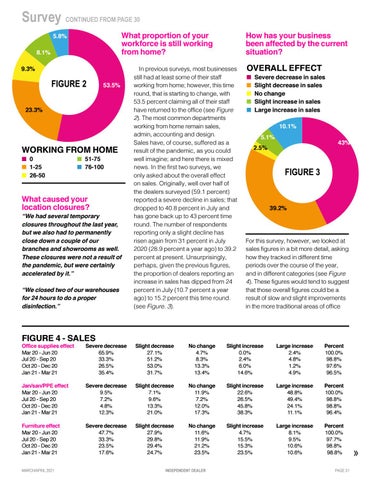

Survey CONTINUED FROM PAGE 30 What proportion of your workforce is still working from home?

5.8% 8.1% 9.3%

FIGURE 2

53.5%

23.3%

WORKING FROM HOME n 0 n 1-25 n 26-50

n 51-75 n 76-100

What caused your location closures?

“We had several temporary closures throughout the last year, FIGURE 5 but we also had to permanently close down a couple of our branches and showrooms as well. These closures were not a result of the pandemic, but were certainly accelerated by it.” “We closed two of our warehouses for 24 hours to do a proper disinfection.”

In previous surveys, most businesses still had at least some of their staff working from home; however, this time round, that is starting to change, with 53.5 percent claiming all of their staff have returned to the office (see Figure 2). The most common departments working from home remain sales, admin, accounting and design. Sales have, of course, suffered as a result of the pandemic, as you could well imagine; and here there is mixed news. In the first two surveys, we only asked about the overall effect on sales. Originally, well over half of the dealers surveyed (59.1 percent) reported a severe decline in sales; that dropped to 40.8 percent in July and has gone back up to 43 percent time round. The number of respondents reporting only a slight decline has risen again from 31 percent in July 2020 (28.9 percent a year ago) to 39.2 percent at present. Unsurprisingly, perhaps, given the previous figures, the proportion of dealers reporting an increase in sales has dipped from 24 percent in July (10.7 percent a year ago) to 15.2 percent this time round. (see Figure. 3).

FIGURE 4 - SALES

FIGURE 1

How has your business been affected by the current situation?

OVERALL EFFECT

n Severe decrease in sales n Slight decrease in sales n No change n Slight increase in sales n Large increase in sales 10.1% 5.1%

FIGURE 3

39.2%

For this survey, however, we looked at sales figures in a bit more detail, asking how they tracked in different time periods over the course of the year, and in different categories (see Figure 4). These figures would tend to suggest that those overall figures could be a result of slow and slight improvements in the more traditional areas of office

Office supplies effect Severe decrease Slight decrease No change Slight increase Mar 20 - Jun 20 65.9% 27.1% 4.7% 0.0% Jul 20 - Sep 20 33.3% 51.2% 8.3% 2.4% Oct 20 - Dec 20 26.5% 53.0% 13.3% 6.0% Jan 21 - Mar 21 35.4% 31.7% 13.4% 14.6% Jan/san/PPE effect Severe decrease Slight decrease No change Slight increase Mar 20 - Jun 20 9.5% 7.1% 11.9% 22.6% Jul 20 - Sep 20 7.2% 9.6% 7.2% 26.5% Oct 20 - Dec 20 4.8% 13.3% 12.0% 45.8% Jan 21 - Mar 21 12.3% 21.0% 17.3% 38.3% Furniture effect Severe decrease Slight decrease No change Slight increase Mar 20 - Jun 20 47.7% 27.9% 11.6% 4.7% Jul 20 - Sep 20 33.3% 29.8% 11.9% 15.5% Oct 20 - Dec 20 23.5% 29.4% 21.2% 15.3% Jan 21 - Mar 21 17.6% 24.7% 23.5% 23.5% MARCH/APRIL 2021

INDEPENDENT DEALER

43%

2.5%

Large increase 2.4% 4.8% 1.2% 4.9%

Percent 100.0% 98.8% 97.6% 96.5%

Large increase 48.8% 49.4% 24.1% 11.1%

Percent 100.0% 98.8% 98.8% 96.4%

Large increase 8.1% 9.5% 10.6% 10.6%

Percent 100.0% 97.7% 98.8% 98.8% PAGE 31

»