“Heritage makes it a lot easier to kind of pull (it) all together...They help get the deal done.”

- Colin McGrath, Lost River Fabrication

As we head into the heart of summer, I’m reminded of the incredible diversity and resilience of the businesses that fuel our communities. Whether you’re building a company from the ground up or exploring ways to evolve, this season offers fresh opportunities—and we’re here to support you every step of the way.

In this issue, we’re proud to highlight efforts to expand access and opportunity for diverse small business owners. At Heritage Bank, we believe that when everyone has a seat at the table, our entire economy grows stronger. You’ll find resources and stories aimed at breaking down barriers and building inclusive success.

We’re also taking a closer look at how emerging technologies—especially AIpowered customer service tools—are helping businesses work smarter. These innovations are transforming how we connect with customers, streamline operations and personalize service. Whether you’re new to AI or exploring your next upgrade, we hope these insights will spark new ideas.

Of course, summer also means vacation season. Our article on fraud prevention shares tips to help protect your finances while you travel. From phishing scams to card skimming, fraudsters are especially active during busy travel months. But, with a few precautions, you can keep your financial information safe and focus on making memories.

Finally, if you’re looking for a well-earned getaway, we’re sharing a few small Pacific Northwest waterfront towns worth visiting. These hidden gems offer charm, natural beauty and a reminder of what we’re all working so hard for—a life well lived, in and outside of business.

As always, thank you for reading Banking Business and for choosing us as your banking partner.

Sincerely,

Don't miss an issue!

Subscribe to the digital version of Banking Business at heritagebanknw.com/ bankingbusiness. We'll email you a link to read the latest issue when it publishes and highlight a few of our favorite articles.

Bryan McDonald President and CEO

Bryan McDonald is president and chief executive officer at Heritage Bank. Bryan joined Heritage Bank in 2014 as executive vice president, chief lending officer. He has more than 20 years of managerial experience in sales, credit, operations, commercial banking and residential real estate. At Whidbey Island Bank, he served as president and chief executive officer from 2012-2014. He currently serves on the board of the Washington Bankers Association.

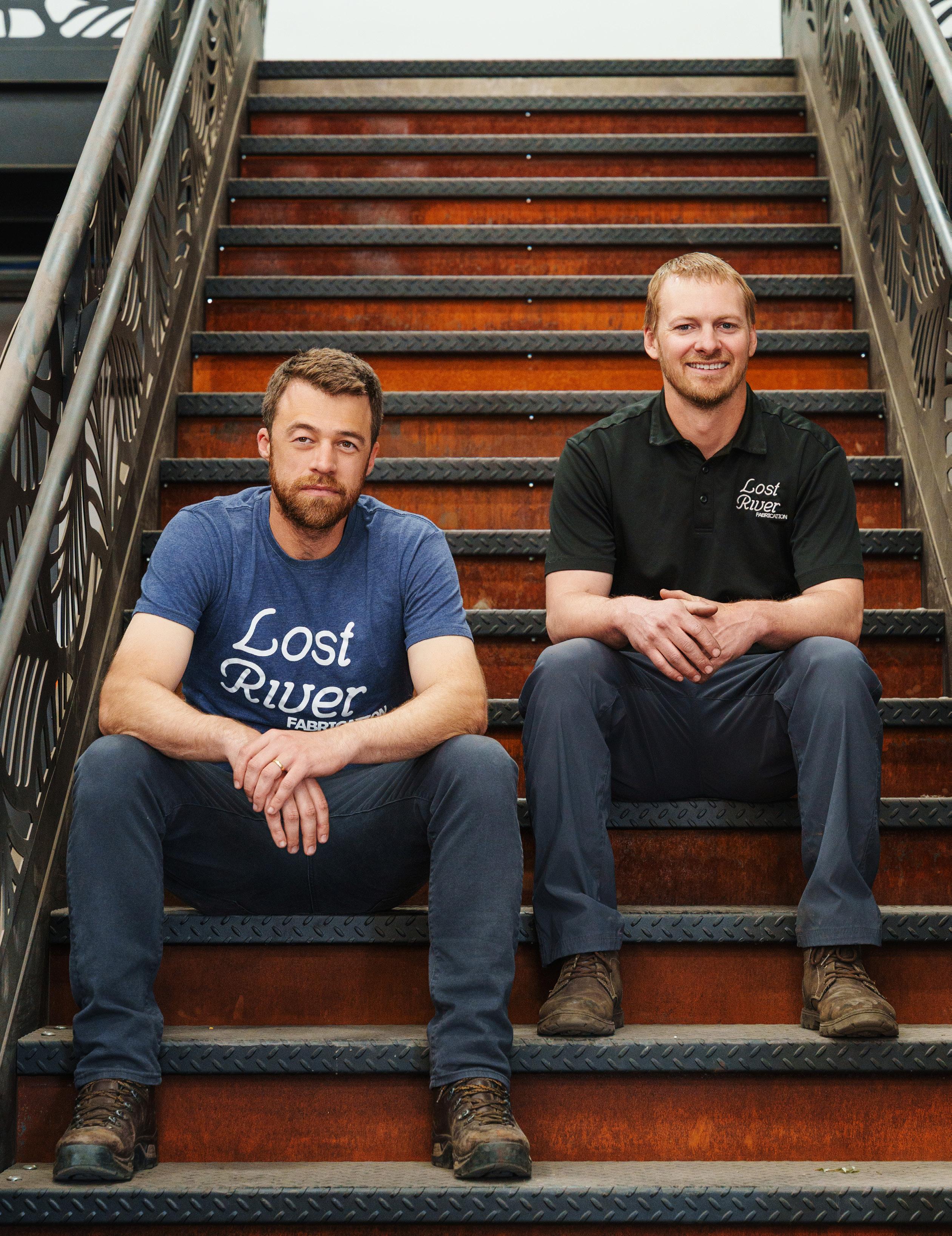

Colin McGrath (left) and Brandon Nicholls in one of the three buildings at their manufacturing facility in Caldwell, Idaho.

IDAHO PARTNERS demonstrate their metal

FOR MAKING CREATIVE AND FUNCTIONAL PRODUCTS

BY JOHN STEARNS

WWhen Brandon Nicholls invited Colin McGrath (a friend from their high school days in Boise, Idaho, more than a decade earlier) to help him buy his late father’s powder coating business in nearby Caldwell in 2016, it launched a partnership that expanded to include a new metal fabrication company whose work has won customers far and wide.

The two are 50/50 partners in Zamco Technologies, the powder coating business, and Lost River Fabrication, the metal shop they started in 2018. Between Lost River and Zamco, they can design and make almost any metal product and then paint and protectively seal it through powder coating, a process that involves curing the coatings in a large oven.

Each business complements the other but reaching that point first required McGrath and Nicholls to rejuvenate Zamco after purchasing it. The business, acquired by Nicholls’s father in 2002, had struggled following his tragic death in 2012 when the plane he was piloting crashed in bad weather. Nicholls ran the company for about nine months before moving on to use his engineering degree designing semi-truck trailers for a Boise company. His stepmother took Zamco’s reins, but the business struggled with debt. She told Nicholls she planned to close Zamco unless he wanted to buy it.

Nicholls and McGrath, who had stayed in touch during and after college, left their respective careers and went into business together.

“We basically created a good reputation with Zamco to the point where, once we could fabricate (through Lost River), a lot of our customers wanted to move their fabrication to us and be a one-stop shop where we make stuff for them, powder coat for them and they get completely finished products,” McGrath said.

In addition to business from Lost River, Zamco powder coats parts and products from many sources. That includes items needing refinishing, from rusty patio furniture to vehicle parts like fenders, wheels, truck beds, trailers and more. Zamco has the longest powder coating oven in the state, at 48 feet, according to Nicholls.

Lost River is equipped with CNC (computer numerical control) equipment that includes a tube laser, fiber lasers, water jet, router table and press brake; a robotic welder for high-volume projects; and 3D design automation. The equipment allows the company to fabricate diverse items, including business and monument signs, staircases, railings, trailers and smaller items like decorative wildlife, patterned garden stakes, planters, fire pits and toolboxes.

