Notes to Consolidated Financial Statements

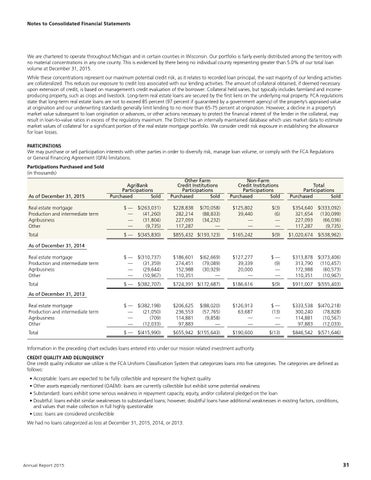

We are chartered to operate throughout Michigan and in certain counties in Wisconsin. Our portfolio is fairly evenly distributed among the territory with no material concentrations in any one county. This is evidenced by there being no individual county representing greater than 5.0% of our total loan volume at December 31, 2015. While these concentrations represent our maximum potential credit risk, as it relates to recorded loan principal, the vast majority of our lending activities are collateralized. This reduces our exposure to credit loss associated with our lending activities. The amount of collateral obtained, if deemed necessary upon extension of credit, is based on management’s credit evaluation of the borrower. Collateral held varies, but typically includes farmland and incomeproducing property, such as crops and livestock. Long-term real estate loans are secured by the first liens on the underlying real property. FCA regulations state that long-term real estate loans are not to exceed 85 percent (97 percent if guaranteed by a government agency) of the property’s appraised value at origination and our underwriting standards generally limit lending to no more than 65-75 percent at origination. However, a decline in a property’s market value subsequent to loan origination or advances, or other actions necessary to protect the financial interest of the lender in the collateral, may result in loan-to-value ratios in excess of the regulatory maximum. The District has an internally maintained database which uses market data to estimate market values of collateral for a significant portion of the real estate mortgage portfolio. We consider credit risk exposure in establishing the allowance for loan losses. PARTICIPATIONS We may purchase or sell participation interests with other parties in order to diversify risk, manage loan volume, or comply with the FCA Regulations or General Financing Agreement (GFA) limitations. Participations Purchased and Sold (in thousands) AgriBank Participations As of December 31, 2015 Purchased Sold

Other Farm Credit Institutions Participations Purchased Sold

Non-Farm Credit Institutions Participations Purchased Sold

Total Participations Purchased Sold

Real estate mortgage Production and intermediate term Agribusiness Other

$ — $(263,031) — (41,260) — (31,804) — (9,735)

$228,838 $(70,058) 282,214 (88,833) 227,093 (34,232) 117,287 —

$125,802 39,440 — —

$(3) (6) — —

$354,640 $(333,092) 321,654 (130,099) 227,093 (66,036) 117,287 (9,735)

Total

$ — $(345,830)

$855,432 $(193,123)

$165,242

$(9)

$1,020,674 $(538,962)

Real estate mortgage Production and intermediate term Agribusiness Other

$ — $(310,737) — (31,359) — (29,644) — (10,967)

$186,601 $(62,669) 274,451 (79,089) 152,988 (30,929) 110,351 —

$127,277 39,339 20,000 —

$— (9) — —

$313,878 $(373,406) 313,790 (110,457) 172,988 (60,573) 110,351 (10,967)

Total As of December 31, 2013

$ — $(382,707)

$724,391 $(172,687)

$186,616

$(9)

$911,007 $(555,403)

Real estate mortgage Production and intermediate term Agribusiness Other

$ — $(382,198) — (21,050) — (709) — (12,033)

$206,625 $(88,020) 236,553 (57,765) 114,881 (9,858) 97,883 —

$126,913 63,687 — —

$— (13) — —

$333,538 $(470,218) 300,240 (78,828) 114,881 (10,567) 97,883 (12,033)

Total

$ — $(415,990)

$655,942 $(155,643)

$190,600

$(13)

$846,542 $(571,646)

As of December 31, 2014

Information in the preceding chart excludes loans entered into under our mission related investment authority. CREDIT QUALITY AND DELINQUENCY One credit quality indicator we utilize is the FCA Uniform Classification System that categorizes loans into five categories. The categories are defined as follows: • Acceptable: loans are expected to be fully collectible and represent the highest quality • Other assets especially mentioned (OAEM): loans are currently collectible but exhibit some potential weakness • Substandard: loans exhibit some serious weakness in repayment capacity, equity, and/or collateral pledged on the loan •D oubtful: loans exhibit similar weaknesses to substandard loans; however, doubtful loans have additional weaknesses in existing factors, conditions, and values that make collection in full highly questionable • Loss: loans are considered uncollectible We had no loans categorized as loss at December 31, 2015, 2014, or 2013.

Annual Report 2015

31