Measuring the performance of the global infrastructure sector Global Leadership Forum Infrastructure Sentiment Survey Q2 2023

Welcome to this first edition of the Global Leadership Forums Infrastructure Sentiment Survey This survey and the subsequent report will be conducted on a quarterly basis to provide the infrastructure sector with metrics on how the market is currently performing and how individuals believe it will be performing in 12 months time.

This first survey acts as a snapshot but, as we progress through the first year, trend analysis and additional sector breakdowns will be included as sample size and data robustness improve.

In this first edition 92 individuals completed the survey across six global regions and multiple sectors. I would like to take this opportunity to thank those that completed the survey and present the key findings below

• Firms overall finances are stable with a positive outlook both currently and 12 months into the future.

• The engineering industry is currently felt to be on a stable but positive outlook and this improves in 12 months. The ability to maintain margins remains a problem currently and into the future.

• Currently, project activity is considered stable with a lean towards positive activity in the public/private sector in 12 months.

• There is significant positive demand for low carbon solutions but funding still remains an issue. It is expected conditions will improve over the next 12 months.

• Bidding time frames and contract conditions are currently and expected to remain a significant issue for projects.

Dr Nelson Ogunshakin OBE CEO, FIDIC• Regionally, Africa had the least positive sentiment and North America the most.

• The energy sector displayed the strongest polarisation of sentiment towards renewables and away from carbon- based generation.

• The water sector had the most positive sentiment across the various sub-sectors.

• Residential, hospitals and data centres were felt to be the main sub-sectors driving the buildings sector.

• Sentiment in the resources sector is most positive in the mining area, which could be a reflection on the use and demand of rare earth minerals for use in batteries and renewables.

Dr Nelson

Ogunshakin OBE CEO, FIDIC

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Transport Waste (solid)

Participants were asked to respond to the following in real terms (accounting for inflation) within the following bands. Below is the subsequent positive/negative balance across key areas affecting the infrastructure sector This balance is therefore not the number of responses.

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Telecommunications Resources

Current sentiment in the global transport sector across all sub sectors was on balance contracting by just over 1% in real terms. Looking forward 12 months the outlook became e positiv with the o all balance f oring gr wth of

Current

Current sentiment

Current sentiment in the waste sector was felt to be stable with a minor possibility of improvement in the next 12 months.

We should, however, caution that in this quarter of the survey the waste sector has a small sample.

Current sentiment in the water and sewerage market was the strongest positive balance of all sectors analysed in this survey. Impressively, in 12 months time the sentiment is expected to be even stronger

All of the sub-sectors (water, sewerage/wastewater, storm water drainage and flood protection) had strong positive balances for growth and these balances all improve when considering sentiment in 12 months time.

The overall balance of opinion for the energy sector was slightly one of negative growth but this was predicted to shift to a more stable/positive position in 12 months time.

It should, however, be pointed out that the majority of positive growth is being driven by the renewable (wind, solar and hydro) sector.

Current sentiment in the telecommunications sector was felt to be stable with a minor possibility of improvement in the next 12 months.

We should, however, caution that in this quarter of the survey the telecommunications sector has a small sample.

Current sentiment in the resource and materials sector was felt to be stable to negative with a minor possibility of improvement in the next 12 months.

We should, however, caution that in this quarter of the survey the resource and minerals sector has a small sample.

Current sentiment in the buildings sector had a negative overall balance, but with improvement in the next 12 months.

Of the sub-sectors the only areas where there was either zero or a positive overall balance was that of residential, hospitals and data centres.

Current sentiment

Sentiment in 12 months

Current sentiment

Sentiment in 12 months

The results in this document are the result of a survey distributed to FIDICs database of contacts and the members of its Global Leadership Forum.

The results are calculated based on the experiences of individuals primarily located within engineering firms and so represents views on the ground of how activity and performance is occurring.

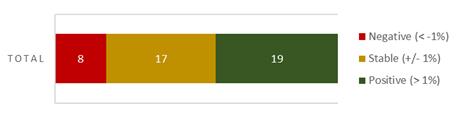

Participants were asked to respond to the areas in this report in real terms (accounting for inflation). Below is the subsequent positive/negative balance across all responses in key areas affecting the infrastructure sector

Negative (< -1% real growth rate)

Stable (+/- 1% real growth rate)

Positive (> 1% real growth rate)

Using the above, a balance of overall sentiment can be calculated to be stable, stable with positive or negative direction, positive or negative.

This document was produced by FIDIC and is provided for informative purposes only. The contents of this document are general in nature and therefore should not be applied to the specific circumstances of individuals. Whilst we undertake every effort to ensure that the information within this document is complete and up to date, it should not be relied upon as the basis for investment, commercial, professional or legal decisions.

FIDIC accepts no liability in respect to any direct, implied, statutory, and/or consequential loss arising from the use of this document or its contents. No part of this report may be copied either in whole or in part without the express permission in writing.

Copyright FIDIC © 2023

Published by International Federation of Consulting Engineers (FIDIC)

World Trade Center II

P.O. Box 311 1215 Geneva 15, Switzerland

Phone +41 22 568 0500

E-mail fidic@fidic.org

Web: www.fidic.org