Anna Gorin Photography

A popular side business that emerged in 2020 from Lost River, called My Metal Rescue, produces metal silhouettes of multiple dog breeds, plus cats and other animals, and sends $5 from every sale to a different animal rescue organization each month. The program has generated monthly donations as high as $5,000, McGrath said.

Nicholls designs the animals, most of which are sold online through the company’s website.

The combined businesses now employ about 32 people in three adjacent buildings. Zamco had three employees when McGrath and Nicholls took over in 2016.

Creative problem-solvers

McGrath, who has college degrees in applied math and physics, and Nicholls, a licensed engineer, aren’t afraid to get their hands dirty and have tapped their inner ingenuity to solve problems that may seem difficult at first—from writing their own job-tracking software to learning how to replace and repair cutting elements on their high-tech tube laser.

“They can basically build and do things internally in the company that a lot of other CNC guys or fab shop owners

would have to outsource,” said Jeff Jones, who is the business’s commercial banking officer at Heritage Bank in Boise. “It’s pretty cool stuff.”

Added Jones, “They’re just of that generation where they immerse themselves in computers; they learned how to code, they learned how to write software, and it’s like they’re kind of the perfect match. And when you think of an average blue-collar business, you don’t necessarily think of some of the resources they’ve got at their disposal. They’re both just drivers; they work hard. They (also) do things like host lunch for their entire crew once a week; they bring lunch and they do safety meetings and sales meetings. They use that get-thecrew-together-for-lunch opportunity to brainstorm and just keep everyone moving in the right direction and focused on company goals and really trying to build that culture.”

Heritage financed the final construction and permanent financing on Lost River’s new building, a 35,800-square-foot structure whose construction had slowed after receiving a construction loan from a previous bank, Jones said, noting McGrath and Nicholls pushed the project along using their own funds. When their previous banker, Mike Trueba, whom McGrath and Nicholls enjoyed working with, joined Heritage to open its first Idaho office in 2023, the pair moved their business. That made them among the bank’s first commercial and industrial clients locally.

“We opened an account there and then they kind of helped us pull this building across the finish line,” McGrath said. The building opened in late 2023.

Heritage provided financing to pay off the previous bank’s construction loan and repay the partners’ out-of-pocket costs, Jones said. Heritage also financed a bridge crane inside the building that has a 10-ton capacity, plus financed a new

Lost River Fabrication and Zamco Technologies design and manufacture their own products as well as fabricate prototypes, parts and products for other businesses. Some of their recent projects include

CNC tube laser to expand Lost River’s capacity for projects requiring special cutting capabilities. Heritage also has all the business’s core operating accounts.

McGrath said the bank has been helpful throughout and easy to work with as needs arise.

“Heritage makes it a lot easier to kind of pull that all together; they’re pretty active and helpful in that process instead of always kicking things on your plate. They help get the deal done,” he said. “And they appear to have the flexibility, too. If something logically makes sense, they can figure out how to make it work on their end.”

Business on the rise

Lost River recently hitched itself to a nice piece of business making trailers for a Pacific Northwest company. The trailers, measuring 40 feet long and 10 feet wide, form the foundation for tiny homes that Lost River’s customer later builds atop the trailers as employee housing for workers at remote jobsites. Lost River builds the frame and adds the axles, wheels and lights.

“A lot of the growth is based on things our customers see that are missing in the market,” Nicholls said. “We’re pretty adaptive and light on our feet so we can transition to all these tiny home trailers that we’re building right now.”

The customer reached out to Lost River in December about making trailers “and 12 weeks later we’re building six trailers a week,” Nicholls said. “So, we have a bunch of customers like that who are happy to work with us because we’re super adaptive and kind of hop into whatever our customers are needing at the time.”

Zamco powder coats the trailers when they’re completed.

“We’ve stepped into a bunch of different areas, like doing the

My Metal Rescue, garden stake stuff, and then we do a bunch of vegetable garden stakes and planter boxes for some local (and national) landscapers,” Nicholls said.

Lost River also makes durable toolboxes, from standard ones it stocks to sell throughout the year to custom toolboxes for certain clients.

“We’re basically like a hybrid between a fabrication job shop where we have customers bring us whatever walks through the door, and then we try to make our own products also to try and add some stability to things,” McGrath said.

Added Nicholls, “We’re always happy to scale with whatever a customer needs. Whenever a customer comes in with an idea they want, we’re happy to work with them and figure out how to get that to volume or out the door, get designs, prototypes, that kind of stuff.”

Some customers are big but most are small, he said, adding that Lost River enjoys helping entrepreneurs produce products to compete with larger companies or foreign competitors.

“We can design it, we can be very hands on in the design process, and then we’re very vertically integrated. So, a customer can come to us with a design idea and then we can flip that around and get them a finished product very quickly and then ramp up and get them at scale,” Nicholls said.

They embody ingenuity, according to Jones.

HERITAGE BANKER: JEFF JONES

Jeff is an experienced commercial banking partner who collaborates with businesses to drive profitability and growth. With over 15 years of commercial banking and relationship management experience, he takes pride in providing hands-on, personalized service.

Greener Together: Recap of the Heritage Helps Ecochallenge

At Heritage, sustainability isn’t just a buzzword, it’s a shared commitment. This April, our team came together for our sixth Ecochallenge, a month-long initiative designed to inspire eco-friendly habits, encourage collaboration and spark creative solutions for a greener future.

Over 320 employees across all departments participated, forming small teams to tackle weekly sustainability goals. From reducing single-use plastics to lowering energy consumption in our offices, every action counted. Participants logged their efforts on an interactive platform, earning points for sustainable choices both at work and at home.

Some standout achievements:

• 75,728 gallons of water have been saved

• 25,783 pounds of CO2 have been saved

• 14,741 minutes spent learning

• 7,047 plastic items not sent to the landfill

• 1,667 miles not traveled by car

• 1,166 meatless or vegan meals consumed

The challenge wasn’t just about numbers—it was about

impact. “I absolutely love Ecochallenge! Every year, the challenges serve as a powerful reminder to be more mindful in my daily choices and to consider the environmental impact of everything I do during these three weeks. From my food choices to waste, water and electricity usage, I become more aware of how each action contributes to my personal footprint—and where small changes can lead to lasting impact,” comments Kristen Connor, senior vice presidentrelationship banking team leader.

The winning team, The Planet Professionals, went above and beyond, completing 8,283 actions. They volunteered; consumed organic, whole and zero-waste meals; and spent 1,370 hours learning about sustainability. One of the seven team members, Abigail Rickert, customer service associate senior, said, “I save the tops and stalks of my veggies and keep them frozen in a ziplock until the bag is full and then turn them into vegetable stock. Composting is another great way to reduce waste if you can’t use something in food.”

We appreciate each and every employee who participated and supported this initiative. Together, we’re proving that meaningful change starts from within—and that sustainability is a journey we’re proud to take, side by side.

Expanding in the Spokane, WA Market

We’re excited to announce the opening of our new commercial banking center in Spokane, Washington! The new team brings deep expertise and a commitment to helping local businesses grow and thrive. Their dedication to personalized service and strategic solutions strengthens our mission to support the region’s economic success.

Volunteer Day Closure

We’re excited to announce that the bank will once again close for a dedicated afternoon of giving back.

On Wednesday, September 10, employees will have the opportunity to volunteer their time and skills at local nonprofits and organizations throughout Washington, Oregon and Idaho. We will be actively engaging in various activities aimed at making a positive impact in our communities.

While our doors may be closed for a few hours, our commitment to serving you remains unwavering. We have taken all necessary measures to ensure minimal disruption to your banking experience during this time. We will have limited customer service staff available during this time to address any immediate banking needs, online and mobile banking services will continue to be available and our ATMs will remain fully operational.

All Heritage Bank locations will close at noon on Wednesday, September 10, 2025, and will remain closed for the remainder of the day. We will open at our regular time the following day.

