FOUNDATIONS

A baseline for the region’s future

OFFICE

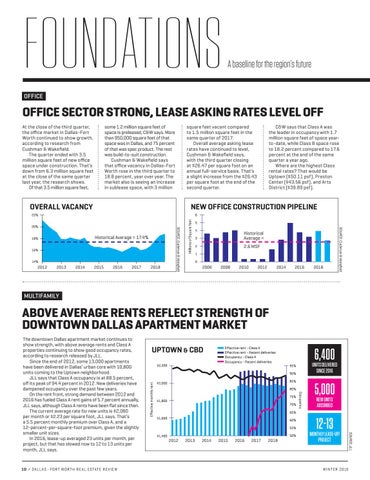

OFFICE SECTOR STRONG, LEASE ASKING RATES LEVEL OFF At the close of the third quarter, the office market in Dallas-Fort Worth continued to show growth, according to research from Cushman & Wakefield. The quarter ended with 3.5 million square feet of new office space under construction. That’s down from 6.3 million square feet at the close of the same quarter last year, the research shows. Of that 3.5 million square feet,

some 1.2 million square feet of space is preleased, C&W says. More than 950,000 square feet of that space was in Dallas, and 75 percent of that was spec product. The rest was build-to-suit construction. Cushman & Wakefield says that office vacancy in Dallas-Fort Worth rose in the third quarter to 18.8 percent, year over year. The market also is seeing an increase in sublease space, with 3 million

square feet vacant compared to 1.5 million square feet in the same quarter of 2017. Overall average asking lease rates have continued to level, Cushman & Wakefield says, with the third quarter closing at $26.47 per square foot on an annual full-service basis. That’s a slight increase from the $26.43 per square foot at the end of the second quarter.

OVERALL VACANCY

NEW OFFICE CONSTRUCTION PIPELINE 6

16% 14%

2013

2014

2015

2016

2017

2018

5 4 3

Historical Average =

2

2.6 MSF

1 0

2006

2008

2010

2012

2014

2016

2018

SOURCE: Cushman & Wakefield

Historical Average = 17.4%

18%

SOURCE: Cushman & Wakefield

20%

Millions of Square feet

22%

2012

C&W says that Class A was the leader in occupancy with 1.7 million square feet of space yearto-date, while Class B space rose to 18.2 percent compared to 17.6 percent at the end of the same quarter a year ago. Where are the highest Class rental rates? That would be Uptown ($50.11 psf), Preston Center ($43.56 psf), and Arts District ($39.89 psf).

MULTIFAMILY

ABOVE AVERAGE RENTS REFLECT STRENGTH OF DOWNTOWN DALLAS APARTMENT MARKET $2,200

Eff ective rent - Class A Eff ective rent - Recent deliveries Occupancy - Class A Occupancy - Recent deliveries

6,400

UNITS DELIVERED SINCE 2016

95%

Eff ective monthly rent

90% 85%

$2,000

80% 75%

$1,800

70%

5,000 NEW UNITS ABSORBED

65% $1,600

60% 55% 50%

$1,400

2012

2013

2014

2015

2016

2017

2018

12-13

MONTHLY LEASE-UP/ PROJECT

WINTER 2018

SOURCE: JLL

1 0 / D A L L A S - F O R T W O R T H R E A L E S TAT E R E V I E W

UPTOWN & CBD

Occupancy

The downtown Dallas apartment market continues to show strength, with above average rents and Class A properties continuing to show good occupancy rates, according to research released by JLL. Since the end of 2012, some 13,000 apartments have been delivered in Dallas’ urban core with 10,800 units coming to the Uptown neighborhood. JLL says that Class A occupancy is at 88.5 percent, off its peak of 94.4 percent in 2012. New deliveries have dampened occupancy over the past few years. On the rent front, strong demand between 2012 and 2016 has fueled Class A rent gains of 5.7 percent annually, JLL says, although Class A rents have been flat since then. The current average rate for new units is $2,080 per month or $2.23 per square foot, JLL says. That’s a 5.5 percent monthly premium over Class A, and a 12-percent-per-square-foot premium, given the slightly smaller unit sizes. In 2016, lease-up averaged 23 units per month, per project, but that has slowed now to 12 to 13 units per month, JLL says.