Benefit Rider available for ages 50+. Guarantees are based on the financial strength and claims paying ability of American Equity and are not guaranteed by any bank or insured by the FDIC. TM

01AD-INN-1020 08.25.20 ©2020 American Equity. All Rights Reserved.

AMERICAN EQUITY INVESTMENT LIFE INSURANCE COMPANY®

2020 InsuranceNewsNet Magazine 39 6000 Westown Parkway | West Des Moines, IAOctober 50266 | Call us at» 888-221-1234 | www.american-equity.com