Customers want to be able to pay a number of ways: in-store, online, or over the phone. This doesn’t need to be expensive or confusing. Elavon offers simple and cost-effective payment processing solutions for your business.

Benefits include:

Flexible payment options – accept all major credit and debit cards

Accept payments from digital wallets like Apple Pay ® and Google Pay™

Loyalty and Gift Card programs that help you market, grow and retain your business

Strategic solutions to partially or completely eliminate credit card acceptance costs1

Faster access to funds

Insightful, and feature-rich tools and reporting

Built to scale and grow with your business

Peace of mind with safety and security

24/7/365 Customer Service, including multilingual

will meet or beat your current payment processing rates, or we’ll give you a

01/02 – 12/31, 2025

1 Certain state or local laws may restrict or limit the amount of the surcharge percentage. Although we offer surcharging in most states, Merchants are responsible for determining the legality of surcharging in their states, and merchants are liable if their activities are found to be unlawful. Credit card surcharge applies to credit card

2 If Elavon is unable to meet or beat the merchant’s current processing rate(s), merchant will receive a $500 Visa® rewards card, limit one

merchant, regardless of the number of business locations. To qualify, merchant must show a minimum of annually in Visa ® and Mastercard® volume as supported by payment processing statements

cost). Elavon compatible processing software/equipment is required. Noncompliant surcharge and acceptance fee programs are not

at any time without notice. The Visa® rewards card value may be reportable as taxable income, please consult your

ACH vs. Wire Transfers

Choosing the Right

Payment

Method for Your Business

When it comes to moving money, businesses have more options than ever. Two of the most common electronic payment methods are ACH (Automated Clearing House) transfers and wire transfers. While both get funds from point A to point B, they differ in speed, cost, security and use cases. Understanding their pros and cons can help your business choose the right tool for each transaction.

What’s the difference?

• ACH transfers move money through the Automated Clearing House network, processing batches of transactions together. They’re commonly used for payroll, vendor payments and recurring billing.

• Wire transfers send funds directly from one bank to another in real time, usually within hours, and are typically used for large or urgent payments. Let’s break down the key pros and cons of each.

ACH TRANSFERS

The Pros:

• Lower cost: ACH payments can be inexpensive or free, depending on your financial institution.

• Automation-friendly: Ideal for recurring payments like payroll or vendor invoices, reducing manual work.

• Secure: Processed through a regulated network with fraud protections built in.

• Easy reconciliation: Since payments are electronic and predictable, they integrate well with accounting systems.

The Cons:

• Slower processing: ACH transfers can take 1-3 business days to settle, depending on your bank and their cutoff times.

• Limited international reach: ACH is primarily a domestic U.S. system; sending payments abroad requires other methods.

• Transaction limits: Some banks impose limits on the size or number of daily ACH payments.

WIRE TRANSFERS

The Pros:

• Speed: Domestic wires are usually processed same-day; international wires can arrive within 1-2 days.

• Certainty of funds: Wires are cleared immediately and can’t be reversed once sent, giving recipients confidence.

• Global capability: Wire transfers work internationally, with currency conversion available through banks.

The Cons:

• Higher cost: There can be a fee per transaction, depending on domestic vs. international transfers.

• Manual process: Wires often require manual entry or bank visits, making them less convenient for frequent payments.

• Less forgiving if errors occur: Since wires are irreversible once sent, incorrect details can delay or even cause loss of funds.

Which should you choose? The right choice depends on your priorities.

• For routine, non-urgent domestic payments (payroll, vendor invoices, customer refunds), ACH is costeffective and reliable.

• For large, time-sensitive or international payments, wire transfers offer speed and global access despite the higher cost.

Many businesses use both methods strategically, reserving wires for critical or one-time payments, while relying on ACH for everyday operations. Understanding these tools can help you streamline your payments, reduce costs and maintain smooth financial operations. Contact your Heritage banker to discuss the best mix of payment solutions for your business needs.

Expanding Opportunities for Diverse Small Business Owners

In recent years, the U.S. has expanded its support for diverse small business owners, helping new segments of entrepreneurs access essential resources. These programs create new opportunities for business owners who identify as LGBTQ+, minority-owned, Native American, rural or veteran-owned.

Each of these segments faces unique challenges, and by acknowledging their needs, the U.S. Small Business Administration (SBA) and related organizations are encouraging a more inclusive and diverse small business landscape.

Here’s a look at the latest initiatives and how they’re transforming these business communities.

LGBTQ+-owned businesses

This community has a growing presence in entrepreneurship, and the SBA and related organizations recognize the importance of inclusive resources and support. By fostering connections with other business owners, mentorship opportunities and certification programs, LGBTQ+ entrepreneurs can find a more equitable business environment. Some of their resources include:

• LGBTQ+-owned businesses can find support by using the SBA’s local assistance tool (sba.gov), which connects them to nearby offices that offer guidance on whether the 8(a) Business Development Program is the right fit.

• The National LGBT Chamber of Commerce offers certification, making LGBTQ+-owned businesses eligible for programs like mentorship, scholarships and other developmental resources after their first year.

• The SBA is dedicated to outreach initiatives, aiming to create a welcoming environment and acknowledge the importance of LGBTQ+ business owners at all community levels.

Through these resources, LGBTQ+-owned businesses are better equipped to build sustainable ventures while contributing to a more inclusive economy.

Native American-owned businesses

These are integral to many local economies, yet they often lack access to essential business resources. The SBA’s Office of Native American Affairs (ONAA) facilitates business growth by offering technical assistance, workshops and specialized tools.

• ONAA provides promotional materials, hosts national economic development events and offers access to resources tailored for Native American entrepreneurs.

• Various organizations, such as the National Center for American Indian Enterprise Development, help Native American entrepreneurs gain access to technical assistance on essential business operations like taxes, marketing and financial management.

• Collaborations with agencies, such as the Department of the Interior’s Bureau of Indian Affairs, offer additional educational and employment opportunities. With these resources, Native American-owned businesses can achieve greater economic empowerment, leading to sustainable growth in their communities.

Minority-owned businesses

These businesses often face barriers in accessing capital, training and networking opportunities. The SBA, alongside other federal agencies, is actively working to reduce these obstacles, offering programs specifically designed to empower minority entrepreneurs.

• The SBA collaborates with organizations like SCORE, small business development centers and women’s business centers to provide high-quality counseling and training for minority business owners.

• T.H.R.I.V.E. is an executive-level program that accelerates growth for small businesses in underserved cities, helping them create three-year strategic growth plans with specific targets.

• Designed for socially and economically disadvantaged businesses, the 8(a) Business Development Program offers set-aside and sole-source contracts and provides business opportunity specialists to help navigate the federal contracting landscape.

These programs are tailored to help minority-owned businesses overcome historic disparities, creating a stronger economic foundation for their communities.

Rural-owned businesses

Businesses in the rural sector play a critical role in local economies but often face unique challenges like limited access to capital and higher operational costs. The SBA and U.S. Department of Agriculture work closely to offer financing, export assistance and disaster recovery support to rural entrepreneurs.

• The SBA offers 7(a) and 504 loans for working capital, real estate purchases and business expansion. The 7(a) loan is a versatile option for rural businesses unable to secure traditional financing, while the 504 loan provides fixed-rate mortgage financing through certified development companies.

• Created under the Tax Cuts and Jobs Act of 2017, Opportunity Zones aim to bring capital investment into underserved communities, while the HUBZone program grants special access to federal contracts for businesses in underutilized areas.

• The Small Business Innovation Research (SBIR) and Small Business Technology Transfer (SBTT) programs provide funding for rural businesses engaged in research and development, fueling innovation in underserved areas.

These targeted programs not only enable rural businesses to grow but also ensure that they contribute to a stronger, more resilient rural economy.

Veteran-owned businesses

These businesses are recognized for their valuable contributions to the economy. The SBA offers specialized programs to support veteran entrepreneurs and help them navigate business challenges after military service.

continued on page 14

Heritage Bank has several programs that may also benefit your business.

The Washington State Small Business Credit Initiative was created to support small businesses and empower them to access the capital needed to invest in job-creating opportunities. A portion of the program funding is targeted towards very small businesses and businesses owned by socially and economically disadvantaged individuals—a population that often faces difficulties in obtaining the necessary funding to start or expand their business. (Read more about this program in our Q3 2024 issue.)

This program is exclusive to businesses and nonprofit organizations located in Washington state. It’s administered by the Washington State Department of Commerce in partnership with the U.S. Department of Treasury and financial institutions statewide.

The Heritage Bank Community Development Entity encourages business expansion in low-income communities by providing an attractive loan program with better rates and terms and more flexibility than a traditional loan. These investments help revitalize development by creating jobs and increasing the availability of goods and services in economically distressed areas. (Read more about this program in our Q4 2021 issue.)

Want to learn more about how Heritage can help? Visit our website at heritagebanknw.com to schedule a meeting with one of our experienced bankers.

Versatility and volunteerism Hallmarks of Heritage’s Yakima & Toppenish Lenders

BY JOHN STEARNS

Similar to the neighboring farmers who produce Central Washington’s bountiful crops, Laura Terrazas and the Yakima area commercial banking team work hard to sow success—from helping local businesses grow to strengthening community safety nets through nonprofit support.

“A lot of times, people are very defined on what type of lending they do, and we wear many hats around here,” said Terrazas, senior vice president-commercial banking team leader for Heritage Bank’s two Yakima branches in downtown, Union Gap and one in nearby Toppenish. “We can do any type of lending; any of us can do it,” including agriculture, commercial and industrial, owner-occupied real estate and nonprofits.

If the bankers don’t know the answer or how to underwrite a customer’s needs, they can tap experts elsewhere in Heritage’s tri-state network to help. The Yakima-

Heritage Bank’s Yakima commercial banking team, (left to right) Laura Terrazas, Steven Gustafson and Dawn Williams

Toppenish team is also cultivating more business in south-central Washington’s Tri-Cities: Kennewick, Pasco and Richland.

Terrazas’s commercial lending team knows the Central Washington region well, leveraging their years of experience living and working there. Terrazas and her six colleagues—Dawn Williams and Steven Gustafson, both vice presidents and commercial banking officers; Shanna Barnhart and Alex Richardson, credit analysts; and Irene Baker and Susana Maria, loan production assistants—have a combined 110 years in banking, with 78 of those years at Heritage or Central Valley Bank, which was a division of Heritage starting in 1999 before its merger with Heritage was completed in 2013. Each team member averages 11 years with the bank. Baker leads the pack with 27 years in-house.

“I think that says a lot about the bank itself and how it treats its employees and that we’re happy here,” Terrazas said of the team’s tenure at Heritage.

The Yakima-Toppenish offices include another 18 people, counting those in the three nearby branches.

Terrazas, Williams and Gustafson were each working on a nonprofit loan in late March when this story was written.

One was bridge financing for the YWCA of Yakima, which has been serving the community since 1909 and assisted more than 14,000 people last year. With YWCA’s current facility at capacity, it turned away more than 1,000 families last year. It will convert the former St. Elizabeth’s School of Nursing building into an emergency shelter with an additional 41 bedrooms and 112 beds, including a separate men’s suite of eight beds. Through grants and a capital campaign, YWCA had raised more than 85% of the project’s costs as of early April. Heritage will provide bridge financing for the balance of costs.

Another is a loan for a larger and centralized commercial kitchen in Yakima for People for People to consolidate meal preparation and distribution for the Meals on Wheels program for seniors, as well as provide onsite dining and socialization for seniors. People for People, which cooks more than 178,000 meals annually, now makes the food at three community centers. As with the YWCA, the loan will bridge whatever is needed to finance the kitchen beyond grants and fundraising. People for People had raised 70% toward its $2.79 million goal as of April 5, according to its website.

The bank has also provided a couple bridge loans recently for the Toppenish School District to cover solar power and lighting projects until the district receives state grant funding for the work, a type of specialized lending the bank has been expanding.

On the business front, Gustafson recently booked a flooring line of credit for a used car dealership that previously used another bank before transitioning to Heritage. Flooring lines are used by auto dealers to buy vehicles at auction, for example, with the credit line paid off as the vehicles are sold. The dealer, happy with Heritage’s service, moved its entire banking relationship, Terrazas said.

“As you can tell, we pride ourselves in relationship banking and knowing and being in our community,” she said in an email.

Banking officers’ specialties

Terrazas, who grew up in Toppenish and has lived in the area on and off the last 30 years, has spent her entire career in banking—25 years, the last 15 with Heritage. Her expertise includes agricultural lending, from tree fruit in Chelan, row crops in the TriCities, to tree fruit, row crops and hops in Yakima, plus other areas of business and nonprofit lending. Her community involvement has included serving on the boards of United Way of Central Washington, United Way of Central Washington Foundation, Yakima County Development Association and the Capitol Theatre.

continued on page 14

BUSINESS IN YAKIMA BY THE NUMBERS

Major industries: agriculture, forestry, fishing and hunting; government; health care and social assistance; retail; manufacturing

Labor supply: 118,088 workers

Yakima is the second largest county in Washington state at 2.75 million acres.

Yakima County Development Association has created 5,750 new jobs at over 150 businesses and facilitated $490 million in investments in Yakima County businesses esd.wa.gov/jobs-and-training/labor-marketinformation/reports-and-research/labor-market-countyprofiles/yakima-county-profile chooseyakimavalley.com/

ABOUT

COMMERCIAL

Versatility and Volunteerism, continued from page 13

Williams has 24 years in banking, with 12 at Heritage. Her expertise includes agricultural lending, and she’s passionate about small-business lending. She loves helping small businesses get to the next level and achieve their dreams, according to Terrazas. Williams also works a lot with businesses in trucking and transportation. Williams’s community involvement includes serving on the YWCA board and being part of Soroptimist International for 22 years.

Gustafson has 12 years in banking, two at Heritage. His expertise is commercial and industrial as well as commercial real estate lending. His community involvement includes membership in the Yakima Downtown Rotary, executive board member for Yakima Valley Tourism and vice president of the Selah National Little League board.

The team’s three branches also volunteered at three sites during the bankwide Volunteer Day last September, with one branch helping a local school district in its food pantry, another assisting in clearing a home damaged by a fire that swept through the Yakima Nation Reservation and a third helping at the YWCA.

“We all have pride in the community that we live in and we all want the best for it,” Terrazas said, noting Heritage was quick to respond to YWCA’s lending query when it was seeking financing. “And even with the (YWCA) domestic violence shelter, it’s something that you hope that you never need, but the need is there for this community and the bank is willing to go ahead and support it.”

It’s about relationship banking, being accessible and listening to clients’ stories, she said.

Terrazas added, “Most of our business comes from us being involved or referrals—and truly we strive for that excellence in banking.”

• Veteran business owners can explore several loan programs through the SBA to find the best fit for their financing needs. The Military Reservist Economic Injury Disaster Loan Program, for example, helps veterans with financial losses when employees are called to active duty.

• SBA’s Veterans Business Outreach Center provides one-on-one mentorship, helping veteran entrepreneurs refine their business plans, understand government contracting and access capital.

• The Veteran-Owned Small Business Certification is essential for veteran businesses seeking government contracts, offering streamlined access to opportunities designated specifically for veteran-owned enterprises. By taking advantage of these resources, veterans can leverage their unique skills and experiences to build thriving businesses.

Next steps

• Determine whether your business qualifies for certifications such as the LGBTQ+owned, HUBZone or veteran-owned certifications to access exclusive contracts and resources.

• Utilize SCORE, small business development centers or veterans business outreach centers to gain specialized training and counseling tailored to your business’s needs.

• Look into SBA loans, grants or the SBIR/STTR programs to secure the capital needed for business expansion, research or disaster recovery.

• Many programs provide mentorships or workshops that offer guidance on growth strategies and navigating federal contracts.

The expanded resources for LGBTQ+, minority, Native American, rural and veteranowned businesses reflect a shift towards a more inclusive entrepreneurial landscape. By recognizing the distinct needs of these segments and providing targeted support, the SBA and other agencies are empowering these business owners to build sustainable, competitive enterprises. As more entrepreneurs explore these resources, they’ll find new avenues to achieve business growth, create jobs and contribute meaningfully to their communities.

Photos: Shutterstock

Harnessing AI-Powered Customer Service Tools

Now more than ever, artificial intelligence (AI) is transforming customer service, enabling small businesses to provide timely, consistent and efficient support.

AI-powered tools allow businesses to bridge the gap between customer expectations and available resources, so that even with a small team, inquiries are handled effectively.

Let’s look at how integrating these tools into daily operations can improve customer satisfaction, reduce response times and optimize your team.

The role of AI in customer support

One of the biggest challenges for small businesses is maintaining high-quality customer service outside of regular business hours. Customers today expect instant responses, and delays in addressing their concerns can lead to lost sales or negative experiences. AI chatbots and virtual assistants provide 24/7 support, answering common inquiries about store hours, product availability and shipping details without requiring human intervention. This allows businesses to be more responsive, improving customer engagement while freeing up employees for more complex issues.

Beyond handling after-hours support, intelligent tools are particularly beneficial in high-traffic environments

where customer inquiries about order statuses, returns or appointment changes can overwhelm staff. By automating routine interactions, you can manage high inquiry volumes more effectively so that customer concerns are addressed without straining human resources.

Improving consistency and reliability

Consistency is important in customer interactions, but humans may inadvertently provide varied responses to similar queries. AI-powered tools eliminate this issue by delivering standardized, accurate answers every time. This consistency helps build trust in the business and reduces customer frustration caused by conflicting information. Businesses that implement these customer service tools make sure that customers always receive the right information, whether they reach out via:

• Website chatbots that provide instant, pre-programmed responses.

• Email automation systems for uniform and timely replies.

• Social media messaging tools that maintain consistency across different platforms.

For businesses that experience seasonal demand spikes, intelligent tools are invaluable. Instead of hiring temporary staff or overloading existing employees, AI can scale up support during peak periods, such as holiday sales or promotional campaigns. Chatbots can efficiently manage increased inquiries, helping businesses maintain a high level of customer service without increasing labor costs.

Personalization and AI-driven customer insights

AI doesn’t just provide generic responses. It can be trained to understand customer preferences, past purchases and browsing history. When you integrate intelligent tools with customer relationship management (CRM) systems, you can offer personalized recommendations, address concerns based on previous interactions and improve the overall user experience.

When you integrate intelligent tools with customer relationship management (CRM) systems, you can offer personalized recommendations, address concerns based on previous interactions and improve the overall user experience.

Vecteezy

Consider this:

• Chatbots on eCommerce sites can suggest related products based on a customer’s past purchases or browsing behavior.

• Service-based businesses can use AI to remind customers of upcoming appointments or offer personalized promotions.

• Intelligent personalization improves customer satisfaction and strengthens brand loyalty.

• Personalized recommendations can drive revenue by encouraging repeat business.

This level of personalization means that customers feel valued and understood, making them more likely to return for future purchases or services.

Implementing AI-powered customer service tools

Here’s how to offload these routine queries to AI so that your staff can focus on more complex issues that require human intervention:

• Identify repetitive customer inquiries, such as returns, cancellations, delivery options and store policies, to determine the best areas for automation.

• Integrate chatbots into websites, social media platforms and messaging apps like Facebook Messenger for instant responses and the handling of thousands of inquiries simultaneously.

• Train AI systems using past customer interactions to improve accuracy and context-awareness, making sure they provide relevant and helpful responses.

• Make sure AI customer service tools integrate with existing CRM systems to maintain a seamless customer experience by tracking past interactions and tailoring future responses accordingly.

Bring intelligent tools on board and you’ll improve efficiency and response times as well as provide a more personalized customer experience without overburdening your staff.

Balancing human and AI interaction

While intelligent customer service tools provide immense benefits, they should complement, not replace, human interaction. The key to a successful strategy is striking the right balance (i.e. allowing AI to handle first-level support while reserving human expertise for more complex inquiries).

For example, a chatbot can manage common questions, but customers should have the option to escalate issues to a live agent when needed. Intelligent tools can also assist human representatives by pulling up relevant customer information, enabling faster and more informed responses.

The idea is to combine AI efficiency with human empathy so you can create a customer service experience that is both responsive and personable.

Monitoring and optimizing AI performance

Intelligent tools require regular evaluation and refinement to maximize their effectiveness. That means you should actively review customer feedback to identify pain points and areas for improvement. If customers report frustrations, such as a chatbot misunderstanding their questions, adjustments should be made to refine the system’s capabilities.

Additionally, it’s highly useful to analyze AI-generated insights to refine your customer service strategy. These tools can track customer sentiment, identify frequently asked questions and highlight service gaps. These insights will help you make datadriven improvements to your customer service approach.

Next steps

• Identify repetitive customer inquiries and automate them with chatbots.

• Leverage customer relationship management tools to offer personalized recommendations and provide a smooth experience across multiple platforms.

• Regularly review customer feedback, AI-generated insights and performance data to continuously improve the effectiveness and accuracy of your intelligent tools.

• Balance human and AI interaction by allowing customers to escalate issues to live agents when necessary.

Intelligent tools provide instant, consistent and scalable support. They will help your business to improve customer satisfaction, reduce operational burdens and realize efficiency gains. When implemented thoughtfully, AI-driven tools can help your business meet growing customer expectations without the need for large support teams.

Vecteezy

Regardless of what you learn, it’s still healthy to have a conversation with your parents about their own experiences and finances.

SETTING YOUR FAMILY’S FINANCIAL VALUES

Without knowing it, you may be part of the so-called “sandwich generation.” These are people who find themselves at the life stage in which they are caught between raising their own kids while watching their parents grow older. They are squeezed between responsibilities to care for parents and children at the same time. This care can take the form of money and capital or time and labor. All of these can have serious financial implications.

Add to this the fact that kids are staying at home longer, and people are living longer. This is the reality of many modern families. If it’s the reality for your family, it means the possibility of greater financial burdens for you, going forward.

But this reality doesn’t mean you should fear the future. You can set your own standards and determine your own future. You can discuss real issues with those who count. With the proper guidance, you can take action, and you can cast a strong vision for your children. Let’s explore how.

Determine your financial values

It’s never too late to take hold of your financial life and desired future, but the sooner you start, the better. While it’s true that some people get off to an earlier, stronger start, with greater resources and success than others, the truth is that everyone can do something. And the first—and perhaps most influential— thing you can do is determine your own financial values.

So, what are financial values and why are they important? Think of it like this.

What is most important to you when it comes to your family’s finances? Is it to feel secure against risk and free from anxiety? Is it simplicity and independence? What about the freedom to do what you want? Or do you desire the ability to be generous? Examples of financial values such as these show what is important to you—what is foremost in your thinking and decision-making processes. Once you are open and honest about them, these values will help shape your financial vision, goals, strategies and behaviors.

Cast a vision for your family

Will your kids attend college? If so, will they or you be able to afford it? Will your parents need long-term and end-of-life care? Have they made a will and plans for their estate? What about your own pension plans and retirement? How long will you need to keep working? These questions require you to formulate detailed answers and make proactive choices. You’ve already thought about why financial values are important and what yours include. Now, you need to determine an overall vision for how you want to approach spending, debt, savings, and investments in your family. That means acquiring knowledge and information from trusted sources, such as your parents, for instance.

Gather knowledge from your parents

As your parents get older, it can be a useful exercise to reflect on their financial values as they are likely to have influenced yours. You will probably uncover a mixture of values—some of which are worth adopting and others that you might want to avoid or adapt to your circumstances. For example, let’s say your parents held strong values against accumulating debt and engaging in what they considered as wasteful spending. They only spent what they needed to and saved any extra in a regular savings account. However, they showed little interest in investing their money, making long-term financial plans or using a financial advisor to help plan and maximize any money they saved. So, while they have little to no debt, they may not be as prepared financially for their retirement years as they would have liked, and the house they live in is likely their only substantial asset. Regardless of what you learn, it’s still healthy to have a conversation with your parents about their own experiences and finances. After all, the decisions they have made—and will make—might impact you. For example, if your parents have property or other investments, you might be expecting a significant inheritance. But you need to be realistic as to how much you might actually receive, given their continued expenses, spending and withdrawal strategy in their retirement years.

Connect with a financial professional

When you have medical questions, you talk with your doctor or medical specialist. When your car needs maintenance or repairs, you probably go to your trusted mechanic. It’s wise— and can even be comforting—to connect with and seek the help of professionals. When it comes to your financial health

and questions, leverage the expertise of financial advisors such as your banker and wealth manager.

Getting professional financial advice is not just for high-networth individuals. We all face real-world pressures at every income level, and we all deserve to get personalized advice and tailored family financial strategies. The trusted advice you can garner from an ongoing relationship with a financial professional means you can explore in an informed way exactly where you are right now. Then, together, you can build a realistic vision and strategic plan for where you want to be.

Perhaps now more than ever, it’s important that to discuss your financial future and form a strategy that works for you. The more you discuss your options and prepare, the more confident you can feel about the future. When you work together with your financial advisor on an ongoing basis, you can also modify your financial strategy as your circumstances change and you move through various life stages.

Help is at hand. All you need to do is reach out. Coincidentally, that’s a lesson we can learn from our children.

Share age-appropriate values with your kids

Just as you likely learned some lessons—good or bad—from watching your parents interact with money and tackle financial issues, your own kids will learn from you. Make sure the lessons they learn are good ones that help them form healthy financial habits and a healthy relationship with money. Avoid associating any financial discussions with pressure, negative emotions or unproductive habits.

Even young kids can learn lessons about money that are positive, age-appropriate and success-forming. For instance, at an age-appropriate level, you could explain to them the different types of bank accounts and their purposes, the value of saving for what you want, the need to think longer-term or why it makes sense to ask someone you trust for financial advice. By doing this, you can begin to pass on your values regarding financial responsibility and family leadership, even to young children. Building these strong, healthy financial values now should be a big help to them in later years as they follow in your footsteps or even as they forge new paths. This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or

2170, Portland, OR 97205, (888) 360-0052. Even young kids can learn lessons about money that are positive, age-appropriate and success-forming.

INDUSTRY PROFILE: Retail

Retail has been under threat for some time with the growth of online shopping, second hand or “vintage” stores, online marketplaces like eBay and the threat of offshore competition (Amazon, Temu, etc.).

The impact of the pandemic sped up the downfall of several retailers who either didn’t have the capital reserves to survive lockdown or where demand fell significantly (such as in tourism). This also accelerated consumer behavior to buy online, diverting traffic and revenue.

The decline in our economy over the last few years has shortened what was supposed to inevitably occur in the long term, which was a shift to online purchasing, online payments and trusting the supply chain to get what you need, when you need it. Though supply chains were brittle initially, deliveries of products around the U.S. are largely back to normal levels (with some delays from offshore still).

The positive is that retail development has continued, shopping malls are being renovated and new housing has created the need for retail infrastructure. New business models, such as drop shipping (where the retailer doesn’t need to hold the inventory), are enabling retailers to offer wider selections online without holding the product.

Success Characteristics

For retailers to succeed it’s important they adapt to today’s highly fluid social, economic and health environments. While some retailers are seeing demand fall away and customers shift channels, others are facing unprecedented spikes in demand (such as grocery retailers).

Retailers must also have a plan that ensures the safety of their employees while maintaining business as usual activities and talk to their key suppliers to assess any risks of being unable to supply. Successful retailers will refocus on the customer relationship and loyalty to their brand, people and community in order to stay relevant.

Other success criteria include:

• Strong online presence to complement the physical store

• Building credibility and excellent customer service

• Customer loyalty programs and reasons for customers to return

• Placing resources into positive online reviews and social media

• Maximizing the number of customers through the door each day and their average spend

• For physical stores, being in high foot traffic locations or having a high marketing budget to drive traffic

• Addressing a real unmet need by adding value and creating customer loyalty

• Continue asking customers what they like and dislike

• Depending on the product and market, strong unique selling points like “Made in the U.S.A.” or “eco-friendly”

• Competing on something other than just price, as large chains and online stores will always win a price war

Challenges

A key challenge has been the disrupted supply of imported products (which many retailers rely on), the increased cost in shipping (often health and safety compliance) and the increase in purchase price (due to lower numbers of items being produced).

Other challenges include:

• Integrating the physical and online presence to give the consumer a seamless brand experience, while juggling the increased price pressure (as consumers can almost always find an item cheaper online)

• Larger retailers leveraging their buying power to maximize economies of scale, which smaller owneroperators find hard to match

• The staffing, stock management and cash flow implications of seasonality where there are huge fluctuations in demand

The National Retail Federation nrf.com

U.S. Department of Commerce commerce.gov

U.S. Small Business Administration sba.gov

• Managing cash flow to avoid overtrading or overstocking at peak times to prevent holding obsolete inventory

• Working closely with suppliers to ensure they can maintain optimal stock levels and be able to order in time

• The increase in online shopping and online share of wallet

Retail Trends

Consumers are shifting their behavior to online shopping and no longer distinguish between online and offline shopping. Older demographics are becoming savvier and are purchasing goods online. Private labels are growing, and more artificial intelligence is being integrated into the retail experience. This includes the development of a C2M (customer to manufacturing) business model, where companies use big data and AI insight to personalize the products for the individual consumer.

Seasonality

Retail experiences the highs and lows of the business cycle often dictated by holidays, events and seasons. Christmas has traditionally been the highest, but other events such as Black Friday see spikes of activity across the year. Seasonality also makes it difficult to plan staff levels, with retailers often requiring part-time staff to fill in the gaps.

Impact of offshore retailers

Larger retailers (H&M, Zara, Ikea) have worldwide appeal and resources to impact local retailers, though we’ve seen some of these retailers struggle. Shoppers prioritize exceptional customer experience, and they’re willing to provide their data to companies but expect a higher quality experience in return. For local retailers and their brands, this means delivering the same promise from overseas companies of personalization, expert service, always-available inventory and seamless cross-channel shopping.

Rise of online behavior

One of the most obvious trends is the impact of online shopping and researching product features online. At times shoppers may know more about a product being sold than the retail staff and will most likely have compared prices. Online is the biggest threat and opportunity for retailers. The option to buy online and pick up in-store will continue to bridge the gap between online and offline retailing.

Sensitivity to wider economic conditions

Retail is one of the more sensitive industry sectors. Sales are driven by consumer sentiment, interest rates, employment levels and disposable income. Often retail is the first sector to feel an immediate effect of concern—from a falling U.S. dollar (retail imported products are more expensive) to lower-thanexpected agricultural prices (farmers have less to spend)

to any general unease over the decision to spend or save disposable income in the event of an economic downturn.

High percentage of owner-operators

Retail has a very high proportion of self-employed owners who provide small, individualized store experiences, especially in smaller population areas that can’t sustain larger stores. This is increasingly under threat as owner-operators find it difficult to compete on price against the big box competitors and wider product choices online.

Technology is a key driver

The store of the future will be heavily influenced by technology with in-store navigation capabilities. More shoppers will pay for items via their smartphones and then linking them to automatic loyalty programs (which signals the end of points based or physical loyalty cards).

Other technology trends include:

• Promotions will be triggered by a shopper’s physical presence, personalized and tailored to them

• Shelf tags will have ratings that change as shoppers review and purchase as well as usage suggestions derived from social media groups providing product information at the store

• Packaging will actively show products in use or communicate directly to smart devices

Retailers will sell experiences not just products

By curating interactions, retailers can pull customers into delightful, memorable experiences that make much more of an emotional impact than buying a product. Stores will also increasingly have smaller footprints (to both lower the footprint cost, and to supplement with online shopping).

CONTRIBUTOR: BRETT WILLIS

Brett has been with Heritage Bank since 2016 and has been in banking for over 30 years. He has broad experience in commercial lending and business banking, with a focus on commercial and industrial (C&I) industries, commercial real estate, contractors, manufacturers, healthcare, nonprofits and distributors.

YOUR SUCCESSION TOOLKIT, PART 3

Valuing

This is the final article in a three-part series on succession planning. Find part one in our October 2024 issue and part two in the February 2025 issue.

S

Successfully exiting a business is a dream for many owners. A financially-sound exit is certainly achievable, but it requires a period of hard work and planning to get the best return. We’ve assembled critical actions you can take to increase the value of your business before you offer it for sale.

Create an operations manual

01 Document your processes

The purpose of an operations manual is to make sure a new owner can run your business without you.

The manual is an essential part of creating a transferable business—and that’s what buyers are willing to pay for. Include simple, day-to-day actions, how you create the culture of your organization and your process for making important decisions. Provide detailed instructions to make any product or deliver any service. Tell them how to make your “secret sauce”—the thing that sets your business apart from the competition.

The operations manual for a McDonald’s franchise instructs owners how to run every facet of the restaurant so there’s no guesswork. Standardizing operations worldwide allows the company to maintain its brand experience for customers.

02 Detail critical elements

While the new owner may perform some operations differently, you want to demonstrate how easy it will be for them to take over and enjoy the same profit. It’s not always the obvious aspects like doing the actual work, or promoting to keeping clients.

Cover how you:

• Pursue outstanding debts and ensure you’re paid on time

• Establish streamlined systems and processes that are frequently checked

• Make the most of technology

• Manage your workloads so that they’re effectively prioritized and delegated

• Identify necessary trainings and engage your employees

• Develop templates for everyday documents like invoices, contracts, statements of work and quotes

• Form alliances or partnerships Include:

• Hiring and firing policies

• Business operation checklists

• Vendor information, key people and their preferences

• The best ways of promoting the business and what works best

• Customer contact list: what they like, don’t like and personalities to be aware of

• Key competitors and how you beat them

03 Set up supplier agreements

If you have supplier agreements that are a good deal for your business, consider renewing those agreements and locking in preferred pricing and terms. A buyer will want to receive the same treatment from suppliers and be able to buy from suppliers at the same price. Locking in your supplier deals will add value to your business in the eyes of a buyer.

Prepare suppliers by letting them know your intention to sell the business, preferably after you have a buyer. If possible, introduce the new business owners to them.

Maintaining positive relationships with suppliers will benefit you in any future business endeavors and will help ensure your company's success when you are gone.

Groom your successor

01 Train and empower

The better you prepare them for their new role, the more successful the handover will be. How you go about it depends on who the new owner will be. For instance, if you’re handing the business over to family make sure they have a genuine desire to run the business and the necessary skills. You want to be sure they’re in it for the long haul.

If you’re selling to employees, whether it’s a favored manager, a group of employees or a set of shareholders, it’s important that everyone is aware early on of your intentions.

In either case, there are some critical steps you need to take to prepare the new owner:

• Let them watch you work. They need to learn as much as they can. Continually explain why you do things a certain way and how you make decisions.

• Dip their toes in by letting them make some decisions, with your guidance. Work together on key projects. Encourage and teach them.

• As they gain in confidence and ability, give them more decisions to make, with you as an advisor rather than guiding them. Let them make mistakes and show them how to fix them.

02 Hand over control

Give them total control. Encourage and empower them so that they are truly ready to run the business without you. This is one of the greatest challenges for most business owners.

As you’ll see, this process works best by gradually easing you out as they ease in. Handing over the reins in one fell swoop almost never works, as the new owner is left feeling overwhelmed and without the necessary skills, while you walk away from the business knowing you’ve left it in the control of someone who doesn’t know what they’re doing. It’s not the kind of legacy you want to leave behind.

03 Transfer assets

When you’re transferring your assets to the new owner, have them valued first by an expert so you can get an idea of what you’ll be paid for the business.

Put together a transition team who’ll help you transfer control. They should be people who are not emotionally involved, like your accountant, lawyer or business broker. Maintain open communication with your team and your successors.

Once the new owner has taken control, all decisions are theirs. And now it’s time to do the hardest part of all—walk away.

Plan your future

01 What will you do after the sale?

Although it can take years to build a business that’s ready to sell, things can move quickly when the time to exit finally arrives.

Create and follow a timetable to keep on top of everything. You don’t want to miss important meetings with advisors or potential buyers. Once a deal has been made, a good timetable will make sure the transfer of ownership benefits your employees, business, and yourself.

It will be easier to let go of your business if you're clear about what you're going to do next.

You could:

• Buy another business. The proceeds from the sale could be invested in a new business (if you’ve identified a better business model) or you might have found a competitor or supplier you’re interested in purchasing.

• Start another business. You may actually want to go back to the start and reinvent your business.

• Help other businesses by becoming an angel investor. You might have run across a promising new start-up you’re interested in helping get off the ground, especially if you think you’ll get a worthwhile return.

• Work part-time. You might have had your fill of being the boss, along with all the stress that goes with it, and are ready to work for someone else in a low-stress, low hours position in a business that’s always interested you.

• Volunteer. There might be charities you’ve previously donated to and now you’re ready to give them your time as well.

• Retire. This doesn’t mean sitting around in front of the TV. You could travel, take up a new hobby or get involved in the community.

• Go back to learning. You may have a degree you want to finish, or learn something that you’ve always wanted to, but never had the time. It’s never too late to continue your education.

continued next page

Your Succession Toolkit, Part 3, continued from previous page

Whatever your decision, the better prepared you are, the more successful you’ll be.

02 How much do you need to retire?

It’s a useful wake up call to find out if you are on track and how much longer you’ll need to work to retire in the lifestyle you’d like. If the business can be sold for a lump sum, will the investment returns provide enough income to support your expected lifestyle? If not then you’ll need to lower your income expectations, keep working and build more value in the business to sell for a higher price or keep some equity/shareholding in the business and rely on business dividends.

Retirement investment strategies to think about:

• A diversification plan based on your age and your future plans. Where to place your capital such as shares, bonds and cash.

• Passive income options, such as commercial or domestic real estate.

• If you’ve received a mix of cash and shares in the company that bought you out, check to see how you can realize any gains, such as the dividend policy.

• Reviewing what exposure you have to liability, especially if you’ve left money in the business that the new owner is paying back. If you’ve left significant assets in the business, make sure you retain the ownership until you receive full payment.

03 What is your savings strategy?

To hit the target, it’s crucial to be able to see it. Start your retirement planning process by answering these three questions:

• When do you want to retire?

• How much money do you think you’ll need to comfortably retire?

• What’s your retirement plan?

Once you have a fairly accurate idea of your retirement objectives, it’s time to consult experts to help develop a strategy. Aim to work closely with your financial advisor, banker, lawyer and accountant.

It's wise to revisit your plan every few years to make sure it's kept up to date. Meanwhile, your financial advisor will be the one actively monitoring your investments to provide you with frequent reports and suggestions.

05 Final tips for success

An exit strategy is something every business owner needs to prepare for the inevitable—the day you’ll transfer assets and control of your business to a family member, business partner, employee or outside buyer.

Many business owners put off succession planning for any number of reasons: they’re busy, they don’t like thinking about falling ill or dying or retirement seems a long way off. But failing to plan for your exit puts you and your business at significant risk.

Having a succession plan means that if life throws a curveball and you need to step away sooner than expected, you’ll have contingency plans in place. You’ll be grateful to have made the tough decisions and laid them out, step by step, for a smooth and successful transition.

Take action

Below are key decisions that you will want to consider as you create a succession plan. Getting clear about your motivations and taking the planning step-by-step will go a long way in ensuring a smooth and successful transition.

1. Detail your plans for leaving your business. Identify your priorities, your goals for the company and your desired payout terms.

2. Explore various scenarios for leaving your business, such as selling to children or employees. Which is ideal for you and why?

3. Identify the factors involved in the timing of leaving your business. When do you want to leave and why do you want to leave then?

4. Detail the steps you can take to increase the value of your business. Develop a strategy for doing so.

5. Outline and explain which method of valuing your business will work best for you.

6. Identify the steps you’ll take to ensure all processes are documented.

7. Write your plan for handing over control of the business to someone else, including a timeline.

8. List the people who could serve as advisors as you leave your business (for example, accountants, lawyers, etc).

9. Identify what you’d need to do to leave the business quickly in case of a sudden emergency.

10. How will you communicate openly and honestly with stakeholders and employees? When will you do so?

This summer, visit these Pacific Northwest SMALL WATERFRONT

TOWNS

SMALL WATERFRONT TOWNS

Wish you were here!

Get out of the city this summer and explore a few of the region’s quaint waterfront towns. You’ll experience local food and drinks, art and history, unique architecture and picturesque backdrops. Here are some PNW towns with populations under 2,000 to chill out and cool off when the temperatures rise.

Coupeville, WA Population 1,942

Settled in the 1850s, Coupeville is proud to be Washington’s secondoldest town. Located in Ebey’s Landing National Historic Reserve on the shores of Penn Cove (mussels anyone?), the famous red wharf on the waterfront is a great place to take in the view. Many buildings are more than 125 years old and feature shops, galleries and local eateries.

Winthrop, WA Population 578

The main street in Winthrop takes visitors back to when the west was won. Situated on the North Cascades Scenic Byway (WA SR 20), this photogenic mountain town boasts limitless outdoor recreation. Visit Pearrygin Lake State Park, one of Washington’s most popular state parks for all your summer activities. With a variety of year-round festivals, outdoor concerts, art shows and seasonal markets, visitors will always find something to do and see.

Long Beach, WA Population 1,688

One of Washington’s charming coastal towns, Long Beach is the selfproclaimed “World’s Longest Beach” with 28 miles of sandy beach. The beach is considered a Washington state highway with a speed limit of 25 mph and makes for a fun little road trip. There are not one, but two historic lighthouses nearby to visit, North Head and Cape Disappointment. Also find souvenir shops, local cafes, a robust art scene and saltwater taffy in almost any flavor you can imagine.

Rockaway Beach, OR

Population

1,441

Drive there or take the train from Garibaldi on the Oregon Coast Scenic Railroad, Rockaway Beach (pictured above) is a small town bursting with outdoor fun at beaches, parks, playgrounds and hiking trails. Visit one of the largest Western Red Cedars in Oregon, approximately 800 years old, 150 feet high and 49 feet around. The corn dog was invented here in the 1930s at The Original Pronto Pup and the same recipe is still used today.

Port Orford, OR Population 1,146

One of the oldest and smallest townsites in Oregon, Port Orford is a fishing town home to one of only six Dolly Docks in the world. There isn’t a protected marina for their

local fleet, so they hoist the boats out of the water and park them on the dock. Don’t miss a stroll through the Prehistoric Gardens to see life-size dinosaurs hanging out in the rainforest. Also find scenic beaches, multiple bikeways, art trails and the Cape Blanco Lighthouse.

Joseph, OR Population 1,146

With nearby Wallowa Lake, snowcapped Wallowa Mountain Range and Hells Canyon, the deepest river gorge in North America, Joseph is a remarkable town to visit for outdoor enthusiasts with so many different terrains to explore. Take a tramway to the summit of Mt. Howard or stay in town and enjoy the life-sized bronze statues during the Art Walk on Main Street.

Cascade, ID Population 1,005

Manmade Lake Cascade along the Payette River is home to this vibrant little town popular for watersports and outdoor activities. Check out the totem poles at Arrowhead RV park, watch the steelhead and Chinook salmon runs in nearby rivers and creeks or take a dip in natural hot springs.

Priest Lake, ID Population approximately 500

Referred to as “Idaho’s Crown Jewel,” glacial movements created sandy beaches along the shores of Priest Lake for visitors to enjoy. Navigate a two-mile thoroughfare channel between upper and lower Priest Lake that is a nature-lover’s dream. Or stop by local shops to pick up scratch-made goodies from local huckleberries.

Meet a Heritage banker with a

burning desire

for making fragrant candles

I’veworked in banking for more than 20 years, but I’ve had an artistic and entrepreneurial flair since childhood. Combine that with my appreciation for pleasing smells— flowers, lotions, perfumes, fresh air, ocean breezes, spices, citrus, pine, coffee (the list is long)—and the ingredients were there for candle-making.

That’s been my side hustle for five years now. I launched Scandi Co. Candles in 2020 and sell my creations, made with all natural ingredients, at several stores and seasonal events on Whidbey Island, Washington, where I live and work. They’re also sold online through my website.

Candle making keeps me busy on the weekends; it fulfills the creative side of my brain, and I’m not one to sit still on days off anyway. Mixing wax and fragrant oils gives me an artistic outlet that fills me up as a person. I also enjoy that my candles evoke sensory happiness in others.

My first candle fragrances were inspired by concepts important to Scandinavians: mandatory coffee breaks, appreciation for the outdoors and enjoying life’s little pleasures like reading a book and cozying up to a fire. As someone born in Minnesota with significant Swedish ancestry, plus some Norwegian, Finnish and Danish thrown in for good measure, I saw the similarities to what we in the Pacific Northwest also enjoy.

My main fragrances are Outdoorsy, Coffee Break and Hygge/ Cozy. Hygge, pronounced who-ga or hue-ga, is a Danish concept of being cozy, comfortable and enjoying the moment. Hygge/Cozy has a fragrance of cinnamon and sugar, or a little bit of sweet and spicy.

Photos courtesy of Lindsay Kelley

Outdoorsy has a pine scent with a hint of teakwood and tobacco, giving it a woodsy-smoky scent. Coffee Break plays off a tradition in Sweden to take an hour each afternoon to have coffee and talk with friends, family or co-workers and maybe enjoy a piece of cake, so this fragrance has a coffee and cinnamon bun scent.

My product line also includes Salish Seas, Tropical Breeze, Spa Day, Pink Magnolia and Cloudberry. Others include twists on popular drinks: Apple Bourbon, Black Cherry Merlot, Espresso Martini, Mint Mojito, Pear Prosecco, Paloma Party, Italian Limoncello and Colada Crush. Popular scents during the holidays are Gnoel, Lingonberry Spice, Gingersnap and Holiday Hygge.

I purchase my fragrance oils from a company in Bellingham, Washington. I blend the oils into my melted wax, then pour each candle by hand into individual jars. I include accents

in some of my candles; for example, I press a few coffee beans into the wax for the Coffee Break candle. I also make a gingerbread cookie-scented candle at Christmastime that has eco-friendly glitter sprinkled on top.

I make all my candles in my kitchen, but I hope to build a studio in my backyard someday to have a dedicated workspace.

How it all started

You might say the business’s roots date back to my childhood, when at seven, I made beaded jewelry packaged with my handmade labels and price tags. I loaded the packages in my wagon and pulled my mobile jewelry store through the neighborhood, knocking on doors. The “business” fanned my entrepreneurial flame.

Many years later, I got the idea for candle making after buying a kit to do something fun with my kids.

I had fun and my candle making passion was lit. Previously, I bought candles for our home that contained ingredients I couldn’t pronounce. I wondered: Why not make my own candles with natural ingredients and fragrances I liked?

I began experimenting and found my homemade candles burned clean, smelled wonderful, lasted a long time and did not induce headaches in my scent-sensitive family. I use an

all-natural soy/coconut wax blend that burns cleanly and evenly, resulting in a longer burn time. My products are Made Better certified, a symbol for clean and eco-friendly materials.

Where to find Scandi Co. Candles